IST,

IST,

Second Bi-monthly Monetary Policy Statement, 2015-16 Dr. Raghuram G. Rajan, Governor

Monetary and Liquidity Measures On the basis of an assessment of the current and evolving macroeconomic situation, it has been decided to:

Consequently, the reverse repo rate under the LAF stands adjusted to 6.25 per cent, and the marginal standing facility (MSF) rate and the Bank Rate to 8.25 per cent. Assessment 2. Since the first bi-monthly monetary policy statement of 2015-16 issued in April 2015, incoming data suggest that the global recovery is still slow and getting increasingly differentiated across regions. In the United States, the economy shrank in Q1 owing to harsh weather conditions, the strength of the US dollar weighing on exports and a decline in non-residential fixed investment. In the euro area, financial conditions have eased due to the European Central Bank’s (ECB) quantitative easing and a depreciating euro. There has, however, been some moderation in composite purchasing managers’ indices (PMI), economic sentiment and consumer confidence in April. In Japan, growth surprised on the upside in Q1, supported by private demand as business spending boosted inventories and personal consumption. For most emerging market economies (EMEs), macroeconomic conditions remain challenging due to domestic fragilities, exacerbated by bouts of financial market turbulence. China continues to decelerate in spite of monetary easing. The recent firming up of crude prices has reduced headwinds to growth for some energy exporters, while increasing them for importers. Even absent a decisive economic recovery or adverse geopolitical shocks, oil prices appear to be volatile. 3. Global financial markets have also been volatile, with risk-on risk-off shifts induced by changing perceptions of monetary policies in the advanced economies. Global currency markets continue to be dominated by the strength of the US dollar, with the G3 currencies reflecting the asynchronicity of their monetary policy stances. Volatility in global bond markets has increased with a number of factors at play: unwinding of European assets by investors due to the Greek crisis; rapidly changing expectations around the Fed’s forward guidance; sharp movements in crude prices; and market corrections due to changes in risk tolerance. 4. As anticipated, the Central Statistics Office has revised downwards its estimate of India’s gross value added (GVA) at basic prices for 2014-15 by 30 basis points from the advance estimates. Domestic economic activity remains moderate in Q1 of 2015-16. Agricultural activity was adversely affected by unseasonal rains and hailstorms in north India during March 2015, impinging on an estimated 94 lakh hectares of area sown under the rabi crop. Reflecting this, the third advance estimates of the Ministry of Agriculture indicate a contraction in foodgrains production by more than 5 per cent in relation to the preceding year’s level. Successive estimates have been pointing to a worsening of the situation, with the damage to crops like pulses and oilseeds – where buffer foodstocks are not available in the central pool – posing an upside risk to food inflation. For the kharif season, the outlook is clouded by the first estimates of the India Meteorological Department (IMD), predicting that the southwest monsoon will be 7 per cent below the long period average. This has been exacerbated by the confirmation of the onset of El Nino by the Australian Bureau of Meteorology. 5. What is clear is that contingency plans for food management, including storage of adequate quantity of seeds and fertilisers for timely supply, crop insurance schemes, credit facilities, timely release of food stocks and the repair of disruptions in food supply chains, including through imports and de-hoarding, need to be in place to manage the impact of low production on inflation. Inflation control will also be helped by limiting the increase in agricultural support prices. 6. Industrial production has been recovering, albeit unevenly. The sustained weakness of consumption spending, especially in rural areas as indicated in the slowdown in sales of two-wheelers and tractors, continues to operate as a drag. Corporate sales have contracted. The disappointing earnings performance could have been worse if not for the decline in input costs. Capacity utilisation has been falling in several industries, indicative of the slack in the economy. While an upturn in capital goods production seems underway, clear evidence of a revival in investment demand will need to build on the tentative indications of unclogging of stalled investment projects, stabilising of private new investment intentions and improving sales of commercial vehicles. In April, output from core industries constituting 38 per cent of the index of industrial production declined across the board, barring coal production. The sustained revival of coal output augurs well for electricity generation and mining and quarrying, going forward. There is some optimism on gas pricing and availability. The resolution of power purchase processes has to be expedited and power distribution companies’ financial stress has to be addressed on a priority basis. Some public sector banks will need more capital to clean up their balance sheets and support lending as investment revives. 7. Leading indicators of services sector activity are emitting mixed signals. A pick-up in service tax collections, sales of trucks, railway freight, domestic air passenger and air freight traffic could augur well for transport and communication and trade. On the other hand, the slowdown in tourist arrivals, railway traffic and international air passenger and freight traffic could affect hotels, restaurants and some constituents of transportation services adversely. The services PMI declined in April 2015, mainly on account of slowdown in new business orders. Community and personal services are likely to be held back by the ongoing fiscal consolidation. 8. In April, retail inflation measured by the consumer price index (CPI) decelerated for the second month in a row, supported by favourable base effects [of about (-) 0.8 per cent] that moderated the rise in the price index for the fourth successive month. Food inflation softened to a contra-seasonal four-month low, with the impact of unseasonal rains yet to show up. Vegetables inflation continued to ease, along with that of other sub-groups such as cereals, oil, sugar and spices. On the other hand, protein items, especially milk and pulses, continued to impart upward inflationary pressures. 9. Fuel inflation rose for the fourth successive month to a twelve-month high, driven by prices of electricity and firewood. Inflation in these components was accentuated by base effects – the recent price uptick coming on top of muted increases a year ago. Inflation excluding food and fuel rose marginally. House rent, education, medical and transport expenses were among the major drivers of inflation in this category. Rural wage growth, although still moderate, picked up. Inflation expectations remain in high single digits, although they may adapt further to current low inflation. Yet, both input and output price pressures remain muted as reflected in the Reserve Bank’s industrial outlook survey. Purchasing managers’ indices also corroborate these developments. 10. Liquidity conditions eased in April 2015 after the tightness in the second half of March 2015 on account of advance tax outflows and financial year-end behaviour of banks. The Reserve Bank’s liquidity management operations were reversed in view of the improvement in liquidity conditions through April. During May, however, rapid increases in currency in circulation and a build-up of government balances resulted in liquidity conditions tightening again. Accordingly, fine tuning operations of varying tenors were conducted, besides the regular overnight repo at fixed rate and 14-day variable rate repo auctions. These injections helped meet the frictional liquidity requirements. In May, the average daily net liquidity injected through LAF fixed rate repos, besides regular 14-day variable rate repos, additional variable rate repos and MSF, was ₹1031 billion as compared with ₹819 billion in April. As a result, weighted average money market rates shadowed the policy rate. Longer term interest rates, particularly gilts, hardened in early May on international cues but eased in the second half of the month, particularly after the issuance of the new benchmark bond. 11. Merchandise export growth has weakened steadily since July 2014 and entered into contraction from January 2015 through April, with a recent shrinking of even volumes exported. The deterioration in export performance affected economies across Asia as global demand fell and the fall in commodity prices impacted terms of trade for commodity exporters. From December 2014 onwards, merchandise import growth also turned negative, led by a sharp decline in the volume of oil imports as inventory build-up by refineries subsided. Gold imports spiked in the month of March and remained elevated in April owing to festival demand and regulatory relaxations. Notably, the volume of imports has been recording increases, despite the value decline. Given these developments, the reduction in the current account deficit resulting from the sharp decline in oil prices has begun to reverse, though the size of the deficit is expected to be contained to about 1.5 per cent of GDP this year. Net exports are, therefore, unlikely to contribute as much to growth going forward as they did in the past financial year. Consequently growth will depend more on a strengthening of domestic final demand. While portfolio and direct foreign investment flows were buoyant during 2014-15, with net foreign direct investment to India at US$ 36.6 billion and net portfolio inflows at US$ 41 billion, the year 2015-16 has begun with net portfolio outflows in the wake of a reduction in global portfolio allocations to India. Foreign exchange reserves are around US$ 350 billion, providing a strong second line of defence to good macroeconomic policies if external markets turn significantly volatile. Policy Stance and Rationale 12. Banks have started passing through some of the past rate cuts into their lending rates, headline inflation has evolved along the projected path, the impact of unseasonal rains has been moderate so far, administered price increases remain muted, and the timing of normalisation of US monetary policy seems to have been pushed back. With low domestic capacity utilization, still mixed indicators of recovery, and subdued investment and credit growth, there is a case for a cut in the policy rate today. 13. Yet, of the risks to inflation identified in April, three still cloud the picture. First, some forecasters, notably the IMD, predict a below-normal southwest monsoon. Astute food management is needed to mitigate possible inflationary effects. Second, crude prices have been firming amidst considerable volatility, and geo-political risks are ever present. Third, volatility in the external environment could impact inflation. Therefore, a conservative strategy would be to wait, especially for more certainty on both the monsoon outturn as well as the effects of government responses if it turns out to be weak. With still weak investment and the need to reduce supply constraints over the medium term to stay on the proposed disinflationary path (to 4 per cent in early 2018), however, a more appropriate stance is to front-load a rate cut today and then wait for data that clarify uncertainty. Meanwhile banks should pass through the sequence of rate cuts into lending rates. 14. Assuming reasonable food management, inflation is expected to be pulled down by base effects till August but to start rising thereafter to about 6.0 per cent by January 2016 – slightly higher than the projections in April. Putting more weight on the IMD’s monsoon projections than the more optimistic projections of private forecasters as well as accounting for the possible inflationary effects of the increases in the service tax rate to 14 per cent, the risks to the central trajectory are tilted to the upside (Chart 1). 15. Reflecting the balance of risks and the downward revision to GVA estimates for 2014-15, the projection for output growth for 2015-16 has been marked down from 7.8 per cent in April to 7.6 per cent with a downward bias to reflect the uncertainties surrounding these various risks (Chart 2). 16. Strong food policy and management will be important to help keep inflation and inflationary expectations contained over the near term. Furthermore, monetary easing can only create the enabling conditions for a fuller government policy thrust that hinges around a step up in public investment in several areas that can also crowd in private investment. This will be important to relieve supply constraints and aid disinflation over the medium term. A targeted infusion of bank capital into scheduled public sector commercial banks, especially those that implement concerted strategies to clean up stressed assets, is also warranted so that adequate credit flows to the productive sectors as investment picks up. 17. The third bi-monthly monetary policy statement will be announced on August 4, 2015. Alpana Killawala Press Release : 2014-2015/2547 |

ಈ ಪುಟವನ್ನು ಹಂಚಿಕೊಳ್ಳಿ:

ಭಾರತೀಯ ರಿಸರ್ವ್ ಬ್ಯಾಂಕ್ ಮೊಬೈಲ್ ಅಪ್ಲಿಕೇಶನ್ ಅನ್ನು ಇನ್ಸ್ಟಾಲ್ ಮಾಡಿ ಮತ್ತು ಇತ್ತೀಚಿನ ಸುದ್ದಿಗಳಿಗೆ ತ್ವರಿತ ಅಕ್ಸೆಸ್ ಪಡೆಯಿರಿ!

ನಮ್ಮ ಅಪ್ಲಿಕೇಶನ್ ಅನ್ನು ಸ್ಥಾಪಿಸಲು QR ಕೋಡ್ ಅನ್ನು ಸ್ಕ್ಯಾನ್ ಮಾಡಿ

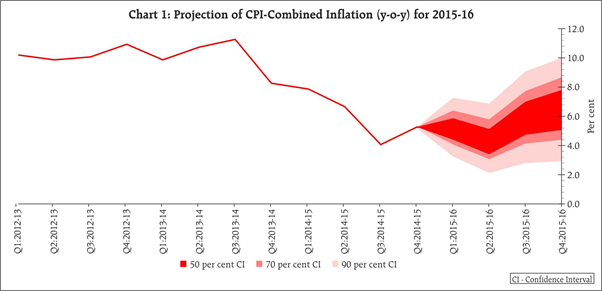

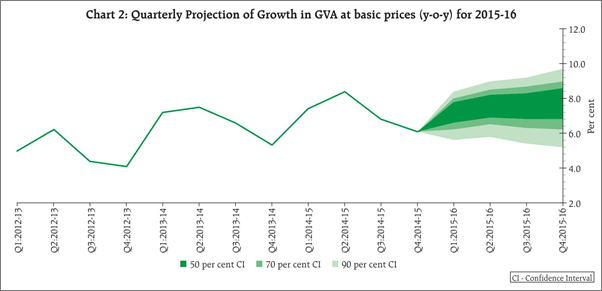

ಪೇಜ್ ಕೊನೆಯದಾಗಿ ಅಪ್ಡೇಟ್ ಆದ ದಿನಾಂಕ: