IST,

IST,

Global Banking Developments

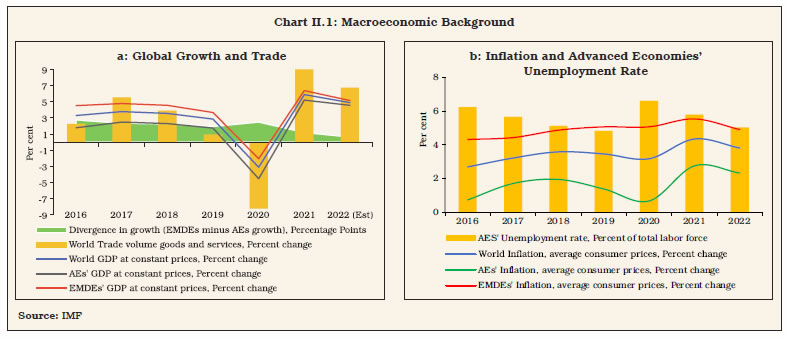

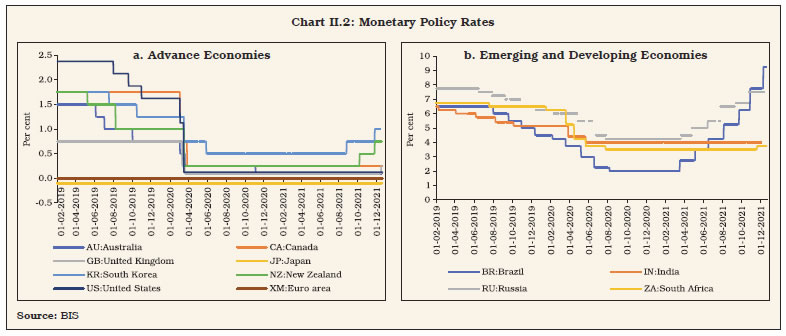

The financial sector remained largely resilient and robust during the pandemic on the back of strong policy support. High capital buffers and lower leverage enabled global banks to provide credit and other critical services to the real sector. The asset quality of the top 100 banks recorded marginal deterioration. Going forward however, as policy support is phased out, banks need to remain vigilant to mitigate stress and emerge stronger. 1. Introduction II.1 The global economy is recovering haltingly amidst renewed surges of the pandemic in some jurisdictions. Taking note of some loss of pace in the second half of 2021, the International Monetary Fund (IMF) revised downwards its global growth forecast for the year to 5.9 per cent1, citing supply chain bottlenecks and rising energy prices as downside risks. The macroeconomic outlook for advanced economies (AEs) and emerging market and developing economies (EMDEs) is diverging, reflecting differentials in infections and vaccination (Chart II.1a). Going forward, this gap could narrow with higher vaccination rates. As on December 25, 2021 about 57.4 per cent of the world’s population had received at least one dose of the vaccine, of which 48.3 per cent were fully vaccinated.2 The pace of the global recovery is also contingent on policy support. While AEs provided substantial fiscal support in 2020 and intend to extend it beyond 2021, fiscal stimuli have either expired or scheduled to end shortly in EMDEs. Some AEs have started monetary policy tapers3 in some form, while EMDEs have been compelled to tighten monetary policy aggressively in the face of elevated inflation risks (Chart II.1b). II.2 Producer price inflation (PPI) is in double digits in the euro area and at 8.0 per cent or more in Japan and the US. Producers have started passing on price increases to the retail level, and as a consequence, CPI inflation is rising rapidly across jurisdictions, reaching 6.8 per cent in the US in November 2021, the highest level in nearly 40 years. In other AEs and EMDEs too, inflation is either above or testing tolerance thresholds. The jury is still out on whether the inflationary pressures are going to be ‘temporary’ or ‘persistent’. II.3 Some AEs, including New Zealand, South Korea and the UK, and some EMDEs namely Brazil, Chile, Hungary, Mexico, Russia, Sri Lanka and Uruguay, have begun raising monetary policy rates to curb price pressures emerging from pent-up demand and supply chain bottlenecks colliding (Chart II.2a and b). Canada has halted its quantitative easing programme (QE).  II.4 The outlook for 2022 remains uncertain and slanted to the downside with the sporadic resurgence of infections from new variants of the coronavirus outweighing the upsides. The IMF projects global growth to slow down to 4.9 per cent and global trade volume to moderate to 6.7 per cent in 2022 from 9.7 per cent in 2021. II.5 The rest of this chapter presents the global banking developments during the period under review in section 2, drawing information from a variety of sources including the IMF, the Bank for International Settlements (BIS) and the Financial Stability Board (FSB). Section 3 evaluates the performance of global banks in terms of credit growth, asset quality, capital buffers and leverage. The performance of the world’s top 100 largest banks ranked by their tier-I capital is covered in Section 4. Section 5 concludes the chapter with what lies ahead for the global banking sector.  2. Global Banking Policy Developments II.6 Recognising the exceptional circumstances brought on by the pandemic, which prompted many regulators and supervisors to use existing flexibilities in the framework to provide regulatory relief, the implementation dates of Basel III standards (finalised in December 2017), the revised Pillar 3 disclosure requirements (finalised in December 2018), and the revised market risk framework (finalised in January 2019) have been deferred by one year to January 1, 20234. They will now be phased in over five years. Meanwhile, progress has been made in the implementation of those Basel III standards, for which agreed timelines continue to apply. II.7 The framework for other aspects of financial reforms such as those pertaining to too-big-to-fail (TBTF), making derivatives markets safer, and promoting resilient non-banking financial institutions (NBFIs) are in place and their implementation is underway. During the pandemic, the focus has shifted to understanding new sources of vulnerabilities5. Building Resilient Financial Institutions II.8 All 27 member jurisdictions have already implemented Basel standards viz., risk-based capital rules, liquidity coverage ratio (LCR), and capital conservation buffers (CCoB) as at end-May 2020. All jurisdictions have final rules in place for implementing the countercyclical capital buffer (CCyB)6. There have been eleven new adoptions in respect of the capital standards, four new adoptions of the net stable funding ratio (NSFR)7, and seven adoptions pertaining to disclosure norms. In respect of Basel III standards which have a deadline in future, there were new adaptors of ‘revised operational risk framework’8 and revised standardised approach for credit risk9. II.9 As at end-September 2021, twenty-six jurisdictions (except for Australia) have enforced the leverage ratio. As regards the systemically important banks, while all members that are home jurisdictions for global systemically important banks (G-SIBs) have final rules in force, twenty-six members have implemented final rules for domestic systemically important banks (D-SIBs). II.10 As alluded earlier, four new jurisdictions adopted the NSFR under liquidity standards in the last year. In addition, twenty-two jurisdictions have enforced final rules pertaining to ‘monitoring tools for intra-day liquidity management’10. A majority of the members (ranging between 22 and 26) have either enforced final rules or published draft rules for the leverage ratio, the standardised approach for measuring counterparty credit risk (SACCR), the supervisory framework for measuring and controlling large exposures (LEX), monitoring tools for intra-day liquidity management, margin requirements for non-centrally cleared derivatives (NCCDs), a revised securitisation framework, capital requirements for equity investments in funds and the revised Pillar 3 disclosure requirements11. II.11 There is, however, limited progress in the implementation of other Basel III standards for which deadlines have passed. These include interest rate risk in the banking book (IRRBB)12; capital requirements for bank exposures to central counterparties13; total loss absorbing capacity (TLAC) holdings14; margin requirements for non-centrally cleared derivatives15 and the revised Pillar 3 framework16. II.12 Almost all G-SIB home and key host jurisdictions have in place comprehensive bank resolution regimes that align with the FSB Key Attributes17. Implementation of the Key Attributes is still incomplete in some other FSB jurisdictions. State support for failing banks has continued. Substantial work remains to be done to operationalise resolution plans for systemically important banks18 and implement effective resolution regimes for insurers and central counterparties (CCPs)19. Work is also ongoing at the international level to enhance CCP resilience, recovery and resolution, and to make trade reporting truly effective; to strengthen governance standards to reduce misconduct risks; to address the decline in correspondent banking; to analyse implications of FinTech for financial stability, financial innovations, payments systems, cyber resilience and market fragmentation. Uncertainty remains around the resolvability of CCPs given their systemic role in the financial system. Challenging and important ongoing work to assess the need for international policy on the use, composition and amount of CCP financial resources in recovery and resolution is being urgently pursued20. Too-big-to-fail (TBTF) reforms II.13 In March 2021, the FSB examined the extent to which the TBTF reforms are working as intended21. Specifically, the evaluation focused on (i) whether the reforms are reducing systemic and moral hazard risks associated with SIBs; and (ii) broader effects (positive or negative) of the reforms on the financial system. The social benefits of TBTF reforms are measured in terms of reduced probability and severity of the financial crisis, while the social costs of the reforms are measured via increases in the cost of bank credit. The evaluation found that too-big-to-fail (TBTF) reforms have made banks more resilient and resolvable and have produced net benefits to society. It also identified gaps to be addressed. As non-bank financial institutions have gained market share, some risks have moved outside the banking system. There is also scope for improving public disclosures of information relating to resolution frameworks and funding mechanisms. II.14 Cross border payments is another area of focus that faces challenges of speed, cost, access and transparency. To address these challenges, a roadmap has been developed by the FSB in coordination with the Committee on Payments and Market Infrastructures (CPMI) and other relevant international organisations and standard-setting bodies22. As part of the roadmap, the FSB has proposed specific targets to be achieved in terms of improvement across all four areas by the end of 2027 through the actions taken under 19 building blocks23. Making Derivatives Markets Safer24 II.15 Overall implementation of the G20’s over-the-counter (OTC) derivatives reforms is well advanced, but there has been incremental progress since October 2020 across FSB member jurisdictions. Progress is monitored along six indicators, namely, (i) trade reporting requirements, (ii) interim capital requirements for non-centrally cleared derivatives (NCCDs), (iii) platform trading, (iv) mandatory central clearing, (v) margin requirements for NCCDs, and (vi) final capital requirements for NCCDs. Trade reporting requirements for OTC derivatives transactions and interim capital requirements for non-centrally cleared derivatives are in place in 23 FSB jurisdictions. Platform trading requirements are in force in 13 jurisdictions while 17 jurisdictions already have comprehensive standards for mandatory central clearing requirements. Fifteen jurisdictions have rules in force for final capital requirement for NCCDs. Sixteen jurisdictions have implemented the final rules for margin requirement for NCCDs. Promoting Resilient Non-Bank Financial Intermediation (NBFI) II.16 The implementation of non-bank financial intermediation (NBFI) reforms is underway but it is at an earlier stage than other reforms25. The FSB and standard-setting bodies (SSBs) have extended implementation deadlines for certain reforms in order to provide additional capacity for firms and authorities to respond to the pandemic shock. FSB together with other SSBs, is working to enhance the resilience of the NBFI sector while preserving its benefits, building on the lessons from the March 2020 market turmoil. Key work undertaken in this area includes policy proposals to enhance the resilience of money market funds (MMFs); addressing liquidity mismatches in open ended funds (OEFs); examining the frameworks and dynamics of margin calls in centrally cleared and non-centrally cleared derivatives. Phasing out of London Inter-bank Offered Rate (LIBOR) II.17 Interest rate benchmarks play a key role in global financial markets. In 2014, in response to cases of attempted manipulation and also declining liquidity in key interbank unsecured funding markets, the FSB made recommendations to reform interbank offered rates (IBORs), working in coordination with national authorities to set out a globally consistent roadmap that encourages firms to stop the use of LIBOR and identify alternative benchmarks. In October 2020, the FSB published a global transition roadmap, which sets out a timetable of actions for financial and non-financial sector firms to take in order to ensure a smooth transition out of LIBOR by end-2021. In March 2020, the UK Financial Conduct Authority (FCA) and Intercontinental Exchange (ICE) Benchmark Administration (IBA) have announced that the one-week and two-month U.S. dollar (USD) LIBOR settings will cease to be published immediately after December 31, 2021. The publication of overnight and one-, three-, six-, and 12-month USD LIBOR settings will, however, be extended till June 30, 2023 providing additional time to wind down or renegotiate existing contracts. The Office of the Comptroller of the Currency (OCC), the US Federal Reserve and the Federal Deposit Insurance Corporation (FDIC) in a joint statement have encouraged supervised institutions to cease entering into new contracts that use USD LIBOR as a reference rate as soon as practicable, but no later than December 31, 2021. Climate-Related Financial Disclosures II.18 With increased frequency and intensity of natural disasters, global attention has now shifted to climate change related risks to financial stability26 (Box II.1). Traditional risk assessments are inadequate to capture these uncertainties. The FSB’s 2015 Task Force on Climate-related Financial Disclosures (TCFD) finalised its recommendations in 201727. These recommendations are being voluntarily implemented. The fourth status report on adoption of the recommendations of the TCFD (October 14, 2021) indicated that disclosure of climate related financial information has steadily increased. However, significant progress is still needed, as on an average only one in three of the companies reviewed disclosed climate-related information aligned with the TCFD recommendations28. The International Financial Reporting Standards (IFRS) Foundation is establishing an International Sustainability Standards Board (ISSB) to develop a baseline global sustainability reporting standard, built from the TCFD framework and the work of an alliance of sustainability standard setters. It also highlighted the need for improving the level of disclosures for greater consistency and comparability. However, a shortage of data to measure financial institutions’ exposures to climate-related risks appears to be the major constraint and various international organisations and SSBs are working to address them.

II.19 In October 2021, the FSB presented to the G20 a comprehensive roadmap for addressing climate related financial risks for firm-level disclosures. The roadmap provides the raw material for the diagnosis of climate-related vulnerabilities. The FSB also provided the G20 another report on ways to promote consistent, high-quality climate disclosures in line with the recommendations of the TCFD. Role of Central Bank Digital Currency (CBDC) and cross border transactions II.20 Over the past decade, cross-border correspondent banking29 has withered, with the number of correspondent banks declining by about 20 per cent during 2011-1830. These banks withdrew more from countries where governance and controls on illicit financing were poor. The retreat of correspondent banks might hurt financial inclusion, raise the cost of cross-border payments or drive them underground. II.21 Several central banks are rapidly moving towards developing central bank digital currencies (CBDCs)31. The design elements and policy decisions for CBDC are complex and require to be resolved. Introduction of the CBDC has a potential to enhance the efficiency of cross border payments and may provide an alternative to correspondent banks, going forward. The BIS Innovation Hub, along with the central banks of Hong Kong. Thailand, China and UAE is working towards building a prototype platform, called “mBridge”. This co-creation project explores the capabilities of distributed ledger technology (DLT) and studies the application of CBDC in enhancing financial infrastructure to support multi-currency cross-border payments. The results of the phase 2 prototype, published in April 2021, demonstrated the potential of using digital currencies and DLT for delivering real-time, cheaper and safer cross-border payments and settlements. The platform was able to complete international transfers and foreign exchange operations in seconds, as opposed to several days normally required, and operates in a 24/7 basis. The cost of such operations to users can also be reduced by up to half. The BIS has, however, warned that the benefits are contingent on meeting the “Hippocratic Oath for CBDC design”, as highlighted by the Group of central banks (2020). Lessons learned from the Pandemic II.22 Although the financial sector remained largely resilient and robust during the pandemic, the FSB observed that banks were somewhat hesitant to dip into their buffers, despite the flexibility embedded in the regulatory framework and using the flexibility inherent in the expected credit loss framework to extend credit. II.23 Fiscal and monetary support measures helped in reducing banks’ funding costs and lending rates. Prolonging support, however, risks delaying the recognition of losses, increasing provisions and tightening lending standards to preserve capital. Policymakers attempted to enhance banks’ lending capacity through a variety of measures such as restrictions on dividends, share buybacks and bonus payments. Banks’ willingness to lend was incentivised by imparting flexibility in asset classification, restructuring, direct fiscal transfers and loan guarantees, moratoriums on loan payments; prohibitions on foreclosures, funding-for-lending schemes and moral suasion. II.24 The costs and benefits of financial institutions relying heavily on third-party service providers, including on a cross-border basis, became evident during the pandemic. While these dependencies reduce costs, they also add to operational risks. Cyber and data security related issues, in particular, need special attention. II.25 Some non-bank financial segments showed vulnerabilities during the pandemic from liquidity mismatches, leverage and interconnectedness. The FSB’s holistic review laid a comprehensive and ambitious work plan programme and FSB focused on the specific issues such as money market funds (MMFs), open-ended funds, margining practices, liquidity, and cross-border USD funding. II.26 The current high level of corporates and sovereigns’ debt overhang have systemic implications for the EMDEs, especially for the eventual policy exit from extraordinary accommodation. Going forward, this will restrict policy choices available to them while accentuating trade-offs. The flight-for-safety and dash-for-cash behaviour of USD funding markets propagated through actions of few investors and dealers led to unprecedented capital outflow from the EMDEs. As current global regulatory regimes offer little help to safeguard against such shocks, policymakers of these countries will have to be watchful of their developments and devise mechanisms to ring-fence their economies from knee-jerk reactions. 3. Performance of the Global Banking Sector II.27 The COVID-19 pandemic was the first major test of the global financial system since the implementation of reforms following the global financial crisis of 2008. Higher capital, better liquidity profiles and lower leverage in large banks allowed them to cushion, rather than amplify, the macroeconomic shock emanating from the pandemic. The banking system played an active role in ensuring availability of credit and other critical services to the real sector, helped by extraordinary official support. Bank Credit Growth32 II.28 Bank credit to the private non-financial sector contracted sharply in the quarter ending March 2020 with the onset of the pandemic, but revived subsequently, primarily led by the EMEs (Chart II.3a). Among the AEs, Korea and Japan bucked the overall trend and their credit growth remained robust even after the onset of the pandemic. Canada and UK are showing nascent signs of credit growth revival (Chart II.3b). A similar revival is taking root across countries in the Euro Area, except in Greece (Chart II.3c). In EMEs, bank credit is conditioned by country specific macroeconomic circumstances and demand side factors (Chart II.3d). Going forward, bank credit growth is expected to accelerate as economies unlock and vaccinations are ramped up.  Asset Quality II.29 Gauged from the metric of asset quality, banks across AEs showed resilience through the pandemic (Chart II.4a). Non-performing loans (NPL) ratios eased in the two peripheral economies of the Euro-zone, viz., Greece and Portugal mainly due to institutional and government intervention (Chart II.4b). Asset quality of EME banks was showing wide divergences even before the pandemic. Although Russia and India continue to have the highest NPL ratios, their asset quality did not deteriorate during the pandemic, as in other EMEs. The South African banking system has started showing signs of distress (Chart II.4c). Going forward, as recognition standstills are phased out, the accumulated capital buffers may help banks in facing adversities. Bank Profitability II.30 Bank profitability, measured by the return on assets (RoA), generally declined in 2020 as banks’ interest income declined but deposit costs increased. In 2021, banks in Australia, the United Kingdom and Spain are showing signs of improvement in profitability (Chart II.5a). The narrative is less sanguine across EMEs. Indian banks turned profitable in 2020 and continue to clock in profits. (Chart II.5b).   Capital Adequacy II.31 There has been steady progress in the implementation of Basel III norms across jurisdictions, albeit at varying speeds. Banks across systemic AEs and EMEs remained adequately capitalised (Chart II.6a and b). The global banking system weathered the pandemic on the back of stronger capital and liquidity positions that were built up in the wake of the global financial crisis. Leverage Ratio II.32 After showing substantial improvement with the implementation of Basel III norms, the leverage ratio measured in terms of capital to total asset ratio declined across jurisdictions in 2020, indicative of sharper fall in banks’ capital relative to assets. The moderation was evident even in jurisdictions which traditionally have higher leverage ratios such as the US and Indonesia. A BIS survey of 47 large internationally active banks in July 2021, however, showed that leverage ratio33 was not a binding constraint on these banks. (Chart II.7). Financial Market Indicators II.33 Financial markets witnessed a meltdown at the onset of the pandemic. In the first phase from late February to early March 2020, investors exhibited ‘flight to safety’ behaviour as they sold riskier assets. In the second and more acute phase from mid-March onwards, their behaviour turned to ‘dash for cash’. In this phase investors sold risky as well as relatively safe assets in an attempt to obtain cash or cash-like instruments. By late March, the stress eased considerably following speedy, sizeable and sweeping interventions by authorities, and markets progressively returned to orderly conditions. II.34 Bank equity prices indices have largely recovered, but their levels remain less than pre-COVID levels (Chart II.8a). Since June 2021, Indian banks equity prices revived sharply, while Chinese banks’ equity prices have started to drop mainly reflecting concern about its real estate sector.   II.35 Credit Default Swap (CDS) spreads declined from December 2019 through February 2020 and showed higher volatility in March 2020 through June 2020. CDS spreads have generally declined since then and were at pre-pandemic levels. An increase in the CDS spreads is seen in the recent period, however, implying rising risk premiums (Chart II.8b).

II.36 During the pandemic, large banks continued to provide market making functions, notwithstanding some evidence that few market segments experienced illiquidity. Financial market infrastructure (FMI), particularly central counterparties (CCPs), functioned as intended34. At the same time, large banks increased their support to trades and built up their securities holdings across an array of instruments. They have continued to actively trade in derivatives, as evidenced by increases in both the notional and gross market values of derivatives positions from end-2019 to mid-2020 (8.6 per cent and 33.6 per cent, respectively)35. Global Systemically Important Banks (G-SIB) II.37 BIS data available since 2014 suggest that the G-SIB buckets of top 15 global banks, except for three China-based banks, have either shifted to become less risky or have remained steady during the period (Chart II.9). Thus, the regulatory push requiring G-SIBs to maintain higher capital seems to have nudged them to reduce complexity, cross jurisdictional presence, interconnectedness, size and substitutability of their operations. II.38 Bank resilience and market discipline were tested by the pandemic. Banks’ risk-based capital and leverage ratios improved, including those of SIBs. Most G-SIBs’ TLAC debt issuances to replace maturing ineligible debt were absorbed by the markets without difficulty. Profitability of SIBs, particularly G-SIBs, have fallen relative to other banks as cross-border lending continued to expand.   Top 100 Largest Banks36 II.39 Ranked by Tier-I capital, China (19), the US (12) and Japan (7) had the largest number of top 100 in December 2020 (Chart II.10a). While nearly 68 per cent of the total assets (in US dollar terms) were held by banks in the AEs, nearly 29 per cent of the total assets were held by banks in China and the rest by the other EMDE countries (Chart II.10b). II.40 There was a marginal deterioration in the asset quality of the top 100 banks. The number of banks with non-performing loans (NPLs) in three categories viz. greater than 5 per cent, between 2 to 3 per cent and 1 to 2 per cent increased (Chart II.11a). However, the capital adequacy of banks remained comfortable, with 69 of the banks having capital to risk weighted assets (CRAR) ratios greater than 16 per cent in 2020, up from 51 banks in 2019 (Chart II.11b).   II.41 There was no significant change in leverage ratios (capital to assets ratio), with 69 per cent of banks having leverage ratios in the range of 4 to 8 per cent. Five banks, two in France and one each in Germany, Denmark, and Japan, had leverage ratios below 4 per cent (Chart II.12a). There was marginal deterioration in the return on assets (RoA). While four banks reported negative RoA, seventy-nine banks posted RoA less than 1 per cent, and 13 banks posted RoA between 1 to 2 per cent (Chart II.12b). II.42 With the gradual recovery of global economic activity and trade boosted by the easing of restrictions across jurisdictions, the impact of pandemic on the global banking sector is turning out to be muted, mainly due to asset quality standstills in many jurisdictions as well as continuation of strong policy support. Going forward however, as policymakers phase out their support, stress on banking sectors may come to the fore. The areas that are likely to be most impacted by the pandemic are asset quality and profitability. High capital buffers have strengthened balance sheets of banks following implementation of Basel III norms which may help banks to manage stress and emerge stronger. 1 International Monetary Fund (2021). ‘World Economic Outlook: Recovery during a Pandemic- Health Concerns, Supply Disruptions, and Price Pressures’ Washington, DC, October. Available at https://www.imf.org/en/Publications/WEO, 2 Source: https://ourworldindata.org/covid-vaccinations# 3 On December 15, 2021, the US Federal Reserve decided to reduce the monthly pace of its net asset purchases by $20 billion for Treasury securities and $10 billion for agency mortgage-backed securities. 4 In March 2020, the Group of Central Bank Governors and Heads of Supervision endorsed a set of measures to provide additional operational capacity for banks and supervisors to respond to the financial stability priorities resulting from the impact of COVID19 on the global banking system. 5 FSB (2021). Implementation and Effects of the G20 Financial Regulatory Reforms. Available at https://www.fsb.org/wp-content/uploads/P131120-1.pdf 6 Source: BIS (2021), Progress Report on Adoption of the Basel Regulatory Framework. Available at https://www.bis.org/bcbs/publ/d525.htm. 7 Japan, Mexico, Switzerland and the UK. 8 Indonesia, Mexico and Russia. 10 China, Japan and Korea have not adopted the rules, while Canada has published the final rules but is yet to be implemented by banks. 11 The adoption of securitisation framework is yet to commence in India, while the implementation of margin requirement for non-centrally cleared derivatives (NCCDs) is in progress. 12 Australia, India, Mexico, Russia, South Africa, and Turkey are yet to issue rules and U.K. is yet to enforce the rules. 13 India issued final rules in 2016. Jurisdictions yet to do so include China, Indonesia, Mexico, Russia and Turkey. 14 China, India, Korea, South Africa and Turkey are yet to issue final guidelines. 15 Argentina, China, Indonesia, India, Mexico, Turkey and Russia are yet to issue final rules. 16 Australia, China, India and U.S. are yet to issue draft rules, while Indonesia, Mexico, U.K. have moved towards only partial implementation. 17 FSB (2011), Key Attributes of Effective Resolution Regimes for Financial Institutions. Available at https://www.fsb.org/wp-content/uploads/r_111104cc.pdf 18 The level of compliance with the BCBS Principles on risk data aggregation and risk reporting is still to be improved. 19 The powers most often lacking are bail-in and to impose a temporary stay on the exercise of early termination rights. 20 FSB (2021), “Glass half-full or still half-empty?” Available at https://www.fsb.org/wp-content/uploads/P071221.pdf 21 FSB (2021). ‘Evaluation of the effects of too-big-to-fail reforms’. Available at https://www.fsb.org/2021/03/evaluation-of-the-effects-of-too-big-to-fail-reforms-final-report/. 22 FSB (2020). Enhancing Cross-border Payments: Stage 3 roadmap. Available at https://www.fsb.org/wp-content/uploads/P131020-1.pdf 23 FSB(2021), Targets for Addressing the Four Challenges of Cross-Border Payments. Available at https://www.fsb.org/wp-content/uploads/P310521.pdf 24 FSB (2021), OTC Derivatives Market Reforms: Implementation progress in 2021. Available at https://www.fsb.org/wp-content/uploads/P031221.pdf 25 Implementation of the FSB policy recommendations for securities financing transactions continues to face significant delays in some jurisdictions. Work is underway to adopt standards and processes on global securities financing data collection and aggregation. Also, Implementation of the FSB and IOSCO recommendations to address structural vulnerabilities from liquidity and leverage in asset management activities is ongoing 26 BIS (2020). The green swan - Central banking and financial stability in the age of climate change. Available at https://www.bis.org/publ/othp31.pdf 27 The aim of the TCFD was ‘to develop a set of voluntary, consistent disclosure recommendations for use by companies in providing information to investors, lenders and insurance underwriters about their climate-related financial risks.’ 28 FSB (2020), The Implications of Climate Change for Financial Stability. Available at https://www.fsb.org/wp-content/uploads/P231120.pdf 29 FSB defines correspondent banking as the provision of banking services by one bank (the “correspondent bank”) to another bank (the “respondent bank”). 30 Rice T, Peter G, and Boar C (2020): ‘On the global retreat of correspondent banks’, BIS Quarterly Review, March. Available at https://www.bis.org/publ/qtrpdf/r_qt2003g.htm 31 BIS (2021): ‘Central bank digital currencies for cross-border payments’. Available at https://www.bis.org/publ/othp38.pdf. 32 Data sourced from the Bank for International Settlements’ (BIS) Total Credit Statistics. Available at https://www.bis.org/statistics/totcredit.htm. 33 In the survey, the leverage ratio is defined as tier I capital to assets ratio, in line with the Basel III norms. However, since comparable data on tier I capital for all jurisdictions is not available, data on a broader concept of capital to assets ratio is analyzed in this sub-section. 34 FSB (2021), Lessons Learnt from the COVID-19 Pandemic from a Financial Stability Perspective. Available at https://www.fsb.org/wp-content/uploads/P281021-2.pdf 35 ISDA (2021), The Role of Financial Markets and Institutions in Supporting the Global Economy During the COVID-19 Pandemic. Available at https://www.isda.org/a/zZzTE/The-Role-of-Financial-Markets-and-Institutions-in-Supporting-the-Global-Economy-During-the-COVID-19-Pandemic.pdf 36 Data sourced from the Banker Database of the Financial Times. |

हे पेज शेअर करा:

भारतीय रिझर्व्ह बँक मोबाईल ॲप्लिकेशन इंस्टॉल करा आणि नवीनतम बातम्यांचा त्वरित ॲक्सेस मिळवा!

आमचे अॅप इंस्टॉल करण्यासाठी QR कोड स्कॅन करा

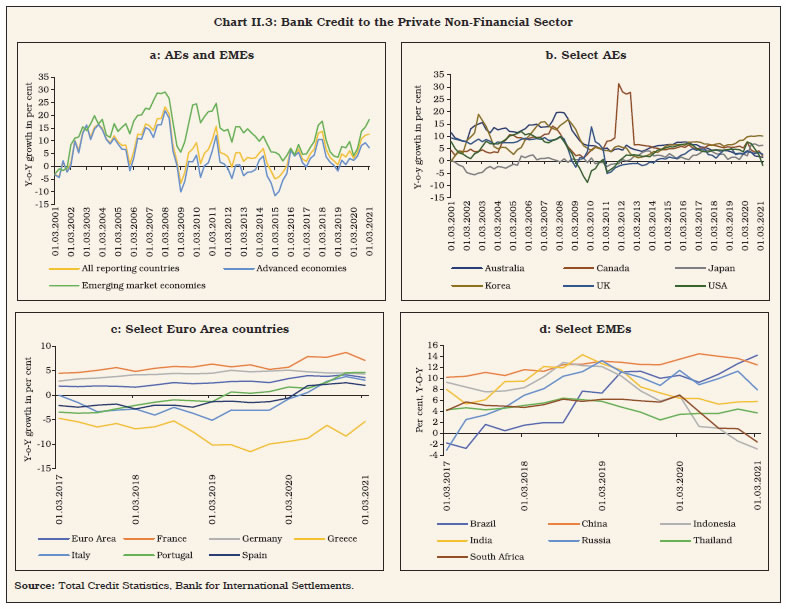

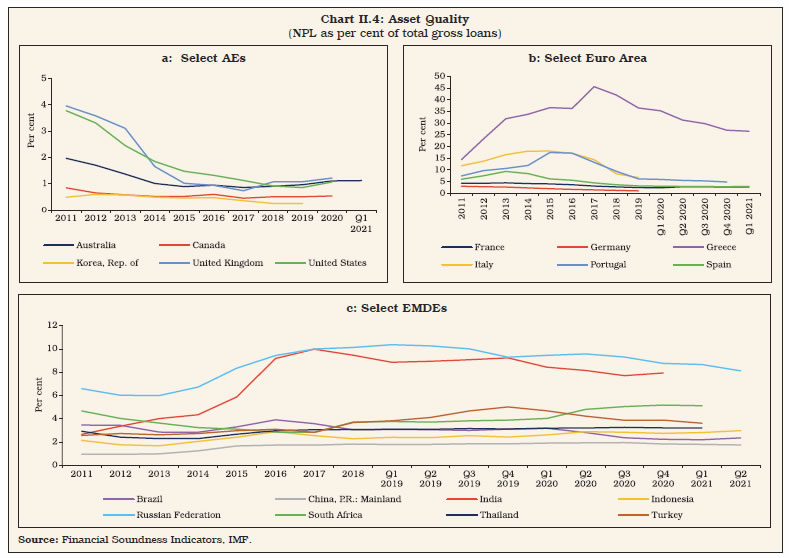

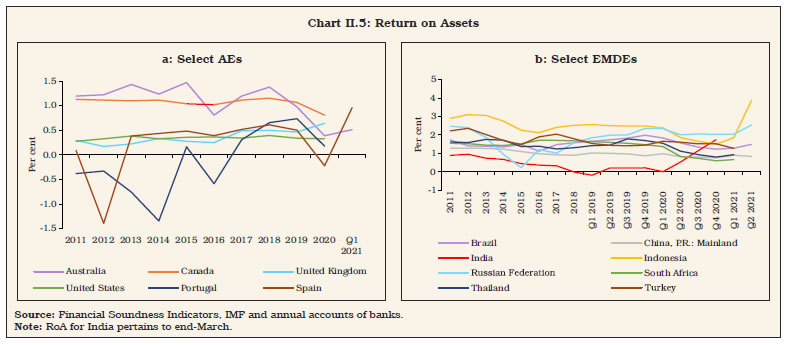

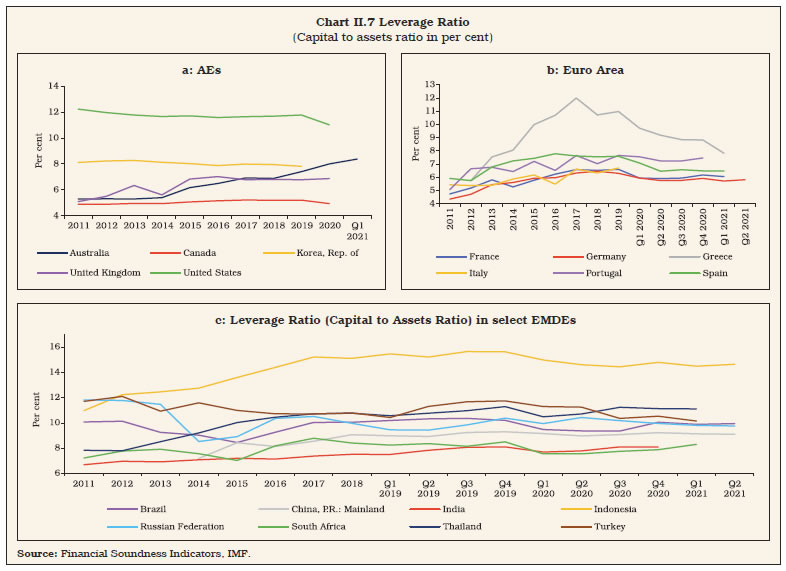

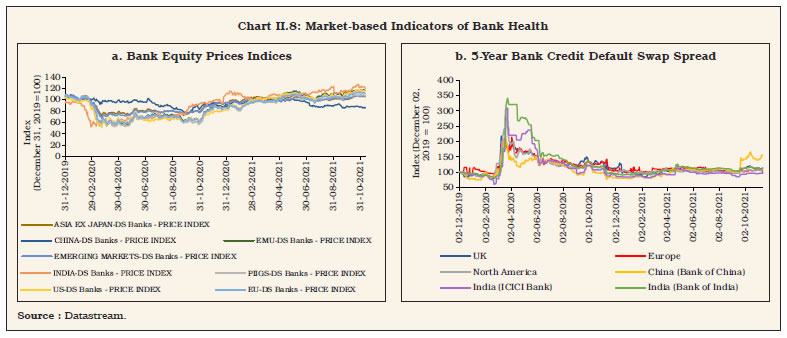

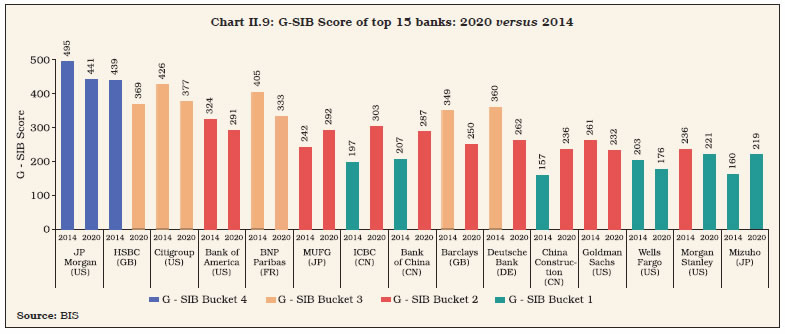

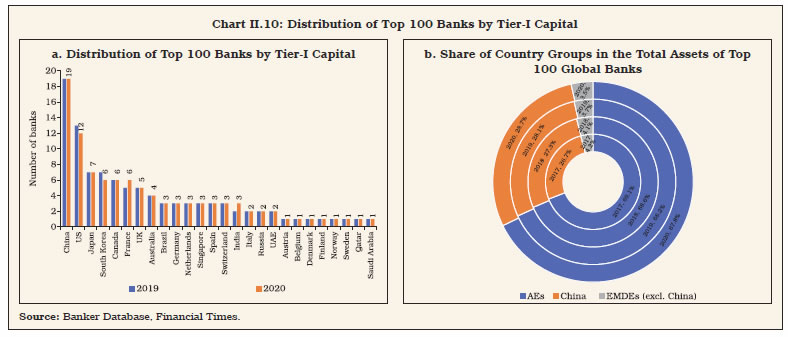

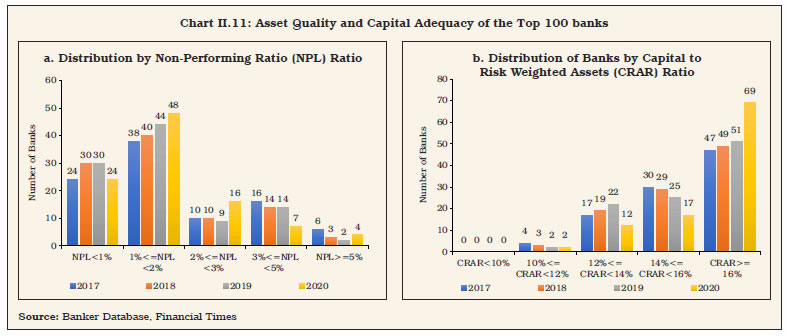

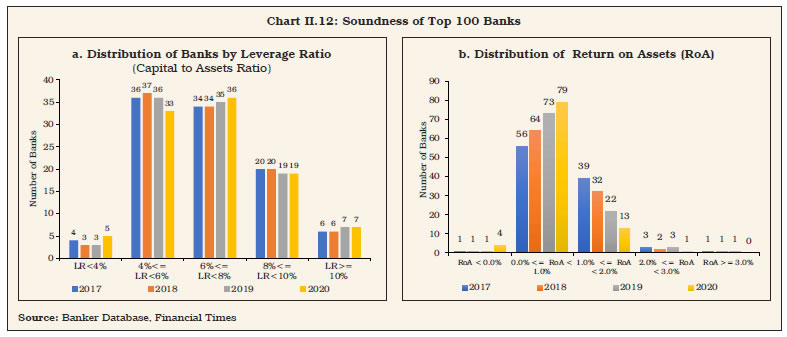

पेज अंतिम अपडेट तारीख: