IST,

IST,

Content Type:

Domestic Deposits

IV. Advances against shares and debentures

Foreign Investment in India

IV. Reporting Delays

Answer: The reporting requirements are laid down in the Master Direction on Reporting under Foreign Exchange Management Act, 1999.

Indian Currency

Updated: ഒക്ടോ 08, 2025

E) Counterfeits/Forgeries

The Reserve Bank of India has been organizing training sessions on the authentication of banknotes security features for people handling significant amounts of cash like banks/consumer forums/merchant associations/educational institutions/police professionals. Apart from the training sessions, information on security features of banknotes is also available on the Bank’s website at https://indiancurrency.rbi.org.in.

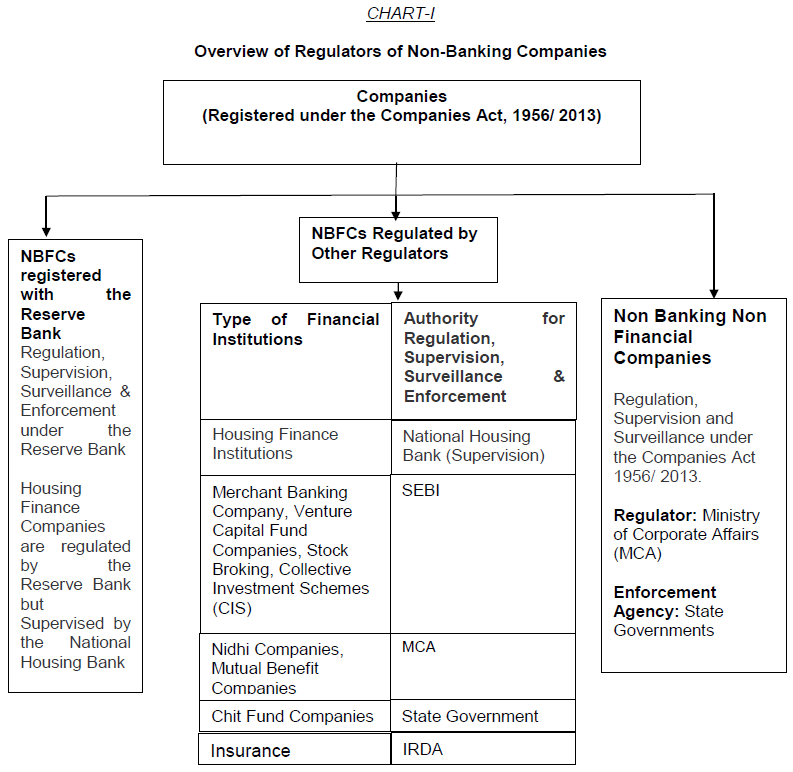

All you wanted to know about NBFCs

G. Other/ miscellaneous aspects

No, since the Company is not fulfilling the Principal Business Criteria (asset-income pattern) of an NBFC i.e. more than 50 % of its total assets should be financial assets and the income derived from these assets should be more than 50% of the gross income, it is not required to register as an NBFC under Section 45 IA of the RBI Act, 1934. However, it should register itself as an NBFC as soon as it fulfils the criteria of an NBFC and comply with the NBFC norms.

FAQs on Non-Banking Financial Companies

Repayment of matured deposits

Retail Direct Scheme

Investment and Account holdings related queries

Yes, securities can be gifted/transferred to a relative/friend/anybody who fulfills the eligibility criteria. The bonds shall be transferred in accordance with the provisions of the Government Securities Act, 2006 and Government Securities Regulations, 2007.

Domestic Deposits

IV. Advances against shares and debentures

Foreign Investment in India

IV. Reporting Delays

Indian Currency

F) COINS

Coins in India are presently being issued in denominations of 50 paise, one rupee, two rupees, five rupees, ten rupees and twenty rupees. Coins up to 50 paise are called 'small coins' and coins of Rupee one and above are called 'Rupee Coins'. Coins can be issued up to the denomination of ₹1000 under The Coinage Act, 2011.

All you wanted to know about NBFCs

G. Other/ miscellaneous aspects

FAQs on Non-Banking Financial Companies

Prudential Norms

Retail Direct Scheme

Investment and Account holdings related queries

Domestic Deposits

IV. Advances against shares and debentures

Indian Currency

F) COINS

Twenty-five (25) paise coins have been withdrawn from circulation with effect from June 30, 2011, vide gazette notification No. 2529 dated December 20, 2010, and are, therefore, no more legal tender. Coins of denominations below 25 paise were withdrawn from circulation much earlier. All other denominations of coins of various size, theme and design minted by Government of India under The Coinage Act, 2011 and issued by RBI for circulation from time to time, continue to remain legal tender.

All you wanted to know about NBFCs

G. Other/ miscellaneous aspects

The directions require assessment of income and indebtedness at household level. There is no requirement of treating all members of the household as applicants/ borrowers of a loan which can be provided to an individual member. Board-approved policies of REs may include the methodologies/ operational frameworks to assess income and indebtedness of all members of the household.

FAQs on Non-Banking Financial Companies

Prudential Norms

- Each category of quoted investments is to be valued scrip-wise. Category of investment means the different types of securities under each head viz. equity shares, preference shares, debentures, bonds and Government securities. Only quoted investments can be classified as long term or current investments. The long term investments are allowed to be valued as per AS-13 of the ICAI but the current investments are required to be valued at their market price. However, the NBFCs have been permitted under Prudential Norm Directions, the facility of block valuation method for accounting for the investments. The net of depreciation and the appreciation in the value of the current quoted investments, is only required to be charged to the Profit and Loss Account of the current year. The appreciation in the value of current investments in any category cannot be booked as profit. The concept of block valuation is explained below :

Example No. 1

Name of the scrip | Market value | Book value | Difference (+)/(-) | |

A | 200 | 150 | (+) 50 | |

B | 210 | 180 | (+) 30 | |

C | 180 | 240 | (-) 60 | |

D | 240 | 300 | (-) 60 |

Total appreciation Rs. 80/-

Total depreciation Rs. 120/-

Net depreciation Rs. 40/- to be charged to Profit and Loss | |

Account as per provisions for | |

Example No. 2

Name of the scrip | Market value | Book value | Difference (+)/(-) | |

A | 150 | 200 | (-) 50 | |

B | 180 | 210 | (-) 30 | |

C | 240 | 180 | (+) 60 | |

D | 300 | 240 | (+) 60 |

Total appreciation Rs. 120/-

Total depreciation Rs. 80/-

Net appreciation Rs. 40/- to be ignored.

This appreciation in the value of equity shares cannot be adjusted against the depreciation in the value of any other category of securities.

Retail Direct Scheme

Investment and Account holdings related queries

Domestic Deposits

V. Donations

Indian Currency

F) COINS

RBI has not prescribed any limit for coin deposits by customers with banks. Banks are free to accept any amount of coins from their customers.

All you wanted to know about NBFCs

G. Other/ miscellaneous aspects

Board-approved policies of REs should cover such operational aspects. One possible way could be to distribute the annualized repayment obligations over twelve months to estimate monthly outgo of the household towards debt repayment.

FAQs on Non-Banking Financial Companies

Prudential Norms

A. Earning Value : | Average Profit after tax (net of | ||

dividend on preference shares | |||

and extra ordinary items ) for | |||

the last three years | Capitalisation | ||

X | factor | ||

Number of equity shares |

Hypothetically, the profit after tax for the last three | } | Rs. 100.00 lakhs, |

financial years net of dividend on preference shares } | Rs. 120.00 lakhs | |

and net of extra ordinary items | } & | Rs. 140.00 lakhs |

No. of equity shares of the company | 10,00,000 shares | |

The investee company is a predominantly manufacturing | ||

company and the capitalisation factor would be | : 8 per cent | |

The earning value will be worked out as under : | ||

(100.00+120.00+140.00) | 100 | ||

X | --- | = Rs.150/- | |

3 X 10,00,000 | 8 |

Retail Direct Scheme

Contact us

You can reach us in three ways:

-

Toll free phone number: 1800 267 7955 (between 9 am to 7 pm on any working day).

-

E-mail id: support@rbiretaildirect.org.in

-

Raise a request on the Retail Direct portal.

For additional details on using the Retail Direct portal, you may refer to the User Manual in the Help section of the Retail Direct Portal.

Domestic Deposits

V. Donations

Indian Currency

F) COINS

The One Rupee notes issued under the Coinage Act, 2011 are legal tender and included in the expression Rupee coin for all the purposes of the Reserve Bank of India Act, 1934. Since the rupee coins issued by Government constitute the liabilities of the Government, one rupee Note is also liability of the Government of India.

All you wanted to know about NBFCs

G. Other/ miscellaneous aspects

The instructions on microfinance loans issued under various Directions are applicable only to the regulated entities mentioned below:

(i) All Commercial Banks (including Small Finance Banks, Local Area Banks, and Regional Rural Banks) excluding Payments Banks;

(ii) All Primary (Urban) Co-operative Banks/ State Co-operative Banks/ District Central Co-operative Banks; and

(iii) All Non-Banking Financial Companies (including Microfinance Institutions and Housing Finance Companies).

However, it may be prudent for other lenders operating in the microfinance sector to follow customer-centric instructions for microfinance loans issued under various Directions. Further, it may be noted that exemptions from Sections 45-IA, 45-IB and 45-IC of the RBI Act, 1934 have been withdrawn for those ‘not for profit’ companies engaged in microfinance activities that have asset size of ₹100 crore and above.

FAQs on Non-Banking Financial Companies

Prudential Norms

- The Prudential Norms have prescribed that the unquoted shares should be valued at break up value. However, an NBFC can also value these shares at fair value, if it so desires.

Break up value and fair value are to be calculated as per the formula given in the Directions. The formula is illustrated as under :

If the paid equity capital of the company is = Rs. 1,00,00,000

The free reserves net of intangible assets

and deferred revenue expenditure = Rs. 3,20,00,000

Number of equity shares = 10,00,000 shares

The break up value will be : | 1,00,00,000 + 3,20,00,000 | = Rs. 42/- |

10,00,000 |

If we take the earning value worked out in the previous question, and since we know that the fair value is the mean of the break up value and the earning value, the fair value will be | 150+42 | = Rs.96/- |

2 |

In the given case, the company may value its shares at fair value viz, Rs.96/- which is higher than the break up value at Rs.42/- or cost, whichever is lower.

Domestic Deposits

V. Donations

Indian Currency

F) COINS

Yes. Different designs of ₹10 coins are currently in circulation. All coins of ₹10 denomination minted from time to time by the Government of India (with/without the Rupee symbol) are legal tender. For more details kindly see our Press Release issued in this regard which is available at the following link www.rbi.org.in>>Issuer of currency>>Press Release>>January 17, 2018. https://rbi.org.in/en/web/rbi/-/press-releases/rbi-reiterates-legal-tender-status-of-%E2%82%B9-10-coins-of-different-designs-42887.

All you wanted to know about NBFCs

G. Other/ miscellaneous aspects

The exemption provided by the Reserve Bank to ‘Not for Profit’ companies (i.e., companies incorporated under Section 8 of the Companies Act, 2013 or Section 25 of the Companies Act, 1956) is applicable to those which are providing microfinance loans as defined in the Reserve Bank of India (Non-Banking Financial Companies – Credit Facilities) Directions, 2025 and subject to conditions specified in para 51 of our ‘Reserve Bank of India (Non-Banking Financial Companies – Registration, Exemptions and Framework for Scale Based Regulation) Directions, 2025 (as amended from time to time). This exemption is not applicable to other ‘Not for Profit’ companies engaged in NBFI business and it is incumbent upon such companies to obtain a certificate of registration under Section 45-IA of the RBI Act, 1934 in case these companies are fulfilling the ‘Principal Business Criteria’ as specified in our Press Release 1998-99/1269 dated April 08, 1999.

FAQs on Non-Banking Financial Companies

Prudential Norms

Domestic Deposits

VI. Premises Loan

-

The Board of Directors of the banks should lay down the policy and formulate operational guidelines separately in respect of metropolitan, urban, semi-urban and rural areas covering all areas in respect of acquiring premises on lease/ rental basis for the banks’ use. These guidelines should include also delegation of powers at various levels. The decision in regard to surrendering or shifting of premises other than at rural centers should be taken at the central office level by a committee of senior executives.

-

The Board of Directors of the bank should lay down separate policy for granting of loans to landlords who provide them premises on lease/ rental basis. The rate of interest to be charged on such loans should be fixed as per the lending rate directives issued by RBI with BPLR as the minimum lending rate for the loans above Rs.2 lakhs. The rate of interest may be simple or compound, in accordance with the usual practice of the bank, as applicable to other term loans.

-

Banks should provide a suitable mechanism for redressing the genuine grievances of the landlord expeditiously.

-

The details of negotiated contracts in respect of advances to landlords and rental (including taxes etc. and deposits of Rs.25 lakhs and above) on premises taken on lease/ rental by the public sector banks, should be reported to the Central Bureau of Investigation (CBI) as per the extant Government instructions. This requirement will not be applicable to banks in the private sector.

Indian Currency

F) COINS

The Government of India is responsible for the designing and minting of coins in various denominations.

All you wanted to know about NBFCs

G. Other/ miscellaneous aspects

The customer should keep in mind, among others, the following:

(i) There is no requirement of keeping any deposit/ margin/ collateral/ primary security with the lender at any stage of the microfinance loan.

(ii) Lender is required to provide a loan card to the borrower in a language understood by the borrower which should have following information:

- Information which adequately identifies the borrower;

- Simplified factsheet on pricing;

- All other terms and conditions attached to the loan;

- Acknowledgements by the lender of all repayments including instalments received and the final discharge; and

- Details of the grievance redress system, including the name and contact number of the nodal officer of the lender.

(iii) Purchase of any non-credit products is purely voluntary. Fee structure for such products shall be explicitly communicated in the loan card.

(iv) Training provided by the lenders is free of cost.

FAQs on Non-Banking Financial Companies

Prudential Norms

Domestic Deposits

VII. Service charges

Indian Currency

F) COINS

The Government of India decides on the quantity of coins to be minted on the basis of indent received from the Reserve Bank on yearly basis.

All you wanted to know about NBFCs

G. Other/ miscellaneous aspects

A customer is required to pay only those charges which are explicitly mentioned in the factsheet provided by the lender. Besides this, the customer should also note the following:

(i) There is no pre-payment penalty on microfinance loans.

(ii) Penalty, if any, for delayed payment can be applied only on the overdue amount and not on the entire loan amount.

(iii) Any change in interest rate or any other charge shall be informed to the borrower in writing well in advance and these changes shall be effective only prospectively.

FAQs on Non-Banking Financial Companies

Depositor Awareness

Indian Currency

F) COINS

Coins of denominations 50 paise, one rupee, two rupees, five rupees, ten rupees and twenty rupees continue to be legal tender.

Reserve Bank of India has been issuing press releases from time to time advising the members of public to accept coins as legal tender in all their transactions without any hesitation. These press releases are available on our website www.rbi.org.in under Currency Management > Press release at the following links:

Further, RBI has been conducting awareness campaigns in Print, SMS and social media and also disseminates awareness on coins through “RBI says’’ and “RBI Kehta Hai’’ from time to time.

Besides, the Reserve Bank has instructed the banks to accept coins for transactions and exchange at all their branches.

All you wanted to know about NBFCs

G. Other/ miscellaneous aspects

FAQs on Non-Banking Financial Companies

Depositor Awareness

Indian Currency

F) COINS

For commemorative coins, you may refer to the website of SPMCIL at http://www.spmcil.com or contact SPMCIL.

All you wanted to know about NBFCs

G. Other/ miscellaneous aspects

NBFC-IFCs can lend to/ invest in InvITs subject to adherence to applicable regulatory guidelines including exposure norms applicable to them. NBFC-IFCs can also lend to/ invest in other trust funds subject to compliance with the criterion of deployment of minimum 75 per cent of total assets towards infrastructure lending and other applicable regulations.

FAQs on Non-Banking Financial Companies

Depositor Awareness

Indian Currency

F) COINS

Customers aggrieved with the services provided by the banks and a related grievance not resolved to the satisfaction of the customers, or not replied to within a period of 30 days by the bank may approach the RBI Ombudsman under ‘The Reserve Bank - Integrated Ombudsman Scheme, 2021’. Complaints can be filed online on https://cms.rbi.org.in and also through the dedicated e-mail or sent in physical mode to the ‘Centralised Receipt and Processing Centre’ set up at Reserve Bank of India, 4th Floor, Sector 17, Chandigarh - 160017 with the bank/ postal receipts as proof for necessary action.

FAQs on Non-Banking Financial Companies

Depositor Awareness

RNBCs

Nomination facility

All you wanted to know about NBFCs

H. Other/ miscellaneous aspects

Disclaimer: These FAQs are issued by the Reserve Bank for information and general guidance purposes only. The Reserve Bank will not be held responsible for actions taken and/or decisions made on the basis of the same. For clarifications or interpretations, if any, one may be guided by the relevant circulars and notifications issued from time to time.

| Related Press Release | |

| May 31, 2013 | Check before Depositing Money with Financial Entities: RBI Advisory |

റിസർവ് ബാങ്ക് ഓഫ് ഇന്ത്യ മൊബൈൽ ആപ്ലിക്കേഷൻ ഇൻസ്റ്റാൾ ചെയ്ത് ഏറ്റവും പുതിയ വാർത്തകളിലേക്ക് വേഗത്തിലുള്ള ആക്സസ് നേടുക!

ഞങ്ങളുടെ ആപ്പ് ഇൻസ്റ്റാൾ ചെയ്യാൻ QR കോഡ് സ്കാൻ ചെയ്യുക

പേജ് അവസാനം അപ്ഡേറ്റ് ചെയ്തത്: