IST,

IST,

II. Fiscal Position of the State Governments

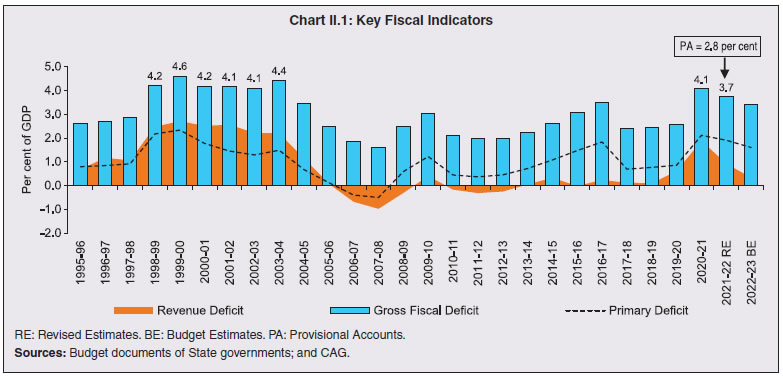

1. Introduction 2.1 The fiscal health of the States bounced back in 2021-22 from a sharp pandemic-induced deterioration in the preceding year. Prudent fiscal management has continued into 2022-23 as reflected in budget estimates (BE). 2.2 This chapter analyses the fiscal performance of States in 2020-21 and 2021-22 as a backdrop to an evaluation of their BE for 2022-23. The rest of this chapter is divided into seven sections. Section 2 presents key fiscal indicators of the State governments. Section 3 and Section 4 analyse revenue and expenditure patterns, respectively. Section 5 throws light on actual fiscal outcomes during 2022-23 so far and the outlook for the remaining part of the year. Section 6 describes the financing pattern of the consolidated fiscal deficit of the States. Section 7 profiles their debt position, including contingent liabilities. Section 8 sets out some concluding observations. 2.3 In 2020-21, States’ consolidated gross fiscal deficit (GFD) rose to 4.1 per cent of gross domestic product (GDP), the highest level since 2004-05 (Chart II.1). The spike, however, was short-lived and a reversion to consolidation was crafted in 2021-22 (PA)1 taking the GFD down to 2.8 per cent of GDP, as against the BE of 3.5 per cent and RE of 3.7 per cent for that year. This correction was brought about by higher-than-expected growth in both tax and non-tax revenues.  2.4 A similar improvement was recorded in their revenue and primary deficits (Table II.1; Annex I). 2.5 For 2022-23, the States have budgeted a consolidated GFD of 3.4 per cent of GDP, which is within the indicative target of 4 per cent2 set by the Centre, albeit, with substantial inter-State variations3 (Table II.2). 2.6 States’ revenue collections declined in 2020-21 on account of the pandemic-induced slump in own tax revenue, non-tax revenue and tax devolution from the Centre (Table II.3). Within own tax revenue, the decline was prominent in the case of States’ goods and services tax (SGST) and vehicle tax. In contrast, their excise collections increased due to an increase in duties on alcohol. Non-tax revenue plummeted in 2020-21, mainly reflecting lower earnings from general services4. Under central transfers, lower tax devolution was broad-based, except for income tax. This was, however, more than offset by a 49 per cent jump in Finance Commission grants5 during the year. 2.7 For 2021-22, States budgeted a sharp rise in revenue receipts led by own tax and non-tax revenues and grants from the Centre. In the RE, however, revenues outperformed BE, with a broad-based recovery in own tax and non-tax revenue, supported by higher tax devolution and grants from the Centre. Yet, unaudited data released by the CAG indicate lower revenue collections than in the revised estimates. In terms of these provisional accounts, the grant component declined in 2021-22. Increasingly over recent years, RE often provide ambiguous signals about the health of State finances (Box II.1).

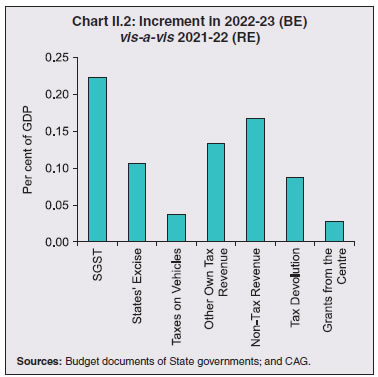

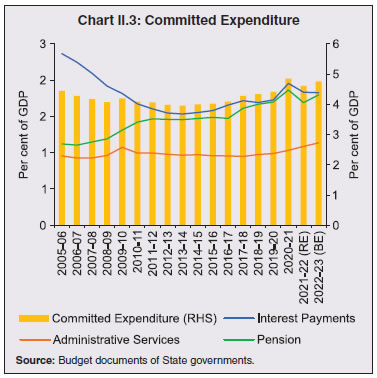

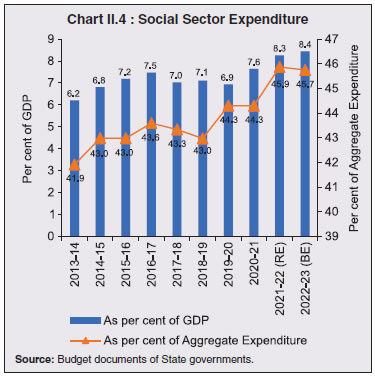

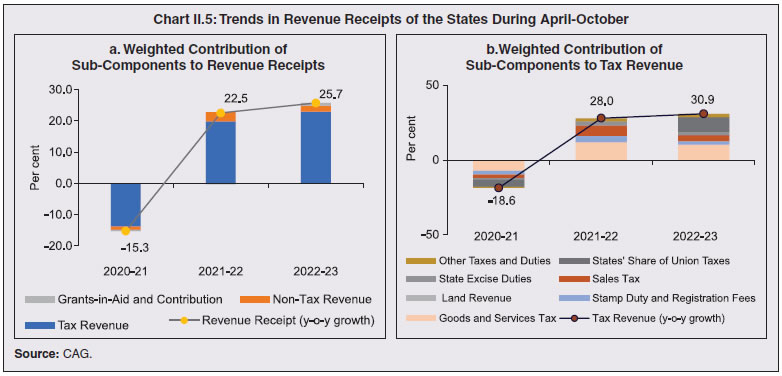

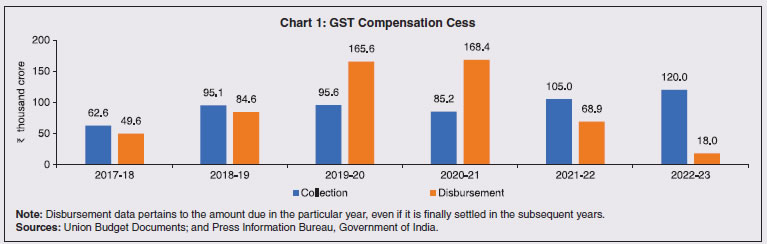

2.8 States have budgeted for higher revenue receipts in 2022-23, driven primarily by SGST, excise duties, and sales tax collections (Chart II.2). Non-tax revenue is also expected to increase, driven by industry and general services. Tax devolution is budgeted to increase on expectations of higher revenue collections by the Centre. 2.9 State governments have initiated various measures to augment their own revenue sources. For instance, Kerala and Rajasthan adopted an amnesty scheme6 in 2020-21 to provide relief to taxpayers as well as to improve their own revenue collections. The scheme, which encompasses various taxes like SGST, stamp and registration duties, motor vehicle tax and excise duties, has been extended to 2022-23. Maharashtra has also introduced the scheme in 2022-23. Punjab has proposed to set up a Tax Intelligence Unit to improve tax compliance under GST. Chhattisgarh is planning to constitute a "Karai Vardhan Cell" for the augmentation of revenue by analysis/ review of taxation acts/rules and tax rates on the basis of data available in the revenue collection departments. Other revenue-generating measures include Assam’s liquidation scheme for payment of arrears, Haryana’s one-time scheme for settlement of old VAT dues, and Assam and Kerala’s Green tax to discourage old vehicles. Additionally, Haryana has taken measures for phased monetization of assets. States have also undertaken specific fiscal reform measures, based on the fifteenth Finance Commission’s (FC-XV) suggestions aimed at improving revenue sources (Annex II). Revenue Expenditure 2.10 States’ revenue expenditure had increased sharply in 2020-21, reflecting the response to the COVID-19 pandemic (Table II.4). Under the developmental head, higher spending was made towards social services such as medical and public health, urban development, relief on account of natural calamities, social security and welfare. Under economic services, higher allocations were provided for rural development, crop husbandry, and transport and communication. Some States also adopted expenditure rationalisation measures like dearness allowance (DA) freeze, deferment of part or full salaries and wages, and deduction from salaries to create fiscal space for accommodating higher expenditure on medical and social services. 2.11 The revenue expenditure of States increased by 20.7 per cent7 in 2021-22 (RE), mainly on account of increase in developmental spending on medical and public health, water supply and sanitation and social security and welfare. 2.12 For 2022-23, States have budgeted an increase in revenue spending, mainly led by non-developmental expenditure such as pension and administrative services. Budget allocations towards medical and public health and natural calamities have been lowered, while housing outlay has been increased. Committed expenditure, comprising interest payments, administrative services and pension, is expected to increase marginally from 2021-22 (RE) (Chart II.3). Social sector expenditure is also budgeted to increase slightly in 2022-23, led by the welfare spending for scheduled castes, scheduled tribes and other backward classes (Chart II.4). Capital Expenditure 2.13 Capital outlay of States recorded a robust growth of 31.7 per cent in 2021-22 (PA). Strong growth in tax and non-tax revenues, coupled with advancement of payment by the Centre of tax devolution and GST compensation, provided the required fiscal space to accelerate capex. The consolidated capital outlay8 of the States is budgeted to grow by 38.4 per cent in 2022-23 (over 2021-22 PA). Accordingly, the capital outlay-GDP ratio is expected to improve from 2.3 per cent in 2021-22 (PA) to 2.9 per cent in 2022-23 (BE).  5. Actual Outcome in 2022-23 So Far and Outlook 2.14 Fiscal parameters of States have remained robust during April-October 20229. GFD and RD declined both in absolute terms, and as a proportion to BE. This was enabled by growth in revenue collections, with SGST and States’ share in the Union taxes being the top contributors (Chart II.5). The upsurge in tax devolution to the States results from a stronger than expected tax mop-up by the Centre due to higher buoyancy in direct tax collections and strong GST, partly on account of rising formalization of the economy. The GST compensation cess ceased from July 2022, even though the GST Council extended the period for the levy of the GST compensation cess up to March 31, 2026, for repaying back-to-back loans taken during the pandemic to meet the shortfall in compensation cess collections. The consolidated GST revenue of the States, comprising SGST and devolution from CGST, however, is budgeted to be higher in 2022-23 (Box II.2). Non-tax revenue of the States continued to grow at a healthy rate albeit at a slower pace than the previous year.

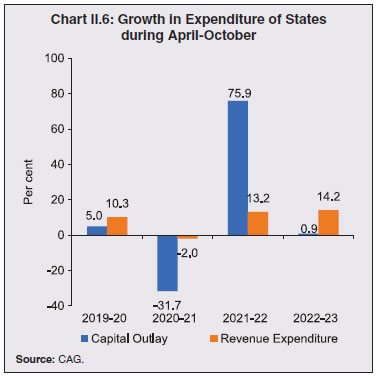

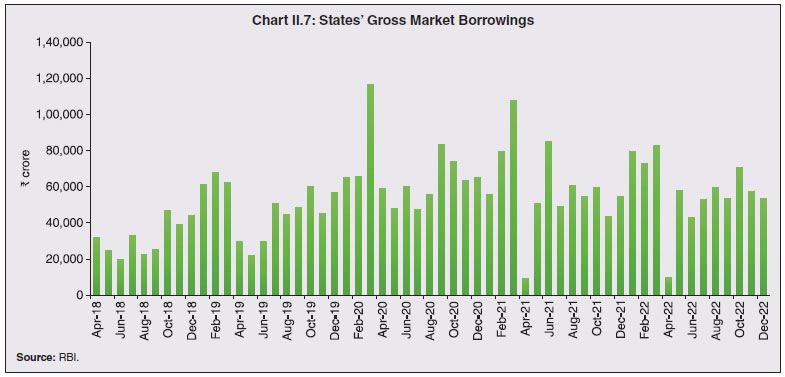

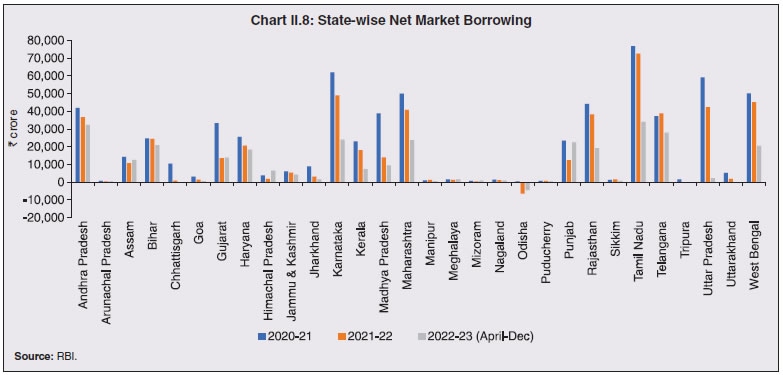

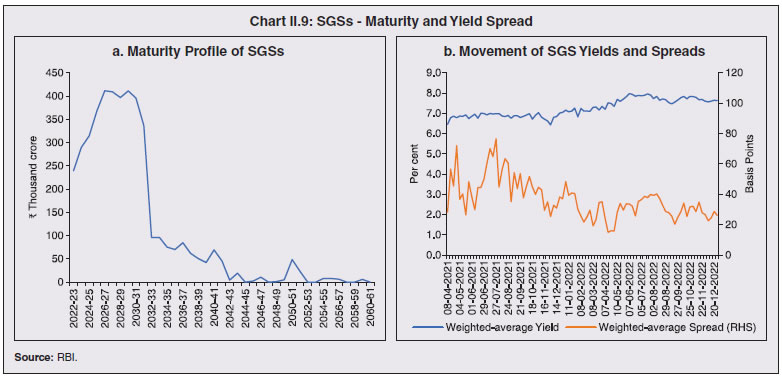

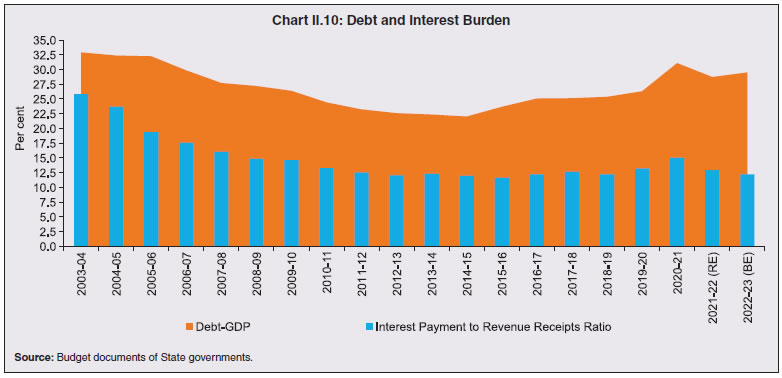

2.15 Revenue spending recorded a growth of 14.2 per cent during April-October 2022 (Chart II.6). The capital outlay of the States registered a y-o-y growth of 0.9 per cent in April-October 2022. This low capital outlay partly reflects the tendency to back-load expenditure in the latter half of the year. The expenditure pattern of States also reveals that they do not always expend the full amount of their budgeted expenditure by the year end, even with sufficient fiscal headroom. 2.16 Despite persisting headwinds, States’ fiscal outlook remains favourable on expectations of high growth in revenue receipts than initial estimates on account of strong GST collections and higher tax devolution. Additionally, capital outlay, which remained muted in initial months, is expected to pick up in H2:2022-23 as States make efforts to meet budgeted capex targets, supported by resource availability through relaxation in the norms for off-budget borrowings12, front-loading of post devolution revenue deficit grants, advance instalments of tax devolution and payment of GST compensation cess. The Centre has already made two advance instalments of tax devolution to the States in August and November. Additionally, the Centre sanctioned ₹77,110 crore13 to States under the Scheme for Special Assistance to States for Capital Investment14. 6. Financing of GFD and Market Borrowing by State Governments and UTs Financing of GFD 2.17 On average, market borrowings financed slightly more than half of the consolidated fiscal deficit of States till 2016-17. States’ dependence on market borrowing has increased significantly following the recommendation of the Fourteenth Finance Commission (FC-XIV) to exclude States from the National Small Savings Fund (NSSF) financing facility (barring Delhi, Madhya Pradesh, Kerala and Arunachal Pradesh). Since 2017-18, the share of market borrowings has increased rapidly and is budgeted to reach 78.1 per cent in 2022-23. Market Borrowings 2.18 The gross market borrowings of States/UTs contracted by 12.2 per cent to ₹7.02 lakh crore in 2021-22 from ₹7.99 lakh crore a year ago. The lower borrowing was partly on account of improved revenue collections by the States. During 2022-23 so far (April-December), the gross market borrowings at ₹4.57 lakh crore have been 1.89 per cent lower than the corresponding period of last year (Chart II.7).  2.19 Similarly, net market borrowings (i.e., gross market borrowings net of repayments) of States and UTs contracted by 24.4 per cent to ₹4.92 lakh crore in 2021-22 from ₹6.52 lakh crore in 2020-21. Net market borrowing was mainly concentrated in a few States like Tamil Nadu, Karnataka, Uttar Pradesh, Maharashtra, Andhra Pradesh and West Bengal (Chart II.8). During 2022-23 so far (up to end-December, 2022), the net market borrowing by the States was ₹3.02 lakh crore. States are expected to raise ₹3.41 lakh crore (gross) during January - March 2023. During the first nine months of 2022-23, the actual market borrowings of the States were much lower than the indicative calendar. For the remaining part of the year, the quantum of issuance by the States is likely to be influenced by the size of monthly tax devolution, the release of the pending GST compensation, the disbursement of interest-free capex loans to States and actual capital spending.  2.20 During 2021-22, the States undertook 608 issuances (of which 60 were re-issuances), compared with 742 issuances (of which 56 were re-issuances) in 2020-21. In line with the policy of passive consolidation15, Haryana, Madhya Pradesh, Maharashtra, Meghalaya, Punjab, Rajasthan and Tamil Nadu undertook re-issuances in 2021-22. During 2022-23 so far (up to end-December, 2022), out of 403 issuances undertaken by States, 37 were re-issuances (Table II.5). 2.21 The issuances in 10-year maturity amounted to 35.1 per cent of the total amount of issuances in 2021-22, lower from 36.3 per cent a year ago. The rest (64.9 per cent) was spread across other maturities. Twenty-one States and two UTs (Puducherry and Jammu and Kashmir) issued securities of various maturities, ranging between 2 and 35 years. Though 63.3 per cent of the outstanding State government securities is in the residual maturity bucket of five years and above (Table II.6), redemption pressure is expected to remain high till 2030-31 (Chart II.9a). 2.22 Yields on State government securities hardened during 2022-23, tracking movements in yields on Central government securities impacted by global spill overs (Chart II.9b). 2.23 In Q1:2021-22, the State Government Securities (SGSs)16 yields hardened, notwithstanding the G-sec acquisition programme (G-SAP) and special open market operations (OMOs) conducted by the Reserve Bank. The release of higher-than-expected CPI inflation figures for May 2021 and the increase in crude oil prices also contributed to the hardening of the SGS yields. Yields softened in Q2:2021-22 due to lower CPI inflation prints for June and July but started hardening again in Q3:2021-22, mainly tracking the unwinding of accommodative monetary policy measures by major central banks and the rise in crude oil prices. Hardening of yields continued during Q4:2021-22 reflecting geo-political risks driving up crude oil and commodity prices and the aggressive policy normalization measures by major central banks. 2.24 Overall, the weighted average (cut-off) yield (WAY) of SGSs issued during 2021-22 stood at 6.98 per cent as compared to 6.55 per cent in the previous year. The weighted average spread of SGS issuances over the corresponding tenor of Central government-dated securities narrowed to 41 bps in 2021-22 as compared to 53 bps in the previous year. The average inter-State spread for 10 years maturity during 2021-22 stood at 4 bps as against 10 bps a year ago. 2.25 During 2022-23 so far (up to December 31, 2022), the WAY of SGSs stood at 7.73 per cent, while the weighted average spread of SGS issuances over the corresponding tenor of Central government dated securities stood at 31 bps. Financial Accommodation to States 2.26 The Reserve Bank offers three short-term liquidity windows – special drawing facility (SDF); ways and means advances (WMA); and overdraft (OD) facilities – to States and two UTs to help them tide over temporary mismatches in cash flows. The aggregate WMA limit for States/UTs was fixed at ₹51,560 crore for the second consecutive year in 2021-22, which was 60 per cent higher than the earlier limit of ₹32,225 crore as on March 31, 2020. The Reserve Bank also relaxed the OD scheme to tide over mismatches in cash flows, increasing the number of days a State/UT can be in OD continuously to 21 working days from 14 working days, and in a quarter to 50 working days from 36 working days, valid till March 31, 2022. On a review of the limits and keeping in view the gradual lifting of COVID-19 restrictions, it was decided to fix the WMA limits and timelines for OD for States/UTs as recommended by the Advisory Committee on Ways and Means Advances to State Governments (Chairman: Shri Sudhir Shrivastava) effective from April 01, 2022. Accordingly, the WMA limit for State Governments/UTs was fixed at ₹47,010 crore.  2.27 The State Governments/UTs can avail of overdraft for 14 consecutive days and be in OD for a maximum number of 36 days in a quarter. Seventeen States/UTs availed the SDF, fourteen States/UTs resorted to WMA, and nine States/UTs availed OD in 2021-22. During 2022-23 so far (April-December), seventeen States have availed SDF, eleven States/UTs resorted to WMA and ten States/UTs availed OD. Cash Management of State Governments 2.28 In recent years, States have been accumulating sizeable cash surpluses in intermediate treasury bills (ITBs) and auction treasury bills (ATBs). Although positive cash balances indicate low intra-year fiscal pressure, they involve a interest rate negative carry, warranting improvement in cash management practices. Outstanding investments of State governments in 14-day ITBs and ATBs stood at ₹2,16,272 crore and ₹87,400 crore, respectively, as on March 31, 2022 as against ₹2,05,230 crore and ₹41,293 crore, respectively, as on March 31, 2021. As on December 31, 2022, the outstanding investments of States in ITBs stood at ₹1,76,208 crore, while their outstanding investments in ATBs stood at ₹1,12,420 crore. States’ Reserve Funds 2.29 It is desirable for States to keep adequate buffers to minimise the fiscal stress arising from redemption pressures and unforeseen liabilities. For this purpose, the States maintain a Consolidated Sinking Fund (CSF) and a Guarantee Redemption Fund (GRF) with the Reserve Bank. The States can also avail SDF at a discounted rate from the Reserve Bank against incremental funds invested in CSF and GRF. So far, twenty-four States and one Union Territory, i.e., Puducherry, have set up CSF. Currently, nineteen States are members of the GRF (Table II.7). 2.30 States’ debt to GDP ratio increased sharply at end-March 2021 to meet pandemic related expenditure (Table II.8). This ratio is estimated to decline slightly by end-March 2022 but is budgeted higher at 29.5 per cent by end-March 2023. At a disaggregated level, the ratio is expected to be higher than 25 per cent17 for 26 States and UTs at end-March 2023 (Statement 20). 2.31 The debt service ratio - measured in terms of interest payment to revenue receipts (IP-RR) ratio – which increased sharply in 2020-21, has moderated in 2021-22 and 2022-23, mainly on account of robust revenue receipts (Chart II.10). Composition of Debt 2.32 As stated earlier, rise in States’ debt levels was primarily led by higher market borrowings and higher borrowings from the Centre. On the other hand, the shares of special securities issued to National Small Saving Funds (NSSF), loans from banks and financial institutions and public accounts declined in 2020-21 (Table II.9). The share of market borrowings in total outstanding liabilities of the State governments is budgeted to increase in 2022-23. Similarly, loans from the Centre are also expected to increase in view of the 50-year interest-free loans being provided by the Centre under the scheme of Special Assistance to the States for Capital Investment.  Contingent Liabilities of States 2.33 State government guarantees increased sharply by end-March 2021, which has implications for their debt sustainability (Table II.10). 2.34 While the first two waves of the pandemic posed a major fiscal management challenge for States following revenue shortfalls and the compelling need for higher spending, the subsequent waves had a relatively milder impact on their finances. Accordingly, the States could bring down their gross fiscal deficit below the Fiscal Responsibility Legislation (FRL) target of 3 per cent of GDP in 2021-22. In 2022-23, the budgeted GFD of 3.4 per cent of GDP is higher but within the target of 4 per cent set by the Centre. The budgeted debt-GDP ratio of States, however, continues to remain significantly higher than 20 per cent recommended by the FRBM Review Committee, 2018 (Chairman: N. K. Singh). 2.35 The fiscal outlook for States remains favourable for the rest of the year and capital expenditure is expected to gain momentum in the second half. 2.36 While the outstanding liabilities of States have moderated from their pandemic time peaks, debt consolidation at the individual State level warrants urgent attention and a glide path needs to be set, keeping in view the need for rebuilding fiscal space to deal with future shocks. Annex II: The fifteenth Finance Commission (FC-XV) has assessed the fiscal challenges facing States through a survey of State-level macroeconomic, socioeconomic and fiscal indicators as well as the status of health infrastructure, power sector and local bodies’ finances. On this basis, specific reform signposts have been provided as guidance to enable States to chart a sustainable development path through fiscal policy actions.

Actions have been taken by various States in response to these recommendations (Table 1). 1 Provisional Accounts (PA) are compiled using data from Comptroller and Auditor General (CAG). 2 The borrowing space of 0.5 per cent of gross state domestic product (GSDP) out of the total net borrowing ceiling is tied to power sector reforms by States. 3 The Fiscal Responsibility Legislation (FRL) limit is 3 per cent. 4 General services include unclaimed deposits, sale of land and property, guarantee fees and the like. 5 As per the Union Budget 2022-23. 6 A tax amnesty can be defined as a limited time offer by the government to a specified group of taxpayers to pay a defined amount, in exchange for forgiveness of a tax liability (including interest and penalties), relating to a previous tax period (s), as well as freedom from legal prosecution. 7 The provisional accounts data from CAG has, however, placed the revenue expenditure growth of the State governments lower at 11.9 per cent in 2021-22. 8 Capital outlay is a part of capital expenditure. The other component is loans and advances by the State governments. 10 https://cbic-gst.gov.in/compensation-cess-bill-e.html 11 https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1736891 12 In March 2022, the Centre had stipulated the States to adjust their off-budget borrowings of 2020-21 and 2021-22 against the borrowing limits for 2022-23. However, in July 2022 the Centre relaxed these norms allowing the States to adjust their off-budget borrowings of 2021-22 against the borrowing limits of the next four years till March 2026. 13 https://doe.gov.in/sites/default/files/Monthly%20Summary%20Report%20of%20DoE%20for%20month%20of%20December%2C%202022.pdf 14 The scheme, initially started in 2020-21, was renewed for 2022-23 with an increased support of ₹1,00,000 crore which would be given as 50-year interest-free loans to the States (this support is over and above the net borrowing ceiling of 4 per cent of GSDP imposed on the States). Out of the total, ₹80,000 crore have been earmarked for allocation amongst the States in accordance with their share in Central taxes and duties as awarded by the 15th Finance Commission, and the remaining ₹20,000 crore will be disbursed to the States for projects relating to PM Gati Shakti, PM Gram Sadak Yojana, Digitization, Optical Fibre Cables, urban reforms and the like. 15 Re-issuance of SDLs/SGSs leads to augmenting the outstanding amount of a stock which may facilitate secondary market activity and passive consolidation. 16 As decided in the 32nd Conference of the State Finance Secretaries held on July 07, 2022, the nomenclature of the “State Development Loan (SDL)” has been changed to “State Government Security (SGS)”. |

हे पेज शेअर करा:

भारतीय रिझर्व्ह बँक मोबाईल ॲप्लिकेशन इंस्टॉल करा आणि नवीनतम बातम्यांचा त्वरित ॲक्सेस मिळवा!

आमचे अॅप इंस्टॉल करण्यासाठी QR कोड स्कॅन करा

पेज अंतिम अपडेट तारीख: