IST,

IST,

Strategy adopted for Financial Inclusion

Dr. (Smt.) Deepali Pant Joshi, Executive Director, Reserve Bank of India

delivered-on જાન્યુ 29, 2014

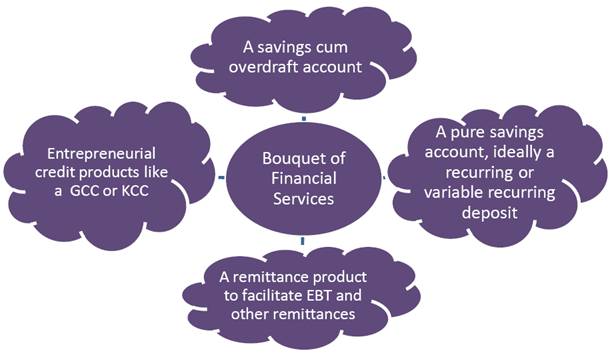

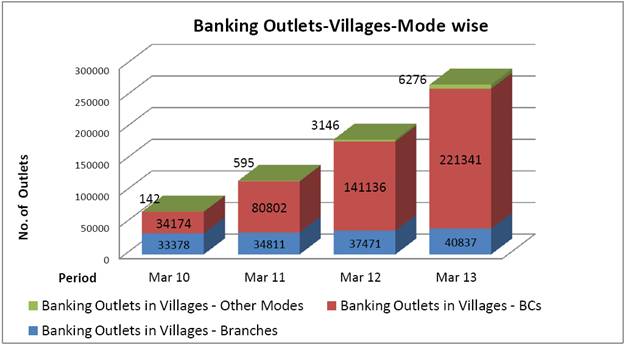

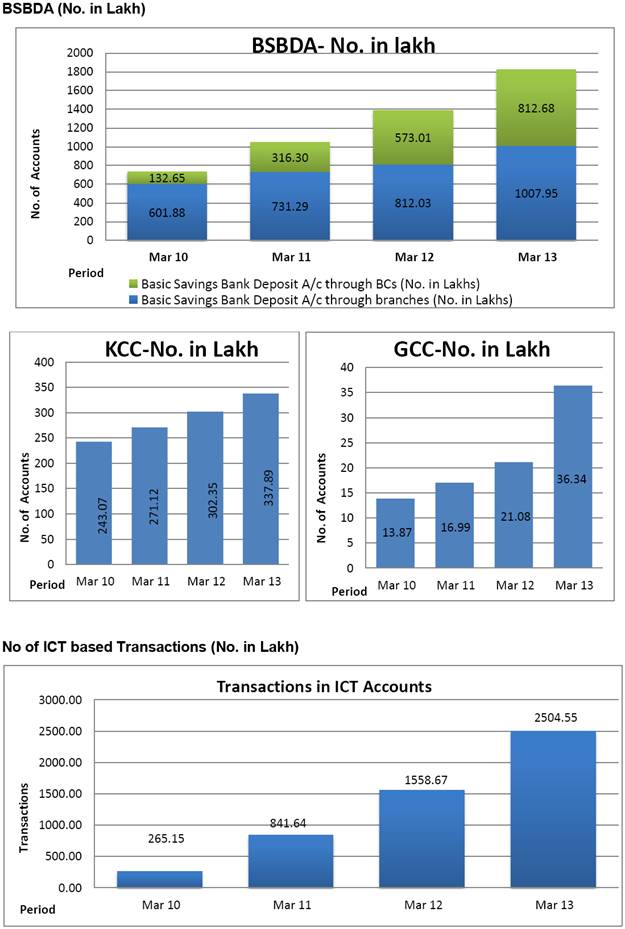

One of the major challenges for next decade or more to banks in the country is to capture the banking business of over 50% population of this country of over 1.2 billion people. Poor people need to be provided with access to financial products at low transaction cost. They need to be provided assistance on the demand side (in terms of financial awareness and literacy) as well as on the supply side (in the form of availability of customized financial products). Taking into account their seasonal inflow of income from agricultural operations, migration from one place to another seasonal and irregular work availability and income, the existing financial system needs to be designed to suit their requirements and to be more responsive to their needs. No doubt banks and regulators play a major role in this, but we also need to think beyond traditional ways and delivery channels to speed up the efforts. Dr. Raghuram Rajan, Hon'ble Governor, RBI has powerfully enunciated the need for broad based diversified growth leading to rapid reduction in poverty. Governor has also laid down RBI's developmental measures for the near future on five pillars and one of the most important pillar amongst them is Financial Inclusion where the objective is to expand access of finance to small and medium enterprises, the unorganized sector, the poor, and remote and underserved areas of the country. The approach adopted for achieving the objectives under Financial Inclusion RBI’s perspective on Financial Inclusion aims at giving a specific direction to the collaborated efforts to gain synergic benefits. Therefore, we have defined Financial Inclusion as “the process of ensuring access to appropriate financial products and services needed by all sections of the society in general and vulnerable groups such as weaker sections and low income groups in particular at an affordable cost in a fair and transparent manner by mainstream institutional players.” Reserve Bank of India has made sustained efforts to increase the penetration of formal financial services in unbanked areas, while continuing with its policy of ensuring adequate but viable flow of credit to priority sectors of the economy. We have adopted a structured, planned and integrated approach towards FI which is focusing on improving access to financial services and also encouraging demand for financial services through financial literacy initiatives. Some of the defining features of our approach to FI are: Institutional Mechanism Under the institutional mechanism put in place for financial inclusion, we have the Financial Stability and Development Council (FSDC), which has an exclusive mandate for financial inclusion and financial literacy. A separate Technical Group on financial inclusion and financial literacy, under the Chairmanship of a Deputy Governor, has been set up under the aegis of FSDC. The Group has representations from all the financial sector regulators. In order to spearhead efforts towards greater financial inclusion, RBI has constituted a Financial Inclusion Advisory Committee (FIAC) under the Chairmanship of Deputy Governor. The FIAC has few Directors from the Central Board of RBI and experts drawn from NGO sector/other civil society representatives, etc. as members. At the State level, there are State Level Bankers Committee (SLBC) further supported by Lead District Managers (671 Districts) at the district level. Bank led Model In India, we have adopted a bank- led model for financial inclusion, which seeks to leverage on technology. The FI initiatives would have to be ICT based and would ride on new delivery models that would need to be developed by the market participants to best suit their requirements. Our experience has shown that the goal of financial inclusion is better served through mainstream banking institutions as only they have the ability to offer the suite of products required to bring in effective/meaningful financial inclusion. Other players such as mobile companies have been allowed to partner with banks in offering services collaboratively. Integrated approach – Financial Inclusion & Financial Literacy Considering that financial Literacy is an important adjunct for promoting financial inclusion, consumer protection and ultimately financial stability, RBI has adopted an integrated approach wherein efforts towards Financial Inclusion and Financial Literacy would go hand in hand. Bouquet of Financial products In the absence of banks a large number of informal intermediaries had mushroomed, mostly in the rural areas, which were acting as proxy to the banks. Such unregulated entities were in the business of extending only credit products that too at exorbitant rates of interest mostly to the illiterate section of the population. This had resulted in huge indebtedness amongst the poor people. With our renewed efforts under financial inclusion we have now advised banks to ensure that all the financial needs of the customers are met by offering, at the minimum, four basic products to customers, viz.  The idea is to ensure that customers who are linked to the banking system is provided with all the basic financial products that are required to enhance their income generation capacity thus helping them to come out of poverty. Such an initiative is expected to be a win-win situation for both banks as also the large section of poor people residing in the rural areas. Combination of Branch and BC Structure We are advocating a combination of Brick and Mortar structure with Click and Mouse technology for extending financial inclusion, especially in geographically dispersed areas. Banks have to make effective use of technology to provide banking services in remote areas. In addition to creating a large network of small branches in rural areas, the Reserve Bank has permitted banks to utilise the services of intermediaries in providing banking services through the use of business correspondents. The BC model allows banks to do ‘cash in - cash out’ transactions at a location much closer to the rural population, thus addressing the last mile problem. Leveraging on Technology Penetrating banking services through the traditional brick and mortar model was expensive for banks. We realized that the task of Financial Inclusion was gigantic and would not be possible without actively leveraging on technology. We have therefore encouraged banks to leverage on technology to attain greater reach and penetration for minimizing the cost of providing financial services in far flung areas of the country. With adoption of technology it has been possible for banks to deliver banking products and services to the doorsteps of villages. Engaging Business Correspondents: The Reserve Bank has permitted banks to engage Business Facilitators (BFs) and Business Correspondents (BCs) as intermediaries for providing financial and banking services. The BC Model allows banks to provide door step delivery of services especially to do ‘cash in - cash out’ transactions, thus addressing the ‘last mile’ problem. The list of eligible individuals/entities who can be engaged as BCs are being widened from time to time and we have adopted a test and learn approach to this process. Now, even for profit organisations excluding NBFCs and Telcos have been permitted to operate as BCs of banks. Relaxation of KYC norms: The strict KYC norms inhibited linkage of common people with the Banking System. Know Your Customer (KYC) requirements for opening bank accounts have been relaxed for small accounts. Further, in order to leverage on the initiative of UIDAI, we have allowed ‘Aadhaar’ as one of the eligible document for meeting KYC requirements and very recently have also allowed banks to provide e-KYC services provided through the Aadhaar platform. Simplified branch authorisation: To address the issue of uneven spread of bank branches, branch licensing norms have been relaxed considerably and banks are now free to open branches in centres with population less than 1 lakh under general permission, subject to reporting. Opening of branches in unbanked rural centres: To further step up the opening of branches in rural areas, banks have been mandated to open at least 25 per cent of the branches in unbanked rural centres. To help facilitate achieving this mandate, banks have been advised to open to open small intermediary brick and mortar structures between the base branch and the unbanked villages. The idea is to create an eco-system for ensuring efficient delivery of services, efficiency in cash management, redressal of customer grievances and closer supervision of BC operations. This is expected to facilitate quicker branch expansion in unbanked rural centres. Financial Inclusion Plan of banks We have encouraged banks to adopt a structured and planned approach to financial inclusion with commitment at the highest levels, through preparation of Board approved Financial Inclusion Plans (FIPs). The first phase of FIPs was implemented over the period 2010-2013. The Reserve Bank has used the FIPs to gauge the performance of banks under their FI initiatives. In this direction we have put in place a structured and comprehensive monitoring mechanism for evaluating banks’ performance vis-à-vis their targets. To ensure support of the Top Management of the Bank to the Financial Inclusion process and to ensure accountability of the senior functionaries of the bank, one on one annual review meetings are held with CMDs/CEOs of banks.

Banking outlets   We have now created a large banking network and have also managed to open a large number of small accounts. The focus under the FI plan has now shifted towards leveraging the banking network created for extending other products viz. credit, etc. which will help make the business more viable for banks. This would also ensure that the large number of accounts opened see large volume of transactions taking place and people reap the benefits of getting linked to the formal financial institutions. Roadmap for providing Banking Services in unbanked villages: With financial inclusion gaining increasing recognition as a business opportunity and with all banks geared to increase presence, we adopted a phase-wise approach to provide banking services in all unbanked villages in the country. On completion of the first phase where nearly 74000 villages with population more than 2000 were provided with a banking outlet, we are now in the second phase where the remaining unbanked villages, numbering close to 4,90,000, have been identified in villages less than 2000 population and allocated to banks, for opening of banking outlets by Match 2016. Under the roadmap for provision of banking facilities in villages with less than 2000 population, SLBC, Madhya Pradesh has identified and allotted 47660 unbanked villages among various, out of which 18986 unbanked villages are required to be covered by March 2014. Direct Benefit Transfer – The GoI has plans to route the social security payments through the banking network by leveraging on the Aadhaar Enabled Payment System based platform. In order to ensure smooth roll out of the Government’s Direct Benefit Transfer (DBT) initiative, banks have been advised to open accounts of all eligible individuals and to seed the existing and new accounts with Aadhaar numbers. Financial Literacy – We have realized that Financial Literacy is an important adjunct for promoting financial inclusion. We have adopted an integrated approach, wherein our efforts towards Financial Inclusion and Financial Literacy go hand in hand. Through Financial literacy and education, we disseminate information on the general banking concepts to diverse target groups, including school and college students, women, rural and urban poor, pensioners and senior citizens to enable them to make informed financial decisions. To support this we have nearly 800 financial literacy centres set up by banks. We have designed a mass scale Financial Literacy Program with an objective to integrate the financially excluded population with low level of income and low literacy level with the formal financial system. Financial Literacy Centres organize Outdoor Literacy camps which are spread over a period of three months and delivered in three phases wherein along with creating awareness, accounts are also opened in the Literacy camps. Way forward - Issues and Challenges Structure With adoption of new branchless delivery channels by banks, there is a need for banks to revamp the structure for carrying out banking operations. There cannot be a fixed structured defined which can be adopted by all the banks. Each bank has to based on its current architecture develop a structure that can enhance its financial inclusion efforts. This would entail the following:-

BC Model There are many challenges being faced while implementing BC model. Sustainability and scalability of the BC model is essential. More and more innovative products will have to be introduced which would benefit both banks as well as the rural people and at the same time make the BC model more viable. Review of the cash management practices for delivery of banking services through the branchless modes need to be done for ensuring scaling up of the various models. Transactions During the first phase of our FI initiative, we have had success as regards opening of banking outlets by banks and also in opening bank accounts for large number of individuals. Going forward our idea is to enable more transactions in these accounts by providing more credit products, which will not only help rural people to avail of credit at comparatively lower rates of interest but at the same time also make the BC model viable for banks. Banks have been advised to leverage upon the Direct Benefit Transfer initiative of the Government of India for linking all the individuals to the banking system and for utilizing the large amounts likely to be credited in these accounts for encouraging issue of deposit and credit products. Collaboration Finally, financial inclusion cannot be achieved without the active involvement of all stakeholders like RBI, other financial regulators, banks, governments, NGOs, civil societies, etc. The current policy objective of inclusive growth with financial stability cannot be achieved without ensuring universal financial inclusion. Banks alone will not be able to achieve this unless an entire support system would be partnering with them in this mission. All the stakeholders need to join hands and make it possible. Thank you. |

આ પેજ શેર કરો:

રિઝર્વ બેંક ઑફ ઇન્ડિયા મોબાઇલ એપ્લિકેશન ઇન્સ્ટૉલ કરો અને લેટેસ્ટ ન્યૂઝનો ઝડપી ઍક્સેસ મેળવો!

અમારી એપ ઇન્સ્ટોલ કરવા માટે QR કોડ સ્કેન કરો

પેજની છેલ્લી અપડેટની તારીખ: