IST,

IST,

Monetary Policy Statement, 2021-22 Resolution of the Monetary Policy Committee (MPC) February 8-10, 2022

On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (February 10, 2022) decided to:

The reverse repo rate under the LAF remains unchanged at 3.35 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 4.25 per cent.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. The main considerations underlying the decision are set out in the statement below. Assessment Global Economy 2. Since the MPC’s meeting in December 2021, the rapid spread of the highly transmissible Omicron variant and the associated restrictions have dampened global economic activity. The global composite purchasing managers’ index (PMI) slipped to an 18 month low of 51.4 in January 2022, with weakness in both services and manufacturing. World merchandise trade continues to grow. There are, however, headwinds emanating from persistent container and labour shortages, and elevated freight rates. In its January 2022 update of the World Economic Outlook, the International Monetary Fund (IMF) revised global output and trade growth projections for 2022 downward to 4.4 per cent and 6.0 per cent from its earlier forecasts of 4.9 per cent and 6.7 per cent, respectively. 3. After reversing the transient correction that had occurred towards end-November, commodity prices resumed hardening and accentuated inflationary pressures. With several central banks focused on policy normalisation, including ending asset purchases and earlier than expected hikes in policy rates, financial markets have turned volatile. Sovereign bond yields firmed up across maturities and equity markets entered correction territory. Currency markets in emerging market economies (EMEs) have exhibited two-way movements in recent weeks, driven by strong capital outflows from equities with elevated uncertainty on the pace and quantum of US rate hikes. The latter also led to an increasing and volatile movement in US bond yields. Domestic Economy 4. The first advance estimates (FAE) of national income released by the National Statistical Office (NSO) on January 7, 2022 placed India’s real gross domestic product (GDP) growth at 9.2 per cent for 2021-22, surpassing its pre-pandemic (2019-20) level. All major components of GDP exceeded their 2019-20 levels, barring private consumption. In its January 31 release, the NSO revised real GDP growth for 2020-21 to (-) 6.6 per cent from the provisional estimates of (-) 7.3 per cent. 5. Available high frequency indicators suggest some weakening of demand in January 2022 reflecting the drag on contact-intensive services from the fast spread of the Omicron variant in the country. Rural demand indicators – two-wheeler and tractor sales – contracted in December-January. Area sown under Rabi up to February 4, 2022 was higher by 1.5 per cent over the previous year. Amongst the urban demand indicators, consumer durables and passenger vehicle sales contracted in November-December on account of supply constraints while domestic air traffic weakened in January under the impact of Omicron. Investment activity displayed a mixed picture – while import of capital goods increased in December, production of capital goods declined on a year-on-year (y-o-y) basis in November. Merchandise exports remained buoyant for the eleventh successive month in January 2022; non-oil non-gold imports also continued to expand on the back of domestic demand. 6. The manufacturing PMI stayed in expansion zone in January at 54.0, though it moderated from 55.5 in the preceding month. Among services sector indicators, railway freight traffic, e-way bills, and toll collections posted y-o-y growth in December-January; petroleum consumption registered muted growth and port traffic declined. While finished steel consumption contracted y-o-y in January, cement production grew in double digits in December. PMI services continued to exhibit expansion at 51.5 in January 2022, though the pace weakened from 55.5 in December. 7. Headline CPI inflation edged up to 5.6 per cent y-o-y in December from 4.9 per cent in November due to large adverse base effects. The food group registered a significant decline in prices in December, primarily on account of vegetables, meat and fish, edible oils and fruits, but sharp adverse base effects from vegetables prices resulted in a rise in y-o-y inflation. Fuel inflation eased in December but remained in double digits. Core inflation or CPI inflation excluding food and fuel stayed elevated, though there was some moderation from 6.2 per cent in November to 6.0 per cent in December, driven by transportation and communication, health, housing and recreation and amusement. 8. Overall system liquidity continued to be in large surplus, although average absorption (through both the fixed and variable rate reverse repos) under the LAF declined from ₹8.6 lakh crore during October-November 2021 to ₹7.6 lakh crore in January 2022. Reserve money (adjusted for the first-round impact of the change in the cash reserve ratio) expanded by 8.4 per cent (y-o-y) on February 4, 2022. Money supply (M3) and bank credit by commercial banks rose (y-o-y) by 8.4 per cent and 8.2 per cent, respectively, as on January 28, 2022. India’s foreign exchange reserves increased by US$ 55 billion in 2021-22 (up to February 4, 2022) to US$ 632 billion. Outlook 9. Since the December 2021 MPC meeting, CPI inflation has moved along the expected trajectory. Going forward, vegetables prices are expected to ease further on fresh winter crop arrivals. The softening in pulses and edible oil prices is likely to continue in response to strong supply-side interventions by the Government and increase in domestic production. Prospects of a good Rabi harvest add to the optimism on the food price front. Adverse base effect, however, is likely to prevent a substantial easing of food inflation in January. The outlook for crude oil prices is rendered uncertain by geopolitical developments even as supply conditions are expected to turn more favourable during 2022. While cost-push pressures on core inflation may continue in the near term, the Reserve Bank surveys point to some softening in the pace of increase in selling prices by the manufacturing and services firms going forward, reflecting subdued pass-through. On balance, the inflation projection for 2021-22 is retained at 5.3 per cent, with Q4 at 5.7 per cent. On the assumption of a normal monsoon in 2022, CPI inflation for 2022-23 is projected at 4.5 per cent with Q1:2022-23 at 4.9 per cent; Q2 at 5.0 per cent; Q3 at 4.0 per cent; and Q4:2022-23 at 4.2 per cent, with risks broadly balanced (Chart 1). 10. Recovery in domestic economic activity is yet to be broad-based, as private consumption and contact-intensive services remain below pre-pandemic levels. Going forward, the outlook for the Rabi crop bodes well for agriculture and rural demand. The impact of the ongoing third wave of the pandemic on the recovery is likely to be limited relative to the earlier waves, improving the outlook for contact-intensive services and urban demand. The announcements in the Union Budget 2022-23 on boosting public infrastructure through enhanced capital expenditure are expected to augment growth and crowd in private investment through large multiplier effects. The pick-up in non-food bank credit, supportive monetary and liquidity conditions, sustained buoyancy in merchandise exports, improving capacity utilisation and stable business outlook augur well for aggregate demand. Global financial market volatility, elevated international commodity prices, especially crude oil, and continuing global supply-side disruptions pose downside risks to the outlook. Taking all these factors into consideration, the real GDP growth for 2022-23 is projected at 7.8 per cent with Q1:2022-23 at 17.2 per cent; Q2 at 7.0 per cent; Q3 at 4.3 per cent; and Q4:2022-23 at 4.5 per cent (Chart 2).  11. The MPC notes that inflation is likely to moderate in H1:2022-23 and move closer to the target rate thereafter, providing room to remain accommodative. Timely and apposite supply side measures from the Government have substantially helped contain inflationary pressures. The potential pick up of input costs is a contingent risk, especially if international crude oil prices remain elevated. The pace of the domestic recovery is catching up with pre-pandemic trends, but private consumption is still lagging. COVID-19 continues to impart some uncertainty to the future outlook. Measures announced in the Union Budget 2022-23 should boost aggregate demand. The global macroeconomic environment is, however, characterised by deceleration in global demand in 2022, with increasing headwinds from financial market volatility induced by monetary policy normalisation in the systemic advanced economies (AEs) and inflationary pressures from persisting supply chain disruptions. Accordingly, the MPC judges that the ongoing domestic recovery is still incomplete and needs continued policy support. It is in this context that the MPC has decided to keep the policy repo rate unchanged at 4 per cent and to continue with an accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward. 12. All members of the MPC – Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das – unanimously voted to keep the policy repo rate unchanged at 4.0 per cent. 13. All members, namely, Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das, except Prof. Jayanth R. Varma, voted to continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward. Prof. Jayanth R. Varma expressed reservations on this part of the resolution. 14. The minutes of the MPC’s meeting will be published on February 24, 2022. 15. The next meeting of the MPC is scheduled during April 6-8, 2022. (Yogesh Dayal) Press Release: 2021-2022/1693 |

ಈ ಪುಟವನ್ನು ಹಂಚಿಕೊಳ್ಳಿ:

ಭಾರತೀಯ ರಿಸರ್ವ್ ಬ್ಯಾಂಕ್ ಮೊಬೈಲ್ ಅಪ್ಲಿಕೇಶನ್ ಅನ್ನು ಇನ್ಸ್ಟಾಲ್ ಮಾಡಿ ಮತ್ತು ಇತ್ತೀಚಿನ ಸುದ್ದಿಗಳಿಗೆ ತ್ವರಿತ ಅಕ್ಸೆಸ್ ಪಡೆಯಿರಿ!

ನಮ್ಮ ಅಪ್ಲಿಕೇಶನ್ ಅನ್ನು ಸ್ಥಾಪಿಸಲು QR ಕೋಡ್ ಅನ್ನು ಸ್ಕ್ಯಾನ್ ಮಾಡಿ

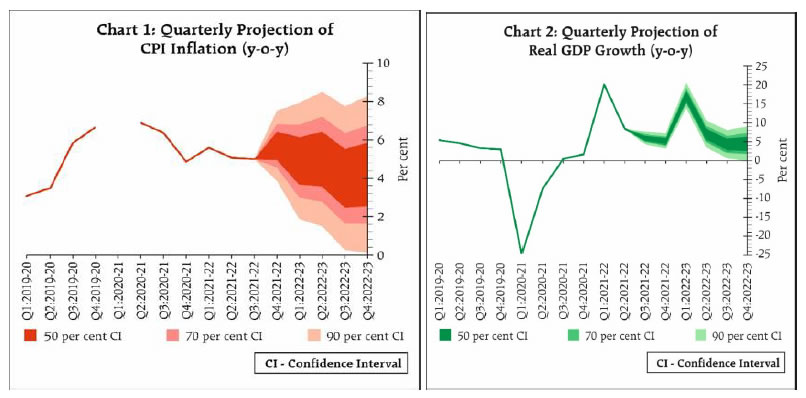

ಪೇಜ್ ಕೊನೆಯದಾಗಿ ಅಪ್ಡೇಟ್ ಆದ ದಿನಾಂಕ: