FAQ Page 1 - আরবিআই - Reserve Bank of India

Content Type:

Core Investment Companies

B. Registration and related matters:

Ans: No, this exemption is specifically given to CICs only. NBFCs other than CICs are not covered by this or any other aspect of the CIC Directions and would have to register with the Bank and comply with all applicable Directions of the Bank as issued from time to time.

Foreign Investment in India

FAQs on Non-Banking Financial Companies

Inter-corporate deposits (ICDs)

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Procedure for submission of the FLA return

Ans: Any query regarding filling of FLA return should be sent by email. We will revert back to you within one or two working days.

External Commercial Borrowings (ECB) and Trade Credits

F. LEVERAGE CRITERIA AND BORROWING LIMIT

Government Securities Market in India – A Primer

"When, as and if issued" (commonly known as ‘When Issued’) security refers to a security that has been authorized for issuance but not yet actually issued. When Issued trading takes place between the time a Government Security is announced for issuance and the time it is actually issued. All 'When Issued' transactions are on an 'if' basis, to be settled if and when the actual security is issued. RBI vide its notification FMRD.DIRD.03/14.03.007/2018-19 dated July 24, 2018 has issued When Issued Transactions (Reserve Bank) Directions, 2018 applicable to ‘When Issued’ transactions in Central Government securities.

Both new and reissued Government securities issued by the Central Government are eligible for ‘When Issued’ transactions. Eligibility of an issue for ‘When Issue’ trades would be indicated in the respective specific auction notification. Participants eligible to undertake both net long and short position in ‘When Issued’ market are (a) All entities which are eligible to participate in the primary auction of Central Government securities,(b) However, resident individuals, Hindu Undivided Families (HUF), Non-Resident Indians (NRI) and Overseas Citizens of India (OCI) are eligible to undertake only long position in ‘When Issued’ securities. (c) Entities other than scheduled commercial banks and Primary Dealers (PDs), shall close their short positions, if any, by the close of trading on the date of auction of the underlying Central Government security.

When Issued transactions would commence after the issue of a security is notified by the Central Government and it would cease at the close of trading on the date of auction. All ‘When Issued’ transactions for all trade dates shall be contracted for settlement on the date of issue. When Issued’ transactions shall be undertaken only on the Negotiated Dealing System-Order Matching (NDS-OM) platform. However, an existing position in a ‘When Issued’ security may be closed either on the NDS-OM platform or outside the NDS-OM platform, i.e., through Over-the-Counter (OTC) market. The open position limits are prescribed in the directions. All NDS-OM members participating in the ‘When Issued’ market are required to have in place a written policy on ‘When Issued’ trading which should be approved by the Board of Directors or equivalent body.

"Short sale" means sale of a security one does not own. RBI vide its notification FMRD.DIRD.05/14.03.007/2018-19 dated July 25, 2018 has issued Short Sale (Reserve Bank) Directions, 2018 applicable to ‘Short Sale’ transactions in Central Government dated securities. Banks may treat sale of a security held in the investment portfolio as a short sale and follow the process laid down in these directions. These transactions shall be referred to as ‘notional’ short sales. For the purpose of these guidelines, short sale would include 'notional' short sale.

Entities eligible to undertake short sales are (a) Scheduled commercial banks, (b) Primary Dealers, (c) Urban Cooperative Banks as permitted under circular UBD.BPD (PCB). Circular No.9/09.29.000/2013-14 dated September 4, 2013 and (d) Any other regulated entity which has the approval of the concerned regulator (SEBI, IRDA, PFRDA, NABARD, NHB). The maximum amount of a security (face value) that can be short sold is (a) for Liquid securities: 2% of the total outstanding stock of each security, or, ₹ 500 crore, whichever is higher; (b) for other securities: 1% of the total outstanding stock of each security, or, ₹ 250 crore, whichever is higher. The list of liquid securities shall be disseminated by FIMMDA/FBIL from time to time. Short sales shall be covered within a period of three months from the date of transaction (inclusive of the date). Banks undertaking ‘notional’ short sales shall ordinarily borrow securities from the repo market to meet delivery obligations, but in exceptional situations of market stress (e.g., short squeeze), it may deliver securities from its own investment portfolio. If securities are delivered out of its own portfolio, it must be accounted for appropriately and reflect the transactions as internal borrowing. It shall be ensured that the securities so borrowed are brought back to the same portfolio, without any change in book value.

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

National Common Mobility Card (NCMC) issued by Paytm Payments Bank

Retail Direct Scheme

Know Your Customer (KYC) related queries

Domestic Deposits

II. Deposits of Non-Residents Indians (NRIs)

Indian Currency

B) Banknotes

In terms of Section 33 of the RBI Act, 1934, all banknotes issued by RBI are backed by assets such as gold coin, gold bullion, foreign securities, rupee coin and rupee securities.

Coordinated Portfolio Investment Survey – India

Some important definitions and concepts

Ans: Debt securities with original maturity of more than one year is classified as long-term debt securities. These include bonds, debentures, and notes that usually give the holder the unconditional right to a fixed cash flow or contractually determined variable money income.

All you wanted to know about NBFCs

B. Entities Regulated by RBI and applicable regulations

NBFCs shall comply with the regulations contained in para 36 of the Master Direction – Reserve Bank of India (Non-Banking Financial Company – Scale Based Regulation) 2023 (as amended from time to time) while granting loans against security of shares. The regulations include, inter alia, maintaining a Loan to Value (LTV) ratio of 50% at all times, accept only Group 1 securities as collateral for loans of value more than ₹5 lakh where lending is done for investment in capital markets, undertake necessary reporting to stock exchanges on shares pledged in their favour, etc.

In addition to the above, there are other related regulations on NBFCs viz., there shall be ceiling of ₹1 crore per borrower for financing subscription to Initial Public Offer (IPO) and NBFCs can fix more conservative limits. Further, NBFCs are prohibited from lending against security of their own shares and debentures.

Core Investment Companies

B. Registration and related matters:

Ans: Yes, CICs presently registered with the Bank but fulfilling the criteria for ‘Unregistered CICs’ as defined under para 6 of the Master Direction DoR(NBFC).PD.003/03.10.119/2016-17 date August 25, 2016 can seek voluntary deregistration. Both audited balance sheet and auditor’s certificate are required to be submitted for the purpose.

Foreign Investment in India

Answer: There are no restrictions under FEMA for investment in Rights shares issued at a discount by an Indian company under the provisions of the Companies Act, 2013. The offer on rights basis to the persons resident outside India shall be:

-

in case of shares of a company listed on a recognized stock exchange in India, at a price, as determined by the company; and

-

in case of shares of a company not listed on a recognized stock exchange in India, at a price, which is not less than the price at which the offer on right basis is made to resident shareholders.

FAQs on Non-Banking Financial Companies

Mutual benefit financial companies (nidhis)

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

Merchants using Paytm Payments Bank to receive payments

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Procedure for submission of the FLA return

Ans: Please follow the below given step to revise the FLA return for a previous year:

Visit https://flair.rbi.org.in/fla/faces/pages/login.xhtml → Login to FLAIR → Click on MENU tab on the left-hand side of the homepage → ONLINE FLA FORM → FLA ONLINE FORM → “Please click here to get the approval to fill revised FLA form for current year after due date /previous year” → select "Year" and click on  → Click “Request”.

→ Click “Request”.

Your request status will be visible in the table below available on the screen. After sending request to RBI through FLA portal, entities need to wait for at least one working day for approval. Entities can check the status of their request in “Multiple Year Enable Screen” under menu on the left corner. Once approved by DSIM, RBI, the entity can revise FLA return for selected year.

External Commercial Borrowings (ECB) and Trade Credits

G. ALL-IN-COST

Government Securities Market in India – A Primer

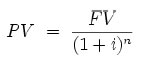

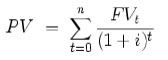

The time value of money functions related to calculation of Present Value (PV), Future Value (FV), etc. are important mathematical concepts related to bond market. An outline of the same with illustrations is provided in Box II below.

| Time Value of Money Money has time value as a Rupee today is more valuable and useful than a Rupee a year later. The concept of time value of money is based on the premise that an investor prefers to receive a payment of a fixed amount of money today, rather than an equal amount in the future, all else being equal. In particular, if one receives the payment today, one can then earn interest on the money until that specified future date. Further, in an inflationary environment, a Rupee today will have greater purchasing power than after a year. Present value of a future sum The present value formula is the core formula for the time value of money. The present value (PV) formula has four variables, each of which can be solved for: Present Value (PV) is the value at time=0

The cumulative present value of future cash flows can be calculated by adding the contributions of FVt, the value of cash flow at time=t

An illustration Taking the cash flows as;

Assuming that the interest rate is at 10% per annum; The discount factor for each year can be calculated as 1/(1+interest rate)^no. of years The present value can then be worked out as Amount x discount factor The PV of ₹100 accruing after 3 years:

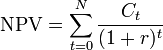

The cumulative present value = 90.91+82.64+75.13 = ₹ 248.69 Net Present Value (NPV) Net present value (NPV) or net present worth (NPW) is defined as the present value of net cash flows. It is a standard method for using the time value of money to appraise long-term projects. Used for capital budgeting, and widely throughout economics, it measures the excess or shortfall of cash flows, in present value (PV) terms, once financing charges are met. Formula Each cash inflow/outflow is discounted back to its present value (PV). Then they are summed. Therefore

Where In the illustration given above under the Present value, if the three cash flows accrues on a deposit of ₹ 240, the NPV of the investment is equal to 248.69-240 = ₹ 8.69 |

Retail Direct Scheme

Nomination related queries

Domestic Deposits

II. Deposits of Non-Residents Indians (NRIs)

Indian Currency

C) Different Types of Bank Notes and Security Features of banknotes

The details are as under:

i. Ashoka Pillar Banknotes:

The first banknote issued by independent India was the one rupee note issued in 1949. While retaining the same designs the new banknotes were issued with the symbol of Lion Capital of Ashoka Pillar at Sarnath in the watermark window in place of the portrait of King George.

The name of the issuer, the denomination and the guarantee clause were printed in Hindi on the new banknotes from the year 1951. The banknotes in the denomination of ₹1000, ₹5000 and ₹10000 were issued in the year 1954. Banknotes in Ashoka Pillar watermark Series, in ₹10 denomination were issued between 1967 and 1992, ₹20 denomination in 1972 and 1975, ₹50 in 1975 and 1981, and ₹100 between 1967-1979. The banknotes issued during the above period, contained the symbols representing science and technology, progress, orientation to Indian Art forms. In the year 1970, banknotes with the legend "Satyameva Jayate", i.e., truth alone shall prevail were introduced for the first time. In October 1987, ₹500, banknote was introduced with the portrait of Mahatma Gandhi and the Ashoka Pillar watermark.

ii. Mahatma Gandhi (MG) Series 1996

The details of banknotes issued in MG Series – 1996 is as under:

| Denomination | Month and year of introduction |

| ₹5 | November 2001 |

| ₹10 | June 1996 |

| ₹20 | August 2001 |

| ₹50 | March 1997 |

| ₹100 | June 1996 |

| ₹500 | October 1997 |

| ₹1000 | November 2000 |

All the banknotes of this series bear the portrait of Mahatma Gandhi on the obverse (front) side, in place of symbol of Lion Capital of Ashoka Pillar, which has also been retained and shifted to the left side next to the watermark window. This means that these banknotes contain Mahatma Gandhi watermark as well as Mahatma Gandhi's portrait.

iii. Mahatma Gandhi series – 2005 banknotes

MG series 2005 banknotes were issued in the denomination of ₹10, ₹20, ₹50, ₹100, ₹500 and ₹1000 and contain some additional/new security features as compared to the 1996 MG series. The year of introduction of these banknotes is as under:

| Denomination | Month and year of Introduction |

| ₹50 and ₹100 | August 2005 |

| ₹500 and ₹1000 | October 2005 |

| ₹10 | April 2006 |

| ₹20 | August 2006 |

The Legal tender of banknotes of ₹500 and ₹1000 of this series was subsequently withdrawn w.e.f. the midnight of November 8, 2016.

iv. Mahatma Gandhi (New) Series (MGNS) – Nov 2016

The Mahatma Gandhi (New) Series, introduced in the year 2016, highlights the cultural heritage and scientific achievements of the country. The banknotes in the series are more wallet friendly, being of reduced dimensions and hence expected to incur less wear and tear. For the first time, designs for banknotes has been indigenously developed on themes reflecting the diverse history, culture and ethos of the country as also its scientific achievements. The colour scheme is sharp and vivid to make the banknotes distinctive.

The first banknote from the new series was introduced on November 8, 2016 in a new denomination i.e. ₹2000 with the theme of Mangalyaan. Subsequently, banknotes in this series in denomination of ₹500, ₹200, ₹100, ₹50, ₹20, and ₹10 have also been introduced.

Coordinated Portfolio Investment Survey – India

Some important definitions and concepts

Ans: Debt securities with original maturity of one year or less is classified as short-term debt securities. Examples of short-term securities are treasury bills, negotiable certificates of deposit, bankers’ acceptances, promissory notes, and commercial paper.

All you wanted to know about NBFCs

B. Entities Regulated by RBI and applicable regulations

The resolution of stressed assets are subject to the provisions of (a) the Prudential Framework for Resolution of Stressed Assets as contained in para 18 and (b) norms on restructuring of advances as contained in para 22, 23, 24 and 25 of the Master Direction – Reserve Bank of India (Non-Banking Financial Company – Scale Based Regulation) 2023 (as amended from time to time). The acquisition of shares due to conversion of debt into equity during a restructuring process will be exempted from regulatory ceilings on capital market exposures.

Core Investment Companies

B. Registration and related matters:

Ans: Yes, company which is a CIC and has achieved the balance sheet size of ₹ 100 crore as per its last audited annual financial statement is required to apply to the Bank for registration as a CIC, subject to its meeting the other conditions for being identified as a CIC.

Foreign Investment in India

Answer: No, renunciation of rights shares shall be done in accordance with the instructions contained in Para 6.11 of Master Direction - Foreign Investment in India dated January 4, 2018, read with Regulation 6 of FEMA 20(R).

FAQs on Non-Banking Financial Companies

Mutual benefit financial companies (nidhis)

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Some Useful Definitions

Ans: Direct investment is a category of international investment in which a resident entity in one economy [Direct Investor (DI)] acquires a lasting interest in an enterprise resident in another economy [Direct Investment Enterprise (DIE)]. It consists of two components, viz., Equity Capital and Other Capital.

External Commercial Borrowings (ECB) and Trade Credits

G. ALL-IN-COST

Government Securities Market in India – A Primer

The price of a bond is nothing but the sum of present value of all future cash flows of the bond. The interest rate used for discounting the cash flows is the Yield to Maturity (YTM) (explained in detail in question no. 24) of the bond. Price can be calculated using the excel function ‘Price’ (please refer to Annex 6).

Accrued interest is the interest calculated for the broken period from the last coupon day till a day prior to the settlement date of the trade. Since the seller of the security is holding the security for the period up to the day prior to the settlement date of the trade, he is entitled to receive the coupon for the period held. During settlement of the trade, the buyer of security will pay the accrued interest in addition to the agreed price and pays the ‘consideration amount’.

An illustration is given below;

For a trade of ₹ 5 crore (face value) of security 8.83% 2023 for settlement date Jan 30, 2014 at a price of ₹100.50, the consideration amount payable to the seller of the security is worked out below:

Here the price quoted is called ‘clean price’ as the ‘accrued interest’ component is not added to it.

Accrued interest:

The last coupon date being Nov 25, 2013, the number of days in broken period till Jan 29, 2014 (one day prior to settlement date i.e. on trade day) are 65.

| The accrued interest on ₹100 face value for 65 days | = 8.83 x (65/360) |

| = ₹1.5943 |

When we add the accrued interest component to the ‘clean price’, the resultant price is called the ‘dirty price’. In the instant case, it is 100.50+1.5943 = ₹102.0943

| The total consideration amount | = Face value of trade x dirty price |

| = 5,00,00,000 x (102.0943/100) | |

| = ₹ 5,10,47,150 |

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

Merchants using Paytm Payments Bank to receive payments

Retail Direct Scheme

Nomination related queries

Domestic Deposits

II. Deposits of Non-Residents Indians (NRIs)

Indian Currency

C) Different Types of Bank Notes and Security Features of banknotes

₹500, ₹1000 and ₹10000 banknotes, which were then in circulation were demonetized in January 1946. The higher denomination banknotes in ₹1000, ₹5000 and ₹10000 were reintroduced in the year 1954, and these banknotes (₹1000, ₹5000 and ₹10000) were again demonetized in January 1978.

Recently, banknotes in the denomination of ₹500 and ₹1000 issued under the Mahatma Gandhi Series have been withdrawn from circulation with effect from the midnight of November 08, 2016, and are, therefore, no more legal tender.

As regards prohibition on holding, transferring, or receiving specified bank notes, Section 5 of The Specified Banknotes (Cessation of Liabilities) Act, 2017 reads as under:

On and from the appointed day, no person shall, knowingly or voluntarily, hold, transfer, or receive any specified bank note:

Provided that nothing contained in this section shall prohibit the holding of specified bank notes -

(a) by any person -

(i) up to the expiry of the grace period; or

(ii) after the expiry of the grace period, -

-

not more than ten notes in total, irrespective of the denomination; or

-

not more than twenty-five notes for the purposes of study, research, or numismatics.

(b) by the Reserve Bank or its agencies, or any other person authorised by the Reserve Bank;

(c) by any person on the direction of a court in relation to any case pending in the court.

Directions and Circulars issued by RBI from time to time in connection with SBNs are available on our website www.rbi.org.in under Function wise sites>>Issuer of Currency>>All You Wanted Know About SBNs - https://website.rbi.org.in/web/rbi/currency-management/all-you-wanted-to-know-about-sbns.

Coordinated Portfolio Investment Survey – India

Some important definitions and concepts

Ans: Equity securities should be reported at market prices converted to domestic currency using the exchange rate prevailing at March 31/ September 30, [Year]. For enterprises listed on a stock exchange, the market value of your holding of the equity securities should be calculated using the market price on the main stock exchange prevailing at March 31/ September 30, [Year]. For unlisted enterprises, if a market value is not available at the close of business on March 31/ September 30, [Year], estimate of the market value of your holding of equity securities can be calculated by using one of the six alternatives methods given in Q23.

Debt securities should be recorded at market prices converted to domestic currency, using the exchange rate prevailing at the close of business on March 31/ September 30, [Year]. For listed debt securities, a quoted traded market price at the close of business on March 31/ September 30, [Year], should be used. When market prices are unavailable (e.g., in the case of unlisted debt securities), the following methods for estimating fair value (which is an approximation of the market value of such instruments) should be used:

-

discounting future cash flows to the present value using a market rate of interest and

-

using market prices of financial assets and liabilities that are similar.

All you wanted to know about NBFCs

B. Entities Regulated by RBI and applicable regulations

Loans which are against the collateral of multiple securities and it is specifically agreed to in the agreement that primary security would be something other than shares/ units of mutual funds, LTV as would not be applicable. However, reporting requirements shall remain. In cases where such differentiation is not made (thereby NBFCs can off-load shares at the instance of a default), LTV would be applicable.

Core Investment Companies

C. Overseas Investments/ ECBs and related matters:

Foreign Investment in India

Answer: Yes, subject to conditions laid down in para 7.11 of the Master Direction on Foreign Investment in India.

FAQs on Non-Banking Financial Companies

Classification of NBFCs into sub-groups

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Some Useful Definitions

Ans: It covers (1) foreign equity in branches and all shares (except non-participating preference shares) in subsidiaries and associates; (2) contributions such as the provision of machinery, land & building(s) by a direct investor to a DIE by equity participation; (3) acquisition of shares by a DIE in its direct investor company, termed as reverse investment (i.e. claims on DI).

External Commercial Borrowings (ECB) and Trade Credits

G. END-USES

Government Securities Market in India – A Primer

If market interest rate levels rise, the price of a bond falls. Conversely, if interest rates or market yields decline, the price of the bond rises. In other words, the yield of a bond is inversely related to its price. The relationship between yield to maturity and coupon rate of bond may be stated as follows:

-

When the market price of the bond is less than the face value, i.e., the bond sells at a discount, YTM > > coupon yield.

-

When the market price of the bond is more than its face value, i.e., the bond sells at a premium, coupon yield > > YTM.

-

When the market price of the bond is equal to its face value, i.e., the bond sells at par, YTM = coupon yield.

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

Merchants using Paytm Payments Bank to receive payments

Retail Direct Scheme

Nomination related queries

Domestic Deposits

II. Deposits of Non-Residents Indians (NRIs)

In respect of deposit accepted in the name of –

-

member or a retired member of the bank’s staff, either singly or jointly with any other member or members of his/ her family, or

-

the spouse of a deceased member or a deceased retired member of the bank’s staff,

the bank may, in its discretion, allow additional interest at a rate not exceeding one per cent per annum over and above the rate of interest stipulated, subject to the condition that overall ceiling prescribed for FCNR(B) deposits is not breached,

Provided that –

-

the depositor or all the depositors of a joint account is/ are non-resident/s of Indian nationality or origin, and

-

the bank shall obtain a declaration from the depositor concerned that the moneys so deposited or which may, from time to time, be deposited, shall be moneys belonging to the depositor as stated in clause (a) and (b) above.

Explanation: The word “family” shall mean and include the spouse of the member/ retired member of the bank’s staff, his/her children, parents, brothers and sisters who are dependent on such a member/ retired member but shall not include a legally separated spouse.

Indian Currency

C) Different Types of Bank Notes and Security Features of banknotes

Reserve Bank of India decided to withdraw from circulation all banknotes issued prior to 2005 as they have fewer security features as compared to banknotes printed after 2005. It is a standard international practice to withdraw old series notes. The RBI has already been withdrawing these banknotes in a routine manner through banks. It is estimated that the volume of such banknotes (pre-2005) in circulation is not significant enough to impact the general public in a big way. The exchange facility for pre-2005 banknotes is available only at the following offices of the Reserve Bank: Ahmedabad, Bengaluru, Belapur, Bhopal, Bhubaneswar, Chandigarh, Chennai, Guwahati, Hyderabad, Jaipur, Jammu, Kanpur, Kolkata, Lucknow, Mumbai, Nagpur, New Delhi, Patna, Thiruvananthapuram, and Kochi. This, however, does not imply that banks cannot accept deposits of pre-2005 banknotes for crediting to the customers’ accounts. Please refer to our Press Release no. 2016-17/1565 dated December 19, 2016 in this regard which can be accessed at the following link https://website.rbi.org.in/en/web/rbi/-/press-releases/banks-should-accept-pre-2005-banknotes-in-deposit-rbi-clarifies-38951.

Coordinated Portfolio Investment Survey – India

Some important definitions and concepts

Ans: When actual market values are not available, an estimate is required. Alternative methods of approximating market value of shareholders’ equity in a direct investment enterprise include the following:

-

Recent transaction price: Unlisted instruments may trade from time to time, and recent prices, within the past year, at which they were traded may be used. Recent prices are a good indicator of current market values to the extent that conditions are unchanged. This method can be used as long as there has been no material change in the corporation’s position since the transaction date. Recent transaction prices become increasingly misleading as time passes and conditions change.

-

Net asset value: Appraisals of untraded equity may be conducted by knowledgeable management or directors of the enterprise or provided by independent auditors to obtain total assets at current value less total liabilities (excluding equity) at market value. Valuations should be recent (within the past year) and should preferably include intangible assets.

-

Present value and price-to-earnings ratios: The present value of unlisted equity can be estimated by discounting the forecast future profits. At its simplest, this method can be approximated by applying a market or industry price-to-earnings ratio to the (smoothed) recent past earnings of the unlisted enterprise to calculate a price. This method is most appropriate in which there is a paucity of balance sheet information but earnings data are more readily available.

-

Market capitalization method: Book values reported by enterprises can be adjusted at an aggregate level by the statistical compiler. For untraded equity, information on “own funds at book value” can be collected from enterprises, and then adjusted with ratios based on suitable price indicators, such as the ratio of market capitalization to book value for listed companies in the same economy with similar operations. Alternatively, assets that enterprises carry at cost (such as land, plant, equipment, and inventories) can be revalued to current period prices using suitable asset price indices.

-

Own funds at book value: This method for valuing equity uses the value of the enterprise recorded in the books of the direct investment enterprise, as the sum of (a) paid-up capital (excluding any shares on issue that the enterprise holds in itself and including share premium accounts); (b) all types of reserves identified as equity in the enterprise’s balance sheet (including investment grants when accounting guidelines consider them company reserves); (c) cumulated reinvested earnings; and (d) holding gains or losses included in own funds in the accounts, whether as revaluation reserves or profits or losses. The more frequent the revaluation of assets and liabilities, the closer the approximation to market values. Data that are not revalued for several years may be a poor reflection of market values.

-

Apportioning global value: The current market value of the global enterprise group can be based on the market price of its shares on the exchange on which its equity is traded, if it is a listed company. Where an appropriate indicator may be identified (e.g., sales, net income, assets, or employment), the global value may be apportioned to each economy in which it has direct investment enterprises, on the basis of that indicator, by making the assumption that the ratio of net market value to sales, net income, assets, or employment is a constant throughout the transnational enterprise group. (Each indicator could yield significantly different results from the others).

All you wanted to know about NBFCs

B. Entities Regulated by RBI and applicable regulations

Core Investment Companies

C. Overseas Investments/ ECBs and related matters:

Ans: The Directions on CICs have not restricted them from making overseas investment. Such investment will be governed by the provisions of Chapter IX of Master Direction DoR(NBFC).PD.003/03.10.119/2016-17 dated August 25, 2016. Similarly, presently CICs can raise funds through ECB. The same would be governed by the instructions contained in the ECB Policy issued by Foreign Exchange Department of the Reserve Bank. Lending to NBFCs/ CICs by banks will be governed by the provisions as applicable to banks and specifically contained in the instructions on ‘bank finance to NBFCs’ issued by Department of Banking Regulation of the Reserve Bank.

Foreign Investment in India

Answer: The following persons can acquire capital instruments on the stock exchanges:

-

FPIs registered with SEBI

-

NRIs

-

Other than (a) and (b) above, a person resident outside India, can acquire capital instruments on stock exchange, subject to the condition that the investor has already acquired and continues to hold the control of such company in accordance with SEBI (Substantial Acquisition of Shares and Takeover) Regulations and subject to conditions specified in Annex I of the Master Direction – Foreign Investment in India.

রিজার্ভ ব্যাঙ্ক অফ ইন্ডিয়া মোবাইল অ্যাপ্লিকেশন ইনস্টল করুন এবং সাম্প্রতিক সংবাদগুলিতে দ্রুত অ্যাক্সেস পান!