IST,

IST,

V. Financial Markets

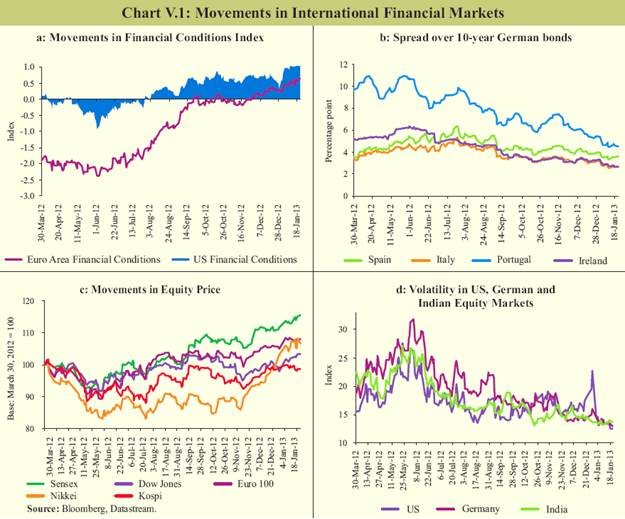

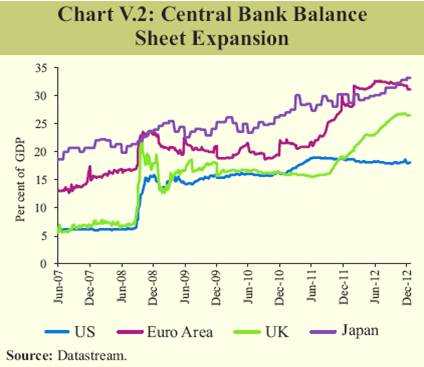

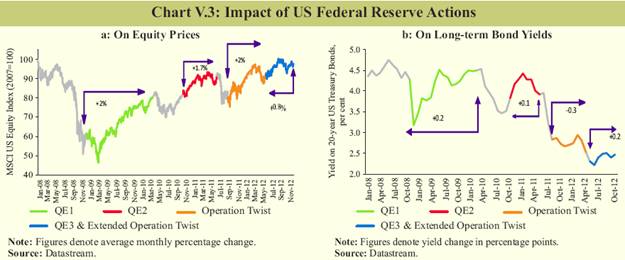

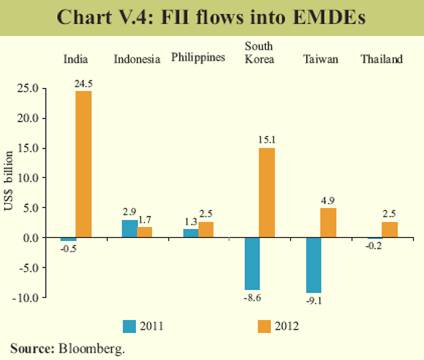

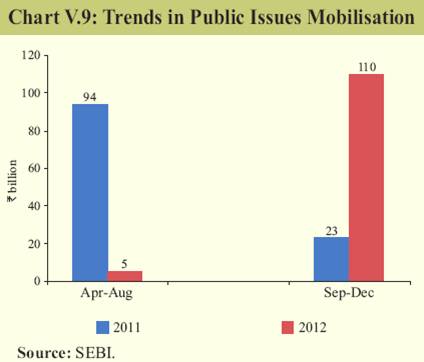

Policy actions, both domestic and global, augured well for the Indian financial markets in Q3 of 2012-13. With aggressive monetary-easing measures by central banks of advanced economies and some policy initiatives in distressed euro area economies, capital flows surged into emerging economies. The Indian rupee and equity markets greatly benefitted from the improved investor optimism. Despite the domestic macroeconomic stress, expectations of a turnaround in the economy drove the rally in the Indian markets. Improved investor confidence was also visible from the pick-up in the IPO market after a subdued year. Global financial markets improve on euro area policy action and fiscal cliff agreement V.1 International financial market conditions improved in Q3 of 2012-13 despite a fragile global economic outlook. Recent financial market developments indicate a perceived reduction in some major downside risks to the world economy. The easing of stress can be seen in the positive streak shown by Bloomberg’s Composite Financial Conditions Index (BFCIUS Index) that tracks the overall stress in money, bond, and equity markets, thereby enabling assessment of the availability and cost of credit (Chart V.1a). V.2 The possibility of a near-term worsening of the euro area crisis also appears to have declined following new policy announcements and the extension of financial help to troubled periphery economies. In December 2012, the euro area finance ministers empowered the European Central Bank (ECB) as the common bank supervisor from 2014. They also approved €39.5 billion aid to Spanish banks. International leaders also agreed upon a deal to again restructure Greece’s debt, with further large hair cuts that paved the way for the release of €34.4 billion in aid payment. Following these developments, credit default swap (CDS) spreads for European economies have reduced. V.3 With the improvement in borrowing conditions in the financial markets, the 10-year G-sec interest rate spread between distressed euro area countries such as Spain, Italy, Ireland and Portugal, and Germany declined (Chart V.1b). The Italian and Spanish governments were also able to raise longer-maturity debt from the markets with improvements in funding conditions. V.4 Global equity prices showed major gains in 2012, as investor preference to hold risky assets increased following quantitative stimuli announced by major central banks, despite weak corporate earnings. The minifiscal deal clinched by the US also aided the rally in global markets in 2013 so far (Chart V.1 c). Stock market uncertainty, as measured by implied volatility, also decreased during the period under review (Chart V.1d). AE central banks’ unconventional policy stimuli boost market sentiments V.5 Unprecedented monetary stimuli by central banks of advanced economies (AEs), which include QE3 and recently announced additional purchase of long-term treasury securities to the tune of US$ 45 billion per month by the US Federal Reserve (Fed), the outright monetary transactions (OMT) programme by the ECB and the asset purchase programme by the Bank of Japan (BoJ), as well as measures taken by the European Union to contain the euro area debt crisis, have helped revive global financial market sentiments. Concomitantly, the balance sheets of these central banks have expanded significantly (Chart V.2). V.6 Despite the positive impact of central banks’ unconventional monetary policy actions, the future impact of such policy is of concern as latter rounds of QE had a subdued effect (Chart V.3a). Monetary policy stimuli in Q4 of 2012 did not necessarily have a dampening effect on the long-term treasury yield in the US (Chart V.3b). This could be because, in the absence of a credible long-term fiscal consolidation plan, yields may have become less responsive to central bank actions. On the whole, the evaluation of the success of QE would require further research. Buoyant capital flows drive asset prices in EMDEs V.7 Excessive global liquidity arising from the easy monetary policy pursued by central banks in AEs, along with the lack of investment opportunities, channelled funds into the emerging market and developing economies (EMDEs) in search of higher returns. India and other Asian countries, such as South Korea, Philippines and Thailand, received higher FII inflows in 2012 than in 2011 (Chart V.4). V.8 Apart from the push factors discussed above, various pull factors emanating from domestic factors, such as the continued dependence of the Indian economy on domestic consumption unlike other exportdriven economies and the relatively stable earnings of listed companies, aided the surge in flows into India. The domestic reform measures announced by the government since mid-September 2012 also boosted investor sentiments. Indian equity markets showed significant turnaround, while the rupee remained range-bound. Money markets remained stable despite liquidity deficit V.9 Notwithstanding tight liquidity conditions due to advance tax payments, high government cash balances and rise in currency in circulation, the weighted average call money rate generally remained around the repo rate in Q3 of 2012-13. The rates in the collateralised segments i.e., CBLO and market repo, which constitute the predominant share (around 80 per cent) of the overnight money market, moved in tandem with the call money rate (Chart V.5). V.10 The amount of outstanding certificates of deposits (CDs) witnessed a fall during 2012- 13. The weighted average effective interest rate (WAEIR) of aggregate CD issuances decreased to 8.7 per cent at end-December 2012 from 11.1 per cent at end-March 2012 (Table V.1). V.11 Increased risk aversion by banks to lend to the corporate sector, as evident from the moderation in credit off-take, also manifested in a significant uptick in the size of fortnightly issuance of commercial paper (CP). The weighted average discount rate (WADR) of aggregate CP issuances decreased to 9.0 per cent at end-December 2012 from 12.2 per cent at end-March 2012. Yield curve gets inverted on economic slack and as borrowing programme stays on track V.12 During Q3 of 2012-13, G-sec yields firmed up in October, but declined markedly since December, with bonds rallying in response to four major factors. First, the market assessed that the year may pass without additional market borrowing. Second, expectations of a rate cut were built on moderating inflation. Third, resumption of OMO purchases by the Reserve Bank also led to a rally in G-sec market. Fourth, on review of the government’s cash position, the auction of dated securities scheduled for January 4, 2013 got postponed to late February 2013, which also caused the yields to soften. The 10-year generic yield declined from 8.63 per cent at end-March 2012 to 7.99 per cent on January 1, 2013 and further to 7.88 per cent as on January 24, 2013 (Chart V.6). V.13 However, during Q3, the fall in short term yields was not as significant, largely on account of persistent tightness in liquidity and the government’s decision to increase the quantity of T-bill issuances during the last quarter of the fiscal. With the spread between the yield on the 10-year G-sec and 91-day T-bill turning negative, the G-sec market showed an inverted yield curve. During the financial year, up to January 21, 2013, the weighted average maturity of the dated securities issued has increased to 13.5 years from 12.5 years during the corresponding period last year. The bid-cover ratio stood in the range of 1.36-4.10 as against 1.39-5.12 in the previous year (Table V.2). V.14 In the same period, 27 states have raised `1.3 trillion on a gross basis compared with around `1.1 trillion raised during the corresponding period of the previous year. Rupee exchange rate remained range bound in Q3 of 2012-13 V.15 Various reform measures, including liberalised FDI limits for certain sectors and the announcement of a fiscal consolidation path, enhanced global investor confidence in the Indian economy. This, along with announcements of quantitative easing by the US Fed and the BOJ, boosted capital inflows to India and aided the recovery of the rupee. Following the significant appreciation in September 2012, the rupee movement turned range bound with a weakening bias, reflecting the wide trade deficit (Chart V.7). V.16 As on January 23, 2013, the rupee showed lower depreciation over end-March 2012 compared to other major EMDEs like Brazil, South Africa and Argentina (Table V.3). Domestic equity markets firmed up as market liquidity improved with FII flows V.17 As on January 24, 2013, the domestic equity markets witnessed a y-o-y gain of 17.2 per cent with a 6.2 per cent gain over end- September 2012. Following the global equity market rally driven by a spate of generally better international economic data and policy actions, the Indian bourses also picked up. The BSE Sensex and S&P CNX Nifty crossed the 20,000 and 6,000 mark, respectively after two years. The BSE Sensex closed at 19,924 on January 24, 2013. V.18 Various factors, including recent reform measures such as the diesel price hike, cap on subsidised LPG, permission for FDI in retail and aviation and the passing of the Banking Laws (Amendment) Bill, 2011 in Parliament, along with hopes of a cut in the policy rate by the Reserve Bank in January 2013, and sustained FII inflows helped revive the domestic equity market. V.19 Market indicators, such as market capitalisation and daily turnover, have shown an increasing trend in 2012, reflecting the positive sentiment in the Indian stock market. Further, the PE ratio of the BSE Sensex increased in 2012, indicating a rise in the valuation of Indian stock over the year. V.20 During 2012-13 (up to January 23, 2013), FIIs made net investments of `1,190 billion in the capital market (both equity and debt) compared with that of `520 billion during the corresponding period in the previous year. FIIs made net investments of `1,011 billion in the equity markets compared with `27 billion last year. V.21 Domestic institutional investors (DIIs) (comprising banks, domestic financial institutions, insurance companies, new pension fund and mutual funds) made net sales during 2012-13 (up to January 23, 2013) (Chart V.8). Bankex outperformed Sensex V.22 As at end-December 2012, the BSE Bankex, which represents major banks in India, recorded much higher y-o-y gains of 57 per cent than the BSE Sensex (26 per cent), despite concerns about modest loan growth, deterioration in asset quality and alleviated risks. The factors that influenced the BSE Bankex favourably are the strong balance sheet performance by some private sector banks, stable net interest margin owing to a reduction in the CRR by 175 basis points of NDTL and expectation of treasury profit as bonds rallied. The Bankex also benefitted from the positive sentiments in the overall Indian equity markets. Signs of IPO market revival in December 2012 after a subdued period V.23 During September–December 2012, `110 billion was mobilised through 18 issues compared to `23 billion mobilised through 11 issues during the corresponding period last year (Chart V.9). Various measures taken by SEBI, such as allowing qualified foreign investors (QFIs) to invest in the primary as well as secondary markets, electronic initial public offers (e-IPOs), requiring companies to attain the minimum public shareholding of 25 per cent by June 2013, introduction of the Rajiv Gandhi Equity Savings Scheme, 2012 and the disinvestment programme by the government may also enhance primary market activity. House prices show slight moderation, but with increasing volumes V.24 The annual growth in the Reserve Bank’s quarterly House Price Index at the all- India level remains strong at 23 per cent in Q2 of 2012-13. The q-o-q increase, however, moderated to 3 per cent, the lowest in the past seven quarters. Transaction volumes have picked up and showed an annual growth of over 12 per cent in Q2 (Table V.4). Markets improve, but uncertainty still significant for 2013 V.25 Reduced fiscal space in several AEs and limited scope for monetary policy actions due to the enlarged balance sheets of central banks are expected to keep sentiments and markets range bound. The stress in the global financial markets has eased in view of reduced uncertainties in the euro area and the temporary resolution of the fiscal cliff in the U.S. However, a credible fiscal consolidation by the US can generate a more significant impact. Quantitative easing by the AEs has translated into higher capital flows to EMDEs, including India, which may witness some moderation going forward, but is nevertheless, likely to remain positive in the near term. V.26 Looking at domestic factors, commitment to reforms and efforts for sustainable fiscal consolidation would provide a positive impetus to the markets. Stronger signs of global and domestic recovery are crucial to support investor optimism. |

हे पेज शेअर करा:

भारतीय रिझर्व्ह बँक मोबाईल ॲप्लिकेशन इंस्टॉल करा आणि नवीनतम बातम्यांचा त्वरित ॲक्सेस मिळवा!

आमचे अॅप इंस्टॉल करण्यासाठी QR कोड स्कॅन करा

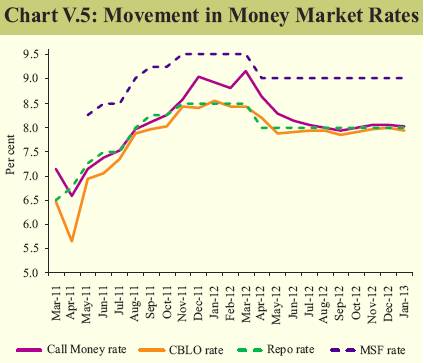

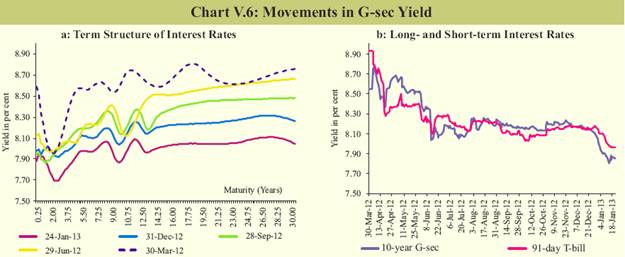

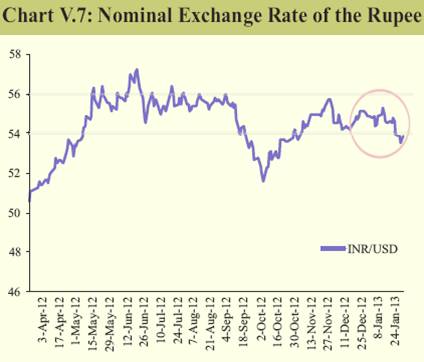

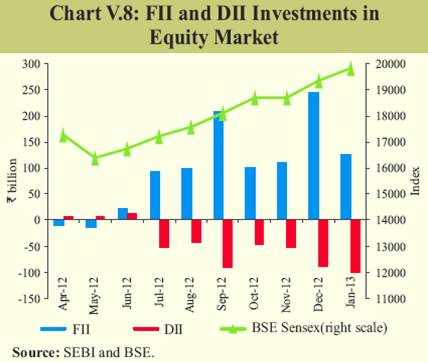

पेज अंतिम अपडेट तारीख: