IST,

IST,

Bank Lending Survey for Q1:2021-22

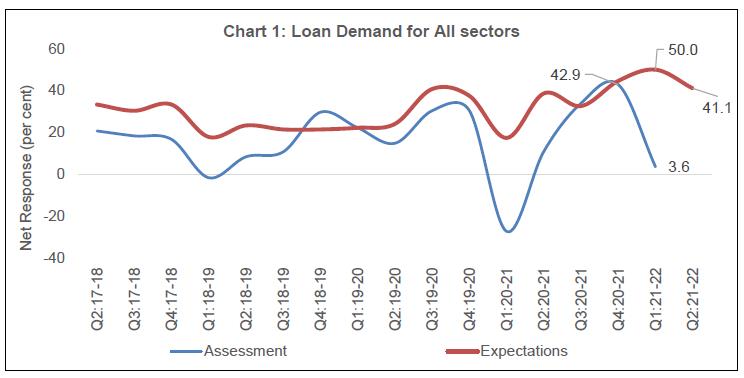

Today, the Reserve Bank released results of 16th round of its quarterly bank lending survey (BLS)1. This forward-looking survey is being conducted since Q2:2017-18 to capture the qualitative assessment and expectations of major scheduled commercial banks (SCBs) on credit parameters (viz., loan demand, terms and conditions of loans) for major economic sectors2. The latest round of the survey, conducted during Q1:2021-22, collected senior loan officers’ assessment of credit parameters for Q1:2021-22 and expectations for Q2:2021-223. Owing to uncertainty driven by the COVID-19 pandemic, an additional block was included in this round of the survey for assessing outlook for two quarters as well as three quarters ahead. Highlights: A. Assessment for Q1:2021-22

B. Expectations for Q2:2021-22

C. Expectations for Q3:2021-22 and Q4:2021-22

Note: Please see the excel file for time series data. 1 The results of 15th round of the BLS with reference period as January-March 2021 were released on the RBI website on April 7, 2021. 2 The survey questionnaire is canvassed among major 30 SCBs accounting for more than 90 per cent of credit by SCBs in India. 3 The survey results reflect the views of the respondents, which are not necessarily shared by the Reserve Bank of India. 4 Net Response (NR) is computed as the difference of percentage of banks reporting increase/optimism and those reporting decrease/pessimism in respective parameter. The weights of +1.0, 0.5, 0, -0.5 and -1.0 are assigned for computing NR from aggregate per cent responses on 5-point scale i.e. substantial increase/ considerable easing, moderate increase/ somewhat easing, no change, moderate decrease/ somewhat tightening, substantial decrease/ considerable tightening for loan demand/loan terms and conditions parameters respectively. NR ranges between -100 to 100. Any value greater than zero indicates expansion/optimism and any value less than zero indicates contraction/pessimism. Increase in loan demand is considered optimism (Tables 1), while for loan terms and conditions, a positive value of net response indicates easy terms and conditions (Table 2). | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Share this page:

Install the RBI mobile application and get quick access to the latest news!

Scan the QR code to install our app

Page Last Updated on: