IST,

IST,

Chapter III: Regulatory Initiatives in the Financial Sector

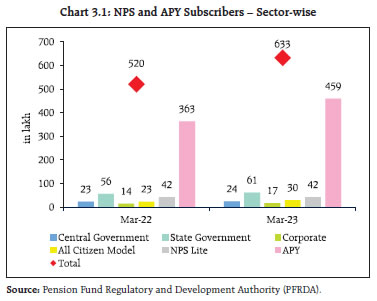

Global regulatory initiatives continue to focus on safeguarding financial stability, improving resilience of banks and non-bank financial intermediaries, managing digital innovation, addressing climate-related financial risks and full and consistent implementation of Basel III regulatory reforms. Domestic regulatory efforts aim to improve financial sector soundness and efficiency, deepen financial markets, strengthen cyber resilience and supervision. The Financial Stability and Development Council (FSDC) and its Sub-Committee remain vigilant and committed to improve operational dynamism, preserve stability and enhance inclusivity of the Indian financial system. Introduction 3.1 The recent banking turmoil in some of the AEs has put post-GFC financial reforms to test. Global regulatory efforts are focussed on addressing banking system fragility and vulnerabilities associated with high debt levels, fragile market liquidity, tightening of financial conditions, and liquidity and leverage issues in non-bank financial intermediaries (NBFIs)1. Risks associated with digital finance, cyber security and climate change are other major focus areas. 3.2 Against this backdrop, this chapter reviews the recent regulatory initiatives undertaken globally and in India to improve the resilience and efficiency of the financial system. III.1 Global Regulatory Developments and Assessments 3.3 Rapid and forceful responses by regulators in the affected economies to the recent bank failures helped to maintain financial stability and limit spillovers. Yet, concerns remain about build up of vulnerabilities in the financial system as the impact of monetary tightening gets exacerbated by idiosyncratic risks such as concentrated business models, presence of wholesale and uninsured deposits, poor risk management and governance2. III.1.1 Deposit Stability 3.4 The report3 of the Federal Deposit Insurance Corporation (FDIC) on the options for deposit insurance reform observed that bank failures were largely caused by convergence of rapid asset growth in banks funded by uninsured deposits, exposure to unrealised losses in their securities portfolio and business models concentrated on providing services to digital asset firms. It highlighted the contribution of technological developments in quickening information dissemination and consequently, faster depositor runs. Three options to reform the deposit insurance system are offered: (a) limited coverage, which maintains the current structure of finite deposit insurance limit; (b) unlimited coverage of all deposits; and (c) targeted coverage, which allows different levels of deposit insurance coverage across different types of accounts and focusses on higher coverage for business payment accounts. It identifies the third option (viz., targeted coverage) as having the greatest potential to mitigate undesirable consequences related to cost of coverage. III.1.2 Markets and Financial Stability 3.5 The report of the Advisory Scientific Committee (ASC) of the European Systemic Risk Board (ESRB)4 observed that the enhanced lender of last resort (LOLR) and market maker of last resort (MMLR) functions of central banks can achieve the stabilisation of financial markets, but moral hazard issues remain a major deterrent. The report presented a set of attributes for effective enhanced LOLR and MMLR functions, including (a) supporting only financial markets that are deemed essential; (b) developing continuous capacity to price securities that could be accepted as collateral in a lending operation or be purchased outright; (c) offering pricing that would be unattractive in normal times to control moral hazard; (d) lending only to regulated and supervised entities to ensure solvency; and (e) exiting quickly when market liquidity has been restored. 3.6 The report5 of the Committee on the Global Financial System (CGFS) (Bank for International Settlements) highlighted the effect of central bank asset purchases (APs) in terms of reduced bond yields, improved liquidity conditions and averting a destabilising loop of downward spirals and fire sales. For EMEs, the motivation for APs was limited to addressing market dysfunction whereas in AEs, the policy objective included implementing an expansionary policy stance when policy rates were constrained by the effective lower bound (ELB). The impact of APs operates through multiple channels like signaling, liquidity and portfolio rebalancing with their relative importance differing across time and economies. The liquidity channel becomes important when market conditions are stressed. The signaling channel indicates the policy stance that impacts financial conditions but is less important than the portfolio rebalancing channel, especially in countries with policy rates above the effective lower bound. The report also observed that APs can have side effects, including cross-country spillovers, suppression of risk premia, losses on balance sheets for central banks and low bond market liquidity. 3.7 In its report6 on financial stability aspects of commodity markets, the Financial Stability Board (FSB) observed that commodity traders are connected to the core financial system through a range of physical and derivatives markets, where banks are a major source of credit and liquidity funding for the segment and provide clearing services. Juxtaposition of concentration and interlinkages in the commodities sector along with large and leveraged commodity traders, less standardised margining practices and opacity in over-the-counter (OTC) markets could propagate losses in the event of stress. This highlights the risk of demand for funding liquidity that commodity market players may face in the event of higher margin calls by central clearing counterparties (CCPs). Continuous monitoring of developments in commodity markets to manage sudden increases in margin on derivatives position and identifying data gaps inhibiting the assessment of vulnerabilities for quantifying the transmission channels for financial stability assume critical importance in this regard. 3.8 The International Organization of Securities Commissions (IOSCO) revised its September 2011 principles for the regulation and supervision of commodity derivatives market (Principles)7 to address volatility and developments in commodity markets. The revised Principles are directed to support price discovery and hedging functions, improve market surveillance, address manipulation and abusive trading schemes and strengthen enforcement powers of trading venues. It is recommended that authorities may provide alternative delivery points for physically settled commodity derivatives to mitigate the stress around delivery point failure during extraordinary disruptions. To manage excessive price volatility, authorities may impose suspension or cancellation of trades in disorderly market conditions. The Principles suggest implementing maximum price fluctuations and position limits to mitigate price volatility and provide time for market participants to arrange necessary financing. A new principle (Principle on unexpected disruptions in the market) has been added to guide the regulators in the scenario of extreme price volatility due to extraordinary disruptions such as pandemics and wars. It aims to maintain orderly markets, safeguard investors’ interest and discourage higher risk-taking by market participants. Acknowledging the differences in structure and practices of the underlying spot market and market participants, the report has suggested implementing the principles with due consideration to the jurisdictional specificities of the underlying market. III.1.3 Decentralised Finance and Financial Stability 3.9 The FSB report on the financial stability risks of decentralised finance (DeFi)8 highlights the vulnerabilities and rising interconnectedness of crypto-based DeFi with centralised crypto-asset trading, lending and borrowing platforms. DeFi inherits and even amplifies existing TradFi vulnerabilities such as operational fragilities, liquidity and maturity mismatches, leverage, and interconnectedness. The amplification of known vulnerabilities comes from novel technological features such as smart contracts and blockchain, the high degree of structural interlinkages and from non-compliance with existing regulatory requirements. Due to pseudonymity, financial intermediation in DeFi largely rests on the use of collateral and leverage. The use of leverage leads to procyclicality and can trigger sharp adjustments in prices that have knock-on effects on other market participants. The report suggests that FSB’s crypto-asset monitoring framework should be complemented with DeFi-specific indicators of vulnerabilities. Furthermore, the growth of tokenisation of real assets could increase interconnections of crypto-asset markets and DeFi with the broader financial system and the real economy. 3.10 The European Union has passed the first comprehensive legislation on Markets in Crypto Assets (MICA)9, a broad framework which covers the issuance, trading and disclosure requirements for crypto-assets10. The regulation mainly covers three types of crypto-assets, namely asset-referenced tokens (ART)11, electronic money tokens (EMT)12, and other crypto-assets like utility tokens13 not covered by existing law. MICA has excluded central bank digital currencies (CBDC) and non-fungible tokens (NFT) from its purview, except where NFTs fall under existing crypto-asset categories. MICA has set rules for crypto-asset issuers and crypto-asset service providers (CASPs), including consumer protection rules for the issuance, trading, exchange, custody of crypto-assets and creating a market abuse regime for prohibiting market manipulation and insider dealing. The framework aims to support market integrity and financial stability by regulating public offers of crypto-assets. Major CASPs will be required to disclose their energy consumption to reduce carbon footprints. The framework is expected to provide regulatory clarity, create safeguards and set standards for the use of blockchain technology. III.1.4 Financial Stability Implications of Stablecoins – An EMDE Perspective 3.11 The previous issues of the Financial Stability Report have highlighted the inherent volatility associated with crypto-assets, the collapse of stablecoins and the potential risks to financial stability. It is globally reckoned that crypto assets are speculative instruments which fail to meet key requirements to be termed as money. The stablecoin category of crypto-assets has been exposed to episodes of collapse and redemption pressures in recent times. It is also recognised that private tokenised money which circulate as bearer instruments may entail departures in their relative exchange values away from par in violation of the “singleness of money” (i.e., monetary exchange is not subject to fluctuating exchange rates between different forms of money)14. Their purported benefits in terms of financial inclusion, cheaper and faster payments and cross-border remittances are, however, yet to be realised. 3.12 The pull factors for crypto-assets, which are inevitably denominated in convertible currencies, lack application of full anti-money laundering (AML)/ countering the financing of terrorism (CFT) standards and have features that facilitate anonymity and bypass controls. The associated risks are serious and include: (i) reserve assets of stablecoins generally comprise of investments denominated in select freely convertible foreign currency, which would be destabilising for EMDEs through currency substitution; (ii) their large scale adoption would lead to cryptoisation (i.e., greater use of crypto-assets as a substitute of fiat currency and traditional financial assets) of an economy, which could lead to major currency mismatch risks15 on the balance sheets of banks, firms, and households; (iii) it would limit an EMDE central bank’s ability to effectively control domestic interest rate and liquidity condition to meet its macroeconomic policy objectives; (iv) the decentralised, borderless, and pseudonymous characteristics of crypto-assets being transacted without involving regulated financial intermediaries for identifying remitter/ beneficiary/nature of transactions, make them potentially attractive instruments to circumvent capital flow management measures16, which have serious financial stability risks, especially in periods of capital flow volatility and negative spillovers; (v) as an alternative to domestic financial system, the crypto ecosystem will hinder banks’ ability to mobilise deposits in fiat currency and, in turn, credit creation, where any loss of customer relationships can undermine the credit risk assessment17; and (vi) peer-to-peer transfer (domestic or cross-border) to un-hosted/self-hosted wallets are difficult to track, and the rise of anonymity-enhanced cryptocurrencies (for e.g., privacy coins, mixers, decentralised platforms and exchanges) increase obfuscation of identity and financial flows, which in turn, give rise to increased potential of money laundering and terrorism financing risks. 3.13 Though the market capitalisation of stablecoins is relatively small (nearly US$ 130 billion in June 202318) when compared to the traditional financial system, there is a possibility of continued growth and interconnectedness, giving rise to financial stability risk concerns and negative spillover risks, which may be difficult to contain once the systemic exposure crosses a threshold. The lack of authenticated data and inherent data gaps in the crypto ecosystem impede a proper assessment of financial stability risks. 3.14 Three policy responses (ban, contain or regulate) have been offered to address the risks posed to consumers, investors, market integrity, financial stability and also specific risks posed to EMDEs with respect to monetary sovereignty and ‘cryptoisation’19. A globally coordinated approach is warranted to analyse risks posed to EMDEs vis-à-vis AEs, especially on macroeconomic challenges (losing monetary control; local currency volatility), development challenges (weaker capacity to address AML/ CFT risks) and cross border challenges (oversight). In this context, under India’s G20 presidency, one of the priorities is to create a framework for global regulation of unbacked crypto-assets, stablecoins and DeFi, by considering both macroeconomic and regulatory perspectives to address the full range of risks posed by crypto-assets, including risks specific to EMDEs. III.1.5 Cyber Risk and Financial Stability 3.15 In its report on advancing macroprudential tools for cyber resilience20, the European Systemic Risk Board (ESRB) highlights the heightened cyber threat environment and encourages authorities to pilot system-wide cyber resilience scenario testing (CyRST), which can complement other analytical tools to deepen their understanding of the associated risks. The report advocates use of the systemic impact tolerance objective (SITO) – the point at which the tolerance of disruption of the financial system is deemed to be breached to assess coordination and action capabilities. ESRB will identify key economic functions where disruptions have cross border implications and also analyse operational policy tools that are most effective in responding to a system-wide cyber incident and identifying gaps across operational and financial policy tools. The report also assesses the efficacy of financial policy tools like capital buffers, deposit insurance, recovery and resolution framework, moratorium powers and central bank liquidity provisions in the event of a cyber incident. 3.16 The FSB report on cyber incident reporting (CIR)21 has focused on measures to address impediments in achieving greater convergence, enhancing the cyber lexicon and setting up a common format for incident reporting exchange (FIRE). Recognising that a one-size-fits-all approach is not feasible, FSB has provided recommendations to address issues on collection of cyber incident information including defining objectives, improving cross- border interoperability, identifying common data requirements and standardised reporting formats, selecting reporting triggers and addressing gaps in cyber incident response capabilities. It observes that triggers, reporting windows and guidelines adopted by financial authorities should be consistent with their legal and regulatory framework. The report stresses on inclusion of severe but plausible cyber scenarios and stress test in the organisational playbook, effective log management and forensic capabilities, sharing information and pooling knowledge in collective defence of financial sector for effective incident detection and reporting. III.2 Domestic Regulatory Developments 3.17 Since the publication of the December 2022 issue of the FSR, the Financial Stability and Development Council (FSDC), chaired by Union Finance Minister, met once on May 08, 2023. The Council deliberated upon the need for expeditious formulation and implementation of the policy and legislative reform measures required to further develop the financial sector and increase the access of financial services to the people. 3.18 The FSDC committed to maintaining constant vigil by all regulators to enhance financial sector stability, reduce compliance burden on regulated entities (REs), monitor debt levels of corporates and households in India, simplification and streamlining of know-your-customer (KYC) framework to meet the needs of Digital India, improve seamless experience for retail investors in government securities, introduction of Bimakrit Bharat – a unique value proposition to take insurance to last mile and resolve inter-regulatory issues relating to Gujarat International Finance Tec-City - International Financial Services Centre (GIFT-IFSC). III.3 Initiatives by Regulators/Authorities 3.19 The financial sector regulators undertook several initiatives to improve the resilience of the Indian financial system (Annex 3). III.3.1 Climate Risk and Sustainable Finance 3.20 The Reserve Bank released a framework for acceptance of Green Deposits22 for REs to foster and develop green finance ecosystem in the country. The framework aims to encourage more REs to offer green deposits to customers, protect depositors’ interest, address greenwashing23 concerns and help augment the flow of credit to green activities/ projects. REs shall put in place a Board approved financing framework (FF) for effective allocation of green deposits covering eligible green activities/ projects. The following sectors, adopted from the Government of India’s ‘Framework for Sovereign Green Bonds’, published in November 2022, have been identified as green activities/projects for allocation of proceeds by REs: (i) renewable energy; (ii) energy efficiency; (iii) clean transportation; (iv) climate change adaptation; (v) sustainable water and waste management; (vi) pollution prevention and control; (vii) green buildings; (viii) sustainable management of living natural resources and land use; and (ix) terrestrial and aquatic biodiversity conservation. REs shall annually undertake the impact assessment and third-party verification and the reports shall be placed on their website. III.3.2 Governance, Measurement and Management of Interest Rate Risk in Banking Book (IRRBB)24 - Final Guidelines 3.21 Excessive IRRBB can pose significant risk to banks’ current capital base and/ or future earnings, if not managed appropriately. The Reserve Bank’s final guidelines on IRRBB require banks to measure, monitor and disclose their IRRBB in terms of potential change in economic value of equity (ΔEVE) and net interest income (ΔNII), computed on the basis of a set of prescribed interest rate shock scenarios. Banks should have a clearly defined Board approved risk appetite statement, articulated in terms of the risk to both economic value and earnings, which lays down policies and procedures for limiting and controlling IRRBB. Banks should also develop and implement an effective stress testing framework for IRRBB as part of their broader risk management and governance processes. Furthermore, banks should perform qualitative and quantitative reverse stress tests to identify interest rate scenarios that could severely threaten their capital and earnings. 3.22 Banks, which generate an EVE decline of more than 15 per cent of their Tier 1 capital under any one of the six prescribed interest rate shock scenarios, shall be identified as outliers with undue IRRBB exposure. These outlier banks shall be required to take one or more of the following actions as determined during the Reserve Bank’s supervisory review and evaluation process (SREP): (a) raise additional capital; (b) reduce IRRBB exposures (e.g., by hedging); (c) set constraints on the internal risk parameters used by the bank; and/ or (d) improve the risk management framework. The extant instructions on interest rate risk management, which require banks to undertake traditional gap analysis (TGA) and Duration Gap Analysis (DGA), shall be phased out post implementation of the new guidelines. III.3.3 Guidelines on Default Loss Guarantee (DLG) in Digital Lending 3.23 Certain business practices of NBFCs could create new risks as, under DLG agreements entered into by some NBFCs with Digital Lending Apps (DLAs)/ Fintech companies, up to 100 per cent of the credit risk was borne by the latter due to the First Loss Default Guarantee (FLDG) provided to the former. Under such arrangements, the DLAs effectively lent their own funds to borrowers using the license of an NBFC who did not share any risk but were getting a guaranteed yield in return. Proliferation of such instances could inflate the risks associated with unregulated lending as well as delay the process of identification of stress in specific sectors/ portfolios. 3.24 Considering the need to strike a balance between prudence and innovation, the Reserve Bank issued instructions permitting DLG arrangements with suitable regulatory guardrails. DLG arrangements involve lending service providers (LSPs) offering to bear default losses on a loan portfolio up to a pre-determined percentage of the portfolio where the RE has an outsourcing agreement with such LSPs. REs shall ensure that total amount of DLG cover on any such portfolio shall not exceed five per cent of the amount of that loan portfolio and the same can be offered only in the form of cash, fixed deposit or bank guarantee. Further, REs shall put in place a Board approved policy before entering into any DLG arrangement. Any DLG arrangement shall not act as a substitute for credit appraisal requirements. Also, in order to promote transparency, REs are required to ensure disclosure of DLG on the website of LSPs. III.3.4 Master Direction on Outsourcing of Information Technology (IT) Services 3.25 The Reserve Bank issued master direction on outsourcing of IT services to third parties to ensure effective management of financial, operational and reputational risks with the underlying principle that outsourcing arrangements neither diminish REs ability to fulfil obligations to customers nor impede effective supervision by the Reserve Bank. 3.26 The directions require REs to ensure that the service provider employs the same high standard of care in performing the services as would have been employed by the RE. Outsourcing should neither impede nor interfere with the ability of the RE to effectively oversee and manage the activities of the service provider located in India or abroad. REs shall evaluate the need for outsourcing of IT services based on a comprehensive assessment of attendant benefits, risks and availability of commensurate processes to manage those risks. Each RE shall also put in place a comprehensive Board approved outsourcing policy and a risk management framework. The directions also mandate REs to require service providers to develop and establish a robust business continuity plan (BCP) and disaster recovery plan (DRP), besides putting in place a management structure to monitor and control the outsourced IT activities. The directions also specify provisions pertaining to cross-border outsourcing, exit strategy, risk management, evaluation and engagement of the service providers. They also envisage a robust grievance redressal mechanism wherein the responsibility for redressal of customers’ grievances related to outsourced services shall rest with the RE. III.3.5 Master Direction on Acquisition and Holding of Shares or Voting rights in Banking Companies 3.27 The Reserve Bank released the guidelines on acquisition and holding of shares or voting rights in banking companies with the intent of ensuring that the ultimate ownership and control of banking companies are well-diversified and their major shareholders are ‘fit and proper’ on a continuing basis. The guidelines that are applicable to all banking companies, including local area banks, small finance banks and payments banks operating in India25 stipulate that any person who intends to make an acquisition which is likely to result in major shareholding i.e., an “aggregate holding” of five per cent or more of the paid-up share capital or voting rights in a banking company26, is required to seek an advance approval of the Reserve Bank. On receipt of the reference from the Reserve Bank, the board of directors of the banking company shall deliberate on the proposed acquisition and assess the ‘fit and proper’ status of the person. The guidelines limit the shareholding to 10 per cent for non-promoters and 26 per cent for promoters, subject to certain conditions. 3.28 A banking company shall continuously monitor that its major shareholders27 and applicants are ‘fit and proper’ on an ongoing basis. Subsequent to such acquisition, if the aggregate holding falls below five per cent at any point in time, the person will be required to seek fresh approval from the Reserve Bank if the person intends to again raise the aggregate holding to five per cent or more of the paid-up share capital or total voting rights of the banking company. The guidelines also clarified the concept of ‘indirect holding’ of shares/voting rights in banks with an illustrative list of such holdings. III.3.6 Framework for Compromise Settlements and Technical Write-offs28 3.29 With a view to provide further impetus to resolution of stressed assets in the system, the framework on compromise settlements and technical write-offs was issued by the Reserve Bank. The framework provides clarity on the definition of technical write-off and a broad guidance on the process to be followed by REs while carrying out technical write-off. Further, it lays down guidance on important process-related matters covering board oversight, delegation of power, reporting mechanism and a cooling period for normal cases of compromise settlements. The penal measures currently applicable to borrowers classified as fraud or wilful defaulter shall, however, remain in cases where banks enter into compromise settlements with such borrowers. III.3.7 Applicability of State Money Lenders Acts and State Microfinance Acts on NBFCs 3.30 Non-banking Financial Companies (NBFCs) are registered and regulated by the Reserve Bank under the Reserve Bank of India Act, 1934. 3.31 Legislations in some states (viz., State Money Lenders Acts and State Microfinance Acts) extended their applicability to include the oversight and functioning of NBFCs which are registered and regulated by the Reserve Bank. Any duality of regulation and potentially discordant compliance requirements can disincentivise the NBFCs from operating in the state. In turn, this may drive vulnerable borrowers to informal sources for meeting their credit requirements, thus rendering them vulnerable to unfair practices. Moreover, this can also reverse the efforts of the Government and the Reserve Bank towards furthering financial inclusion. In case of major defaults by borrowers of NBFCs and, in turn, by NBFCs on loans from their upstream lenders, including banks, the risk of contagion spreading is high. In this context, the High Court of the State of Telangana in its judgement dated February 14, 2023 has held that NBFCs (registered under the Reserve Bank of India Act, 1934 and regulated by the Reserve Bank) operating in the states of Telangana and Andhra Pradesh would be excluded from the purview of the Telangana Microfinance Act and Andra Pradesh (AP) Microfinance Act, respectively. Earlier, in its judgement dated May 10, 2022 the Supreme Court held that State Money Lenders Act will have no application to NBFCs registered under the RBI Act and regulated by the Reserve Bank. The clarity provided by these judgements on regulatory authority for NBFCs operating in a state bodes well for the financial intermediation in the country. III.3.8 Single Settlement for Three Cheque Truncation System Grids 3.32 Currently, the cheque truncation system (CTS) architecture comprises of three regional grids – northern, southern and western. Each grid provides clearing services to banks under its respective jurisdiction. The Payments Vision 202529 envisages migration from the current architecture of the three regional grids to a National Grid for CTS. This is expected to improve cost effectiveness and make the related operations simpler for banks and also provide the benefit of CTS clearing for outstation cheques. As a first step, single settlement for three CTS grids has been put in place from March 1, 2023. This has enhanced liquidity efficiency of the CTS and reduced the risk of default by participants. III.3.9 Ringfencing India’s Payment Systems 3.33 The removal of certain banks from the international card schemes and financial messaging networks since the onset of the Russia-Ukraine conflict has highlighted the necessity to have a robust domestic payments infrastructure to effectively manage the risks of disruption/ discontinuity of operations and dependence on international payment system operators/ service providers. The domestic card network, viz., RuPay was implemented in 2012 to ensure availability of country’s own card network with global acceptance. The Reserve Bank’s guidelines30 on mandatory storage of payments data within India are also aimed at safeguarding data and protecting customer interests. 3.34 The Indian Financial Network (INFINET), a membership-only Closed User Group (CUG) network comprising the Reserve Bank, member banks and financial institutions, is the communication backbone whereas the Structured Financial Messaging System (SFMS), the Indian standard for domestic financial messaging is the mainstay for messaging in interbank financial transactions and centralised payment systems, viz., Real Time Gross Settlement (RTGS) and National Electronics Funds Transfer (NEFT). The National Payments Corporation of India (NPCI) operated payment systems are implemented by using domestic messaging solutions with final settlement in RTGS. 3.35 For cross-border payments, India is seeking to extend/ leverage its domestic payment systems through bilateral interlinkages with other countries interested to establish such inter-linkages. The Fast Payment System interlinking between unified payments interface (UPI) and PayNow (Singapore) in February 2023 has created digital infrastructure for instant digital payments and funds transfer between the two countries. Further, quick response (QR) code based acceptance of UPI has been facilitated in Bhutan, Singapore, and United Arab Emirates for merchant payments. On similar lines, expansion of the framework of INFINET and SFMS, to provide financial messaging platform in other jurisdictions, is required to moderate the dependence on international financial messaging platforms. These initiatives could provide alternative cross-border payment channels in the countries that adopt SFMS, INFINET and interlink with India’s payment systems. Some of the targets proposed under the Payment Vision 2025 are aimed to protect the critical payment system operations while ensuring business continuity in the event of unforeseen adverse scenarios. III.3.10 Customer Protection 3.36 The number of complaints received by the Offices of the Reserve Bank of India Ombudsman (ORBIOs) under the ‘Reserve Bank – Integrated Ombudsman Scheme (RB-IOS), 2021’ indicates that the complaints relating to loans and advances, mobile/ electronic banking and credit cards constituted nearly 60 per cent of the total complaints received during Q3 and Q4 of 2022-23 (Table 3.1). Complaints relating to deposit accounts, automatic teller/ cash deposit machines and debit cards also had a large share in the number of complaints. 3.37 With increasing usage of technology for availing financial services and upward adjustment in the benchmark lending rates of banks, complaints related to loans and advances, non-adherence to the Fair Practices Code and mobile/electronic banking related issues need to be addressed swiftly and holistically by REs at their end, to further enhance consumers’ confidence in the financial system. III.3.11 Enforcement 3.38 During December 2022 - May 2023, the Reserve Bank undertook enforcement action against 122 REs (five public sector banks; two private sector banks; hundred co-operative banks; two foreign banks; one small finance bank; three regional rural banks; eight non-banking financial companies and one housing finance company) and imposed an aggregate penalty of ₹26.34 crore for non-compliance with/ contravention of statutory provisions and/ or directions issued by the Reserve Bank. III.4 Other Developments III.4.1 Deposit Insurance 3.39 The Deposit Insurance and Credit Guarantee Corporation (DICGC) extends insurance cover to depositors of all the banks operating in India. As on March 31, 2023 the number of registered insured banks was 2,026, comprising 139 commercial banks {including forty three regional rural banks (RRBs), two local area banks (LABs), six payment banks and twelve small finance banks (SFBs)} and 1,887 co-operative banks. With the present deposit insurance limit of ₹5 lakh, 98.1 per cent of the total number of deposit accounts (300 crore) and 46.3 per cent of assessable deposits (₹181.14 lakh crore) were insured (Table 3.2). 3.40 The insured deposits ratio (i.e., the ratio of insured deposits to assessable deposits) was higher for cooperative banks (64.9 per cent) followed by commercial banks (45.2 per cent) (Table 3.3). Within commercial banks, PSBs had a much higher insured deposit ratio vis-à-vis PVBs, indicating concentration of larger-sized deposits with the latter. 3.41 Deposit insurance premium received by the DICGC grew by 9.7 per cent (y-o-y) to ₹21,381 crore during 2022-23, of which the share of commercial banks was 94 per cent (Table 3.4). 3.42 The Deposit Insurance Fund (DIF) with the DICGC is primarily built out of the premia paid by insured banks, recoveries from settled claims and investment incomes, net of income tax. DIF recorded a 15.5 per cent increase during 2022-23 to reach ₹1.70 lakh crore on March 31, 2023. The reserve ratio (i.e., ratio of DIF to insured deposits) increased to 2.02 per cent from 1.81 per cent a year ago (Table 3.5). 3.43 In case of liquidated banks and banks under the Reserve Bank’s All Inclusive Directions (AIDs), the DICGC settled claims amounting to ₹751.8 crore during 2022-23. The recovery of claims increased substantially to ₹882.8 crore in 2022-23 from ₹399.0 crore in 2021-22. (Table 3.6). III.4.2 Corporate Insolvency Resolution Process (CIRP) 3.44 Since provisions relating to the CIRP came into force in December 2016, a total of 6,571 CIRPs have commenced by March 2023, of which, 4,515 CIRPs (69 per cent) have been closed (Table 3.7). Of the closed CIRPs, 21 per cent have been closed on appeal or review or settled, 19 per cent have been withdrawn, 45 per cent have ended in orders for liquidation and the remaining 15 per cent have ended in approval of resolution plans (Table 3.8). 3.45 A stakeholder-wise analysis of the CIRPs that were closed as on March 31, 2023 indicates that of the CIRPs initiated by operational creditors (OCs), 53 per cent were closed on appeal, review, settled or withdrawal (Table 3.9). Such closures accounted for 72 per cent of all such closures. 3.46 Till March 31, 2023 678 CIRPs have ended in resolution. Realisation by financial creditors (FCs) under resolution plans in comparison to liquidation value was 169 per cent, while the realisation by them was 32 per cent in comparison to their claims. Importantly, out of the 678 corporate debtors (CDs) rescued through resolution plans, 249 were either pending before the erstwhile Board for Industrial and Financial Reconstruction (BIFR) or were defunct. 3.47 45 per cent of the CIRPs which were closed yielded orders for liquidation as compared to 15 per cent ending up with a resolution plan. The remaining 40 per cent were settled. The economic value in most of these CDs has been almost completely eroded even before they were admitted into CIRP. The average value of the assets of these CDs was nearly 7 per cent of the outstanding debt amount. (Table 3.10). 3.48 The primary objective of the Insolvency and Bankruptcy Code (IBC), 2016 (the Code) is to provide relief to CDs in distress. The Code has rescued 678 CDs till March 2023 through resolution plans, one third of which were in deep distress. Further, it has referred 2,030 CDs for liquidation, three-fourth of which were sick or defunct. The rescued CDs had assets valued at ₹1.69 lakh crore, while the CDs referred for liquidation had assets valued at ₹0.64 lakh crore, when they were admitted to the CIRP. Thus, in value terms, more than 72 per cent of distressed assets were rescued. Till March 31, 2023, 25,107 applications for initiation of CIRPs of CDs having underlying default of ₹8.81 lakh crore were disposed of before their admission into CIRP. 3.49 The realisable value of the assets available with the 678 rescued CDs when they entered the CIRP was only ₹1.69 lakh crore, though they owed ₹8.95 lakh crore to creditors. The resolution plans realised ₹2.85 lakh crore, which is 68 per cent more than the liquidation value of these CDs (i.e., the creditors recovered 168 per cent of the realisable value of the CDs’ assets, whereas under other recovery option or liquidation, they would have recovered at best the realisable value of assets less minus the cost of recovery/liquidation; the additional recovery can be considered as a bonus from the IBC process). Though realisation is incidental under the Code, financial creditors recovered 34.3 per cent of their claims which only reflects the extent of value erosion by the time the CDs entered CIRP. Nevertheless, it is the highest among all options available to creditors for recovery. On an average, resolution plans are yielding around 84 per cent of fair value of the CDs. These realisations are exclusive of realisations that would arise from value of equity holdings post-resolution, resolution of personal guarantors to CDs and from disposal of applications for avoidance transactions. 3.50 The 2,030 CDs, which ended up with orders for liquidation, had an aggregate claim of ₹9.20 lakh crore and their ground assets valued were at only ₹0.64 lakh crore. Till March 2023, 520 CDs, which have been completely liquidated, had total claims of ₹1.18 lakh crore, but their assets were valued at ₹5,168 crore. Nearly ₹4,638 crore were realised through liquidation of these companies. The Code endeavours to close the various processes at the earliest and prescribes timelines for some of them. The 678 CIRPs, which have yielded resolution plans by the end of March 2023, took an average 512 days {after excluding the time excluded by the adjudicating authority (AA)} for conclusion of the process. Similarly, the 2,030 CIRPs, which ended up in orders for liquidation, took an average 456 days for conclusion. 520 liquidation processes, which were closed by submission of final reports, took an average of 531 days for closure. Similarly, 1,024 voluntary liquidation processes, which have been closed by submission of final reports, took an average of 411 days for closure. III.4.3 Cybersecurity Risks and their potential impact on Financial Stability 3.51 Rising dependence on technology for financial services has increased the potential threat from cybersecurity risks to the financial sector. Financial entities’ response to cyberattacks may not be effective, resulting in long duration of non-availability of systems, thereby affecting the ability of the NBFC to service its customers for a long period. Given the evolving nature of cyber risks and interconnectedness of the financial sector entities, cyber security incidents in NBFCs and UCBs could also make a dent on the trust of customers. Data leakage can give rise to concerns on protection of financial data, where remediation measures become challenging if the cause remains unidentified. 3.52 As regards cyber frauds on customers, the Reserve Bank has issued guidelines for further strengthening of banks’ IT systems (e.g., Master Direction on Digital Payment Security Controls, 2021) and implementing robust fraud prevention and detection measures, including monitoring of transactions and customer behaviour, to detect and prevent instances of fund losses through cyber frauds. 3.53 Some of the initiatives undertaken by the SEBI to tackle cyber risks in the securities market include monitoring the vulnerability assessment and penetration testing (VAPT) by the regulated entities, conduct of VAPT and cyber audits of REs by the SEBI, deployment of cyber incidents reporting portal, issuance of frameworks for adoption of cloud services, cyber security and cyber resilience, active participation in Cyber Swachhta Kendra (Botnet Cleaning and Malware Analysis Centre) of the Government of India and conduct of quarterly cyber security table top exercise in collaboration with Indian Computer Emergency Response Team (CERT-IN). III.4.4 Developments in International Financial Services Centres (IFSC) 3.54 The International Financial Services Centres Authority (IFSCA) has brought in an internationally aligned regulatory regime for, inter alia, banking, capital markets, fund management, insurance, bullion exchange, fintech, aircraft and ship leasing. The GIFT-IFSC has been witnessing strong growth momentum, with the international and domestic financial services industry gravitating to this jurisdiction which is treated as a non-resident zone under the Foreign Exchange Management Regulations. The total banking asset size of IFSC banking units (IBU) stood at US$ 38 billion. The cumulative banking transactions undertaken by IBUs crossed US$ 422.6 billion till March 2023. Additionally, the cumulative OTC derivatives transactions including non-deliverable forwards (NDFs) crossed US$ 535 billion. 3.55 The IFSCA banking regulations were amended, which allowed a global administrative office (GAO) to be setup in IFSC. The GAO can undertake activities such as management, administration, coordination as well as support services from IFSC without the need of opening a banking unit. 3.56 The IFSCA (Finance Company) Regulations have enabled specific activities in the IFSC which include undertaking leasing of aircrafts, ships, and other equipment notified by IFSCA, setting up of Global and Regional Treasury Centers and International Trade Finance Services Platform (ITFS). As of March 2023, 21 Aircraft Lessors are registered as Finance Company. ITFS platform is first of its kind of international platform which would connect entities across the globe with the advantage of enabling price discovery through transparent auction process and funds from financiers across the globe. There are four entities registered as Finance Company within IFSC for the purpose of operating ITFS platforms. 3.57 The capital market ecosystem in GIFT-IFSC comprises two international stock exchanges offering 20+ hours of trading in various product categories including index, stock, currency, and commodity derivatives. The average daily turnover on the stock exchanges stood at US$ 29.5 billion (notional value) during March 2023 and the cumulative debt listed at GIFT-IFSC stock exchanges as on March 31, 2023 was US$ 50.65 billion, including US$ 9.25 billion of debt listing related to environment, social and governance (ESG) bonds. 3.58 As on March 31, 2023 four entities had been registered by IFSCA as a bullion trading member (Bullion TM), five as bullion trading and clearing member (Bullion TMCM), two as bullion professional clearing member (Bullion PCM) and one as bullion trading member cum self-clearing member. Further, 84 ‘Qualified Jewellers’ had been notified by IFSCA till March 31, 2023. The asset management ecosystem is growing rapidly and consists of 60 fund management entities and 50 funds with US$ 12.6 billion of committed investment, eight portfolio managers and six investment advisors as on March 31, 2023. Currently, the insurance ecosystem in the IFSC comprises of 23 entities, including six IFSC Insurance Offices (IIOs) and 17 IFSC Insurance Intermediary Offices (IIIOs). Under the IFSCA fintech entity framework, 22 entities have been issued limited use authorisation (sandbox) and four entities have been issued authorisation as on March 31, 2023. III.4.5 Climate Change Initiatives by SEBI 3.59 SEBI had mandated ESG related disclosures for the top 100 listed entities (by market capitalisation) since 2012 (later extended to top 1,000 entities) as per the business responsibility report (BRR) which was replaced with the business responsibility and sustainability report (BRSR) in 2021. BRSR disclosures include environment risks, environment related disclosures {viz., greenhouse gas (GHG) emissions, air pollutant emissions, energy consumption, biodiversity, waste generated and waste management practices}. BRSR allows cross-referencing of disclosures made on internationally accepted reporting frameworks through inter-operability of reporting. 3.60 The SEBI has also introduced BRSR Core which is intended to enhance the reliability of ESG disclosures and will be applicable to the top 150 listed entities (by market capitalisation) from 2023- 24 and gradually extended to the top 1,000 listed entities by 2026-27. 3.61 In 2017, the SEBI had introduced the concept of “green debt securities” to address increasing demand for sustainable finance. The framework was revised after extensive public consultation and inclusion of views from international bodies {viz., the International Capital Market Association (ICMA) the Climate Bond Initiative and the London Stock Exchange} by aligning it with the green bond principles (GBPs) of the ICMA, which are recognised by IOSCO. The framework also introduced the concepts of (a) blue bonds (related to water management and marine sector); (b) yellow bonds (related to solar energy); and (c) transition bonds (for entities moving from carbon intensive to carbon neutral projects), as subcategories of green debt securities. 3.62 Transition bonds provide funding for migrating to a more sustainable form of operations in line with India’s Intended Nationally Determined Contributions (INDCs). The SEBI has given guidelines to avoid the occurrence of greenwashing which prescribe that an issuer shall utilise the funds only for the purposes for which funds were raised, issuers shall not cherry pick data while making disclosures and issuers shall not use any misleading labels. III.4.6 Insurance 3.63 The Indian insurance industry, encompassing both life and general (including health) insurance, has registered a compound annual growth rate of 10.3 per cent during the last 10 years. The total premium income for life insurance industry has consistently increased over the years. Factors such as increasing disposable income, rising awareness on the need for insurance and evolving customer preferences have contributed to the industry’s growth. During 2022-23, the total premium income of life insurers registered a robust growth of 12.8 per cent amounting to ₹7.81 lakh crore (provisional) from ₹6.93 lakh crore in 2021-22. 3.64 During 2022-23, the total premium underwritten by general and health insurers at ₹2.57 lakh crore (provisional) recorded a robust growth of 16.4 per cent. Amongst the segments of general insurance business, the health insurance segment grew by 23 per cent followed by motor insurance with 15 per cent. 3.65 The Insurance Regulatory and Development Authority of India (IRDAI) has shifted its focus towards ensuring “Insurance for all by 2047” by making insurance more accessible, affordable, and customised, thereby enhancing the overall insurance penetration in the country. To promote ease of doing business and reduction in compliance burden, the IRDAI has brought in a number of reforms which include, inter alia, (a) extending ‘Use and File’ procedure for all the health and general insurance products and most of the life insurance products; (b) simplifying the process of registration of insurance companies, raising investment threshold for individual investors and specifying indicative criteria for determination of ‘Fit and proper’ status of investors and promoters; (c) increasing the period for considering state/ central government dues for calculation of solvency margin and reduction of solvency factor related to crop insurance; (d) revising factor for calculation of solvency for Unit Linked Business (without guarantees) and Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY); (e) increasing the roles and responsibilities of Appointed Actuaries; (f) increasing the threshold for companies to raise other forms of capital (viz., subordinated debt and/or preference shares); (g) increasing the experimentation period of regulatory sandbox to test innovative products; (h) increasing the maximum limit of tie-ups for corporate agents and insurance marketing firms with insurers; (i) revamping the guidelines for cross-border reinsurers; and (j) revising expenses of management (EoM) and commission limits for insurers. III.4.7 Pension Funds 3.66 The number of subscribers under the National Pension System (NPS) and the Atal Pension Yojana (APY) increased by 21.6 per cent (y-o-y) during 2022- 23, whereas the assets under management (AUM) recorded 22.0 per cent growth (Chart 3.1 and 3.2). NPS and APY have both continued to progress in terms of the total number of subscribers and AUM. The number of subscribers under NPS and APY altogether has reached 6.32 crore and AUM touched ₹8.98 lakh crore as at end-March 2023. 3.67 APY enrolled more than 1.19 crore new subscribers during 2022-23 as compared to 99 lakhs in the previous year. The scheme has 4.59 crore subscribers with an AUM of ₹0.27 lakh crore as on March 31, 2023. The total enrolments under APY crossed the 5.20 crore mark. Out of the total enrolments during the latest year, around 45 per cent were female. Also, 45 per cent of the total subscribers were between the age of 18-25 years. Summary and Outlook 3.68 The recent banking turmoil has reaffirmed the importance of prudent regulatory standards, strong supervision and sound corporate governance and risk management practices by financial institutions for the stability of the financial system. In addition to banking system stability, international regulatory efforts are focused on addressing existing and emerging vulnerabilities such as high levels of debt, liquidity and leverage issues in NBFIs, climate change, disruptive innovations like crypto-assets and DeFi, cyber threats and financial fragmentation.   3.69 Domestic regulatory initiatives continue to focus on improving efficiency and resilience of the financial system through sound regulatory practices and strong supervision. Improving access to finance, reducing regulatory costs, promoting responsible innovation and deepening financial markets remain key regulatory priorities. Regulators remain alert to evolving changes in the regulatory landscape. Through robust regulation, supervision and surveillance, they aim to safeguard financial stability and support economic growth. 1 FSB (2023), “FSB Chair’s letter to G20 Finance Ministers and Central Bank Governors”, April. 2 Federal Reserve (2023), “Review of the Federal Reserve’s Supervision and Regulation of Silicon Valley Bank”, April. 3 FDIC (2023), “Options for Deposit Insurance Reform”, May. 4 ESRB (2023), “Stabilising financial markets: lending and market making as a last resort”, January. 5 CGFS/ BIS (2023), “Central bank asset purchases in response to the Covid-19 crisis”, March. 6 FSB (2023). “The financial stability aspects of commodities markets”, February. 7 IOSCO (2023), “Principles for the Regulation and Supervision of Commodity Derivatives Markets”, January. 8 FSB (2023), “The financial stability risks of Decentralised Finance”, February. 9 EU (2023), “Regulations on markets in crypto-assets (MICA)”, May. 10 ‘crypto-asset’ means a digital representation of value or rights which may be transferred and stored electronically, using distributed ledger technology or similar technology. 11 ‘asset-referenced token’ means a type of crypto-asset that purports to maintain a stable value by referring to the value of several fiat currencies that are legal tender, one or several commodities or one or several crypto-assets, or a combination of such assets. 12 ‘electronic money token’ or ‘e-money token’ means a type of crypto-asset the main purpose of which is to be used as a means of exchange and that purports to maintain a stable value by referring to the value of a fiat currency that is legal tender. 13 ‘utility token’ means a type of crypto-asset which is intended to provide digital access to a good or service, available on DLT, and is only accepted by the issuer of that token. 14 Garratt, Rodney, and Shin, Hyun Song (2023), “Stablecoins versus tokenised deposits: Implications for the singleness of money”, BIS Bulletin No 73, April. 15 IMF (2021), “Global Financial Stability Report”, October. 16 IMF (2022), “FinTech Note – Capital Flow Management Measures in the Digital Age: Challenges of Crypto-Assets”, May. 17 IMF (2021), “Global Financial Stability Report”, October. 18 As on June 26, 2023 (https://www.coingecko.com/en/categories/stablecoins). 19 Aquilina, Matteo, Frost, Jon and Schrimpf, Andreas (2023), “Addressing the risks in Crypto: Laying out the options”, BIS Bulletin No 66, January. 20 ESRB (2023), “Advancing macroprudential tools for cyber resilience”, February. 21 FSB (2023), “Recommendations to achieve greater convergence in cyber incident reporting”, April. 22 “Green deposit” would be interest-bearing deposit, received by the RE for a fixed period and the proceeds of which are earmarked for being allocated towards green finance. 23 “Greenwashing” means the practice of marketing products/services as green, when in fact they do not meet requirements to be defined as green activities/projects. 24 Interest rate risk in banking book (IRRBB) refers to the current or prospective risk to banks’ capital and earnings arising from adverse movements in interest rates that affect its banking book positions. 25 These directions are not applicable to foreign banks [operating either through branch mode or Wholly Owned Subsidiary (WOS) mode]. 26 Shall be computed assuming that all the instruments (including convertible instruments) issued/to be issued to the person have been converted into shares (with applicable voting rights) and deemed to be included in the paid-up share capital or total voting rights of the banking company. 27 Major shareholders include promoter(s) with major shareholding. 28 Read with FAQs issued on June 20, 2023. 29 RBI (2022), “Payments Vision 2025 - Department of Payment and Settlement Systems”, June. 30 Press Release – “Storage of Payment System Data” - RBI/2017-18/153 - DPSS.CO.OD No.2785/06.08.005/2017-2018. |

ಭಾರತೀಯ ರಿಸರ್ವ್ ಬ್ಯಾಂಕ್ ಮೊಬೈಲ್ ಅಪ್ಲಿಕೇಶನ್ ಅನ್ನು ಇನ್ಸ್ಟಾಲ್ ಮಾಡಿ ಮತ್ತು ಇತ್ತೀಚಿನ ಸುದ್ದಿಗಳಿಗೆ ತ್ವರಿತ ಅಕ್ಸೆಸ್ ಪಡೆಯಿರಿ!

ನಮ್ಮ ಅಪ್ಲಿಕೇಶನ್ ಅನ್ನು ಸ್ಥಾಪಿಸಲು QR ಕೋಡ್ ಅನ್ನು ಸ್ಕ್ಯಾನ್ ಮಾಡಿ

ಪೇಜ್ ಕೊನೆಯದಾಗಿ ಅಪ್ಡೇಟ್ ಆದ ದಿನಾಂಕ: