IST,

IST,

Report of the Expert Committee on Resolution Framework for Covid-19 related Stress

The Expert Committee would like to gratefully acknowledge the valuable contributions from various stakeholders in compilation of this Report. The Committee would like to thank the representatives of Rating Agencies for their suggestions and perspectives on the subject. The Expert Committee places on record its deep appreciation for the valuable inputs it received from the representatives of various Industry Associations. The Expert Committee would like to place on record its commendation to Dr. P K Agrawal, Senior Advisor, IBA who participated in all the meetings of the Committee and contributed in the deliberations. The Committee also conveys its appreciation for the excellent support provided by the Committee’s Secretariat at Indian Banks’ Association and in responding to the complex information and analytical requirements and efficiently coordinating the meetings, besides contributing to the compilation of the Report. This greatly facilitated the work of the Committee. List of Abbreviations used in the Report

The Reserve Bank of India as part of its Statement on Developmental and Regulatory Policies released along with the Monetary Policy Statement on August 6, 2020, a ‘Resolution Framework for Covid-19 related Stress’, vide circular RBI/2020-21/16 DOR.No.BP.BC/3/21. 04.048/2020-21 dated August 6, 2020 as a special window under the Prudential Framework on Resolution of Stressed Assets issued on June 7, 2019. The Committee recommendations are not applicable for accounts covered by Part A of the Annex to the above circular i.e., personal loans and the borrowers not covered by the circular, as listed in Paragraph 2 of the annex to the said circular. The framework enables lending institutions including NBFCs, which are an essential part of the lenders’ pool under this Framework, to implement a Resolution Plan (RP) in respect of eligible corporate exposure even without change in ownership while classifying such exposure as Standard, subject to specified conditions. The Resolution Framework inter alia envisages constitution of an Expert Committee (Committee) under the Chairmanship of Shri K V Kamath with following composition:

2. Terms of Reference of the Expert Committee i) To identify suitable financial parameters that should be factored into the assumptions underlying RP finalised by the lending institutions under the Resolution Framework. The parameters shall cover aspects related to leverage, liquidity, debt serviceability, etc. ii) To recommend sector-specific ranges for such financial parameters that will serve as boundary conditions for the RP. iii) To make any other recommendations relating to financial or non-financial conditions to be considered for the RP, within the contours of the framework announced by the Reserve Bank of India. iv) To undertake the process validations of RP submitted in respect of borrowers where the aggregate exposure of the lending institutions at the time of invocation of the resolution process is Rs. 1500 crore and above. The process validation shall entail verification of the RP in terms of their adherence to the conditions prescribed in the Resolution, without interfering with the commercial judgement exercised by the lenders. The Committee’s term will be until June 30, 2021. IBA shall function as the Secretariat to the Committee. The Committee shall submit report within 30 days to RBI in terms of i, ii and iii above. 3. Key Highlights of Resolution Framework dated August 6, 2020 Eligibility:

Invocation Date and implementation:

Signing of ICA and provision requirements:

General Guidelines:

Conversion of Loans into Securities and Valuation:

Post Implementation Performance:

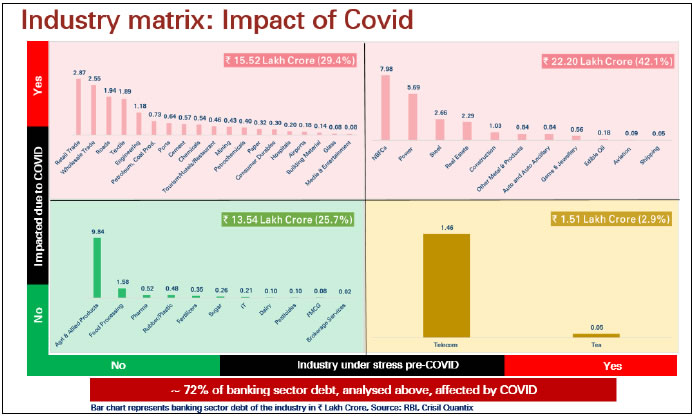

Chapter II 1. The first and foremost task before the Committee was to identify the sectors where the impact of Covid-19 was visible. 2. To have a better understanding of the above objective, the Expert Committee held several meetings with various stakeholders through the digital platform (details of the meetings are given in Annexure I). The Committee also studied the RBI’s Financial Stability Report and other Publications and Research Reports. It also studied comparison of Q1 FY 2021 with Q1FY 2020 financials of companies across many sectors, which clearly indicated stress in several sectors as summarized below:  3. The Committee recognizes that:

4. Based on past experience, it takes a few months to finalize a large restructuring proposal because of the host of compliances, as under:

5. As per RBI’s August 6, 2020 circular, all the norms applicable to implementation of a RP, including mandatory requirements of ICA and specific implementation conditions, as laid out in June 7, 2019, circular are applicable to all lending institutions for the RP implemented under this circular (Item No. 6, Page 2). 6. Time is of essence at the present juncture. Considering the large volume and the fact that only Standard assets are eligible under the proposed scheme, a segmented approach of bucketing these accounts under mild, moderate and severe stress, may ensure quick turnaround. To complete this task simplified restructuring for mild and moderate stress may be prescribed. Severe stress cases would require comprehensive restructuring. 7. The task before the Committee was to select the set of financial parameters where the threshold has to be recommended for each identified sector. The financial parameters inter alia should include aspects related to leverage, liquidity, debt serviceability etc. 8. On the evaluation and analysis, the following parameters were selected based on their relevance while considering the RP:

Definitions of Key Ratios

8. These ratios would provide the requisite assessment framework for the RP. 9. The Committee decided to source sector specific reports / company data from various sources to have a better sectoral outlook and to obtain industry benchmarks to formulate the financial parameters in a rational manner. 10. Based on the outstanding and the severity impact, the Committee selected the following sectors for the purpose of recommending financial parameters to be factored in the RP:

The Committee deliberated on the financial parameters applicable to the above 26 sectors, which are discussed in Chapter III. Chapter III 1. The following table gives the summary of sector specific threshold parameters recommended by the Committee. These parameters were selected by the Committee based on its discussions with the Rating Agencies and lending institutions. For this purpose, sector reports were obtained from rating agencies and lending institutions as also experience of the banking sector in their own credit appraisal and polices. Certain outliers found by the Committee are explained later. 2. The sector specific parameters may be considered as guidance for preparation of RP for a borrower in the specified sector. The RP may be prepared based on the pre-Covid-19 operating and financial performance of the borrower and impact of Covid-19 on its operating and financial performance in Q1 and Q2FY21, to assess the cash-flows for FY21 / FY22 and subsequent years. In these financial projections, the threshold TOL/Adjusted TNW and Debt/ EBIDTA ratios should be met by FY23. The other three threshold ratios should be met for each year of the projections starting from FY22. The base case financial projections need to be prepared as part of RP. 3. In respect of those sectors where the threshold parameters have not been specified by the Committee, lenders can make their own internal assessments for the solvency ratios i.e. TOL/Adj TNW and Total Debt/EBIDTA. However, the current ratio and DSCR shall be 1.0 and above, and ADSCR shall be 1.2 and above. 4. The Committee has uniformly proposed thresholds for current ratio, DSCR and ADSCR as in the table below in most of the sectors (exceptions flagged in the table). The borrowers eligible under the current Framework are Standard Accounts and as such, they may require some time to restore their position to pre-Covid-19 levels.

*Automobile Manufacturing: We are not prescribing any threshold for Current Ratio due to the “just in time inventory” business model for raw materials and parts, and finished goods inventory is funded by channel financing available from the dealers. **Aviation: 1. Targeted Current Ratio for Airline Industry is kept at 0.40 and above because of following key reasons:

2. DSCR is not ascertainable for airline industry since most of the airline companies work on refinancing of debt as a financing strategy. As a consequence, Avg. DSCR is not ascertainable for airline industry. ***Real Estate: Considering the typical nature of Real Estate projects, the parameters to be considered at project level rather than at entity level. ****Roads: In the roads sector, the financing is cash flow based and at SPV level where the level of debt is decided at the time of initial project appraisal. It may also be noted that the working capital cycle in this sector is negative. Accordingly, ratios like TOL / ATNW, Debt/EBITDA and Current ratio may not be relevant at the time of restructuring in this sector. Since cash flows of several projects are by way of annuity payments, the threshold ADSCR has been kept at 1.10. *****Trading - Wholesale: DSCR/ Avg. DSCR is not ascertainable for trading business as most of the companies do not use long term debt for funding their operations and are unlisted. Details of the Meetings held by the Expert Committee

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

রিজার্ভ ব্যাঙ্ক অফ ইন্ডিয়া মোবাইল অ্যাপ্লিকেশন ইনস্টল করুন এবং সাম্প্রতিক সংবাদগুলিতে দ্রুত অ্যাক্সেস পান!

আমাদের অ্যাপটি ইনস্টল করতে QR কোডটি স্ক্যান করুন

পেজের শেষ আপডেট করা তারিখ: