IST,

IST,

Master Direction - Reserve Bank of India (Securitisation of Standard Assets) Directions, 2021 (Updated as on December 05, 2022)

updated-as-on:

- 2022-12-05

- 2021-09-24

|

RBI/DOR/2021-22/85 September 24, 2021 All Scheduled Commercial Banks (including Small Finance Banks but excluding Regional Rural Banks); Master Direction – Reserve Bank of India (Securitisation of Standard Assets) Directions, 2021 Please refer to the Draft Framework for Securitisation of Standard Assets that was released on June 8, 2020 for comments from various stakeholders. 2. Based on the examination of the comments received, the Reserve Bank has issued the Master Direction – Reserve Bank of India (Securitisation of Standard Assets) Directions, 2021, which are enclosed. These directions have been issued in exercise of the powers conferred by the Sections 21 and 35A of the Banking Regulation Act, 1949; Chapter IIIB of the Reserve Bank of India Act, 1934; and Sections 30A, 32 and 33 of the National Housing Bank Act, 1987. 3. These directions come into immediate effect replacing the existing instructions on the matter of securitisation of standard assets. All lending institutions are advised to take necessary steps to ensure compliance with these directions. Yours faithfully, (Manoranjan Mishra) DOR.STR.REC.54/21.04.177/2021-22 September 24, 2021 Master Direction – Reserve Bank of India (Securitisation of Standard Assets) Directions, 2021 Introduction Securitisation involves transactions where credit risk in assets are redistributed by repackaging them into tradeable securities with different risk profiles which may give investors of various classes access to exposures which they otherwise might be unable to access directly. While complicated and opaque securitisation structures could be undesirable from the point of view of financial stability, prudentially structured securitisation transactions can be an important facilitator in a well-functioning financial market in that it improves risk distribution and liquidity of lenders in originating fresh loan exposures. Given the above, in exercise of the powers conferred by the Sections 21 and 35A of the Banking Regulation Act, 1949; Chapter IIIB of the Reserve Bank of India Act, 1934; and Sections 30A, 32 and 33 of the National Housing Bank Act, 1987, the Reserve Bank, being satisfied that it is necessary and expedient in the public interest so to do, hereby, issues the directions hereinafter specified. Short title and commencement 1. These directions shall be called the Reserve Bank of India (Securitisation of Standard Assets) Directions, 2021. 2. These directions shall come into force with immediate effect. Chapter I: Scope and Definitions A. Applicability and Purpose 3. The provisions of these directions shall apply to the following entities (collectively referred to as lenders in these directions) unless specifically mentioned otherwise:

4. These directions will be applicable to securitisation transactions undertaken subsequent to the issue of these directions. B. Definitions 5. For the purpose of these directions, the following definitions apply: (a) “bankruptcy remote" means the unlikelihood of an entity being subjected to voluntary or involuntary bankruptcy proceedings, including by the originator or the creditors to the originator; (b) “clause” means a clause of these directions, unless otherwise specified; (c) “clean-up call” means an option that permits the originator to call the underlying exposures or the securitisation exposures when the outstanding value of the underlying exposures falls below a pre-defined threshold, thereby extinguishing the remaining securitisation exposures of all parties; (d) “credit enhancement” means a contractual arrangement in which an entity mitigates the credit risk associated with a securitisation exposure and, in substance, provides some degree of added protection to other parties to the transaction so as to mitigate the credit risk of their securitisation exposures; (e) “early amortisation provision” means a mechanism that, once triggered, accelerates the reduction of the investor’s interest in underlying exposures of a securitisation structure and allows investors to be paid out prior to the originally stated maturity of the securitisation notes issued; (f) “excess spread (or future margin income)” means the difference between the gross finance charge collections and other income received by the special purpose entity (SPE), and securitisation notes interest, servicing fees, charge-offs, and other senior SPE expenses. (g) “exposure amount” of a securitisation exposure means the sum of the on-balance sheet amount of the exposure, or carrying value – which takes into account purchase discounts and writedowns/specific provisions the lender took on this securitisation exposure – and the off-balance sheet exposure amount, where applicable. (h) "first loss facility" means the first level of financial support provided by the originator or a third party to improve the creditworthiness of the securitisation notes issued by the SPE such that the provider of the facility bears the part or all of the risks associated with the assets held by the SPE; (i) “implicit support” means the protection arising when a lender provides support to a securitisation in excess of its predetermined contractual obligation; (j) “interest-only strip (I/O)” means an on-balance sheet asset of the originator that represents a valuation of cash flows related to future margin income;

(k) “mortgage backed securities” mean securitisation notes issued by the special purpose entity against underlying exposures that are all secured by commercial or residential real estate mortgages; (l) "originator" refers to a lender that transfers from its balance sheet a single asset or a pool of assets to an SPE as a part of a securitisation transaction and would include other entities of the consolidated group to which the lender belongs;

(m) “overcollateralisation” means any form of credit enhancement by virtue of which underlying exposures are posted in value which is higher than the value of the securitisation notes; (n) “replenishment” means the process of using the cash flows from the securitised assets to acquire more assets in the manner disclosed upfront in the prospectus of the scheme, which will continue for a pre-announced replenishment period, following which the securitisation structure switches to an amortising one;

(o) “residential mortgage backed securities (RMBS)” mean securitisation notes issued by the special purpose entity against underlying exposures that are all secured by residential mortgages; (p) “re-securitisation exposure” means a securitisation exposure where at least one of the underlying exposures is a securitisation exposure; (q) “standard assets” for the purpose of these directions shall mean exposures which are not classified as non-performing asset; (r) “second loss facility” means a second level of financial support providing a second (or subsequent) tier of protection to the securitisation notes issued by the special purpose entity against potential losses not covered by the first loss facility, and is invoked only after the first loss facility has been drawn down and repudiated or exhausted, or the first loss provider is under insolvency or bankruptcy or liquidation; (s) “securitisation” means a structure where a pool of assets are transferred by an originator to a SPE and the cash flow from this pool of assets is used to service securitisation exposures of at least two different tranches reflecting different degrees of credit risk, where payments to the investors depend upon the performance of the specified underlying exposures, as opposed to being derived from an obligation of the originator;

(t) “securitisation exposures” include but are not restricted to exposures to securitisation notes issued by the special purpose entity including asset-backed securities and mortgage-backed securities, credit enhancements, underwriting commitments, liquidity facilities, interest rate or currency swaps, credit derivatives and tranched cover;

(u) “securitisation notes” mean securities issued by the special purpose entity as a part of securitisation; (v) “senior tranche” means a tranche which is effectively backed or secured by a first claim on the entire amount of the assets in the underlying securitised pool;

(w) “special purpose entity (SPE)” means a company, trust or other entity organised for a specific purpose, the activities of which are limited to those appropriate to accomplish the purpose of the SPE, and the structure of which is intended to isolate the SPE from the credit risk of an originator;

(x) “subordinate tranche” means any tranche that is junior to the senior tranche(s); (y) “synthetic securitisation” means a structure where credit risk of an underlying pool of exposures is transferred, in whole or in part, through the use of credit derivatives or credit guarantees that serve to hedge the credit risk of the portfolio which remains on the balance sheet of the lender;

(z) “tranche” means a contractually established segment of the credit risk associated with an exposure or a pool of exposures, where a position in the segment entails a risk of credit loss greater than or less than a position of the same amount in another segment, without taking account of credit protection provided by third parties directly to the holders of positions in the segment or in other segments;

(aa) “tranche maturity” means the tranche’s effective maturity in years, and is measured as prescribed in Section E of Chapter VI of these directions; (bb) “tranche thickness” means the measure calculated as detachment point (D) minus attachment point (A), where D and A are calculated in accordance with Section D of Chapter VI of these directions; Chapter II: General requirements for securitisation A. Assets eligible for securitisation 6. Lenders, including overseas branches of Indian banks, shall not undertake the securitisation activities or assume securitisation exposures as mentioned below: a. Re-securitisation exposures; b. Structures in which short term instruments such as commercial paper, which are periodically rolled over, are issued against long term assets held by a SPE c. Synthetic securitisation; and d. 1Securitisation with the following assets as underlying:

Provided that loans with tenor up to 24 months extended to individuals for agricultural activities (as described in Chapter III of the Reserve Bank of India (Priority Sector Lending – Targets and Classification) Directions, 2020) where both interest and principal are due only on maturity and trade receivables with tenor up to 12 months discounted/purchased by lenders from their borrowers will be eligible for securitisation. However, only those loans/receivables will be eligible for securitisation where a borrower (in case of agricultural loans) /a drawee of the bill (in case of trade receivables) has fully repaid the entire amount of last two loans/receivables (one loan, in case of agricultural loans with maturity extending beyond one year) within 90 days of the due date. In case such assets are securitised, the investors in the securitisation notes issued against them should be able to verify the compliance of the underlying asset with the above requirement. 7. It is clarified that securitisation of exposures held by overseas branches of Indian banks shall not contravene any provision/s of extant legal/regulatory framework, including Foreign Exchange Management Act, 1999 and the rules or regulations thereunder. 8. Subject to the above, all other on-balance sheet exposures of originators, which are in the nature of loans and advances and are classified as Standard, are eligible as underlying assets in a securitisation transaction. 9. The originators of such exposures shall have satisfied the Minimum Holding period requirement as per Clause 39 of the Reserve Bank of India (Transfer of Loan Exposures) Directions, 2021 including the proviso to the above Clause.2 3Provided that for commercial or residential real estate mortgages, MHP shall be counted from the date of full disbursement of the loan, or registration of security interest with Central Registry of Securitisation Asset Reconstruction and Security Interest of India (CERSAI), whichever is later. 10. The MHP will be applicable to individual loans in the underlying pool of securitised loans. MHP will not be applicable to loans referred to in the proviso to Clause 6. 11. The transactions undertaken in terms of these directions must not contravene the rights of underlying obligors. To ensure compliance with this stipulation, enabling clauses must be included in the contract between originator and servicing agent and all necessary consent from obligors (including from third parties), where necessary as per the respective contracts, should have been obtained. B. Minimum Retention Requirement (MRR) 12. The MRR is primarily designed to ensure that the originators have a continuing stake in the performance of securitised assets so as to ensure that they carry out proper due diligence of loans to be securitised. The originators should adhere to the MRR as detailed below while securitising loans leading to issuance of securitisation notes other than residential mortgage backed securities:

13. In the case of residential mortgage backed securities, the MRR for the originator shall be 5% of the book value of the loans being securitised, irrespective of the original maturity. 14. The MRR shall be retained by the originator as follows: a. Upto 5 per cent of the book value of loans being securitised:

b. Greater than 5 per cent of the book value of loans being securitised:

15. Investment in the Interest Only Strip representing the Excess Interest Spread/ Future Margin Income, whether or not subordinated, will not be counted towards the MRR. 16. MRR should not be reduced either through hedging of credit risk or selling or encumbering the retained interest. MRR has to be maintained by the originating lender itself and not by any of its group entities. The form of MRR should not change during the life of securitisation. The MRR as a percentage of unamortised principal should be maintained on an ongoing basis except for reduction of retained exposure due to repayment or through the absorption of losses. Specifically, in cases of securitisations featuring replenishment period, MRR should be maintained not only at the initiation of the securitisation but also at the end of the replenishment period. 17. For complying with the MRR under these guidelines lenders should ensure that proper documentation in accordance with law is made. C. Origination Standards 18. Underwriting standards for exposures securitised should not be less stringent than those applied to exposures retained on the balance sheet of the originator. Where underwriting standards change between the loan origination and till all the claims associated with securitised note are paid-off, the originator should disclose to the entities having securitisation exposures the timing and purpose of such changes. 19. In cases of securitisation of exposures purchased by originator from other lenders, the requirements applicable for underwriting standards shall apply to the standards of due diligence process adopted by the originator which may include verification of sufficiency and consistency of loan origination process of the lender from whom the exposures were purchased by the originator. D. Payment priorities and observability 20. To prevent investors being subjected to unexpected repayment profiles during the life of a securitisation, the priorities of payments for all liabilities in all circumstances should be clearly defined at the time of securitisation and appropriate legal comfort regarding their enforceability should be provided. 21. To help provide investors with full transparency over any changes to the cash flow waterfall, payment profile or priority of payments that might affect a securitisation, all triggers affecting the cash flow waterfall, payment profile or priority of payments of the securitisation should be clearly and fully disclosed in offer documents and in investor reports, with information in the investor report that clearly identifies the breach status in respect of expected cash flows to the note holders, the ability for the breach to be reversed and the consequences of the breach. 22. To ensure rights and interest of the securitisation note holders are protected, definitions, policies and remedies pertaining to the contours and caveats around the performance of the underlying loans must be suitably communicated. Further, the rights and control of the securitisation note holders must be documented to account for all circumstances, including insolvency of all entities involved in securitisation, such as the originator SPE, etc. Full disclosure and supporting documentation regarding legal and financial risk factors must be made available to prospective and existing investors within a reasonable period of time, on an ongoing or on demand basis. 23. Securitisations featuring a replenishment period should include provisions for appropriate early amortisation events and/or triggers of termination of the replenishment period, including, notably:

24. In the event actions of associated institutional stakeholders (originator, SPE, servicing agent, credit enhancement provider and others) that are not prohibited in this framework, result in material alteration of the risk profile of the securitisation notes at any point, the originator shall ensure that same is adequately informed and disclosed to investors, credit rating agencies and other service providers within a maximum time frame of 14 calendar days. E. Limit on Total Retained Exposures by Originators 25. The total exposure of an originator to the securitisation exposures belonging to a particular securitisation structure or scheme should not exceed 20% of the total securitisation exposures created by such structure or scheme. However, the exposure of originators to credit enhancing interest only strip shall be excluded from this limit. 26. Credit exposure on account of interest rate swaps/currency swaps entered into with the SPE will be excluded from this limit. 27. The 20% limit on total retained exposures will not be deemed to have been breached if it is exceeded due to amortisation of securitisation notes issued. F. Issuance and Listing 28. The minimum ticket size for issuance of securitisation notes shall be Rs.1 crore. 4Explanation: Ticket size, for the purpose of these directions, refers to the size of investment by a single investor. 29. Listing of securitisation notes, especially in respect of certain product class, such as RMBS, and/or generally above a certain threshold is recommended, though not mandatory. In any case, any offer of securitisation notes to fifty or more persons in an issuance would be required to be listed in terms of Securities and Exchange Board of India (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008. G. Conditions to be satisfied by the special purpose entity 30. The SPE should meet the following criteria to enable the originator to apply the guidelines on capital adequacy and other aspects as prescribed in these directions with regard to the securitisation exposures assumed by it: a. Any transaction between the originator and the SPE should be strictly on arm’s length basis. b. The SPE and the trustee should not resemble in name or imply any connection or relationship with the originator of the assets in its title or name. c. The originator should not have any ownership, proprietary or beneficial interest in the SPE except those specifically permitted under these directions. The originator should not hold any share capital in the SPE. d. The originator should not have more than one representative, without veto power, on the board of the SPE provided the board has at least four members and independent directors are in majority. e. If the SPE is set up as a trust, then:

f. The originator shall not support the losses of the SPE except under the facilities explicitly permitted under these directions and shall also not be liable to meet the recurring expenses of the SPE. g. The SPE should make it clear to the investors in the securitisation notes issued by it that these securitisation notes are not insured and that they do not represent deposit liabilities of the originator, servicer or trustees. 31. In cases where the originator has purchased loans from another lender, the provisions of Clause 30 shall apply to the lender from whom the originator has purchased the exposures, as well.

H. Representations and Warranties 32. An originator that sells assets to SPE may make representations and warranties concerning those assets. The originator will be required to hold capital against such representations and warranties if any of the following conditions are not satisfied: a. Any representation or warranty is provided only by way of a formal written agreement. b. The originator undertakes appropriate due diligence before providing or accepting any representation or warranty. c. The representation or warranty refers to an existing state of facts that is capable of being verified by the originator at the time the assets are sold. d. The representation or warranty is not open-ended and, in particular, does not relate to the future creditworthiness of the assets, the performance of the SPE and/or the securitisation notes the SPE issues. e. The exercise of a representation or warranty, requiring an originator to replace assets (or any parts of them) sold to a SPE, must be:

f. An originator that is required to pay damages for breach of representation or warranty can do so provided the agreement to pay damages meets the following conditions:

g. An originator should notify RBI (Department of Supervision) of all instances where it has agreed to replace assets sold to SPE or pay damages arising out of any representation or warranty. I. Accounting provisions 33. Originators shall sell assets to SPE only on cash basis and the sale consideration should be received not later than the transfer of the asset to the SPE. Further, there should not be gap of more than 30 days between transfer of the assets and the issuance of securitisation notes. 34. NBFCs which are required to comply with Indian Accounting Standards (IndAS) shall continue to be guided by the Standards and the ICAI Advisories with respect to accounting for securitisation exposures and transactions. 35. In case of other lenders, any loss, profit or premium realised at the time of the sale should be accounted accordingly and reflected in the Profit & Loss account for the accounting period during which the sale is completed. 36. For such lenders specified at Clause 35, the following treatment shall be applicable in the case of unrealised gains arising out of sale of underlying assets to the SPE such as that associated with expected future margin income (represented by interest-only strips or otherwise):

Chapter III: Simple, transparent and comparable (STC) securitisations 37. Only securitisations that additionally satisfy all the criteria laid out in Annex 1 of these directions fall within the scope of the STC framework. The above criteria are based on the prescriptions of the Basel Committee on Banking Supervision. Exposures to securitisations that are STC-compliant can be subject to the alternative capital treatment as determined by Clauses 108 to 110. 38. The originator must disclose to investors all necessary information at the transaction level to allow investors to determine whether the securitisation is STC-compliant. Based on the information provided by the originator, the investor must make its own assessment of the securitisation‘s STC compliance status before applying the alternative capital treatment. 39. For securitisation exposures retained by the originator, where significant credit risk transfer in terms of the requirements of the Clauses 81 and 82 have been achieved by the originator, the determination of compliance with STC requirements shall be made by the originator. 40. STC criteria need to be met at all times. Checking the compliance with some of the criteria might only be necessary at origination (or at the time of initiating the exposure, in case of guarantees or liquidity facilities) of an STC securitisation. Notwithstanding, investors and holders of the securitisation positions are expected to take into account developments that may invalidate the previous compliance assessment, for example deficiencies in the frequency and content of the investor reports, in the alignment of interest, or changes in the transaction documentation at variance with relevant STC criteria. 41. In cases where the criteria refer to underlying, and the pool is dynamic, the compliance with the criteria will be subject to dynamic checks every time that assets are added to the pool. The criteria for the addition of assets shall be clearly described in relevant transaction documents. 42. Investors should consider whether the originator, servicer and other parties with a fiduciary responsibility to the securitisation note holders have an established performance history for substantially similar credit claims or receivables to those being securitised and for an appropriately long period of time. 43. RBI would verify the preferential regulatory capital treatment assignments made by the lenders, including the originator, as part of the supervisory review. If it is discovered that a transaction does not satisfy the STC criteria for regulatory capital purposes, RBI would take appropriate supervisory action including inter alia additional capital under the Pillar 2 framework, and/or by denying preferential regulatory capital treatment for that specific transaction and potentially others as well. Chapter IV: Provision of facilities supporting securitisation structures A. General conditions 44. Lenders may provide supporting facilities such as credit enhancement facilities, liquidity facilities, underwriting facilities and servicing facilities. Apart from lenders, since such facilities may also be provided by entities that are not lenders, entities providing such facilities are generally referred to in these directions as “facility providers”. Such facility provider(s) must be regulated by at least one financial sector regulator. 45. The facilities, as above, provided by facility providers should satisfy the following conditions, in addition to the specific conditions applicable to each facility as prescribed in the remaining sections of this Chapter: a. Provision of the facility should be structured in a manner to keep it distinct from other facilities and documented separately from any other facility provided by the facility provider. The nature, purpose, extent of the facility and all required standards of performance should be clearly specified in a written agreement to be executed at the time of originating the transaction and disclosed in the offer document. b. The facility is provided on an 'arm's length basis' on market terms and conditions, and subjected to the facility provider’s normal credit approval and review process. c. Payment of any fee or other income for the facility is not subordinated or subject to deferral or waiver. d. The facility is limited to a specified amount and duration. e. The duration of the facility is limited to the earlier of the dates on which:

f. There should not be any recourse to the facility provider beyond the fixed contractual obligations. In particular, the facility provider should not bear any recurring expenses of the securitisation. g. The facility provider has obtained legal opinion that the terms of agreement protect it from any liability to the investors in the securitisation or to the SPE / trustee, except in relation to its contractual obligations pursuant to the agreement governing provision of the facility. h. The SPE and/or investors in the securitisation notes issued by the SPE have the clear right to select an alternative party to provide the facility subject to compliance of instructions in this direction. B. Credit enhancement facilities 46. Credit enhancement is the process of enhancing credit profile of a structured financial transaction through provision of additional security/financial support, for covering losses on securitised assets in adverse conditions. The enhancements can be broadly divided into two types viz. internal credit enhancement and external credit enhancement. A credit enhancement which, for the investors, creates exposure to entities other than the underlying borrowers is called the external credit enhancement. For instance, cash collaterals and first/second loss guarantees are external forms of credit enhancements. Investment in subordinated tranches, over-collateralisation, excess spreads, credit enhancing interest-only strips are internal forms of credit enhancements. 47. Credit enhancement facilities include all arrangements that could result in a facility provider absorbing losses of the investors in a securitisation transaction. Such facilities may be provided by both originators and third parties. The facility provider providing credit enhancement facilities should ensure that the following conditions are fulfilled failing which credit enhancement provider will be required to hold capital equal to the full value of the securitised assets:

C. Reset of credit enhancements 48. Resets can be applied to external forms of credit enhancements, which is in first or second loss position. The original amount of external credit enhancements provided at the time of initiation of securitisation transaction can be reset by the credit enhancement provider subject to the conditions enumerated below. a. At the time of reset, all the outstanding tranches of securitisation notes should be re-rated (other than equity tranches). The first reset of credit enhancement will not be permitted if the rating of any of the tranches has deteriorated vis-a-vis the original rating of these securitisation positions. Subsequent resets would not be permitted if the rating of any of the tranches has deteriorated vis-à-vis the rating at the time of previous reset. b. If reset is permissible in terms of (a) above, the amount of credit enhancement required for retaining the original or current outstanding rating, whichever is higher should be determined by the concerned rating agency for the first reset. Similarly, for subsequent resets, the amount of credit enhancement required for retaining the higher of the rating at the time of previous reset and current outstanding rating should be determined by the concerned rating agency.

c. The reset of credit enhancement would be subject to the consent of the investors in the securitisation notes. The consent may either be explicitly obtained during every reset or the transactions documents may contain general clauses providing implicit consent of the investors for rest of credit enhancement. d. The reset of credit enhancement should be provided for in the contractual terms of the transaction and the initial rating of the transaction should take into account the likelihood of resets. Such contractual clause should include clearly defined portfolio-level delinquency triggers, which, if met, should result in the credit enhancement resets not available or possible. e. In case such a contractual clause was not available originally, reset of credit enhancement may be carried out subject to the consent of all investors of outstanding securitisation notes. f. In structures where external credit enhancements exist providing first loss credit enhancement (FLCE) and second loss credit enhancement (SLCE), the reset may be carried out simultaneously between FLCE and SLCE in a proportion such that the reset maintains at least the outstanding rating [as envisaged in (b) above] of SLCE. g. Reset of equity tranche is not allowed as it would tantamount to a reset of an internal credit enhancement. 49. For all securitisations other than residential mortgage backed-securitisations, at the time of first reset, at least 50% of the total principal amount assigned at the time of initiation of the securitisation transaction must have been amortised. The subsequent resets may be carried out after the pool principal has amortised in steps of 10%, i.e., up to at least 60%, 70% and 80% of the original level. However, a minimum gap of six months should be maintained between successive resets. 50. For residential mortgage-backed securitisations, at the time of first reset, at least 25% of the total principal amount assigned at the time of initiation of the securitisation transaction must have been amortised. The subsequent resets may be carried out at every 10% (of the original level) further amortisation of the pool principal. A minimum gap of six months should be maintained between successive resets. 51. The excess credit enhancement can be released subject to the following conditions: a. The release of credit enhancement would be subject to a reserve floor as a percentage of the initial credit enhancement provided at the time of transaction, i.e., at any time, the level of credit enhancement available, following any reset shall not drop below the prescribed reserve floor. Thus, even if the required level of credit enhancement to maintain the ratings, as assessed by the credit rating agency during a reset, is lower than the reserve floor, the excess amount available for reset shall be computed as the difference between the available credit enhancement and the reserve floor. b. The stipulation of the floor may be based on the transaction structure, depending on asset class, the track record of the originator and other pool specific factors such as concentration of long term contracts in a pool, and in no case should be less than:

c. A maximum of 60% of the credit enhancement in excess of that required to retain the credit rating of all the tranches as referred to in sub-clause (b) of Clause 48 assigned to them can be considered for release, at any point of time subject to fulfilling the reserve floor indicated at (a) above. d. The reset should not lead to exposures retained by originators along with credit enhancements offered by them falling below the level of MRR prescribed in Section B of Chapter II of these directions. 52. In order to facilitate a common understanding amongst stakeholders and to allow the market to understand the linkage between good pool performance and CE reset, credit rating agencies will disseminate information pertaining to CE reset via press release and would confirm that ratings will not be adversely affected by such reset. D. Liquidity facilities 53. A liquidity facility is provided to help smoothen the timing differences faced by the SPE between the receipt of cash flows from the underlying assets and the payments to be made to investors. A liquidity facility should meet all of the following conditions to guard against the possibility of the facility functioning as a form of credit enhancement and/ or credit support: a. All conditions specified in Clauses 44-45. b. The documentation for the facility must clearly define the circumstances under which the facility may or may not be drawn on. c. The facility should be capable of being drawn only where there is a sufficient level of non-defaulted assets to cover drawings, or the full amount of assets that may turn non-performing are covered by a substantial credit enhancement. d. The facility shall not be drawn for the purpose of:

e. The liquidity facility should not be available for the following purposes:

f. Facility should be provided to SPE and not directly to the investors. g. When the liquidity facility has been drawn the facility provider shall have a priority of claim over the future cash flows from the underlying assets, and thus will be senior to the senior tranche. h. The originator must not be liable to meet any shortfall in liquidity support provided by any independent third party. 54. If any of the conditions are not satisfied, a liquidity facility will be regarded as serving the economic purpose of credit enhancement. In such cases, the liquidity facility provided by a third party shall be treated as a credit enhancement. 55. Since the liquidity facility is meant to smoothen temporary cash flow mismatches, the facility will remain drawn only for short periods, preferably not used for two consecutive repayments to investors. If the drawings under the facility are outstanding for more than 90 days it should be classified as NPA and fully provided for. E. Underwriting facilities 56. An originator or a third-party service provider may act as an underwriter for the issue of securitisation notes by SPE and treat the facility as an underwriting facility for capital adequacy purposes subject to the following conditions:

57. In case any of the above conditions are not satisfied, the facility will be considered as a credit enhancement. 58. An originator may underwrite only investment grade senior notes issued by the SPE. The holdings of securitisation notes devolved to the originator through underwriting would not attract provisions of Clause 25 provided they are sold to unrelated third parties within three-month period following the acquisition. For the period between acquisition and upto three months, the originator will maintain capital equal to as if the exposures were held on the books of the originator. F. Servicing Facilities 59. A servicing facility provider administers or services the securitised assets. Hence, it should not have any obligation to support any losses incurred by the SPE, except to the extent contractually provided in the servicing facility agreement indemnifying the SPE from defaults, breaches, negligence or fraud by the servicing facility provider, and should be able to demonstrate this to the investors in the securitisation exposures. A facility provider performing the role of a service provider for a proprietary or a third-party securitisation transaction should ensure that the following conditions are fulfilled:

60. Where any of the above conditions are not met, the service provider may be deemed as providing liquidity facility to the SPE or investors and treated accordingly for capital adequacy purpose. Chapter V: Requirements to be met by lenders who are investors in securitisation exposures A. Due Diligence Requirements 61. Lenders can invest in securitised notes only if the originator has explicitly disclosed to the purchasing lenders that it has adhered to the MRR and MHP requirements and will adhere to MRR on an ongoing basis, as applicable and advised in this direction. 62. For the overseas branches of Indian lenders, they should not invest or assume exposure to securitisation positions in other jurisdictions which have not laid down any MRR. Regarding MHP, the overseas branches of Indian lenders operating in jurisdictions which do not have regulations related to MHP, may comply with regulations prescribed in those jurisdictions. 63. Further, only if the originator has explicitly disclosed that it has complied with the applicable provisions of the Reserve Bank of India (Know Your Customer (KYC)) Directions, 2016 (as amended from time to time), lenders may invest in such securitised notes. 64. Lenders must have a comprehensive understanding of the risk characteristics of its individual securitisation exposures as well as the risk characteristics of the pools underlying its securitisation exposures, at all times. Lenders also have to demonstrate that for making such an assessment they have implemented formal policies and procedures as appropriate. 65. Lenders should be able to access performance information on the underlying pools on an ongoing basis. Such information may include, as appropriate, but not limited to the following: the average credit quality through average credit scores or similar aggregates of creditworthiness, extent of diversification of the pool of loans, volatility of the market values of the collaterals supporting the loans, cyclicality of the economic activities in which the underlying borrowers are engaged, exposure type, prepayment rates, property types, occupancy, etc. 66. Lenders should have a thorough understanding of all structural features of a securitisation transaction that would materially impact the performance of their exposures to the transaction. Such information may include, as appropriate, but not limited to the following: seniority of the tranche, thickness of the subordinate tranches, its sensitivity to prepayment risk and credit enhancement resets, structure of repayment waterfalls, waterfall related triggers, the position of the tranche in sequential repayment of tranches, liquidity enhancements, availability of credit enhancements in the case of liquidity facilities, deal-specific definition of default, etc. 67. Apart from the above, lenders should take note of, analyse and record the following while taking the decision regarding a securitisation exposure:

B. Stress testing 68. Lenders should regularly perform their own stress tests appropriate to their securitisation positions. For this purpose, various factors which may be considered include, but are not limited to, rise in default rates in the underlying portfolios in a situation of economic downturn, rise in pre-payment rates due to fall in rate of interest or rise in income levels of the borrowers leading to early redemption of exposures, fall in rating of the credit enhancers resulting in fall in market value of securitisation notes and drying of liquidity of the securitisation notes resulting in higher prudent valuation adjustments. Based on the results of stress tests, additional capital shall be held to support any higher risk, if required. C. Credit monitoring and valuation 69. Lenders shall have Board approved policies detailing valuation of the securitisation notes in which they have invested. The policies should inter alia describe the models used for valuation, the assumptions underpinning the models, the policy regarding back-testing and stress testing the valuation model and its parameters etc. The Board approved valuation policies and the use of such policies in assigning valuation to the investment positions in securitisation notes by lenders will be a part of supervisory review. 70. The counterparty for the investor in the securitisation notes would not be the SPE but the underlying assets in respect of which the cash flows are expected from the obligors. The securitisation exposures of lenders will be subject to the requirements of Paragraphs 8.3 to 8.10 of the circular DBR.No.BP.BC.43/21.01.003/2018-19 dated June 3, 2019 on “Large Exposures Framework” (as amended from time to time). 71. Lenders need to monitor on an ongoing basis and in a timely manner, performance information on the exposures underlying their securitisation positions and take appropriate action, if any, required. Action may include modification to exposure ceilings to certain type of asset class underlying securitisation, modification to ceilings applicable to originators etc. 72. For this purpose, lenders should establish formal procedures appropriate to their banking book and trading book and commensurate with the risk profile of their exposures in securitised positions as stipulated in Clauses 65 to 67. Where relevant, this shall include the exposure type, the percentage of loans more than 30, 60 and 90 days past due, default rates, prepayment rates, loans in foreclosure, collateral type and occupancy and frequency distribution of credit scores or other measures of credit worthiness across underlying exposures, industry and geographical diversification, frequency distribution of loan to value ratios with bandwidths that facilitate adequate sensitivity analysis. Lenders may inter alia make use of the disclosures made by the originators in the form given in Annex 2 to monitor the securitisation exposures. Chapter VI: Capital requirements for securitisation exposures A. General Conditions 73. Lenders must maintain capital against all securitisation exposure amounts, including those arising from the provision of credit risk mitigants to a securitisation transaction, investments in asset-backed or mortgage-backed securities, retention of a subordinated tranche, and extension of a liquidity facility or credit enhancement. For the purpose of capital computation, whenever securitisation exposures are a subject of repurchase agreements and repurchased by a lender, the exposure must be treated as retained exposure and not a fresh exposure. Lenders must deduct from Common Equity Tier 1 or net owned funds any increase in equity capital resulting from a securitisation transaction, either realised at the time of sale of underlying assets to the SPE, or unrealised gains on sale of underlying assets such as that associated with expected future margin income, where recognised upfront, till the maturity of such assets. 74. For the purpose of calculating exposure amount, a lender shall measure the exposure amount of its off-balance exposure as follows:

75. For the purposes of calculating capital requirements, a lender’s exposure A overlaps another exposure B if in all circumstances the lender will preclude any loss for the lender on exposure B by fulfilling its obligations with respect to exposure A. For example, if a lender provides full credit support to some securitisation notes and holds a portion of these securitisation notes, its full credit support obligation precludes any loss from its exposure to the securitisation notes. If a lender can verify that fulfilling its obligations with respect to exposure A will preclude a loss from its exposure to B under any circumstance, the lender does not need to calculate risk-weighted assets for its exposure B. 76. To arrive at an overlap, a lender may, for the purposes of calculating capital requirements, split or expand its exposures, i.e., splitting exposures into portions that overlap with another exposure held by the lender and other portions that do not overlap; and expanding exposures by assuming for capital purposes that obligations with respect to one of the overlapping exposures are larger than those established contractually. For example, a liquidity facility may not be contractually required to cover defaulted assets in certain circumstances. For capital purposes, such a situation would not be regarded as an overlap to the securitisation notes issued by that securitisation. However, the lender may calculate risk-weighted assets for the liquidity facility as if it were expanded (either in order to cover defaulted assets or in terms of trigger events) to preclude all losses on the securitisation notes. In such a case, the lender would only need to calculate capital requirements on the liquidity facility. 77. Overlap could also be recognised between relevant capital charges for exposures in the trading book and capital charges for exposures in the banking book, provided that the lender is able to calculate and compare the capital charges for the relevant exposures. 78. Liquidity facilities provided by lenders that satisfy the requirements of Section D of Chapter IV of these directions shall attract risk weights as per the SEC-ERBA approach prescribed in Section H of this Chapter. 79. Liquidity facilities provided by lenders that do not satisfy the requirements of Section D of Chapter IV of these directions shall maintain capital charge equal to the actual exposure, after applying a credit conversion factor of 100% for the undrawn portion. 80. All securitisation exposures, which are not covered by these directions, or which do not satisfy the conditions prescribed in these directions (including the exposures prohibited as per Clause 6), or where originator is not a lender referred to in Clause 3, or for which prudential treatment is not advised explicitly in these directions, lenders shall keep capital charge equal to the actual exposure and will be subjected to supervisory scrutiny and suitable action. B. Derecognition of transferred assets for the purpose of capital adequacy 81. An originator has to maintain capital against the exposures transferred to a SPE, which then forms the underlying for securitisation notes issued by the SPE, i.e., the exposures transferred to a special purpose entity must be included in the calculation of risk-weighted assets of the originator and the consideration received from SPE must be recognised as an advance, unless atleast the following conditions are satisfied: a. The originator does not maintain direct or indirect control over the transferred exposures. For this purpose, the originator is deemed to have maintained effective control over the transferred credit risk exposures if it: (i) is able to repurchase from the SPE the previously transferred exposures in order to realise their benefits; or (ii) is obligated, contractually or otherwise, to retain the risk of the transferred exposures.

b. The originator should not be able to repurchase the transferred exposures unless it is done through invocation of a clean-up call option.

c. The transferred exposures are legally isolated from the originator in such a way that the exposures are put beyond the reach of the originator or its creditors, even in bankruptcy (specially IBC) or administration. d. The securitisation notes issued by the SPE are not obligations of the originator. Thus, the investors who purchase the securitisation notes have a claim only to the underlying exposures. e. The holders of the securitisation notes issued by the SPE against the transferred exposures have the right to pledge or trade them without any restriction, unless the restriction is imposed by a statutory or regulatory risk retention requirement. f. The exercise of the clean-up calls, if any, should not be mandatory on the originator, in form or substance and must be at the discretion of the originator. g. The clean-up call options, if any, should not be structured to avoid allocating losses to credit enhancements or positions held by investors or otherwise structured to provide credit enhancements.

h. The threshold at which clean-up calls become exercisable shall not be more than 10% of the original value of the underlying exposures or securitisation notes. i. The securitisation does not contain clauses that require the originator to replace or replenish the underlying exposures to improve the credit quality of the pool in the event of deterioration in the underlying credit quality, except under conditions specifically permitted in these Directions. j. If the originator provides credit enhancement or first loss facility, the securitisation structure shall not allow for increase in the above positions after inception. k. The securitisation does not contain clauses that increase the yield payable to parties other than the originator such as investors and third-party providers of credit enhancements, in response to a deterioration in the credit quality of the underlying pool.

l. There must be no termination options or triggers to the securitisation exposures except eligible clean-up call options or termination provisions for specific changes in tax and regulation (regulatory or tax call options) or early amortisation provisions.

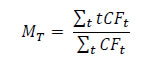

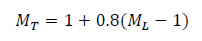

82. The originator should obtain legal opinion that the transfer of exposures to a special purpose entity satisfies the above conditions if the exposures are to be excluded from the calculation of risk weighted assets. C. Approaches for computation of risk weighted assets 83. Lenders shall apply Securitisation External Ratings Based approach (SEC-ERBA) for calculation of risk weighted assets for credit risk of securitisation exposures. For unrated securitisation exposures, lender shall maintain capital charge equal to the actual exposure. 84. The capital charges computed based on the prescribed risk weights are subject to a cap of the actual exposure in respect of which capital adequacy is being computed such that the capital requirement for any securitisation position does not exceed the securitisation exposure amount. 85. However, the originator may apply a maximum capital requirement for the securitisation exposures it holds, upto the permissible aggregate threshold, equal to the capital requirement that would have been assessed against the entire underlying loan exposures had they not been securitised. 86. When a lender provides implicit support to a securitisation, it must, at a minimum, hold capital against all of the underlying exposures associated with the securitisation transaction as if they had not been securitised. Additionally, lenders would not be permitted to recognise in regulatory capital any gain on sale. D. Determination of attachment point (A) and detachment point (D) 87. The attachment point (A) represents the threshold at which losses within the underlying pool would first be allocated to the relevant securitisation exposure. The attachment point (A) shall be expressed as a decimal value between zero and one and shall be equal to the greater of zero and the ratio of the outstanding balance of the pool of underlying exposures in the securitisation minus the outstanding balance of all tranches that rank senior or pari passu to the tranche containing the relevant securitisation position including the exposure itself to the outstanding balance of all the underlying exposures in the securitisation. 88. The detachment point (D) represents the threshold at which losses within the underlying pool result in a total loss of principal for the tranche in which a relevant securitisation exposure resides. The detachment point (D) shall be expressed as a decimal value between zero and one and shall be equal to the greater of zero and the ratio of the outstanding balance of the pool of underlying exposures in the securitisation minus the outstanding balance of all tranches that rank senior to the tranche containing the relevant securitisation position to the outstanding balance of all the underlying exposures in the securitisation. 89. For the calculation of A and D, over-collateralisation and funded reserve accounts must be recognised as tranches; and the assets forming these reserve accounts must be recognised as underlying assets. Only the loss-absorbing part of the funded reserve accounts that provide credit enhancement can be recognised as tranches and underlying assets. 90. Unfunded reserve accounts, such as those to be funded from future receipts from the underlying exposures (eg unrealised excess spread) and assets that do not provide credit enhancement related to these instruments must not be included in the above calculation of A and D. 91. Lenders should take into consideration the economic substance of the transaction rather than the form and apply these definitions conservatively in the light of the structure. E. Determination of tranche maturity 92. For risk based capital purposes, tranche maturity (MT) can be measured at the lender’s discretion in either of the following manners: a. As the rupee weighted-average maturity of the contractual cash flows of the tranche, as expressed below, where CFt denotes the cash flows (principal, interest payments and fees) contractually payable by the borrower in period t. The contractual payments must be unconditional and must not be dependent on the actual performance of the securitised assets. If such unconditional contractual payment dates are not available, the final legal maturity shall be used.  b. On the basis of final legal maturity of the tranche, where ML is the final legal maturity of the tranche. (MT and ML are in years)  93. In all cases, MT will have a floor of one year and a cap of five years. The cap of five years is only for the capital computation purposes and is not applicable for the actual permissible maturity for tranches. 94. When determining the maturity of a securitisation exposure, lenders should take into account the maximum period of time they are exposed to potential losses from the securitised assets. In cases where a lender provides a commitment, the lender should calculate the maturity of the securitisation exposure resulting from this commitment as the sum of the contractual maturity of the commitment and the longest maturity of the asset(s) to which the lender would be exposed after a draw has occurred. 95. For credit protection instruments that are only exposed to losses that occur up to the maturity of that instrument, a lender would be allowed to apply the contractual maturity of the instrument and would not have to look through to the protected position. F. Treatment by banks (including small finance banks) of credit risk mitigation for securitisation exposures 96. Banks may recognise credit protection purchased on a securitisation exposure when calculating capital requirements subject to the following:

97. When a bank provides full (or pro rata) credit protection to a securitisation exposure, it must calculate its capital requirements as if it directly holds the portion of the securitisation exposure on which it has provided credit protection (in accordance with the definition of tranche maturity). 98. Provided that the conditions set out in Clause 96 are met, the bank buying full (or pro rata) credit protection may recognise the credit risk mitigation on the securitisation exposure in accordance with the CRM framework. 99. Under all approaches, a lower-priority sub-tranche must be treated as a non-senior securitisation exposure even if the original securitisation exposure prior to protection qualifies as senior tranche as defined in sub-clause (v) of Clause 5. 100. A maturity mismatch exists when the residual maturity of a hedge is less than that of the underlying exposure. When protection is bought on a securitisation exposure(s), for the purpose of setting regulatory capital against a maturity mismatch, the capital requirement will be determined in accordance with Paragraph 7.6 of the “Master Circular – Basel III Capital Regulations” dated July 1, 2015 (as amended from time to time). When the exposures being hedged have different maturities, the longest maturity must be used. G. Securitisation – External Ratings Based Approach (SEC-ERBA) 101. For securitisation exposures that are externally rated, risk-weighted assets under the securitisation external ratings-based approach (SEC-ERBA) will be determined by multiplying securitisation exposure amounts by the appropriate risk weights as determined by Clauses 102 to 104 provided that the following operational criteria are met:

102. For exposures with short-term ratings, the following risk weights will apply:

103. For exposures with long-term ratings, the risk weights depend on:

104. Specifically, for exposures with long-term ratings, risk weights will be determined according to the following table and will be adjusted for tranche maturity and tranche thickness for non-senior tranches as prescribed in Clause 105 of these directions.

105. The risk weight assigned to a securitisation exposure when applying the SEC-ERBA is calculated as follows5: a. To account for tranche maturity, lenders shall use linear interpolation between the risk weights for one and five years. b. To account for tranche thickness, lenders shall calculate the risk weight for non-senior tranches as follows:  106. In the case of market risk hedges such as currency or interest rate swaps, the risk weight will be inferred from a securitisation exposure that is pari passu to the swaps or, if such an exposure does not exist, from the next subordinated tranche. 107. The resulting risk weight is subject to a floor risk weight of 15%. In addition, the resulting risk weight should never be lower than the risk weight corresponding to a senior tranche of the same securitisation with the same rating and maturity. Alternative capital treatment for term Short, Transparent and Comparable (STC) securitisations 108. For exposures with short-term ratings, the following risk weights will apply:

109. For exposures with long-term ratings, risk weights will be determined according to the following table and will be adjusted for tranche maturity, and tranche thickness for non-senior tranches according to Clause 105.

110. The resulting risk weight is subject to a floor risk weight of 10% for senior tranches, and 15% for non-senior tranches. Chapter VII: Disclosures 111. Wherever a third-party servicing agent service have been availed, the originator shall ensure robust and legally binding information sharing mechanisms are in place to comply with stipulated reporting requirements with requisite frequency and rigor. In such cases of obtaining data from third-party entities, originator must get information duly certified by the respective third-party auditors, preferably at a frequency of no more than a year. A. Disclosures to be made in Servicer/Investor/Trustee Report 112. The originator(s) should disclose to investors the weighted average holding period of the assets securitised and the level of their MRR in the securitisation. 113. The originator(s) should ensure that prospective investors have readily available access to all materially relevant data on the credit quality and performance of the individual underlying exposures, cash flows and collateral supporting a securitisation exposure as well as such information that is necessary to conduct comprehensive and well-informed stress tests on the cash flows and collateral values supporting the underlying exposures. 114. The disclosure by an originator of its fulfilment of the MHP and MRR should be made available publicly and should be appropriately documented; for instance, a reference to the retention commitment in the prospectus for securitisation notes issued under that securitisation programme would be considered appropriate. The disclosure should be made at origination of the transaction, and should be confirmed thereafter at a minimum half yearly (end-September and March), and at any point where the requirement is breached. The above periodical disclosures should be made separately for each securitisation transaction, throughout its life, in the servicer report, investor report, trustee report, or any similar document published. 115. The aforesaid disclosures can be made in the format given in Annex 2. These disclosures should be made separately for each securitisation transaction throughout the life of the transaction. B. Disclosures to be made in Notes to Accounts 116. The Notes to Annual Accounts of the originators should indicate the outstanding amount of securitised assets as per books of the SPEs and total amount of exposures retained by the originator as on the date of balance sheet to comply with the MRR. These figures should be based on the information duly certified by the SPE’s auditors obtained by the originator from the SPE. 117. These disclosures should be made in the format given in Annex 3. C. Reporting of Transactions to the Reserve Bank 118. The originator must also submit the details of the securitisation transactions undertaken, including the details of the securitisation notes issued, to the Reserve Bank on a quarterly basis. The format for the same shall be communicated separately and shall be effective from the date advised therein. Chapter VI: Repeal of circulars 119. The list of circulars / directions / guidelines that stand repealed with immediate effect is given below:

Simple, transparent and comparable securitisation – criteria for regulatory capital purposes All the following criteria must be satisfied in order for a securitisation to receive the alternative regulatory capital treatment as determined by Clauses 108 to 110. Nature of Assets 1. The assets underlying the securitisation should be homogeneous credit claims or receivables eligible under Part A of Chapter II. Credit claims or receivables should have contractually identified periodic payment streams relating to principal, interest, or principal and interest payments. Any referenced interest payments or discount rates should be based on an external benchmark. 2. For this purpose, the “homogeneity” criterion should be assessed taking into account the following principles:

Asset performance history 3. In order to provide investors with sufficient information on an asset class to conduct appropriate due diligence and access to a sufficiently rich data set to enable a more accurate calculation of expected loss in different stress scenarios, verifiable loss performance data, such as delinquency and default data, should be available for credit claims and receivables with substantially similar risk characteristics to those being securitised, for a time period long enough to permit meaningful evaluation by investors. 4. Sources of and access to data and the basis for claiming similarity to credit claims or receivables being securitised should be clearly disclosed to all market participants. 5. The originator of the securitisation or the original lender of the exposures that are securitised, as the case may be, must have sufficient experience in originating exposures similar to those securitised. For capital purposes, investors must determine whether the performance history of the originator for substantially similar claims or receivables to those being securitised has been established for an "appropriately long period of time”. This performance history must be no shorter than a period of seven years for non-retail exposures. For retail exposures, the minimum performance history is five years. Payment status 6. Credit claims or receivables being transferred to the SPE may not, at the time of inclusion in the pool, include obligations that are in default or delinquent or obligations for which the originator, servicer and other parties with a fiduciary responsibility to the securitisation note holders are aware of evidence indicating a material increase in expected losses or of enforcement actions. 7. To ensure that the quality of the securitised credit claims and receivables is not affected by changes in underwriting standards, the originator should demonstrate to investors that any credit claims or receivables being transferred to the SPE have been originated in the ordinary course of the originator’s business to materially non-deteriorating underwriting standards. 8. The originator should verify that the underlying credit claims or receivables meet the following conditions:

9. The assessment of these conditions should be carried out by the originator no earlier than 45 days prior to the date on which the securitisation comes into effect. Additionally, at the time of this assessment, there should, to the best knowledge of the originator, be no evidence indicating likely deterioration in the performance status of the credit claim or receivable. Consistency of underwriting 10. Underwriting standards should not be less stringent than those applied to credit claims and receivables retained on the balance sheet. In all circumstances, all credit claims or receivables must be originated in accordance with sound and prudent underwriting criteria based on an assessment that the obligor has the “ability and volition to make timely payments” on its obligations. 11. The originator of the securitisation is expected, where underlying credit claims or receivables have been acquired from third parties, to review the underwriting standards (ie to check their existence and assess their quality) of these third parties and to ascertain that they have assessed the obligors’ “ability and volition to make timely payments on obligations”. Asset selection and transfer 12. While assets transferred to a securitisation will be subject to defined criteria as approved by the Board of the originator, the performance of the securitisation should not rely upon the ongoing selection of assets through active management on a discretionary basis of the securitisation’s underlying portfolio.

13. Credit claims or receivables transferred to a securitisation should satisfy clearly defined eligibility criteria. Credit claims or receivables transferred to a securitisation after the date on which securitisation becomes effective may not be actively selected, actively managed or otherwise cherrypicked on a discretionary basis. 14. The securitisation should be such that the underlying credit claims or receivables:

15. The originator should provide representations and warranties that the credit claims or receivables being transferred to the SPE are not subject to any condition or encumbrance that can be foreseen to adversely affect enforceability in respect of collections due. 16. To assist investors in conducting appropriate due diligence prior to investing in a new offering, sufficient loan-level data in accordance with applicable laws or, in the case of granular pools, summary stratification data on the relevant risk characteristics of the underlying pool should be available to potential investors before pricing of a securitisation. Initial and ongoing data 17. To assist investors in conducting appropriate and ongoing monitoring of their investments’ performance and so that investors that wish to purchase a securitisation in the secondary market have sufficient information to conduct appropriate due diligence, timely loan-level data in accordance with applicable laws or granular pool stratification data on the risk characteristics of the underlying pool and standardised investor reports should be readily available to current and potential investors at least quarterly throughout the life of the securitisation. Cut-off dates of the loan-level or granular pool stratification data should be aligned with those used for investor reporting. 18. To provide a level of assurance that the reporting of the underlying credit claims or receivables is accurate and that the underlying credit claims or receivables meet the eligibility requirements, the initial portfolio should be reviewed for conformity with the eligibility requirements by an appropriate legally accountable and independent third party.

Redemption cash flows 19. To help ensure that the underlying credit claims or receivables do not need to be refinanced over a short period of time, there should not be a reliance on the sale or refinancing of the underlying credit claims or receivables in order to repay the liabilities of the SPE, unless the underlying pool of credit claims or receivables is sufficiently granular and has sufficiently distributed repayment profiles. Rights to receive income from the assets specified to support redemption payments should be considered as eligible credit claims or receivables in this regard Currency and interest rate asset and liability mismatches 20. To reduce the payment risk arising from the different interest rate and currency profiles of assets and liabilities and to improve investors’ ability to model cash flows, interest rate and foreign currency risks should be appropriately mitigated at all times, and if any hedging transaction is executed the transaction should be documented according to industry-standard master agreements. Only derivatives used for genuine hedging of asset and liability mismatches of interest rate and / or currency should be allowed.

Payment priorities and observability 21. Investor reports should contain information that allows investors to monitor the evolution over time of the indicators that are subject to triggers. Any triggers breached between payment dates should be disclosed to investors on a timely basis in accordance with the terms and conditions of all underlying transaction documents. 22. Following the occurrence of a performance-related trigger, an event of default or an acceleration event, the securitisation positions should be repaid in accordance with a sequential amortisation priority of payments, in order of tranche seniority, and there should not be provisions requiring immediate liquidation of the underlying assets at market value. 23. To assist investors in their ability to appropriately model the cash flow waterfall of the securitisation, the originator should make available to investors, both before pricing of the securitisation and on an ongoing basis, a liability cash flow model or information on the cash flow provisions allowing appropriate modelling of the securitisation cash flow waterfall. 24. To ensure that debt forgiveness, loan moratoriums, payment holidays, restructurings and other asset performance remedies can be clearly identified, policies and procedures, definitions, remedies and actions relating to delinquency, default or restructuring of underlying debtors should be provided in clear and consistent terms, such that investors can clearly identify debt forgiveness, loan moratoriums, payment holidays, restructuring and other asset performance remedies on an ongoing basis. Voting and enforcement rights 25. To help ensure clarity for note holders of their rights and ability to control and enforce on the underlying credit claims or receivables, upon insolvency of the originator, all voting and enforcement rights related to the credit claims or receivables should be transferred to the SPE. Investors’ rights in the securitisation should be clearly defined in all circumstances, including the rights of senior versus junior note holders. Documentation disclosure and legal review 26. To help investors to fully understand the terms, conditions, legal and commercial information prior to investing in a new offering and to ensure that this information is set out in a clear and effective manner for all programmes and offerings, sufficient initial offering and draft underlying documentation should be made available to investors (and readily available to potential investors on a continuous basis) within a reasonably sufficient period of time prior to pricing, or when legally permissible, such that the investor is provided with full disclosure of the legal and commercial information and comprehensive risk factors needed to make informed investment decisions.

27. Final offering documents should be available from the closing date and all final underlying transaction documents shortly thereafter. These should be composed such that readers can readily find, understand and use relevant information. Fiduciary and contractual responsibilities 28. To ensure that all the documentation of securitisation transactions has been subject to appropriate review prior to publication, the terms and documentation of the securitisation should be reviewed by an appropriately experienced third party legal practice, such as a legal counsel already instructed by one of the transaction parties. Investors should be notified in a timely fashion of any changes in such documents that have an impact on the structural risks in the securitisation. 29. To help ensure servicers have extensive workout expertise, thorough legal and collateral knowledge and a proven track record in loss mitigation, such parties should be able to demonstrate expertise in the servicing of the underlying credit claims or receivables, supported by a management team with extensive industry experience. The servicer should at all times act in accordance with reasonable and prudent standards. 30. Policies, procedures and risk management controls should be well documented and adhere to good market practices and relevant regulatory regimes. There should be strong systems and reporting capabilities in place. In assessing whether “strong systems and reporting capabilities are in place” for capital purposes, well documented policies, procedures and risk management controls, as well as strong systems and reporting capabilities, may be substantiated by a third-party review. 31. The party or parties with fiduciary responsibility should act on a timely basis in the best interests of the securitisation note holders, and both the initial offering and all underlying documentation should contain provisions facilitating the timely resolution of conflicts between different classes of note holders by the trustees, to the extent permitted by applicable law. 32. The party or parties with fiduciary responsibility to the securitisation and to investors should be able to demonstrate sufficient skills and resources to comply with their duties of care in the administration of the SPE. 33. To increase the likelihood that those identified as having a fiduciary responsibility towards investors as well as the servicer execute their duties in full on a timely basis, remuneration should be such that these parties are incentivised and able to meet their responsibilities in full and on a timely basis. Transparency to investors 34. To help provide full transparency to investors, assist investors in the conduct of their due diligence and to prevent investors being subject to unexpected disruptions in cash flow collections and servicing, the contractual obligations, duties and responsibilities of all key parties to the securitisation, both those with a fiduciary responsibility and of the ancillary service providers, should be defined clearly both in the initial offering and all underlying documentation.

35. Provisions should be documented for the replacement of servicers, bank account providers, derivatives counterparties and liquidity providers in the event of failure or non-performance or insolvency or other deterioration of creditworthiness of any such counterparty to the securitisation. 36. To enhance transparency and visibility over all receipts, payments and ledger entries at all times, the performance reports to investors should distinguish and report the securitisation’s income and disbursements, such as scheduled principal, redemption principal, scheduled interest, prepaid principal, past due interest and fees and charges, delinquent, defaulted and restructured amounts under debt forgiveness and payment holidays, including accurate accounting for amounts attributable to principal and interest deficiency ledgers. Credit risk of underlying exposures 37. At the portfolio cut-off date6 the underlying exposures have to meet the conditions under the Standardised Approach for credit risk, and after taking into account any eligible credit risk mitigation, for being assigned a risk weight equal to or smaller than:

Granularity of the pool 38. At the portfolio cut-off date, the aggregated value of all exposures to a single obligor shall not exceed 1% of the aggregated outstanding exposure value of all exposures in the portfolio.

1 Amended vide amendment dated December 05, 2022 2 The transferor can transfer loans only after a minimum holding period (MHP), as prescribed below, which is counted from the date of registration of the underlying security interest: