IST,

IST,

Minutes of the Monetary Policy Committee Meeting, October 7 to 9, 2024

|

[Under Section 45ZL of the Reserve Bank of India Act, 1934] The fifty first meeting of the Monetary Policy Committee (MPC), constituted under Section 45ZB of the Reserve Bank of India Act, 1934, was held during October 7 to 9, 2024. 2. The meeting was attended by all the members – Dr. Nagesh Kumar, Director and Chief Executive, Institute for Studies in Industrial Development, New Delhi; Shri Saugata Bhattacharya, Economist, Mumbai; Professor Ram Singh, Director, Delhi School of Economics, Delhi; Dr. Rajiv Ranjan, Executive Director (the officer of the Reserve Bank nominated by the Central Board under Section 45ZB(2)(c) of the Reserve Bank of India Act, 1934); Dr. Michael Debabrata Patra, Deputy Governor in charge of monetary policy – and was chaired by Shri Shaktikanta Das, Governor. 3. According to Section 45ZL of the Reserve Bank of India Act, 1934, the Reserve Bank shall publish, on the fourteenth day after every meeting of the Monetary Policy Committee, the minutes of the proceedings of the meeting which shall include the following, namely:

4. The MPC reviewed the surveys conducted by the Reserve Bank to gauge consumer confidence, households’ inflation expectations, corporate sector performance, credit conditions, the outlook for the industrial, services and infrastructure sectors, and the projections of professional forecasters. The MPC also reviewed in detail the staff’s macroeconomic projections, and alternative scenarios around various risks to the outlook. Drawing on the above and after extensive discussions on the stance of monetary policy, the MPC adopted the resolution that is set out below. Resolution 5. After assessing the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (October 9, 2024) decided to:

Consequently, the standing deposit facility (SDF) rate remains unchanged at 6.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 6.75 per cent.

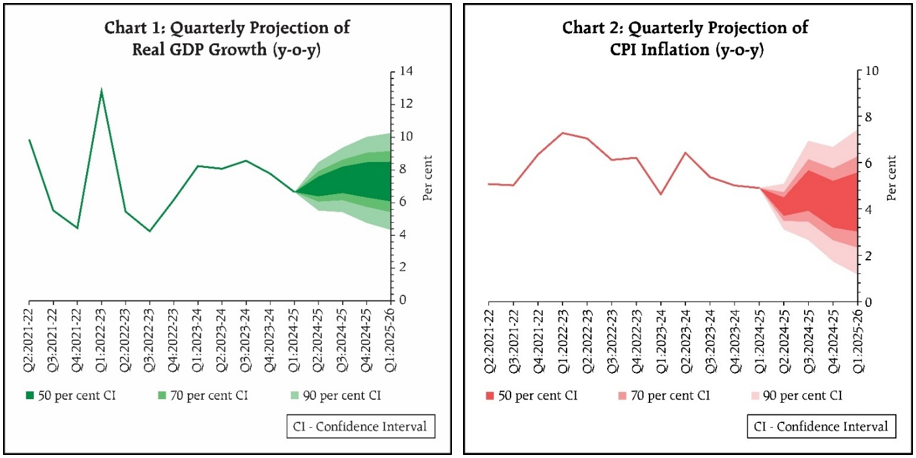

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. Growth and Inflation Outlook 6. The global economy has remained resilient and is expected to maintain stable momentum over the rest of the year, amidst downside risks from intensifying geopolitical conflicts. In India, real gross domestic product (GDP) registered a growth of 6.7 per cent in Q1:2024-25, driven by private consumption and investment. Looking ahead, the agriculture sector is expected to perform well on the back of above normal rainfall and robust reservoir levels, while manufacturing and services activities remain steady. On the demand side, healthy kharif sowing, coupled with sustained momentum in consumer spending in the festival season, augur well for private consumption. Consumer and business confidence have improved. The investment outlook is supported by resilient non-food bank credit growth, elevated capacity utilisation, healthy balance sheets of banks and corporates, and the government’s continued thrust on infrastructure spending. External demand is expected to get support from improving global trade volumes. Taking all these factors into consideration, real GDP growth for 2024-25 is projected at 7.2 per cent with Q2 at 7.0 per cent; Q3 at 7.4 per cent; and Q4 at 7.4 per cent. Real GDP growth for Q1:2025-26 is projected at 7.3 per cent (Chart 1). The risks are evenly balanced. 7. Headline inflation declined sharply to 3.6 and 3.7 per cent in July and August respectively from 5.1 per cent in June. Going forward, the September inflation print may see a significant pick-up as base effects turn adverse and food prices register an upturn. Food inflation, however, is expected to ease by Q4:2024-25 on better kharif arrivals and rising prospects of a good rabi season. Sowing of key kharif crops are higher than last year and the long-period average. Sufficient buffer stocks for cereals are available for ensuring food security. Adequate reservoir levels, the likelihood of a good winter and favorable soil moisture conditions augur well for the ensuing rabi season, though adverse weather events remain a risk. Firms polled in the Reserve Bank enterprise surveys expect input cost pressures to ease; however, the very recent upturn in key commodity prices, especially metals and crude oil needs to be closely monitored. Taking all these factors into consideration, CPI inflation for 2024-25 is projected at 4.5 per cent with Q2 at 4.1 per cent; Q3 at 4.8 per cent; and Q4 at 4.2 per cent. CPI inflation for Q1:2025-26 is projected at 4.3 per cent (Chart 2). The risks are evenly balanced. Rationale for Monetary Policy Decisions 8. The MPC noted that the domestic growth outlook remains resilient supported by domestic drivers – private consumption and investment. This provides headroom for monetary policy to focus on the goal of attaining a durable alignment of inflation with the target. The MPC reiterates that enduring price stability strengthens the foundations of a sustained period of high growth. After a transient spike in the near term, headline inflation is expected to moderate as projected above. With better prospects for both kharif and rabi crops and ample buffer stocks of foodgrains, there is now greater confidence on the disinflation path later in the financial year. Keeping in view the prevailing and expected inflation-growth dynamics, which are well balanced, the MPC decided to change the monetary policy stance from withdrawal of accommodation to ‘neutral’ and remain unambiguously focused on a durable alignment of inflation with the target, while supporting growth. The change in stance provides flexibility to the MPC while enabling it to monitor the progress on disinflation which is still incomplete. Risks stem from uncertainties relating to heightened global geo-political risks, financial market volatility, adverse weather events and the recent uptick in global food and metal prices. Hence, the MPC has to remain vigilant of the evolving inflation outlook. Accordingly, the MPC decided to keep the policy repo rate unchanged at 6.50 per cent in this meeting. 9. Shri Saugata Bhattacharya, Professor Ram Singh, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to keep the policy repo rate unchanged at 6.50 per cent. Dr. Nagesh Kumar voted to reduce the policy repo rate by 25 basis points. 10. Dr. Nagesh Kumar, Shri Saugata Bhattacharya, Professor Ram Singh, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted for a change in stance from withdrawal of accommodation to ‘neutral’ and to remain unambiguously focused on a durable alignment of inflation with the target, while supporting growth. 11. The minutes of the MPC’s meeting will be published on October 23, 2024. 12. The next meeting of the MPC is scheduled during December 4 to 6, 2024.

Voting on the Resolution to keep the policy repo rate unchanged at 6.50 per cent

Statement by Dr. Nagesh Kumar 13. At the outset, I must say, that looking at the global economic situation, one feels proud of the management of the Indian economy that has made it the fastest-growing large economy globally, with a relatively low inflation rate, exchange rate stability, large foreign exchange reserves, among other robust macroeconomic fundamentals. The effective monetary management by the RBI combined with the prudent fiscal management by the Finance Ministry over the years deserve to be applauded. 14. Within the broad overall picture, zooming in to the current juncture, however, certain pointers require consideration by the MPC. I wish to situate the discussion on the policy rates and inflation targeting in the context of the overall development priorities of the country from the perspective of the real sector, particularly the manufacturing sector. After all, the policies are the ‘means’ for achieving the ‘ends’ that are our development aspirations. 15. The job creation imperative for India’s youthful population has pushed the Government to focus attention on the manufacturing sector which has the potential to create decent jobs not only directly but also indirectly, especially for semi-skilled and unskilled workers. Several reforms and policy measures such as PLI have been taken over the past decade as a part of the ‘Make-in-India’. India is not alone in pushing the manufacturing sector. The US, until recently the greatest champion of free markets, for instance, is pushing industrial policy aggressively with a trinity of the Inflation Reduction Act, the CHIPS and the Science Act, and the Infrastructure Investment and Jobs Act adopted in 2022 which have collectively put more than a trillion dollars on the table to be handed out to industry in incentives and tax breaks, besides heavy tariffs imposed on the imports from China to protect the domestic industry. The EU is following the same playbook. 16. The external context for pursuing industrial policy, however, has turned less benign compared to the 1990s and early part of the 2000s when China’s industrial policy was supported by rapidly expanding world trade and investments. World trade and investments have never quite recovered from the global financial crisis and their growth rates have come down dramatically from an annual average of over 16% to under 4% for world trade and from around 20% to just 2% for FDI between the pre-and post-GFC periods. The rise of protectionism in the West, trade wars, and the collapse of multilateral trade negotiations have turned globalization into ‘slowbalization.’ The situation is complicated further, especially for India, by large excess industrial capacities sitting next door in China, with access to the Western markets made more difficult, and the threat of predatory dumping in our markets is real. 17. The disruptions during the pandemic have sparked a trend of global companies derisking their supply chains by restructuring them on a China+1 basis. This trend of restructuring of supply chains by global companies could be an opportunity for India to attract investments to build our productive capacities if we can get our act together in terms of investment climate, efficient logistics, stable macroeconomic environment, cost of capital, and overall cost of doing business vis-a-vis peer countries. To some extent, India’s success in attracting Apple and its vendors like Foxconn to assemble iPhones in India is a part of this trend. 18. The emerging trends in the Indian economy suggest a slowdown of the economic growth from 8.2% in 2023-24 to 6.7% in 2024-25:Q1 and the projection for the full year 2024-25, according to the Survey of Professional Forecasters, has been revised down by 10 basis points to 6.9%. The core sectors such as cement, iron & steel, and chemicals showing negative growth over the past two quarters despite a rather heavy infrastructure push by the government through unprecedented capital expenditure since 2023-24 is a matter of concern. The cost of finance of private companies has gone up steadily since March 2022 when the RBI started to raise the policy rates. According to the Enterprise Surveys, the demand conditions in manufacturing and the job landscape moderated across major sectors. The Consumer Confidence Surveys suggest that the general economic conditions have worsened compared to a year ago. Overall business sentiment has moderated in 2024-25:Q2. PMI for manufacturing eased somewhat in September although stayed in the expansionary zone. All these trends point to the weaknesses in demand in the domestic economy in general, and industry in particular. Similarly, India’s merchandise exports have shrunk by 9.3% in August due to subdued demand abroad. The April-August growth of merchandize exports has been just a marginal 1.1% only. 19. Therefore, the Indian industry is clearly suffering from demand deficits in both domestic and external markets. Demand deficits may be the reason private investment has not picked up momentum despite the companies' healthy balance sheets and all the reforms and incentives extended by the government. 20. The inflationary trends, on the other hand, suggest that the monetary policy interventions of RBI have had greater success in managing inflation. The CPI headline has been around 4.5%, and was slightly lower at 3.6% in July-August 2024. The inflation excluding vegetables is even lower at 3.2% (July-August). Food inflation especially cereals and vegetables has been challenging but it is driven by cyclical supply side issues rather than demand which is addressed by monetary policy. Household inflationary expectations/ perceptions have declined by 10 basis points. A lower proportion of households expect prices and inflation to increase over 3 or 12 months ahead. Therefore, it is apparent that the policy tightening by the RBI has succeeded in anchoring inflationary expectations well. 21. Furthermore, several industrialized and emerging economies have started to cut interest rates to revive economic growth. In the US, the Fed has cut the policy rate by 50 basis points. The EU, Switzerland, Mexico, China, and South Africa have begun to normalize monetary policy by cutting rates. India risks currency appreciation if we do not follow the process of normalization. The rupee has been already appreciating in real terms and a further appreciation would hurt the competitiveness of Indian products. 22. Given that inflationary expectations have been successfully anchored, and industrial demand in both domestic as well as export markets is flagging, a rate cut could help to revive demand and help boost private investment. I believe that it is an opportune moment for RBI to start the process of normalizing the monetary policy. In view of these observations, I vote for a 25 basis point cut in the repo rate and the adoption of a neutral stance in the monetary policy. Statement by Shri Saugata Bhattacharya 23. Global growth, while resilient, remains uneven, slowing in many large economies, prompting central banks to start cutting policy rates. Prospects for future demand remain hazy, with each emerging data point seeming to present a confusing and occasionally dissonant outlook. The forthcoming IMF World Economic Outlook is awaited for forecast updates. Future G-7 central banks’ rate actions and guidance, other than affecting economic activity, are likely to induce financial markets volatility, with expected spillovers to emerging markets. 24. In India, signals on growth momentum present a mixed picture, with uncertainty regarding aggregate demand. RBI projects a 7.2% real GDP growth for FY25. Forecasts of many institutional and multilateral organisations seem to be progressively converging closer to this. 25. In the near term, however, some high frequency economic indicators (both hard data and surveys) suggest a loss of momentum, but still do not seem to show a material slowdown. The Manufacturing and Services Purchasing Managers Indices (PMIs) for September, and the IIM Ahmedabad August Business Expectations Survey show a moderation in current and expected activity metrics. Lower cement and steel growth are a concern, but might partially reflect the base effects of very high growth rates in the corresponding months in FY24. Domestic IT hiring is reported to have slowed. The much-discussed slowdown in Personal Vehicles (PV) retail sales, with reported large inventory stocks at dealers, is a concern. The last reported prints for rural wages remain subdued. Tepid export growth is worrisome, accentuated by reports of China “dumping” excess capacity. 26. A contrarian viewpoint is equally compelling. RBI surveys show increasing consumer confidence, Two-wheeler sales are doing well, particularly in rural areas. Tailwinds from the largely good rains are likely to bolster rural demand. Steel consumption recorded double digit year on year growth during April – August 20241 . The automobile dealerships’ industry body notes that expectations of higher PV sales in October have improved. Manufacturing Capacity Utilisation (CU), seasonally adjusted, had inched up in Q1 FY25, auguring well for private sector investment. A study on banks’ capex sanctions and disbursements in FY24 reinforces this2 . Although dated, RBI collation of non-financial private listed corporate Q1 FY25 results show that high interest rates have not hurt corporate financials to any significant extent; interest costs as a share of sales were actually creeping lower (2.7% in Q1 FY25). Retail credit, conjectured (albeit untested) to be a driver of consumption demand, while slowing, still remains robust. Weighing these metrics, we assess that domestic growth outlook remains largely resilient, even as we recognise the need to closely monitor developments in near term economic indicators. 27. Inflation, on the other hand, appears to be more stable now. Persistent high food inflation might gradually trend down, given the relatively good distribution of above average rains and higher acreage sown. High reservoir levels and ground moisture augur well for rabi crops. Excluding vegetables, CPI inflation has remained below 4% for the past 8 months. All synthetic measures of core inflation have remained stable despite persistent and overlapping food price shocks. Diffusion indices of price dispersion for CPI Core also indicated a seasonally adjusted annualised rate (saar) price momentum of less than 4 to 6 per cent3 . Yet, the September CPI inflation is likely to be significantly higher than in the last couple of months. Although we expect this likely rise to be transitory over a couple of months, we need to closely monitor trends in commodities prices. The arduous battle against inflation is far from won, but we are more confident of eventual success in bringing CPI inflation durably closer to the target. One important reason for this confidence is that household inflation expectations remain well anchored and have trended lower in the latest survey round. 28. Yet, risks on commodities inflation seem to be building up. The FAO Food Price Index (FFPI) was up 2.1% yoy in September ‘24. Geopolitical risks have risen sharply. Most metals prices had hitherto remained moderate, largely due to the China slowdown, but now some metals prices, particularly aluminium, are trending up. The magnitude and contours of China’s ongoing stimulus and their impact on Chinese demand still remain unclear. A study which had estimated India’s potential output growth at 7% for January-March 20244 reinforces the heightened risks of premature easing. 29. Given this assessment, risks to the near-term growth – inflation trade-off at this point in time seem largely balanced, even as inflation is projected to be trending towards the target and is eventually likely to durably align with it. The effects of the current uncertainty on the evolving and fluid economic conditions need to be understood in greater detail in order to guide policy actions at this inflexion point. However, the extent of ambiguity emanating from economic signals warrants a need for policy to be able to respond readily to evolving economic conditions, based on incoming data. The first step is to change the policy stance to neutral, providing flexibility and optionality for future actions. 30. It needs to be emphasized, given the current heightened uncertainty, both global and domestic, that a very cautious and calibrated approach to easing is called for; the costs of a “policy error” are likely to be large. The multi-dimensional implications of a repo rate cut at this time and in the future needs careful evaluation. One of these might be a further and excessive easing of financial conditions; these conditions, to an extent, have already in the recent past resulted in a de facto easing of restrictive policy. In addition, structural system liquidity has shifted over time from deficit to surplus, helping to anchor overnight and short-term rates close to the repo rate. Updates inter alia on the ongoing festive season sales and the results of listed private sector corporates for the July-September quarter of FY25 might provide more clarity on evolving demand conditions. 31. Accordingly, based on my assessment of the appropriate response to this complex economic environment, I vote for a change of the monetary policy stance to neutral while keeping the repo rate unchanged at 6.5 per cent. Statement by Prof Ram Singh Domestic Growth 32. The macroeconomic data and indicators available so far suggest that domestic economic activity remains steady. The real GDP has grown by 6.7 per cent in Q1:2024-25, a tad less than the projected value for the quarter. The GVA, on the other hand, expanded by 6.8 per cent in Q1 of 2024-25, higher than 6.3 per cent in the previous quarter. The core of production, i.e., manufacturing and services, grew by 7.0 per cent and 7.7 per cent, respectively, and drove the growth of GVA primarily in Q1. The data also suggest that a revival in private consumption and improvement in private investment has driven the growth in the first quarter. The GFCF has stood at 7.5 per cent in Q1:2024-25. It is also noteworthy that the investment as a share of the GDP has reached 34.8 per cent – the highest since Q2:2012-13. 33. The agriculture and services sectors remain resilient. Better kharif sowing owing to the above-normal monsoon rainfall is expected to help sustain the growth path. The improved reservoir levels and soil moisture conditions also augur well for the ensuing rabi crop. The services sector has continued to grow at a steady pace. PMI services at 57.7 in September indicate robust expansion though the pace slackened to a 10-month low in September as demand slowed. 34. The eight core industries' output fell by 1.8 per cent in August on an adverse base. Excess rainfall also dampened production in some sectors, such as electricity, coal and cement, in August. This comes in the backdrop of a tapering trend in the PMI over the last few months. However, PMI remains in expansion territory with a comfortable margin, and India has continued to record the highest PMI reading among major economies for manufacturing and services since July 2022 and April 2023, respectively. Also, the industrial outlook survey of manufacturing firms suggests improved expectations for production, order books, employment, capacity utilisation, and overall business situation during Q4:2024-25 and Q1:2025-26. Moreover, improving domestic demand with lower commodities and other input costs is conducive to the sustainability of manufacturing activities. On the external front, recent merchandise exports have contracted, but services exports support overall growth. 35. Regarding demand, PFCE growth has shown a moderate but consistent upward trajectory. It accelerated to a seven-quarter high of 7.4 per cent in Q1:2024-25. Rural demand is trending upwards, as manifested by several vital indicators: sales of two-wheelers during July-August 2024, a 16.6 per cent decline in demand for the MGNREGA work during July-September, and a higher growth of FMCG in rural areas. The sale of consumer durables and air traffic manifests a sustained urban demand. 36. Investment also remains buoyant, as indicated by steel consumption, production, and imports of capital goods. The GFCE is moderately improving after a 0.2 percent contraction during Q1:2024-25. Government capex is also rebounding from the contraction observed in the first quarter due to general elections. Government expenditures of the centre and the states are expected to pick up further pace in Q3 and Q4. The government’s continued thrust on capex and healthy twin-balance sheets would help sustain business optimism. 37. An expansion in non-food bank credit for most manufacturing and infrastructure subsectors is sustaining private investment. An increase in the seasonally adjusted capacity utilisation—from 74.6 per cent in Q4:2023-24 to 75.8 per cent in Q1:2024-25—also adds to the positive outlook, as does a rise in investment intentions. A downtrend in finished goods inventory (FGI)/sales and steady raw material inventory (RMI)/sales are also a source of comfort. 38. In the rest of the fiscal year, growth will also depend on whether government spending in the remaining two quarters remains in line with the budget estimates, the growth rate for the core industries, and the growth in the flow of financial resources to the commercial sector. 39. However, fundamental growth drivers and the mainstay of aggregate demand – consumption and investment demand – are gaining momentum. The core components of aggregate demand, viz., private consumption and gross fixed capital formation, have remained strong with over 7.0 per cent growth in Q1, suggesting resilience of the growth. Further, momentum in private consumption looks sustainable on the back of improved agricultural outlook and rural demand. Sustained buoyancy in services is also expected to support urban demand. The high-frequency indicators point toward a sustained momentum in domestic economic activity. Overall, the real GDP growth for 2024-25 is projected at 7.2 per cent, which seems very much achievable. Inflation 40. The headline CPI inflation rate was below 4.0 per cent for the second consecutive month in August 2024. This is very comforting, especially given the core inflation readings remaining in the range of 3.3-3.4 per cent during this period. The fuel component of CPI remains in a contractionary phase. The RBI projected CPI inflation for 2024-25 at 4.5 per cent, with balanced risks. 41. Food inflation is an important source of uncertainty, which has increased in August from the preceding month. Moreover, there is a significant divergence within the food sub-groups. Going forward, the moderation in headline inflation can be unsteady in the near term due to adverse base effects. Food inflation is expected to moderate later this financial year because of strong kharif and rabi sowing on top of adequate buffer stocks. Adverse weather events, however, remain un-insurable risks to food inflation. 42. Considering all these factors, there is a case for remaining vigilant about food inflation and, at the same time, supporting growth. Therefore, I vote for:

Statement by Dr. Rajiv Ranjan 43. In my August 2024 statement, I had stated that we could see a window opening up for monetary policy to change its course backed by steady progress in monsoon, higher kharif sowing, favourable rabi prospects and softening global commodity prices. Today, we have more clarity and definiteness on some of these aspects, all of which may contribute positively to our disinflation path. 44. There is ample evidence now to say that monetary policy actions since May 2022 have worked well. First, inflation expectations have come down significantly since September 2022, when they had reached a peak. Since September 2022, current perception, 3-month and 1-year ahead household inflation expectations declined by 210 bps, 160 bps and 100 bps, respectively, while business inflation expectations5 have seen a decline of 104 bps over these last two years. Second, core inflation has softened from a 6 per cent level during May to September 2022 to around 3.2 per cent during the current financial year. Third, the cumulative rate hikes have percolated through the system adequately, broadly in line with the transmission observed during the easing phase. Fourth, beyond the near-term hump, inflation projections during the latter part of the financial year give us comfort with food inflation likely to benefit from strong kharif sowing, adequate buffer stocks and likely good soil moisture conditions for rabi sowing. 45. Fifth, policy rate hikes since May 2022 along with the prudential measure of increasing the risk weights for certain unsecured loan segments undertaken in November 2023 helped lower credit growth in the targeted sectors. Thus, prudential measures – whether ahead of or during a monetary tightening – complements monetary policy by providing central banks with more policy headroom to fight inflation, while helping to reduce the likelihood of financial stress6. Recent trends also indicate that credit and deposit growth gap, which has been a concern for some time, is narrowing. In absolute terms, the accretion to bank deposits has been higher than loan growth during the current financial year so far. 46. While being focussed on its task of containing inflation, monetary policy has also ensured that growth remains on a steady path. Both the major drivers of growth, consumption and investment, having more than 90 per cent share in GDP in Q1: 2024-25, continue to grow at a good pace. The confidence in the strength of domestic demand is led by the recovery in rural consumption emanating from buoyant agricultural activity which had been lagging during the previous two years. Festive season will provide further impetus to demand. It is also supported by the expected recovery in Government consumption (both central and state governments) as budgeted for 2024-25 – which is evidenced in the data available for Q2 so far. Government capex is rebounding after having contracted in Q1. It is expected to keep pace to match the budgeted amount. Private investment continues to gain traction, supported by rising capacity utilisation, strong corporate and bank balance sheets, and higher industrial credit. The improving outlook of capex is led by infrastructure, speciality chemical, EVs, pharma, solar PV module, automobile, steel and renewable energy. Global trade volumes remain strong which is good for our exports. Softer crude prices, if sustained, could be a tailwind for growth. 47. On the global front, it seems like we are in an interesting but challenging phase. First, uncertainties on the global front undoubtedly remain high, yet some resilience is getting built in. Notwithstanding the rise in geopolitical risks along with Chinese stimulus and its demand side impact, oil remains volatile within a range that is neither striking nor worrying like yesteryears. Second, countries seem to be determining their monetary policies based on indigenous factors, while remaining largely immune to the Fed policy pivots. Post the Fed rate cut in mid-September, the world is divided - while 10 countries have followed the Fed, another 11 countries have taken a pause, while one has hiked its policy rate. Such varying monetary policy responses reflect growing divergence in the inflation-growth dynamics across countries that coupled with continued uncertainties have prompted central banks across the globe to steer their policy path in a guarded manner managing the risk of policy errors. Third, those who have begun their policy pivot by rate cuts can be categorised into three types – those who face sharp slowdown in their economies (UK, EU, South Korea), those who had very restrictive policies (US, Canada, Norway and Iceland) and lastly, those who had started hiking very early in 2021 (like Brazil, Hungary, Columbia and Chile). Clearly, India does not fall in any of these categories. 48. To conclude, there are enough evidence to give confidence that we are on the right track. Our cautious and calibrated approach has paid off. Monetary policy is working well to contain inflation. Going ahead, there is now greater confidence on inflation aligning with the target unless disrupted significantly by weather events and worsening of geo-political risks. We also need to keep a close watch on global commodity prices, especially food and metal prices, which have shown some signs of hardening. Keeping in mind the balance in the growth-inflation outlook, the risk-reward for a change of stance to neutral is favourable now. This would allow flexibility to adapt and operate in accordance with the evolving situation. But change in stance in no way implies dropping the guard on inflation. Considering the uncertainties still prevailing on the global front, a cautious data dependent approach with regard to further course of monetary policy actions is called for. Between now and December, we will have greater clarity on some of the uncertainties – US elections, geopolitical risks and Chinese fiscal stimulus and its impact on global commodity prices. At this juncture, India’s resilient growth story helps us to continue our determined focus on inflation and keep the policy rate unchanged at 6.5 per cent. Hence, I vote for a status quo on rates and change of stance to neutral. Statement by Dr. Michael Debabrata Patra 49. Since the beginning of 2022-23, monetary policy has pursued a sustained restrictive stance to achieve the goals of maintaining price stability while keeping in mind the objective of growth. There is now growing evidence that as the effects of some of the global shocks that drove up inflation are fading, our commitment is bringing about a better balance between aggregate demand and aggregate supply domestically. Accordingly, the path of inflation is reconfiguring towards the target in the baseline forecast, by my metric of four quarters ahead inflation. This trajectory will likely encounter a hump in the near months as the projections indicate, but this is largely due to an adverse base and one-off shocks to prices of vegetables, edible oils and gram. The expectation is that effects of these shocks should dissipate by December as supply conditions improve. It is, therefore, possible for monetary policy to look through these spikes while monitoring their evolution closely until they are seen off. The overall inflation environment is improving. Households’ and businesses’ inflation expectations have eased and remain anchored. Consumer confidence on the price situation a year ahead is improving. Input cost pressures are expected to ease in the manufacturing sector and selling prices are expected to moderate in the services and infrastructure sectors during the third quarter of 2024-25. The decline in capacity utilisation in the manufacturing sector is highly correlated with a slackening of the output gap in the sector, which should also work toward easing core price pressures. 50. Economic activity remains resilient in spite of the disinflationary monetary policy stance, supported by domestic drivers. While some high frequency indicators have slowed in the second quarter of 2024-25, this appears attributable to idiosyncratic factors like unusually heavy rainfall in the retreat of the south west monsoon and pitrupaksha. They should stabilize in the second half of the year as consumption receives a boost in the festival season, the revival of rural demand gathers further strength, and investment is buoyed by budgeted government capital expenditure gaining steam. Enterprises expect demand conditions to pick up for manufacturing companies; services and infrastructure firms indicate an optimistic outlook on demand. Overall business expectations for the last quarter of 2024-25 and the first quarter of 2025-26 are optimistic. 51. Given this outlook, it is possible to envisage that the persistence of inflationary pressures experienced so far could dissipate with a less restrictive stance of monetary policy. This assessment gains credence with the success in squeezing out inflation persistence that has been achieved. It would be apposite in this meeting to undertake an appropriate recalibration of the monetary policy stance that reflects an openness to reducing the degree of policy restraint if inflation evolves along the trajectory set out in the baseline projection. At the same time, reducing restraint too quickly may negate the progress made on disinflation. Hence, a gradual wait-and-assess approach to removing policy restraint in terms of the policy rate remains appropriate as long as inflation is not lastingly close to its target. Accordingly, I vote for maintaining status quo on the policy rate but a shift in the stance to neutral in this meeting. Statement by Shri Shaktikanta Das 52. The global economy continues to grow at a steady pace, with trade remaining resilient. Despite its uneven progress, headline inflation is softening. Divergent growth-inflation trajectories across countries have led to varying monetary policy responses from central banks. 53. In India, high frequency indicators suggest that economic activity remained steady during Q2:2024-25. Agricultural activity has significantly picked up due to a good south-west monsoon. This will contribute to both supply and demand side factors behind GDP growth. Manufacturing companies are expected to benefit from lower input costs. Services activity retains its buoyancy. 54. The Reserve Bank surveys indicate an improvement in consumer and business sentiments. Government expenditure has improved in Q2:2024-25 and this trend is likely to continue during rest of the year in line with the budget estimates. Private corporate investment is gaining steam with seasonally adjusted capacity utilisation improving in Q1:2024-25, and healthy balance sheets of banks and corporates. The two major drivers of GDP – consumption and investment – are expected to sustain their momentum observed in Q1. Consequently, the real GDP is projected to grow at 7.2 per cent in 2024-25. Further, the Reserve Bank’s model based projection suggests that the economy will grow at 7.1 per cent during 2025-26. India’s growth story remains intact. 55. Headline CPI inflation moderated during July-August 2024, as anticipated, benefiting primarily from a favourable base effect in July. Food prices registered a decline in July-August, but high frequency food price indicators available for September indicate an upturn in food prices. Together with a large unfavourable base effect, this would in all probability lead to a substantial jump in headline inflation in September. The momentum in food prices continues even in the first week of October which, if sustained, is likely to keep even October headline inflation high. Beyond the short-term, however, the outlook for food inflation is becoming more favourable with improvement in kharif and rabi season prospects. Core inflation, in absence of a major cost-push shock, is likely to remain contained on continuing transmission of past monetary policy actions. These considerations have resulted in inflation projection of 4.5 per cent for 2024-25. 56. Overall, the Indian economy presents a picture of stability and strength. The balance between inflation and growth is well-poised. Despite the near-term uptick in inflation, the outlook for headline inflation towards the later part of the year and early next year points to further alignment with the 4 per cent target. Thus, the conditions are appropriate for a change in monetary policy stance to neutral from withdrawal of accommodation. This would provide greater flexibility and optionality to monetary policy to act in accordance with the evolving outlook. It also provides space to watch out for the uncertainties on the horizon – ranging from heightened geo-political tensions and volatile commodity prices to risks of adverse weather in food inflation. These are significant risks and their impact cannot be underestimated. We need to remain vigilant. 57. At this stage of the economic cycle, having come so far, we cannot risk another bout of inflation. The best approach now would be to remain flexible and wait for more evidence of inflation aligning durably with the target. Monetary policy can support sustainable growth only by maintaining price stability. Taking all these factors into consideration, I vote for changing the stance from withdrawal of accommodation to ‘neutral’ while keeping the policy repo rate unchanged at 6.50 per cent. (Puneet Pancholy) Press Release: 2024-2025/1359 [2] K. Gupta et al, RBI Bulletin August 2024, pp. 149-162. [4] H. K. Behera, “Updating Estimates of the Natural Rate of Interest for India with Post Pandemic Evidence”, RBI Bulletin, July 2024, pp. 77-88.

|

ഈ പേജ് ഷെയർ ചെയ്യുക:

റിസർവ് ബാങ്ക് ഓഫ് ഇന്ത്യ മൊബൈൽ ആപ്ലിക്കേഷൻ ഇൻസ്റ്റാൾ ചെയ്ത് ഏറ്റവും പുതിയ വാർത്തകളിലേക്ക് വേഗത്തിലുള്ള ആക്സസ് നേടുക!

ഞങ്ങളുടെ ആപ്പ് ഇൻസ്റ്റാൾ ചെയ്യാൻ QR കോഡ് സ്കാൻ ചെയ്യുക

പേജ് അവസാനം അപ്ഡേറ്റ് ചെയ്തത്: