IST,

IST,

VII. Public Debt Management

In the face of heightened uncertainty, both domestic and global, the market borrowing programme of the centre and the states for 2019-20 was conducted by the Reserve Bank in pursuance of the objectives of cost minimisation, risk mitigation and market development. VII.1 The Internal Debt Management Department (IDMD) of the Reserve Bank is entrusted with managing the domestic debt of the central government vide Sections 20 and 21 of the RBI Act, 1934, and of 28 state governments and two Union Territories (UTs) in accordance with bilateral agreements as provided in Section 21A of the Act. Further, there is a provision for providing short-term credit up to three months to central government, state governments and UTs in the form of Ways and Means Advances (WMA) to bridge temporary mismatches in cash flows, as laid down in Section 17(5) of the RBI Act, 1934. VII.2 The rest of the chapter is arranged in three sections. The immediately following section presents the implementation status in respect of the agenda for 2019-20. Section 3 covers major initiatives to be undertaken in the agenda for 2020-21 on debt management for central and state governments. The chapter has been summarised at the end. 2. Agenda for 2019-20: Implementation Status Goals Set for 2019-20 VII.3 Last year, the Department had set out the following goals:

Implementation Status of Goals VII.4 During 2019-20, the market borrowing programme was conducted following the debt management strategy of minimising cost, risk mitigation and market development. Amidst heightened uncertainty characterising domestic and global economic and financial conditions, the Reserve Bank successfully managed the combined gross market borrowings of the central and the state governments, which increased by 28.1 per cent to ₹13,44,521 crore during the year. VII.5 The Reserve Bank continued its policy of passive consolidation by way of reissuances and active consolidation through buyback/switches. During 2019-20, 185 out of 194 issuances of G-sec were re-issuances as compared with 206 re-issuances out of 212 issuances in the previous year. VII.6 Switch auction for conversion of G-sec is generally conducted on every third Monday of the month, for which a specific press release, indicating the securities to be switched, is announced before the switch auction date. Accordingly, switch operations of G-sec amounting to ₹1,64,803 crore were completed during 2019-20 as against ₹28,059 crore in the previous year. Like last year, the budget for buyback operations was kept zero for the year. VII.7 Following the discontinuation of old 2-year and 5-year G-sec, issuance of new G-sec in these maturities was undertaken, including a new 7-year security (7.27% GS 2026). Floating Rate Bonds (FRBs) were also issued during the year in order to broaden the investor base. The share of FRBs in total issuances during 2019-20 was 8.5 per cent, lower than 9.1 per cent in the previous year. VII.8 Under the Foreign Central Bank (FCB) scheme, the Department invests in Indian G-sec on behalf of select FCBs and multilateral development institutions in the secondary market. In consultation with the central government, the scheme has been extended to multilateral financial institutions and multilateral development banks. Further, Treasury Bills (T-Bills) were also included as eligible instruments under the scheme. Total volumes (purchase and sell) transacted on behalf of FCBs stood at ₹4,500 crore (face value) during 2019-20, up from ₹1,297 crore in the previous year. During 2019-20, 180 Gilt Account Holders (GAHs) accessed the NDS-OM-Web and undertook 93,697 trades worth ₹11.54 lakh crore as compared with 72,229 trades worth ₹6.97 lakh crore in the previous year. VII.9 The guidelines for PDs are under review to, inter alia, achieve the objectives of Market Making Scheme and to ensure better retailing of G-sec by PDs. VII.10 Various measures have been taken to diversify the investor base for SDLs. Among them are steps taken to encourage participation of retail investors in SDL market, including introduction of non-competitive bidding in primary auctions. In this direction, Specified Stock Exchanges (besides scheduled banks and primary dealers) have been permitted to act as Aggregators/Facilitators to consolidate the bids of their stockbrokers/other retail participants and submit a single bid under the non-competitive segment of the primary auction of the SDLs, following an announcement through circular dated November 7, 2019. A stripping/reconstitution facility for SDLs, similar to the one for central government securities was announced in the Reserve Bank’s Statement on Developmental and Regulatory Policies of August 7, 2019. This measure will be implemented in consultation with the state governments. VII.11 A proposal to explore various investment avenues for state governments including the review of the Consolidated Sinking Fund (CSF) / Guarantee Redemption Fund (GRF) scheme is in progress. In this regard, a Discussion Paper has already been submitted to the Executive Committee (EC) to State Finance Secretaries (SFS). VII.12 In 2016, the Advisory Committee on WMA scheme for state governments (Chairman: Shri Sumit Bose) had recommended that the WMA limits be revised to ₹32,225 crore for all states/ UTs together and Committee-based next revision of WMA may be effected in 2020-21, taking into account the roadmap laid by the Report of the Fifteenth Finance Commision. Currently, a new Committee (Chairman: Shri Sudhir Shrivastava) is examining these limits. The Committee is yet to submit its report to the Reserve Bank. VII.13 Capacity building programmes for sensitising state governments about the prudent measures of cash and debt management were conducted in five states (viz., Rajasthan, Bihar, Assam, Karnataka and Odisha). Meetings between states and investors were also facilitated during the year. VII.14 In order to improve data dissemination, dashboards were created and made available to the public through Database on Indian Economy (DBIE). It provides current information related to auctions, gross and net market borrowings of the central and state governments and secondary market yield movements. Debt Management of the Central Government VII.15 During 2019-20, the gross market borrowings through dated G-sec were higher by 24.3 per cent than a year ago. Net market borrowing through dated G-sec also increased by 12.1 per cent on account of higher borrowings during the year. Net market borrowing through dated G-sec financed 61.8 per cent of the centre’s gross fiscal deficit (GFD) as against 65.1 per cent in the previous year. The net market borrowing through dated securities and T-Bills taken together also increased in 2019-20 (Table VII.1). Debt Management Operations VII.16 The weighted average yield (WAY) on GoI dated securities issued during 2019-20 declined by 93 basis points (bps) on a year-on-year basis. The weighted average coupon on dated securities on the entire debt stock also decreased albeit marginally. Consequent upon the decision by the GoI to undertake more borrowings in the maturity bucket of over 15 years, the weighted average maturity (WAM) of issuances increased during 2019-20, resulting in a marginal increase in WAM on the outstanding debt (Table VII.2). VII.17 During 2019-20, G-sec yields softened considerably with 10-year benchmark yield moderating by 121 basis points (bps) from 7.35 per cent to 6.14 per cent, attributed to cumulative reduction in repo rate by 185 bps during the year, coupled with accommodative policy stance and OMO purchases. A new 10-year G-sec paper (6.45% GS 2029) was also issued on October 7, 2019 with a coupon considerably lower than that of the previous issuance (7.26% GS 2029 issued on January 8, 2019). Further, the Reserve Bank announced various other monetary easing measures which impacted the yield curve. Specifically, special OMOs of ₹40,000 crore were conducted in December 2019 and January 2020, wherein the Reserve Bank bought long-term securities and sold short-term securities simultaneously. The Reserve Bank also conducted Long Term Repo Operations (LTROs) for 1-year and 3-year tenors at policy repo rate for ₹1,25,000 crore in February and March 2020 to provide durable liquidity to the system at reasonable cost. Since the credit offtake in the system remains muted, the LTROs resulted in significant softening in G-sec yields for short-tenor papers. These developments led to increase in spreads between short-term and long-term G-sec yields, steepening the yield curve towards the end of March 2020. A downward kink was observed in the G-sec yield curve around the 10-year tenor, partly explained by the high liquidity premium in the 10-year benchmark paper and also on account of the special OMOs conducted by the Reserve Bank, which brought down yields of the 10-year paper more than the adjacent tenors. The yield curve remained flat beyond 14-year G-sec papers and took a roughly parallel shift downward relative to the previous year (Chart VII.1).  VII.18 During 2019-20, about 54.2 per cent of the market borrowing were raised through issuance of dated securities with a residual maturity of 10 years and above, as compared with 53.5 per cent in the previous year, resulting in a marginal decrease in the share of securities with maturity less than 10 years during the year. Further, 30-year and 40-year tenor papers were issued/reissued during the year with the objective of catering to the demand for long-term investors such as insurance companies and pension funds (Table VII.3). Issuance of Special GoI Securities VII.19 Special GoI securties (non-transferable) for the purpose of recapitalisation were issued to 13 public sector banks (PSBs), EXIM Bank, IDBI Bank and Indian Infrastructure Finance Company Ltd. (IIFCL) for a total amount of ₹75,847.60 crore in 7 tranches on a cash-neutral basis. Coupons on those securities ranged between 6.13 - 6.79 per cent. Treasury Bills VII.20 Short-term cash requirements of the government are met through issuance of T-Bills. The net short-term market borrowing of the government through T-Bills (91, 182 and 364 days) marginally increased to ₹37,528 crore during 2019-20 as against ₹35,600 crore in the previous year. Ownership of Securities VII.21 Commercial banks and cooperative banks taken together remained the largest holders of G-sec accounting for 41.9 per cent as at end-March 2020, followed by insurance companies (26.2 per cent) and provident funds (10 per cent). The share of the Reserve Bank was 9.5 per cent and the share of FPIs was 1.5 per cent. The other holders of G-sec are pension funds, mutual funds, state governments, financial institutions (FIs) and corporates. Primary Dealers and Devolvement VII.22 The number of primary dealers (PDs) stood at 21 [14 Bank-PDs and 7 Standalone PDs (SPDs)] at end-March 2020. All the PDs maintained capital to risk-weighted assets ratio (CRAR) above the minimum requirement of 15 per cent during the year. The mandate of underwriting primary auctions of dated G-sec has been given to PDs with a target of achieving bidding commitment/success ratio in respect of Treasury Bills (T-Bills)/cash management bills (CMBs). The PDs individually achieved the stipulated minimum success ratio of 40 per cent, with an average of 62.78 per cent in H1: 2019-20 and 60.62 per cent in H2. The share of PDs in auctions of T-Bills/ CMBs was 71.67 per cent during 2019-20 as compared with 71.44 per cent in the previous year. The underwriting commission paid to PDs during 2019-20 was ₹41.04 crore as compared with ₹139.86 crore in the previous year, reflecting reduced domestic market volatility relative to previous year. Sovereign Gold Bonds Scheme VII.23 In consultation with the Government of India, the Reserve Bank issued 10 tranches of Sovereign Gold Bonds (SGBs) for an aggregate amount of ₹2,316.37 crore (6.13 tonnes) during 2019-20. Under the SGB scheme, bonds are denominated in units of one gram of gold and multiples thereof. The minimum annual investment is one gram with a maximum limit of 4 kg per individual, 4 kg per Hindu Undivided Family (HUF) and 20 kg for trusts and similar entities notified by the government from time to time. A total of ₹9,652.78 crore (30.98 tonnes) has been raised through the scheme (37 tranches) since its inception in November 2015. Cash Management of the Central Government VII.24 The central government started the year 2019-20 with a cash balance of ₹1,27,693 crore. The WMA limits for the first and second half of the year were ₹75,000 crore and ₹35,000 crore, respectively. The central government resorted to WMA for 189 days during 2019-20 vis-à-vis 173 days in the previous year and went into overdraft (OD) for 52 days vis-à-vis 50 days during the same period. The highest amount of WMA/OD resorted to was ₹1,33,188 crore on January 4, 2020. The central government issued CMBs of ₹3,00,000 crore, with tenors ranging between 10 to 84 days to tide over short-term mismatches in cash flows during 2019-20. The year ended with central government’s cash balance at ₹ 55,573 crore (Chart VII.2).  Debt Management of State Governments VII.25 Following the recommendation of the 14th Finance Commission (FC) to exclude states from the National Small Savings Fund (NSSF) financing facility (barring Delhi, Madhya Pradesh, Kerala and Arunachal Pradesh), market borrowings of states have been increasing over the last few years. The share of market borrowing in financing GFD consequently rose to 87.9 per cent in 2019-20 (BE) from 84.0 per cent in 2017-18. VII.26 Both gross and net market borrowing of states were higher during 2019-20 than a year ago. Gross market borrowing increased by 32.7 per cent, while the net borrowing increased by 39.8 per cent, reflecting lower growth (y-o-y) in redemptions during the year (Table VII.4). There were 636 issuances in 2019-20, of which 114 were re-issuances (467 issuances in 2018-19, of which 59 were re-issuances), reflecting the efforts of state governments towards debt consolidation. VII.27 The weighted average yield (WAY) of cut-off yield for State Development Loans (SDLs) issued during 2019-20 was lower at 7.24 per cent than 8.32 per cent in the previous year. Accordingly, the weighted average spread (WAS) of SDL issuances over comparable central government securities was 55.02 bps in 2019-20 as compared with 64.66 bps in the previous year. In 2019-20, seventeen states and one union territory issued non-standard securities of tenors ranging from 2 to 40 years. As a strategic response to higher spreads, 9 states rejected all the bids in some of the auctions. Following the policy of passive consolidation, 11 states (viz., Bihar, Gujarat, Haryana, Himachal Pradesh, Karnataka, Madhya Pradesh, Maharashtra, Punjab, Rajasthan, Tamil Nadu and Telangana) undertook re-issuances during 2019-20, which helped in creating liquidity for their securities in the secondary market. The average inter-state yield spread on 10 year fresh issuance was 6 bps in 2019-20, the same as observed in 2018-19, reflecting their continued disconnect from the fiscal health of issuing states. Cash Management of State Governments VII.28 Following the recommendations of the Advisory Committee on WMA scheme for state governments (Chairman: Shri Sumit Bose), the WMA limit was set at ₹32,225 crore for all states/ UTs together until the next review in 2020-21. Currently, a new Committee (Chairman: Shri Sudhir Shrivastava) is reviewing these limits. Pending its recommendations, it was decided on April 1, 2020 to increase the WMA limit by 30 per cent from its existing level to enable states/ UTs to tide over COVID-19. On April 17, 2020, the Reserve Bank decided to further increase the WMA limit by 60 per cent over and above the level as on March 31, 2020. This interim measure will remain valid till September 30, 2020. Relaxation in the overdraft (OD) scheme has been given to state governments/UTs to tide over mismatches in cash flows by increasing the number of days for OD, effective April 7, 2020, till September 30, 2020. Sixteen states availed the Special Drawing Facility (SDF) in 2019-20. Thirteen states resorted to WMA and ten states availed OD. VII.29 Over the years, states have been accumulating a sizeable cash surplus in the form of intermediate treasury bills (ITBs) and auction treasury bills (ATBs), which, however, entail a negative carry cost, i.e., there is a negative spread of 524 bps as at end-March 2020 between the average borrowing cost of states (7.24 per cent) and the average rate of return on ATBs/ ITBs (2 per cent). The outstanding investment of states in ITBs was ₹1,54,757 crore at end-March 2020, while outstanding investment in ATBs was ₹33,504 crore (Table VII.5). Investments in Consolidated Sinking Fund/ Guarantee Redemption Fund VII.30 The Reserve Bank manages two reserve fund schemes on behalf of state governments (SGs) – the Consolidated Sinking Fund (CSF) and the Guarantee Redemption Fund (GRF) [Box VII.1]. These reserve funds are built up from the contributions made by the SGs voluntarily and are being managed as per the schemes notified by SGs. CSF is an amortisation fund and was introduced in 1999 to meet repayment obligations of the SGs. After a 5-year lock-in period, states are eligible to withdraw the interest accrued and accumulated up to the close of previous financial year (FY). A working group in 2012 recommended to build up a minimum corpus of 3 to 5 per cent of state liabilities within next 5 years. So far, 24 states and one union territory, i.e., Puducherry have set up CSF. GRF is constituted by SGs for meeting their obligations arising out of the guarantees issued on behalf of state level entities. The Reserve Bank circulated the scheme of GRF to the SGs in August 2001 for voluntary adoption and it envisaged an initial contribution of at least 1.0 per cent of outstanding guarantees at the end of the previous year and thereafter minimum 0.5 per cent every year to achieve a minimum level of 3 per cent in next five years. Accretions in the Fund can be utilised only towards payment of guarantees issued by the SGs and invoked by the beneficiary. Presently, 18 states are members of the GRF. States can also avail a special drawing facility (SDF) at a discounted rate from the Reserve Bank against their incremental annual investment in CSF and GRF. Outstanding investment by states in the CSF and GRF at end-March 2020 was ₹1,30,431 crore and ₹7,486 crore, respectively, as against ₹1,14,701 crore and ₹6,513.73 crore at end-March 2019. Total investment in CSF/GRF was ₹23,464 crore in 2019-20. Total disinvestment by states from CSF and GRF was ₹47.40 crore during 2019-20.

VII.31 The Union Budget 2020-21 projects gross market borrowing through dated securities at ₹7,80,000 crore (3.5 per cent of GDP), higher by about 9.9 per cent than ₹7,10,000 crore in 2019-20. Net market borrowing [including short-term debt and repayment of Post Office Life Insurance Fund (POLIF)] is budgeted at ₹5,35,870 crore, financing 67.3 per cent of the GFD in 2020-21 [65.1 per cent in 2019-20 (RE)]. After reviewing the cash position and requirements of the central government, the Government of India (GoI) in consultation with the Reserve Bank of India, decided to modify the indicative calendar for issuance of G-sec for the remaining part of the first half of the fiscal 2020-21 (May 11-September 30, 2020) and revised the gross market borrowings to ₹12 lakh crore for the full year 2020-21. Further, in order to provide additional resources to the states in view of COVID-19, the borrowing limits of the state governments has also been increased from the existing 3 per cent to 5 per cent of GSDP, subject to conditions. VII.32 Given these requirements, the market borrowing programme is proposed to be conducted with the following strategic milestones so as to achieve the overall goals of debt management set out in the beginning of this chapter:

VII.33 In sum, during 2019-20, combined gross market borrowings of centre and states were conducted successfully in line with the guiding principles of debt management. The Reserve Bank has also announced a number of interim measures to manage the stress on the finances of both centre and states in the wake of the COVID-19 pandemic. Going ahead, consolidation of government debt will be the key area of focus of the Reserve Bank. |

ಈ ಪುಟವನ್ನು ಹಂಚಿಕೊಳ್ಳಿ:

ಭಾರತೀಯ ರಿಸರ್ವ್ ಬ್ಯಾಂಕ್ ಮೊಬೈಲ್ ಅಪ್ಲಿಕೇಶನ್ ಅನ್ನು ಇನ್ಸ್ಟಾಲ್ ಮಾಡಿ ಮತ್ತು ಇತ್ತೀಚಿನ ಸುದ್ದಿಗಳಿಗೆ ತ್ವರಿತ ಅಕ್ಸೆಸ್ ಪಡೆಯಿರಿ!

ನಮ್ಮ ಅಪ್ಲಿಕೇಶನ್ ಅನ್ನು ಸ್ಥಾಪಿಸಲು QR ಕೋಡ್ ಅನ್ನು ಸ್ಕ್ಯಾನ್ ಮಾಡಿ

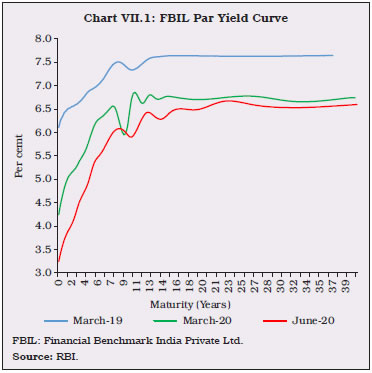

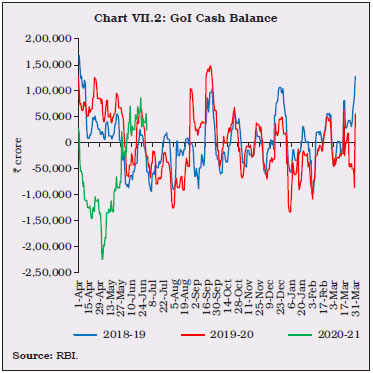

ಪೇಜ್ ಕೊನೆಯದಾಗಿ ಅಪ್ಡೇಟ್ ಆದ ದಿನಾಂಕ: