FAQ Page 1 - আরবিআই - Reserve Bank of India

Content Type:

FAQs on Master Directions on Priority Sector Lending Guidelines

J. PSLCs

Clarification: PSLCs may be construed in the nature of 'goods' in the course of inter-state trade or commerce, dealing in which has been notified as a permissible activity under section 6(1)(o) of BR Act vide Government of India Notification dated May 4, 2016. GST on PSLCs for the period July 01, 2017 to May 28, 2018 has to be paid by the seller bank on forward charge basis at the rate of 12%. With effect from May 28, 2018, GST has to be paid by the buyer bank under Reverse Charge Mechanism (RCM) at the rate of 18%. Further, IGST is payable on the supply of PSLC traded over e-kuber portal. If a bank which was liable to pay GST had already paid CGST/SGST or CGST/UGST, the bank is not required to pay IGST towards such supply. Further, as per the extant guidelines, no transaction charge/ fees is applicable on the participating banks payable to RBI for usage of the PSLC module on e-Kuber portal.

(The clarification given above is not a legal advice or opinion in the matter and it may not necessarily reflect the most current legal developments. The market participants should seek the advice of the tax experts/consultants/specialists before acting upon any of the information provided above).

Clarification: There are only four eligible categories of PSLCs i.e. PSLC General, PSLC Small and Marginal Farmer, PSLC Agriculture & PSLC Micro Enterprises.

Clarification: 'Export Credit' can form a part of underlying assets against the PSLC - General. However, any bank issuing PSLC-General against 'Export Credit' shall ensure that the underlying 'Export Credit' portfolio is also eligible for priority sector classification by domestic banks.

Clarification: Foreign banks with less than 20 branches are not allowed to buy PSLC General for achieving their 8% target of lending to sectors other than exports. However, such banks are allowed to buy PSLC Agriculture, PSLC Micro Enterprises and PSLC Small and Marginal Farmer for the same.

Clarification: The trade summary of PSLC market is available to the participants through the e-Kuber portal. Any new functionality will be notified to the participants via 'News & Announcements' section under e-Kuber portal.

Clarification: A bank can purchase PSLCs as per its requirements. Further, a bank is permitted to issue PSLCs upto 50 percent of previous year’s PSL achievement without having the underlying in its books. This is applicable category-wise. The net position of PSLCs (PSLC Buy – PSLC Sell) has to be considered while reporting the quarterly and annual priority sector returns. However, with regard to ascertaining the underlying assets, as on March 31st, the bank must have met the priority sector target by way of the sum of outstanding priority sector portfolio and net of PSLCs issued and purchased.

Clarification: The misclassifications, if any, will have to be reduced from the achievement of PSLC seller bank only. There will be no counterparty risk for the PSLC buyer, even if, the underlying asset of the traded PSLC gets misclassified.

Clarification: The premium will be completely market determined. No floor/ ceiling has been prescribed by RBI in this regard.

Clarification: There will be real time settlement of the matched premium and accordingly respective current accounts of the participating banks with RBI will be debited/ credited to the extent of matched premium

Clarification: The order matching will be done on anonymous basis through the portal and the buyer/ seller cannot select the counterparty. Partial matching will happen depending on the matching of premium and availability of category wise PSLC lots for sale and purchase.

Clarification: The normal trading hours shall be from 10 AM to 4:30 PM. The PSLC market operates on all days except Saturdays, Sundays, holidays declared under The Negotiable Instruments Act, 1881 by the Government of Maharashtra. and such holidays as RBI may declare from time to time.

Clarification: The nature of PSLC trading has been kept anonymous to maintain most efficient price discovery. There is no provision for settling deals on bilateral basis and reporting on the portal subsequently. RBI has the discretion to cancel any deals which is settled at substantially higher/ lower premiums as compared to the prevailing rates on the portal.

External Commercial Borrowings (ECB) and Trade Credits

D. RECOGNISED LENDERS/ INVESTORS

Retail Direct Scheme

Account opening related queries

Biennial survey on Foreign Collaboration in Indian Industry (FCS)

Details of survey launch

Ans.: In case the reporting entity does not receive the soft-form of the survey schedule, they may download the same from RBI website www.rbi.org.in---> ‘Regulatory Reporting’-→ ‘List of Returns’-→ ‘FCS – Survey Schedule’ or Forms→Survey or send a request to the email: fcsquery@rbi.org.in.

Targeted Long Term Repo Operations (TLTROs)

FAQs pertaining to TLTRO 2.0

Ans: In order to provide banks flexibility in investment, this condition will not be applicable for funds availed under TLTRO 2.0.

Housing Loans

Ensure that the documents being provided to you are not colour photocopies. Check the internet for other modus operandi to fraud and ensure clear title to the asset. Seek advice only from authentic sources such as your bank.

Get the no encumbrance certificate to find the true title holder and if it is mortgaged to any financier. Obtain all tax papers to ensure that all documents are up to date.

Indian Currency

B) Banknotes

Not necessarily. In terms of Section 24 of the Reserve Bank of India Act, 1934, bank notes shall be of the denominational values of two rupees, five rupees, ten rupees, twenty rupees, fifty rupees, one hundred rupees, five hundred rupees, one thousand rupees, five thousand rupees and ten thousand rupees or of such other denominational values, not exceeding ten thousand rupees, as the Central Government may, on the recommendation of the Central Board, specify in this behalf.

Government Securities Market in India – A Primer

11.1 For every transaction entered into by the trading desk, a deal slip should be generated which should contain data relating to nature of the deal, name of the counter-party, whether it is a direct deal or through a broker (if it is through a broker, name of the broker), details of security, amount, price, contract date and time and settlement date. The deal slips should be serially numbered and verified separately to ensure that each deal slip has been properly accounted for. Once the deal is concluded, the deal slip should be immediately passed on to the back office (it should be separate and distinct from the front office) for recording and processing. For each deal, there must be a system of issue of confirmation to the counter-party. The timely receipt of requisite written confirmation from the counter-party, which must include all essential details of the contract, should be monitored by the back office. The need for counterparty confirmation of deals matched on NDS-OM will not arise, as NDS-OM is an anonymous automated order matching system. In case of trades finalized in the OTC market and reported on NDS-OM reported segment, both the buying and selling counter parties report the trade particulars separately on the reporting platform which should match for the trade to be settled.

11.2 Once a deal has been concluded through a broker, there should not be any substitution of the counterparty by the broker. Similarly, the security sold / purchased in a deal should not be substituted by another security under any circumstances.

11.3 On the basis of vouchers passed by the back office (which should be done after verification of actual contract notes received from the broker / counter party and confirmation of the deal by the counter party), the books of account should be independently prepared.

All you wanted to know about NBFCs

B. Entities Regulated by RBI and applicable regulations

Foreign Investment in India

Answer: Please refer to the ‘Standard Operating Procedure (SOP) for Processing FDI Proposals’ issued by Department of Industrial Policy & Promotion, Government of India → http://fifp.gov.in/Forms/SOP.pdf

Domestic Deposits

I. Domestic Deposits

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Eligible entities and requirements to submit the FLA return

Ans: If an entity has not ‘received any fresh FDI and/or ODI (overseas direct investment)’ in the latest FY but has outstanding FDI and/or ODI as at end-March of that financial year, then it is required to submit their outstanding position as on March 31 in the FLA return every year by July 15.

Remittances (Money Transfer Service Scheme (MTSS) and Rupee Drawing Arrangement (RDA))

Money Transfer Service Scheme (MTSS)

Core Investment Companies

Core Investment Companies (CICs)

Ans: No, only investments in companies registered under Section 3 of the Companies Act 1956 would be regarded as investments in Group companies for the purpose of calculating 90% investment in Group companies. Moreover, CICs are prohibited from contributing capital to any partnership firm or to be partners in partnership firms including Limited Liability Partnerships (LLPs) or any association of person similar in nature to partnership firms.

FAQs on Non-Banking Financial Companies

Exemptions to the companies not accepting public deposits

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

Paytm Payments Bank Wallet

Coordinated Portfolio Investment Survey – India

What to report under CPIS?

Ans: The survey collects details of portfolio investment assets of domestic residents made in securities issued by unrelated non-residents i.e., securities issued by unrelated non-residents and owned by residents.

FAQs on Master Directions on Priority Sector Lending Guidelines

K. On-lending under Priority Sector

Clarification: In the case of bank’s lending to NBFCs / MFIs / HFCs for on-lending, only that portion of the portfolio should be reckoned for PSL classification that has been disbursed by the NBFC / MFI / HFC to the ultimate borrower/s as on the reporting date. The reckoning of residual portfolio, if any, can be done on subsequent reporting dates, based on the disbursement of eligible loans and reported by the NBFC / MFI / HFC to the bank.

Clarification: The Master Directions on Priority Sector Lending, 2020 under para 21, 22, 23 allows banks to classify as PSL its lending to NBFCs including HFCs and NBFC-MFIs and other MFIs (Societies, Trusts etc.) which are members of RBI recognised SRO for the sector for on-lending to eligible priority sectors. Banks may adopt a uniform methodology for on-lending as follows:

a) Classification under PSL:

• The banks can classify on-lending to NBFC in the respective categories of PSL. The classification will be allowed only when the NBFC has disbursed the Priority Sector Loans to the ultimate beneficiary after receiving the funds from the bank.

• The NBFCs must provide a CA certificate to the banks stating that the individual loans of the portfolio, against which on-lending benefit is being claimed, are not being used to claim benefit from any other bank(s). Also, NBFC must put in place a suitable process to flag such loan(s) in their systems to enable its internal/statutory auditors as well as RBI supervisors to verify the same.

b) Information sharing:

• The banks may devise internal control mechanisms to ensure that the portfolio under on-lending is PSL compliant and adheres to co-terminus clause. The same should be made available to RBI supervisor/s as and when required. The following information/record should be collected by the bank from the EI:

-

Name of the beneficiary, Amount sanctioned, Loan amount outstanding, Loan tenure, disbursement date, category of PSL.

-

A statement to the effect that the portfolio is PSL compliant must be certified by a CA and shared by the EI with the bank on a quarterly basis in line with the PSL reporting by the bank to RBI. With respect to adherence to the co-terminus clause, the bank should ensure the same as on March 31 each year.

c) Adherence to co-terminus condition:

• The banks availing benefit of on-lending for PS assets must adhere to the condition that the tenure of the loan under on-lending to an EI is broadly co-terminus with the tenure of PS assets created by the EI.

• In view of the operational difficulties of exactly matching the co-terminus duration, the banks are allowed a variance of 3 months from the portfolio duration. An illustration for calculating adherence to the co-terminus duration is given below:

| Sr. No. | Loan outstanding (A) | 31st March of current FY (B) | Loan end date (C) | Loan period (days) (D= C-B) | Weighted average loan outstanding days (E=A*D) |

| 1 | 50000 | 31-03-21 | 01-02-23 | 672 | 33600000 |

| 2 | 80000 | 31-03-21 | 01-05-24 | 1127 | 90160000 |

| 3 | 100000 | 31-03-21 | 11-08-23 | 863 | 86300000 |

| 4 | 300000 | 31-03-21 | 16-10-22 | 564 | 169200000 |

| 5 | 400000 | 31-03-21 | 23-11-22 | 602 | 240800000 |

| Total | 930000 | 620060000 | |||

| Weighted maturity of portfolio in days (F=(sum of E)/(sum of A) | 666.73 | ||||

| In months (F/30) | 22.22 | ||||

| In years (F/365) | 1.83 | ||||

In the above illustration, the residual maturity of bank loan to NBFC should be around 22.22 months. Banks are expected to calculate the weighted average residual maturity of portfolio ever year as on March 31 and ensure that residual maturity of bank loan to NBFC matches with the weighted average residual maturity of on-lending portfolio within the tolerance limit of +-3 months.

d) Treatment of pre-payment, foreclosure loans:

-

The PS assets created by the entity may undergo pre-payment or foreclosure thereby changing the ‘weighted maturity’ of the portfolio.

-

As the banks are required to calculate ‘weighted maturity’ at the end of FY, the loan outstanding in the event of pre-payment/foreclosure will also change accordingly.

-

The NBFC may add PS assets to the on-lending portfolio. However, it must meet conditions mentioned above such as disbursements for the PS asset by the eligible entity must be on/after receipt of funds from the bank. The addition of PS assets to the portfolio pool can also be done in case of pre-payment/foreclosure of other PS assets in the pool to ensure adherence to the co-terminus clause.

Clarification: Bank lending to NBFCs (other than MFIs) and HFCs are subjected to a cap of 5% of average PSL achievement of the four quarters of the previous financial year. In case of a new bank the cap shall be applicable on an on-going basis during its first year of operations. The prescribed cap is not applicable for bank lending to registered NBFC-MFIs and other MFIs (Societies, Trusts, etc.) which are members of RBI recognised ‘Self-Regulatory Organisation’ of the sector. Bank lending to such MFIs can be classified under different categories of PSL in accordance with conditions specified in our Master Directions FIDD.CO.Plan.BC.5/04.09.01/2020-21 dated September 04, 2020 and updated from time to time.

Biennial survey on Foreign Collaboration in Indian Industry (FCS)

Some important definitions and concepts

Ans.: Indian company which has entered into an agreement with a foreign entity in terms of technology transfer, know-how transfer, use of patent, brand name etc, then such type of agreement are treated as Foreign Technical Collaborations (FTC).

Retail Direct Scheme

Account opening related queries

Targeted Long Term Repo Operations (TLTROs)

FAQs pertaining to TLTRO 2.0

Ans: This condition applies only to the fourth TLTRO conducted on April 17, 2020. It does not apply to the TLTROs conducted before April 17, 2020. It also does not apply to TLTRO 2.0.

Housing Loans

Give yourself comfortable time. Do not hurry your purchase or loan in any case. Shopping around for a home loan will help you to get the best financing deal. Shopping, comparing, seeking clarification and negotiating with banks may save you thousands of rupees.

a) Obtain information from several banks

Home loans are available from mainly two types of lenders--commercial banks and housing finance companies. Different lenders may quote you different rates of interest and other terms and conditions, so you should contact several lenders to make sure you’re getting the best value for money.

Find out how much of a down payment you are required to pay, and find out all the costs involved in the loan (including processing fees, administrative charges and prepayment charges levied by banks). Knowing just the amount of the EMI or the interest rate is not good enough. Similarly, ask for information on loan amount, loan term, and type of loan (fixed or floating) so that you can compare the information and take an informed decision.

The following is some important information that you will require.

i) Rates

Ask your lender about its current home loan interest rates and whether the rate is fixed or floating. Remember that when interest rates in the economy go up so does the floating rates and hence the monthly re-payment.

If the rate quoted is a floating rate, ask how your rate and loan payment will vary, including the extent to which your loan payment will be reduced when rates go down by a certain percentage. Ask your lender to what index your floating home loan is referenced / linked and the periodicity of updation of that index. Also ask your bank whether the index is internal or external and how and where it is published.

Ask about the loan’s annual percentage rates (APR). The APR takes into account not only the interest rate but also fees and certain other charges that you may be required to pay, expressed as a yearly rate. Banks are obliged to reveal the APR if requested for by the customer.

ii) Reset Clause

Check the reset clause, especially in the case of fixed interest rate loan as the rates will not be fixed throughout the tenure of the loan.

iii) Spread/Mark up

Check if the margin in the case of the floating rate is fixed or variable. The rate of interest you have to pay will vary accordingly.

iv) Fees

A home loan often requires payment of various fees, such as loan origination or processing charges, administrative charges, documentation, late payment, changing the loan tenure, switching to different loan package during the loan tenure, restructuring of loan, changing from fixed to floating interest rate loan and vice versa, legal fee, technical inspection fee, recurring annual service fee, document retrieval charges and pre-payment charges, if you want to prepay the loan. Every lender should be able to give you an estimate of its fees. Many of these fees are negotiable / can be waived also.

Ask what each fee includes. Sometimes several components are lumped into one fee. Ask for an explanation of any fee you do not understand. Also, remember that most of these fees are perhaps negotiable! Do negotiate with your bank before agreeing to a particular fee. See how the all inclusive rate compares with the all inclusive rates offered by other banks. While planning your finances, don't forget to include the costs of stamp duty and registration.

v) Down Payments / Margin

Some lenders require 20/30 percent of the home’s purchase price as a down payment from you. However, many lenders also offer loans that require less than 20/30 percent down payment, sometimes as little as 5 percent .Ask about the lender’s requirements for a down payment and also negotiate with him to reduce the down payments.

b) Obtain the best deal

Once you know what each bank has to offer in terms of rates, fees and down payments, negotiate for the best deal. Ask the lender to write down all the costs associated with the loan. Then ask if the bank will waive or reduce one or more of its fees or agree to a lower rate. Do make sure that the bank is not agreeing to lower one fee while raising another or to lower the rate while raising the fees. Ask for clarification in case you do not understand any particular term. All banks are obliged to explain the most important terms and conditions of the home loan in detail.

Once you are satisfied with the terms you have negotiated, please do obtain a written offer letter from the lender and keep a copy with you. Read the offer letter carefully before signing.

Indian Currency

B) Banknotes

The highest denomination note ever printed by the Reserve Bank of India was the ₹10000 note in 1938 which was demonetized in January 1946. The ₹10000 was again introduced in 1954. These notes were demonetized in 1978.

Government Securities Market in India – A Primer

The following steps should be followed in purchase of a security:

-

Which security to invest in – Typically this involves deciding on the maturity and coupon. Maturity is important because this determines the extent of risk an investor like an UCB is exposed to – normally higher the maturity, higher the interest rate risk or market risk. If the investment is largely to meet statutory requirements, it may be advisable to avoid taking undue market risk and buy securities with shorter maturity. Within the shorter maturity range (say 5-10 years), it would be safer to buy securities which are liquid, that is, securities which trade in relatively larger volumes in the market. The information about such securities can be obtained from the website of the CCIL (http://www.ccilindia.com/OMMWCG.aspx), which gives real-time secondary market trade data on NDS-OM. Pricing is more transparent in liquid securities, thereby reducing the chances of being misled/misinformed. The coupon rate of the security is equally important for the investor as it affects the total return from the security. In order to determine which security to buy, the investor must look at the Yield to Maturity (YTM) of a security (please refer to Box III under para 24.4 for a detailed discussion on YTM). Thus, once the maturity and yield (YTM) is decided, the UCB may select a security by looking at the price/yield information of securities traded on NDS-OM or by negotiating with bank or PD or broker.

-

Where and Whom to buy from- In terms of transparent pricing, the NDS-OM is the safest because it is a live and anonymous platform where the trades are disseminated as they are struck and where counterparties to the trades are not revealed. In case, the trades are conducted on the telephone market, it would be safe to trade directly with a bank or a PD. In case one uses a broker, care must be exercised to ensure that the broker is registered on NSE or BSE or OTC Exchange of India. Normally, the active debt market brokers may not be interested in deal sizes which are smaller than the market lot (usually ₹ 5 cr). So it is better to deal directly with bank / PD or on NDS-OM, which also has a screen for odd-lots (i.e. less than ₹ 5 cr). Wherever a broker is used, the settlement should not happen through the broker. Trades should not be directly executed with any counterparties other than a bank, PD or a financial institution, to minimize the risk of getting adverse prices.

-

How to ensure correct pricing – Since investors like UCBs have very small requirements, they may get a quote/price, which is worse than the price for standard market lots. To be sure of prices, only liquid securities may be chosen for purchase. A safer alternative for investors with small requirements is to buy under the primary auctions conducted by RBI through the non-competitive route. Since there are bond auctions almost every week, purchases can be considered to coincide with the auctions. Please see question 14 for details on ascertaining the prices of the G-Secs.

All you wanted to know about NBFCs

B. Entities Regulated by RBI and applicable regulations

Foreign Investment in India

Domestic Deposits

I. Domestic Deposits

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Eligible entities and requirements to submit the FLA return

Ans: If the Partnership firms, Branches or Trustees have any outward FDI outstanding as on end-March of the latest FY, then they are required to file the FLA return.

External Commercial Borrowings (ECB) and Trade Credits

E. AVERAGE MATURITY PERIOD

You may refer to /documents/87730/39016390/12EC160712_A6.pdf for illustration purposes.

Remittances (Money Transfer Service Scheme (MTSS) and Rupee Drawing Arrangement (RDA))

Money Transfer Service Scheme (MTSS)

Core Investment Companies

Core Investment Companies (CICs)

Ans: No, they are only exempt from norms regarding submission of Statutory Auditor Certificate regarding continuance of business as NBFC, capital adequacy and concentration of credit / investments norms.

FAQs on Non-Banking Financial Companies

Exemptions to the companies not accepting public deposits

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

Paytm Payments Bank Wallet

Coordinated Portfolio Investment Survey – India

What to report under CPIS?

Ans: The portfolio investment assets are required to be reported on marked to market basis as at the end of the reference period, with the breakups into type of securities viz., equity securities, short-term debt securities (with and original maturity of up to one year) and long-term debt securities (with an original maturity of more than a year) and country of residence of issuer.

FAQs on Master Directions on Priority Sector Lending Guidelines

L. Co-lending by Banks & NBFCs

Clarification: While the guidelines allow sharing of risks and rewards between the bank and the NBFC for ensuring appropriate alignment of respective business objectives, the priority sector assets on the bank’s books should at all times be without recourse to the NBFC.

Clarification: Only if the bank can exercise its discretion regarding taking into its books the loans originated by NBFC as per the Agreement, the arrangement will be akin to a direct assignment transaction. If the Agreement entails a prior, irrevocable commitment on the part of the bank to take into its books its share of the individual loans as originated by the NBFC, it shall not be akin to direct assignment transaction.

Clarification: Both entities, the bank & the NBFC shall be guided by the bilateral Master Agreement entered by them for implementing the Co-lending Model (CLM). The agreement may state any cap on the number and amount of loans that can be originated by the NBFC under the Co-lending model.

Clarification: If the Agreement entails a prior, irrevocable commitment on the part of the bank, it has been advised that the partner bank and NBFC shall have to put in place suitable mechanisms for ex-ante due diligence by the bank. Such due diligence should ensure compliance with RBI regulations on KYC and outsourcing of activities before disbursal of the loans by the NBFC.

Clarification: Back-to-back basis implies that the loans will be first opened by NBFC and then bank will open loan accounts subsequently.

Clarification: The bank and the NBFC can decide on this aspect as per the Master agreement between them.

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Eligible entities and requirements to submit the FLA return

Ans: FLA return and Annual Performance Report (APR) for ODI are two different returns and monitored by two different departments of RBI. So, you are required to submit both the returns if these are applicable for your entity. For more information on APR, please refer to the Master Direction – Reporting under Foreign Exchange Management Act, 1999 on RBI’s website.

Biennial survey on Foreign Collaboration in Indian Industry (FCS)

Some important definitions and concepts

Ans.: An Indian company is called as a Foreign Subsidiary if a non-resident investor owns more than 50 per cent of the voting power / equity capital or where a non-resident investor and its subsidiary(s) combined own more than 50 per of the voting power / equity capital of an Indian enterprise.

Government Securities Market in India – A Primer

Retail Direct Scheme

Know Your Customer (KYC) related queries

Housing Loans

Indian Currency

B) Banknotes

The paper currently being used for printing of banknotes in India is made by using 100% cotton.

All you wanted to know about NBFCs

B. Entities Regulated by RBI and applicable regulations

Foreign Investment in India

Domestic Deposits

I. Domestic Deposits

Savings bank account cannot be opened in the name of the Government Department/ Government Scheme, except in respect of deposits of Government organizations/ agencies listed below:

-

Primary Co-operative Credit Society which is being financed by the bank.

-

Khadi and Village Industries Boards.

-

Agriculture Produce Market Committees.

-

Societies registered under Societies Registration Act, 1860 or any other corresponding law in force in State or a Union Territory.

-

Companies governed by the Companies Act, 1956 which have been licensed by the Central Government under Section 25 of the said Act, or under the corresponding provision in the Indian Companies Act, 1913 and permitted, not to add to their names the word “Limited” or the words “Private Limited”.

-

Institutions other than those mentioned in clause (i) above and whose entire income is exempt from payment of income tax under Income-Tax Act, 1961.

-

Government departments/ bodies/ agencies in respect of grants/ subsidies released for implementation of various programmes/ Schemes sponsored by Central Government/ State Governments subject to production of an authorisation from the respective Government departments to open savings bank accounts.

-

Development of Women and Children in Rural Areas (DWCRA).

-

Self-help Groups (SHGs), registered or unregistered, which are engaged in promoting savings habits among their members.

-

Farmers’ Clubs – Vikas Volunteer Vahini (VVV).

Remittances (Money Transfer Service Scheme (MTSS) and Rupee Drawing Arrangement (RDA))

Money Transfer Service Scheme (MTSS)

Core Investment Companies

Core Investment Companies (CICs)

Ans: Yes, as they are regulated by RBI, they would require NOC from Department of Non-Banking Supervision (DNBS) for making investments in the financial sector. However, a registered CIC making investments in the non-financial sector need not obtain prior approval from the Department of Non-Banking Supervision (DNBS), RBI. It will only need to report such investments to the Department within 30 days of such investment.

Targeted Long Term Repo Operations (TLTROs)

FAQs pertaining to TLTRO 2.0

Ans: In terms of the press release 2237/2019-2020 dated April 17, 2020 notifying the TLTRO 2.0 scheme, at least 50 per cent of the total funds availed under the scheme has to be deployed in specified securities issued by small NBFCs of asset size of ₹ 500 crores and below, mid-sized NBFCs of asset size between ₹ 500 crores and ₹ 5000 crores and MFIs. The objective is to ease any liquidity stress and/or impediments to market access that these small and mid-sized entities might be facing. In order to incentivise banks’ investment in the specified securities of these entities, it has been decided that a bank can exclude the face value of such securities kept in the HTM category from computation of adjusted non-food bank credit (ANBC) for the purpose of determining priority sector targets/sub-targets. This exemption is only applicable to the funds availed under TLTRO 2.0.

FAQs on Non-Banking Financial Companies

Net owned fund

External Commercial Borrowings (ECB) and Trade Credits

E. AVERAGE MATURITY PERIOD

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

Paytm Payments Bank Wallet

Coordinated Portfolio Investment Survey – India

What to report under CPIS?

Ans: Reporting entities should report the data in the unit mentioned in the survey schedule (for eg., INR Lakh).

Foreign Investment in India

Biennial survey on Foreign Collaboration in Indian Industry (FCS)

Some important definitions and concepts

Ans.: An Indian company is called as Foreign Associate if non-resident investor owns at least 10% and no more than 50% of the voting power/equity capital or where non-resident investor and its subsidiary(s) combined own at least 10% but no more than 50% of the voting power/equity capital of an Indian enterprise.

Retail Direct Scheme

Know Your Customer (KYC) related queries

-

Enter your PAN card number and date of birth to retrieve details available in CKYC.

-

Provide address details, scanned copy of your signature, bank account details and nominee details.

-

Authenticate the user agreement form using Aadhaar by submitting the OTP sent on your mobile number linked to Aadhaar.

Targeted Long Term Repo Operations (TLTROs)

FAQs pertaining to TLTRO 2.0

Ans: The funds availed under TLTRO 2.0 are to be deployed in investment grade bonds, commercial paper (CPs) and non-convertible debentures (NCDs) of Non-Banking Financial Companies (NBFCs) and MFIs in the manner outlined in the press release dated April 17, 2020.

Housing Loans

When other banks reduce the interest rate, you may prefer to close your account with the bank with whom you are banking, to avail of the loan from the bank offering reduced rates of interest. You have to pay pre-payment charges for doing so. In order to ensure that their customers do not approach other banks for availing reduced interest rates, banks allow customers to switch over from a higher interest loan to a lower interest loan by paying a switch over fees which is lesser than the pre-payment charges. Generally switchover fee is taken as percentage of the outstanding loan amount.

Keep up-dating yourself on various changes in the home loan market. Visit the branch, discuss with the officials to get the best out of any changes in the home loan scenario.

Indian Currency

B) Banknotes

Fifteen languages are appearing in the language panel of banknotes in addition to Hindi prominently displayed in the centre of the note and English on the reverse of the banknote.

Government Securities Market in India – A Primer

14.1 The return on a security is a combination of two elements (i) coupon income – that is, interest earned on the security and (ii) the gain / loss on the security due to price changes and reinvestment gains or losses.

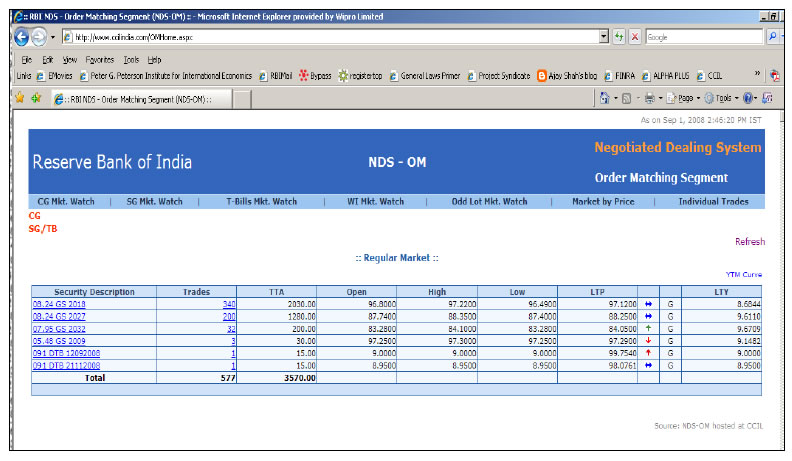

14.2 Price information is vital to any investor intending to either buy or sell G-Secs. Information on traded prices of securities is available on the RBI website http://www.rbi.org.in under the path Home → Financial Markets → Financial Markets Watch → Order Matching Segment of Negotiated Dealing System. This will show a screen containing the details of the latest trades undertaken in the market along with the prices. Additionally, trade information can also be seen on CCIL website http://www.ccilindia.com/OMHome.aspx. On this page, the list of securities and the summary of trades is displayed. The total traded amount (TTA) on that day is shown against each security. Typically, liquid securities are those with the largest amount of TTA. Pricing in these securities is efficient and hence UCBs can choose these securities for their transactions. Since the prices are available on the screen they can invest in these securities at the current prices through their custodians. Participants can thus get near real-time information on traded prices and take informed decisions while buying / selling G-Secs. The screenshots of the above webpage are given below:

NDS-OM Market

The website of the Financial Benchmarks India Private Limited (FBIL), (www.fbil.org.in) is also a right source of price information, especially on securities that are not traded frequently.

All you wanted to know about NBFCs

B. Entities Regulated by RBI and applicable regulations

The list of registered NBFCs is available on the web site of Reserve Bank of India and can be viewed at www.rbi.org.in → Sitemap → NBFC List. The instructions issued to NBFCs from time to time are also hosted at www.rbi.org.in → Notifications → Master Circulars → Non-banking, besides, being issued through Official Gazette notifications and press releases.

Domestic Deposits

I. Domestic Deposits

-

In the case of term deposit standing in the name/s of a deceased individual depositor, or two or more joint depositors, where one of the depositor has died, the criterion for payment of interest on matured deposits in the event of death of the depositor in the above cases has been left to the discretion of individual banks subject to their Board laying down a transparent policy in this regard.

-

In the case of balances lying in current account standing in the name of a deceased individual depositor/ sole proprietorship concern, interest should be paid only from May 1, 1983 or from the date of death of the depositor, whichever is later, till the date of repayment to the claimant/s at the rate of interest applicable to savings deposit as on the date of payment. However, in the case of NRE deposit, if the claimants are residents, the deposit on maturity is treated as domestic rupee and interest is paid for the subsequent period at a rate applicable to the domestic deposit of similar maturity.

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Eligible entities and requirements to submit the FLA return

Ans: If all non-resident shareholders of an entity have transferred their shares to the residents during the reporting period and the entity does not have any outstanding investment in respect of inward and outward FDI as on end-March of the latest FY, then the entity need not submit the FLA return.

External Commercial Borrowings (ECB) and Trade Credits

E. AVERAGE MATURITY PERIOD

Remittances (Money Transfer Service Scheme (MTSS) and Rupee Drawing Arrangement (RDA))

Money Transfer Service Scheme (MTSS)

Core Investment Companies

Core Investment Companies (CICs)

Ans: Exempted CICs desirous of making overseas investment in financial sector shall first need to hold a Certificate of Registration (CoR) from Reserve Bank of India (the Bank) and will have to comply with all the regulations applicable to registered CIC-ND-SI. However, they need not obtain NOC from the Bank if their investments overseas are in the non-financial sector.

FAQs on Non-Banking Financial Companies

Ceiling on deposits

A. As per the new Regulatory framework, there is no overall ceiling on the borrowings of NBFCs. However, limits have been prescribed for acceptance of Public Deposits as indicated here.

Level of credit rating |

Ceiling on public deposits |

|

EL/HP Cos. |

LC/ICs |

|

AAA |

4.0 |

2.0 |

AA |

2.5 |

1.0 |

A |

1.5 |

0.5 |

A - (CRISIL & ICRA) } |

||

BBB (CARE) } |

0.5 |

Nil |

BBB- (DCR India) } |

||

It is to be noted that there is an in-built ceiling on the total borrowings of the NBFCs accepting deposits from public, because they are required to maintain a capital adequacy ratio of 10 per cent of their risk weighted assets effective from 31.3.1998 and 12 per cent from 31.3.1999. Their capacity to create assets and raise corresponding borrowings will be restricted because of capital adequacy norms.

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

Paytm Payments Bank Wallet

Coordinated Portfolio Investment Survey – India

What to report under CPIS?

Ans: If the responding entity does not have any portfolio investment asset during the reference period, then that entity is required to submit NIL survey schedule to the generic email ID of the Reserve Bank as per the instruction in the survey schedule.

Biennial survey on Foreign Collaboration in Indian Industry (FCS)

Some important definitions and concepts

Ans.: An Indian company is said have Pure Technical Collaboration if the company has only foreign technical collaboration and have not received any foreign direct investment.

Retail Direct Scheme

Know Your Customer (KYC) related queries

Housing Loans

Targeted Long Term Repo Operations (TLTROs)

FAQs pertaining to On Tap TLTRO/ reversal of TLTRO/ TLTRO 2.0 transactions

Ans: Banks can submit their request for exercising the repayment option till October 28, 2020. On repayment of funds availed under TLTRO/ TLTRO 2.0, the associated securities shall be shifted out of the HTM category. The shifting of the TLTRO/ TLTRO 2.0 investments out of HTM shall be in addition to the shifting of investments permitted at the beginning of the accounting year and subject to adherence to the guidelines contained in the Master Circular – Prudential Norms for Classification, Valuation and Operation of Investment Portfolio by Banks dated July 1, 2015. These investments under TLTRO/ TLTRO 2.0 against which funds are being repaid will not be exempted from reckoning under the large exposure framework (LEF) and computation of adjusted non-food bank credit (ANBC) for the purpose of determining priority sector targets/sub-targets.

Indian Currency

B) Banknotes

Yes, it is possible to have two or more banknotes with the same serial number, but they would either have a different Inset Letter or year of printing or signature of a different Governor of RBI. An Inset Letter is an alphabet printed on the Number Panel of the banknote. There can be notes without any inset letter also.

Government Securities Market in India – A Primer

15.1 Transactions undertaken between market participants in the OTC / telephone market are expected to be reported on the NDS-OM platform within 15 minutes after the deal is put through over telephone. All OTC trades are required to be mandatorily reported on the NDS-OM reported segment for settlement. Reporting on NDS-OM is a two stage process wherein both the seller and buyer of the security have to report their leg of the trade. System validates all the parameters like reporting time, price, security etc. and when all the criterias of both the reporting parties match, the deals get matched and trade details are sent by NDS-OM system to CCIL for settlement.

15.2 Reporting on behalf of entities maintaining gilt accounts with the custodians is done by the respective custodians in the same manner as they do in case of their own trades i.e., proprietary trades. The securities leg of these trades settles in the CSGL account of the custodian. Funds leg settle in the current account of the PM with RBI.

15.3 In the case of NDS-OM, participants place orders (amount and price) in the desired security on the system. Participants can modify / cancel their orders. Order could be a ‘bid’ (for purchase) or ‘offer’ (for sale) or a two way quote (both buy and sell) of securities. The system, in turn, will match the orders based on price and time priority. That is, it matches bids and offers of the same prices with time priority. It may be noted that bid and offer of the same entity do not match i.e. only inter-entity orders are matched by NDS-OM and not intra-entity. The NDS-OM system has separate screen for trading of the Central Government papers, State Government securities (SDLs) and Treasury bills (including Cash Management Bills). In addition, there is a screen for odd lot trading also essentially for facilitating trading by small participants in smaller lots of less than ₹ 5 crore. The minimum amount that can be traded in odd lot is ₹ 10,000 in dated securities, T-Bills and CMBs. The NDS-OM platform is an anonymous platform wherein the participants will not know the counterparty to the trade. Once an order is matched, the deal ticket gets generated automatically and the trade details flow to the CCIL. Due to anonymity offered by the system, the pricing is not influenced by the participants’ size and standing.

All you wanted to know about NBFCs

B. Entities Regulated by RBI and applicable regulations

The regulation on non-deposit accepting NBFCs with asset size of less than ₹ 500 crore would be as under:

(i) They shall not be subjected to any regulation either prudential or conduct of business regulations viz., Fair Practices Code (FPC), KYC, etc., if they have not accessed any public funds and do not have a customer interface.

(ii) Those having customer interface will be subjected only to conduct of business regulations including FPC, KYC etc., if they are not accessing public funds.

(iii) Those accepting public funds will be subjected to limited prudential regulations but not conduct of business regulations if they have no customer interface.

(iv) Where both public funds are accepted and customer interface exist, such companies will be subjected both to limited prudential regulations and conduct of business regulations.

Foreign Investment in India

Answer: No, refer to Para 7.13 of Master Direction-Foreign Investment in India.

FAQs on Non-Banking Financial Companies

Ceiling on deposits

Domestic Deposits

I. Domestic Deposits

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Eligible entities and requirements to submit the FLA return

Ans: Shares issued by reporting entities to non-resident on non-repatriable basis should not be considered as foreign investment; therefore, entities which have issued the shares to non-resident only on non-repatriable basis, is not required to submit the FLA return.

External Commercial Borrowings (ECB) and Trade Credits

F. LEVERAGE CRITERIA AND BORROWING LIMIT

Core Investment Companies

Core Investment Companies (CICs)

Ans: Yes, CICs presently registered with the Bank but fulfilling the criteria for exemption under Notification No 220 dated January 05, 2010 can seek voluntary deregistration. Both audited balance sheet and auditors certificate are required to be submitted for the purpose.

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

FASTag issued by Paytm Payments Bank

Coordinated Portfolio Investment Survey – India

What to report under CPIS?

Ans: If the entity’s accounts are not audited before the due date of submission, then they should report in the survey based on unaudited (provisional) account.

Domestic Deposits

II. Deposits of Non-Residents Indians (NRIs)

Biennial survey on Foreign Collaboration in Indian Industry (FCS)

Some other important points to be noted

Ans.: Please read the definitions of foreign subsidiary, foreign associate, Pure Technical Collaboration and accordingly select the type of reporting company. Further, if you have chosen “Others” in identification of reporting company, please specify.

Core Investment Companies

Core Investment Companies (CICs)

Ans: CICs having asset size of below Rs 100 crore are exempted from registration and regulation from the Reserve Bank, except if they wish to make overseas investments in the financial sector.

Retail Direct Scheme

Know Your Customer (KYC) related queries

-

Upload a scanned copy of your PAN card.

-

Download the XML version of your Aadhaar from the UIDAI website and upload it. Use the 4-digit pin specified while downloading XML version.

-

Provide address details, scanned copy of your signature, bank account details and nominee details.

-

Complete the video KYC by choosing a time slot for later or immediately, depending on the availability at that point of time.

-

Authenticate the user agreement form by Aadhaar using the OTP sent on your mobile number linked to Aadhaar.

Targeted Long Term Repo Operations (TLTROs)

FAQs pertaining to On Tap TLTRO/ reversal of TLTRO/ TLTRO 2.0 transactions

Ans: Banks can use either of the alternatives. However, the request of the bank will be subject to availability of funds as on date of application i.e., funds cannot be guaranteed in case the total amount of ₹1,00,000 crore is already availed.

Housing Loans

- At the time of sourcing the loan, banks are required to provide information about the interest rate applicable, the fees / charges and any other matter which affects your interest and the same are usually furnished in the product brochure of the banks. Complete transparency is mandatory.

- The banks will supply you authenticated copies of all the loan documents executed by you at their cost along with a copy each of all enclosures quoted in the loan document on request.

A bank cannot reject your loan application without furnishing valid reason(s) for the same.

Indian Currency

B) Banknotes

With a view to enhancing operational efficiency and cost effectiveness in banknote printing, non-sequential numbering was introduced in 2011 consistent with international best practices. Packets of banknotes with non-sequential numbering contain 100 notes which are not sequentially numbered.

All you wanted to know about NBFCs

B. Entities Regulated by RBI and applicable regulations

Foreign Investment in India

FAQs on Non-Banking Financial Companies

Ceiling on deposits

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Eligible entities and requirements to submit the FLA return

Ans: No, balance sheet or profit and loss (P&L) accounts are not required to be submitted along with the FLA return.

External Commercial Borrowings (ECB) and Trade Credits

F. LEVERAGE CRITERIA AND BORROWING LIMIT

Government Securities Market in India – A Primer

Primary Market

16.1 Once the allotment process in the primary auction is finalized, the successful participants are advised of the consideration amounts that they need to pay to the Government on settlement day. The settlement cycle for auctions of all kind of G-Secs i.e. dated securities, T-Bills, CMBs or SDLs, is T+1, i.e. funds and securities are settled on next working day from the conclusion of the trade. On the settlement date, the fund accounts of the participants are debited by their respective consideration amounts and their securities accounts (SGL accounts) are credited with the amount of securities allotted to them.

Secondary Market

16.2 The transactions relating to G-Secs are settled through the member’s securities / current accounts maintained with the RBI. The securities and funds are settled on a net basis i.e. Delivery versus Payment System-III (DvP-III). CCIL guarantees settlement of trades on the settlement date by becoming a central counter-party (CCP) to every trade through the process of novation, i.e., it becomes seller to the buyer and buyer to the seller. 16.3 All outright secondary market transactions in G-Secs are settled on a T+1 basis. However, in case of repo transactions in G-Secs, the market participants have the choice of settling the first leg on either T+0 basis or T+1 basis as per their requirement. RBI vide FMRD.DIRD.05/14.03.007/2017-18 dated November 16, 2017 had permitted FPIs to settle OTC secondary market transactions in Government Securities either on T+1 or on T+2 basis and in such cases, It may be ensured that all trades are reported on the trade date itself.

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

FASTag issued by Paytm Payments Bank

Coordinated Portfolio Investment Survey – India

Some important definitions and concepts

Ans: Equity consists of all instruments and records that acknowledge claims on the residual value of a corporation or quasi-corporation, after the claims of all creditors have been met. Equity may be split into listed shares, unlisted shares, and other equity. Both listed and unlisted shares are equity securities. Equity securities are commonly called shares or stocks. Other equity is equity that is not in the form of securities.

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Procedure for submission of the FLA return

Ans: Entities can submit the FLA return through the online web-based portal Foreign Liabilities and Assets Information Reporting (FLAIR) system, having address https://flair.rbi.org.in/fla/faces/pages/login.xhtml.

-

To access the URL https://flair.rbi.org.in/fla/faces/pages/login.xhtml, any of the browsers viz, Internet Explorer, Google chrome, Firefox etc. can be used, as all of these would support this application.

-

The entity has to register on the portal by clicking Registration for New Entity Users.

-

The entity has to fill the details in the FLA user registration form, upload the documents mentioned (Verification Letter and Authority Letter) and click submit to complete the registration.

-

After successful registration, user id and default password will be sent to the authorized person’s mail id. Using this user id and password, entities can login to the FLAIR portal and file the FLA Return.

- Please note: The excel-based format and email-based reporting system has been replaced by the web-based format for submission of annual FLA return from June 2019.

Biennial survey on Foreign Collaboration in Indian Industry (FCS)

Some other important points to be noted

Ans.: In the FCS form, industry codes are given as per the National Industrial Classification (NIC) (2 digit) codes. Please specify, if you have chosen “Other” industry codes, like Other manufacturing, Other services activities.

Retail Direct Scheme

Know Your Customer (KYC) related queries

Targeted Long Term Repo Operations (TLTROs)

FAQs pertaining to On Tap TLTRO/ reversal of TLTRO/ TLTRO 2.0 transactions

Ans: There is no restriction with respect to primary/ secondary market investments in specified securities under the on Tap TLTRO scheme.

Housing Loans

If you have a complaint against only scheduled bank on any of the above grounds, you can lodge a complaint with the bank concerned in writing in a specific complaint register provided at the branches as per the recommendation of the Goiporia Committee or on a sheet of paper. Ask for a receipt of your complaint. The details of the official receiving your complaint may be specifically sought. If the bank fails to respond within 30 days, you can lodge a complaint with the Banking Ombudsman. (Please note that complaints pending in any other judicial forum will not be entertained by the Banking Ombudsman). No fee is levied by the office of the Banking Ombudsman for resolving the customer’s complaint. A unique complaint identification number will be given to you for tracking purpose. (A list of the Banking Ombudsmen along with their contact details is provided on the RBI website).

Complaints are to be addressed to the Banking Ombudsman within whose jurisdiction the branch or office of the bank complained against is located. Complaints can be lodged simply by writing on a plain paper or online at www.bankingombudsman.rbi.org.in or by sending an email to the Banking Ombudsman. Complaint forms are available at all bank branches also.

Complaint can also be lodged by your authorised representative (other than a lawyer) or by a consumer association / forum acting on your behalf.

If you are not happy with the decision of the Banking Ombudsman, you can appeal to the Appellate Authority in the Reserve Bank of India.

Indian Currency

B) Banknotes

Fresh banknotes issued by Reserve Bank of India till August 2006 were serially numbered. Each of these banknote bears a distinctive serial number along with a prefix consisting of numerals and letter/s. The banknotes are issued in packets containing 100 pieces.

The Bank adopted the "STAR series" numbering system for replacement of defectively printed banknote in a packet of 100 pieces of serially numbered banknotes. The Star series banknotes are exactly similar to the other banknotes, but have an additional character viz., a *(star) in the number panel in the space between the prefix.

Core Investment Companies

Core Investment Companies (CICs)

Ans: CICs are prohibited from contributing capital to any partnership firm or to be partners in partnership firms including Limited Liability Partnerships (LLPs) or any association of person similar in nature to partnership firms.

All you wanted to know about NBFCs

B. Entities Regulated by RBI and applicable regulations

The Bank has issued detailed directions on prudential norms, vide Non-Banking Financial (Deposit Accepting or Holding) Companies Prudential Norms (Reserve Bank) Directions, 2007, Non-Systemically Important Non-Banking Financial (Non-Deposit Accepting or Holding) Companies Prudential Norms (Reserve Bank) Directions, 2015 and Systemically Important Non-Banking Financial (Non-Deposit Accepting or Holding) Companies Prudential Norms (Reserve Bank) Directions, 2015. Applicable regulations vary based on the deposit acceptance or systemic importance of the NBFC.

The directions inter alia, prescribe guidelines on income recognition, asset classification and provisioning requirements applicable to NBFCs, exposure norms, disclosures in the balance sheet, requirement of capital adequacy, restrictions on investments in land and building and unquoted shares, loan to value (LTV) ratio for NBFCs predominantly engaged in business of lending against gold jewellery, besides others. Deposit accepting NBFCs have also to comply with the statutory liquidity requirements. Details of the prudential regulations applicable to NBFCs holding deposits and those not holding deposits is available in the section ‘Regulation – Non-Banking – Notifications - Master Circulars’ in the RBI website.

Foreign Investment in India

FAQs on Non-Banking Financial Companies

Inter-corporate deposits (ICDs)

Domestic Deposits

II. Deposits of Non-Residents Indians (NRIs)

External Commercial Borrowings (ECB) and Trade Credits

F. LEVERAGE CRITERIA AND BORROWING LIMIT

Government Securities Market in India – A Primer

Coordinated Portfolio Investment Survey – India

Some important definitions and concepts

Ans: The following are included under equity securities:

-

Ordinary shares.

-

Stocks.

-

Participating preference shares.

-

Shares/units in mutual funds and investment trusts

-

Depository receipts (e.g., American Depository Receipts) denoting ownership of equity securities issued by non-residents.

-

Securities sold under repos or “lent” under securities lending arrangements.

-

Securities acquired under reverse repos or securities borrowing arrangements and subsequently sold to a third party should be reported as a negative holding.

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

FASTag issued by Paytm Payments Bank

Biennial survey on Foreign Collaboration in Indian Industry (FCS)

Some other important points to be noted

Ans.: Yes, it is mandatory. Here the person authorised to fill the form owns the responsibility of information furnished and declares its accuracy including CIN number. It is a final check for all the details which are filled-up in the survey schedule of FCS survey.

Government Securities Market in India – A Primer

Delivery versus Payment (DvP) is the mode of settlement of securities wherein the transfer of securities and funds happen simultaneously. This ensures that unless the funds are paid, the securities are not delivered and vice versa. DvP settlement eliminates the settlement risk in transactions. There are three types of DvP settlements, viz., DvP I, II and III which are explained below:

Delivery versus Payment (DvP) is the mode of settlement of securities wherein the transfer of securities and funds happen simultaneously. This ensures that unless the funds are paid, the securities are not delivered and vice versa. DvP settlement eliminates the settlement risk in transactions. There are three types of DvP settlements, viz., DvP I, II and III which are explained below:

i. DvP I – The securities and funds legs of the transactions are settled on a gross basis, that is, the settlements occur transaction by transaction without netting the payables and receivables of the participant.

ii. DvP II – In this method, the securities are settled on gross basis whereas the funds are settled on a net basis, that is, the funds payable and receivable of all transactions of a party are netted to arrive at the final payable or receivable position which is settled.

iii. DvP III – In this method, both the securities and the funds legs are settled on a net basis and only the final net position of all transactions undertaken by a participant is settled.

Liquidity requirement in a gross mode is higher than that of a net mode since the payables and receivables are set off against each other in the net mode.

Retail Direct Scheme

Know Your Customer (KYC) related queries

Housing Loans

REVERSE MORTGAGE LOAN

The scheme of reverse mortgage has been introduced recently for the benefit of senior citizens owning a house but having inadequate income to meet their needs. Some important features of reverse mortgage are:

- A homeowner who is above 60 years of age is eligible for reverse mortgage loan. It allows him to turn the equity in his home into one lump sum or periodic payments mutually agreed by the borrower and the banker.

- The property should be clear from encumbrances and should have clear title of the borrower.

- NO REPAYMENT is required as long as the borrower lives, Borrower should pay all taxes relating to the house and maintain the property as his primary residence.

- The amount of loan is based on several factors: borrower’s age, value of the property, current interest rates and the specific plan chosen. Generally speaking, the higher the age, higher the value of the home, the more money is available.

- The valuation of the residential property is done at periodic intervals and it shall be clearly specified to the borrowers upfront. The banks shall have the option to revise the periodic / lump sum amount at such frequency or intervals based on revaluation of property.

- Married couples will be eligible as joint borrowers for financial assistance. In such a case, the age criteria for the couple would be at the discretion of the lending institution, subject to at least one of them being above 60 years of age.

- The loan shall become due and payable only when the last surviving borrower dies or would like to sell the home, or permanently moves out.

- On death of the home owner, the legal heirs have the choice of keeping or selling the house. If they decide to sell the house, the proceeds of the sale would be used to repay the mortgage, with the remainder going to the heirs.

- As per the scheme formulated by National Housing Bank (NHB), the maximum period of the loan period is 15 years. The residual life of the property should be at least 20 years. Where the borrower lives longer than 15 years, periodic payments will not be made by lender. However, the borrower can continue to occupy.

- From FY 2008-09, the lump sum amount or periodic payments received on reverse mortgage loan will not attract income tax or capital gains tax.

Note- Reverse mortgage is a fixed interest discounted product in reverse. It does not take into account the changes in interest rates as yet.

Important – This part is fine printed to help you practice reading the fine print. The loan agreement documentation runs into nearly 50 pages and its language is complex. If you thought everyone signs the same agreements with the bank, where is the need to read? You are not taking an informed decision. If you thought somebody would have pointed this to me if there was any problem, then maybe they did but you could not read or listen to it. Think again! Borrowers' and lenders' rights may not be expressed clearly in a transparent manner in all the loan agreements. The home loan agreement may not be provided to you in advance so that this could be read and understood before you sign the agreement. Every method may be used to delay handing over a copy to the borrower in sufficient time. Some areas you may focus are a) check the “reset clause” incorporated by some banks in their home loan agreements that allows them to change the interest rate in the future, even on fixed rate loans. Banks may set their reset clauses for 3 or 2 year intervals. They say a lender cannot have an agreement that a fixed rate is set for the entire tenure of 15 to 20 years as this will cause an asset-liability mismatch. Talk to your bank. b) Please seek clarifications on the term “exceptional circumstances” (if stated in the loan agreement) under which loan rates can be unilaterally changed by your bank. c) A common person thinks that default ideally means non-payment of one or more loan installments. In some loan documentation it can include divorce and death (in individual case) and even involvement in civil litigation or criminal offence. d) Does the loan agreement say that disbursement of the loan may be made directly to the builder or developer and in the case of a ready-built property to the vendor thereof and/or in such other manner as may be decided solely by bank? It is the borrower whose original property papers are retained with the bank, so why disburse to the builder. Possession of property has been delayed in some cases when the cheque was issued in the name of the builder and the builder refused to pay delay penalty to the borrower e) Does the agreement enable assignment of your loan to a third party? You take into account reputation and credibility of the bank before entering into a loan agreement with it. Are you comfortable with third party takes over or should you also be allowed to move your home loan from one bank to another in that case? Look for ambiguous clauses and discuss with the banker. Some agreements say changes in employment etc. have to be informed well in advance without quantifying the term “well in advance”. f) In one case the loan documentation says “issuance of pre-approval letter should not be construed as a commitment by the bank to grant the housing loan and processing fees is not re-fundable even if the home loan is not processed”. This is never ending it seems. The above are only indicative instances of what has been observed / reported/ indicated by various sources. However, our main objective was to get you into the habit of reading the fine print. If you have read this, you would have understood the importance of reading fine print in any document and we have achieved our objective. I only wish I could have made the print smaller as in the real cases.

Indian Currency

B) Banknotes

In terms of Section 25 of the RBI Act, the design, form and material of bank notes shall be such as may be approved by the Central Government after consideration of the recommendations made by Central Board.

Core Investment Companies

Core Investment Companies (CICs)

Ans: The term used in the CIC circulars is block sale and not block deal which has been defined by SEBI. In the context of the circular, a block sale would be a long term or strategic sale made for purposes of disinvestment or investment and not for short term trading. Unlike a block deal, there is no minimum number/value defined for the purpose.

All you wanted to know about NBFCs

B. Entities Regulated by RBI and applicable regulations

Foreign Investment in India

Answer: Please refer to regulation 11 of FEMA 20(R).

| Particulars | Listed Company | Un-Listed Company |

| Issue by an Indian company or transferred from a resident to non-resident - Price should not be less than | The price worked out in accordance with the relevant SEBI guidelines | The fair value worked out as per any internationally accepted pricing methodology for valuation on an arm’s length basis, duly certified by a Chartered Accountant or a SEBI registered Merchant Banker or a practicing Cost Accountant. |

| Transfer from a non-resident to resident - Price should not be more than | The price worked out in accordance with the relevant SEBI guidelines | The fair value as per any internationally accepted pricing methodology for valuation on an arm’s length basis, duly certified by a Chartered Accountant or a SEBI registered Merchant Banker. |

The pricing guidelines shall not be applicable for investment by a person resident outside India on non-repatriation basis.

FAQs on Non-Banking Financial Companies

Inter-corporate deposits (ICDs)

Domestic Deposits

II. Deposits of Non-Residents Indians (NRIs)

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Procedure for submission of the FLA return

Ans: You will receive the system-generated acknowledgement of FLA data submitted by you at the time of final submission itself. No separate mail will be sent in this regard.

External Commercial Borrowings (ECB) and Trade Credits

F. LEVERAGE CRITERIA AND BORROWING LIMIT

Coordinated Portfolio Investment Survey – India

Some important definitions and concepts

Ans: The following are not included under equity securities:

-

Equity securities issued by a nonresident enterprise that is related to the resident owner of those securities should be excluded from this survey.

-

Non-participating preference shares.

-

Securities acquired under reverse repos.

-

Securities acquired under borrowing arrangements.

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

National Common Mobility Card (NCMC) issued by Paytm Payments Bank

External Commercial Borrowings (ECB) and Trade Credits

F. LEVERAGE CRITERIA AND BORROWING LIMIT

Retail Direct Scheme

Know Your Customer (KYC) related queries

Domestic Deposits

II. Deposits of Non-Residents Indians (NRIs)

Housing Loans

REVERSE MORTGAGE LOAN

EXAMPLE OF EMI CALCULATION (PURE FIXED LOAN)

|

|

Amount of Loan |

1,000,000.00 |

|

|

|

|

Annual Interest Rate |

15.00% |

|

|

|

|

Number of Payments |

120 |

|

|

|

|

Monthly Payment |

16,133.50 |

|

|

| Number |

Payment |

Interest |

Principal |

Balance |

| 0 |

|

|

|

1,000,000.00 |

| 1 |

16,133.50 |

12,500.00 |

3,633.50 |

996,366.50 |

| 2 |

16,133.50 |

12,454.58 |

3,678.91 |

992,687.59 |

| 3 |

16,133.50 |

12,408.59 |

3,724.90 |

988,962.69 |

| 4 |

16,133.50 |

12,362.03 |

3,771.46 |

985,191.23 |

| 5 |

16,133.50 |

12,314.89 |

3,818.61 |

981,372.62 |

| 6 |

16,133.50 |

12,267.16 |

3,866.34 |

977,506.28 |

| 7 |

16,133.50 |

12,218.83 |

3,914.67 |

973,591.62 |

| 8 |

16,133.50 |

12,169.90 |

3,963.60 |

969,628.02 |

| 9 |

16,133.50 |

12,120.35 |

4,013.15 |

965,614.87 |

| 10 |

16,133.50 |

12,070.19 |

4,063.31 |

961,551.56 |

| 11 |

16,133.50 |

12,019.39 |

4,114.10 |

957,437.46 |

| 12 |

16,133.50 |

11,967.97 |

4,165.53 |

953,271.93 |

| 13 |

16,133.50 |

11,915.90 |

4,217.60 |

949,054.34 |

| 14 |

16,133.50 |

11,863.18 |

4,270.32 |

944,784.02 |

| 15 |

16,133.50 |

11,809.80 |

4,323.70 |

940,460.32 |

| 16 |

16,133.50 |

11,755.75 |

4,377.74 |

936,082.58 |

| 17 |

16,133.50 |

11,701.03 |

4,432.46 |

931,650.12 |

| 18 |

16,133.50 |

11,645.63 |

4,487.87 |

927,162.25 |

| 19 |

16,133.50 |

11,589.53 |

4,543.97 |

922,618.28 |

| 20 |

16,133.50 |

11,532.73 |

4,600.77 |

918,017.51 |

| 21 |

16,133.50 |

11,475.22 |

4,658.28 |

913,359.24 |

| 22 |

16,133.50 |

11,416.99 |

4,716.51 |

908,642.73 |

| 23 |

16,133.50 |

11,358.03 |

4,775.46 |

903,867.27 |

| 24 |

16,133.50 |

11,298.34 |

4,835.15 |

899,032.12 |

| 25 |

16,133.50 |

11,237.90 |

4,895.59 |

894,136.52 |

| 26 |

16,133.50 |

11,176.71 |

4,956.79 |

889,179.73 |

| 27 |

16,133.50 |

11,114.75 |

5,018.75 |

884,160.98 |

| 28 |

16,133.50 |

11,052.01 |

5,081.48 |

879,079.50 |

| 29 |

16,133.50 |

10,988.49 |

5,145.00 |

873,934.50 |

| 30 |

16,133.50 |

10,924.18 |

5,209.31 |

868,725.18 |

| 31 |

16,133.50 |

10,859.06 |

5,274.43 |

863,450.75 |

| 32 |

16,133.50 |

10,793.13 |

5,340.36 |

858,110.39 |

| 33 |

16,133.50 |

10,726.38 |

5,407.12 |

852,703.28 |

| 34 |

16,133.50 |

10,658.79 |

5,474.70 |

847,228.57 |

| 35 |

16,133.50 |

10,590.36 |

5,543.14 |

841,685.43 |

| 36 |

16,133.50 |

10,521.07 |

5,612.43 |

836,073.00 |

| 37 |

16,133.50 |

10,450.91 |

5,682.58 |

830,390.42 |

| 38 |

16,133.50 |

10,379.88 |

5,753.62 |

824,636.81 |

| 39 |

16,133.50 |

10,307.96 |

5,825.54 |

818,811.27 |

| 40 |

16,133.50 |

10,235.14 |

5,898.35 |

812,912.92 |

| 41 |

16,133.50 |

10,161.41 |

5,972.08 |

806,940.83 |

| 42 |

16,133.50 |

10,086.76 |

6,046.74 |

800,894.10 |

| 43 |

16,133.50 |

10,011.18 |

6,122.32 |

794,771.78 |

| 44 |

16,133.50 |

9,934.65 |

6,198.85 |

788,572.93 |

| 45 |

16,133.50 |

9,857.16 |

6,276.33 |

782,296.59 |

| 46 |

16,133.50 |

9,778.71 |

6,354.79 |

775,941.81 |

| 47 |

16,133.50 |

9,699.27 |

6,434.22 |

769,507.58 |

| 48 |

16,133.50 |

9,618.84 |

6,514.65 |

762,992.93 |

| 49 |

16,133.50 |

9,537.41 |

6,596.08 |

756,396.85 |

| 50 |

16,133.50 |

9,454.96 |

6,678.54 |

749,718.31 |

| 51 |

16,133.50 |

9,371.48 |

6,762.02 |

742,956.30 |

| 52 |

16,133.50 |

9,286.95 |

6,846.54 |

736,109.75 |

| 53 |

16,133.50 |

9,201.37 |

6,932.12 |

729,177.63 |

| 54 |

16,133.50 |

9,114.72 |

7,018.78 |

722,158.85 |

| 55 |

16,133.50 |

9,026.99 |

7,106.51 |

715,052.34 |

| 56 |

16,133.50 |

8,938.15 |

7,195.34 |

707,857.00 |

| 57 |

16,133.50 |

8,848.21 |

7,285.28 |

700,571.72 |

| 58 |

16,133.50 |

8,757.15 |

7,376.35 |

693,195.37 |

| 59 |

16,133.50 |

8,664.94 |

7,468.55 |

685,726.82 |

| 60 |

16,133.50 |

8,571.59 |

7,561.91 |

678,164.91 |

| 61 |

16,133.50 |

8,477.06 |

7,656.43 |

670,508.47 |

| 62 |

16,133.50 |

8,381.36 |

7,752.14 |

662,756.33 |

| 63 |

16,133.50 |

8,284.45 |

7,849.04 |

654,907.29 |

| 64 |

16,133.50 |

8,186.34 |

7,947.15 |

646,960.14 |

| 65 |

16,133.50 |

8,087.00 |

8,046.49 |

638,913.64 |

| 66 |

16,133.50 |

7,986.42 |

8,147.08 |

630,766.57 |

| 67 |

16,133.50 |

7,884.58 |

8,248.91 |

622,517.65 |

| 68 |

16,133.50 |

7,781.47 |

8,352.03 |

614,165.63 |

| 69 |

16,133.50 |

7,677.07 |

8,456.43 |

605,709.20 |

| 70 |

16,133.50 |

7,571.37 |

8,562.13 |

597,147.07 |

| 71 |

16,133.50 |

7,464.34 |

8,669.16 |

588,477.91 |

| 72 |

16,133.50 |

7,355.97 |

8,777.52 |

579,700.39 |

| 73 |

16,133.50 |

7,246.25 |

8,887.24 |

570,813.15 |

| 74 |

16,133.50 |

7,135.16 |

8,998.33 |

561,814.82 |

| 75 |

16,133.50 |

7,022.69 |

9,110.81 |

552,704.01 |

| 76 |

16,133.50 |

6,908.80 |

9,224.70 |

543,479.31 |

| 77 |

16,133.50 |

6,793.49 |

9,340.00 |

534,139.31 |

| 78 |

16,133.50 |

6,676.74 |

9,456.75 |

524,682.56 |

| 79 |

16,133.50 |

6,558.53 |

9,574.96 |

515,107.59 |

| 80 |

16,133.50 |

6,438.84 |

9,694.65 |

505,412.94 |

| 81 |

16,133.50 |

6,317.66 |

9,815.83 |

495,597.11 |

| 82 |

16,133.50 |

6,194.96 |

9,938.53 |

485,658.58 |

| 83 |

16,133.50 |

6,070.73 |

10,062.76 |

475,595.81 |

| 84 |

16,133.50 |

5,944.95 |

10,188.55 |

465,407.26 |

| 85 |

16,133.50 |

5,817.59 |

10,315.90 |

455,091.36 |

| 86 |

16,133.50 |

5,688.64 |