IST,

IST,

Chapter III : Financial Sector: Regulations and Developments

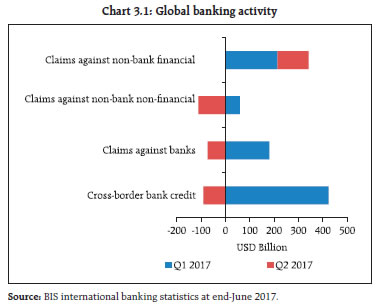

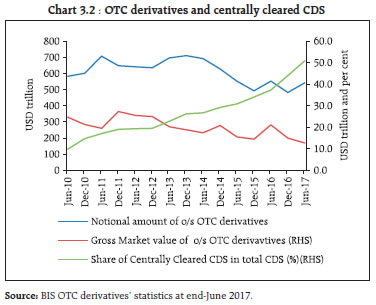

While global banks have strengthened their resilience in terms of capital and liquidity, their activity moderated in terms of cross-border lending. On the domestic front, regulations on resolution have ultimately evolved into the bankruptcy framework and stakeholders have to maintain a fine balance among various options available to them for the most optimum resolution. The new insolvency and bankruptcy regime, which came into existence in May 2016 has enabled the introduction of a market-determined and time-bound mechanism to handle insolvencies. As corporate governance in banks is key to ensuring the success of the recapitalisation of banks, the Government has explicitly committed to the compatibility of governance issues of PSBs while committing funds for capitalisation. Financial savings in the form of mutual funds (MF) investments and pension schemes not only continued to grow but have also got broad-based in terms of the spatial distribution and investor profile. Fintech is expanding its relevance to banking and is testing the technological capabilities of traditional banks. With a fast changing operating environment and the attendant risks on the cyber front for banks, a number of steps have been taken by the government and the financial sector regulators to ensure cyber resilience. SEBI has taken a number of steps to further deepen commodity derivatives market, which include a principle based methodology to fix open position limits for agricultural commodities vis-à-vis ‘deliverable supply’. On the supervisory front, IRDAI and PFRDA have taken initiatives towards introduction of risk-based supervision (RBS) for their regulated entities. The Reserve Bank has reviewed its instructions on customer liabilities in unauthorised/fraudulent electronic transactions and facilities for senior citizens and differently abled customers. Similarly, SEBI, PFRDA and IRDAI have strengthened their customer protection frameworks. ’History doesn’t repeat itself, but it often rhymes’ – Mark Twain Section A International and domestic regulatory developments I. Banks a. International regulatory developments 3.1 Globally, banks’ resilience continued to strengthen in terms of capital and liquidity1. However, international banking activity moderated in 2017:Q2 (Chart 3.1) following a rebound in 2017:Q1.2 Consequently, cross-border bank credit in 2017:Q2 contracted by $91 billion from the previous quarter.  3.2 Reducing the systemic risk from over-the-counter (OTC) derivatives market was one of the important aspects of the post-crisis reforms initiated by the Basel Committee on Banking Supervision (BCBS) and the International Organisation of Securities Commissions (IOSCO). Notwithstanding the delayed implementation of the ‘margin requirements for non-centrally cleared derivatives’ standard issued in May 2015 jointly by BCBS and IOSCO, globally there has been significant decline in OTC derivatives’ volume in terms of their gross market value3 (Chart 3.2).  3.3 The recent standards and guidelines issued by the BCBS include guidelines on ‘Identification and management of step-in risks’ (October 2017). These are part of the G20 initiative to strengthen the oversight and regulation of the shadow banking system to mitigate risks arising from banks’ interactions with shadow banking entities. The guidelines define ‘step-in risk’ as a risk that a bank faces when it decides to provide financial support to an unconsolidated entity that is facing stress, in the absence of, or in excess of, any contractual obligations4 to provide such support. 3.4 In the meantime, corporates’ high debt and interest expense have triggered a debate on the justification for allowing interest payment as a tax deductible expense in the context of an emerging view that such tax benefits might be incentivising excessive leverage. This may potentially have a significant impact on governance by altering incentive structures (Box 3.1).

b. Domestic banking – preparing for take-off 3.5 In 1932, in a book way ahead of its time, Berle and Means6 documented that dispersed ownership confers significant managerial discretion which can be potentially abused. This initiated subsequent academic thinking on corporate governance and corporate finance. The recent global financial crisis and the twin balance sheet7 crisis closer home affirm that the risks arising out of managerial discretion are not merely academic. The recent announcement of recapitalisation of PSBs has justifiably initiated a debate as to whether it will be another episode of throwing good money after bad. Most of the commentaries also focus on the deficiencies of board oversight and consequential remedies. Boards in fact operate under a regulatory framework drawn up by the assigned regulators and are supposed to take critical decisions based on available information. They also reappraise the adequacy of internal controls and governance mechanisms based on internal audit reports, while external audits provide an independent third party appraisal of the performance. The scale of the recent crisis throws up valuable lessons on the effectiveness of each of these layers that interface with bank performance. The broad contours of this reform to help this cause can be divided into:

Improving data quality and availability for effective oversight 3.6 Economic theory has long emphasised the role of information in credit markets. Jaffe and Russell (1976) and Stiglitz and Weiss (1981) demonstrated that asymmetric information between the borrower and lender poses problems of adverse selection and moral hazards and makes it impossible to price the loan, i.e., information asymmetry prevents the interest rate to play a market-clearing function. Information asymmetry is considerably reduced if borrowers’ credit history is made available to lenders. In this context, having put in place the Central Repository of Information on Large Credits (CRILC) to facilitate exchange of information among critical stakeholders, India has taken the initial steps towards the setting up of a public credit registry. 3.7 Legal Entity Identifier (LEI) Code, which has been conceived as a key measure for improving the quality and accuracy of financial data systems for better risk management post the global financial crisis, is being introduced in a gradual manner. The LEI system was initially introduced for all participants in the over-the-counter (OTC) markets. Subsequently, the phased introduction of LEI for large corporate borrowers (total exposure of ₹500 million and above) has been announced, which will be extended to smaller corporate borrowers. Strengthening resolution mechanisms 3.8 Recognition of impairments and resolution of stressed assets in the banking industry are two aspects attracting a lot of attention currently (Box 3.2).

3.9 The promulgation of the IBC Code in May 2016 is a watershed event – it has allowed valuation of aged impaired assets to be put in perspective. While the transfer of such assets to various asset reconstruction intermediaries was not effective owing to valuation issues, IBC, through its auction mechanism allows such assets specifically to have executable bids. Such a mechanism also points to the possible recovery values embedded in assets of similar ageing profiles. The government recently tightened IBC to prevent wilful defaulters and other unscrupulous promoters from taking over a company under resolution. 3.10 The impairment crisis in domestic banks has also highlighted certain basic deficiencies with regard to the appraisal of long term projects with a significant gestation time. A significant part of such projects undertaken were consortium lending with appraisals being carried out by professional merchant bankers with built-in conflict of interest (since they were paid by the borrowers). Public-private partnership (PPP) projects were also undertaken in project financing mode with high leverage. The exact implications of such risky projects implemented through the Special Purpose Vehicle (SPV) route were sometimes not clear to bankers. Further, PPP contracts of long term duration are complex in nature due to involvement of multiple stakeholders and there is a need to align their objectives for mutual benefit. Successful implementation of PPP projects calls for more due diligence by all stakeholders including the public sector contracting agencies, the private concessionaires, the bankers, etc. Addressing capital and governance needs for a reformed banking sector 3.11 Committees/working groups set up over the years (Box 3.3) to bring improvements in the banking sector also have a touch of sameness implying that there are structural factors at work which make the PSBs particularly vulnerable. Yet, the delayed or partial implementation of recommendations imply that the basic vulnerabilities have not been adequately addressed. This has had significant fiscal implications. Recently, the Government of India announced a larger recapitalisation plan amounting to ₹2.11 trillion. However, it may be noted that this time as the owner, Government has explicitly committed to the compatibility of governance issues of PSBs while committing funds for capitalisation.

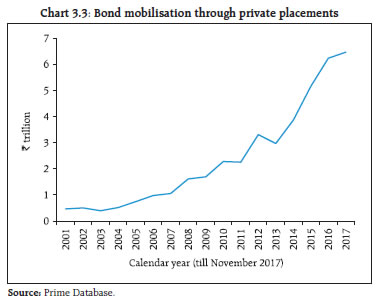

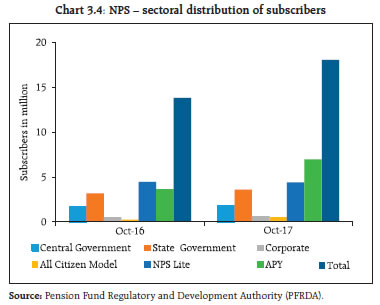

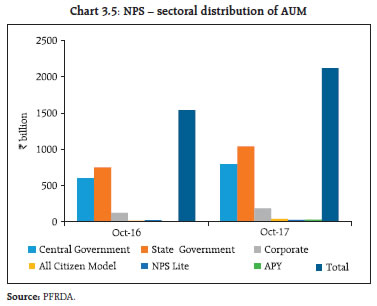

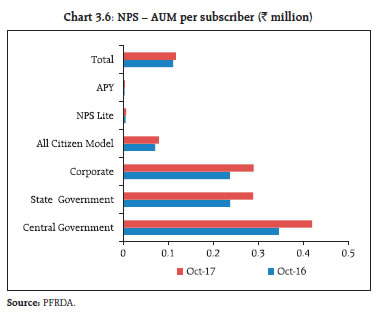

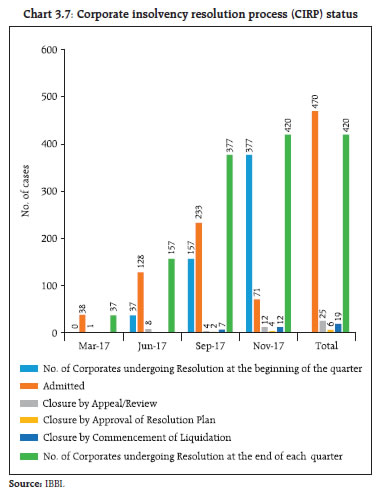

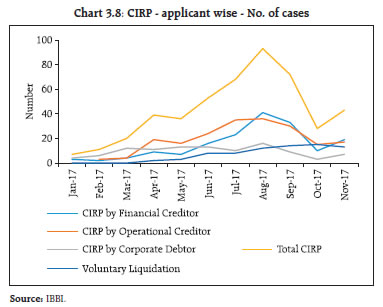

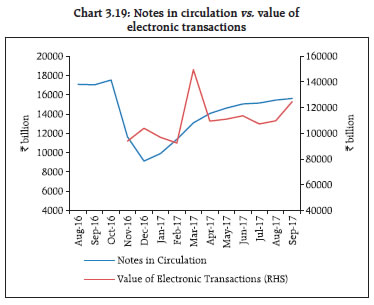

3.12 Governance also has a regulatory dimension. ‘... A regulatory regime susceptible to forbearing instincts carries the concomitant chance of risk inducing behaviour from the stakeholders…’12 In this regard, the regulators’ commitment to not condone the consequences of bank specific action should be seen as a hard constraint. Incidentally, such hard constraint on lending practices and prudential accounting treatment does not take away lenders’ discretion for prudential measures aimed at rehabilitating borrowers. Rather, such hard constraints strive to place such rehabilitation measures as exceptions and aim not to institutionalise them. The emerging NPA recognition norms from continental Europe reinforce such mechanisms. 3.13 There is significant information asymmetry between external auditors and internal stakeholders. The recent reforms globally aim to put in place institutional structures that incentivise auditors to learn more and internal stakeholders to divulge more about the functioning of the institutions. Disclosure of ‘Critical Audit Matters’ in the US (‘Key Audit Matters’ in the EU) in the audit report allows information asymmetry between internal stakeholders and external auditors to be put in perspective since such disclosures can be validated post facto with realised risks. Moreover, unlike some jurisdictions, reasons for any omission / commission on the part of external auditors can be assigned and hence auditor performance can be back-tested13. Similarly, internal audit has undergone a significant evolution globally as banks reorganise from branch-centric delivery of financial services to web-centric delivery. The introduction of IFRS globally has also put governance of internal models in the limelight. This has necessitated internal audit extending to areas involving the overall model governance framework encompassing validation of rating models, applicability of datasets and an analysis of deviations. An institutionalised structure of sharing of best practices may allow some of the laggards in governance and control to leapfrog the intermediate steps. 3.14 Globally, supervision is increasingly taking a forward looking approach. In other words, it is providing an assessment of medium term risks. In this regard, issues of standardisation of subjective assessments, developing yardsticks for materiality tests of exceptions and back-testing model predictions with realised risks require particular emphasis. 3.15 The recent referrals under IBC for resolution have implications for the capitalisation requirement too. A record of recovery based impairment assessments, however, has inevitable elements such as the time lag between such assessments and underlying resolutions which can lead to a significant recovery risk associated with ageing impaired assets. However, the recent substantial recapitalisation announced by the government will help banks with requisite capital cushions to tackle the issue and repair their balance sheets. 3.16 The worsening of the negative association between CRAR and asset quality has been documented in Chapter 2. It stands to reason that it is asset quality that is driving the poor capitalisation on the face of a muted balance sheet growth. In this regard, PSBs’ capital plans in particular need to take into account the somewhat elevated levels of slippage from uncontaminated standard assets (standard assets less restructured standard assets) and recovery risks embedded in assets referred to NCLT as outlined earlier. II. The securities market 3.17 The International Organisation of Securities Commissions (IOSCO) had published a report in 2014 regarding the Protection of Client Assets. The report had prescribed eight principles pertaining to the Protection of Client Assets. A thematic review14 was carried out by the Assessment Committee of IOSCO to review the progress made by the jurisdictions15 in adopting the principles. The findings of the thematic review was published in July 2017. In general, the review observed that as on the reporting date, a majority of the participating jurisdictions had adopted a client asset protection regime. India was observed to be compliant with the principles except Principle 316. With reference to Principle 3, the report noted that the intermediaries in India are not required to take additional steps other than using the approved custodians. 3.18 Public transparency and accessibility to information are key components of robust capital markets. Transparency is generally considered to be ‘the degree to which information about trading (both pre-trade and post-trade information) is made publicly available.’ In this regard, in August 2017 the IOSCO board published a consultation report on regulatory reporting and public transparency in the secondary corporate bond markets. The report, inter alia, recommends regulatory authorities to enhance the public availability of appropriate pre-trade information relating to corporate bonds. Such transparency becomes important in the Indian context where the corporate bond market is recording increased activity (Chart 3.3).  3.19 An analysis of the ratings of listed companies by major credit rating agencies (CRAs) (Table 3.1) shows that the upgrades picked up during 2017:Q2 suggesting a turnaround in corporate performance. 3.20 Various committees17 constituted by the government and the Securities and Exchange Board of India (SEBI) have been instrumental in improving corporate governance practices in India. Corporate governance, however, is an evolving area which requires periodic reviews. Accordingly, SEBI constituted a Committee on Corporate Governance in June 2017 with a view to enhancing the standards of corporate governance of listed entities in India. The recommendations of the committee, cover a wide-range of areas including aspects relating to board composition, board of directors, independent directors, role of auditors, ratings and disclosures and information sharing with promoters and other stakeholders. Further, as per the committee all listed entities, government or private, should be at par with governance standards. The committee’s recommendations, along with the public comments received are presently under SEBI’s consideration. 3.21 SEBI prescribed a framework categorising commodities as Sensitive, Broad and Narrow with an objective of outlining a principle based methodology for revising the commodity-wise numerical values at the overall client level open position limits for agricultural commodities vis-à-vis ‘deliverable supply’ of such commodities available in the country during any specific year. Accordingly, the position limit for each commodity is to be fixed as a per cent of their deliverable supply, which is the combination of production and imports for the particular commodity. Other regulatory developments pertaining to the capital market are given in Table 3.2. III. Insurance 3.22 The contribution of insurance to financial stability was comprehensively discussed in a report18 of the International Association of Insurance Supervisors (IAIS). The business model of insurers exposes them to unique risks like mortality, morbidity, property and liability risks, which are not typically found in banking. Although interconnected with other financial market entities, a majority of the insurers withstood the global financial crisis of 2008-09 better than other financial institutions due to their inverted production cycle business model. The report, inter alia, cautions that insurance groups and conglomerates that engage in non-traditional or non-insurance activities are more vulnerable to financial market developments and importantly more likely to amplify, or contribute to, systemic risk. It also adds that just as the insurance business model is different from the banking model, the impact of insurance failures on other financial institutions and the real economy are different. Accordingly, it suggests that loss absorbency and resolution regimes for insurers should be different as there are differences between insurers and banks in the impact of failures. 3.23 The insurance sector in India has shown a robust growth so far during 2017-18. For the period ended October 2017, the general insurance industry grew at 18.63 per cent in gross direct premium and life insurance grew by 21.29 per cent in new business premium. Going forward, increasing life expectancy, favourable savings trends and greater employment in the private sector are expected to fuel demand for pension plans and protection plans. Likewise, strong growth in the automotive industry over the next decade will be a key driver for the motor insurance market. Health Insurance is an emerging area and includes indemnity based, critical illness based, benefit based, personal accident, domestic travel and overseas travel products. Health Insurance Products are offered by General, Health and Life insurers in the market. During the FY 2016-17, the total amount of premium collected under health insurance segment by all insurers in the industry was ₹35,430 crore. Further, the opening of branches of foreign reinsurers is a step towards developing the country as a reinsurance hub. 3.24 The Indian insurance sector has recently seen a lot of activity in terms of going public and consolidation; five19 insurance companies have already been listed on the stock exchanges and two more are in the process of being listed. This has been facilitated by the regulatory initiatives of the Insurance Regulatory and Development Authority of India (IRDAI) and the government’s decision to bring down its stake in public sector insurers and increase foreign investments in the sector. 3.25 IRDAI had earlier decided to implement the Ind AS in the insurance sector from the year 2018-19. However, due to replacement of IFRS 4 (on insurance contracts) with IFRS 17 by the International Accounting Standards Board (IASB), the authority has reviewed its position. To avoid a mismatch in the valuation of assets and liabilities and multiple compliance costs, the date of implementation of Ind AS has been deferred by two years, i.e., from FY 2020-21. IV. Pension funds 3.26 The National Pension System (NPS) continued to grow in terms of the number of subscribers and assets under management (AUM). NPS’ total subscribers increased from 13.82 million in October 2016 to 18.05 million in October 2017. At the same time, AUM increased from ₹1,539 billion to ₹2,120 billion during the same period (Charts 3.4 and 3.5). Atal Pension Yojana (APY) and NPS Lite subscribers formed 63 per cent of the total subscribers, while AUM of state governments and central government subscribers formed 88 per cent of the total. However, in terms of AUM per subscriber, the central government was highest at ₹0.41 million, followed by state governments and corporates, the all citizen model, NPS Lite and APY in that order (Chart 3.6).    V. Insolvency and Bankruptcy Regime 3.27 The new insolvency and bankruptcy regime, came into existence with the enactment of the Insolvency and Bankruptcy Code (IBC) in May 2016 followed by establishment of the Insolvency and Bankruptcy Board of India (IBBI) as the regulator on 1st October, 2017. An important pillar of ecosystem, the National Company Law Tribunal (NCLT) as the adjudicating authority for Corporate Insolvency Resolution Process (CIRP) was already in place. Since then, there has been a significant amount of progress. A large number of corporate debtors have entered the insolvency process, and a few have even exited the process. As on November 2017, over 4300 applications under CIRP were filed in the various benches of NCLT. Since the majority of these are the cases where the insolvent firm has been previously admitted under the then prevalent laws like Companies Act, Sick Industrial Companies Act (SICA) etc., many cases were not pursued and became time-barred. Out of these, more than 500 applications for admission have been rejected, dismissed or withdrawn. 470 cases admitted by NCLT are at various stages of the insolvency process. So far in 25 CIRP transactions, NCLTs have approved the resolution plans or liquidation orders, whereas admission of cases have been set aside by the orders of appellate authorities i.e. NCLAT/the Supreme Court in 25 CIRPs admitted by the adjudicating authority. The details of transactions under CIRP are given in Chart 3.7.  3.28 Apart from the speed of resolution, another notable feature is that operational creditors, such as trade suppliers, employees, or workmen, have been empowered. Such creditors were served neither by previous restructuring mechanisms (such as SICA) nor the existing recovery mechanisms (SARFAESI, RDDBFI). The distribution of admitted applications based on the applicant for initiating the CIRP is given in Chart 3.8.  3.29 This market-determined and time-bound mechanism to handle insolvencies has been recognised in the World Bank Group’s “Doing Business 2018: Reforming to Create Jobs” report issued in October 2017. India’s ranking on ease of doing business has jumped from 130 to 100. The ranking under the Insolvency head, taken alone, also improved sharply from 136 to 103. VI. Recent regulatory initiatives and their rationale 3.30 Some of the recent regulatory initiatives, including prudential and consumer protection measures and the rationale thereof are given in Table 3.2. Section B Other developments, market practices and supervisory concerns I. The Financial Stability and Development Council 3.31 Since the publication of the last FSR in June 2017, the Financial Stability and Development Council (FSDC) held its 17th meeting on August 22, 2017 under the chairmanship of the Finance Minister where issues related to the state of the economy, setting-up of the Computer Emergency Response Team in the Financial Sector (CERT-Fin), progress regarding the Financial Sector Assessment Program (FSAP) 2017, setting up the Financial Data Management Centre (FDMC), Annual Report of FSDC, the Central KYC Registry (CKYCR) and Credit Rating Agencies (CRAs) were discussed. 3.32 The FSDC sub-committee held a meeting chaired by the Governor on November 23, 2017. It reviewed the major developments on global and domestic fronts impinging the financial stability of the country. The sub-committee also discussed issues related to the establishment of the National Centre for Financial Education (NCFE), operationalisation of information utilities registered by the Insolvency and Bankruptcy Board of India (IBBI), sharing of data among regulators and LEI’s implementation status. Further, the sub-committee also reviewed the activities of its various technical groups and also the functioning of the state level coordination committees (SLCCs) in various states / UTs. The recommendations of the committees on FinTech and Digital Innovations, the Shadow Banking Implementation Group and Stewardship Code were also discussed. II. Fund flows: FPI and mutual funds Mutual funds 3.33 Mutual funds as an asset class seem to be entering the maturity phase in India with broad-basing of investors and geographical spread. Assets under management (AUM) increased from ₹17.55 trillion in March 2017 to ₹20.40 trillion in September 2017. Contributions to mutual funds through systematic investment plans (SIPs) has added further stability to this sector. While the number of outstanding SIPs has continuously increased from 6 million in 2013-14 to 16.5 million in July 2017, the number of premature terminations came down from 1.9 million to 0.6 million during the same period. Added to this, AUM of B-15 cities grew 230 per cent in 2016-17 of what it was in 2012-13. Further, the share of individual holdings in mutual funds’ AUM has increased from 46 per cent in April 2016 to 51 per cent by September 2017, while the share of holdings by institutions (corporates and banks) went down from 54 per cent to 49 per cent during the same period. Diversity in terms of the investor base will provide resilience against redemption pressures in case the markets see corrections in their valuations (Chart 3.9).  III. Ownership patterns of Indian stocks 3.34 A diverse ownership in public listed companies is conducive to the depth and liquidity of stock markets. An analysis of the shareholding patterns of the top-500 scrips in terms of market capitalisation shows a gradual increase in the shareholding percentage of domestic institutional investors (DIIs). The share of mutual funds, especially, increased over the past three years (Chart 3.10). In both NIFTY 50 and top 500 scrips, promoters and the government continue to hold a dominant share of ownership (Chart 3.11)  3.35 Another important feature of the evolution of Indian equity markets is investors’ increasing interest in small cap and mid-cap securities over the last two years as seen from a significant increase in turnovers in beyond top 100 scrips in 2016-17 over the previous financial year (Chart 3.12). The turnover of the scrips in the group 501-1000 (in terms of market capitalisation) increased by nearly 36 per cent as compared to a 12 per cent increase in the case of the top 50 scrips and a 19 per cent increase in the total exchange turnover. However, fresh supply of equities remains muted as capital raised through ‘offer for sale’ (OFS)20 is much more than that raised through ‘initial public offerings‘ (IPOs). During April-September 2017, out of the total primary market equity raising, fresh issues through IPOs and OFSs were 15 per cent and 85 per cent respectively as against 25 per cent and 75 per cent respectively during the corresponding period of the previous year. Over the past six years, growth in listed companies in terms of number has increased marginally by 15 per cent on both the exchanges. In the long run, there is a need to increase the supply of quality listed securities so as to be able to meet rising demand, particularly through the mutual funds route.  IV. Commodity derivatives 3.36 The commodity derivatives market registered encouraging trends during April-September 2017 with metals and agriculture commodities recording positive growth (Charts 3.14 and 3.15).    V. Impact of demonetisation on Basic savings bank deposit (BSBD) accounts and digital transactions 3.37 Withdrawal of specified bank notes (SBNs) had a substantial impact on financial inclusion reflected in increase in the number of BSBD21 accounts and outstanding deposits. The total number of BSBD accounts post-demonetisation increased from 504 million in October 2016 to 533 million by March 2017, while the outstanding amount in such accounts rose from ₹732 billion to ₹976 billion during the corresponding period. Overdraft (OD) facility availed by such accounts also peaked in November 2016, which could be attributed to non-availability of informal sources of credit (Charts 3.16 and 3.17).   3.38 Demonetisation gave a substantial push to electronic transactions (Charts 3.18 and 3.19). Expanding smartphone and internet access and rationalisation of incentives for digital transactions can buttress this trend. The rapidly evolving ecosystem of new technologies will also play an important role as can be seen in the recent data.   VI. FinTech 3.39 FinTech has not only continued to expand its relevance and presence in banking but also may emerge as a preferred way of doing the business of banking in the near future. Machine learning (ML) and artificial intelligence (AI) along with big data are metamorphosing banking thereby increasing regulatory challenges. Exponentially declining costs of data storage and processing is facilitating the gainful use of large amount of data, which is being generated from all walks of the universe. Although FinTech is only the latest wave of innovation to affect the banking industry, the rapid adoption of enabling technologies and emergence of new business models pose an increasing challenge to incumbent banks. In its recent report on FinTech22, the Financial Stability Board (FSB) cited that the lack of interpretability or auditability of AI and machine learning methods could become a macro-level risk while a widespread use of opaque models may result in unintended consequences. 3.40 Globally, interest and investment in regtech and suptech are picking up as traditional banks and financial institutions strive to link compliance automation with other business processes such as improved customer service. A KPMG report23 states that the ‘growing breadth of fintech activities globally has led to the evolution of numerous distinct fintech hubs. While traditional hubs like the US, the UK, and Israel continue to dominate, other jurisdictions are working to become leaders in unique sub-sectors of fintech. For example, Japan is becoming a leader in fostering engagement around robotics process automation (RPA), while Taiwan is growing as a blockchain center, and Malaysia is defining itself as a hub for cybersecurity innovation.’ This may be an opportunity for the Indian FinTech sector to evolve in relevant niche areas like financial inclusion and digital payments. Apart from regtech and suptech, insurtech is another emerging area with Singapore emerging as its hub. Insurtech is still considered a relatively new phenomenon when compared to banking and other areas of financial services, but it is rapidly catching up. 3.41 India has made substantial progress in the digital payments aspect of FinTech under a facilitating regulatory environment. While a number of payments banks have started operations, the Reserve Bank recently issued guidelines on peer-to-peer (P2P) lending, which lay down prudential norms for the registration and operations of companies desiring to undertake the business of the P2P lending platform. However, private sector investments in Indian FinTech ventures substantially slowed down in 2017. As per the KPMG report23, venture investments in FinTech in India slowed down to less than $100 million and less than 10 closed deals in 2017:Q3 from the peak of $800 million of investments and more than 20 closed deals in 2015:Q3. VII Cyber security 3.42 The exponential developments in FinTech and related fields are also giving rise to unknown risks in addition to the hitherto known cyber risks. Increasing sophistication and complexity amongst financial system’s entities is also making them vulnerable to cyber risks. In this context, the Reserve Bank has been performing focused IT examinations of the banks to evaluate their cyber risk management systems and procedures. While the assessment is factored in the overall risk profile of a bank under Risk Based Supervision (RBS), certain specific areas like payment systems and network security are proposed to be subjected to more intensive scrutiny during the year. As part of strengthening the offsite monitoring system, information regarding banks’ cyber security postures is being collected on a quarterly basis through various data points (both objective and subjective). Cyber drills are conducted periodically to assess banks’ preparedness and response capabilities. This effort is supported by the Reserve Bank Information Technology Private Ltd. (ReBIT), a wholly owned subsidiary of the Reserve Bank. 3.43 The Working Group set up by the Government under the chairmanship of DG, Indian Computer Emgency Response Team (CERT-In) with representation from financial sector regulators, departments and various stakeholders submitted its report for setting up a Computer Emergency Response Team for the Financial Sector (CERT-Fin). The report was placed in the public domain for feedback in June 2017 and the comments received on the report are under examination. It was recommended that CERT-Fin may, inter alia, do an analysis of reported financial sector cyber incidents, forecast and alert on cyber security incidents, monitor sectoral efforts in the financial sector towards maintaining a dynamic and modern cyber security architecture, offer policy suggestions to all stakeholders and contribute to developing awareness amongst regulated entities and the public. The Reserve Bank may act as the lead regulator till transition to a fully functional CERT-Fin. Simultaneously, the government also constituted a Digital Payment Security Committee to examine security issues in both the process and technology of digital payments. 3.44 SEBI advised Market Infrastructure Institutions (MIIs) to prepare a list of various cyber-threat vectors and cyber-attack scenarios and also take corrective actions with regards to the same. Subsequently, SEBI circulated a comprehensive list of Cyber Threat vectors and attacks scenarios based on the CERT-In’s Cyber Crisis Management Plan (CCMP) and internal research. MIIs were also advised to create FAQs and guidance for best practices for circulation to internal users, market intermediaries and investors with regard to Cyber Security, and safety against current prevailing threats and scams. Based on the Ransomware threats and inputs received from other agencies like National Cyber Security Co-ordinator (NCSC), SEBI also issued advisories to MIIs. Training of staff of MIIs by CERT-In was also conducted. Further, Cyber Security and Cyber Resilience framework was extended by SEBI to each of those Registrar and Transfer Agents (RTAs) servicing more than 2 crore folios. 3.45 Pension funds: In the NPS architecture there is a significant quantum of data and recordkeeping with the Central Recordkeeping Agency (CRA), the custodian, PFs and trustee banks whose safety and security are of primary concern to the regulator. In the context of emerging cyber security threats in the IT system, a ‘cyber security policy for intermediaries registered with PFRDA’ was proposed. As per the policy, the intermediary shall identify critical IT assets and risks associated with such assets, plans to protect assets by deploying suitable controls, tools and measures, plans to detect incidents, anomalies and attacks through appropriate monitoring tools/ processes, respond by taking immediate steps after identification of the incident, anomaly or attack and recover from the incident through incident management, disaster recovery and business continuity framework. The intermediary should also conduct suitable periodic drills to test the adequacy and effectiveness of the response and recovery plan. VIII. Supervision, enforcement and market surveillance 3.46 Taking note of the changes in the global and domestic financial sector environment, with a view to separating the function of identification of contravention of respective statutes/guidelines and directives by the regulated entities from imposition of punitive action and to make this process endogenous, formal and structured, a separate Enforcement Department has been created within the Reserve Bank in April 2017. The core function of the department is to enforce regulations and improve compliance with the overall objective of ensuring financial system stability and promoting public interest and consumer protection. The department will, inter alia, (i) develop a sound policy framework for enforcement consistent with international best practices; (ii) identify actionable violations on the basis of inspections/supervisory reports and market intelligence reports received/generated by it; (iii) conduct further investigations/verifications, if required, on actionable violations thus identified and enforce them in an objective, consistent and non-partisan manner; (iv) deal with the complaints referred to it by the management for possible enforcement action; and (v) act as a secretariat to the Executive Directors’ Committee constituted for adjudication. To begin with, the department will focus on the enforcement of penalty provisions in case of commercial banks, under section 47A of the Banking Regulation Act. The department has since developed a policy framework for enforcement and has initiated enforcement action. 3.47 Risk based supervision (RBS) for pension funds: Increasing interconnectedness and focus on managing contagion risks has shifted the supervisory approach from a compliance based to a risk based one. Adequate identification and analysis of the inherent risks will enable regulatory and supervisory authorities to undertake more comprehensive and prudent measures to address those risks and deploy the limited resources to contain any systemic risks more efficiently and effectively. In coordination with the Department of Financial Services, Ministry of Finance, PFRDA collaborated with the World Bank on two different themes – expansion of the NPS/APY coverage and introduction of RBS. The World Bank team assisted PFRDA in developing a basic framework on RBS on the basis of which it has initiated the pilot testing of intermediaries. The framework lays emphasis on financial performance, financial strength and the following six oversight/control functions: (i) board, (ii) senior management, (iii) compliance, (iv) risk management, (v) internal audit, and (vi) actuarial. 3.48 Risk based supervision of insurance companies: IRDAI has taken a significant step by initiating the process of building a risk based supervisory framework. In June 2016, it set up a committee on ‘Risk Based Capital’ to draw a roadmap on the implementation of a risk based capital system in India. The committee submitted its final report in July 2017. Consequently, a steering committee was formed to implement the Risk Based Capital (RBC) regime. Further, an internal project committee was also assigned with the task of studying and developing an appropriate framework for risk based supervision. IX. Consumer protection 3.49 The global financial crisis has highlighted the importance of consumer protection and financial literacy for financial stability. For instance, the stability of financial markets may be undermined when consumers assume more debt than they can afford or are misinformed about their financial options or obligations23. Today’s digital age and hyper-connected environment and competition amongst banks is leading to innovative complex financial products which are being marketed aggressively. This is leading to a rise in the incidence of frauds and misconduct and often the less informed and gullible consumers fall prey to fraudsters. This is corroborated from the data in respect of complaints relating to ATMs/Debit cards and credit cards24. Similarly, complaints on mis-selling of financial products are also gaining ground. A robust and responsive customer grievance redressal system is essential to build an environment of trust in the institutions with which the consumers entrust their savings and investments. A high volume of complaints combined with inadequate grievance redressal mechanism, can contribute significantly to systemic instability through the confidence channel. Thus, the robustness of this system in banks is, to an extent, a significant indicator of the health of banks. The number of complaints referred to the Banking Ombudsman have increased by nearly 21 per cent and 27 per cent in 2015-16 and 2016-1725 respectively. A major factor contributing to this rise in complaints is the approach of ground level staff of banks, who are not only less trained to deal with complainants and are given ‘tough’ target based incentives, but also are continuously being rotated and thus unable to justify their duties as front line staff. 3.50 The Reserve Bank is working on multiple fronts, to spread awareness, improve the level of customer service, strengthen the grievance redressal system, and enhance consumer protection. These, inter alia, include introducing Ombudsman Scheme for customers of select NBFCs, implementing the Internal Ombudsman scheme in select banks, and increasing the number of Offices of Banking Ombudsman from 15 to 20 in 2016-17. The Reserve Bank has also initiated the development of a comprehensive web-based application for lodging and processing of complaints with a view to provide end-to-end online grievance redressal mechanism. In order to enhance consumer education, awareness campaign is being intensified by Reserve Bank and efforts are being made to reach out to the last mile through SMSes using the RBISAY handle as well as through upcoming Centres for Financial Learning. With a view to create the requisite ecosystem to encourage and stabilise the digital payment mode, necessary protection by limiting the liability of customers in case of unauthorised electronic transactions in their account has been put in place (Table 3.2). 3.51 The Reserve Bank launched a mobile friendly portal Sachet (sachet.rbi.org.in) on August 4, 2016 to help the public as well as regulators to ensure that only regulated entities accept deposits from the public. The portal can be used by the public to obtain information regarding entities who accept deposits, share information and also to lodge and track complaints. The portal has a section for a closed user group – the state level co-ordination committees (SLCCs), an inter-regulatory forum, where they could exchange information and co-ordinate action on unauthorised deposit collection and financial activities. Complaints relating to such activities that have been lodged in Sachet have been taken up expeditiously for resolution. 3.52 In the insurance sector, IRDAI notified duly revised regulations on ‘protection of policyholders’ interests’ with a view to enhancing the effectiveness of the grievance redressal mechanism and other relevant aspects. It has also formed a Working Group on Visiting Product Structure for Dwellings, Offices, Hotels, Shops etc., and Micro, Small and Medium Enterprises for cover against fire and allied perils for recommending changes in the current product structure. Various consumer protection measures taken by regulators are given in Table 3.2. 1 https://www.bis.org/bcbs/publ/d416.pdf 2 BIS international banking statistics at end-June 2017. 3 Gross market value: Sum of the absolute values of all outstanding derivatives contracts with either positive or negative replacement values evaluated at market prices prevailing on the reporting date. It provides a more meaningful measure of market and counterparty credit risk than the outstanding notional amount. 4 Banks’ contractual commitments provided to third parties are subject to extant prudential measures such as capital and liquidity charges. 5 The taxation measure is unlikely to have a first order effect on household or corporate savings although the savings mix between debt and equity is likely to undergo modification. 6 Berle, A., Jr. and G. Means (1932), The Modern Corporation and Private Property. Chicago: Commerce Clearing House. 7 The twin balance sheet problem (TBS) refers to two balance sheet problems -- problem of overleverage in company balance sheets and problem of impaired assets in banks’ balance sheets. 8 On recommendations of the Committee on Financial System (Chairman: M. Narasimham). 9 Available at: /en/web/rbi/-/publications/reports/tables-21 10 The WG identified weak banks on the basis of two basic criteria as recommended by Committee on Banking Sector Reforms (CBSR): (a) accumulated losses and net NPAs being more than the net worth of the bank, or (b) operating profits less the income on recapitalisation bonds being negative for three consecutive years, and, seven additional parameters -- (i) capital adequacy ratio, (ii) coverage ratio, (iii) return on assets, (iv) net interest margin, (v) ratio of operating profit to average working funds, (vi) ratio of cost to income, and (vii) ratio of staff cost to net interest income (NII) + all other income. 11 Available at: www.rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&ID=784 12 Urjit R. Patel (2017), ‘Financial regulation and economic policies for avoiding the next crisis’, October 15 at the 32nd Annual G30 International Banking Seminar, Inter-American Development Bank, Washington, DC. 13 In addition, in the wake of Enron accounting scandal, the restrictions imposed on the audit firms through Sarbanes Oxley Act (in the United States) to provide non-audit (consulting) services for their audit clients has removed a potential source of conflict of interest. 14 Available at: http://www.iosco.org/library/pubdocs/pdf/IOSCOPD577.pdf 15 Thirty-eight IOSCO members from 36 jurisdictions. 16 Principle 3. An intermediary should maintain appropriate arrangements to safeguard the clients’ rights in client assets and minimise the risk of loss and misuse. 17 The Naresh Chandra Committee and the Dr J. J. Irani Committee constituted by the Ministry of Corporate Affairs; the Kumar Mangalam Birla Committee and the N. R. Narayana Murthy Committee constituted by SEBI. 18 Insurance and Financial Stability. Available at https://www.iaisweb.org/page/news/other-papers-and-reports//file/34041/insurance-and-financial-stability 19 Two life insurance companies, two general insurance companies and one reinsurance company. 20 Offer for sale is essentially offloading existing equities held by the shareholders. OFS essentially means change of ownership of existing equities and does not lead to addition of fresh equities. 21 Basic savings bank deposit accounts (BSBDA) are considered as a normal banking service available to all customers and offer the following minimum common facilities: (i) no minimum balance, (ii) services include deposits and withdrawal of cash at bank branches as well as ATMs; receipt / credit of money through electronic payment channels or by means of deposit / collection of cheques drawn by central / state government agencies and departments; (iii) no limit on the number of deposits in a month, but a maximum of four withdrawals in a month, and (iv) ATM/TM-cum-debit cards. 22 FSB: Finanical Stability implications for FinTech (27 June, 2017). 23 Pulse of Fintech Q3’17, Global Analysis of Investment in Fintech, KPMG International. 23 World Bank Report, 2010 : Diagnostic Review of Consumer Protection and Financial Literacy. 24 18.9% of complaints in 2016-17 under Banking Ombudsman Scheme (BOS) relate to ATM/Debit and Credit cards. 25 Number of complaints -2014-15: 85,131; 2015-16: 1,02,894; and 2016-17: 1,30,987. |

Install the RBI mobile application and get quick access to the latest news!

Scan the QR code to install our app

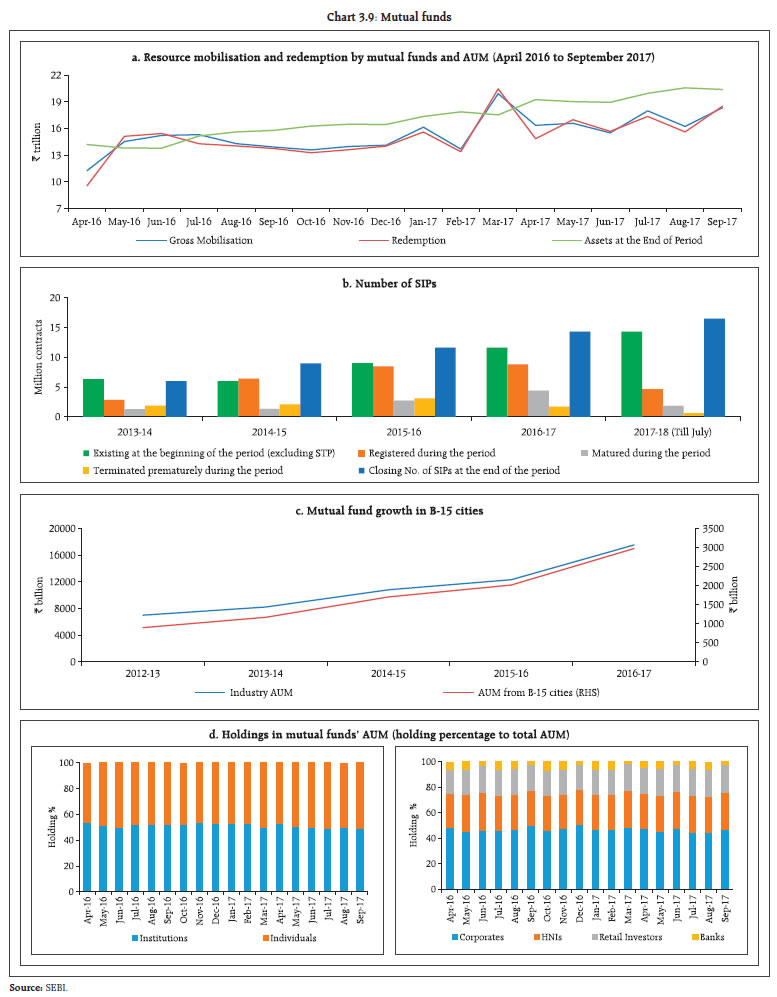

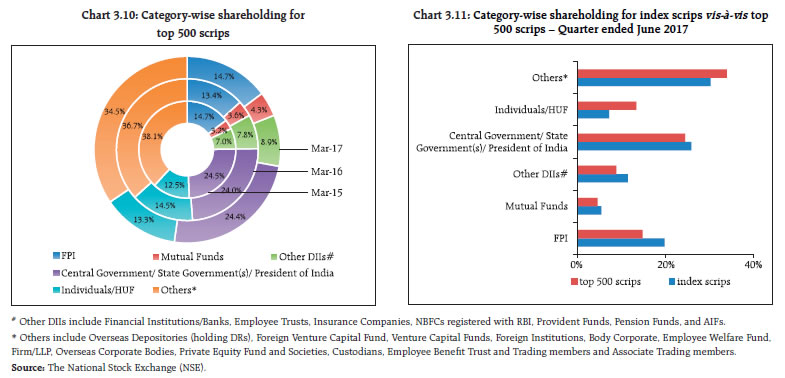

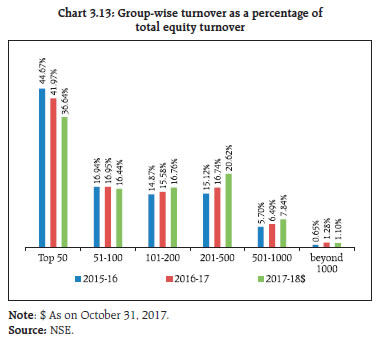

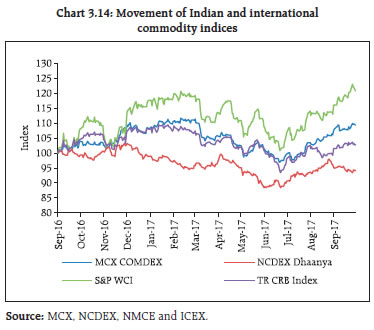

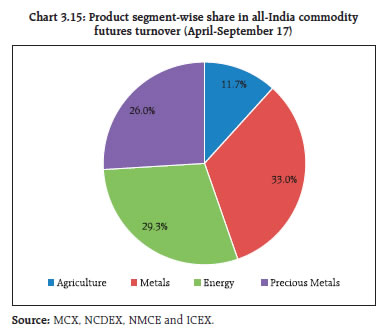

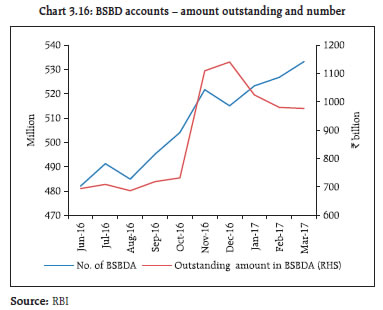

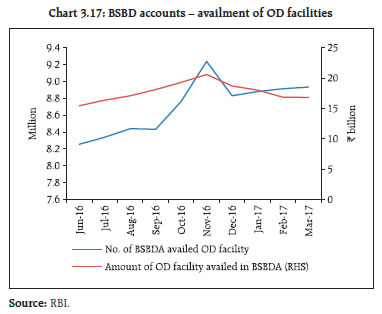

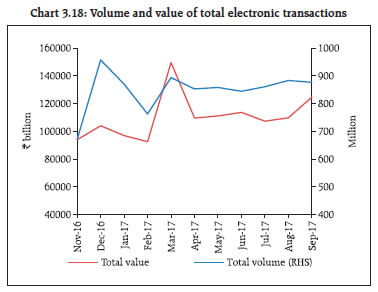

Page Last Updated on: