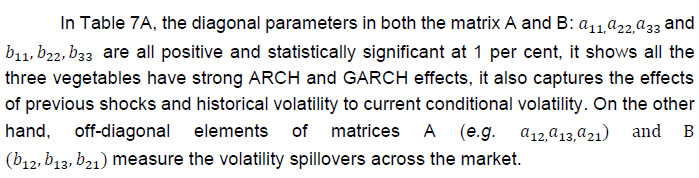

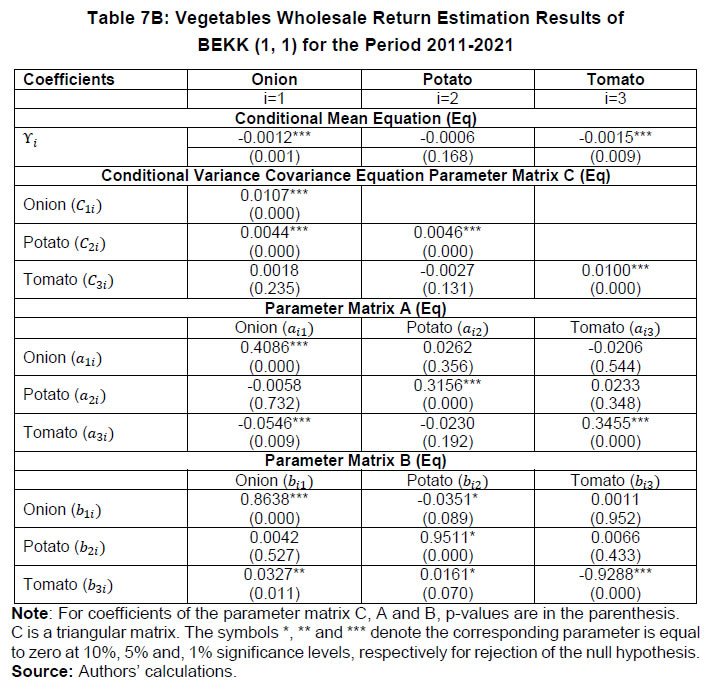

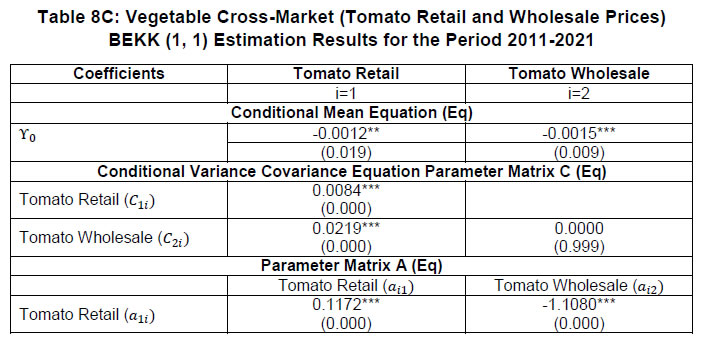

IST,

IST,

DRG Study No. 49: Anatomy of Price Volatility Transmission in Indian Vegetables Market