IST,

IST,

Content Type:

Biennial survey on Foreign Collaboration in Indian Industry (FCS)

Some other important points to be noted

Ans.: In the FCS form, industry codes are given as per the National Industrial Classification (NIC) (2 digit) codes. Please specify, if you have chosen “Other” industry codes, like Other manufacturing, Other services activities.

Housing Loans

If you have a complaint against only scheduled bank on any of the above grounds, you can lodge a complaint with the bank concerned in writing in a specific complaint register provided at the branches as per the recommendation of the Goiporia Committee or on a sheet of paper. Ask for a receipt of your complaint. The details of the official receiving your complaint may be specifically sought. If the bank fails to respond within 30 days, you can lodge a complaint with the Banking Ombudsman. (Please note that complaints pending in any other judicial forum will not be entertained by the Banking Ombudsman). No fee is levied by the office of the Banking Ombudsman for resolving the customer’s complaint. A unique complaint identification number will be given to you for tracking purpose. (A list of the Banking Ombudsmen along with their contact details is provided on the RBI website).

Complaints are to be addressed to the Banking Ombudsman within whose jurisdiction the branch or office of the bank complained against is located. Complaints can be lodged simply by writing on a plain paper or online at www.bankingombudsman.rbi.org.in or by sending an email to the Banking Ombudsman. Complaint forms are available at all bank branches also.

Complaint can also be lodged by your authorised representative (other than a lawyer) or by a consumer association / forum acting on your behalf.

If you are not happy with the decision of the Banking Ombudsman, you can appeal to the Appellate Authority in the Reserve Bank of India.

Portfolio Investment Positions (PIP) by Counterpart Economy (formerly CPIS) – India

Some important definitions and concepts

Ans: The following are included under equity securities:

-

Ordinary shares.

-

Stocks.

-

Participating preference shares.

-

Shares/units in mutual funds and investment trusts

-

Depository receipts (e.g., American Depository Receipts) denoting ownership of equity securities issued by non-residents.

-

Securities sold under repos or “lent” under securities lending arrangements.

-

Securities acquired under reverse repos or securities borrowing arrangements and subsequently sold to a third party should be reported as a negative holding.

Core Investment Companies

B. Registration and related matters:

Ans: The company would have to apply for COR to RBI, giving a satisfactory time-bound business plan within which, it would achieve CIC status.

All you wanted to know about NBFCs

C. Definition of deposits, Eligible / Ineligible Institutions to accept deposits and Related Matters

A company which does not have financial assets which are more than 50% of its total assets and does not derive at least 50% of its gross income from such assets is not an NBFC. Its principal business would be non-financial activity like agricultural operations, industrial activity, purchase or sale of goods or purchase/construction of immovable property, and will be a non-banking non-financial company. Acceptance of deposits by a Non-Banking Non-Financial Company are governed by the rules and regulations issued by the Ministry of Corporate Affairs.

Indian Currency

B) Banknotes

With a view to enhancing operational efficiency and cost effectiveness in banknote printing, non-sequential numbering was introduced in 2011 consistent with international best practices. Packets of banknotes with non-sequential numbering contain 100 notes which are not sequentially numbered.

Housing Loans

REVERSE MORTGAGE LOAN

The scheme of reverse mortgage has been introduced recently for the benefit of senior citizens owning a house but having inadequate income to meet their needs. Some important features of reverse mortgage are:

- A homeowner who is above 60 years of age is eligible for reverse mortgage loan. It allows him to turn the equity in his home into one lump sum or periodic payments mutually agreed by the borrower and the banker.

- The property should be clear from encumbrances and should have clear title of the borrower.

- NO REPAYMENT is required as long as the borrower lives, Borrower should pay all taxes relating to the house and maintain the property as his primary residence.

- The amount of loan is based on several factors: borrower’s age, value of the property, current interest rates and the specific plan chosen. Generally speaking, the higher the age, higher the value of the home, the more money is available.

- The valuation of the residential property is done at periodic intervals and it shall be clearly specified to the borrowers upfront. The banks shall have the option to revise the periodic / lump sum amount at such frequency or intervals based on revaluation of property.

- Married couples will be eligible as joint borrowers for financial assistance. In such a case, the age criteria for the couple would be at the discretion of the lending institution, subject to at least one of them being above 60 years of age.

- The loan shall become due and payable only when the last surviving borrower dies or would like to sell the home, or permanently moves out.

- On death of the home owner, the legal heirs have the choice of keeping or selling the house. If they decide to sell the house, the proceeds of the sale would be used to repay the mortgage, with the remainder going to the heirs.

- As per the scheme formulated by National Housing Bank (NHB), the maximum period of the loan period is 15 years. The residual life of the property should be at least 20 years. Where the borrower lives longer than 15 years, periodic payments will not be made by lender. However, the borrower can continue to occupy.

- From FY 2008-09, the lump sum amount or periodic payments received on reverse mortgage loan will not attract income tax or capital gains tax.

Note- Reverse mortgage is a fixed interest discounted product in reverse. It does not take into account the changes in interest rates as yet.

Important – This part is fine printed to help you practice reading the fine print. The loan agreement documentation runs into nearly 50 pages and its language is complex. If you thought everyone signs the same agreements with the bank, where is the need to read? You are not taking an informed decision. If you thought somebody would have pointed this to me if there was any problem, then maybe they did but you could not read or listen to it. Think again! Borrowers' and lenders' rights may not be expressed clearly in a transparent manner in all the loan agreements. The home loan agreement may not be provided to you in advance so that this could be read and understood before you sign the agreement. Every method may be used to delay handing over a copy to the borrower in sufficient time. Some areas you may focus are a) check the “reset clause” incorporated by some banks in their home loan agreements that allows them to change the interest rate in the future, even on fixed rate loans. Banks may set their reset clauses for 3 or 2 year intervals. They say a lender cannot have an agreement that a fixed rate is set for the entire tenure of 15 to 20 years as this will cause an asset-liability mismatch. Talk to your bank. b) Please seek clarifications on the term “exceptional circumstances” (if stated in the loan agreement) under which loan rates can be unilaterally changed by your bank. c) A common person thinks that default ideally means non-payment of one or more loan installments. In some loan documentation it can include divorce and death (in individual case) and even involvement in civil litigation or criminal offence. d) Does the loan agreement say that disbursement of the loan may be made directly to the builder or developer and in the case of a ready-built property to the vendor thereof and/or in such other manner as may be decided solely by bank? It is the borrower whose original property papers are retained with the bank, so why disburse to the builder. Possession of property has been delayed in some cases when the cheque was issued in the name of the builder and the builder refused to pay delay penalty to the borrower e) Does the agreement enable assignment of your loan to a third party? You take into account reputation and credibility of the bank before entering into a loan agreement with it. Are you comfortable with third party takes over or should you also be allowed to move your home loan from one bank to another in that case? Look for ambiguous clauses and discuss with the banker. Some agreements say changes in employment etc. have to be informed well in advance without quantifying the term “well in advance”. f) In one case the loan documentation says “issuance of pre-approval letter should not be construed as a commitment by the bank to grant the housing loan and processing fees is not re-fundable even if the home loan is not processed”. This is never ending it seems. The above are only indicative instances of what has been observed / reported/ indicated by various sources. However, our main objective was to get you into the habit of reading the fine print. If you have read this, you would have understood the importance of reading fine print in any document and we have achieved our objective. I only wish I could have made the print smaller as in the real cases.

FAQs on Non-Banking Financial Companies

Inter-corporate deposits (ICDs)

Domestic Deposits

II. Deposits of Non-Residents Indians (NRIs)

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Procedure for submission of the FLA return

Ans: You will receive the system-generated acknowledgement of FLA data submitted by you at the time of final submission itself. No separate mail will be sent in this regard.

Retail Direct Scheme

Know Your Customer (KYC) related queries

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

National Common Mobility Card (NCMC) issued by Paytm Payments Bank

Government Securities Market in India – A Primer

Delivery versus Payment (DvP) is the mode of settlement of securities wherein the transfer of securities and funds happen simultaneously. This ensures that unless the funds are paid, the securities are not delivered and vice versa. DvP settlement eliminates the settlement risk in transactions. There are three types of DvP settlements, viz., DvP I, II and III which are explained below:

Delivery versus Payment (DvP) is the mode of settlement of securities wherein the transfer of securities and funds happen simultaneously. This ensures that unless the funds are paid, the securities are not delivered and vice versa. DvP settlement eliminates the settlement risk in transactions. There are three types of DvP settlements, viz., DvP I, II and III which are explained below:

i. DvP I – The securities and funds legs of the transactions are settled on a gross basis, that is, the settlements occur transaction by transaction without netting the payables and receivables of the participant.

ii. DvP II – In this method, the securities are settled on gross basis whereas the funds are settled on a net basis, that is, the funds payable and receivable of all transactions of a party are netted to arrive at the final payable or receivable position which is settled.

iii. DvP III – In this method, both the securities and the funds legs are settled on a net basis and only the final net position of all transactions undertaken by a participant is settled.

Liquidity requirement in a gross mode is higher than that of a net mode since the payables and receivables are set off against each other in the net mode.

Foreign Investment in India

Answer: Please refer to regulation 11 of FEMA 20(R).

| Particulars | Listed Company | Un-Listed Company |

| Issue by an Indian company or transferred from a resident to non-resident - Price should not be less than | The price worked out in accordance with the relevant SEBI guidelines | The fair value worked out as per any internationally accepted pricing methodology for valuation on an arm’s length basis, duly certified by a Chartered Accountant or a SEBI registered Merchant Banker or a practicing Cost Accountant. |

| Transfer from a non-resident to resident - Price should not be more than | The price worked out in accordance with the relevant SEBI guidelines | The fair value as per any internationally accepted pricing methodology for valuation on an arm’s length basis, duly certified by a Chartered Accountant or a SEBI registered Merchant Banker. |

The pricing guidelines shall not be applicable for investment by a person resident outside India on non-repatriation basis.

Indian Currency

B) Banknotes

In terms of Section 25 of the RBI Act, the design, form and material of bank notes shall be such as may be approved by the Central Government after consideration of the recommendations made by Central Board.

Biennial survey on Foreign Collaboration in Indian Industry (FCS)

Some other important points to be noted

Ans.: Yes, it is mandatory. Here the person authorised to fill the form owns the responsibility of information furnished and declares its accuracy including CIN number. It is a final check for all the details which are filled-up in the survey schedule of FCS survey.

Core Investment Companies

B. Registration and related matters:

Ans: CICs that (a) have an asset size of less than ₹100 crore irrespective of whether they are accessing public funds or not and (b) have an asset size of ₹ 100 crore and above and are not accessing public funds have been exempt from registration with the Bank under Section 45IA of the RBI Act, 1934 in terms of Master Direction DoR(NBFC).PD.003/03.10.119/2016-17 dated August 25, 2016. Thus, they are not required to register with the Bank at all. As this is an exemption given under Section 45NC of the RBI Act, 1934, they are not required to approach the Bank at all.

Portfolio Investment Positions (PIP) by Counterpart Economy (formerly CPIS) – India

Some important definitions and concepts

Ans: The following are not included under equity securities:

-

Equity securities issued by a nonresident enterprise that is related to the resident owner of those securities should be excluded from this survey.

-

Non-participating preference shares.

-

Securities acquired under reverse repos.

-

Securities acquired under borrowing arrangements.

All you wanted to know about NBFCs

C. Definition of deposits, Eligible / Ineligible Institutions to accept deposits and Related Matters

Para 5.1.25 of Master Direction – Reserve Bank of India (Non-Banking Financial Company – Scale Based Regulation) 2023 (as amended from time to time) defines ‘Owned Fund’ as aggregate of the paid-up equity capital, preference shares which are compulsorily convertible into equity, free reserves, balance in share premium account and capital reserves representing surplus arising out of sale proceeds of asset, excluding reserves created by revaluation of asset; as reduced by accumulated balance of loss, book value of intangible assets and deferred revenue expenditure, if any.

'Net Owned Fund' is defined under Section 45-IA(7) of the RBI Act, 1934. As per this definition, the Net Owned Fund means–

(a) aggregate of the paid-up equity capital and free reserves as disclosed in the latest balance-sheet of the company after deducting there from, accumulated balance of loss, deferred revenue expenditure, and other intangible assets; and

FAQs on Non-Banking Financial Companies

Inter-corporate deposits (ICDs)

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Procedure for submission of the FLA return

Ans: An AIF needs to register on the FLAIR portal. Since there is no provision for online filing of FLA return for AIF in the prescribed format as of now, they need to send a mail requesting for the latest format for filing of FLA Return for AIF after completing registration process on the portal. Thereafter FLA Team will send the excel based format for filling FLA return by AIF via mail to them. They need to fill the excel format and send us the same on email. Email based acknowledgement form will be sent to them by FLA Team on receiving the filled-in FLA form.

Domestic Deposits

II. Deposits of Non-Residents Indians (NRIs)

Retail Direct Scheme

Know Your Customer (KYC) related queries

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

National Common Mobility Card (NCMC) issued by Paytm Payments Bank

Government Securities Market in India – A Primer

Housing Loans

REVERSE MORTGAGE LOAN

EXAMPLE OF EMI CALCULATION (PURE FIXED LOAN)

|

|

Amount of Loan |

1,000,000.00 |

|

|

|

|

Annual Interest Rate |

15.00% |

|

|

|

|

Number of Payments |

120 |

|

|

|

|

Monthly Payment |

16,133.50 |

|

|

|

Number |

Payment |

Interest |

Principal |

Balance |

|

0 |

|

|

|

1,000,000.00 |

|

1 |

16,133.50 |

12,500.00 |

3,633.50 |

996,366.50 |

|

2 |

16,133.50 |

12,454.58 |

3,678.91 |

992,687.59 |

|

3 |

16,133.50 |

12,408.59 |

3,724.90 |

988,962.69 |

|

4 |

16,133.50 |

12,362.03 |

3,771.46 |

985,191.23 |

|

5 |

16,133.50 |

12,314.89 |

3,818.61 |

981,372.62 |

|

6 |

16,133.50 |

12,267.16 |

3,866.34 |

977,506.28 |

|

7 |

16,133.50 |

12,218.83 |

3,914.67 |

973,591.62 |

|

8 |

16,133.50 |

12,169.90 |

3,963.60 |

969,628.02 |

|

9 |

16,133.50 |

12,120.35 |

4,013.15 |

965,614.87 |

|

10 |

16,133.50 |

12,070.19 |

4,063.31 |

961,551.56 |

|

11 |

16,133.50 |

12,019.39 |

4,114.10 |

957,437.46 |

|

12 |

16,133.50 |

11,967.97 |

4,165.53 |

953,271.93 |

|

13 |

16,133.50 |

11,915.90 |

4,217.60 |

949,054.34 |

|

14 |

16,133.50 |

11,863.18 |

4,270.32 |

944,784.02 |

|

15 |

16,133.50 |

11,809.80 |

4,323.70 |

940,460.32 |

|

16 |

16,133.50 |

11,755.75 |

4,377.74 |

936,082.58 |

|

17 |

16,133.50 |

11,701.03 |

4,432.46 |

931,650.12 |

|

18 |

16,133.50 |

11,645.63 |

4,487.87 |

927,162.25 |

|

19 |

16,133.50 |

11,589.53 |

4,543.97 |

922,618.28 |

|

20 |

16,133.50 |

11,532.73 |

4,600.77 |

918,017.51 |

|

21 |

16,133.50 |

11,475.22 |

4,658.28 |

913,359.24 |

|

22 |

16,133.50 |

11,416.99 |

4,716.51 |

908,642.73 |

|

23 |

16,133.50 |

11,358.03 |

4,775.46 |

903,867.27 |

|

24 |

16,133.50 |

11,298.34 |

4,835.15 |

899,032.12 |

|

25 |

16,133.50 |

11,237.90 |

4,895.59 |

894,136.52 |

|

26 |

16,133.50 |

11,176.71 |

4,956.79 |

889,179.73 |

|

27 |

16,133.50 |

11,114.75 |

5,018.75 |

884,160.98 |

|

28 |

16,133.50 |

11,052.01 |

5,081.48 |

879,079.50 |

|

29 |

16,133.50 |

10,988.49 |

5,145.00 |

873,934.50 |

|

30 |

16,133.50 |

10,924.18 |

5,209.31 |

868,725.18 |

|

31 |

16,133.50 |

10,859.06 |

5,274.43 |

863,450.75 |

|

32 |

16,133.50 |

10,793.13 |

5,340.36 |

858,110.39 |

|

33 |

16,133.50 |

10,726.38 |

5,407.12 |

852,703.28 |

|

34 |

16,133.50 |

10,658.79 |

5,474.70 |

847,228.57 |

|

35 |

16,133.50 |

10,590.36 |

5,543.14 |

841,685.43 |

|

36 |

16,133.50 |

10,521.07 |

5,612.43 |

836,073.00 |

|

37 |

16,133.50 |

10,450.91 |

5,682.58 |

830,390.42 |

|

38 |

16,133.50 |

10,379.88 |

5,753.62 |

824,636.81 |

|

39 |

16,133.50 |

10,307.96 |

5,825.54 |

818,811.27 |

|

40 |

16,133.50 |

10,235.14 |

5,898.35 |

812,912.92 |

|

41 |

16,133.50 |

10,161.41 |

5,972.08 |

806,940.83 |

|

42 |

16,133.50 |

10,086.76 |

6,046.74 |

800,894.10 |

|

43 |

16,133.50 |

10,011.18 |

6,122.32 |

794,771.78 |

|

44 |

16,133.50 |

9,934.65 |

6,198.85 |

788,572.93 |

|

45 |

16,133.50 |

9,857.16 |

6,276.33 |

782,296.59 |

|

46 |

16,133.50 |

9,778.71 |

6,354.79 |

775,941.81 |

|

47 |

16,133.50 |

9,699.27 |

6,434.22 |

769,507.58 |

|

48 |

16,133.50 |

9,618.84 |

6,514.65 |

762,992.93 |

|

49 |

16,133.50 |

9,537.41 |

6,596.08 |

756,396.85 |

|

50 |

16,133.50 |

9,454.96 |

6,678.54 |

749,718.31 |

|

51 |

16,133.50 |

9,371.48 |

6,762.02 |

742,956.30 |

|

52 |

16,133.50 |

9,286.95 |

6,846.54 |

736,109.75 |

|

53 |

16,133.50 |

9,201.37 |

6,932.12 |

729,177.63 |

|

54 |

16,133.50 |

9,114.72 |

7,018.78 |

722,158.85 |

|

55 |

16,133.50 |

9,026.99 |

7,106.51 |

715,052.34 |

|

56 |

16,133.50 |

8,938.15 |

7,195.34 |

707,857.00 |

|

57 |

16,133.50 |

8,848.21 |

7,285.28 |

700,571.72 |

|

58 |

16,133.50 |

8,757.15 |

7,376.35 |

693,195.37 |

|

59 |

16,133.50 |

8,664.94 |

7,468.55 |

685,726.82 |

|

60 |

16,133.50 |

8,571.59 |

7,561.91 |

678,164.91 |

|

61 |

16,133.50 |

8,477.06 |

7,656.43 |

670,508.47 |

|

62 |

16,133.50 |

8,381.36 |

7,752.14 |

662,756.33 |

|

63 |

16,133.50 |

8,284.45 |

7,849.04 |

654,907.29 |

|

64 |

16,133.50 |

8,186.34 |

7,947.15 |

646,960.14 |

|

65 |

16,133.50 |

8,087.00 |

8,046.49 |

638,913.64 |

|

66 |

16,133.50 |

7,986.42 |

8,147.08 |

630,766.57 |

|

67 |

16,133.50 |

7,884.58 |

8,248.91 |

622,517.65 |

|

68 |

16,133.50 |

7,781.47 |

8,352.03 |

614,165.63 |

|

69 |

16,133.50 |

7,677.07 |

8,456.43 |

605,709.20 |

|

70 |

16,133.50 |

7,571.37 |

8,562.13 |

597,147.07 |

|

71 |

16,133.50 |

7,464.34 |

8,669.16 |

588,477.91 |

|

72 |

16,133.50 |

7,355.97 |

8,777.52 |

579,700.39 |

|

73 |

16,133.50 |

7,246.25 |

8,887.24 |

570,813.15 |

|

74 |

16,133.50 |

7,135.16 |

8,998.33 |

561,814.82 |

|

75 |

16,133.50 |

7,022.69 |

9,110.81 |

552,704.01 |

|

76 |

16,133.50 |

6,908.80 |

9,224.70 |

543,479.31 |

|

77 |

16,133.50 |

6,793.49 |

9,340.00 |

534,139.31 |

|

78 |

16,133.50 |

6,676.74 |

9,456.75 |

524,682.56 |

|

79 |

16,133.50 |

6,558.53 |

9,574.96 |

515,107.59 |

|

80 |

16,133.50 |

6,438.84 |

9,694.65 |

505,412.94 |

|

81 |

16,133.50 |

6,317.66 |

9,815.83 |

495,597.11 |

|

82 |

16,133.50 |

6,194.96 |

9,938.53 |

485,658.58 |

|

83 |

16,133.50 |

6,070.73 |

10,062.76 |

475,595.81 |

|

84 |

16,133.50 |

5,944.95 |

10,188.55 |

465,407.26 |

|

85 |

16,133.50 |

5,817.59 |

10,315.90 |

455,091.36 |

|

86 |

16,133.50 |

5,688.64 |

10,444.85 |

444,646.51 |

|

87 |

16,133.50 |

5,558.08 |

10,575.41 |

434,071.09 |

|

88 |

16,133.50 |

5,425.89 |

10,707.61 |

423,363.48 |

|

89 |

16,133.50 |

5,292.04 |

10,841.45 |

412,522.03 |

|

90 |

16,133.50 |

5,156.53 |

10,976.97 |

401,545.06 |

|

91 |

16,133.50 |

5,019.31 |

11,114.18 |

390,430.88 |

|

92 |

16,133.50 |

4,880.39 |

11,253.11 |

379,177.77 |

|

93 |

16,133.50 |

4,739.72 |

11,393.77 |

367,784.00 |

|

94 |

16,133.50 |

4,597.30 |

11,536.20 |

356,247.80 |

|

95 |

16,133.50 |

4,453.10 |

11,680.40 |

344,567.40 |

|

96 |

16,133.50 |

4,307.09 |

11,826.40 |

332,741.00 |

|

97 |

16,133.50 |

4,159.26 |

11,974.23 |

320,766.77 |

|

98 |

16,133.50 |

4,009.58 |

12,123.91 |

308,642.85 |

|

99 |

16,133.50 |

3,858.04 |

12,275.46 |

296,367.39 |

|

100 |

16,133.50 |

3,704.59 |

12,428.90 |

283,938.49 |

|

101 |

16,133.50 |

3,549.23 |

12,584.26 |

271,354.23 |

|

102 |

16,133.50 |

3,391.93 |

12,741.57 |

258,612.66 |

|

103 |

16,133.50 |

3,232.66 |

12,900.84 |

245,711.82 |

|

104 |

16,133.50 |

3,071.40 |

13,062.10 |

232,649.72 |

|

105 |

16,133.50 |

2,908.12 |

13,225.37 |

219,424.35 |

|

106 |

16,133.50 |

2,742.80 |

13,390.69 |

206,033.66 |

|

107 |

16,133.50 |

2,575.42 |

13,558.07 |

192,475.58 |

|

108 |

16,133.50 |

2,405.94 |

13,727.55 |

178,748.03 |

|

109 |

16,133.50 |

2,234.35 |

13,899.15 |

164,848.89 |

|

110 |

16,133.50 |

2,060.61 |

14,072.88 |

150,776.00 |

|

111 |

16,133.50 |

1,884.70 |

14,248.80 |

136,527.21 |

|

112 |

16,133.50 |

1,706.59 |

14,426.91 |

122,100.30 |

|

113 |

16,133.50 |

1,526.25 |

14,607.24 |

107,493.06 |

|

114 |

16,133.50 |

1,343.66 |

14,789.83 |

92,703.23 |

|

115 |

16,133.50 |

1,158.79 |

14,974.71 |

77,728.52 |

|

116 |

16,133.50 |

971.61 |

15,161.89 |

62,566.63 |

|

117 |

16,133.50 |

782.08 |

15,351.41 |

47,215.22 |

|

118 |

16,133.50 |

590.19 |

15,543.31 |

31,671.91 |

|

119 |

16,133.50 |

395.90 |

15,737.60 |

15,934.32 |

|

120 |

16,133.50 |

199.18 |

15,934.32 |

0.00 |

Loan amount x rpm x (1+pm)

(1+pm)

- rpm= interest per month (rate of interest per year/12)

- n= number of installments

NB: If you have a fixed budget towards EMI you can arrive at loan amount by changing the other variables such as by reducing the rate of interest or by increasing the tenure of loan. This can also be arrived at through EMI calculator by a trial-and-error approach.

Foreign Investment in India

Indian Currency

B) Banknotes

The volume and value of banknotes to be printed in a year depends on various factors such as (i) the expected increase in Notes in Circulation (NIC) to meet the growing needs of the public and (ii) the need for replacing soiled/mutilated notes so as to ensure that only good quality notes are in circulation. The expected increase in NIC is estimated using statistical models which consider macro-economic factors such as expected growth in GDP, inflation, interest rates, growth in non-cash modes of payment etc. The replacement requirement depends on the volume of notes already in circulation and the average life of banknotes. The Reserve Bank estimates the volume and value of notes to be printed in a year based on the above factors as well as feedback received from its own Regional Offices and banks regarding expected demand for cash and finalises the same in consultation with the Government of India and the printing presses.

Biennial survey on Foreign Collaboration in Indian Industry (FCS)

Some other important points to be noted

Ans.: Please refer to the below table containing the error codes (Fatal error, non-Fatal error) with their descriptions. If you get an acknowledgment of the processed data with any Fatal error codes, then follow the below-mentioned fatal error message/description and revise your data and resubmit it on fcs@rbi.org.in. If you get an acknowledgment of the processed data with any Non-fatal error codes then give justification/clarification on the errors, by sending the same to fcsquery@rbi.org.in.

| Sr. No. | Revised- Rejection Criteria | Revised - Error Message/descriptions | Error Code |

| Fatal Error | |||

| 1 | When the year is left blank | The year cannot be left blank. Please specify the reference year and fill the return. | FCS_F_001 |

| 2 | When the survey year is incorrect | Survey year should be the subsequent survey after the latest closed survey year in the system. Please specify the correct Survey year | FCS_F_001 |

| 3 | When survey year is null | The survey year cannot be NULL. Please specify the survey year and fill the return. | FCS_F_001 |

| 4 | When survey year is incorrect | Please specify proper survey year, please fill the form for the survey year | FCS_F_001 |

| 5 | When survey year is invalid | The year for which the information is pertaining, is invalid survey year. Please mention the reference year for which the return is filled | FCS_F_001 |

| 6 | When survey year is closed | FCS survey for {year} is closed | FCS_F_001 |

| 7 | When name of company not provided | Name of company is not provided. Please provide the name of company. | FCS_F_002 |

| 8 | When CIN Number is not given | CIN number is not provided. Please provide CIN number of the company. | FCS_F_003 |

| 9 | When telephone number is not given | Please provide the telephone number of contact person. | FCS_F_004 |

| 10 | When email id is not given | Please provide the email id of the contact person. | FCS_F_005 |

| Non-Fatal Error | |||

| 1 | When type of organization is not given | Please provide the type of organization. | FCS_NF_001 |

| 2 | Identification of the Reporting company when it is not given | Please specify the Identification of the Reporting company. | FCS_NF_002 |

| 3 | When economic activity is not given | Please provide the economic activity. | FCS_NF_003 |

| 4 | Please provide details for country name / equity share. | Please provide details for country name / equity share. | FCS_NF_008 |

| 5 | When provide details for country name / loan details is not given | Please provide details for country name / loan details. | FCS_NF_009 |

| 6 | When provide details for country name / amount details is not given | Please provide details for country name / amount details. | FCS_NF_011 |

| 7 | When the total equity capital of organization is not given | Please provide the total equity capital of the organization. | FCS_NF_004 |

| 8 | When foreign participation in equity capital cannot be more than total equity capital. | The foreign participation in equity capital cannot be more than total equity capital. | FCS_NF_005_PY |

| 9 | When foreign participation in equity capital cannot be more than total equity capital. | The foreign participation in equity capital cannot be more than total equity capital. | FCS_NF_005_CY |

| 10 | When foreign participation in equity capital cannot be more than total equity capital. | The foreign participation in equity capital cannot be more than total equity capital. | FCS_NF_005 |

| 11 | When Field 2: (2a) cannot be blank for both the years as company is foreign subsidiary. | Field 2: (2a) cannot be blank for both the years as company is foreign subsidiary. | FCS_NF_006 |

| 12 | When Field 2 cannot be blank for both the years as company is foreign associate. | Field 2 cannot be blank for both the years as company is foreign associate. | FCS_NF_007 |

| 13 | In part II, block 7, Total value of imports (7.1) cannot be less than sum of imports from foreign parent/associate/collaborator (7.1.1) and imports under collaboration arrangement (7.1.2). | In part II, block 7, Total value of imports (7.1) cannot be less than sum of imports from foreign parent/associate/collaborator (7.1.1) and imports under collaboration arrangement (7.1.2). | FCS_NF_012_PY |

| 14 | In part II, block 7, Total value of imports (7.1) cannot be less than sum of imports from foreign parent/associate/collaborator (7.1.1) and imports under collaboration arrangement (7.1.2). | In part II, block 7, Total value of imports (7.1) cannot be less than sum of imports from foreign parent/associate/collaborator (7.1.1) and imports under collaboration arrangement (7.1.2). | FCS_NF_012_CY |

| 15 | In part II, block 7, Total value of imports (7.1) cannot be less than sum of imports from foreign parent/associate/collaborator (7.1.1) and imports under collaboration arrangement (7.1.2). | In part II, block 7, Total value of imports (7.1) cannot be less than sum of imports from foreign parent/associate/collaborator (7.1.1) and imports under collaboration arrangement (7.1.2). | FCS_NF_012 |

| 16 | In part II, block 7, Exports of goods (7.2.1) cannot be less than sum of export of goods produced under foreign collaboration agreements (7.2.1.1) and exports to/on behalf of/through foreign collaborator/associate (7.2.1.2). | In part II, block 7, Exports of goods (7.2.1) cannot be less than sum of export of goods produced under foreign collaboration agreements (7.2.1.1) and exports to/on behalf of/through foreign collaborator/associate (7.2.1.2). | FCS_NF_013_PY |

| 17 | In part II, block 7, Exports of goods (7.2.1) cannot be less than sum of export of goods produced under foreign collaboration agreements (7.2.1.1) and exports to/on behalf of/through foreign collaborator/associate (7.2.1.2). | In part II, block 7, Exports of goods (7.2.1) cannot be less than sum of export of goods produced under foreign collaboration agreements (7.2.1.1) and exports to/on behalf of/through foreign collaborator/associate (7.2.1.2). | FCS_NF_013_CY |

| 18 | In part II, block 7, Exports of goods (7.2.1) cannot be less than sum of export of goods produced under foreign collaboration agreements (7.2.1.1) and exports to/on behalf of/through foreign collaborator/associate (7.2.1.2). | In part II, block 7, Exports of goods (7.2.1) cannot be less than sum of export of goods produced under foreign collaboration agreements (7.2.1.1) and exports to/on behalf of/through foreign collaborator/associate (7.2.1.2). | FCS_NF_013 |

| 19 | In part II, block 7, Export of services and other foreign exchange earnings (7.2.2) cannot be less than exports to foreign collaborator/associate (7.2.2.1). | In part II, block 7, Export of services and other foreign exchange earnings (7.2.2) cannot be less than exports to foreign collaborator/associate (7.2.2.1). | FCS_NF_014_PY |

| 20 | In part II, block 7, Export of services and other foreign exchange earnings (7.2.2) cannot be less than exports to foreign collaborator/associate (7.2.2.1). | In part II, block 7, Export of services and other foreign exchange earnings (7.2.2) cannot be less than exports to foreign collaborator/associate (7.2.2.1). | FCS_NF_014_CY |

| 21 | In part II, block 7, Export of services and other foreign exchange earnings (7.2.2) cannot be less than exports to foreign collaborator/associate (7.2.2.1). | In part II, block 7, Export of services and other foreign exchange earnings (7.2.2) cannot be less than exports to foreign collaborator/associate (7.2.2.1). | FCS_NF_014 |

| 22 | In part II, block 7, Total value of export on f. o. b. basis (7.2) cannot be less than sum of export of goods (7.2.1) and export of services and other foreign exchange earnings (7.2.2). | In part II, block 7, Total value of export on f. o. b. basis (7.2) cannot be less than sum of export of goods (7.2.1) and export of services and other foreign exchange earnings (7.2.2). | FCS_NF_015_PY |

| 23 | In part II, block 7, Total value of export on f. o. b. basis (7.2) cannot be less than sum of export of goods (7.2.1) and export of services and other foreign exchange earnings (7.2.2). | In part II, block 7, Total value of export on f. o. b. basis (7.2) cannot be less than sum of export of goods (7.2.1) and export of services and other foreign exchange earnings (7.2.2). | FCS_NF_015_CY |

| 24 | In part II, block 7, Total value of export on f. o. b. basis (7.2) cannot be less than sum of export of goods (7.2.1) and export of services and other foreign exchange earnings (7.2.2). | In part II, block 7, Total value of export on f. o. b. basis (7.2) cannot be less than sum of export of goods (7.2.1) and export of services and other foreign exchange earnings (7.2.2). | FCS_NF_015 |

| 25 | when company has foreign technical collaboration agreements, please provide the number of agreements. | Since your company has foreign technical collaboration agreements, please provide the number of agreements. | FCS_NF_016 |

| 26 | agreement details by providing information on all fields need to be filled | Please provide the agreement details by providing information on all fields. | FCS_NF_017 |

| 27 | Incomplete information. Please provide the agreement details for all the foreign technical collaboration agreements mentioned in field 11(b). | Incomplete information. Please provide the agreement details for all the foreign technical collaboration agreements mentioned in field 11(b). | FCS_NF_018 |

Core Investment Companies

B. Registration and related matters:

Ans: No, this exemption is specifically given to CICs only. NBFCs other than CICs are not covered by this or any other aspect of the CIC Directions and would have to register with the Bank and comply with all applicable Directions of the Bank as issued from time to time.

Portfolio Investment Positions (PIP) by Counterpart Economy (formerly CPIS) – India

Some important definitions and concepts

Ans: Debt securities are negotiable instruments serving as evidence of a debt. They include bills, bonds, notes, negotiable certificates of deposit, commercial paper, debentures, asset-backed securities, money market instruments, and similar instruments normally traded in the financial markets.

All you wanted to know about NBFCs

C. Definition of deposits, Eligible / Ineligible Institutions to accept deposits and Related Matters

NBFCs that ought to have sought registration from the Reserve Bank but are functioning without doing so are committing a breach of law. Such companies are liable for action as envisaged under the RBI Act, 1934. To identify such entities, the Reserve Bank has multiple sources of information. These include market intelligence, complaints received from affected parties, industry sources, and exception reports submitted by statutory auditors in terms of Master Direction - Non-Banking Financial Companies Auditor’s Report (Reserve Bank) Directions, 2016 (as amended from time to time). Further, the State Level Co-ordination Committees (SLCC) is convened by the Reserve Bank in all the States/UTs on quarterly basis. The SLCC is now chaired by the Chief Secretary/ Administrator of the concerned State/UT and has, as its members, apart from the Reserve Bank, the Regional Directorate of the MCA/ ROC, local unit of SEBI, NHB, Registrar of Chits, ICAI, Economic Intelligence Unit of the State Police and officials from Law and Home Ministries of the State Government. As all the relevant financial sector regulators and enforcement agencies participate in the SLCC, it is possible to quickly share the information and agree on an effective course of action to be taken against entities indulging in unauthorized and suspect businesses involving funds mobilization from public.

FAQs on Non-Banking Financial Companies

Inter-corporate deposits (ICDs)

Domestic Deposits

II. Deposits of Non-Residents Indians (NRIs)

Retail Direct Scheme

Know Your Customer (KYC) related queries

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Procedure for submission of the FLA return

Ans: Any query regarding filling of FLA return should be sent by email. We will revert back to you within one or two working days.

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

National Common Mobility Card (NCMC) issued by Paytm Payments Bank

Government Securities Market in India – A Primer

"When, as and if issued" (commonly known as ‘When Issued’) security refers to a security that has been authorized for issuance but not yet actually issued. When Issued trading takes place between the time a Government Security is announced for issuance and the time it is actually issued. All 'When Issued' transactions are on an 'if' basis, to be settled if and when the actual security is issued. RBI vide its notification FMRD.DIRD.03/14.03.007/2018-19 dated July 24, 2018 has issued When Issued Transactions (Reserve Bank) Directions, 2018 applicable to ‘When Issued’ transactions in Central Government securities.

Both new and reissued Government securities issued by the Central Government are eligible for ‘When Issued’ transactions. Eligibility of an issue for ‘When Issue’ trades would be indicated in the respective specific auction notification. Participants eligible to undertake both net long and short position in ‘When Issued’ market are (a) All entities which are eligible to participate in the primary auction of Central Government securities,(b) However, resident individuals, Hindu Undivided Families (HUF), Non-Resident Indians (NRI) and Overseas Citizens of India (OCI) are eligible to undertake only long position in ‘When Issued’ securities. (c) Entities other than scheduled commercial banks and Primary Dealers (PDs), shall close their short positions, if any, by the close of trading on the date of auction of the underlying Central Government security.

When Issued transactions would commence after the issue of a security is notified by the Central Government and it would cease at the close of trading on the date of auction. All ‘When Issued’ transactions for all trade dates shall be contracted for settlement on the date of issue. When Issued’ transactions shall be undertaken only on the Negotiated Dealing System-Order Matching (NDS-OM) platform. However, an existing position in a ‘When Issued’ security may be closed either on the NDS-OM platform or outside the NDS-OM platform, i.e., through Over-the-Counter (OTC) market. The open position limits are prescribed in the directions. All NDS-OM members participating in the ‘When Issued’ market are required to have in place a written policy on ‘When Issued’ trading which should be approved by the Board of Directors or equivalent body.

"Short sale" means sale of a security one does not own. RBI vide its notification FMRD.DIRD.05/14.03.007/2018-19 dated July 25, 2018 has issued Short Sale (Reserve Bank) Directions, 2018 applicable to ‘Short Sale’ transactions in Central Government dated securities. Banks may treat sale of a security held in the investment portfolio as a short sale and follow the process laid down in these directions. These transactions shall be referred to as ‘notional’ short sales. For the purpose of these guidelines, short sale would include 'notional' short sale.

Entities eligible to undertake short sales are (a) Scheduled commercial banks, (b) Primary Dealers, (c) Urban Cooperative Banks as permitted under circular UBD.BPD (PCB). Circular No.9/09.29.000/2013-14 dated September 4, 2013 and (d) Any other regulated entity which has the approval of the concerned regulator (SEBI, IRDA, PFRDA, NABARD, NHB). The maximum amount of a security (face value) that can be short sold is (a) for Liquid securities: 2% of the total outstanding stock of each security, or, ₹ 500 crore, whichever is higher; (b) for other securities: 1% of the total outstanding stock of each security, or, ₹ 250 crore, whichever is higher. The list of liquid securities shall be disseminated by FIMMDA/FBIL from time to time. Short sales shall be covered within a period of three months from the date of transaction (inclusive of the date). Banks undertaking ‘notional’ short sales shall ordinarily borrow securities from the repo market to meet delivery obligations, but in exceptional situations of market stress (e.g., short squeeze), it may deliver securities from its own investment portfolio. If securities are delivered out of its own portfolio, it must be accounted for appropriately and reflect the transactions as internal borrowing. It shall be ensured that the securities so borrowed are brought back to the same portfolio, without any change in book value.

Foreign Investment in India

Indian Currency

B) Banknotes

In terms of Section 33 of the RBI Act, 1934, all banknotes issued by RBI are backed by assets such as gold coin, gold bullion, foreign securities, rupee coin and rupee securities.

Core Investment Companies

B. Registration and related matters:

Ans: Yes, CICs presently registered with the Bank but fulfilling the criteria for ‘Unregistered CICs’ as defined under para 6 of the Master Direction DoR(NBFC).PD.003/03.10.119/2016-17 date August 25, 2016 can seek voluntary deregistration. Both audited balance sheet and auditor’s certificate are required to be submitted for the purpose.

Portfolio Investment Positions (PIP) by Counterpart Economy (formerly CPIS) – India

Some important definitions and concepts

Ans: Debt securities with original maturity of more than one year is classified as long-term debt securities. These include bonds, debentures, and notes that usually give the holder the unconditional right to a fixed cash flow or contractually determined variable money income.

All you wanted to know about NBFCs

C. Definition of deposits, Eligible / Ineligible Institutions to accept deposits and Related Matters

No. Proprietorship and partnership concerns are un-incorporated bodies. Hence, they are prohibited under the RBI Act 1934 from accepting public deposits. Such unincorporated entities, if found accepting public deposits, are liable for penal action under the Act.

FAQs on Non-Banking Financial Companies

Mutual benefit financial companies (nidhis)

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Procedure for submission of the FLA return

Ans: Please follow the below given step to revise the FLA return for a previous year:

Visit https://flair.rbi.org.in/fla/faces/pages/login.xhtml → Login to FLAIR → Click on MENU tab on the left-hand side of the homepage → ONLINE FLA FORM → FLA ONLINE FORM → “Please click here to get the approval to fill revised FLA form for current year after due date /previous year” → select "Year" and click on  → Click “Request”.

→ Click “Request”.

Your request status will be visible in the table below available on the screen. After sending request to RBI through FLA portal, entities need to wait for at least one working day for approval. Entities can check the status of their request in “Multiple Year Enable Screen” under menu on the left corner. Once approved by DSIM, RBI, the entity can revise FLA return for selected year.

Domestic Deposits

II. Deposits of Non-Residents Indians (NRIs)

Retail Direct Scheme

Nomination related queries

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

Merchants using Paytm Payments Bank to receive payments

Government Securities Market in India – A Primer

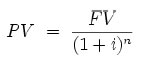

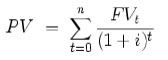

The time value of money functions related to calculation of Present Value (PV), Future Value (FV), etc. are important mathematical concepts related to bond market. An outline of the same with illustrations is provided in Box II below.

| Time Value of Money Money has time value as a Rupee today is more valuable and useful than a Rupee a year later. The concept of time value of money is based on the premise that an investor prefers to receive a payment of a fixed amount of money today, rather than an equal amount in the future, all else being equal. In particular, if one receives the payment today, one can then earn interest on the money until that specified future date. Further, in an inflationary environment, a Rupee today will have greater purchasing power than after a year. Present value of a future sum The present value formula is the core formula for the time value of money. The present value (PV) formula has four variables, each of which can be solved for: Present Value (PV) is the value at time=0  The cumulative present value of future cash flows can be calculated by adding the contributions of FVt, the value of cash flow at time=t  An illustration Taking the cash flows as;

Assuming that the interest rate is at 10% per annum; The discount factor for each year can be calculated as 1/(1+interest rate)^no. of years The present value can then be worked out as Amount x discount factor The PV of ₹100 accruing after 3 years:

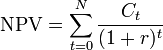

The cumulative present value = 90.91+82.64+75.13 = ₹ 248.69 Net Present Value (NPV) Net present value (NPV) or net present worth (NPW) is defined as the present value of net cash flows. It is a standard method for using the time value of money to appraise long-term projects. Used for capital budgeting, and widely throughout economics, it measures the excess or shortfall of cash flows, in present value (PV) terms, once financing charges are met. Formula Each cash inflow/outflow is discounted back to its present value (PV). Then they are summed. Therefore  Where In the illustration given above under the Present value, if the three cash flows accrues on a deposit of ₹ 240, the NPV of the investment is equal to 248.69-240 = ₹ 8.69 |

Foreign Investment in India

Answer: There are no restrictions under FEMA for investment in Rights shares issued at a discount by an Indian company under the provisions of the Companies Act, 2013. The offer on rights basis to the persons resident outside India shall be:

-

in case of shares of a company listed on a recognized stock exchange in India, at a price, as determined by the company; and

-

in case of shares of a company not listed on a recognized stock exchange in India, at a price, which is not less than the price at which the offer on right basis is made to resident shareholders.

റിസർവ് ബാങ്ക് ഓഫ് ഇന്ത്യ മൊബൈൽ ആപ്ലിക്കേഷൻ ഇൻസ്റ്റാൾ ചെയ്ത് ഏറ്റവും പുതിയ വാർത്തകളിലേക്ക് വേഗത്തിലുള്ള ആക്സസ് നേടുക!

ഞങ്ങളുടെ ആപ്പ് ഇൻസ്റ്റാൾ ചെയ്യാൻ QR കോഡ് സ്കാൻ ചെയ്യുക