IST,

IST,

Report of the Committee on Capacity Building in Banks and non-Banks

Committee on Capacity Building July 23, 2014 Chairman Dr Raghuram Rajan Dear Sir, I have great pleasure in submitting the Report of the Committee on Capacity Building in Banks and Non Banks. On behalf of the members of the Committee, colleagues and on my own behalf, I convey my sincere thanks for entrusting us with this responsibility. With regards, Yours sincerely,

(G. Gopalakrishna) LETTER OF TRANSMITTAL Committee on Capacity Building July 23, 2014 Chairman Shri R Gandhi Dear Sir, I have great pleasure in submitting the Report of the Committee on Capacity Building in Banks and Non Banks. On behalf of the members of the Committee, colleagues and on my own behalf, I convey my sincere thanks for entrusting us with this responsibility. With regards, Yours sincerely, (G. Gopalakrishna)  Recommendations of the Committee on Capacity Building in Banks and Non Banks

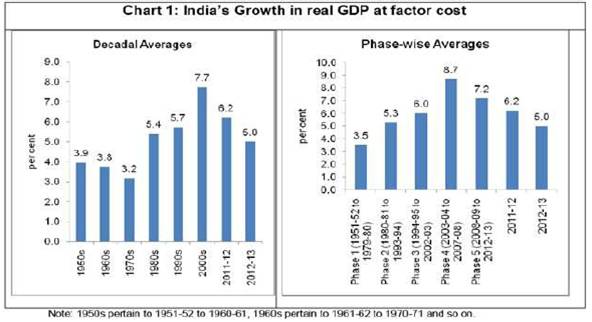

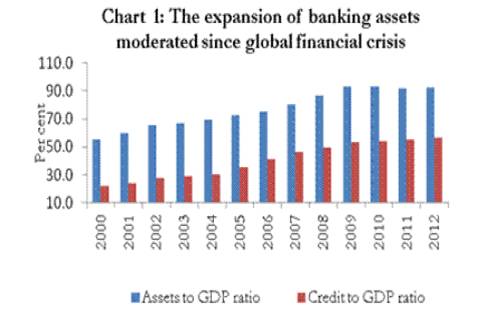

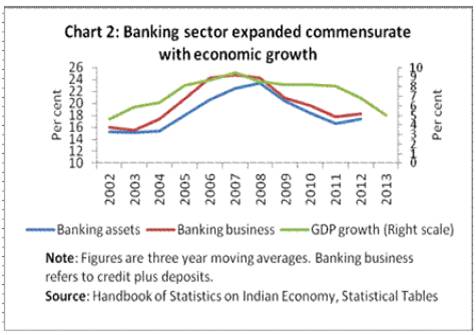

Introduction THE GENESIS The Committee on capacity building in banks and non-bank institutions in India(the Committee) was constituted with the objective of implementing non-legislative recommendations of the Financial Sector Legislative Reforms Commission (FSLRC), relating to capacity building in banks and non-banks, streamlining training intervention and suggesting changes thereto in view of ever increasing challenges in banking and non-banking sector; also on anvil were objectives of evolving an appropriate certification mechanism where feasible, examining possible incentives for undergoing such certification and covering all stages of hierarchy-from the lowest rung to the Board level executives. The recommendations of FSLRC on the legislative as also non-legislative front are legion now and focus on bringing about a paradigm shift in the arenas of financial regulation and supervision. While the legislative changes would result in amendments to various financial enactments where necessary and feasible, the Committee on capacity building derives its inspiration from the non legislative recommendations exhorting the financial sector to enhance capacities and capabilities of human resources in financial sector. The ambit of the Committee is essentially human resource intervention that would be required for improving the efficacy and efficiency of personnel employed at various levels by banks and non-banking financial companies regulated by the Reserve Bank. Scores of NBFCs regulated and supervised by RBI would essentially form part and parcel of the initiative to enhance skill building of employees serving them. Needless to add, their training requirements would be slightly variegated when compared to the employees engaged by the banking sector. This is on account of significant evolution of the training ethos in banking companies as compared to those in NBFCs. Training needs were essentially found to be certainly better oriented, more organized and definitive in banks. NBFCs (at least most of them) possibly do not imbibe such regimented training curricula as found in banks and perhaps may not have essential rigors of continuous training, entry level expertise and building upon existing capabilities which seem more evolved in banks. However, there seems to be significant focus on training initiatives in non bank institutions of late. The Committee’s interaction with McKinsey India and Manipal Global Education Services also corroborated such heightened focus on training. NBFCs seem keener to be abreast with all other financial institutions and are found to be spear-heading training intervention. It was against the aforesaid background that the committee was constituted by RBI. The Committee consisted of the following members: 1. Shri G.Gopalakrishna, Director, CAFRAL(Ex-ED, RBI) - Chairman TERMS OF REFERENCE 1. To identify capacity building requirements keeping in view the role of the financial sector and what it should deliver. The Committee’s work was steered in certain desired and desirable directions by the Chairman Shri G. Gopalakrishna, former Executive Director of RBI, who has since assumed the role of a trainer cum administrator in his existing capacity as Director of Centre for Advanced Financial Research and Learning(CAFRAL) and eminent bankers, trainers and HR specialists who have been intimately associated with the training functions in respective institutions. Keeping in view the background of various members associated with the Committee, their wide and diverse experience in putting in place practical approaches to training and skill building, it was decided that the task of the Committee could be accomplished if each member had at his disposal a definite set of objectives on which recommendations could evolve. Thus, the Committee in its very first meeting on February 20, 2014 set for itself the task of allocating the terms of reference amongst members for deliberation, discussion and crystallization of views that would ultimately come to be summed up in the form of a report and relevant recommendations of the committee. The mandate of the Committee was essentially to delineate an entire philosophy on capacity building, replete with processes associated with systematic approach to training that is codified by institutions across India and the globe. The approach thus sought to include “Training needs analysis”, “Training of Trainers”, “Codification of knowledge, content and training inputs available vastly in the banking sector and across the training universe” as well as “leveraging technology to evolve the best possible form of propagating, propagandizing and disseminating the vast reservoir of knowledge, skill, attitude and habit inputs that form the core of any training methodology that can be applied to constituents of financial sector”. The approach to the whole process can be summarized as follows:- 1. Brainstorming: Regular meetings and interaction amongst members through face to face discussions, correspondence and exchange of views through mail, 2. Engaging external experts: Co-coordinating and synergizing the views of special invitees - for instance Shri. VK Madhav Mohan, a leadership and management mentor and an ex-banker and former Director on the Board of State Bank of Travancore with diverse qualifications and skills was specifically co-opted for imbibing external inputs, which could otherwise be submerged by more or less homogeneous views of members having similar background as bankers or trainers for banks. This also enabled a counterpoint of view to emerge vis-à-vis convergent views that could stem from likeminded bankers. Also McKinsey India and Manipal Global Education Services made presentations and shared their experience with the Committee members on capacity building in financial institutions. 3. Multi-pronged analysis of training needs: Needless to add, the Committee also tapped the large reservoir of training experience accumulated by banks over a period of time and the Chairman steered the committee’s task on a 40 parameter approach to training intervention seeking to examine the present scenario in terms of age-wise, entry-wise, cadre and category wise requirement for capacity building/training. 4. Synergising diverse training needs of bank groups on one hand and banks and non-banks on the other: The Committee also had the important task of understanding the dissimilar needs of training in similarly regulated banks. Public sector, private sector and foreign banks come with their own individual and idiosyncratic approaches to training based on the organizational profile, business objectives and special focus area(s) of their operations. In addition, there was also the significant requirement of clearly identifying and recognizing the fact that NBFCs with their different business model could not be equated with banks on parameters of evolution of training philosophies, budgetary allowances, impetus on training and extent of training intervention. The Committee had this diversity in evolution of institutions as an essential challenge to reckon with while identifying precise training requirements of banks/non banks. This approach is delineated in greater detail in some of the following chapters. 5. Attitude and habits to coalesce with functional training: The Committee, during the course of discussions also had to come to terms with the fact that mere allocation of budgetary resources and making available human resources for training would not perhaps serve the issue. The essential task of honing, refining and re-orienting attitudes of employees while subjecting them to new forms of skill upgradation and preparing them for managerial or higher responsibilities was considered to be a factor that could not be ignored. Attitudinal training was thus considered to be an essential adjunct to any other field of training, be it in operations, learning of new skills or upgrading one’s own knowledge quotient. The need for preparing a prospective executive/manager or supervisor with an appropriate mental framework was considered to be as important as exposing him to new work responsibilities and challenges. 6. Board level training-handling sensitively: The Committee recognized that the aspect of training Board level executives would have to be approached a little differently, as many of them came in with expertise in certain very specialized areas and could possibly perceive any effort to train them as an affront to or an exercise at undermining their capabilities. It was felt that perhaps some form of regular and periodical interaction with such members could serve as an effective instrument for training them than subjecting them to a more rigorous regimen based on classroom sessions or skill building tests. This, primarily, became the approach to enunciating knowledge/skill/attitude interventions for them. 7. Customer protection to be the desirable end by utilizing all means: It was felt that the training focus should have a definite emphasis on front office areas which aid in creating a first impression of any financial institution in the minds of customer. The Committee completely took note of the essential backbone of FSLRC recommendations that hinged on consumer protection. 8. Mentoring: Mentoring as a means of “on the job coaching” was discussed at some length and the need for “chief learning officers” in banks and non banks came to be re-iterated at several points in time. The need for a more or less “personalized coach” for trainee executives was considered to be essential to keep the latter abreast with the right way to perform jobs, the appropriate systems that needed to be followed and for larger customer satisfaction and protection. There was an overwhelming influence on ensuring transfer of knowledge in institutions by such means. Mentoring of Board was also looked upon as inevitable in this day and age. 9. Incentives for training: Some form of direct correlation between training and incentives in career progression was also given a lot of thought, especially in view of “burn out” of young entrants within few years of serving banking/non banking sectors. 10. Technology in training: E-learning was espoused as a useful tool by all members who advocated the same for wider learning, reach and portability. The overwhelming premise behind advocacy of e-learning was the consequent reduction in training costs that institutions could achieve. 11. Collaborative training: Training jointly conducted by institutions with similar mandate for training, client profile and objectives as a means to enhance efficacy of indigenous training programmers and comparative studies on training methods adopted by international institutions was also identified as a useful tool for imparting the best to the trainee fraternity. 12. Capacity Building – Systemic Measures: Host of systemic measures were deliberated upon to ensure that capacity building initiatives are comprehensive and also sustainable over the long run. There was also agreement on the thought that training requirements in Regional Rural Banks/Urban Co-operative Banks were often overshadowed by those of larger commercial banks; the aspirations of the former were thus sought to be integrated with those of the larger commercial, banking network. With the above basic approach, the members were given the tasks of undertaking intense and focused study on various aspects to the terms of reference. The recommendations of the Committee are summarized in the Executive Summary. These also find a mention in relevant chapters at appropriate places. While the main focus of the Committee’s work is in respect to commercial banks, the recommendations would also apply equally in respect of other categories of banks as also to NBFCs. The Committee acknowledges with gratitude the support of Governor Dr. Raghuram Rajan in entrusting the Committee with the task of examining and offering recommendations on the vital issue of capacity building in banks and non-banking financial institutions. The Chairman acknowledges the cooperation extended by the members of the Committee in completing the task entrusted to it. The Committee gratefully acknowledges the immense contribution of Shri.V.K.Madhav Mohan, Management expert and Mentor for providing vital inputs and suggestions to facilitate effective capacity building. Shri.Madhav Mohan was co-opted as an external member to the Committee. The Committee wishes to acknowledge useful inputs by McKinsey and Company and Manipal Global Education Services. The Committee would also like to express its gratitude for inputs on competencies, skillsets and training interventions across various functions by IIBF and NIBM. The Committee thanks the concerned commercial banks for providing feedback on the questionnaire on capacity building. The Group wishes to gratefully acknowledge the contribution by Shri R.Kesavan, GM, DBS, Central Office in providing excellent Secretarial support to the Committee by preparing detailed agenda items and background material, preparing material for draft chapters and also taking care of all the logistics for the meetings of the Committee. The supporting role played by other team members of the Secretariat - Shri.Umesh Panaria, AGM, Shri.S.Balaji, Manager and Shri Rohan Mane, Assistant - is also acknowledged by the Committee. The Committee also places on record its deep appreciation for the dedication and efforts put in by Shri.N.Suganandh, DGM, Reserve Bank of India for providing research assistance and in compiling, refining and generating comprehensive final draft report. Contributions made by Shri Rajesh R Tiwary, AGM in compiling the responses from banks on the 40-point questionnaire and Ms V Mala, Manager and Shri Vishal Awachar, Assistant in providing logistic support for a crucial meeting involving McKinsey and Manipal Institute are also gratefully acknowledged. Chapter - I 1.1 Introduction Given the need for the Committee to examine capacity building requirements for banks and non-banks, it is imperative to set the context. There is a need to clarify about the concept of capacity and capacity development and articulate the elements/components of capacity development. These would need to be juxtaposed against the developments in the Indian economy in general and in banking sector in particular. This chapter thus sets the context to further unravel the dimensions of capacity development in subsequent chapters of the report. 1.2 Concept of Capacity and Capacity Development A broad review of the literature on capacity and capacity building reveal the following facts and facets: Capacity has been defined as “the ability of people, institutions and societies to perform functions, solve problems, and set and achieve objectives” (UNDP 2002.) Capacity development is the process whereby individuals, groups, and organizations enhance their abilities to mobilize and use resources in order to achieve their objectives on a sustainable basis. Efforts to strengthen abilities of individuals, groups, and organizations can comprise a combination of (i) human skills development; (ii) changes in organizations and networks; and (iii) changes in governance/institutional context. (ADB, 2004). Capacity building is a complex notion – it involves individual and organizational learning which builds social capital and trust, develops knowledge, skills and attitudes and when successful creates an organizational culture which enables organizations to set objectives, achieve results, solve problems and create adaptive procedures which enable it to survive in the long term. (DFID, 2007). The OECD (2001) defines human capital as the knowledge, skills, competencies and attributes embodied in individuals that facilitate the creation of personal, social and economic well-being. DFID states that In thinking about capacity building there is also a need to recognize different elements of capacity that together form a ‘capacity system’ which is made up of: • institutions and organizations with buildings and core infrastructure (such as ICT and libraries); 1.3.1 Perspectives on capacity In Concept of Capacity (2006), Morgan states that there was a range of perspectives on the concept of capacity. Some practitioners and analysts continue to see capacity mainly as a human resource issue to do with skill development and training at the individual level. This ‘capacity as training’ perspective has a long-standing history and is still a widely-held view. In development cooperation programmes, such an approach is usually combined with external interventions in the form of technical assistance and functional improvements. Many other practitioners and analysts now accept that the scope of capacity issues goes beyond the usual training and technical assistance approach. The general sense of the term from this perspective is one of the ability to deliver or implement better. The focus here is on capacity as general management problem-solving - the means - as part of an effort to improve results and performance - the ends. A more grounded operational way of assessing and managing capacity issues is to recognize that the concept of capabilities can provide a basic organizing concept which enables participants to find a useful focus. Without such an organizing concept, most ventures into this boundaryless subject soon lose traction. A few key questions in this context are the following: • What capabilities do we need to make our contribution and why? The aforesaid details elucidate that the notion of capacity building or capacity development goes beyond exclusively focusing on training or building skillsets in terms of an individual institutional context and encompass the wider dimensions of achievement of outcomes in an evolving economic environment from a systemic perspective. The end result is to bring about efficiency and effectiveness by improving the system’s ability to deliver and perform at the optimum level. 1.4 Indian Growth Story India’s economic growth story since independence is charted below. The golden period was during the period of 2003-04 to 2007-08 during which average growth of nearly 9 per cent was posted with pick-up in investment. The Indian economy grew at 9.5 per cent during the three-year period from 2005-06 to 2007-08 enabled by moderate inflation, fiscal consolidation and acceleration in savings and investment. This was the highest average growth rate achieved during any three year period in the history of independent India and it was second only to China among the major countries during that period. India’s high growth story was cut-short beginning with the global financial crisis of 2008-09 (real GDP growth dropped to 6.7 per cent). The economy rebounded strongly in 2009-10 (8.6 per cent) and 2010-11 (9.3 per cent). Coordinated fiscal and monetary policies played a significant role in the recovery of the economy and in the maintenance of financial market stability. The growth momentum has been losing steam since then, with growth rates of 6.2 per cent in 2011-12, 5.0 per cent in 2012-13 and projected to be around 5.5 per cent in the current year 2013-14.  From a cross-country perspective, India has been one of the fastest growing economies in the world. This is evidenced in the growing share of India in the world’s GDP in Purchasing Power Parity (PPP) terms since 1980. Looking at India’s growth history and our performance vis-à-vis the rest of the world, Indian economy has the potential to grow at 9 per cent and above in future. India is a young nation and her population is also young. This ‘demographic dividend’, which has helped us in the past, would definitely help in the future as well. However, in this age of technology and innovation, there is a need for highly skilled human capital to give us an edge over other nations. More funds need to be invested for setting up institutions in the areas of Research and Development. India has been lagging behind in innovation and entrepreneurship. It is ranked 89th out of the 118 nations in the Global Entrepreneurship and Development Index, 2013 (GEDI), published by GEDI, a specialized non-profit research and consulting firm. The ‘Doing Business 2013 report’, a study conducted by the International Finance Corporation of the World Bank Group ranks India at 173rd among the 185 countries surveyed on the criteria of ‘starting a business’. Our education system needs to restructure itself significantly to promote innovation and entrepreneurship. Productivity and efficiency in banking services would be the bulwark for all round economic development in India. A FICCI-Ernst and Young report in 2013, highlighted following projections about India in the year 2030: (i) India is expected to become the most populous country by 2030. India will have one of the youngest populations in the world by 2030. 1.5 Banking Sector India has a bank dominated financial sector: commercial banks account for over 60 per cent of the total assets of the financial system comprising banks, insurance companies, non-banking financial companies, cooperatives, mutual funds and other smaller financial entities. Banking expansion as reflected in the growth of total assets of banks was rapid till the intensification of the global financial crisis which affected the Indian economy through trade, finance and confidence channels. Bank assets as a percentage of gross domestic product (GDP) rose from 60 per cent in 2000-01 to 93 per cent by 2008-09, but thereafter it has plateaued. Bank credit to GDP ratio more than doubled from 24 per cent to 53 per cent during this period but has remained around that level in the following years (Chart 1). The growth of the banking sector was influenced by the performance of the economy and vice-versa, reflected in a co-movement between the growth in banking business and real GDP growth (Chart 2). Banking sector plays a very important role in the economic growth of the country. Our banking system has to ensure that it remains efficient and supports the activities of the real sector. In order to improve productivity and efficiency, banks need to be given more flexibility in operational matters, particularly in manpower practices. Attaining greater productivity and efficiency requires not just the right technology, systems and processes, but also the manpower with the right skills and attitude, demonstrating the necessary flexibility and adaptability to be able to keep pace with the changing times. 1.6 Capacity Building in banks and non banks Given the issues of growth and development and the impact of the banking sector and non-banking financial sector to the development of the real economy, the capacity building needs to be accorded priority focus to prepare for the growth trajectory and to broad base our growth. Human capital being the key factor in the service oriented world of banking, it is imperative that various strategies of capacity building are conceived and implemented to augment capacity for the present and the future. The Committee opines that the examination of any given stream of thought on capacity building would necessitate the following: (i) analyzing from an individual bank’s context the various key success factors for augmenting capacity in its employees The subsequent chapters elucidate the assessment of the Committee on these dimensions and the recommendations thereon. The comprehensive approach to the issue of capacity building would also address the requirements of implementation of any specific FSLRC related recommendations by the concerned key stakeholders like Government of India and the regulators. The Committee examined the extant practices obtaining in banks for undertaking focused training programmes, the training calendars and schedules envisaged from the larger need of ascertaining whether employees continued to receive inputs for enhancing knowledge, skills and attitude on a continuous basis. A 40-point agenda was prescribed for banks with the latter being required to address these 40 points and furnish their feedback. These related to such diverse aspects as average age of employees in banks, the training impetus, whether there was an articulation of training policies and implementation thereof, whether there were ad-hoc systems for launching training initiatives of the human resource intervention was well entrenched and spanned all cadres of employees. These are separately tabled in Annex I at the end of the report. Chapter - II 2.1 Introduction The quality of practices and processes of the Human Resources Management function impacts the success of capacity development and talent management in individual banks. The best practices in respect of various components of HR functions like recruitment, induction programme for new recruits, performance assessment, competency mapping and job placement, career progression/promotion policy and training together support and facilitate capacity building. Under the overall framework of best in class HRM framework, specific focus needs to be accorded to the training practices in banks. The premise on which the committee’s approach was based was that irrespective of background and academic credentials of any entrant to the financial sector, continuous and unabated training intervention on operational, functional and specialized areas can be of help and such endeavor alone would aid in updating, scaling up and building capacities. Hence, capacity building will require improvements in human resource management practices in general and greater impetus in particular on the training front in terms of new strategies and methodologies. Survey by McKinsey As part of Bancon 2013, McKinsey conducted survey covering 20 leading banks—public sector as well as private - accounting for about 70 per cent of the banking staff and over 70 per cent of assets in India’s banking system. In addition, approximately 10,000 employees across management levels from the participating banks were covered in their “Voice of Employee” survey. The survey observed talent gap across levels in banks. The shortfall for talent for public sector banks was driven by high average age leading to high retirements at senior management levels (Figures 1 and 3), whereas for private sector banks it was driven by high attrition rates especially at junior management levels (Figure 2). The average age of employees across levels was 41 years for public sector banks in 2012–13 (down from 46 years in 2010–11). The same for private sector banks was 33 years in 2012–13 (again down from 34 years in 2010–11). In public sector banks, more than three-fourths of the current population for levels AGM and above is expected to retire by 2020 (Figure 3). 2.2 HR Strategy 2.2.1 Enhancing Human Resources Management practices The above survey presents the challenges staring at the face of banks in general and public sector banks in particular. The Committee felt that there is a need for major improvement in human resource management practices internally in banks, with particular focus on public sector banks to improve human capital and build HR capacity and capability. It may also be mentioned in this context that among the many findings in the report released by the Senior Supervisors Group in connection with financial crisis was that firms which weathered the recent crisis better have senior management members who have expertise in a range of risks. This underscores the need to attract and develop talent across all critical functions and various levels of the organisation. Contemporary HR literature reveals that certain human resource management policies and practices do distinguish many high performing companies. These sets of practices are called high performance work systems. They promote organisational effectiveness. There is a need for HR functions in banks to imbibe such practices. In particular, in public sector banks there is a need to enhance professionalism in HR management to keep pace with the challenges in the emerging environment. Committee extensively deliberated on the key aspects of Human Resources Management framework in banks. It recommends the following for enhancing the framework in the current milieu:

2.2.2 Creation of position of “Chief Learning Officer” and concept of return on learning Given the high rate of knowledge obsolescence, all commercial banks must commit to create a culture of learning in their organizations. To drive this culture of learning on a mission mode, the Office of The Chief Learning Officer (CLO) could be considered. The concept of Return on Learning (ROL): The most popular model for training evaluation is the Kirkpatrick Model. The 4 levels of evaluation in the model are Reaction, Learning, Behaviour and Results. Till date, most global organizations have struggled to meaningfully go beyond the second level viz. Learning. A very miniscule number have experimented with Behaviour level. There is not much credible evidence on measurement of results viz ROL. Hence, detailed research needs to be undertaken in this regard. The Committee recommends the following:

2.2.3 Strategies for addressing issue of replacement/replenishment of talent in banks One of the major bottlenecks banks face is in terms of finding suitable replacement of talent that is necessitated on account of attrition, retirement etc. To tide over this issue, the Committee recommends various solutions like developing an Expert Pool internally and allowing free movement of talent within the organization for creation of a larger workforce of trained personnel. Special recruitments based on job roles and competency could also be considered. (i) Develop Expert pool internally An expert pool can be created in-house for critical/specialized roles and the pool can be trained/ certified so as to develop on the required competencies. Succession planning can be programmed from this pool. (ii) Free Movement of talent Recruitment can also be streamlined by opening new channels like Lateral recruitment where there is free movement of talent. Currently, public sector banks have a constraint in opting for middle and senior level talent from other organizations. This needs to be changed to facilitate lateral movement of talent atleast for positions where there is dire need for talent. (iii) Job Rotation It is observed that job rotation and transfers have become a matter of routine. Given the need to maintain good relationship with the customer, job rotation has to be a carefully planned exercise. Possibly, rule based job rotation and transfers are coming in the way of developing specialist officers, particularly in public sector banks.Job placement should be undertaken on the basis of employee’s education/qualifications, skill level, experience, business needs etc. The Committee feels that this issue needs to be examined by banks, particularly by public sector banks. Banks must avoid transfer for the sake of preset norms. Job rotation in banks especially, PSBs, should not be done in a mechanical manner but through a well laid down criteria. Banks should allow specialization up to say level III or IV such that the demands of contemporary banking needs are met. Transfers should focus on critical requirement like leadership across the geography and posts that require high concentration of power. In short, need based transfers may be undertaken. 2.3 Training 2.3.1 Empirical analysis and statistics: Are banks and FIs keen on training today? The regulatory requirements and economic landscape in the contemporary milieu have pushed the training needs to a higher scale. The training provided to employees would need to fit in with the requirements of the job. McKinsey survey revealed that employees seek higher training support at the beginning and during the lifetime of a new role (Figure 4). Figure 4 While each of the surveyed banks had a fully-functional in-house training centre, only 42 per cent of the total manpower on-roll attended a training program in the year 2012-13. This proportion has improved only marginally, by 6 per cent, since 2010-11. Some significant pointers based on survey conducted as part of Committee exercise (indicated in Annex I) are summarized below:-

2.3.2 Process of Skill development - Six Steps The Committee deliberated in detail on evolving a systematic approach to skill development/capacity building in banks. The Committee recommends that the process of skill development should ideally move through the following six steps: i) Identification of Business Objectives and learning objectives for the year – The task commences with prime focus on the following question- “what are the specific areas of operations in the organization which need to be developed and how to meet the skill gap?”. Before venturing into skill development plan, the important aspect that needs to be answered is whether the bank has a clear view regarding the roles currently existing in the organization and where expertise is required to be developed. ii) Sourcing of Training requirements - Once skill development requirements are derived from the business context, the next stage is to identify people matching the role and to identify their development requirements. The identification can be done through a skill mapping/assessment exercise or recommended sourcing/self-assessment. Recommended sourcing - Here, the supervisor/ talent review committee recommends a particular employee for a specific training program. Sourcing can be also done by analyzing performance reports of employees; Self-assessment - Where the employee himself offers his nomination through an online platform on perusing an option for training in a specific job environment. Once the sourcing is done, the group of employees to whom the training needs to be imparted is identified. iii) Administering Training through adoption of the 70:20:10 learning model - Different methodologies can be adopted for training people; however one of the contemporary methods adopted throughout the world is the 70/20/10 learning model. 70:20:10 learning model is a unique learning system where people are trained through experiences (70%), feedback (20%) and formal training sessions (10 %). It is said that adult learning happens maximum through experiences or on the job exercises, the balance through coaching and formal classroom training techniques. Thus, there needs to be more emphasis on job learning exercises, for example learning through projects. iv) Formulation of training schedule - How do we plan in advance, so that employees have minimum ambiguity as to what is their future learning curve - In this phase a detailed schedule containing the training objectives, the names of people for whom the training will be administered, the type of activities to support the 70:20:10 learning model are identified and charted. This list and individual letters should be published in the beginning of the year so that employees clearly know about training programs they will have an access to, during the year. v) Monitoring through tests and talent review - This stage reviews whether the training delivered as per the plan has really proven beneficial for the organization and has given a return for the employee as well as for the organization. Some ways to measure the effectiveness of training programs administered are as under: Conduct of tests (Certification) - An annual test may be held to gauge the improvement in the knowledge level of employees who had undergone training in a relevant sphere. Alternatively there can be a system where employee has to pass a certification program compulsorily to progress to the next band or grade. Talent review – The supervisor or a talent review committee may check upon whether the employee has benefitted or has shown improvement as a result of the training administered, this can be done by conducting interviews or Viva sessions. vi) Rewarding Learning - Creating a learning organization Deciding Placement/ rewards based on Score obtained - To boost learning attitude in the Bank, reward and recognition programs must also be designed around it. For example, employees who successfully pass certification programs can be provide weightage during promotion. Incentives can be designed for encouraging learning. A leadership development centre can be opened and people who continuously perform and learn can become a member of the centre. Top 100 or 200 leader’s pool can be developed through this way to be groomed as future leaders of the bank. The data which we get out of this exercise can be used in myriad number of ways. For example, employees who score good marks in the tests/assessments can be given choice placements or awards that will help them to develop themselves as domain experts in the field. 2.3.3 Training to be customized to the nature of institutions Any exercise or endeavor in capacity building is incomplete unless broad parameters on which the edifice can be built is laid out. There is undoubtedly competition amongst peer groups in banks, domestic banks have to compete with foreign banks internationally and even locally on technology and brain-drain fronts, relative conservatism in government run banks have to face up to challenges of profit oriented dynamics of private banks and then there are non-bank institutions, which have different profiles of employees with different mind sets, attitudes and functional style. Within the banking sector, one has to reckon the distinction between larger commercial banks on one hand and urban and rural banks on the other. Training needs accordingly have to be modified to suit the profile of employees in such banks and also on larger analysis based on clientele. Therefore, in the training arena, there is no concept of “one size fits all”. The only thing common is that every institution needs to imbibe a training culture that is the only “unifying” factor amongst other diverse factors affecting training needs. Customer profile in such diverse institutions is expected to be marked by diversity as well. Efforts will thus have to be geared to address these differences ably. In fact, the need perceived is even greater when we look at the clientele banks have to deal with in remote areas, villages and the not so urban centres. There would be an added imperative in such areas to be more attuned to challenges posed by customer queries, curiosity and possibly the need for guidance to customers. The modes and methodologies to coach customers and guide them in an appropriate manner can possibly be steered better through specific training modules prescribed by recognized training institutions. The Committee, therefore, recommends that recognized training institutions, apart from those run or sponsored by RBI, may organise appropriate courses for NBFCs and RRBs more particularly in customer interface areas. Further, Cooperatives have established a number of training institutions across the country. However in terms of latest courseware and training methodology there is scope for improvement. CAB, NIBM, IIBF etc may engage with co-operatives to improve the quality of training in these institutions. 2.3.4 Capacity building- Need for trainers The ideal strategy to build capacity would also have to incorporate precise training needs of employees operating at different levels, entrusted with varying responsibilities and essentially performing variegated jobs and operations. There would be a need to synergize capacity building exercises with allocable budgets, choosing the right kind of training intervention for the right work profile and also to determine which quotient of capacity building should be targeted-knowledge, skill, attitude or habit, the nature of training – internal or external and the appropriate faculty. FIBAC survey 2012 and BCG analysis indicated that the number of trainers per 1000 employees varied between various bank groups as follows: Private New-Big (14), Private New-Small (10.8), Private-Old (2.3), PSU-Large (0.8) and PSU-Medium (1.9). Further, while the majority of faculty was part-time faculty (regular employees who came in as faculty) for new private sector banks, majority of faculty in respect of public sector banks consisted of full time faculty. This mainly explained low level trainers per 1000 employees in respect of public sector banks. It would be imperative that a readily available batch of job trainers be present in organizations as it may not be possible to impart all kinds of training in external institutions or simulating all types of work circumstances and situations. In contemporary competitive times, there is also significant talent crunch in certain banks when it comes to placing people as trainers. Such placements get superseded by demands of business, operational requirements at various levels, as a result of which perhaps there would also be need to supplement the efforts of training institutions run by banks and the recognized trainers within the banks. Committee recommends that: (i) Banks should endeavour to expand enrolment of select internal employees as part-time faculty to provide for adequate internal support for training initiatives. (ii) In the event of talent crunch at middle or senior management level, banks may consider the possibility of outsourcing various training activities including management of their training institutes. 2.3.5 Perspective on Training Strategy Sample survey among various categories of banks in respect of officer cadres conducted as part of the Committee exercise (Annex I) had revealed the following: (a) For Public Sector Banks: Average per employee man hours for training reported during 2011-12 varied from 12.62 hours to 25.00 hours whereas during 2012-13 it varied from 13.85 hours to 34 hours. (b) For private sector banks: Average per employee man hours for training reported during 2011-12 varied from 13.42 hours to 27.00 hours whereas during 2012-13 it varied from 15.74 hours to 31.73 hours. One private sector bank reported 76.8 man hours during 2011-12 and 78.7 man hours during 2012-13. (c) For foreign banks: Average per employee man hours for training reported during 2011-12 varied from 22.7 hours to 45.00 hours whereas during 2012-13 it varied from 20.1 hours to 36 hours. The Committee recommends the following:

2.3.6 Coaching and mentoring paradigm Coaching and mentoring are key talent development methods. Coaching involves educating, instructing and training subordinates while mentoring means advising, counselling and guiding. Formal mentoring process needs to be introduced at higher levels. Team of potential future leaders should be mentored and groomed to enable them to take on higher responsibilities. One of the suggestions is the possible employment of retired bankers/financial professionals as tutor officers, who can guide new employees at work, monitor and correct the course of learning for them. With fresh campus recruitments happening today more frequently, an increasing proportion of valuable workforce now consists of “freshly out of the oven” recruits who would stand to benefit the most from such coaching/mentoring processes. Another perspective is that most mentoring and coaching programs work better when it is semi-formal and limited to middle to senior level employees. At junior levels it degenerates into a ritual when it is formal and leads to very little value in an highly attriting pool. The sheer numbers, logistics and bringing it together makes it an improbable intervention when it is for several hundreds of employees. In this context, blending mentoring into the classroom training works much better. Then, if it is supplemented by systems like engagement sessions with leaders wherein groups of employees spend a few hours with leaders the outcome would be much better. In this context, Committee recommends the following: While individual banks may consider putting in place coaching/mentoring processes for entry level employees if required based on their individual requirements and needs, the focus of coaching and mentoring may be mainly on middle and senior management. This could be further supplemented with system like sessions with leaders wherein groups of select employees spend a few hours with leaders/top management. 2.3.7 Mentoring programme for CMD/CEO Given the exponential rate of knowledge obsolescence in the 21st century knowledge economy, continuous learning and personal growth is mandatory for the CMD/CEO. However his position, responsibilities and overall stress level demand that the learning and personal growth program has to be crafted on a bespoke basis. The CMD/CEO’s individual needs have to be carefully assessed and understood. Only a trusted Mentor can design and oversee such a program. The CMD/CEO’s relationship with his immediate reportees is immeasurably important to the organization. The Mentor can bridge the gaps, alleviate conflict and smoothen the relationships at the very top of the organization. Further, the Mentor can facilitate the building of the relationship between the management team (including the CMD/CEO) and the Board of Directors. Considering the strategic importance of leadership at the very top, mentoring of the CMD/CEO is far more critical than mentoring of anyone else in the hierarchy. An independent, creative approach beyond the hierarchy is vital for the renewal and sustainability of the organization. CMD/CEOs need an “insider-outsider” who can provide an independent perspective and who can indicate alternative courses of action and their implications in the utmost confidence. Such an “insider-outsider” is the Mentor who is neither a member of the hierarchy nor is interested in furthering his own position and therefore is not driven by any interest other than the welfare of the organization and the CMD/CEO. The Committee recommends the following: CAFRAL can administer the mentoring program for CMD/CEOs of banks. It can create a pool of select, top notch, highly regarded Mentors who can be invited to conduct the mentoring programs for CMD/CEOs of banks. 2.3.8 Mode of providing training programmes The banking network is well spread in India. There are a large number of rural branches and a number of other RFIs. Considering that the reach of training benefits should encompass employees in various places, rural centres, remote areas etc, e-learning could be the best solution, in terms of availability, time and cost. The Committee suggested in this context that significant doses of functional training may be imparted in future through e-learning and other alternate delivery channels. Private sector and Foreign banks have already introduced e-learning based modules and certification. Fortunately, in today’s times there is no dearth of training material, media for training and a fraternity of willing trainers who comprise people who form the active workforce, the retired banking/non-banking community and field experts as also freelancers. The training environment has actively embraced technology and successfully converted the conventional class-room mode to an interactive, more communicative, one-to-one and one-to-many personalized training methods involving technology (Skype, dedicated learning portals, web enabled universities etc.). Capacity building can be immense and diverse provided the technological tools are used to the best possible extent with minimum load on resources of training and maximization of receivers of training. The Committee accordingly recommends:

2.3.9 Top Management Training There is an imperative need to understand the training requirements of top management and fulfil the same. Public Sector Banks have also been witnessing an increasing number of relatively younger officers scaling new peaks in hierarchy in short spans of time. Their needs will have to be integrated in the present and future scenario. Accordingly, in the arena of top management training, the Committee recommends that

2.4 Supervisory Focus on HR Management in banks HR management function impinges upon the governance and oversight activity of a bank. HR management practices would directly impact strategic, reputational, operational risks and indirectly impact other risk categories through ineffectiveness of controls. The Committee noted that succession planning and key HR related policies are examined in detail as part of Risk Based Supervision/Annual Financial Inspection process of RBI. In the light of the other recommendations made by the Committee in the report, the Committee recommends the following in regard to regulatory/supervisory focus on HR management function in banks:

Chapter - III 3.1 Introduction: There is a compelling need for a strong focus on human capital management given the requirement of keeping abreast with a fast evolving and dynamic economic environment and to support the needs of the real economy and its growth in a sustainable manner. There are various challenges in the context of prevailing trends in terms of scarcity of suitable talent pipeline, significant attrition and retirements and continuous demand for specialised skills in the banking industry. To address these concerns and to enable professionalism keeping in view the demands of a growing economy like India, there is a need to examine measures relating to identification of requisite qualifications and to suggest the need for obtaining certifications by the workforce in the banking industry and the non-banking industry. The Committee discussed the present state of affairs, perused the best practices in a few international jurisdictions and considered various choices before offering the recommendations in respect of the following areas of terms of reference: (i) Examine the skills required at various levels/operations to deliver on the required role, (ii) ‘Identifying qualifications relevant to specific areas of operation in banks and non-banks’; While the need for compulsory certification is also examined in this chapter, the methodologies for prescribing certification for required qualifications are addressed as part of Chapter V. While the recommendations relate particularly to banking sector, these could also be appropriately made applicable in respect of non-banking financial sector. 3.2 Key Drivers and challenges for the banking system:

All these developments will present significant challenges for the banking system and banks will need to prepare themselves to these challenges adequately in terms of human capital, technology and processes. 3.3 Areas where the financial world needs greater inputs today Some essential inputs that were furnished by members centered on the following. These then would be construed as areas which have an ever increasing scope for building capacities and applying:-

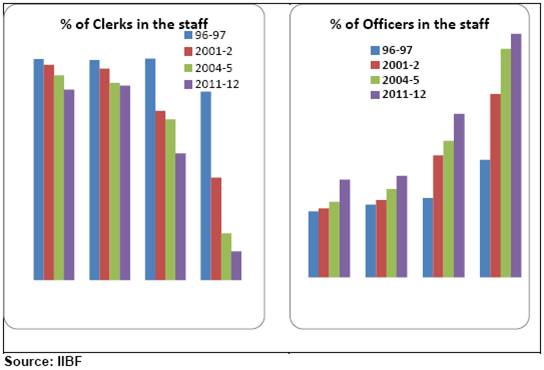

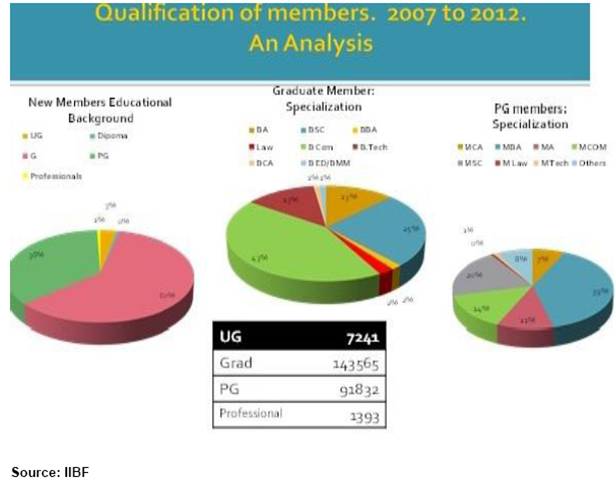

3.4 Deliberations of the Committee and Recommendations: 3.4 1 Prescribing Qualifications Prescribing requisite qualifications, enabling employees to attain certain basic and advanced levels of expertise would be the logical consequences in the effort to constantly undertake skill building of employees and upgrade them on a regular basis. Thus, the Committee examined the above perspectives to evolve appropriate methodologies in order to arrive at certain pointers to what could possibly be construed as a set of desirable qualifications. Changing dimensions in staff composition would also decide on what qualifications are required at various levels. The PSU banks and old Private Banks have clerks and officers. New Private and foreign banks are more officer oriented. The following chart (based on RBI data) gives the breakup of staff positions: Chart 1. Staff strength and distribution.  In contemporary times, a major chunk of staff in banks belongs to the Y and Mobile Generation. There is a genuine and pressing need to acquaint them and equip them in taking up leading banking roles and acquiring critical banking skills. As banks do not prescribe ‘specific subject qualification’ such as banking, commerce etc for being eligible for recruitment and as the majority of the current recruitment exam is based on IQ, the profile of entrants to this sector could be as wide and varied as the number of educational disciplines available today. Thus there would be an imminent need to synergize these variable skill sets in one direction to achieve maximization of banking process know-how, organizational goals and operational skills. A depiction of variously qualified entrants is as under:- Chart 2: Academic Qualification of new recruits  3.4.1.1 Entry Point Qualification The committee observed that there are no prescribed entry point qualifications in the banking industry. The PSU banks recruit through a common written test cum interview process managed by IBPS. Many old Private Banks also use IBPS route and also undertake campus recruitment. New Private Banks engage with some educational institutions for preparing graduates for bank jobs. These institutes identify the candidates subject to certain minimum educational qualifications and act as finishing schools for such identified candidates. Almost the entire requirement of some private sector banks is met by these institutions. In these cases, the training institutions have a structured MoU with the banks concerned that ensures that the candidates are placed with banks immediately on successfully completing the course. The committee observed that since the year 2005 the annual intake of banks is around 40,000 new employees each year. The current level of recruitment will taper down and it is reasonable to assume that the annual intake will come down in future. In this connection, the committee observed that the banking sector employs more than a million employees and the annual turnover could be anywhere around 10% (retirement plus recruitment). The PSBs’ employment program is possibly the largest recruitment drive monitored by GOI and as such stipulating an implementable minimum entry point criterion for such banks may not be feasible. Further, stipulating an entry point qualification may involve some cost to the individual concerned. The committee also observed that in the case of PSBs, the post recruitment training efforts pose a major challenge and banks are found to be outsourcing the same to many agencies. Major commercial banks have their own training systems though the same cannot be said of all such banks. Taking into account all the above views, the Committee recommends that

3.4.1.2 Qualifications for generalists and specialists It is observed that banks often differentiate between specialists and generalists. The business functions for specialists included areas such as treasury, derivatives trading, IT, Forex, Risk Management, Service Delivery Groups, Product roles, legal, etc. The generalists are deployed in branches, administrative functions, finance, some areas of treasury, taxation, branch managers, operations, relationship/sales managers etc. In public sector banks, the educational requirement is generally as per the field of specialization. In private sector banks and foreign banks, post-graduation and professional qualifications like CA/MBA/LLB etc. are preferred for certain specialist positions, depending on job requirements. In this context, the Committee recommends:

An indicative list of qualifications in respect of various positions identified by the Committee and training interventions for such positions are provided in Annex II and III respectively. 3.4.2 Skill Requirements As regards the skill sets that are needed in the banks, the Committee notes that the skill set requirements is linked to the various hierarchical levels and role functions. The Committee provides the broad indicative skill requirements as follows: First line staff: At this level there is not much of discretion with the staff about the job role. The products are standardized. The job role is predominantly one of delivery of service. The systems are well laid and the supervision machinery is well structured. Staff should be able to do the job once they are given basic information, knowledge and process skills. The knowledge and skills required by this set of people are.

Banks use many forms of outsourcing. Essentially outsourcing has customer interface and therefore there is close supervision. Employee is able to carry out the transaction on a routine manner and not much of discretion is granted. Back office does not have to innovate or customize the transaction to each customer. The banks require that products and procedures are handled as prescribed. Employees of service Providers such as Software Companies, Debt Collection agents, Business correspondents (financial inclusion), Relationship executives: Specific process knowledge, domain knowledge for marketing and Do’s and Don’ts. Good customer handling skills. Supervisory roles - Employees in this level supervise the front line, undertake trouble shooting, do business development and have certain KPIs. Some of them take up functional roles also. They need a full knowledge of the products, processes, procedures and ensure good delivery of transactions and products. The knowledge and skill requirements are:

Specialist functions - These are functions which are not part of business verticals but are critical for overall goals of the bank. Some of these can be called support functions.

It is essential to point out that the depth of functions, namely specialization will somewhat vary depending upon the volume of business/transaction, size and geographical spread of the bank. Each of the above roles needs different knowledge and distinct skill sets. Imparting of knowledge, skill and other attitudes call for different interventions. All employees need knowledge and skill for the job they do. The required level of knowledge and skill will vary depending up on the job role and business size. Whether an employee needs knowledge and standard skills (certificate) and whether he needs specialised skills (Training and Certification) and how much of the skills and expertise can be obtained on the job will depend up on (a) the position of the person in the hierarchy, (b) length of service and (c) the level of expertise needed in the job. While the above provides a broad overview, a more detailed indicative requirement of key skillsets across various banking domains in the emerging milieu is provided at Annex IV. 3.4.3 Skill gaps in commercial banks The responses to the survey conducted with cross section of banks revealed insights into some of the skill gaps faced by them. Skill gaps vary across various cadres of employees across banks. Skill gaps for frontline staff include lack of complete knowledge of products, processes and systems, at higher levels skill gaps are concentrated around motivational, leadership and team management skills. In some of the banks skill gaps existed at entry levels owing to constant churn of employees, while such gaps were prominent in the area of forex, treasury, risk management due to large scale retirements. The constraints faced by public sector banks in identifying/recruiting personnel with suitable skill sets are primarily due to inability to offer differential pay or incentive to select personnel, not resorting to campus selection, selection from common pool of candidates clearing IBPS exam etc. For private sector banks, availability of skilled talent for key business areas, attractiveness of banking sector as employer, talent retention particularly in view of increased rural push, scarcity of candidates with requisite skill sets for specialized positions are some of the challenges. The Committee recommends that banks should clearly articulate the skill gaps faced by them as an integral part of their human resource management practices, and clear cut strategy to address the gaps and tackle the challenges faced by them in this regard. 3.4.4 Mandating Certification A comparative study of profile of banking related courses offered by various universities reveals that there are certain educational institutions which offer MBA in Banking & Finance, while some other universities offer bachelor degree courses in commerce, with banking & finance as key subjects. Many bank employees also invariably acquire professional qualifications related to banking and finance from IIBF. Though the Institute’s JAIIB and CAIIB courses are well recognized by the banking industry, presently, there is no course whose completion and obtaining a mandatory certification on such completion is mandated. There are other ancillary requirements though, for instance, bankers handling demat accounts must pass the exam conducted by SEBI and NSE while those selling insurance products must pass the exams prescribed by IRDA. NISM (an institute promoted by SEBI) accredits institutes which train and certify wealth management advisors. NISM accredited qualification is compulsory for wealth managers in capital market segment. IIBF conducts training cum certification for Debt Recovery Agents, as per requirement of RBI guidelines. Similarly they also certify BC/BFs. FIMMDA, FEDAI, ICSI etc collaborate with IIBF in the certification process in treasury, forex and compliance areas respectively. IIBF’s certification for customer service is in association with BCSBI. The committee while acknowledging the benefit of certification for improved functional competency observed that it may be difficult to mandate certification in all areas of banking. Nevertheless, the Committee felt that mandating of certification in certain critical areas would be necessary to bring about a general discernible improvement in professionalism and competency in such key areas. One of the prime focus areas of FSLRC report is the aspect of consumer protection in general and on retail consumer protection in particular. In this context, it has become imperative that the persons entrusted with selling function in banks who interface with customers clearly appreciate the regulatory/statutory requirements, possess required product knowledge and are capable of advising adequately. Accordingly, the Committee recommends the following:

3.4.5 Continuing professional education requirements for enhancing knowledge and skills The Committee noted that there was no specific mandated requirement for continuous professional education for employees in banks and non bank institutions. Certain banks encouraged adoption of E-learning and various other certification programmes by way of incentives and reimbursement of course fee for continuous professional development of workforce, while some others were providing structured training programmes at regular intervals. One of the banks had also indicated that certification emanating from JAIIB/CAIIB, KYC/AML programmes of IIBF, other similar certified courses from NISM/AMFI/IRDA etc., is deemed essential before absorbing employees in certain critical areas. One bank also reported that they conducted tests for employees on areas related to banking awareness every year. In one of the foreign banks there were prescribed benchmarks for completion of training. In another foreign bank, 5 days of training per individual were targeted which varied per business profile of employees, while relationship managers were required to be certified on products and skills. The Committee recommends that at least for those areas where mandatory certification was recommended by the Committee, the validity of certificate and its continuation would have to be made contingent upon completion of certain number of learning hours through various modes like attending training/seminars/conferences, certifications, e-learning etc., which would aid and abet continued learning. The requirement of continuous education in respect of various job functions/profiles could be developed accordingly. The CPE in respect of certification awarded by various national/international professional bodies like ICAI, CFA Institute, GARP, ISACA, IIA etc. can be given due recognition as part of the framework. 3.4.6 FSLRC recommendations – Imperatives for skill-building The Financial Stability and Development Council (FSDC) in its meeting in October, 2013, identified and agreed to voluntarily implement the twelve non-legislative recommendations of FSLRC relating to regulatory governance, transparency and improved operational efficiency in the Indian financial sector. These 12 steps/measures to implement FSLRC by the financial sector regulators relates to (1)Customer protection in general (2) Customer Protection for retail customers (3) Framing regulations(4) Notices for violation of regulations (5) Transparency in providing regulatory information (6) Transparency in Board meetings (7) Reporting – publishing information about the activities of an organization measured against its objectives(8) Approvals – moving towards a 90 days approval period for all permissions/ licenses to do business, launching new products and services (9) Investigation for violation of regulation- should be time bound and investigating persons should be separate from those determining violation or imposing penalty (10) Adjudication (11) Imposition of Penalty; and (12) Capacity Building. The requirements specifically related to capacity building, as indicated in the Handbook released by MoF, GoI, included:(i) internal capacity building within MoF and DEA (ii) DEA to design and initiate training and certification programs for staff of regulators, in order to bring them up to date on recent developments in financial regulatory governance, and common principles necessary to harmonise financial sector regulation. (iii) workshop and conferences for senior staff of financial agencies to be organized by DEA (iv) All financial agencies need to issue regulations which require 15 per cent of all existing staff of all financial firms to pass the certification test every year. This would ensure that within a horizon of three years, a large swathe of individuals within financial firms would also possess adequate knowledge about the policy and legal environment. As regards point (iv), the recommendations relating to mandatory certifications, need for continuing education requirements have also been provided earlier in the chapter. In the context of implementation of FSLRC non legislative recommendations, the Committee recommends that any regulations/guidelines arising therefrom need to be factored in for testing as part of certifications. Further, certification for relevant personnel in compliance, legal and policy/planning functions should incorporate curriculum relating to current policy and legal environment. Chapter - IV 4.1 Introduction Post financial crisis, the ability of Boards of banks to adequately guide and oversee their institutions have been called into question several times across the global financial world. Concerns have been raised on whether Boards with their wide ranging representations from different segments of financial streams have actually risen to the occasion in stemming the rot that pervaded the financial world post crisis. There have been indications to the effect that many such Board Members actually happened to be passive spectators in good and bad times. There have been queries on their credibility, competencies and ability to steer the course of the institutions in desirable directions. In the wake of the economic crisis, directors are expected to have an enhanced understanding of the business of banking and the legal/regulatory imperatives underpinning the banking business. 4.2 Deliberations of the Committee and Recommendations 4.2.1 Examination of compulsory certification 4.2.1.1 Looking back at the mistakes and bank failures of the past few years, many boards regret that they did not clearly understand the risks their management team assumed. While the directors are not involved in the day-to-day management of the bank, they are involved in the strategic planning of the bank. In the rapidly changing economic and regulatory environment, bank boards have come under constant scrutiny of the regulator, shareholders, government bodies, rating agencies and media. Needless to add, the involvement of the board is likely to increase with the implementation of new regulations and requirements. It will become increasingly challenging to profitably undertake banking operations in a safe and sound manner in future. This will require directors to possess knowledge and skills to perform their duties and help their banks stay competitive, be abreast of all developments on the banking front and help organization grow. In fact, they could possibly use their knowledge and experience gained from their own profession in their role as a director. The directors may already possess various attributes such as basic management experience and skills, ability to discern from modern banking developments and a willingness to participate actively in matters relating to the respective bank’s functioning despite lack of time. Their competencies are put to test invariably when they are required to contribute to i) framing of internal policies and guidelines that provide controls and limits on the various risks a bank is/may be exposed to; ii) monitoring of risks through periodic control reports, to ensure they remain within acceptable ranges; iii) oversee bank management to ensure it operates in the best interest of the various stakeholders and iv) an active compliance process by ensuring that the bank is in tune with various rules and regulations prescribed by the regulators from time to time. There was an overwhelming agreement on the fact that members on Bank Boards are invariably endowed with specific and also expert skills in banking matters and especially in certain fields where they have achieved expertise and excellence. It is this professional achievement in the respective sphere that is responsible for their induction on various Boards. The point that had to be debated intensely was whether such skills and knowledge could be assumed as “given and existing” or would there be requirements of upgradation of the same though some process of training and certification. 4.2.2.2 The Committee discussed extensively the issue of whether certification of the members on bank Boards should be made mandatory for every individual before appointment to the Board of the bank. In terms of the Banking Regulation Act, 1949, not less than fifty-one per cent, of the total number of members of the Board of Directors of a banking company are required to have special knowledge or practical experience in accountancy, agriculture and rural economy, banking, co-operation, economics, finance, law, small-scale industry or any other matter the special knowledge of, and practical experience in, which would, in the opinion of the Reserve Bank, would be useful to the banking company. Thus, in the absence of any requirement for a specific educational qualification for nomination as a Director, the issue required elaborate discussion. While some of the members were strongly of the view that compulsory certification before appointment will help in bridging the knowledge gaps, certain other views were not in favour of such a proposal, primarily considering limited pool of suitable executives willing to take up the position of a Director in a bank. Also internationally, no major country has the requirement for compulsory certification of such a prescription of compulsory certification of individuals before their appointment as a Director of the Board. 4.2.2.3 Further, considering the aspect of such Directors coming in with accomplished levels of performance in their own respective fields and the exalted status they are bestowed with on becoming a Board member, it was also surmised that such Directors may have reservations on being treated as relative novices. It has to be borne in mind that their appointment to Boards is based on certain credentials for which they are known, like exemplary legal skills, years of experience in co-operative management, steering leading industries to growth etc. As such, it was felt that the aspect of training intervention needs to be approached sensitively. None can deny the basic benefits of training on banking subjects to bankers including Board members, but as has been repeatedly stressed across various chapters in this report, it is attitude coupled with aptitude that can ensure receptivity to training inputs. Perceived reluctance to get trained by Board members counted as top management may actually prove to be detrimental to any effort or attempt to put them through training schedules. Nevertheless, it was agreed that this alone could not be the reason to dissuade banks from training their new inductees on Boards or constantly upgrade their skills in banking. It was felt that an alternative medium of regular interactions amongst top management of banks within the organization coupled with interactions with banking regulators/supervisors, special seminars on topics of banking relevance and conferences as are organized by RBI for their own Directors on the Board of various banks could be an effective alternative. This would nullify the opposition or reluctance to the regimented rigor of a training programme, while simultaneously allowing free-wheeling interactions amongst Board members of various banks, when they assemble for a common cause. The advantages in getting a firsthand view from regulators etc during conferences of Directors would further pave the way for transmission and transfer of bank related know-how. The Committee, therefore, recommends that compulsory certification of individuals before their appointment as a Director of the Board may not be considered as of now. However, as prescribed by the Reserve Bank under extant regulations on corporate governance, some form of training intervention albeit under a different nomenclature could be considered. These training inputs could be administered by various organizations including RBI, the banks concerned themselves, specialised training on areas like treasury management, foreign exchange etc by such institutions as NIBM, IIBF, CAFRAL etc. Banks could also consider deputing them to institutions in India and abroad for embellishing their banking skills. 4.2.3 Induction Process for Board members 4.2.3.1 In the absence of prescribed qualification / certification, the Committee studied the existing training imparted to the Directors across the banking system and the adequacy thereof. It observed that presently most banks do not have an internal training programme for training new inductees on the Board, however, the new inductees are deputed for training with external agencies like IDRBT, IPE, ASCI, CAFRAL, Thomson Reuters Academy etc. In some of the banks, new inductees on the Board are imparted an overview of the organizational structure, businesses of the Bank and its subsidiaries, financial performance of the Bank and the Group, pre-joining regulatory requirements and compliances to be done, Board composition etc. The inductees are given copies of presentations which include such overview as well as the Annual Reports of the Bank. This, of course, is complemented by the “on the job” quotient that comes while the Board member participates in various proceedings where top management is involved. 4.2.3.2 In some banks it was observed that though there was no structured design for imparting induction training to new board members, the systems put in place by banks ensured that long term strategic directions, business plans, process of decision making and other key management processes are provided to the new inductees by the Whole Time Directors of the Bank/ Board. Additionally, they are provided an understanding of the organizational structure, businesses and related strategies, governance policies and procedures which is also accompanied by a one-to-one presentation from key Departments/ Business Heads on focussed areas of work and projects. It is the primary duty of the director to represent what he or she believes to be the true long-term interest of the bank. Where those interests are not being considered by fellow directors, it is up to the individual to challenge such a decision. While doing so, the director needs to take a balanced view and should be prepared and be able to confront others on the board including the Managing Director/CEO. The ability to intervene, when and how to intervene would be based on strategic judgement skills that the Director already bring in, in the wake of his exemplary credentials in his own sphere and the “what why and how” would depend upon the banking awareness modules that banks put in place for such new inductees. It was definitely felt that the responsibility of banks training their own Directors both on and off the job was immense and needed to be under-scored and underlined and where necessary possibly to be re-iterated as well. Considering the extent of responsibility cast on the Directors, the Committee is of the opinion that the skills of the Directors would need constant and substantial upgradation. As a starting point, the Committee feels that a good induction process will go a long way in welcoming a newly appointed director and impressing upon him or her expectations of the bank as also the regulator. Committee therefore recommends a formal and systematic induction process which should inter-alia be able to sensitize the new inductees in the following areas:

4.2.4 Training intervention for Board members 4.2.4.1 Apart from the above induction process, the knowledge level of the directors needs to be further developed and enhanced by providing regular training in the following areas: