IST,

IST,

Pilot Survey on Indian Startup Sector - Major Findings

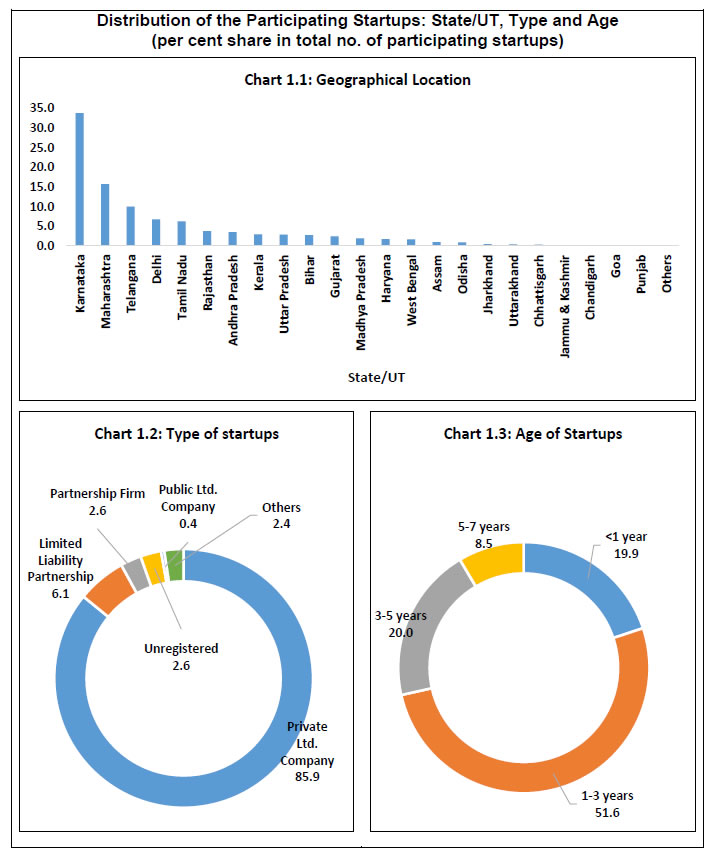

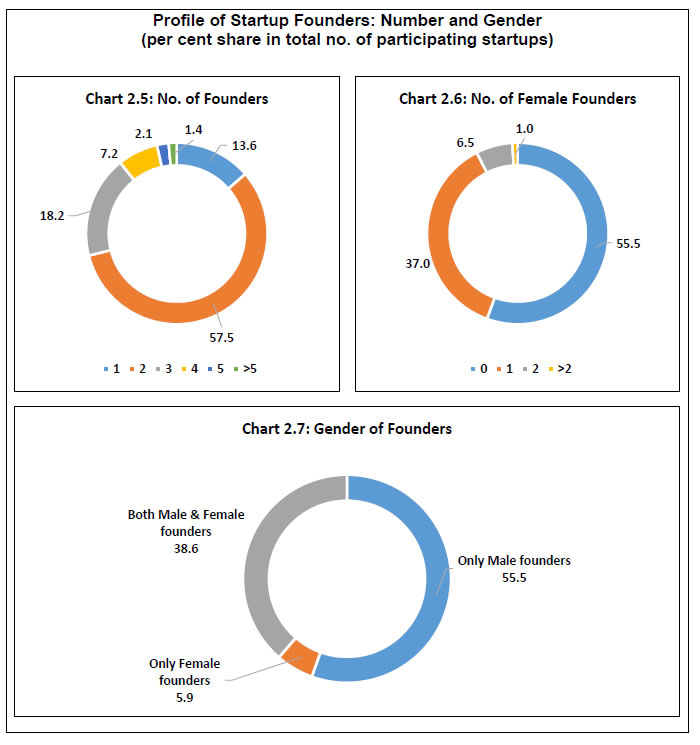

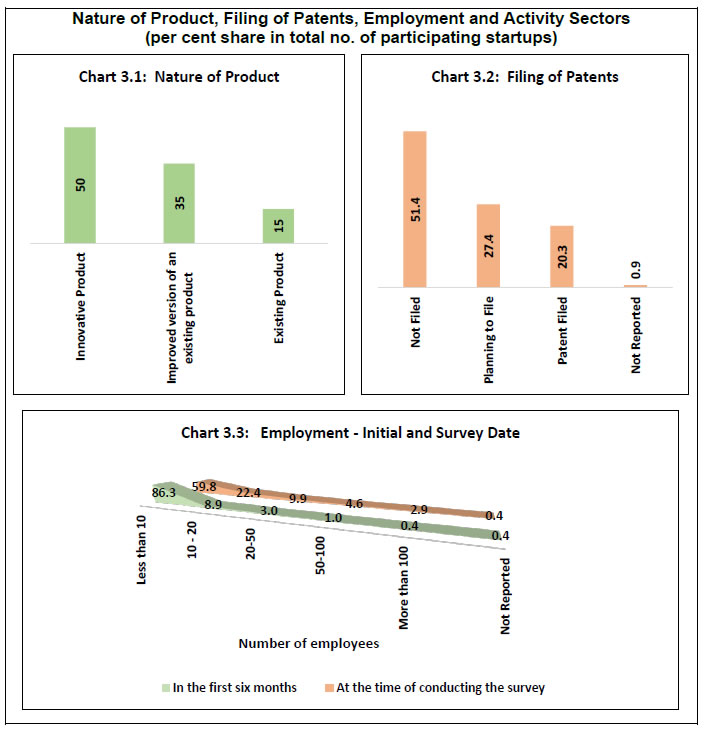

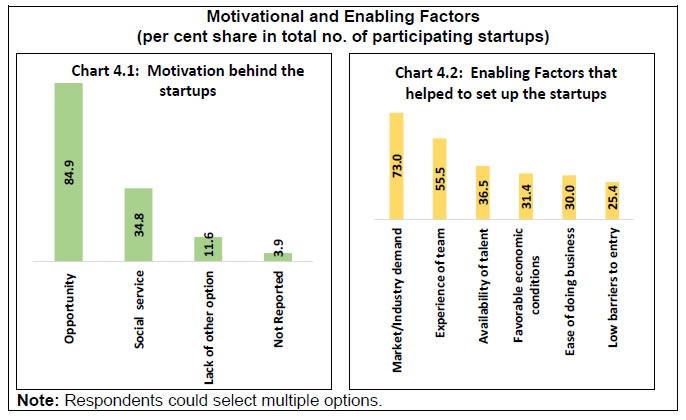

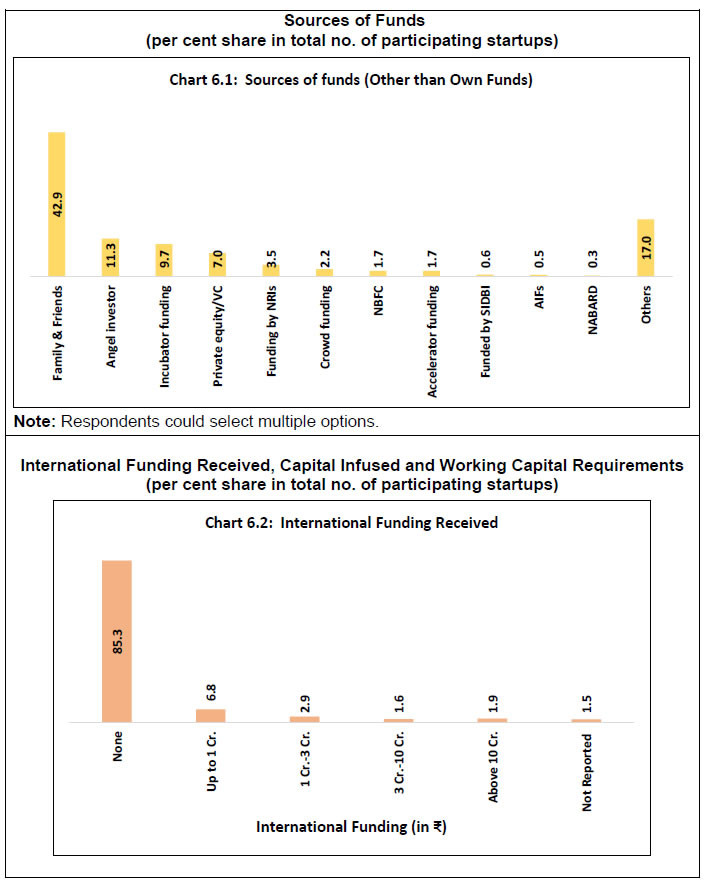

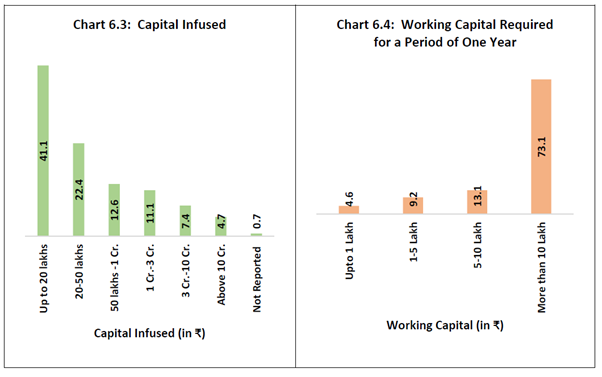

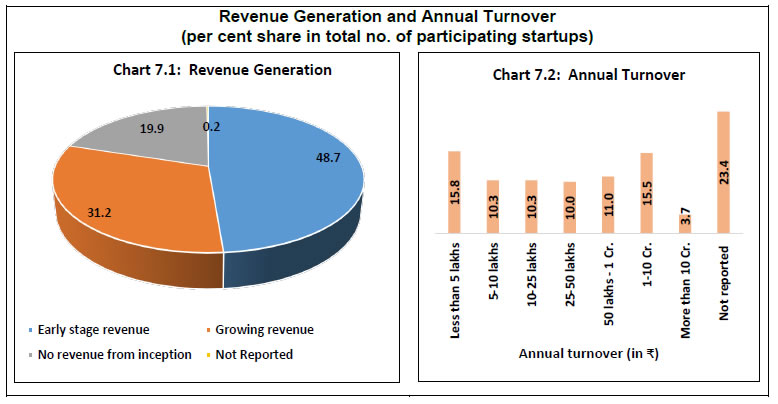

Findings from a pilot survey on Indian startup sector conducted by the Reserve Bank are presented in this document. It presents the feedback received from the survey respondents and does not reflect the views of the Bank. Comments/suggestions are solicited from stakeholders on the findings of the survey as well as on methodology, usefulness of information and scope for improvement in the survey. The same may be forwarded to - The Director, E-Commerce and New Age Survey Division, Department of Statistics and Information Management, Reserve Bank of India, C-8, 2nd floor, Bandra-Kurla Complex, Bandra (East), Mumbai-400051; e-mail. 1.The Reserve Bank conducted a pilot survey on Indian startup sector during November 2018 to April 2019. A total of 1,246 startups (public/private limited companies, partnership firms, limited liabilities partnerships and others) participated in the survey. Around three-fourths of respondents were from the states of Karnataka, Maharashtra, Telangana, Delhi and Tamil Nadu. 2.Startups in six sectors, viz., agriculture, data & analytics, education, health, IT consulting/solution and manufacturing accounted for nearly 50 per cent of the survey respondents. 3.Respondents cited market/industry demand and team experience as the major enabling factors for setting up the startups. Both domestic markets (mainly semi-urban, urban and metropolitan areas in India) and foreign countries were the target destination of the startups. 4.Almost half of the respondents informed that they were in an early stage of revenue generation while 31 per cent were in a growing stage. Of the remaining startups which were yet to generate any revenue, as high as 86 per cent were aged below three years. 5.The annual turnover for over one-fourths of the respondents was up to ₹ 10 lakhs whereas around 20 per cent startups did not report any revenue generation. Less than one-fifths of the respondents reported that their turnover exceeded ₹ 1 crore. 6.Only 14 per cent of startups had more than 10 employees in the first six months of their operation but as the sector matured, the share increased to 40 per cent at the time of conducting the survey. 7. Around 36 per cent of the startups availed institutional loans (including from banks) to finance their activities. Pilot Survey on Indian Startup Sector - Major Findings 1.1 In view of the emerging importance of the startup sector in the Indian economy, the Reserve Bank of India (RBI) conducted a pilot survey on Indian startup sector during November 2018 to April 2019. Responses were received from 1,246 startups. This report presents the major findings of the survey. 1.2 The structure of the report is as follows: section 2 presents the objectives of the survey while the survey coverage and design are briefly described in section 3. Major findings from the survey are discussed in section 4 and the conclusions are summarised in section 5. 2.1 Startups are ignited by entrepreneurial and innovative spirit in an economy and play an important role in its growth. The pilot survey was aimed at collecting information on select important characteristics of the startup sector, viz., geographical, institutional and age profile of the sector, academic, professional and gender profile of the founders, motivational factors, turnover, workforce, target markets, types of products, technology used, sources of funds and future plans (the survey questionnaire is provided in the Annex). 3.1 The pilot survey approached the following target groups: (a) startup entities recognised by the Department for Promotion of Industry and Internal Trade (DPIIT) of the Ministry of Commerce and Industry, Government of India; and (b) entities under incubators/accelerators1 with age not more than seven years2, which might be outside the DPIIT list and could also participate in the survey by downloading the survey questionnaire from RBI website. Keeping in view the objectives, the pilot survey collected information on certain important aspects such as profiles of the startups and their founders, nature of products, sources of funds and future plans. Salient observations on these aspects are presented below. 4.1 Startup Sector in India: The Contours The summary profile of the survey respondents is presented below. 4.1.1 Nearly three-fourths of the participants were from the states of Karnataka, Maharashtra, Telangana, Delhi and Tamil Nadu, indicating large concentration of the startup sector in India in a few states (Chart 1.1). 4.1.2 Private efforts spearhead the startup sector in India: nearly 86 per cent of the participating startups were private limited companies (Chart 1.2). 4.1.3 Over 70 per cent of the participating startups were set up in the last three years (i.e., in the period from 2016-17 to 2018-19) (Chart 1.3).  Founders of the startup sector are business initiators and the entrepreneurs, and a gist of their profile is given below. 4.2.1 Nearly 88 per cent of the founders had academic qualification of at least a bachelor’s degree (Chart 2.1). Over 10 per cent of the founders were below 25 years of age and another 55 per cent were in the age group 25 to 40 years (Chart 2.2). 4.2.2 One third of the founders had academic background in engineering (Chart 2.3). A majority of the founders had professional experience and 7.3 per cent of the founders were still students (Chart 2.4).  4.2.3 Most of the startups had at least two co-founders (Chart 2.5). Nearly 45 per cent of the participating startups had at least one female founder (Chart 2.6). In all, 5.9 per cent of the participating startups were founded by only females in comparison to 55.5 per cent by only male founders. The remaining 38.6 per cent of the participating startups had both male and female as co-founders (Chart 2.7).  4.3 Product Innovation and Sectoral Spread Product innovation often drive startups, who develop entrepreneurship, propel productivity gains and create employment opportunities across economic sectors. The pilot survey reflected on some of these aspects, which are presented below. 4.3.1 Around half of the participating startups dealt in innovative products and over 20 per cent had filed patents for their products whereas another 27 per cent were planning to file patents (Charts 3.1 and 3.2). 4.3.2 Only 14 per cent of startups had more than 10 employees in the first six months of their operation but, as the sector matured, this share increased to nearly 40 per cent at the time of conducting the survey (Chart 3.3). 4.3.3 Startups worked in diverse areas of activities, where emerging sectors had a fair share (Chart 3.4). Data analytics was the leading sector followed by health, education and agriculture.   4.4 Motivation and Professional Support The pilot survey shed light on the motivation behind the startup founders’ entrepreneurial spirit. 4.4.1 An overwhelming majority of the startups aimed to capitalise on available opportunities. Many of them were inspired by multiple reasons and a substantial section of them also intended to serve social causes (Chart 4.1). Their efforts were facilitated by favourable market/industry demand perception as well as reassurances on human resources in terms of internal experience and availability of talent (Chart 4.2).  4.4.2 Entities were accessing professional support mainly from mentors & advisers. They also enlisted support of chartered accountants/company secretaries. 4.5 Technology, Customers and Markets Use of the latest or innovative technology often helps startup business in differentiating from others and taking advantage vis-a-vis the traditional business, which they need to supplement with sound strategy for marketing their innovative products. Major features on these aspects are presented below. 4.5.1 Around a third of the startups used online marketing, big data analytics, machine learning and internet of things (IoT) for their business (Chart 5.1). 4.5.2 Most of the respondents targetted business to business (B2B) and business to consumer (B2C) channels for selling their products (Chart 5.2). 4.5.3 Startups targetted both domestic and foreign markets: for business within India, they targetted both urban and rural markets, with a preference for the former (Chart 5.3).  Following are the major features of capital support for entrepreneurial activities of the participating startups. 4.6.1 Families & friends emerged as the largest source of funding (around 43 per cent), apart from own funds (Chart 6.1). 4.6.2 About 13 per cent of the startups received international funding (Chart 6.2). 4.6.3 Over three-fourths of the startups had up to ₹ one crore of capital investment, whereas around 41 per cent infused capital up to ₹ 20 lakhs each. On the other hand, nearly 5 per cent startups infused capital above ₹ 10 crore each (Chart 6.3). 4.6.4 Nearly three-fourths of the startups had working capital requirements of more than ₹10 lakh for a year (Chart 6.4). 4.6.5 Around 36 per cent of the participating startups availed loans from institutions (including banks). Only 1.7 per cent of the startups availed external commercial borrowings.   4.7 Financial Performance and Constraints Reported The pilot survey also endeavoured to get some ideas about the financial performance of the participating startups. Following are the noteworthy observations in this regard. 4.7.1 Almost a half (49 per cent) of the respondents informed that they were in early stage of revenue generation while another 31 per cent were in growing stage (Chart 7.1). Of the remaining startups, which were yet to generate any revenue, as high as 86 per cent were aged below three years. 4.7.2 While one-fourth of the respondents reported annual turnover up to ₹ 10 lakhs, nearly one-fifth reported annual turnover above ₹ 1 crore (Chart 7.2). Nearly a quarter of the respondents did not report turnover.  4.7.3 Access to new markets, finance and lack of skilled labour/technology/talent/distribution channel were some of the constraints cited by the respondents. The participating startups were asked about their future plans and a summary of their feedback is given below. 4.8.1 Almost 58 per cent of the startups had plans to get listed on the Indian stock exchanges in the next five years (Chart 8.1). Most of these startups were in health, software development, IT consulting/solution sectors and were of age less than three years. 4.8.2 About 24 per cent of the respondents intended to seek acquisition at a later date (Chart 8.2). Such startups were mostly in product development, software development and IT consulting/solution sectors and were of age less than three years. 4.8.3 Over 63 per cent of the respondents reported to have plans to hire at least 20 new employees in the next two to three years (Chart 8.3). These startups were mainly from software development, IT consulting/solution and health sectors and were of age less than three years. 4.8.4 About 10 per cent of the respondents had intentions to exit (Chart 8.4). Funding requirements and market conditions were reported as major reasons for such intentions.  This pilot survey shed light on certain important aspects of the startup sector in the Indian economy. Participants reported market/industry demand and team experience as the most important factors for setting up the startups. The survey revealed that startups were able to augment employment generation as they grew. Data and analytics, health, education and agriculture were major startup sectors in the country. Some of the constraints cited by the startups pertained to access to new markets, finance and lack of skilled labour/technology/talent/distribution channel. Future plans of the startups included hiring staff for supporting business expansion, getting listed on the Indian stock exchanges and seeking acquisition, among others.

1 An accelerator is typically a 3-4 month program for startups at early traction and scaling stage. It is a process of intense, rapid and immersive education aimed at accelerating the growth of the startup. The accelerator may take a set amount of seed equity from the startups in their cohorts in exchange for capital and mentorship. An incubator is a workspace created to offer early-stage startups access to all resources they need under one roof. They provide office space, mentoring, business services, funding, and networking opportunities to the incubatees. (Source: Startup India Kit, October 2019, DPIIT, GoI). 2 As per the Gazette notification G.S.R. 364 (E) dated 11th April, 2018, an entity shall be considered as a startup up to seven years from the date of its incorporation/registration (in the case of startups in the biotechnology sector, the period is upto ten years from the date of its incorporation/registration) if it is incorporated as a private limited company (as defined in the Companies Act, 2013) or registered as a partnership firm (registered under section 59 of the Partnership Act, 1932) or a limited liability partnership (under the Limited Liability Partnership Act, 2008) in India; turnover of the entity for any of the financial years since incorporation/registration has not exceeded Rs. 25 crore; entity is working towards innovation, development or improvement of products or processes or services, or if it is a scalable business model with a high potential of employment generation or wealth creation; the Gazette notification however provided that an entity formed by splitting up or reconstruction of an existing business shall not be considered a ‘startup’. This pilot survey was launched in November 2018 and followed the above criteria. Subsequently, in the notification G.S.R. 127(E) dated 19th February, 2019, the seven years’ period was increased up to ten years across all sectors of startups and turnover limit was increased to not exceeding Rs. 100 crore. |

Install the RBI mobile application and get quick access to the latest news!

Scan the QR code to install our app

Page Last Updated on: