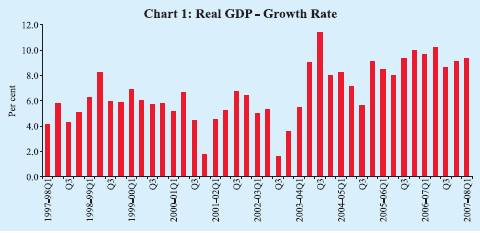

The Indian economy continued to maintain strong growth momentum during the first quarter of 2007-08, underpinned by sustained performances of the manufacturing and services sectors which continued to register double-digit growth. According to the estimates released by the Central Statistical Organisation (CSO) in August 2007, real GDP growth remained high at 9.3 per cent during the first quarter of 2007-08 on top of 9.6 per cent during the same period in 2006-07 (Table 1 and Chart 1). A positive feature was a recovery in the agricultural sector which recorded an increase of one percentage point over the corresponding quarter of the previous year.

Table 1: Growth Rates of Real GDP |

(Per cent) |

Sector |

2000-01to 2006-07

(Average) |

2004-05 |

2005-06* |

2006-07# |

2006-07 |

2007-08 |

|

|

|

|

|

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

10 |

1. |

Agriculture and |

2.5 |

0.0 |

6.0 |

2.7 |

2.8 |

2.9 |

1.6 |

3.8 |

3.8 |

|

Allied Activities |

(21.4) |

(20.2) |

(19.7) |

(18.5) |

|

|

|

|

|

2. |

Industry |

7.0 |

8.4 |

8.0 |

11.0 |

10.6 |

11.3 |

10.8 |

11.2 |

10.6 |

|

|

|

(19.6) |

(19.6) |

(19.4) |

(19.7) |

|

|

|

|

|

|

2.1 |

Mining and Quarrying |

4.6 |

7.5 |

3.6 |

5.1 |

3.7 |

3.9 |

5.5 |

7.1 |

3.2 |

|

2.2 |

Manufacturing |

7.7 |

8.7 |

9.1 |

12.3 |

12.3 |

12.7 |

11.8 |

12.4 |

11.9 |

|

2.3 |

Electricity, Gas and |

|

|

|

|

|

|

|

|

|

|

|

Water Supply |

4.8 |

7.5 |

5.3 |

7.4 |

5.8 |

8.1 |

9.1 |

6.9 |

8.3 |

3. |

Services |

8.6 |

10.0 |

10.3 |

11.0 |

11.6 |

11.7 |

10.9 |

10.0 |

10.6 |

|

|

|

(59.0) |

(60.2) |

(60.9) |

(61.8) |

|

|

|

|

|

|

3.1 |

Trade, Hotels, |

|

|

|

|

|

|

|

|

|

|

|

Restaurants, Transport, |

|

|

|

|

|

|

|

|

|

|

|

Storage and |

|

|

|

|

|

|

|

|

|

|

|

Communication |

10.3 |

10.9 |

10.4 |

13.0 |

12.4 |

14.2 |

13.1 |

12.4 |

12.0 |

|

3.2 |

Financing, Insurance, |

|

|

|

|

|

|

|

|

|

|

|

Real Estate and |

|

|

|

|

|

|

|

|

|

|

|

Business Services |

7.9 |

8.7 |

10.9 |

10.6 |

10.8 |

11.1 |

11.2 |

9.3 |

11.0 |

|

3.3 |

Community, Social and |

|

|

|

|

|

|

|

|

|

|

|

Personal services |

6.0 |

7.9 |

7.7 |

7.8 |

11.3 |

8.3 |

6.7 |

5.7 |

7.6 |

|

3.4 |

Construction |

9.9 |

14.1 |

14.2 |

10.7 |

10.5 |

11.1 |

10 |

11.2 |

10.7 |

4. |

Real GDP at Factor Cost |

6.9 |

7.5 |

9.0 |

9.4 |

9.6 |

10.2 |

8.7 |

9.1 |

9.3 |

|

|

|

(100) |

(100) |

(100) |

(100) |

|

|

|

|

|

Memo: |

(Amount in Rupees crore) |

a) |

Real GDP at factor cost |

|

23,89,660 |

26,04,532 |

28,48,157 |

|

|

|

|

|

|

(1999-2000) |

|

|

|

|

|

|

|

|

|

b) |

GDP at current market prices |

|

31,26,596 |

35,67,177 |

41,25,725 |

|

|

|

|

|

* : Quick Estimates.

# : Revised Estimates.

Note : Figures in parentheses denote shares in real GDP.

Source : Central Statistical Organisation. |

Agricultural Situation

The cumulative rainfall during the South-West monsoon season 2007 (June to September) was 5 per cent above normal as compared to one per cent below normal during the corresponding period of the previous year. The South-West monsoon set in over Kerala on May 28, 2007, four days in advance of the normal date of onset over the State. After a brief spell of hiatus during early June due to the formation of a super cyclone “Gonu” over the East-Central Arabian Sea, the South-West monsoon covered the North-Eastern States by June 10, 2007, peninsular and central India by June 25, 2007 and subsequently the entire country by July 4, 2007, nearly 11 days ahead of the normal schedule. Of the 36 meteorological sub-divisions, cumulative rainfall was deficient in 6 sub-divisions (10 sub-divisions during last year) (Table 2). As on October 18, 2007, the total live water storage of 81 important reservoirs1 was 81 per cent of the Full Reservoir Level (FRL), lower than that of 83 per cent last year but higher than the average of 68 per cent for the past 10 years.

The area coverage of kharif crops has increased during 2007-08 (as on October 12, 2007) with reported sown area of 103.8 per cent of the normal, which was about 3.1 per cent higher than the previous year. While foodgrain crops such as pulses and rice have shown improvement in area sown, coarse grains witnessed a decline (Table 3). Among non-foodgrains, while area covered under oilseeds, sugarcane, cotton and jute increased, that under mesta declined.

The Ministry of Agriculture has set targets for foodgrains, pulses and oilseeds production for 2007-08 at 221.5 million tonnes, 15.5 million tonnes

Table 2: Rainfall – South-West Monsoon (June-September) |

Year |

Cumulative Rainfall: |

Spatial Distribution |

|

Above(+)/

Below (-)

Normal

(per cent) |

(Number of Sub-Divisions) |

|

|

Excess

Rainfall |

Normal

Rainfall |

Deficient

Rainfall |

Scanty/

No Rain |

1 |

2 |

3 |

4 |

5 |

6 |

2000 |

-8 |

5 |

23 |

8 |

0 |

2001 |

-8 |

1 |

30 |

5 |

0 |

2002 |

-19 |

1 |

14 |

19 |

2 |

2003 |

2 |

7 |

26 |

3 |

0 |

2004 |

-13 |

0 |

23 |

13 |

0 |

2005 |

-1 |

9 |

23 |

4 |

0 |

2006 |

-1 |

6 |

20 |

10 |

0 |

2007 |

5 |

13 |

17 |

6 |

0 |

Excess : +20 per cent or more. Normal : +19 per cent to -19 per cent.

Deficient : -20 per cent to -59 per cent. Scanty : -60 per cent to -99 per cent.

No Rain : -100 per cent.

Source : India Meteorological Department. |

and 30 million tonnes, respectively. Reflecting the good rainfall and increase in area sown, total kharif foodgrains production during 2007-08, at 112.2 million tonnes (according to the First Advance Estimates), is likely to be 1.6 per cent higher than the previous year. Production of oilseeds, pulses, cotton and sugarcane is also expected to show improvement over the previous year. Kharif foodgrains production is, however, expected to fall short of the target of 114.2 million tonnes on account of coarse cereals. While kharif production of oilseeds is expected to

Table 3: Progress of Area under Kharif Crops - 2007-08 |

(Million hectares) |

Crop |

Normal |

Area Coverage

(as on October 12, 2007) |

|

Area |

2006 |

2007 |

Variation |

1 |

2 |

3 |

4 |

5 |

Rice |

38.2 |

36.9 |

37.2 |

0.3 |

Coarse Cereals |

22.9 |

22.1 |

22.0 |

-0.1 |

of which: |

|

|

|

|

Bajra |

9.4 |

9.3 |

8.7 |

-0.6 |

Jowar |

4.4 |

3.8 |

3.6 |

-0.2 |

Maize |

6.2 |

6.8 |

7.5 |

0.6 |

Total Pulses |

10.9 |

11.4 |

12.5 |

1.2 |

Total Oilseeds |

15.4 |

16.5 |

17.6 |

1.1 |

of which: |

|

|

|

|

Groundnut |

5.5 |

4.8 |

5.4 |

0.7 |

Soyabean |

6.6 |

8.1 |

8.8 |

0.6 |

Sugarcane |

4.2 |

4.8 |

5.1 |

0.3 |

Cotton |

8.3 |

8.9 |

9.3 |

0.4 |

All Crops |

100.8 |

101.5 |

104.7 |

3.2 |

Source : Ministry of Agriculture, Government of India. |

Table 4: Agricultural Production |

(Million tonnes) |

Crop |

2003-04 |

2004-05 |

2005-06 |

2006-07* |

2007-08 |

|

|

|

|

|

|

T |

A @ |

1 |

|

2 |

3 |

4 |

5 |

6 |

7 |

Rice |

88.5 |

83.1 |

91.8 |

92.8 |

93.0 |

|

|

Kharif |

78.6 |

72.2 |

78.3 |

80.1 |

80.0 |

80.2 |

|

Rabi |

9.9 |

10.9 |

13.5 |

12.7 |

13.0 |

|

Wheat |

72.2 |

68.6 |

69.4 |

74.9 |

75.5 |

|

Coarse Cereals |

37.6 |

33.5 |

34.1 |

34.3 |

37.5 |

|

|

Kharif |

32.2 |

26.4 |

26.7 |

25.7 |

28.7 |

26.6 |

|

Rabi |

5.4 |

7.1 |

7.3 |

8.6 |

8.8 |

|

Pulses |

14.9 |

13.1 |

13.4 |

14.2 |

15.5 |

|

|

Kharif |

6.2 |

4.7 |

4.9 |

4.7 |

5.5 |

5.5 |

|

Rabi |

8.7 |

8.4 |

8.5 |

9.5 |

10.0 |

|

Total Foodgrains |

213.2 |

198.4 |

208.6 |

216.1 |

221.5 |

|

|

Kharif |

117.0 |

103.3 |

109.9 |

110.5 |

114.2 |

112.2 |

|

Rabi |

96.2 |

95.1 |

98.7 |

105.6 |

107.3 |

|

Total Oilseeds |

25.2 |

24.4 |

28.0 |

23.9 |

30.0 |

|

|

Kharif |

16.7 |

14.1 |

16.8 |

13.9 |

18.5 |

16.1 |

|

Rabi |

8.5 |

10.2 |

11.2 |

9.9 |

11.5 |

|

Sugarcane |

233.9 |

237.1 |

281.2 |

345.3 |

310.0 |

345.6 |

Cotton # |

13.7 |

16.4 |

18.5 |

22.7 |

22.0 |

22.9 |

Jute and Mesta ## |

11.2 |

10.3 |

10.8 |

11.3 |

11.0 |

11.3 |

T : Target. A : Achievement.

* : Fourth Advance Estimates as on July 19, 2007.

@ : First Advance Estimate as on September 19, 2007.

# : Million bales of 170 kgs each. ## : Million bales of 180 kgs each.

Source : Ministry of Agriculture, Government of India. |

be lower than the target for 2007-08, output of cotton and sugarcane is expected to exceed the targets (Table 4).

Food Management

Total procurement of rice and wheat during 2007-08 (up to October 16, 2007) aggregated 19.5 million tonnes, which was lower by 1.9 per cent than the corresponding period of 2006-07. While rice procurement declined by 21.4 per cent, wheat procurement increased by 20.6 per cent over the previous year. Total off-take of rice and wheat during 2007-08 (up to June 30, 2007) at 8.9 million tonnes was lower by 4.1 per cent than that of the corresponding period of the previous year. As on July 1, 2007, total stocks of foodgrains with the Food Corporation of India (FCI) and other Government agencies were at 23.9 million tonnes, which were higher by 16.6 per cent than those in the previous year (20.5 million tonnes) (Table 5). While the stocks of rice at 11.0 million tonnes were higher than the buffer stock norm of 9.8 million tonnes, those of wheat at 12.9 million tonnes were lower than the buffer stock norm of 17.1 million tonnes.

Table 5: Management of Food Stocks |

(Million tonnes) |

|

Opening Stock of Foodgrains |

Procurement of Foodgrains |

Foodgrains Off-take |

Closing

Stock |

Norms |

Month |

Rice |

Wheat |

Total |

Rice |

Wheat |

Total |

PDS |

OWS |

OMS -

Domestic |

Exports |

Total |

|

|

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

10 |

11 |

12 |

13 |

14 |

2004-05 |

13.1 |

6.9 |

20.7 |

24.0 |

16.8 |

40.8 |

29.7 |

10.6 |

0.2 |

1.0 |

41.5 |

18.0 |

|

2005-06 |

13.3 |

4.1 |

18.0 |

26.9 |

14.8 |

41.7 |

31.4 |

9.8 |

1.1 |

0.0 |

42.2 |

16.6 |

|

2006-07 |

13.7 |

2.0 |

16.6 |

26.7 |

9.2 |

35.9 |

31.6 |

5.1 |

0.0 |

0.0 |

36.8 |

17.8 |

|

2006-07@ |

13.7 |

2.0 |

16.6 |

10.7 |

9.2 |

19.9 |

7.9 |

1.4 |

0.0 |

0.0 |

9.3 |

|

|

2007-08@ |

13.2 |

4.6 |

17.8 |

8.4 |

11.1 |

19.5 |

8.1 |

0.8 |

0.0 |

0.0 |

8.9 |

|

|

2006 |

|

|

|

|

|

|

|

|

|

|

|

|

|

April |

13.7 |

2.0 |

16.6 |

1.7 |

8.7 |

10.3 |

2.5 |

0.3 |

0.0 |

0.0 |

2.8 |

22.8 |

16.2 |

May |

12.8 |

9.0 |

22.8 |

1.6 |

0.6 |

2.2 |

2.5 |

0.4 |

0.0 |

0.0 |

3.0 |

22.3 |

|

June |

12.0 |

9.3 |

22.3 |

1.5 |

0.0 |

1.5 |

2.5 |

0.6 |

0.0 |

0.0 |

3.1 |

20.5 |

|

July |

11.1 |

8.2 |

20.5 |

0.8 |

0.0 |

0.8 |

2.7 |

0.4 |

0.0 |

0.0 |

3.1 |

17.1 |

26.9 |

August |

9.5 |

7.3 |

17.1 |

0.5 |

0.0 |

0.5 |

2.7 |

0.4 |

0.0 |

0.0 |

3.1 |

15.5 |

|

September |

7.8 |

6.7 |

15.5 |

0.2 |

0.0 |

0.2 |

2.3 |

0.5 |

0.0 |

0.0 |

2.8 |

12.6 |

|

October |

6.0 |

6.4 |

12.6 |

8.0 |

0.0 |

8.0 |

2.4 |

0.3 |

0.0 |

0.0 |

2.7 |

18.7 |

16.2 |

November |

12.5 |

6.0 |

18.7 |

2.0 |

0.0 |

2.0 |

2.5 |

0.4 |

0.0 |

0.0 |

2.9 |

17.8 |

|

December |

12.1 |

5.6 |

17.8 |

2.6 |

0.0 |

2.6 |

2.6 |

0.3 |

0.0 |

0.0 |

3.0 |

17.5 |

|

2007 |

|

|

|

|

|

|

|

|

|

|

|

|

|

January |

12.0 |

5.4 |

17.5 |

4.3 |

0.0 |

4.3 |

2.7 |

0.4 |

0.0 |

0.0 |

3.1 |

18.1 |

20.0 |

February |

12.6 |

5.4 |

18.1 |

2.4 |

0.0 |

2.4 |

2.7 |

0.5 |

0.0 |

0.0 |

3.1 |

19.1 |

|

March |

14.0 |

5.1 |

19.1 |

1.2 |

0.0 |

1.2 |

2.7 |

0.5 |

0.0 |

0.0 |

3.2 |

17.8 |

|

April |

13.2 |

4.6 |

17.8 |

0.9 |

7.9 |

8.7 |

2.5 |

0.2 |

0.0 |

0.0 |

2.8 |

25.1 |

16.2 |

May |

13.5 |

11.6 |

25.1 |

1.5 |

2.6 |

4.0 |

2.8 |

0.2 |

0.0 |

0.0 |

3.0 |

25.9 |

|

June |

12.6 |

13.3 |

25.9 |

1.3 |

0.7 |

2.0 |

3.7 |

0.4 |

0.0 |

0.0 |

3.1 |

23.9 |

|

July |

11.0 |

12.9 |

23.9 |

0.8 |

0.0 |

0.8 |

– |

– |

– |

– |

– |

– |

26.9 |

August |

– |

– |

– |

0.1 |

0.0 |

0.1 |

– |

– |

– |

– |

– |

– |

|

September |

– |

– |

– |

0.1 |

0.0 |

0.1 |

– |

– |

– |

– |

– |

– |

|

October* |

– |

– |

– |

3.8 |

0.0 |

3.8 |

– |

– |

– |

– |

– |

– |

16.2 |

PDS : Public Distribution System. OWS : Other Welfare Schemes. OMS : Open Market Sales. – : Not Available.

@ : Procurement up to October 16 and offtake up to June 30.

* : Procurement up to October 16, 2007.

Note : Closing stock figures may differ from those arrived at by adding the opening stocks and

procurement and deducting offtake, as stocks include coarse grains also.

Source : Ministry of Consumer Affairs, Food and Public Distribution, Government of India.

|

Industrial Performance

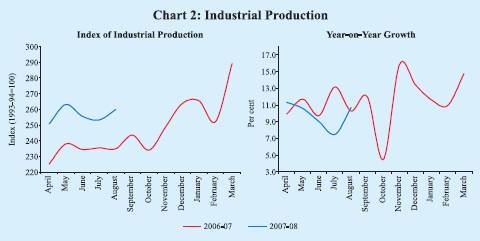

During April-August 2007, the index of industrial production rose by 9.8 per cent as compared with a growth of 11.0 per cent recorded during the corresponding period of the previous year (Chart 2). The manufacturing sector registered a growth of 10.3 per cent during April-August 2007 on top of 12.2 per cent during April-August 2006. Growth rates in the mining and electricity sectors were higher at 5.4 per cent and 8.3 per cent, respectively, than a year ago (Table 6). Electricity sector registered the highest growth since 1998-99.

The moderation in the growth of manufacturing sector during April-August 2007 was on account of deceleration/negative growth in 12 out of 17 manufacturing industry groups, which account for 60.1 per cent weight in the manufacturing

index (Table 7). ‘Chemicals and chemical products except products of petroleum and coal’, ‘machinery and equipment’, ‘basic metal and alloy industries’, ‘non-metallic mineral products’, ‘cotton textiles’ and ‘transport equipment and parts’ are among the major groups which registered a deceleration in growth, largely due to base effect. ‘Metal products and parts’ recorded a decline due to slowdown in the production of tin metal containers, welded link chains and razor blades.

Table 6: Index of Industrial Production – Sectoral and Use-Based Classification |

(Per cent) |

Industry Group |

Weight

in the IIP |

Growth Rate |

Weighted Contribution # |

|

|

April-March |

April-August |

April-March |

April-August |

|

|

2006-07 |

2006-07 |

2007-08 P |

2006-07 |

2006-07 |

2007-08 P |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

Sectoral |

|

|

|

|

|

|

|

Mining |

10.5 |

5.3 |

3.0 |

5.4 |

3.4 |

2.0 |

3.8 |

Manufacturing |

79.4 |

12.5 |

12.2 |

10.3 |

91.1 |

93.3 |

88.8 |

Electricity |

10.2 |

7.3 |

5.7 |

8.3 |

5.5 |

4.8 |

7.4 |

Use-Based |

|

|

|

|

|

|

|

Basic Goods |

35.6 |

10.3 |

8.3 |

10.0 |

27.2 |

23.4 |

30.7 |

Capital Goods |

9.3 |

18.2 |

19.5 |

21.3 |

17.6 |

18.1 |

23.8 |

Intermediate Goods |

26.5 |

12.0 |

10.4 |

9.3 |

27.0 |

25.7 |

25.7 |

Consumer Goods (a+b) |

28.7 |

10.1 |

11.4 |

6.2 |

28.5 |

33.0 |

20.2 |

a) Consumer Durables |

5.4 |

9.2 |

16.1 |

-2.3 |

6.7 |

11.9 |

-2.0 |

b) Consumer Non-durables |

23.3 |

10.4 |

9.8 |

9.3 |

21.8 |

21.1 |

22.2 |

General |

100.0 |

11.5 |

11.0 |

9.8 |

100.0 |

100.0 |

100.0 |

P : Provisional. # : Figures may not add up to 100 due to rounding off.

Source : Central Statistical Organisation. |

Table 7: Growth of Manufacturing Groups |

(Per cent) |

Industry Group |

Weight |

Growth Rate |

Weighted Contribution # |

|

|

in the IIP |

April-March |

April-August |

April-March |

April-August |

|

|

|

2006-07 |

2006-07 |

2007-08 P |

2006-07 |

2006-07 |

2007-08 P |

1 |

|

2 |

3 |

4 |

5 |

6 |

7 |

8 |

1. |

Machinery and equipment |

|

|

|

|

|

|

|

|

other than transport equipment |

9.6 |

14.2 |

16.7 |

13.4 |

18.3 |

20.2 |

20.7 |

2. |

Basic metal and alloy Industries |

7.5 |

22.9 |

21.5 |

19.4 |

16.6 |

14.9 |

17.8 |

3. |

Chemicals and chemical products |

|

|

|

|

|

|

|

|

except products of petroleum and coal |

14.0 |

9.4 |

10.8 |

7.9 |

14.6 |

17.8 |

15.6 |

4. |

Non-metallic mineral products |

4.4 |

12.9 |

13.0 |

8.3 |

6.6 |

6.7 |

5.2 |

5. |

Beverages, tobacco and related products |

2.4 |

11.3 |

12.6 |

8.3 |

4.7 |

5.3 |

4.3 |

6. |

Other manufacturing industries |

2.6 |

7.7 |

24.7 |

9.3 |

2.4 |

6.5 |

3.3 |

7. |

Cotton textiles |

5.5 |

14.8 |

13.1 |

6.4 |

4.8 |

4.4 |

2.6 |

8. |

Transport equipment and parts |

4.0 |

15.0 |

20.4 |

2.3 |

8.2 |

10.5 |

1.5 |

9. |

Textile products |

|

|

|

|

|

|

|

|

(including wearing apparel) |

2.5 |

11.5 |

19.4 |

3.8 |

3.2 |

5.3 |

1.4 |

10. |

Wool, silk and man-made fibre textiles |

2.3 |

8.1 |

7.3 |

4.0 |

2.0 |

1.8 |

1.2 |

11. |

Paper and paper products and printing, |

|

|

|

|

|

|

|

|

publishing and allied activities |

2.7 |

8.4 |

10.7 |

0.8 |

2.2 |

2.9 |

0.2 |

12. |

Metal products and parts |

|

|

|

|

|

|

|

|

(except machinery and equipment) |

2.8 |

11.4 |

5.5 |

-1.7 |

2.3 |

1.1 |

-0.4 |

13. |

Food products |

9.1 |

8.7 |

-1.9 |

16.4 |

5.8 |

-1.1 |

9.7 |

14. |

Rubber, plastic, petroleum and |

|

|

|

|

|

|

|

|

coal products |

5.7 |

12.7 |

8.8 |

12.6 |

6.3 |

4.5 |

7.8 |

15. |

Wood and wood products, |

|

|

|

|

|

|

|

|

furniture and fixtures |

2.7 |

29.1 |

-2.1 |

80.1 |

2.4 |

-0.2 |

7.6 |

16. |

Leather and leather and fur products |

1.1 |

0.4 |

-7.9 |

7.8 |

0.0 |

-0.7 |

0.7 |

17. |

Jute and other vegetable fibre textiles |

|

|

|

|

|

|

|

|

(except cotton) |

0.6 |

-15.8 |

2.5 |

22.3 |

-0.4 |

0.1 |

0.6 |

|

Manufacturing – Total |

79.4 |

12.5 |

12.2 |

10.3 |

100.0 |

100.0 |

100.0 |

P : Provisional. # : Figures may not add up to 100 due to rounding off.

Source : Central Statistical Organisation. |

‘Food products’, ‘wood and wood products’ and ‘leather and leather and fur products’, however, made a turnaround to register positive growth rates.

In terms of use-based classification, the basic and capital goods sectors witnessed strong growth during April-August 2007 (see Table 6). The basic goods sector benefited from the accelerated growth of the electricity sector and increased production of high speed diesel, caustic soda and some steel products. The growth in the capital goods sector was supported by strong investment demand. The growth in intermediate goods sector, however, moderated due to decline in the production of certain industries such as chemicals, metal and petroleum products. Consumer goods sector slowed down significantly due to the decline in the consumer durables segment, particularly in production of telephone instruments, television receivers, motor cycles and wrist watches.

Infrastructure

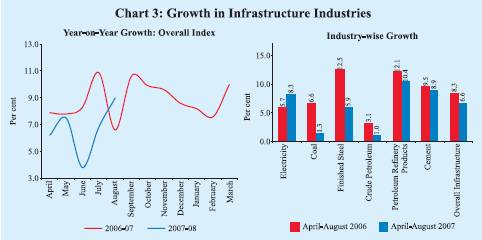

During April-August 2007, the infrastructure sector recorded a growth of 6.6 per cent as compared with 8.3 per cent a year ago, with five of the six core infrastructure industries registering a deceleration (Chart 3). The electricity sector was the only sector which recorded a higher growth than a year ago on account of increased plant load factor (PLF) in thermal power plants at 77.1 per cent during April-August 2007 (74.5 per cent during April-August 2006) and double-digit growth in power generation of hydropower plants. Moderation of growth in petroleum refinery products, cement and steel sectors could be attributed to base effect and capacity constraints. Decline in crude oil production reflected the decline in production in some of the ONGC oilfields such as Bassein, Neelam and Gujarat fields.

Services Sector

The services sector continued to record double-digit growth (10.6 per cent in April-June 2007 on top of 11.6 per cent in April-June 2006), driving the growth momentum of the economy. Services sector activity continued to be led by the sub-sector ‘trade, hotel, transport and communication’ (Table 8). This sub-sector recorded a growth of 12.0 per cent in the first quarter of 2007-08, contributing nearly 33.6 per cent to the overall real GDP growth of 9.3 per cent during the quarter. ‘Financing, insurance, real estate and business services’ recorded a growth of 11.0 per cent during April-June 2007 (10.8 per cent a year ago). The construction sector also recorded a higher growth at 10.7 per cent during the first quarter of 2007-08 than a year ago.

Table 8: Growth in Services Sectors |

(Contribution to real GDP growth; percentage points) |

Year/Quarter |

Construction |

Trade,

Hotels, |

Financing,

Insurance, |

Community,

Social |

Total

Services |

|

|

Transport, and

Communication |

Real Estate and

Business Services |

and Personal

Services |

|

1 |

2 |

3 |

4 |

5 |

6 |

2000-01 |

0.4 |

1.6 |

0.5 |

0.7 |

3.2 |

2001-02 |

0.2 |

2.0 |

0.9 |

0.6 |

3.8 |

2002-03 |

0.5 |

2.1 |

1.1 |

0.6 |

4.2 |

2003-04 |

0.7 |

2.9 |

0.8 |

0.8 |

5.2 |

2004-05 |

0.9 |

2.7 |

1.2 |

1.1 |

5.9 |

2005-06 |

0.9 |

2.7 |

1.5 |

1.1 |

6.2 |

2006-07 |

0.7 |

3.4 |

1.5 |

1.1 |

6.7 |

2006-07: Q1 |

0.7 |

3.2 |

1.5 |

1.6 |

7.0 |

2006-07: Q2 |

0.8 |

3.7 |

1.6 |

1.3 |

7.4 |

2006-07: Q3 |

0.7 |

3.3 |

1.4 |

0.9 |

6.3 |

2006-07: Q4 |

0.8 |

3.4 |

1.3 |

0.8 |

6.2 |

2007-08: Q1 |

0.7 |

3.1 |

1.6 |

1.1 |

6.5 |

Leading indicators of services sector activity for April-August 2007 show that cargo handled at major ports and import cargo handled by civil aviation witnessed strong growth. Growth rates in commercial vehicles production, new cell phone connections, passengers handled by civil aviation and steel have moderated during 2007-08 (April-August), albeit over a high base (Table 9).

Table 9: Indicators of Services Sector Activity |

(Growth rates in per cent) |

Item |

2005-06 |

2006-07 |

April-August |

|

|

|

2006 |

2007 |

1 |

2 |

3 |

4 |

5 |

Tourist arrivals |

13.8 |

13.0 |

14.3 @ |

10.8 @ |

Commercial vehicles production* |

10.6 |

33.0 |

33.5 |

3.1 |

Railway revenue earning freight traffic |

10.7 |

9.2 |

9.9 |

7.0 |

New cell phone connections |

89.4 |

85.4 |

120.9 |

52.9 |

Cargo handled at major ports |

10.4 |

9.5 |

6.0 |

14.2 |

Civil aviation |

|

|

|

|

a) Export cargo handled |

7.3 |

3.6 |

5.9 |

5.4 |

b) Import cargo handled |

15.8 |

19.4 |

21.2 |

23.5 |

c) Passengers handled at international terminals |

12.8 |

12.1 |

12.9 |

12.4 |

d) Passengers handled at domestic terminals |

27.1 |

34.0 |

40.1 |

27.8 |

Cement** |

12.4 |

9.1 |

9.5 |

8.9 |

Steel** |

10.8 |

11.7 |

12.5 |

5.9 |

Aggregate deposits |

18.1 |

23.7 |

8.5 # |

9.6 # |

Non-food credit |

31.8 |

28.4 |

9.4 # |

5.3 # |

@ : April-September

# : Up to October 12.

* : Leading indicator for transportation.

** : Leading indicators for construction.

Sources : Ministry of Tourism, Ministry of Commerce and Industry, Ministry of Statistics and

Programme Implementation, Reserve Bank of India and Centre for Monitoring Indian Economy. |

Aggregate Demand

Estimates of expenditure of GDP for the first quarter of 2007-08 vis-a-vis the corresponding quarter of the previous year indicate that the growth remained domestic demand driven. The share of real private final consumption expenditure in total output declined from 60.8 per cent in 2006-07 to 58.8 per cent in the first quarter of 2007-08, while that of real gross fixed capital formation (GFCF) rose from 27.9 per cent to 29.6 per cent during the same period. Real GFCF rose by 15.9 per cent during the first quarter of 2007-08 as compared with 15.8 per cent during the corresponding quarter of the previous year. Total final consumption expenditure, both private and government, decelerated during this period indicating dominance of investment demand (Table 10). Around 37 per cent of the incremental growth in real GDP during April-June 2007 was on account of private final consumption demand (49.6 per cent during April-June 2006), while around 48 per cent (50.7 per cent a year ago) was on account of the rise in real GFCF.

Corporate Performance

The corporate sector continued to show impressive performance during the first quarter of 2007-08, notwithstanding some deceleration in the growth of sales and profits over the corresponding quarter of 2006-07 (Table 11). Net profits of select non-Government non-financial companies rose by 33.9 per cent, benefiting from the rise in other income and the lower rise in interest payments. Buoyant asset markets and hedging gains at the back of appreciating Indian rupee appears to have helped corporates to record marked increase in other income. Interest payments as proportion to gross profits declined to 11.7 per cent in the first quarter of 2007-08 from 13.9 per cent in April-June 2006-07. Profitability in terms of gross and net profit margins-gross profits to sales and profits after tax to sales-has shown

Table 10: Disposition of National Income (at 1999-2000 prices) |

(Growth rates in per cent) |

Item |

2005-06 |

2006-07 |

2006-07 RE |

2007-08 |

|

|

QE |

RE |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

|

|

2 |

3 |

4 |

5 |

6 |

7 |

8 |

1. |

Total Final Consumption Expenditure |

7.2 |

6.6 |

11.8 |

3.7 |

5.1 |

6.1 |

6.5 |

|

a. Private Final Consumption Expenditure (PFCE) |

6.7 |

6.2 |

6.5 |

6.3 |

6.0 |

6.0 |

5.6 |

|

b. Government Final Consumption Expenditure |

9.8 |

9.0 |

47.6 |

-9.7 |

0.4 |

6.6 |

10.5 |

2. |

Gross Fixed Capital Formation (GFCF) |

15.3 |

14.6 |

15.8 |

13.3 |

15.5 |

14.1 |

15.9 |

3. |

Change in Stocks |

69.0 |

10.2 |

10.2 |

10.6 |

9.7 |

10.3 |

8.4 |

4. |

Valuables |

0.4 |

38.0 |

38.4 |

47.1 |

29.8 |

37.8 |

10.5 |

5. |

Exports |

5.9 |

8.6 |

10.3 |

18.9 |

-1.9 |

8.7 |

5.5 |

6. |

Imports |

10.3 |

11.4 |

11.7 |

18.7 |

4.8 |

11.3 |

16.1 |

|

|

|

|

|

|

|

|

|

Memo: |

|

|

|

|

|

|

|

Real GDP at market prices |

9.2 |

9.4 |

8.1 |

10.7 |

9.0 |

9.6 |

9.2 |

QE : Quick Estimates.

RE : Revised Estimates.

Source : Central Statistical Organisation. |

Table 11: Corporate Financial Performance |

(Growth rates in per cent) |

Item |

|

|

|

2006-07 |

2007-08 |

|

2004-05 |

2005-06 |

2006-07 |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

Sales |

24.1 |

16.9 |

26.2 |

25.6 |

29.2 |

30.3 |

22.5 |

19.2 |

Other Income |

-0.9 |

10.3 |

7.4 |

22.4 |

19.3 |

11.3 |

9.8 |

76.4 |

Expenditure |

23.6 |

16.4 |

23.5 |

24.6 |

26.6 |

26.9 |

19.5 |

19.3 |

Depreciation provision |

11.2 |

10.2 |

15.4 |

14.9 |

16.4 |

16.8 |

18.1 |

18.1 |

Gross profits |

32.5 |

20.3 |

41.5 |

33.9 |

45.9 |

51.8 |

39.2 |

28.6 |

Interest Payments |

-5.8 |

1.9 |

17.4 |

19.9 |

18.0 |

11.9 |

32.3 |

4.4 |

Profits after tax |

51.2 |

24.2 |

45.2 |

34.7 |

49.4 |

59.5 |

39.6 |

33.9 |

Select Ratios |

(Per cent) |

Gross Profits to Sales |

11.9 |

13.0 |

15.6 |

15.6 |

15.9 |

15.8 |

15.3 |

16.7 |

Other income to Profits after tax |

30.1 |

32.0 |

26.4 |

24.0 |

26.1 |

22.1 |

31.9 |

33.3 |

Profits After Tax to Sales |

7.2 |

8.7 |

10.7 |

10.6 |

11.0 |

11.0 |

10.6 |

11.6 |

Interest to Sales |

2.6 |

2.0 |

2.1 |

2.2 |

2.0 |

2.0 |

2.0 |

2.0 |

Interest to Gross Profits |

21.8 |

15.7 |

13.3 |

13.9 |

12.8 |

12.5 |

13.0 |

11.7 |

Interest Coverage (Times) |

4.6 |

6.4 |

7.5 |

7.2 |

7.8 |

8.0 |

7.7 |

8.5 |

Memo: |

(Amount in Rupees crore) |

No of Companies |

2,214 |

2,210 |

2,388 |

2,228 |

2,263 |

2,258 |

2,356 |

2,342 |

Sales |

5,49,449 |

7,74,578 |

10,41,894 |

2,34,610 |

2,51,125 |

2,60,064 |

2,94,223 |

2,80,814 |

Other income |

11,927 |

21,600 |

29,385 |

5,962 |

7,245 |

6,331 |

9,963 |

10,879 |

Expenditure |

4,77,609 |

6,66,690 |

8,72,168 |

1,95,556 |

2,09,437 |

2,16,053 |

2,48,740 |

2,34,596 |

Depreciation Provision |

22,697 |

28,883 |

37,095 |

8,449 |

8,892 |

9,172 |

10,338 |

10,173 |

Gross profits |

65,301 |

1,00,666 |

1,62,017 |

36,567 |

40,041 |

41,169 |

45,108 |

46,925 |

Interest Payments |

14,268 |

15,789 |

21,500 |

5,083 |

5,121 |

5,162 |

5,862 |

5,504 |

Profits after tax |

39,599 |

67,506 |

1,11,107 |

24,845 |

27,710 |

28,698 |

31,251 |

32,699 |

Note : 1. Data for 2004-05 are based on audited balance sheet, while those for 2005-06 and 2006-07 are

based on their abridged financial results of the select non-Government non-financial public limited companies.

2. Growth rates are percentage changes in the level for the period under reference over the

corresponding period of the previous year for common set of companies.

3. Data for the full year may not add up to the quarterly totals due to difference in the composition and

number of companies covered in each period. |

improvement in April-June 2007-08 over the corresponding period of the preceding year mainly on account of substantial rise in other income.

Business Expectations Surveys

Business confidence surveys conducted by various agencies present a mixed short-term outlook of the economy (Table 12). According to the latest business confidence survey conducted by Federation of Indian Chambers of Commerce and Industry (FICCI) in August 2007, the overall business confidence index during April-June 2007 marginally declined by 0.9 per cent over the previous quarter, reflecting concerns over rupee appreciation and rising interest rates. The FICCI’s expectations index for July-December 2007, however, showed improvement of 2.8 per cent over the previous survey. A majority of 70 per cent of the respondents (as compared with 64 per cent respondents in the previous survey) found the current overall economic conditions to be ‘moderately to substantially better’ than in the preceding six months. Among the three industry sectors surveyed, respondents from the services and heavy industry sectors were less optimistic about the current performance as well as

Table 12: Business Expectations Surveys |

(Per cent) |

Agency |

Business Expectations |

Growth over |

Growth |

|

|

|

a year ago |

over |

|

Period |

Index |

|

previous round |

1 |

2 |

3 |

4 |

5 |

FICCI |

July-December 2007 |

Expectations Index |

-0.3 |

2.8 |

Dun & Bradstreet |

October-December 2007 |

Business Optimism Index |

9.1 |

15.5 |

NCAER |

July-December 2007 |

Business Confidence Index |

-2.7 |

-8.8 |

Reserve Bank of India |

October-December 2007 |

Business Expectation Index |

-0.7 |

2.7 |

performance in the ensuing six months than those from the light industry sector. The business optimism index of the survey by Dun and Bradstreet for October-December 2007 (conducted in September 2007) recorded a rise of 15.5 per cent over the preceding quarter albeit over a low base; five of the six optimism indices, viz., volume of sales, selling prices, new orders, inventory levels and employees increased during the period. Among the sectors surveyed, expectations for October-December 2007 were the most optimistic in the capital goods and consumer durables sectors, while they were least optimistic in the case of services sector, due in part to the appreciation of the rupee.

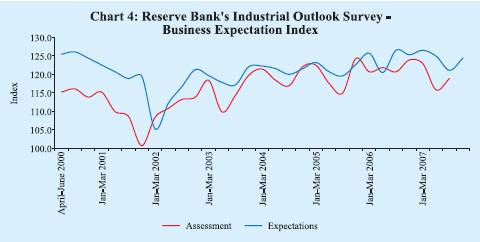

According to the Reserve Bank’s Industrial Outlook Survey conducted during July-September 2007, the business expectations indices based on assessment for July-September 2007 and on expectations for October-December 2007 increased by 2.7 per cent each over the previous quarter. In comparison with the previous year, the indices based on assessment and expectations were, however, lower by 1.5 per cent and 0.7 per cent, respectively (Chart 4).

The increase in the expectations index for October-December 2007 over the previous quarter was on account of improvement in expectations for most of

the parameters of the survey such as overall business situation, production, availability of finance, order books, capacity utilisation and profit margin. Expectations of increase in exports, imports, employment and selling prices were, however, lower than those in the previous quarter. The maximum proportion of respondents continued to be placed in the category of ‘no change in expectations over the preceding quarter’ for most of the parameters including pending orders and inventories of raw materials and finished goods (Table 13).

Table 13: Net Response on 'A Quarter Ahead' Expectations About the |

Industrial Performance |

(Per cent) |

Parameter |

Response |

Oct- |

Jan- |

Apr- |

July- |

Oct- |

|

|

|

Dec. |

March |

June |

Sept. |

Dec. |

|

|

|

2006 |

2007 |

2007 |

2007 |

2007 |

1 |

|

2 |

3 |

4 |

5 |

6 |

7 |

1. |

Overall business situation |

Better |

51.8 |

53.7 |

51.7 |

49.5 |

50.5 |

|

|

|

(41.2) |

(40.7) |

(43.3) |

(41.2) |

(42.1) |

2. |

Financial situation |

Better |

41.9 |

44.5 |

43.8 |

41.3 |

40.1 |

|

|

|

(50.6) |

(49.9) |

(49.8) |

(49.8) |

(51.3) |

3. |

Working capital finance requirement |

Increase |

35.4 |

36.2 |

35.3 |

34.5 |

32.2 |

|

|

|

(58.3) |

(59.2) |

(59.2) |

(59.2) |

(62.6) |

4. |

Availability of finance |

Improve |

33.4 |

36.2 |

35.2 |

32.1 |

33.8 |

|

|

|

(57.8) |

(56.6) |

(57.2) |

(58.6) |

(58.8) |

5. |

Production |

Increase |

49.7 |

50.7 |

47.8 |

46.6 |

49.0 |

|

|

|

(39.6) |

(40.1) |

(41.6) |

(41.1) |

(40.9) |

6. |

Order books |

Increase |

46.3 |

47.3 |

45.7 |

43.6 |

44.1 |

|

|

|

(42.6) |

(43.1) |

(45.4) |

(46.1) |

(46.0) |

7. |

Pending orders, if applicable |

Below normal |

-2.1 |

-2.7 |

-2.2 |

2.2 |

-3.5 |

|

|

|

(81.7) |

(82.9) |

(82.8) |

(82.6) |

(82.4) |

8. |

Cost of raw material |

Decrease |

-49.2 |

-41.7 |

-42.1 |

46.0 |

-42.4 |

|

|

|

(46.4) |

(51.0) |

(52.0) |

(49.7) |

(51.0) |

9. |

Inventory of raw material |

Below average |

-6.1 |

-7.1 |

-7.3 |

5.4 |

-6.3 |

|

|

|

(83.5) |

(83.8) |

(85.0) |

(85.0) |

(85.0) |

10. |

Inventory of finished goods |

Below average |

-4.9 |

-5.2 |

-4.4 |

2.7 |

-3.5 |

|

|

|

(83.5) |

(84.5) |

(85.2) |

(87.1) |

(86.4) |

11. |

Capacity utilisation (Main product) |

Increase |

33.2 |

33.3 |

29.4 |

27.0 |

28.4 |

|

|

|

(56.6) |

(57.7) |

(60.4) |

(61.4) |

(61.5) |

12. |

Level of capacity utilisation (Compared to the |

Above normal |

10.9 |

12.8 |

11.5 |

9.4 |

10.7 |

|

average in the preceding four quarters) |

|

(76.6) |

(76.4) |

(77.1) |

(76.5) |

(77.2) |

13. |

Assessment of the production capacity (With regard |

More than |

5.1 |

4.8 |

4.0 |

3.0 |

4.2 |

|

to expected demand in the next six months) |

adequate |

(79.7) |

(81.8) |

(82.2) |

(82.2) |

(83.0) |

14. |

Employment in the company |

Increase |

17.9 |

18.1 |

18.3 |

17.4 |

16.7 |

|

|

|

(73.3) |

(73.7) |

(73.3) |

(73.5) |

(74.1) |

15. |

Exports, if applicable |

Increase |

34.2 |

32.6 |

33.4 |

32.6 |

31.4 |

|

|

|

(57.2) |

(57.3) |

(56.8) |

(55.6) |

(55.9) |

16. |

Imports, if any |

Increase |

23.4 |

20.8 |

21.6 |

23.7 |

20.8 |

|

|

|

(68.1) |

(68.0) |

(68.4) |

(68.2) |

(68.6) |

17. |

Selling prices are expected to |

Increase |

16.8 |

14.2 |

15.5 |

19.0 |

13.0 |

|

|

|

(68.0) |

(69.2) |

(68.9) |

(67.1) |

(68.5) |

18. |

If increase expected in selling prices |

Increase at |

14.5 |

10.5 |

12.1 |

-10.4 |

-3.7 |

|

|

lower rate |

(67.0) |

(68.1) |

(66.7) |

(65.0) |

(66.8) |

19. |

Profit margin |

Increase |

9.2 |

11.6 |

9.9 |

7.5 |

9.6 |

|

|

|

(60.6) |

(61.7) |

(62.5) |

(62.6) |

(59.6) |

Memo: |

|

|

|

|

|

|

Number of companies included in the results |

|

1,138 |

1,115 |

1,108 |

1,056 |

1,047 |

Note :

1. 'Net response' is measured as the percentage share differential between the companies reporting 'optimistic' (positive)

and 'pessimistic' (negative) responses; responses indicating status quo (no change) are not

reckoned. Higher 'net response' indicates higher level of confidence and vice versa.

2. Figures in parentheses are the percentages of respondents with 'no change over the preceding quarter' as responses. |

Forecasts by various agencies for real GDP growth in 2007-08 are set out in Table 14.

Table 14: Projections of Real GDP for India by various Agencies – 2007-08 |

(Per cent) |

Agency |

Overall |

Agriculture |

Industry |

Services |

Month of |

|

Growth |

|

|

|

Projection |

1 |

2 |

3 |

4 |

5 |

6 |

ASSOCHAM |

8.5-8.7 |

– |

– |

– |

August 2007 |

Confederation of Indian Industry (CII) |

8.5 |

3.0 |

9.3 |

9.9 |

April 2007 |

|

9.2 |

3.0 |

9.4 |

11.2 |

July 2007 |

Citigroup |

9.3 |

3.0 |

10.3 |

10.9 |

April 2007 |

|

9.3 |

3.0 |

10.0 |

11.0 |

September 2007 |

Merrill Lynch |

8.5 |

– |

– |

– |

March 2007 |

|

8.8 |

4.0 |

9.5 |

10.0 |

September 2007 |

JP Morgan |

8.0 |

– |

– |

– |

March 2007 |

|

8.6 |

2.6 |

9.8 |

10.0 |

September 2007 |

ICRA |

8.5 |

– |

– |

– |

April 2007 |

|

9.0 |

– |

– |

– |

September 2007 |

Standard and Poor |

8.6 |

3.4 |

9.2 |

10.0 |

October 2007 |

Indicus Analytics |

8.4 |

3.0 |

7.9 |

9.7 |

March 2007 |

|

8.4 |

2.7 |

8.5 |

10.1 |

October 2007 |

Centre for Monitoring the Indian Economy (CMIE) |

8.5 |

– |

– |

– |

June 2007 |

|

9.1 |

3.9 |

9.5 |

10.7 |

September 2007 |

National Council for Applied Economic |

|

|

|

|

|

Research (NCAER) |

8.3 |

2.6 |

8.7 |

9.9 |

April 2007 |

|

8.5 |

3.4 |

9.0 |

10.1 |

August 2007 |

|

|

|

|

|

|

Asian Development Bank |

8.0 |

– |

– |

– |

March 2007 |

|

8.5 |

– |

– |

– |

September 2007 |

International Monetary Fund |

9.0 * |

– |

– |

– |

July 2007 |

|

8.9 * |

– |

– |

– |

October 2007 |

Organisation for Economic Cooperation |

|

|

|

|

|

and Development (OECD) |

8.5 |

– |

– |

– |

May/October 2007 |

United Nations Conference on Trade and |

|

|

|

|

|

Development (UNCTAD) |

8.5 |

– |

– |

– |

September 2007 |

Reserve Bank of India |

Around 8.5 |

– |

– |

– |

April/July 2007 |

– : Not Available.

* : Calendar Year. |

1 These 81 important reservoirs have FRL of 151.77 billion cubic metres and account for around 72 per cent of the total reservoir capacity of the country. |

IST,

IST,