IV. Credit Delivery and Financial Inclusion - आरबीआय - Reserve Bank of India

IV. Credit Delivery and Financial Inclusion

During 2015-16, the Reserve Bank intensified its efforts towards expanding formal banking facilities covering hitherto excluded sections of society. Greater focus was placed on ensuring adequate credit flow to various segments in the priority sectors. Measures such as introduction of Priority Sector Lending Certificates (PSLCs) and implementation of the recommendations of the Committee on Medium Term Path on Financial Inclusion are expected to provide further impetus to financial inclusion in the country. IV.1 The Reserve Bank continued its focus on ensuring the availability of banking services throughout the country and instituting an efficient and comprehensive credit delivery mechanism catering to the productive sectors of the economy. During 2015-16, efforts were directed at fostering a more conducive environment for flow of credit to priority sectors, in particular to the micro, small and medium enterprises (MSME) sector. A national programme for capacity building of bankers was launched with the sole objective of upgrading skills related to the financing of the MSME sector. The Committee on Medium-Term Path on Financial Inclusion submitted its report charting out a measurable action plan for financial inclusion that will guide the financial inclusion process going forward. The Financial Inclusion and Development Department (FIDD) is the nodal department for the seamless implementation of the Reserve Bank’s financial inclusion agenda. Agenda 2015-16: Implementation Status Priority Sector Lending IV.2 During 2015-16, PSLCs were introduced as a mechanism for incentivising banks having surplus in lending1 to different categories of the priority sector thereby enhancing lending to these sectors (Box IV.1). Like carbon credit trading, PSLCs will allow the market mechanism to drive priority sector lending by leveraging the comparative strengths of different banks. For trading purposes, a dedicated portal was launched in April 2016. In view of the critical role played by regional rural banks (RRBs) in driving the financial inclusion agenda, priority sector lending guidelines were revised for RRBs in December 2015 and an overall target of 75 per cent of the total outstanding loans to the priority sector was set for them. Initiatives for MSME Sector IV.3 In August 2015, the banks were advised to review their existing lending policies to the micro and small enterprises (MSEs) sector and fine-tune them by allowing for standby credit facilities in case of term loans, additional working capital limits, mid-term review of regular working capital limits and timelines for credit decisions. Subsequent to the notification of a ‘Framework for Revival and Rehabilitation of Micro, Small and Medium Enterprises’ by the Government to provide a simpler and faster mechanism for addressing the stress in MSME accounts, the Reserve Bank issued related guidelines along with operating instructions on March 17, 2016. Under this framework, the revival and rehabilitation of MSME units having loan limits up to ₹ 250 million will be undertaken. Banks were also required to put in place Board approved policies to operationalise the framework not later than June 30, 2016. Box IV.1 A scheme of PSLCs was introduced in April 2016. The Reserve Bank provided a platform to enable trading in the certificates through its core banking solution (CBS) portal (e-Kuber). All scheduled commercial banks (including RRBs), urban co-operative banks, small finance banks (when they become operational) and local area banks are eligible to participate in trading. Some of the main features of the scheme are:

IV.4 In a move to boost entrepreneurial sensitivity among banks’ field-level functionaries, the Reserve Bank in collaboration with the College of Agricultural Banking (CAB), Pune, launched the National Mission for Capacity Building of Bankers for financing the MSME sector (NAMCABS). Since its inception, NAMCABS has imparted training to about 3,000 bankers. Natural Calamities and Policy Response IV.5 Following the Government’s revision of the criteria for crop loss from 50 per cent to 33 per cent for providing input subsidies (compensation) to farmers, State Level Bankers’ Committees/ District Level Consultative Committees/banks were allowed to take a view on rescheduling of loans if the crop loss turned out to be 33 per cent or more. Banks were permitted to allow a maximum period of repayment of up to two years (including the moratorium period of one year) if the loss was between 33 per cent and 50 per cent. If the crop loss is 50 per cent or more, the restructured period for repayment can be extended to a maximum of five years (including the moratorium period of one year). CREDIT DELIVERY Priority Sector IV.6 The objective of priority sector lending is to ensure that timely and adequate credit is available to vulnerable sections of society. Priority sector loans include small value loans to farmers for agriculture and allied activities; MSMEs; loans up to ₹ 2.5 million for low cost housing and up to ₹ 1 million to students for education; social infrastructure and renewable energy; and to other low income groups and weaker sections of society. Usually these categories of people/activities are unable to access credit due to a perceived lack of viability and creditworthiness even though there are some recent signs of improvement on this front (Box IV.2). Box IV.2 The term ‘small’ in ‘small borrowers’ has been redefined from time to time. Currently, accounts with a credit limit of ₹ 200,000 are taken as small borrowal accounts (SBAs). The credit limit for SBAs was ₹ 25,000 till 1998 and ₹ 10,000 till 1983. There has been a fall in the share of SBAs in total loan accounts and amount since the 1990s (Charts 1 and 2). However, real bank credit per SBA has been on the rise in rural areas; this is contrary to the trend in urban areas (Chart 3). Secondly, gender disparities in bank credit too appear to have been on a decline in rural areas. On average, for every 100 SBAs held by rural men, rural women held about 32 accounts in 2015. As against this, urban women held only 16 loan accounts per every 100 accounts held by urban men. Thirdly, the ratio of bank credit per capita (under SBA) for rural women to urban women has also been largely on a rising trend (Chart 4). This underlines the need for focused attention to urban poor, keeping in view the increasing urbanisation. Besides expanding the branch network, tailor-made platforms and products need to be designed to reach out to small borrowers in urban areas, including slum-dwellers and domestic workers. Reference: Chavan, Pallavi (2016), ‘Bank Credit to Small Borrowers: An Analysis based on Supply and Demand-side Indicators’, mimeo. IV.7 The performance of various bank groups in achieving priority sector targets is given in Table IV.1. Flow of Credit to Agriculture IV.8 Led by the performance of scheduled commercial banks (SCBs), the actual credit flow to agriculture exceeded the target fixed by the Government for 2015-16 (Table IV.2). Credit to the MSME Sector IV.9 Reflecting several of the Government’s initiatives for the MSME sector, such as ‘Make in India’, ‘Start-up India’, ‘Ease of Doing Business’ and ‘Udyog Aadhar’, which were reinforced by the Reserve Bank’s initiatives such as capacity building of field level banking functionaries, addressing life-cycle needs of enterprises and providing simpler and faster mechanisms to address the stress in MSME accounts, credit to this sector has improved in recent times (Table IV.3). Studies on the Efficacy of Credit Delivery Models IV.10 A number of studies were commissioned during the year to assess the efficacy of various schemes and models for credit delivery and financial inclusion – the business correspondent (BC) model, self-help group (SHG)-bank linkage programme, credit guarantee trust for micro and small enterprises (CGTMSE), and the lead bank scheme. A study on farmers’ funding requirements was also undertaken in collaboration with CAB, Pune. IV.11 The study on the efficacy of the BC model brought out the need for certification-training programmes for BCs along with providing them other support in terms of timely and adequate remuneration, effective ways of cash management and improving the acceptance infrastructure and technology. The need for creating a BC registry and effective monitoring and supervision involving banks were also highlighted in the study. The study on the efficacy of SHG-bank linkage found that banks could consider appointing Bank Mitras functioning under the Deendayal Antyodaya Yojana-National Rural Livelihoods Mission (DAYNRLM) as BC agents so that they can formally transact the banking business for SHG members as well as for other customers of banks in a specific area. The study also recommended that the SHG-bank linkage activity may be treated as corporate social responsibility. Furthermore, there could be an SHG specific mark for every product involving the engagement of SHGs. A cadre of last mile delivery nodes may be created by leveraging the BC model. FINANCIAL INCLUSION IV.12 The Reserve Bank continued its efforts towards fulfilling the financial inclusion agenda during the year. In this direction, the Committee on Medium-Term Path on Financial Inclusion suggested improvements in the governance system as a means of strengthening credit infrastructure and augmenting the government’s social cash transfers to the poor, propelling the economy on to a medium-term sustainable inclusion path (Box IV.3). Financial Inclusion Plan IV.13 The Financial Inclusion Plan (FIP) provides a structured and planned approach to financial inclusion with a commitment at the highest echelons within banks in terms of Board approval of the plans. Out of 2,259 rural bank branches opened during April 2015-March 2016, 1,670 branches were opened in unbanked rural centres under FIP. Around 71 million basic savings bank deposit accounts were added taking the total to 469 million by March 2016. The total number of small farm sector credits (Kisan Credit Cards) and small non-farm sector credits (General Credit Cards) stood at 47 million and 11 million, respectively (Table IV.4). With the conclusion of FIP’s Phase II (2013-16) on March 31, 2016, all domestic scheduled commercial banks (including RRBs) were advised to set new Board approved FIP targets for the next three years (April 2016 to March 2019). Box IV.3 The Committee on Medium-Term Path on Financial Inclusion (Chairman: Shri Deepak Mohanty) which was constituted to work out a medium-term (five year) measurable action plan for financial inclusion, submitted its report in December 2015. The Committee recognised that substantial progress had been made in terms of access to financial products and services especially after the launch of the Pradhan Mantri Jan Dhan Yojana (PMJDY). The Committee identified significant gaps in terms of usage, inadequate ‘last mile’ service delivery, exclusion of women and small and marginal farmers and a very low formal link for micro and small enterprises. Against this background, the committee set a much wider vision of financial inclusion as ‘convenient’ access to a basket of basic formal financial products and services that should include savings, remittances, credit, government-supported insurance and pension products to small and marginal farmers and low-income households at reasonable costs with adequate protection progressively supplemented by social cash transfers. The Committee also suggested increasing micro and small enterprises’ access to formal finance with a greater reliance on technology to cut costs and improve service delivery, such that by 2021 over 90 per cent of the hitherto underserved sections of society become active stakeholders in economic progress empowered by formal finance. Some of the recommendations of the committee are:

Roadmap for Banking Facilities in Unbanked Villages IV.14 Banks were initially advised to complete Phase II of the roadmap for covering all 490,298 unbanked villages with population less than 2,000 by March 31, 2016. The timeline was advanced to August 14, 2015 in view of the on-going implementation of the Pradhan Mantri Jan Dhan Yojana (PMJDY). At end-March 2016, as reported by the State Level Bankers’ Committees (SLBCs), 450,686 villages (91.9 per cent of the target) had been covered by 14,901 branches, 415,207 villages through BCs and 20,578 villages through other modes such as ATMs and mobile vans. Keeping in view the necessity of brick and mortar branches for promoting banking penetration and financial inclusion, a roadmap for establishing such branches in villages with population above 5,000 but without a bank branch of a scheduled commercial bank was rolled out in December 2015. SLBC convenor banks have been advised to ensure opening of bank branches under this roadmap by March 2017. Financial Inclusion Advisory Committee (FIAC) IV.15 The Reserve Bank set up an advisory body, the FIAC, in 2012 to review financial inclusion policies on an on-going basis and to provide expert advice to the Reserve Bank in this matter. Given the renewed focus on financial inclusion by the Government of India, the on-going implementation of the PMJDY and the need for convergence of the efforts of various stakeholders, FIAC was re-constituted in June 2015. Its revised terms of reference include: (i) preparing a national strategy for financial inclusion which aims at converging financial inclusion efforts of various stakeholders and PMJDY, apart from monitoring the progress; (ii) monitoring progress on FIP; and (iii) monitoring progress on financial literacy. Financial Inclusion Fund (FIF) IV.16 The financial inclusion fund (FIF) and the financial inclusion technology fund (FITF) were set up in 2007-08 for a period of five years with a corpus of ₹ 5 billion for each to be contributed by the Government of India, the Reserve Bank and NABARD in the ratio of 40:40:20. The Government of India merged FIF and FITF to form a single financial inclusion fund in July 2015 with a corpus of ₹ 20 billion. The new FIF, which will be administered by an advisory Board constituted by the Government, will be maintained by NABARD. The fund will be in operation for another three years or till such period as may be decided by the Government of India and the Reserve Bank in consultation with other stakeholders. FIF aims to support developmental and promotional activities leading to greater financial inclusion, for example, the creation of FI infrastructure across the country, capacity building of stakeholders, spreading awareness to address demand side issues, enhanced investments in green information and communication technology (ICT) solutions, research and transfer of technology and improving the technological absorption capacity of financial service providers/users. The fund will not be utilised for normal business/banking activities. FINANCIAL LITERACY IV.17 Financial literacy is crucial for imparting efficacy to financial inclusion initiatives. In the context of a changing financial landscape, especially with the introduction of PMJDY, the emphasis is on keeping new bank accounts operationally active. Banks were, accordingly, advised in January 2016 to focus on enhancing the efficacy of financial literacy programmes through: (i) Board-level policies for a stronger financial literacy architecture; (ii) a tailor-made approach to financial literacy and organising camps for different target groups; and (iii) following a concerted approach among various stakeholders at the district/panchayat/village level (local officials of NABARD and the Reserve Bank, district and local administration, block level officials, NGOs, SHGs, BCs, farmers’ clubs, panchayats, primary agricultural credit society (PACS), and village level functionaries). IV.18 As at end-March 2016, 1,384 financial literacy centres (FLCs) were operational in the country, up from 1,181 FLCs at end-March 2015. During the year ended March 2016, 87,710 financial literacy activities were conducted by FLCs as against 84,089 activities during the preceding year. Agenda for 2016-17 IV.19 Going forward, an action plan based on the recommendations of the Committee on Medium-Term Path on Financial Inclusion will be worked out. Three recommendations of the committee, viz., creating a BC registry; formalising certification-training programmes for BCs; and designing a framework for accreditation of credit counsellors have been identified for immediate implementation. Formulating a National Strategy for Financial Inclusion, which forms part of the revised terms of reference of FIAC, will be taken up during the year. District level data on the progress made by banks under FIP will also be collected for better monitoring of banks’ FI initiatives. As an impetus to financial literacy activities, capacity building programmes for financial literacy counsellors will be launched in collaboration with CAB, Pune. 1 For instance, a bank with expertise in lending to small farmers can over-perform there and get benefits by selling its over-performance through PSLCs. |

हे पेज शेअर करा:

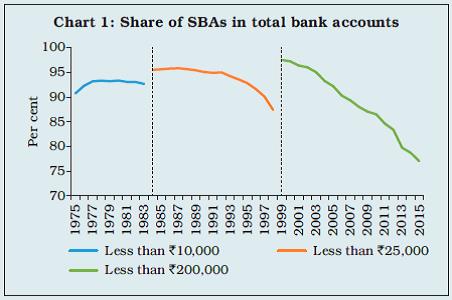

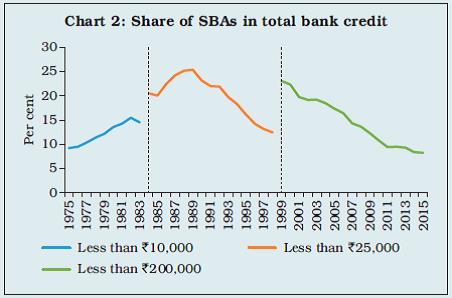

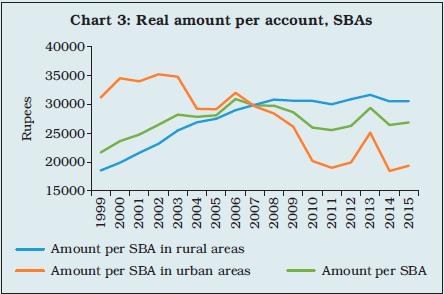

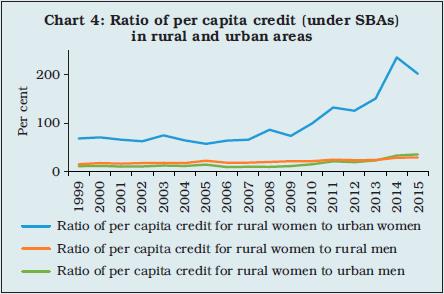

भारतीय रिझर्व्ह बँक मोबाईल ॲप्लिकेशन इंस्टॉल करा आणि नवीनतम बातम्यांचा त्वरित ॲक्सेस मिळवा!