IX. Payment and Settlement Systems and Information Technology - আরবিআই - Reserve Bank of India

IX. Payment and Settlement Systems and Information Technology

| The Reserve Bank continued with its initiatives during 2024-25 to enhance the efficiency, security, and accessibility of payment systems, fostering a more inclusive and resilient digital payments ecosystem. Efforts towards accelerating global outreach of India’s domestic payment systems, particularly Unified Payments Interface (UPI) and RuPay cards, were sustained. The Reserve Bank seeks to leverage the latest technology to provide the best-in-class information and communication technology (ICT) infrastructure. IX.1 Building on the foundations of the Payments Vision documents1, the Reserve Bank focused on expanding digital payment adoption across all segments of society by promoting innovation and a supportive regulatory framework. The year witnessed greater emphasis on cyber resilience and payment security controls of payment system operators (PSOs), fraud prevention and consumer awareness to ensure a safe and seamless experience for users. On the global front, the Reserve Bank explored various avenues for expanding the global outreach of UPI and RuPay cards. IX.2 The Department of Information Technology (DIT) made significant advancements during the year in leveraging technology to enhance its operations, including the launch of PRAVAAH2 - a centralised web-based portal for submission of applications to the Reserve Bank for seeking authorisation, licenses or regulatory approvals. Several initiatives were taken in the areas of expanding cloud infrastructure for the financial sector and strengthening cyber security. IX.3 Against this backdrop, section 2 covers developments in the area of payment and settlement systems during 2024-25 and an assessment of the implementation status of the agenda for the year. Section 3 provides various measures undertaken by the DIT vis-à-vis the agenda set for 2024-25. The chapter has been summarised in section 4. 2. DEPARTMENT OF PAYMENT AND SETTLEMENT SYSTEMS (DPSS) IX.4 During the year, DPSS launched many initiatives in line with Payments Vision 2025, across the pillars of integrity, inclusion, innovation, institutionalisation and internationalisation. Payment Systems IX.5 India’s payment and settlement systems3 recorded a robust growth of 34.8 per cent in terms of transaction volume during 2024-25 on top of the expansion of 44 per cent in the previous year (Table IX.1). In value terms, the growth was 17.3 per cent in 2024-25 as compared with 15.8 per cent in the previous year, mainly due to growth in the large value payment system, viz., Real Time Gross Settlement (RTGS). The share of digital transactions in the total volume of non-cash retail payments was 99.9 per cent during 2024-25 (99.8 per cent a year ago). Digital Payments IX.6 During 2024-25, RTGS transactions increased by 12 per cent in volume terms and 17.8 per cent in value terms. The volume and value of retail transactions increased by 34.9 per cent and 16.1 per cent, respectively (Table IX.1). As on March 31, 2025, RTGS services were available through 1,73,688 IFSCs4 of 250 member banks, while NEFT services were available through 1,74,762 IFSCs of 236 member banks. IX.7 The retail payment system recorded robust growth in transaction volume as well as value in 2024-25 (Table IX.1). Amongst the retail payment system, UPI transactions increased by 41.7 per cent in terms of volume and 30.3 per cent in terms of value, while NEFT transactions rose by 32.4 per cent in terms of volume and 13.4 per cent in terms of value. In terms of volume, UPI transactions had the highest share (84 per cent) in total retail payments during 2024-25. IX.8 Payments Infrastructure Development Fund (PIDF) aided the growth in digital payments during the year by subsidising the availability of acceptance infrastructure, especially in Tier III to Tier VI centres. During 2024-25, the number of point of sale (PoS) terminals increased by 24.7 per cent to 1.1 crore. UPI Quick Response (QR) codes increased by 91.5 per cent to 65.8 crore as on March 31, 2025. Authorisation of Payment Systems IX.9 During the year, the Reserve Bank accorded authorisation/approval to 26 online Payment Aggregators (PAs), five Payment Aggregators - Cross Border (PA-CB), 11 non-bank Prepaid Payment Instrument (PPI) issuers, one Trade Receivables and Discounting System (TReDS) entity and one white label ATM (WLA) operator, besides granting in-principle authorisation to a few other online PAs, PPIs and WLA operators. Moreover, the Reserve Bank also granted approval to four banks for PPI issuance during the year (Table IX.2). Agenda for 2024-25 IX.10 The Department had set out the following goals for 2024-25:

Implementation Status IX.11 CPFIR, a web-based payment related fraud reporting solution, has been implemented from March 31, 2020. CPFIR reporting was made available to all scheduled commercial banks (SCBs) [including small finance banks (SFBs) and payments banks (PBs)], non-bank PPI issuers and non-bank credit card issuers. The reporting has now been extended to 49 scheduled UCBs, all local area banks, 43 RRBs, 71 district central co-operative banks (DCCBs) and 234 non-scheduled UCBs. The remaining banks are being on-boarded to CPFIR reporting in a gradual manner. IX.12 To improve the efficiency of cheque clearing, reduce settlement risk for participants and enhance customer experience, continuous clearing of cheques under CTS was announced in the statement on developmental and regulatory policies of the Reserve Bank (August 8, 2024). The approach paper and technical specification document on continuous clearing and on-realisation settlement under CTS were released to the CTS member banks by NPCI in August 2024. NPCI and banks are in the process of updating their systems, post which go-live will be scheduled. Once implemented, the cheque clearing cycle will reduce from the present T+1 day to a few hours. IX.13 The Reserve Bank is committed towards the goal of taking UPI to 20 countries with a completion timeline of 2028-29 and has been facilitating the global outreach of expanding the footprint of UPI as well as the RuPay cards. The Reserve Bank has joined Project Nexus and is actively collaborating with other countries on interlinking of FPS (Box IX.1). IX.14 To enable the payments ecosystem and leverage the technological advancements, the Reserve Bank issued a draft framework on ‘Alternative Authentication Mechanisms for Digital Payment Transactions’ on July 31, 2024. IX.15 A circular on introduction of beneficiary bank account name look-up facility for RTGS and NEFT systems was issued on December 30, 2024. The facility shall enable the remitters using RTGS and NEFT systems to verify the name of the bank account to which money is being transferred before initiating the fund transfer and thereby avoid mistakes and prevent frauds. Based on the account number and IFSC of the beneficiary entered by the remitter, the facility will fetch the beneficiary’s account name from the bank’s Core Banking Solution (CBS). All banks who are direct members or sub members of RTGS and NEFT were advised to offer this facility no later than April 1, 2025.

Major Developments Integrity Domestic Money Transfer (DMT) – Review of Framework IX.16 The framework for DMT was introduced in 2011 for opening up the formal banking channel to facilitate domestic fund transfers of small value, and users now have multiple digital options for funds transfer. Based on a review, the extant DMT framework was revised to enhance the safety of cash-based remittances by mandating due diligence process like: (a) registration of remitter with verified mobile number and officially valid document (OVD) as provided in ‘Master Direction – Know Your Customer Directions, 2016’; (b) validation of each transaction with additional factor of authentication (AFA); and (c) use of identifiers to classify the transactions as cash-based remittances. Updation of RTGS System Regulations and NEFT Procedural Guidelines IX.17 The Reserve Bank revised the RTGS regulations and the NEFT procedural guidelines on October 25, 2024, which include instructions on access criteria for membership to centralised payment systems (CPS), periodic review of membership, adherence to cyber security guidelines by CPS members on an ongoing basis and instructions from extant circulars concerning RTGS and NEFT. Revision of Central Counterparties (CCPs) Directions, 2024 IX.18 The Reserve Bank repealed ‘Directions for CCPs’ dated June 12, 2019 and issued the revised ‘Directions for CCPs’ on October 28, 2024 to strengthen corporate governance in CCPs. Some of the major changes in the Directions include increased representation of independent directors in Board meetings as well as in important committees such as Nomination and Remuneration Committee, Risk Management Committee and Audit Committee. Oversight of CPS IX.19 An onsite inspection of CPS was carried out in April 2024 by a team of internal experts sourced from different departments of the Reserve Bank. RTGS, being a financial market infrastructure (FMI) and a systemically important payment system, was assessed against the principles for financial market infrastructure (PFMIs)6 as outlined in the Reserve Bank’s oversight framework for FMIs and retail payment systems (RPS). The NEFT system, though not an FMI, was also assessed against the PFMIs. Cyber Resilience and Payment Security Controls of PSOs IX.20 Based on the feedback received from the stakeholders on the draft Master Direction, the final ‘Master Directions on Cyber Resilience and Digital Payment Security Controls for Non-bank PSOs’ were issued by the Reserve Bank on July 30, 2024. The Directions cover robust governance mechanisms for identification, analysis, monitoring and management of cyber security risks and vulnerabilities by providing a framework for overall information security preparedness, with an emphasis on cyber resilience. Enabling Additional Factor of Authentication (AFA) in Cross-border Card Not Present Transactions IX.21 Introduction of AFA for digital payments has enhanced the safety of transactions which, in turn, provided confidence to customers to adopt digital payments. This requirement, however, is mandatory for domestic transactions only. In order to provide a similar level of safety for online international transactions using cards issued in India, the Reserve Bank has proposed to enable AFA for non-recurring cross-border card not present transactions where request for an authentication is raised by an overseas merchant or overseas acquirer. Financial Inclusion Facilitating Accessibility to Digital Payment Systems for Persons with Disabilities IX.22 The Reserve Bank issued guidelines to promote effective access to digital payment systems wherein payment system participants (PSPs) [i.e., banks and authorised non-bank payment system providers] were advised to review their payment systems/devices in terms of accessibility to persons with disabilities. Based on the review, PSPs may carry out necessary modifications so that all their payment systems and devices such as PoS machines can be easily accessed and used by persons with disabilities. Introduction of Delegated Payments Through UPI IX.23 ‘Delegated Payments’/’UPI Circle’ enable individuals (primary user) to allow another individual (secondary user) to make UPI transactions up to a limit from the primary user’s bank account, without the need for the secondary user to have a separate bank account linked to UPI. This payment solution, introduced in August 2024, will further deepen the reach and usage of digital payments. UPI Access for PPIs Through Third-party Applications IX.24 The Reserve Bank permitted linking of PPIs through third-party UPI applications. This will enable PPI holders to make/receive UPI payments through third-party UPI applications. Payment Aggregators (PAs)-Offline - Draft Guidelines IX.25 PAs play an important role in the payments ecosystem and, hence, were brought under regulations in March 2020 and designated as PSOs. However, the current regulations are not applicable to offline PAs which handle proximity/ face-to-face transactions and play a significant role in the spread of digital payments. New draft Directions applicable to offline PAs as well were placed on the Reserve Bank’s website for feedback/comments. Business-to-Business (B2B) Payments in Bharat Bill Payment System (BBPS) IX.26 Businesses today are serviced through enterprise resource planning (ERP) systems, B2B service providers, FinTechs and banks. These solutions are currently not interoperable which makes payments and reconciliation of invoices across these platforms difficult. Hence, the Reserve Bank decided to include B2B as a category in BBPS operated by NPCI Bharat BillPay Ltd. (NBBL). Through BBPS, the systems will be able to interact with each other thereby reducing manual overheads. UPI - Enhancement of Limits IX.27 In order to encourage wider adoption of UPI, limits were enhanced for the following products of UPI:

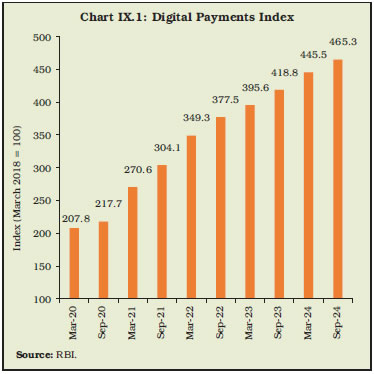

Pre-sanctioned Credit Lines Through UPI - Extending the Scope to SFBs IX.28 Credit lines on UPI has the potential to make available low-ticket, low-tenor products to ‘new-to-credit’ customers. SFBs leverage on a high-tech, low-cost model to reach the last mile customer and can play an enabling role in expanding the reach of credit on UPI. The Reserve Bank, therefore, permitted SFBs to extend pre-sanctioned credit lines through UPI. Enhancing Public Awareness Through Various Channels IX.29 During the year, 419 electronic banking awareness and training (e-BAAT) programmes were conducted by the regional offices of the Reserve Bank, in which safe usage of electronic payment systems, their benefits and grievance redressal mechanisms were explained to the participants. Innovation Auto-replenishment of FASTag, National Common Mobility Card (NCMC) and UPI Lite IX.30 The e-mandate framework for processing recurring transactions was issued by the Reserve Bank on January 10, 2020, enabling recurring payments with defined periodicity. Recurring payments such as replenishment of balances in FASTag and NCMC, which do not have any fixed periodicity, and/or are not time/amount specific, were permitted to be auto-replenished using e-mandate, and were exempted from the requirement of pre-debit notification on processing of e-mandates for recurring transactions. The Reserve Bank also brought UPI Lite facility within the ambit of the e-mandate framework by introducing an auto-replenishment facility for loading the UPI Lite wallet if the balance goes below a threshold amount set by the customer. Since the funds remain with the customer (funds move from the customer’s account to the wallet), the requirement of additional authentication or pre-debit notification has also been dispensed with. UPI for Cash Deposit IX.31 Cash deposit machines (CDMs) deployed by banks enhance customer convenience while reducing cash-handling load on bank branches. Given the popularity and acceptance of UPI, interoperable cash deposit facility through use of UPI has been enabled since June 2024. Internationalisation Global Outreach of Payment Systems IX.32 The Payments Vision 2025 Document envisaged expanding the global outreach of UPI and RuPay cards as one of the key objectives under the internationalisation pillar. The Reserve Bank has been facilitating the linkage of UPI with FPS of other countries on a bilateral basis, enabling both inward and outward remittance payments. Acceptance of India’s UPI apps via QR code has been operationalised in Bhutan, France, Mauritius, Nepal, Singapore, Sri Lanka, and the UAE, which enables Indian tourists, students, and business travellers in other countries to make payments to merchants using their Indian UPI apps. RuPay cards acceptance is presently live in Nepal, Bhutan, Mauritius, Singapore, the UAE and Maldives. Furthermore, the issuance of RuPay cards is live in Bhutan and Mauritius, and RuPay cards issued in Bhutan and Mauritius are acceptable in India as well. The Reserve Bank has given approval to NIPL for deployment of UPI like infrastructure in Namibia, Peru, Trinidad and Tobago, and Jamaica. Other Initiatives Review of ATM Interchange Fee and Customer Charges IX.33 The Reserve Bank had, from time to time, issued various instructions on the number of free ATM transactions and maximum charges that can be levied on a customer beyond the mandatory number of free transactions. Instructions were also issued on interchange fee structure for ATM transactions. Based on a review, it has been prescribed, vide the updated (as on March 28, 2025) circular on ‘Usage of Automated Teller Machines/Cash Recycler Machines – Review of Interchange Fee and Customer Charge’, that the ATM interchange fee will be as decided by the ATM networks. Further, with effect from May 1, 2025, banks may charge customers a maximum fee of ₹23 per ATM transaction, beyond the mandatory number of free transactions. Digital Payments Index (DPI) IX.34 The Reserve Bank had constructed a composite DPI in 2021 to capture the extent of digitisation of payments across the country. The RBI-DPI index, computed semi-annually, demonstrates significant growth representing the rapid adoption and deepening of digital payments across the country in recent years (Chart IX.1). Inspection of PSOs IX.35 Under Section 16 of the Payment and Settlement Systems Act, 2007, onsite inspections of 84 entities, viz., one financial market infrastructure (CCIL), one retail payment organisation [NPCI which includes NPCI Bharat BillPay Ltd. (NBBL), RuPay Cards, NPCI BHIM Services Ltd. (NBSL), and NPCI International Payments Ltd. (NIPL)], 31 non-bank PPI issuers, 10 BBPOUs, two TReDS platform providers, one ATM network provider, 34 online PAs, one PA-CB, two WLAOs and one entity facilitating instant money transfer (IMT) were carried out by the Reserve Bank. During 2024-25, the Department undertook enforcement action against three PSOs for contraventions/non-compliance of the directions issued by the Reserve Bank.

First Onsite Inspection of AMC Repo Clearing Ltd. IX.36 An onsite inspection of AMC Repo Clearing Ltd., a CCP authorised by the Reserve Bank to act as a triparty agent and for settling repo in corporate bond securities traded in recognised stock exchanges, was carried out in June 2024. Being a CCP, the entity was assessed against the PFMIs. Agenda for 2025-26 IX.37 In 2025-26, the Department will focus on the following goals:

3. DEPARTMENT OF INFORMATION TECHNOLOGY (DIT) IX.38 DIT continued its endeavour to ensure the smooth functioning of all the IT systems and applications of the Reserve Bank and leverage the latest technology to provide the best-in-class ICT infrastructure. PRAVAAH, the secure and centralised web-based portal, was made live during the year. The Reserve Bank has been selected for the Digital Transformation Award 2025 by Central Banking, London, UK for PRAVAAH and Sarthi, for transformation in the internal and external processes, reducing reliance on paper-based workflows and increasing transparency and efficiency in the Reserve Bank. Further, in order to reduce the risks associated with dependence on external vendors, and to support the ‘AatmaNirbhar Bharat’ initiative, the Department prioritised the in-house development of projects like e-Kuber 3.0 (i.e., core banking system of the Reserve Bank), alternate messaging system and alternate mechanism for digital payment systems. To ensure the security of the Reserve Bank’s IT infrastructure, best practices in cyber security and cyber hygiene were followed during the year. To maintain the heightened state of cyber security awareness and resilience across the organisation, the second series of the six-month long Cybersecurity Awareness Drive (CAD 2.0) was launched with the theme of ‘Cyber Surakshit Bharat (#SatarkNagrik)’. Agenda for 2024-25 IX.39 The Department had set out the following goals for 2024-25:

Implementation Status IX.40 Construction activity of the second greenfield data centre is progressing well. The facility has been designed and built to ensure a high level of redundancy, resilience and system availability, incorporating in-built fault tolerance. It has achieved Tier IV certification for its design, underscoring its compliance with the highest standards of reliability and performance. IX.41 IFTAS was entrusted with building the Indian Financial Sector (IFS) cloud with the objective of providing secure and cost-effective cloud-based services and ease the challenges of adopting modern technology, governance and data localisation. The work on Phase I of the IFS cloud services was initiated during the year. Simultaneously, work on beta phase of the IFS cloud, involving a few banks/financial intermediaries having Minimum Viable Product (MVP) services, has commenced to obtain customer feedback, understand the challenges, and help improve the cloud services offering. IX.42 The Reserve Bank had initiated INFINET 3.0 project through IFTAS with the objective of refreshing the existing INFINET 2.0 with transformative changes in technology, framework, automation, improved bandwidth, and overall services. The latest SD-WAN technology has been adopted in the INFINET 3.0 solution design which allows for better traffic engineering, application visibility and enhanced security. Presently, the project is at an advanced stage of implementation. IX.43 To enable cross-border payments in local currencies, the Reserve Bank has completed the development of Global SFMS Hub during the year. Using the services of this Hub, interested countries through their central bank or designated bank may directly send/receive financial messages to/from the designated bank in India. Technical discussions with countries that have expressed interest in connecting with the Hub are presently underway. IX.44 The e-Kuber 3.0 application is being developed with many business and functional modules along with an enterprise application technical platform. The development of e-Payments and e-Receipts as part of GPx was completed during the year, and the implementation of the core accounting platform is underway. Major Initiatives PRAVAAH - A Secure and Centralised Web-based Portal IX.45 As a part of the Reserve Bank’s commitment to leveraging technology for enhanced governance, PRAVAAH was successfully launched on May 28, 2024. This secure, centralised web-based portal has digitised the submission and processing of applications, requests and references from regulated entities and individuals ensuring seamless and faster delivery of services in a transparent manner. PRAVAAH was also integrated with Sarthi, the internal workflow application of the Reserve Bank, thereby, ensuring end-to-end digitisation of the entire processing lifecycle of the applications and facilitating ease of doing business for the Regulated Entities (REs). Going forward, planned enhancements in PRAVAAH would include: (a) Aadhaar based e-Sign services to authenticate uploaded documents; and (b) dedicated access to other regulators and government agencies to receive their inputs in PRAVAAH itself. Further, the Reserve Bank plans to build a unified technology platform to enhance integration, security and interoperability across the departments. ChiRAG: A Generative Conversational AI Tool IX.46 The potential of emerging technologies, particularly generative AI which can generate context-aware, human-like responses and analyse vast amounts of data, is rapidly gaining traction in the central banking landscape, offering transformative opportunities to enhance operations and decision-making processes. To this effect, the Reserve Bank has also developed its generative AI platform, Chat interface with Retrieval Augmented Generation (ChiRAG). Initially designed as a tool for information extraction and synthesis, ChiRAG has potential to evolve into a sophisticated orchestration layer, which will seamlessly coordinate with diverse types of information and data associated with the Reserve Bank’s wide array of functions. Sarthi 2.0 IX.47 During the year, the Reserve Bank undertook revamping of its Electronic Document Management System (Sarthi 2.0). Sarthi 2.0 is being implemented with a host of features such as improved User Interface (UI)/ User eXperience (UX), innovative workflow processes, mobile responsiveness, knowledge repository functionality, and integration with Microsoft Office. Making NEFT Compliant with ISO 20022 Messaging Standards IX.48 The NEFT system at the Reserve Bank has been compliant with ISO 20022 messaging standards since 2023. Over 230 member banks of the NEFT system were migrated to ISO standards using a converter solution facilitating conversion between INFINET Format Number (IFN) and ISO messages by August 2024. The member banks are now in the process of making their respective Core Banking Solutions (CBS) compliant with ISO 20022, thus, enabling direct, end-to-end transmission of ISO messages. The adoption of ISO 20022 will provide structured and granular data, end-to-end automation, effective compliance, and interoperability across domestic and foreign payment solutions. Continuous Upgradation of Information Technology (IT) and Cyber Security IX.49 Upgradation of IT and cyber security forms a part of the Reserve Bank’s ongoing efforts to navigate the ever-evolving landscape of digital threats. As part of the CAD, ‘Red Teaming’ cyber security exercise was conducted for officials managing critical IT infrastructure. To develop new approaches and technical solutions to address problems/challenges encountered while carrying out day-to-day operations in the Reserve Bank, an all-India competition ‘Cyber Codefest - Let’s Develop Together’ was conducted. While the construction of the Enterprise Computing and Cybersecurity Training Institute (ECCTI) at Bhubaneswar, which aims at fostering a safe and responsible cyber culture within the Reserve Bank, is in progress, advanced training programmes for officers of the Reserve Bank have already commenced. A high-level conference on IT, ‘Tech Connect’, organised during July 25-27, 2024, served as a forum for exploring current technological trends and gaining a comprehensive understanding of the best practices that play a key role for benefit of the stakeholders. Agenda for 2025-26 IX.50 The Department’s goals for 2025-26 are set out below:

IX.51 During 2024-25, the Reserve Bank continued with its endeavour towards enhancing the efficiency, security and accessibility of the payment systems, while further expanding the global outreach, promoting digital payments adoption and strengthening cyber resilience. The efforts towards fostering innovation, reducing operational risks and ensuring robust ICT infrastructure for the smooth functioning of its IT systems and applications were sustained. The work relating to cloud facility for the financial sector, next generation core banking (i.e., e-Kuber 3.0), registration of banks for ‘bank.in’ domain and AI governance policy framework would be initiated in 2025-26. 1 Payments Vision documents were released by the Reserve Bank in 2005, 2009, 2010, 2012, 2016, 2019 and 2022 to provide strategic direction along with implementation roadmap to drive structured development of the payments ecosystem. 2 Platform for Regulatory Application, Validation And AutHorisation. 3 Total payments, including digital payments and paper-based instruments. 4 Indian Financial System Codes. 5 Bhutan, France, Mauritius, Nepal, Singapore, Sri Lanka and the United Arab Emirates (UAE). 6 PFMIs are international standards for financial market infrastructures issued by the Committee on Payments and Market Infrastructures (CPMI) and the International Organisation of Securities Commissions (IOSCO) in April 2012. |

এই পেজটি শেয়ার করুন:

রিজার্ভ ব্যাঙ্ক অফ ইন্ডিয়া মোবাইল অ্যাপ্লিকেশন ইনস্টল করুন এবং সাম্প্রতিক সংবাদগুলিতে দ্রুত অ্যাক্সেস পান!