VI. Regulation, Supervision and Financial Stability - ఆర్బిఐ - Reserve Bank of India

VI. Regulation, Supervision and Financial Stability

In a deteriorating macroeconomic environment during 2019-20, policy attention came to be focused on improving the supply of credit sectorally. The introduction of external benchmarks for bank lending rates strengthened the transmission of monetary policy. The banking sector went through a structural transformation with consolidation in the form of mergers and amalgamation. The regulatory and supervisory framework was unified across regulated entities and strengthened in alignment with global best practices. Harnessing technology for customer services, strengthening fraud detection, and consumer protection were concurrent objectives during the year. VI.1 The chapter discusses regulatory and supervisory measures undertaken during the year to strengthen the financial system and preserve financial stability. As part of the overall objective of aligning the regulatory framework with global best practices, steps were taken in the areas of corporate governance and risk management. Operationalisation of regulatory sandbox, enabling video-based know-your-customer (KYC) processing, Regulatory Technology (RegTech)/ Supervisory Technology (SupTech) initiatives and cyber security measures marked the rising importance of FinTech in the regulatory and supervisory functions. Steps towards development of an active secondary market for corporate loans, lending to Infrastructure Investment Trusts (InvITs) and linking pricing of bank loans to external benchmarks were undertaken in order to deleverage the banks’ balance sheets and to improve the flow of credit to critical sectors of the economy in which credit demand remained supported. In response to the COVID-19 pandemic, measures were taken for mitigating the burden of debt servicing by borrowers and ensuring the continuity of viable businesses. VI.2 In other areas, the asset-liability management (ALM) framework of Non-Banking Financial Companies (NBFCs) was strengthened while the overall liquidity risk management system was aligned with that of the banking sector. Regulation of Housing Finance Companies (HFCs) was brought under the Reserve Bank's purview, and wider supervisory powers over NBFCs were vested with it. VI.3 In the cooperative banking space, progress was made in the process of establishing the Umbrella Organisation for Urban Cooperative Banks (UCBs). The Supervisory Action Framework (SAF) was reviewed and reporting of large exposures to Central Repository of Information on Large Credits (CRILC) was implemented during the year. Other major developments include issuance of guidelines on constitution of Board of Management (BoM) and developing a Central Fraud Registry (CFR) as well as a comprehensive cyber security framework for UCBs. A major policy drive during the year was towards amalgamation and consolidation of cooperative banks. VI.4 The rest of this chapter is divided into six sections. Section 2 deals with the mandate and functions of the Financial Stability Unit (FSU). Section 3 addresses various regulatory measures undertaken by the Department of Regulation (DoR). Section 4 covers several supervisory measures undertaken by the Department of Supervision (DoS), and enforcement actions carried out by the Enforcement Department during the year. Section 5 highlights the role played by the Consumer Education and Protection Department (CEPD) and the Deposit Insurance and Credit Guarantee Corporation (DICGC) in protecting consumer interests, spreading awareness and upholding consumer confidence. These departments have also set out agenda for 2020-21 in their respective sections. The chapter ends with a conclusion. 2. FINANCIAL STABILITY UNIT (FSU) VI.5 The mandate of the Financial Stability Unit (FSU) is to monitor the stability and soundness of the financial system by examining risks to financial stability, undertaking macro-prudential surveillance through systemic stress tests, financial network analysis and by disseminating information and analysis through the Financial Stability Report (FSR). It also functions as a secretariat to the Sub-Committee of the Financial Stability and Development Council (FSDC), an institutional mechanism of regulators for maintaining financial stability and monitoring macro-prudential regulation in the country. Agenda for 2019-20: Implementation Status Goals Set for 2019-20 VI.6 The Department had set out the following goals for 2019-20:

Implementation Status of Goals VI.7 A framework for estimation of sectoral probability of default of private listed firms was developed and is being tested using alternate data sources for incorporation in the stress testing framework of the Department. However, this work has partly been affected by disruptions caused by the COVID-19 pandemic. VI.8 The FSRs were published in December 2019 and July 2020. These editions reflected the collective assessment of the Sub-Committee of FSDC on the balance of risks around financial stability. The December 2019 edition of FSR highlighted that the economic prospects, both global and domestic, are being weighed down by uncertainties which are affecting consumption and business investment. The report underscored the resilience of Indian financial institutions, even as it projected a rise in gross non-performing assets (GNPA) ratio driven by weakening macroeconomic scenario and consequent slackening of credit growth as also marginal increase in slippages. The July 2020 edition of FSR highlighted the impact of disruptions arising from the COVID-19 pandemic-induced lockdown on near-term domestic economic prospects. The report also underscored the policy measures adopted by the financial sector regulators and the Government of India, spanning monetary stimulus and regulatory relief, to offset the impact of the pandemic and to ensure normalcy of financial intermediation functions. It also examined the credit allocation dynamics in the wake of the pandemic-induced uncertainty. Financial sector assessment emphasised the resilience of the Indian financial system, even though stress tests projected a rise in scheduled commercial banks’ (SCBs’) GNPA ratio due to the stressed macroeconomic environment. Network analysis revealed reduction in contagion losses to the banking system under various scenarios, in relation to a year ago. VI.9 The FSDC Sub-Committee held two meetings in 2019-20, both of which were held under distinct economic conditions. In the meeting held in September 2019, the forum discussed various issues impinging on financial stability, including concerns regarding NBFCs, UCBs, and debt mutual funds. The regulatory framework of credit rating agencies (CRAs) and creation of a Central KYC registry also engaged the Sub- Committee. Steps taken for resolution and prevention of contagion effect of the Infrastructure Leasing & Financial Services Ltd. (IL&FS) crisis, operationalising individual insolvency and promotion of financial inclusion through insurance marketing firms were also discussed in the meeting. VI.10 In the meeting held in June 2020, the Sub Committee reviewed the major developments in global and domestic economy, and financial markets that impinge upon financial stability. Amongst other things, the Sub-Committee also discussed about the proposal of setting up of an Inter Regulatory Technical Group on FinTech (IRTG-FinTech), the importance of cyber security across the financial system and the National Strategy on Financial Education (NSFE) 2020-25. It also deliberated upon the status and developments under the Insolvency and Bankruptcy Code (IBC), 2016 and the working of CRAs. Impact of COVID-19 Pandemic VI.11 The Department’s functions have not been significantly impacted by the COVID-19 pandemic-induced disruptions. The FSDC and FSDC-Sub Committee meetings were held through video conferencing during the period. However, the 21st issue of the FSR was published in July due to delay in the receipt of some primary data. Agenda for 2020-21 VI.12 In the year ahead, FSU will focus on the following:

3. REGULATION OF FINANCIAL INTERMEDIARIES Department of Regulation (DoR) Commercial Banks VI.13 The Department of Regulation - Banks (DoR - Banks) is the nodal Department for regulation of commercial banks for ensuring a healthy and competitive banking system, which provides cost effective and inclusive banking services. The regulatory framework is fine-tuned as per the requirements of the Indian economy while adapting to international best practices. Agenda for 2019-20: Implementation Status Goals Set for 2019-20 VI.14 The Department had set out the following goals for regulation of commercial banks in 2019-20:

Implementation Status of Goals Aligning the Prudential Regulatory Framework with Global Standards/Practices VI.15 With the Basel Committee on Banking Supervision (BCBS) deferring the implementation of Basel III reforms by one year, from January 1, 2022 to January 1, 2023, on account of the COVID-19 pandemic, the milestones for issue of - (i) draft guidelines on minimum capital requirements for operational risk, and (ii) draft and final guidelines for standardised approach for credit risk - have also been deferred. The adoption of Ind AS was also deferred, pending necessary legislative amendments. Further, the implementation of the Net Stable Funding Ratio (NSFR) has been deferred for six months, from April 1, 2020 to October 1, 2020, as also, the deadline for meeting the last tranche of capital conservation buffer has been extended by six months, i.e., from March 31, 2020 to September 30, 2020. Development of an Active Secondary Market for Corporate Loans VI.16 As part of the initiatives to develop an active secondary market for corporate loans in line with the international practices, a task force constituted for this purpose has made important recommendations (Box VI.1). Digital Onboarding of Customers and Video-based KYC VI.17 A circular has been issued on January 9, 2020 amending master direction on KYC, permitting Video-based Customer Identification Process (V-CIP) and digital KYC for customer on-boarding. Further, equivalent e-documents, including documents issued to the digital locker account of the customer, with valid digital signature of the issuing authority have been allowed for Customer Due Diligence (CDD) purpose. Projects under Implementation in Commercial Real Estate (CRE) Sector VI.18 Project loans in the CRE sector have been permitted to be restructured without a downgrade in the asset classification, by way of revision of date of commencement of commercial operation (DCCO) up to one additional year (i.e., total 2 years extension from the original DCCO), as in the case of projects in non-infrastructure sectors, with a view to harmonising the guidelines for projects under implementation in non-infrastructure and CRE sectors. Restructuring Scheme for Micro, Small and Medium (MSME) Advances VI.19 The scheme of restructuring of accounts, which was allowed for stressed MSME accounts as on January 1, 2019, was extended to the accounts that were in default but ‘standard’ as on January 1, 2020 and continue to be classified as a ‘standard asset’ till the date of implementation of the restructuring. The restructuring under this scheme has to be implemented by December 31, 2020. The detailed guidelines were issued on February 11, 2020. Large Exposures Framework (LEF) VI.20 On September 12, 2019, the exposure limit of banks to a single NBFC (excluding gold loan companies) was harmonised by increasing the general single counterparty limit under the LEF from 15 per cent to 20 per cent of bank’s eligible capital base. On March 23, 2020, a clarification was issued to the banks that exposure can be shifted from Credit Risk Mitigation (CRM) provider to the original counterparty, even if the counterparty was a person resident outside India, if CRM benefits like shifting of exposure/risk weights are not derived. Exposures thus shifted to a person resident outside India will attract a minimum risk weight of 150 per cent. The date of applicability of the LEF guidelines to non-centrally cleared derivatives exposures was deferred by one year, i.e., to April 1, 2021. On account of COVID-19 pandemic, with a view to facilitate greater flow of resources to corporates, as a onetime measure, the limit for bank’s exposure to a group of connected counterparties was increased from 25 per cent to 30 per cent of the eligible capital base of the bank till June 30, 2021. International Financial Services Centre (IFSC) Banking Units (IBUs) VI.21 During 2019-20, the scheme for setting up of IBUs was amended permitting IBUs: (a) to open current accounts (including escrow accounts) for their corporate borrowers subject to compliance with provisions of Foreign Exchange Management Act (FEMA) 1999; (b) to accept fixed deposits in foreign currency of tenor less than one year from non-bank entities and also repay fixed deposits prematurely without any time restrictions, and (c) to participate in exchange traded currency derivatives on Rupee (with settlement in foreign currency) listed on stock exchanges set up at IFSCs. Regional Rural Banks (RRBs) – Perpetual Debt Instruments (PDIs) and Merchant Acquiring Business VI.22 During 2019-20, RRBs were permitted to issue PDIs eligible for inclusion as Tier 1 capital, thus providing them an additional option for augmenting regulatory capital funds. They were also allowed to act as merchant acquiring banks using Aadhaar Pay-BHIM App and POS terminals. External Benchmarking of Loans VI.23 All new floating rate personal or retail loans (housing, auto, etc.) and floating rate loans extended by banks to Micro and Small Enterprises from October 1, 2019 and floating rate loans to Medium Enterprises from April 1, 2020, were linked to external benchmarks with the freedom to choose from any of several indicated benchmarks. The banks were also free to choose their spread over the benchmark rate, subject to the condition that the credit risk premium may undergo change only when the borrower’s credit assessment undergoes a substantial change, as agreed upon in the loan contract. Fit and Proper Criteria for Public Sector Banks’ (PSBs’) Shareholder Directors VI.24 Revised guidelines on ‘fit and proper’ criteria for shareholder directors in the PSBs were issued in August 2019, thereby aligning them with the eligibility requirements applicable for other directors. Compensation of Whole Time Directors/CEOs/ Material Risk Takers and Control Function Staff VI.25 The Reserve Bank issued revised compensation guidelines for whole time directors, CEOs, material risk takers and control function staff of all private sector banks, effective April 1, 2020. These guidelines are in alignment with the principles of the Financial Stability Board (FSB) for sound compensation practices. Merger of PSBs VI.26 In line with the Government of India scheme of amalgamation dated March 4, 2020, ten PSBs were merged to form four PSBs with effect from April 1, 2020 (Table VI.1). Accordingly, the bank(s) that merged into another bank ceased to carry on banking business and were excluded from the Second Schedule of the Reserve Bank of India (RBI) Act, 1934. Doorstep Banking Services for Senior Citizens and Differently Abled Persons VI.27 Banks were advised to offer doorstep banking services to senior citizens and differently abled persons on pan India basis, by updating the list of branches offering such services on websites regularly and by giving adequate publicity on the availability of such services in their public awareness campaigns, including policy and charges. COVID-19 Pandemic Measures VI.28 In response to COVID-19 pandemic, the Reserve Bank instituted a number of measures to mitigate the burden of debt servicing by borrowers, ensure the continuity of viable businesses, maintain adequate liquidity in the system, facilitate and incentivise bank credit flows, ease financial stress and enable the normal functioning of financial markets. VI.29 In respect of all term loans (including agricultural term loans, retail and crop loans) outstanding as on March 1, 2020, all lending institutions [Commercial Banks including Small Finance Banks (SFBs), Local Area Banks (LABs), RRBs, UCBs/ State Co-operative Banks (StCBs)/ District Central Co-operative Banks (DCCBs), AIFIs and NBFCs including HFCs] were permitted to grant a moratorium of six months on payment of all instalments falling due between March 1, 2020 and August 31, 2020. Likewise, in respect of working capital facilities sanctioned in the form of cash credit/overdraft (CC/OD), lending institutions were permitted to defer the recovery of interest applied in respect of all such facilities during March 1, 2020 to August 31, 2020. Lending institutions were also permitted, at their discretion, to convert the accumulated interest in case of CC/ OD for the deferment period up to August 31, 2020, into a funded interest term loan (FITL) which shall be repayable not later than March 31, 2021. VI.30 In respect of working capital facilities sanctioned in the form of CC/OD to borrowers facing stress on account of the pandemic, lending institutions were permitted to recalculate the drawing power by reducing the margins till August 31, 2020, as a one-time measure, such that the margins are restored by March 31, 2021, and / or review the working capital sanctioned limits up to March 31, 2021, based on a reassessment of the working capital cycle. VI.31 These measures will not result in asset classification downgrade of the respective facilities and will not be treated as a default for supervisory reporting and reporting to credit information companies. Lending institutions were advised to frame Board-approved polici.es for providing these reliefs to all eligible borrowers with full public disclosure. VI.32 The lending institutions were advised that in respect of all accounts classified as standard as on February 29, 2020, where moratorium or deferment is granted, the 90-day NPA norm shall exclude the moratorium period, i.e., there would be an asset classification standstill for all such accounts from March 1, 2020 to August 31, 2020. Lending institutions were advised that in respect of accounts which have availed the relief provided by the Reserve Bank on March 27, 2020, they are required to make general provisions of not less than 10 per cent of the total outstanding of such accounts in a phased manner in two quarters, viz., not less than 5 per cent each, in quarters ended March 31, 2020 and June 30, 2020. Lending institutions were also advised that: (a) they are permitted to adjust these provisions against the actual provisioning requirements for slippages from the accounts reckoned for such provisions; (b) the residual provisions at the end of the financial year can be written back or adjusted against the provisions required for all other accounts; (c) till such adjustments, these provisions shall not be netted from gross advances but are to be shown separately in the balance sheet, as appropriate; and (d) all other provisions required to be maintained by lending institutions, including the provisions for accounts already classified as NPA as on February 29, 2020 as well as subsequent ageing in these accounts, shall continue to be made in the usual manner. VI.33 Under the Reserve Bank’s Prudential Framework for Resolution of Stressed Assets dated June 7, 2019, SCBs (excluding RRBs), AIFIs, Systemically Important Non-Deposit taking Non-Banking Financial Companies (NBFCs-NDSI), and Deposit taking Non-Banking Financial Companies (NBFCs-D) are required to hold an additional provision of 20 per cent in the case of large accounts under default, if a resolution plan has not been implemented within 210 days from the date of such default. Recognising the challenges to resolution of stressed assets in the current volatile environment, the above lenders were advised that the period from March 1, 2020 to August 31, 2020 may be excluded from the review period or, in cases where review period is over, the resolution period during which resolution may be implemented without any additional provisions. VI.34 The Liquidity Coverage Ratio (LCR) requirement for SCBs was brought down from 100 per cent to 80 per cent, with effect from April 17, 2020, to ease the liquidity position at the level of individual institutions. The requirement shall be gradually restored back in two phases – 90 per cent by October 1, 2020 and 100 per cent by April 1, 2021. Further, entire SLR-eligible assets held by banks have now been permitted to be reckoned as high-quality liquid assets (HQLAs) for meeting LCR. The implementation of NSFR guidelines, which were to come into effect from April 1, 2020 onwards, was deferred by six months to October 1, 2020. VI.35 The implementation of the last tranche of 0.625 per cent of Capital Conservation Buffer (CCB) was deferred from March 31, 2020 to September 30, 2020. The activation of Countercyclical Capital Buffer (CCyB) was not found to be necessary. VI.36 At the same time, banks were advised that they shall not make any further dividend payouts from profits pertaining to the financial year ended March 31, 2020 to conserve capital and absorb losses in an environment of heightened uncertainty. This restriction will be reviewed on the basis of the financial position of banks for the quarter ending September 30, 2020. VI.37 The maximum permissible period of pre-shipment and post-shipment export credit sanctioned by banks has also been increased from one year to 15 months, for disbursements made up to July 31, 2020, in line with the permitted increase in time period for realisation and repatriation of the export proceeds to India. VI.38 As an additional measure to support the MSME sector in these uncertain times, banks were permitted to reckon the funds infused by the promoters in their MSME units, through loans availed under the Credit Guarantee Scheme for Subordinate Debt for stressed MSMEs issued by the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE), as equity/quasi equity from the promoters for debt-equity computation. VI.39 To mitigate the difficulties in timely submission of various regulatory returns to DoR, the Reserve Bank, due to disruptions caused by COVID-19 pandemic, all the regulated entities (REs) were advised that such returns (required to be submitted up to June 30, 2020) can be submitted with a delay of a maximum of 30 days from the due date. However, extension was not permitted for submission of statutory returns, i.e., returns prescribed under the Banking Regulation (BR) Act 1949, RBI Act 1934, or any other Acts [for instance, returns related to cash reserve ratio (CRR)/statutory liquidity ratio (SLR)]. VI.40 Due to strains on reporting requirements caused by COVID-19 pandemic, the relaxation of the minimum daily maintenance of the CRR of 80 per cent, effective from the fortnight beginning March 28, 2020 till June 26, 2020, was extended for a further period of three months, i.e., up to September 25, 2020. VI.41 Master Direction on KYC was amended, in alignment with PML rules of the Government of India, pertaining to small accounts [opened for those customers who are not able to furnish Officially Valid Document (OVDs) to the banks] that remained operational initially for a period of twelve months, which could be extended for a further period of twelve months provided the account holder applied for any of the OVDs during the first twelve months. Post this amendment, the small accounts shall remain operational between April 1, 2020 and June 30, 2020 and such other periods as may be notified by the Government of India, notwithstanding the conditions stipulated. The amendment was carried out to enable the Direct Benefit Transfer (DBT) to the beneficiaries’ accounts and allow the beneficiaries to withdraw the amount for their needs in the current situation due to COVID-19 pandemic, without causing any hardships due to the KYC requirements. Other Initiatives VI.42 Some of the other initiatives during 2019-20 were as follows:

Agenda for 2020-21 VI.43 For the year ahead, the Department will focus on the following key deliverables in respect of the commercial banks under Utkarsh:

Cooperative Banks VI.44 The Reserve Bank continues to play a key role in strengthening the cooperative banking sector by fortifying the regulatory and supervisory framework. In this context, the DoR - Cooperative Banks, which is in charge of prudential regulations of cooperative banks, took several initiatives in 2019-20 in pursuance of the agenda set in the beginning of the year. Agenda for 2019-20: Implementation Status Goals Set for 2019-20 VI.45 The Department had set out the following goals for cooperative banks in 2019-20:

Implementation Status of Goals Establishment of UO for UCBs VI.46 The National Federation of Urban Cooperative Banks and Credit Societies Ltd. (NAFCUB) is setting up the UO for UCBs for which regulatory approval was accorded on June 6, 2019. Review of SAF for UCBs to Deal with Stress at an Early Stage VI.47 Under the revised guidelines on SAF for UCBs, issued on January 6, 2020, initiation of corrective action by the UCBs and/or supervisory action by the Reserve Bank is envisaged on breach of specified thresholds (triggers) in respect of specified financial parameters/indicators. The guidelines intend to make SAF more effective in bringing about improvement in weak but viable UCBs and resolving non-viable UCBs in an expeditious manner. Guidelines Issued to UCBs on BoM VI.48 Under the extant legal framework, the Board of Directors (BoD) of UCBs perform both executive and supervisory roles, with the responsibility to oversee the functioning of the UCBs as a cooperative society as well as a bank. UCBs with deposits of ₹100 crore and above have been advised to constitute BoM comprising of members with special knowledge and practical experience in banking so as to facilitate professional management, improve corporate governance and protect the interests of depositors (Box VI.2). Guidelines Issued to UCBs on Reporting of Large Exposures to CRILC VI.49 SCBs, SFBs, AIFIs, NBFCs-ND-SI, NBFCs-D and Non-Banking Financial Company in Factoring Services (NBFC-Factors) are currently required to report credit exposures of ₹5 crore and above on CRILC. UCBs with assets of ₹500 crore and above were brought under the CRILC reporting framework from the quarter ending December 31, 2019 in order to bring transparency and ensure early detection of stress in large exposures. ‘In Principle’ Approval for SFB License VI.50 Guidelines for voluntary transition of UCBs into SFBs were issued on September 27, 2018. Shivalik Mercantile Cooperative Bank Ltd. became the first UCB to receive ‘in-principle’ approval on January 6, 2020. Exposure to Single Borrower/Party and Group of Borrowers/Parties, Large Exposures and Priority Sector Lending VI.51 The exposure limits for single borrower/ party and group of borrowers/parties of UCBs were reduced from the existing 15 per cent and 40 per cent of the capital funds to 15 per cent and 25 per cent of the tier-I capital, respectively, on March 13, 2020. Moreover, 50 per cent of the loan portfolio of UCBs should comprise loans up to ₹25 lakh or 0.2 per cent of Tier I capital, whichever is higher, subject to a maximum of ₹1 crore per borrower/party. The target for lending to priority sector was increased from the existing 40 per cent to 75 per cent of adjusted net bank credit (ANBC) or credit equivalent amount of off-balance sheet exposure (CEOBSE), whichever is higher, in order to further strengthen the role of UCBs in financial inclusion. Further, UCBs will be required to contribute to Rural Infrastructure Development Fund (RIDF) with NABARD and other funds with NABARD/NHB/SIDBI/Micro Units Development and Refinance Agency (MUDRA) Bank against the shortfall in their achievement of the priority sector lending targets with effect from March 31, 2021, thereby harmonising the guidelines in this regard with those for SCBs. Amendments to the BR Act, 1949 (As Applicable to Cooperative Societies) VI.52 With a view to improving the quality of management and governance in co-operative banks and to ensure more effective regulation, thereof, by the Reserve Bank, Government of India has promulgated the BR (Amendment) Ordinance, 2020 on June 26, 2020, amending certain sections of the BR Act, 1949, thereby bringing additional areas of functioning of cooperative banks under the regulatory purview of the Reserve Bank. The major provisions amended through the ordinance pertain to areas such as non-applicability of the Act to certain types of co-operative societies, governance/ management of cooperative banks including certain restrictions on whole-time directors, approval of appointment/ removal of statutory auditors (SAs), time allowed for disposal of non-banking assets, providing additional avenues for raising capital, voluntary/ compulsory amalgamation, preparation of scheme of reconstruction and winding up by the concerned High Court at the instance of the Reserve Bank. The Ordinance has come into force presently for UCBs by notification in the official Gazette on June 29, 2020. Scheduling and Licensing of Cooperative Banks VI.53 The Meghalaya Cooperative Apex Bank Ltd. was included in the Second Schedule of the RBI Act, 1934 on August 30, 2019. Banking license was issued to Supaul District Central Cooperative Bank, Supaul, Bihar on December 19, 2019. Amalgamation of DCCBs VI.54 The short-term rural cooperative credit structure in India consists of a three-tier structure, with State Co-operative Banks (StCBs) as the apex institution in each state, DCCBs operating at the intermediate (district) level and Primary Agricultural Credit Societies (PACS) at the base (village) level. The structure, however, varies from state to state, with some states having a two-tier co-operative credit structure comprising only StCBs and PACS. Based on the recommendations of the Expert Committee constituted by the Reserve Bank in 2012 (Chairman: Shri Prakash Bakshi), some state governments have found a two-tier structure more effective. In August 2017, the government of Kerala had proposed for amalgamation of its fourteen DCCBs with Kerala State Cooperative Bank (KStCB) and on October 3, 2018, the Reserve Bank had accorded in-principle approval for the amalgamation, contingent to fulfilment of conditions stipulated by it and additional conditions imposed by NABARD. The final approval for the amalgamation (except Malappuram DCCB) was given by the Reserve Bank on October 7, 2019, subject to approval by the Hon’ble High Court of Kerala and infusion of additional capital by the government of Kerala, to ensure a capital to risk-weighted assets ratio (CRAR) of 9 per cent on an ongoing basis. Accordingly, thirteen DCCBs were amalgamated with the KStCB on November 29, 2019. VI.55 ‘In-principle’ approval has also been granted on June 8, 2020 to the government of Punjab for amalgamation of DCCBs in the state with the Punjab State Cooperative Bank, subject to fulfilment of the conditions stipulated by the Reserve Bank and additional conditions, if any, imposed by NABARD. Other Initiatives VI.56 It is envisaged to bring out a Discussion Paper on Formulation of Policy Framework for promoting consolidation in the UCB sector, which is presently under process. Agenda for 2020-21 VI.57 The agenda for cooperative banks in 2020- 21 would include the following:

Non-Banking Financial Companies (NBFCs) VI.58 NBFCs play an important role in providing credit by complementing the efforts of commercial banks, providing last mile financial intermediation and catering to niche sectors. The DoR - NBFC is entrusted with the responsibility of regulating the NBFC sector. Agenda for 2019-20: Implementation Status Goals Set for 2019-20 VI.59 The Department had set out the following goals in respect of NBFCs in 2019-20:

Implementation Status of Goals Harmonisation of NBFC Categories VI.60 Three categories of NBFCs, viz., Asset Finance Companies (AFCs), Loan Companies (LCs) and Investment Companies (ICs), were merged into a new category called NBFC-Investment and Credit Company (NBFC-ICC). Feasibility of merging other categories of NBFCs was also examined and it was decided to continue with the status quo for now. Issuance of FPC for ARCs VI.61 With the objective of ensuring transparency and fairness in the operations of ARCs, FPC providing minimum regulatory expectations has been issued while allowing ARCs’ Board to enhance its scope and coverage. The FPC, inter alia, covers transparent and non-discriminatory practices for acquisition as well as sale of assets, reasonableness of fees and grievance redressal mechanism. Liquidity Risk Management Framework VI.62 The Reserve Bank revised the guidelines on liquidity risk management to strengthen the asset-liability management (ALM) framework of NBFCs, including core investment companies (CICs). The revised guidelines specify granular maturity buckets and tolerance limits, and adoption of liquidity risk monitoring tools. NBFCs are required to monitor liquidity by employing the stock approach, in addition to the measurement of structural and dynamic liquidity while adopting the principles of sound liquidity risk management, stress testing and measures for diversification of funding. The framework requires maintenance of a liquidity buffer in terms of LCR starting at 50 per cent for all NBFCs-D and NBFCs-ND with an asset size of ₹10,000 crore and above, and 30 per cent for NBFCs-ND with an asset size of ₹5,000 crore and above, but less than ₹10,000 crore, from December 1, 2020 to reach 100 per cent by December 1, 2024. Review of Household Income and Lending Limits for Non-Banking Financial Company – Micro Finance Institutions (NBFC-MFIs) VI.63 NBFC-MFIs play a key role in delivering credit to those at the bottom of the economic pyramid. In view of their importance in a growing economy, the household income limits for borrowers of NBFC-MFIs were raised from the current level of ₹1,00,000 for rural areas and ₹1,60,000 for urban/semi urban areas to ₹1,25,000 and ₹2,00,000, respectively. Moreover, lending limit for NBFC-MFIs was increased from ₹1,00,000 to ₹1,25,000 per eligible borrower. Technical Specifications for all Participants of the Account Aggregator (AA) Ecosystem VI.64 The Non-Banking Financial Company - Account Aggregator (NBFC-AA) consolidates financial information of a customer held with different financial entities spread across financial sector regulators and using different information technology (IT) systems and interfaces. A set of core technical specifications based on Application Programme Interface (API) framed by the Reserve Bank Information Technology Private Ltd. (ReBIT) has been prescribed for the participants of the AA ecosystem regulated by the Reserve Bank, namely NBFC-AA, financial information providers and financial information users, in order to ensure secured, authorised and seamless movement of data. The open API based specifications framed for movement of data and consent architecture will go a long way in realising the full potential of the AA ecosystem. Review of Limits for Lenders on Non-Banking Financial Company - Peer to Peer Lending Platform (NBFC-P2P) VI.65 The aggregate exposure of a lender to all borrowers at any point of time across all Peer to Peer Lending (P2P) platforms was increased from ₹10,00,000 to ₹50,00,000. Escrow accounts to be operated by bank-promoted trustee(s) for transfer of funds need not be mandatorily maintained with the bank which has promoted the trustee. Temporary Relaxation of Minimum Holding Period (MHP) Requirement VI.66 MHP requirement for originating NBFCs was relaxed in November 2018 in respect of loans of original maturity above 5 years, in order to encourage NBFCs to securitise/assign their eligible assets. This dispensation, given initially for a period of six months, i.e., up to May 2019, was extended till December 31, 2019 and further till June 30, 2020. Implementation of Ind AS VI.67 Implementation guidelines on specific prudential aspects of Ind AS for NBFCs and ARCs have been issued, in order to promote a high quality and consistent implementation as also to facilitate comparison and better supervision. The implementation guidelines cover governance framework, prudential floor for expected credit losses including impairment reserve, certain principles for computation of regulatory capital and regulatory ratios, etc. Regulation of HFCs VI.68 Under the provisions of the NHB Act, 1987, HFCs have been regulated and supervised by the NHB. Over time, the mandate of the NHB widened and it assumed the role of refinancer and lender to the sector. Recognising the conflicting aspects of the mandate, the Union Budget 2019-20 returned regulatory authority over the housing finance sector to the Reserve Bank on August 9, 2019, with supervision and grievance redressal mechanisms retained with the NHB. Income Recognition, Asset Classification and Provisioning Norms VI.69 On February 7, 2020, it was decided to harmonise the guidelines for deferment of DCCO for projects of CRE sectors with those of non-infrastructure sector exposures held by SCBs (excluding RRBs) and SFBs. These guidelines were extended mutatis mutandis to NBFCs. Insolvency Resolution and Liquidation Proceedings of NBFCs VI.70 Government of India, vide its notification dated November 15, 2019, has expanded the applicability of Insolvency and Bankruptcy Code (IBC) to cover systemically important Financial Service Providers (FSPs) other than banks. This special framework under IBC is essentially aimed at serving as an interim mechanism to deal with any exigency, pending introduction of a full-fledged enactment to deal with financial resolution of banks and other systemically important FSPs. Subsequently, the Government of India, vide notification dated November 18, 2019, has empowered the Reserve Bank to initiate the Corporate Insolvency Resolution Process (CIRP) against NBFCs including HFCs with asset size of Rs.500 crore or more. In December 2019, the Reserve Bank initiated CIRP against one problematic HFC under this framework. Loans Sourced by Banks and NBFCs over Digital Lending Platforms: Adherence to FPC and Outsourcing Guidelines VI.71 It has been observed that many digital platforms have emerged in the financial sector claiming to offer hassle free loans to retail individuals, small traders, and other borrowers. Banks and NBFCs are also seen to be engaging digital platforms to provide loans to their customers. In addition, some NBFCs have been registered with Reserve Bank as ‘digital-only’ lending entities while some NBFCs are registered to work both on digital and brick-mortar channels of credit delivery. Thus, banks and NBFCs are observed to lend either directly through their own digital platforms or through a digital lending platform under an outsourcing arrangement. The lending platforms tend to portray themselves as lenders without disclosing the name of the bank/ NBFC at the backend, as a consequence of which, customers are not able to access grievance redressal avenues available under the regulatory framework. In order to address the concerns emanating from non-transparency of transactions and violation of extant guidelines on outsourcing of financial services and FPC issued to banks and NBFCs, the Reserve Bank has reiterated the need to adhere to the guidelines in this regard in letter and spirit. Other Initiatives VI.72 Some of the other initiatives during 2019-20 were as follows:

Agenda for 2020-21 VI.73 During 2020-21, the Department will pursue the following goals in respect of NBFCs: • Review of Regulatory Arbitrage between Banks and NBFCs - with a view to harmonise the regulations of NBFCs with those of banks (Utkarsh); • Scale-based Approach to Regulation of NBFCs - with a view to identify a small set of ‘systemically significant’ NBFCs, which can potentially impact financial stability as also to adopt a graded regulatory framework for the NBFCs; • Issuance of Master Directions for HFCs - proposals for defining the term housing finance, introduction of principal business criteria, qualifying assets for HFCs and classification of HFCs as systemically important, etc., were placed on the Bank's website on June 17, 2020 for public comments and, the revised regulations will be issued after receipt of such comments; and • Comprehensive Review of CIC Guidelines-in view of the recent failure of a CIC and its adverse impact on the non-banking financial sector, the Reserve Bank constituted a Working Group (WG) to review the regulatory and supervisory framework of CICs, whose recommendations are set to shape the overall policy approach to CICs (Box VI.3). 4. SUPERVISION OF FINANCIAL INTERMEDIARIES Department of Supervision (DoS) Commercial Banks VI.74 In the banking area, a number of measures were taken by DoS - Banks to sharpen the supervisory oversight of SCBs (excluding RRBs), LABs, Payments Banks (PBs), SFBs, Credit Information Companies and AIFIs during the year. Agenda for 2019-20: Implementation Status Goals Set for 2019-20 VI.75 The Department had set out the following goals for supervision of SCBs during 2019-20 under Utkarsh:

Implementation Status of Goals Off-site Surveillance Mechanism VI.76 A system-wide analysis of the banking system, capturing major risk patterns, was strengthened during 2019-20. The Department started carrying out a detailed “Quarterly Off-site Surveillance with Sharper Focus and Pro-active Indicators” for banks from September 2019, on identification of outliers for deeper examination, which was replicated for other SEs too. VI.77 During the year, the frequency of data collected as part of CRILC was increased to monthly from quarterly, with data on defaults being collected on a weekly basis. Interactive dashboards, summary dossiers, entity-level reports and technological solutions are envisaged to be part of the revamped data warehouse system of the Reserve Bank – the Centralised Information and Management System (CIMS). Process Audit VI.78 As part of continuous monitoring framework, process audit of critical processes in the banks has been embedded into existing systems. Concurrent and Statutory Audit System VI.79 The guidelines on concurrent audit system were amended giving discretion to banks to determine the scope and coverage of concurrent audit within the broad prescribed parameters. This was necessitated considering the differing levels of centralisation in banks, the diverse nature of activities undertaken by banks and commencement of operations by SFBs and PBs. VI.80 A web-based Auditor Allocation System for appointment of statutory branch auditors of PSBs was put in place. This application is expected to reduce the turnaround time in branch auditors’ appointments. Frauds Analysis VI.81 The total cases of frauds (involving ₹1 lakh and above) reported by banks/FIs increased by 28 per cent by volume and 159 per cent by value during 2019-20 (Table VI.2). The date of occurrence of these frauds are, however, spread over several previous years. VI.82 Frauds have been predominantly occurring in the loan portfolio (advances category), both in terms of number and value. There was a concentration of large value frauds, with the top fifty credit-related frauds constituting 76 per cent of the total amount reported as frauds during 2019-20. Incidents relating to other areas of banking, viz., off-balance sheet and forex transactions, fell in 2019-20 vis-à-vis the previous year (Table VI.3). VI.83 While the frauds framework focuses on prevention, early detection and prompt reporting, the average lag in detection of frauds remains long. The average lag between the date of occurrence of frauds and their detection by banks/ FIs was 24 months during 2019-20. In large frauds, i.e., ₹100 crore and above, however, the average lag was 63 months. The sanction of the credit facility in many of these accounts was much older. Weak implementation of Early Warning Signals (EWS) by banks, non-detection of EWS during internal audits, non-cooperation of borrowers during forensic audits, inconclusive audit reports and lack of decision making in Joint Lenders' meetings account for delay in detection of frauds. The EWS mechanism is getting revamped alongside strengthening of the concurrent audit function, with timely and conclusive forensic audits of borrower accounts under scrutiny. Advisory Board for Banking Frauds (ABBF) VI.84 The ABBF was created in consultation with the Central Vigilance Commission (CVC). The ABBF functions as the first level of examination of all large value fraud cases before recommendations/references are made to the investigating agencies by PSBs. The jurisdiction of ABBF would be confined to those cases involving the level of General Manager (GM) of banks and above. Other Initiatives VI.85 Some of the other initiatives during 2019-20 were as follows: • A standing committee on analytics comprising experts from eminent institutions such as Indian Institute of Technology (IIT), Indian Institute of Management (IIM), Indian Statistical Institute (ISI) and Institute for Development and Research in Banking Technology (IDRBT) was set up to engage in adopting industry standards in SupTech, best practices in business intelligence and data analytics for risk modelling that would deliver improved inputs to supervisory managers. • Apart from governance, the macroeconomic, environmental and socio-economic factors can impact the health of financial system. Hence, inclusion of disclosures based on Environment, Social and Governance (ESG) principles in the integrated supervisory framework would greatly facilitate consolidated supervision of financial conglomerates (Box VI.4). Agenda for 2020-21 VI.86 The Department has identified the following goals for supervision of SCBs in 2020-21:

Urban Cooperative Banks (UCBs) VI.87 In the cooperative institutions space, DoS - Cooperative Banks undertook periodic on-site and continuous off-site monitoring of UCBs during the year to ensure the development of a safe and well-managed cooperative banking sector. Agenda for 2019-20: Implementation Status Goals Set for 2019-20 VI.88 The Department had set out the following goals for supervision of UCBs in 2019-20 under Utkarsh:

Implementation Status of Goals Early Assessments of Deficiencies and Timely Supervisory Action VI.89 A model was developed for early assessment of deficiencies in the cooperative banking sector based on application of stress to selective financial parameters. The banks indicating weaknesses were identified and pre-emptive measures were taken to address the weakness in a timely manner. Making UCBs CBS Compliant VI.90 As on June 30, 2020, 1,529 (99.4 per cent) out of 1,538 UCBs, had implemented CBS. 3 out of the remaining 9 UCBs are under All-Inclusive Directions (negative net worth). Only 6 banks with positive net worth remain, that need to complete CBS implementation. CFR for UCBs VI.91 A CFR for UCBs was developed in 2019-20 and the User Approval Test (UAT) was completed. Workshops on Fraud Risk Management (FRM) and reporting by banks with a focus on improving the reporting quality and effective usage of CFR were conducted in Mumbai, New Delhi, Kolkata, Chennai, Bengaluru, and Thiruvananthapuram. A separate workshop for scheduled cooperative banks on reporting issues was also conducted in the College of Agricultural Banking (CAB), Pune. Cyber Security Related Measures VI.92 A comprehensive Cyber Security Framework for UCBs was formulated in December 2019, based on a graded approach. The UCBs have been categorised into four levels, based on their digital depth and interconnectedness in the payment systems landscape, digital products offered by them and assessment of cyber security risk. Other Initiatives VI.93 Some of the other initiatives during 2019-20 were as follows:

Agenda for 2020-21 VI.94 The Department has identified the following goals for supervision of UCBs in 2020-21:

Non-Banking Financial Companies (NBFCs) VI.95 With regard to NBFCs, DoS - NBFCs monitored the entities (excluding HFCs) registered with the Reserve Bank with the objective of protecting the interests of depositors and customers, while ensuring financial stability. Agenda for 2019-20: Implementation Status Goals Set for 2019-20 VI.96 The Department had set out the following goals for supervision of NBFCs for 2019-20 under Utkarsh:

Implementation Status of Goals Strengthening On-Site Supervision VI.97 Strengthening on-site supervision of NBFCs during the year included greater coverage of CICs and government owned companies; and incisive on-site supervision of smaller NBFCs with an event-based approach. This led to initiation of enforcement action against several non-compliant NBFCs and cancellation of Certificates of Registration of 120 NBFCs during 2019-20. VI.98 The top 50 NBFCs (representing 76 per cent of the asset size of the NBFCs) are closely and intensively monitored by the Reserve Bank, including through deep dives into their books of accounts and avoiding slippages. Supervisory Structure and Processes VI.99 The Reserve Bank has been empowered to remove the Directors of NBFCs, other than government-owned entities, to supersede their boards and appoint administrators through insertion of new sections 45-ID and 45-IE in the RBI Act, 1934 and through the new section 45MAA, to remove or debar an auditor for a maximum period of three years with a view to strengthening the governance of NBFCs. The Reserve Bank may also frame schemes for amalgamation, reconstruction and splitting of NBFCs into different units. Monitoring of related parties of NBFCs has been strengthened by inserting section 45 NAA in the RBI Act, 1934, directing group companies of NBFCs to furnish financial statements. The quantum of penalties applicable on NBFCs has been raised substantially too. Data Quality and Consistency VI.100 The submission of returns by NBFCs using the XBRL platform was formalised. This will make available data received from on-site inspection, off-site surveillance and SAs on an integrated platform. Consistent data quality enables the identification of early warning signals of stress in the SEs. VI.101 A new XBRL software has been developed to improve data quality through in-form and cross-form validations, provisions for auto calculation of sub-totals and totals to obviate human error in reporting, and the generation of variance reports to check data consistency across time as well as between returns. All returns for NBFCs have been revised and rationalised from the present 21 to 19 in order to deepen and widen the information being obtained. The Department also developed on-going surveillance frameworks which extensively use data available under off-site supervision. The frequent usage of such data (Use Test) will help in improving data quality further. Engagement with Stakeholders VI.102 Engagement with stakeholders of the NBFC sector, including their SAs, CRAs, other regulators, banks and mutual funds facilitated the early identification of emerging risks in the sector to enable prompt supervisory intervention. VI.103 The Sachet portal, which facilitates lodging of complaints related to deposits/schemes of various companies and serves as a source of market intelligence (MI), was made available in 11 regional languages, in addition to Hindi and English. This has widened the coverage for receipt of information on Ponzi schemes and deposit collection by unauthorised bodies. Other Initiatives VI.104 A template designed for SAs that enables them to directly upload the audited data to the Reserve Bank’s database through XBRL platform, will be activated for submission of audited data from the financial year 2020-21 onwards. The initiative is expected to facilitate benchmarking of financials of various NBFCs. Agenda for 2020-21 VI.105 The Department has identified the following goal for supervision of NBFCs in 2020-21 under Utkarsh:

Supervisory Measures for All Supervised Entities (SEs) VI.106 A unified DoS has been operationalised in which the supervision of banks, UCBs and NBFCs are undertaken in a holistic manner under one umbrella Department. This is intended to address inter-institutional issues on regulatory/supervisory arbitrage, information asymmetry and interconnectedness. A number of measures were taken to sharpen the intensity of on-site examinations while developing a proactive off-site surveillance framework for the SEs taken together. Agenda for 2019-20: Implementation Status Goals Set for 2019-20 VI.107 The Department had set out the following supervisory goals for all SEs in 2019-20 under Utkarsh:

Implementation Status of Goals Unification of Supervisory Departments VI.108 The supervision function was integrated under a unified DoS with effect from November 1, 2019, by merging all supervisory departments, viz., Department of Banking Supervision (DBS), Department of Co-operative Banking Supervision (DCBS) and Department of Non-Banking Supervision (DNBS), into one Department. The objective is to develop a holistic approach for the supervision of REs so as to address growing complexities, including size and inter-connectedness, as also to deal more effectively with potential systemic risks from supervisory arbitrage and information asymmetry. This redesigning will establish a graded supervisory approach and a more effective consolidated supervision of financial conglomerates. Supervisory Structure and Processes VI.109 A horizontal Risk Specialist Division was created in the Department to create a specialised wing to support risk discovery in an SE and to strengthen off-site supervisory bandwidth. A virtual College of Supervisors (COS) was set up under the aegis of the RBI Academy for capacity building among supervisory examiners. Its first online course was held on May 22, 2020. Areas of focus include research and modelling for supervision; microdata analytics for improved transaction testing; KYC/AML for better compliance by the SEs; risk and compliance culture and business strategy for improved governance practices in the SEs; and extension of the concept of a designated Senior Supervisory Manager (SSM), which started from banks with implementation of RBS, to all SEs. Separate Structure for KYC/AML Risk VI.110 A separate and specialised structure for KYC/AML risk based supervision has been created to supervise all SEs. Proactive Off-site Supervision Mechanism VI.111 The objective of an effective proactive off-site surveillance system is to be able to ‘smell distress’ early and initiate pre-emptive actions. This requires use of MI inputs, on-going engagement with the top management of the SEs on the alerts on potential vulnerabilities and selective bilateral engagements with the CEOs. In order to achieve this objective, the Department put in place a system for identification of vulnerable SEs for timely and proactive action to address these vulnerabilities. This involves both direct and indirect methodologies towards assessment of vulnerabilities in SCBs, NBFCs, SFBs and UCBs. VI.112 Quarterly proactive off-site vulnerability assessment exercises were carried out for banks, NBFCs, SFBs and UCBs using data analytics, early warning systems, identification of vulnerable borrowers, stress testing, vulnerability on cyber security parameters and through different thematic analyses. All these together are targeted to guide towards better awareness about the risks in the group; cognition gap, if any; ‘smell distress’ early; and take timely proactive action. Macro-Stress Tests VI.113 The Department has been conducting supervisory stress tests since 2013 to assess the impact of shocks to the portfolios of banks under adverse scenarios, while also factoring in supervisory heuristics. In 2018, a revised top-down stress-testing model was developed in collaboration with the World Bank. Further improvements include a revised credit-risk stress test incorporating a set of three panel-data econometric models linking the real and financial sectors; reverse stress tests to assess liquidity risk; a new stress test to analyse large exposures at the system level; and a new duration-based stress test for interest-rate risk (IRR) that incorporates stress to the loan book as well as the trading book. EWS Framework VI.114 EWS was introduced as part of the off-site surveillance framework to streamline the process of risk discovery and capture potential vulnerabilities by leveraging on off-site analysis of data and predictive supervisory assessments, based on empirical data combined with scenario-based analysis. A pool of indicators including macro-economic variables, market indicators and balance sheet indicators is used from which statistically significant variables are chosen as Early Warning Indicators (EWIs) [credit growth, deposit growth, weighted average lending rate, net interest margin, capital to risk-weighted assets ratio, tier-I capital ratio and off-balance sheet exposure to total assets ratio]. The focus is to diagnose and detect vulnerability proactively, identify stress in the all SEs, viz., banks, NBFCs and UCBs, and take corrective measures, as required. Measuring Interconnectedness VI.115 In view of the significant increase in the intermediation between banks and NBFCs and the stress faced by some NBFCs in the recent period, a Bank-NBFC Intermediation Index (BNII) was created to quantify inter-linkages. Similarly, an Asset Quality Index (AQI) was created to track the changes in asset quality of a bank’s exposure to NBFCs. Integrated Compliance Management and Tracking System (ICMTS) VI.116 A web-based online application, ICMTS has been envisaged with an apt automated approach to manage the inspection lifecycle of SEs, supported by robust complaints and compliance management system. The application will act as a centralised repository of inspection reports/scrutiny reports/ instructions/guidelines/ circulars/complaints and their compliance with the documents/evidences submitted by SEs. The application is being designed in such a way that it will be capable of capturing/monitoring the end-to-end compliance life cycle. The application will help in improving the on-site/off-site monitoring process and response mechanism. Cyber Security Measures VI.117 During 2019-20, thirty-nine banks were subjected to IT examinations to assess their level of cyber security preparedness and degree of compliance with the circulars, advisories and alerts issued by the Reserve Bank from time to time. Thematic studies on select application service providers (ASPs) of the banking sector were undertaken during the year. A joint cyber security exercise was conducted by the Reserve Bank and Indian Computer Emergency Response Team (CERT-In) on February 12, 2020 and February 13, 2020 in which 70 select UCBs participated. VI.118 Considering the dependency of SEs on the third-party ASPs for ATM Switch applications, adherence to the baseline cyber security controls by the ASPs was mandated, with access allowed to the Reserve Bank for on-site/off-site supervision of these entities, through contractual agreements with SEs. Graded SAF VI.119 A SAF for all SEs has been put in place with a structured escalation matrix for supervisory actions which would act as a tool for early supervisory interventions mostly prior to enforcement action. The objective is to bring consistency, reasonableness and transparency in supervisory actions and to ensure compliance with the Reserve Bank's guidelines, including KYC/AML, and more generally to improve the quality and timeliness of submission of supervisory returns. Other Initiatives VI.120 Some of the other initiatives during 2019-20 were as follows:

Impact of COVID-19 Pandemic and the Mitigating Measures VI.121 With the spread of COVID-19 pandemic, supervisory measures initiated by the Reserve Bank were aimed at operational issues which included ensuring business continuity, cyber security and unhindered operations of the financial market infrastructure, while moderating the compliance burden on banks. The Reserve Bank not only ensured continuity of its own operations, but also enhanced its supervisory monitoring to ensure that any threat to financial stability is identified early and acted upon without delay. Through the pandemic, the financial system of the country, including all the payment systems, is functioning without any hindrance. To ensure that resilience of SEs is not affected materially, the Reserve Bank has also directed the SEs to assess the impact of the pandemic on their solvency and liquidity positions and to enhance their resilience by raising additional capital, if required. Cyber risk is being mitigated through issue of advisories, including from CERT-IN, regulatory reporting and periodic meetings with the top management of the SEs. VI.122 An assessment of the relief extended by SEs so far indicated that for the system as a whole, 48.6 per cent of total customers availed benefit of the Reserve Bank’s COVID-19 pandemic relief measures that constitute 50.1 per cent of the total outstanding amount up to April 2020. In the case of SCBs, 55.1 per cent of total customers availed of the Reserve Bank’s COVID-19 pandemic relief measures and constituted nearly 50.0 per cent of total outstanding amount. In case of NBFCs and UCBs, 29.0 per cent and 56.5 per cent of total customers availed the Reserve Bank’s relief measures, which constituted nearly 49.0 per cent and 64.5 per cent of the total outstanding amount, respectively. Agenda for 2020-21 VI.123 The Department has identified the following supervisory goals for all SEs in 2020-21:

Enforcement Department (EFD) VI.124 The Enforcement Department (EFD) was set up in April 2017 to enforce regulations uniformly across banks, with the objective of engendering compliance by REs, within the overarching principles of ensuring financial stability, public interest and consumer protection. The enforcement policy and framework approved by the Board for Financial Supervision (BFS) emphasises the need to be objective, consistent and non-partisan in undertaking enforcement. Enforcement in respect of cooperative banks and NBFCs was also brought under the scope of operations of the Department with effect from October 3, 2018. Agenda for 2019-20: Implementation Status Goals Set for 2019-20 VI.125 The Department had set out the following goals for 2019-20 under Utkarsh:

Implementation Status of Goals VI.126 During the year, in furtherance to the goal set out in Utkarsh, the enforcement policy and framework was reviewed and updated to include cooperative banks and NBFCs. In view of their relatively large number, decentralisation of enforcement work related to these entities was envisaged by setting up ROs of EFD at six centres, viz., Ahmedabad, Chennai, Kolkata, Mumbai, Nagpur and New Delhi, to ensure operational efficiency and facilitate focused enforcement. Pursuant to the creation of ROs of EFD, approval for staffing them with requisite manpower was obtained. VI.127 During July 2019-June 2020, the Department undertook enforcement action against 41 REs and imposed an aggregate penalty of ₹61.15 crore (Table VI.4) for non-submission of compliance to Risk Assessment Reports’ (RAR) findings; non-compliance with/contravention of directions on fraud classification and reporting; not adhering to discipline while opening current accounts and granting non-fund based facilities to non-constituent borrowers; not reporting to CRILC platform under RBS; violations of directions/ guidelines issued by the Reserve Bank on KYC/ Income Recognition and Asset Classification (IRAC) norms; non-compliance with the directions on cyber security framework and time-bound implementation and strengthening of Society for Worldwide Interbank Financial Telecommunication (SWIFT) related operational controls. Enforcement actions were also undertaken against contravention of the directions pertaining to third party account payee cheques; non-compliance with directions contained in risk mitigation plan (RMP); non-compliance with Prudential Norms for classification, valuation and operation of investment portfolio by banks; non-compliance with directions on window-dressing of balance sheet; contravention of the directions on ‘Loans and Advances to Directors, Relatives and Firms/Concerns in which they are interested’; non-compliance with the guidelines on promoter holding contained in ‘Guidelines for Licensing of New Banks in Private Sector’; and, failure to comply with the provisions of section 10B of the BR Act, 1949. Impact of COVID-19 Pandemic VI.128 The substantial source material for the Department’s functions being available in soft form, there was no significant impact of the pandemic induced lockdown on the initial processing of the cases and obtaining approvals for initiating enforcement action. The lockdown, however, impacted the conduct of personal hearings for the REs, which in turn caused some delay in bringing the cases to a logical conclusion within a reasonable time period. With the gradual withdrawal of lockdown, complemented by use of appropriate information and communication technology, the adverse bearing of COVID-19 pandemic on completion of enforcement process was sought to be minimised. VI.129 Some impact of the disruptions due to lockdown was also felt on the development of the software application for automating enforcement process flow as per the timelines originally envisaged. Agenda for 2020-21 VI.130 During the year ahead, the Department proposes to achieve the following goals:

5. CONSUMER EDUCATION AND PROTECTION Consumer Education and Protection Department (CEPD) VI.131 The Consumer Education and Protection Department (CEPD) frames policy guidelines to ensure protection of the interest of customers of REs in line with global best practices (Box VI.5), undertakes oversight of the functioning of the Ombudsman Schemes of the Reserve Bank and creates public awareness on safe banking practices, extant regulations on customer service and protection and avenues for redressal of customer complaints. Agenda for 2019-20: Implementation Status Goals Set for 2019-20 VI.132 The Department had set out the following goals for 2019-20:

Implementation Status of Goals Strengthening the Grievance Redressal System based on RCA VI.133 RCA of the major areas of complaints received in the offices of Ombudsmen, CEP cells and select banks was undertaken. Root causes of the complaints were identified at the level of customers and REs, on account of gaps in regulatory guidelines and from external threats. Issues relating to gaps in regulatory guidelines have been referred to the regulatory and supervisory departments. Issues to be addressed in coordination with other regulators are being followed up. In addition, banks and offices of Ombudsmen have been advised to intensify efforts to create awareness among bank customers and members of public for adopting safe banking practices. Going forward, RCA will be undertaken on a regular basis. Review of the IO Scheme for Extension to NBFCs VI.134 The proposal to extend the IO Scheme to all NBFCs covered under the Ombudsman Scheme for NBFCs - 2018, was examined. Considering the diversity in the size and business profile of NBFCs, the number of complaints received and customer interface, the implementation of the IO Scheme for NBFCs is under review for roll-out on the basis of selective applicability. Review of the Ombudsman Schemes for Updation and Effective Implementation VI.135 An In-house Committee was set up to examine, inter alia, issues relating to the convergence of the three schemes - the Banking Ombudsman Scheme, 2006 (BOS), the Ombudsman Scheme for NBFCs, 2018 (NBFC-OS) and the Ombudsman Scheme for Digital Transactions, 2019 (OSDT) - into an Integrated Ombudsman Scheme, and suggest measures for improving the effectiveness of the Ombudsman mechanism. The Committee has submitted its report and the proposals are being examined. Review of CEP cells VI.136 CEP cells redress complaints not covered by the Ombudsman Schemes. Amidst the challenges that affect grievance redressal by CEP cells, in particular the lack of quasi-judicial powers, the issue of strengthening CEP cells on the lines of the Ombudsmen has been examined by an internal working group. The recommendations of the internal working group have been reviewed by the in-house Committee studying the issues relating to the convergence of the Ombudsman schemes. The Committee has included recommendations on CEP cells in its report, which are being examined. IVRS for Online Support to the Complainant VI.137 Information on the Reserve Bank’s Complaint Management System (CMS) is made available on IVRS. Any person can dial 14440 and obtain basic guidance on CMS, the Banking Ombudsman Scheme, consumer protection regulations such as the limited liability of a customer in fraudulent electronic banking transactions, etc. Going forward, the IVRS will serve as an on-tap source of information on important aspects of customer service and grievance redressal for consumers of financial services. Launching the IO Scheme for Non-Bank System Participants VI.138 Launched in October 2019, the IO Scheme for Non-Bank System Participants is applicable to non-bank issuers of pre-paid payment instruments (PPIs) with more than one crore outstanding PPIs as on March 31, 2019. Customer complaints that are partly or wholly rejected by the non-bank issuer of PPI must be referred to the IO, an internal, independent authority at the apex of the internal grievance redressal mechanism, for a final decision. Satisfaction Survey of Customers VI.139 A third-party satisfaction survey of customers was undertaken by the Reserve Bank during the year (Box VI.6). The findings of the survey are also available on the Reserve Bank’s website (Annual Report on Banking Ombudsman Scheme, 2018-19). Dissolution of the Banking Codes and Standards Board of India (BCSBI) VI.140 The BCSBI was set up by the Reserve Bank in February 2006 as an independent and autonomous body, assigned to formulate codes of conduct to be adopted by banks voluntarily for ensuring fair treatment of customers. The Reserve Bank has since set up CEPD, issued the Charter of Customer Rights (CoCR) and considerably strengthened the Ombudsman mechanism to enhance consumer protection. It was accordingly decided to dissolve BCSBI, which is now in an advanced stage of completing its dissolution process. Consumer Awareness VI.141 During 2019-20, the Reserve Bank conducted country-wide awareness campaigns in coordination with its Department of Communication (DoC) through print and electronic media on various topics such as Ombudsman Schemes, Basic Savings Bank Deposit Account, banking facilities for senior citizens and differently abled persons, and safe digital banking. The Reserve Bank’s SMS handle ‘RBISAY’ was also used extensively for sending text messages on these issues. The IVRS further strengthened the Reserve Bank’s awareness generation efforts. The offices of Ombudsmen conducted 26 town hall events and 113 awareness/outreach programs, mainly in Tier II cities to create awareness regarding the Ombudsman Schemes.

Impact of COVID-19 Pandemic VI.142 The grievance redressal function was carried out uninterrupted amidst the COVID-19 pandemic. The CMS, which brings all stakeholders viz., the Reserve Bank, REs and customers on a single platform, and has a system-driven workflow process, ensured continued and effective grievance redressal even during the lockdown. REs were advised to ensure redressal of all COVID-19 pandemic related customer complaints on priority. Agenda for 2020-21 VI.143 The Department proposes the following agenda for 2020-21:

Deposit Insurance and Credit Guarantee Corporation (DICGC) VI.144 Deposit insurance system plays an important role in maintaining the stability of the financial system, particularly in assuring the protection of interests of small depositors and, thereby, ensuring public confidence. Deposit Insurance and Credit Guarantee Corporation (DICGC) is a wholly owned subsidiary of the Reserve Bank constituted under the DICGC Act, 1961. The deposit insurance extended by DICGC covers all commercial banks including LABs, PBs, SFBs, RRBs and co-operative banks. VI.145 The number of registered insured banks as on March 31, 2020 stood at 2,067 comprising 144 commercial banks (including 45 RRBs, 3 LABs, 6 PBs and 10 SFBs) and 1,923 co-operative banks (33 StCBs, 352 DCCBs and 1,538 UCBs). The DICGC raised the limit of insurance cover for depositors in banks to ₹5 lakh per depositor with effect from February 4, 2020 from the earlier level of ₹1 lakh with the approval of Government of India, with a view to providing a greater measure of protection to depositors in banks. The premium was also raised to 12 paise from 10 paise per ₹100 of assessable deposits per annum from the half year beginning April 1, 2020, in order to maintain an adequate level of the deposit insurance fund. With the present limit of deposit insurance in India at ₹5 lakh, the number of fully protected accounts (231 crore) as at end-March 2020 constituted 98.3 per cent of the total number of accounts (235 crore) as against the international benchmark1 of 80 per cent. In terms of amount, the total insured deposits of ₹68,71,500 crore as at end-March 2020 constituted 50.9 per cent of assessable deposits of ₹1,34,88,888 crore as against the international benchmark of 20 to 30 per cent. At the current level, the insurance cover works out to be 4.0 times per capita income for 2019-20. VI.146 DICGC builds up its Deposit Insurance Fund (DIF) through transfer of its surplus, i.e., excess of income (mainly comprising premium received from insured banks, interest income from investments and cash recovery out of assets of failed banks) over expenditure (payment of claims of depositors and related expenses) each year, net of taxes. This Fund is available for settlement of claims of depositors of banks taken into liquidation/amalgamation. During April 2019 - March 2020, the Corporation sanctioned total claims of ₹80.7 crore as against claims aggregating ₹40 crore during the preceding year. The size of the DIF stood at ₹1,10,380 crore as on March 31, 2020, resulting in a reserve ratio of 1.61 per cent (Box VI.7).

VI.147 In sum, amidst the concerns related to COVID-19 pandemic and economic growth, decisive measures were undertaken to remove impediments in supply of credit to sectors such as MSMEs and NBFCs. To smoothen the transmission of interest rates, linking of bank lending rates with external benchmarks was introduced. Banking sector witnessed consolidation in the form of mergers of some PSBs and amalgamation of certain DCCBs. Measures were also undertaken to strengthen regulatory and supervisory framework of SCBs, cooperative banks and NBFCs in line with the global best practices, and also with an objective to bring them under uniform enforcement framework to minimise the policy arbitrage. Measures to harness technology for efficient customer services and effective fraud detection were also put in place. Promoting doorstep banking services for the needy, extending the IO Scheme for Non- Bank System Participants and review of Ombudsman Schemes of the Reserve Bank were some of the major strides taken towards ensuring effective consumer protection. 1 International Association of Deposit Insurers (2013), “Enhanced Guidance for Effective Deposit Insurance Systems: Deposit Insurance Coverage”, Guidance Paper, March. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

ఈ పేజీని షేర్ చేయండి:

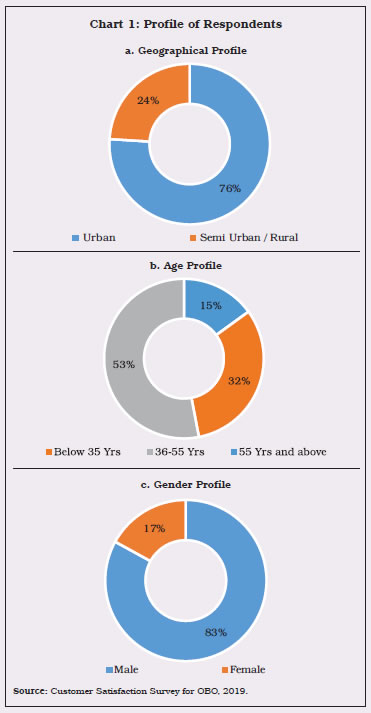

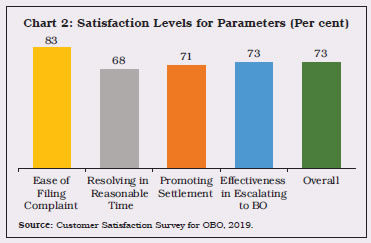

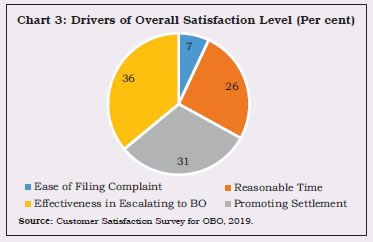

భారతీయ రిజర్వ్ బ్యాంక్ మొబైల్ అప్లికేషన్ను ఇన్స్టాల్ చేయండి మరియు తాజా వార్తలకు త్వరిత యాక్సెస్ పొందండి!