IST,

IST,

Financial Intermediation for All - Economic Growth with Equity

Dr. (Smt.) Deepali Pant Joshi, Executive Director, Reserve Bank of India

delivered-on सप्टें 02, 2014

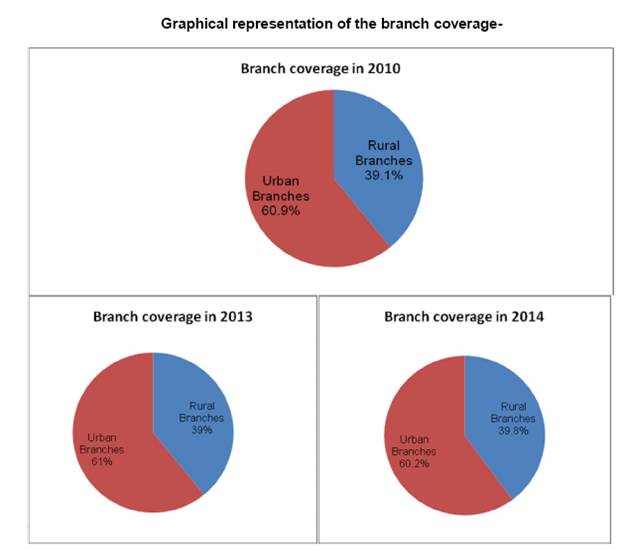

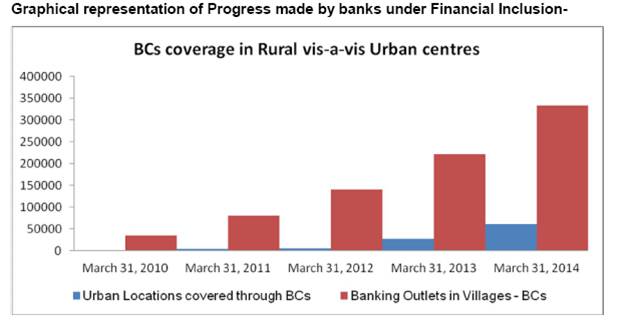

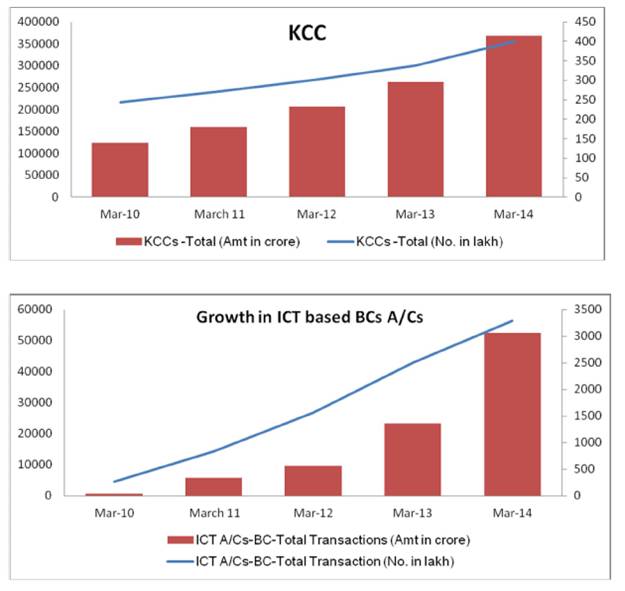

At the very outset, I thank Dun & Bradstreet for the kind invitation to address the Financial Inclusion conclave today. I attach a great deal of value to this interaction. Financial Inclusion Financial Inclusion is defined as the process of ensuring access to appropriate financial products and services needed by all sections of the society in general and vulnerable groups such as weaker sections and low income groups in particular at an affordable cost in a fair and transparent manner by mainstream institutional players. RBI's Approach to Financial Inclusion Planned and structured Approach RBI has accorded high priority to Financial Inclusion. We have followed a planned and structured approach to address the twin issues of demand and supply. We have framed regulations with an objective of providing banking services to six lakh plus villages and to create an enabling environment for banks to do so. We are furthering financial inclusion in a mission mode through a combination of strategies ranging from relaxation of regulatory guidelines, provision of new products and supportive measures to achieve sustainable and scalable Financial Inclusion. Financial Inclusion is at the centre stage of international policy discourse under the G-20 umbrella. More than fifty countries have set formal targets and goals of Financial Inclusion. If half of our country’s population were to be financially included and permitted to move from the marginal level to the main stream as producers and consumers of goods and services, consider the tremendous entrepreneurial energies which would be unleashed leading to a multiple effect on the economic growth of the poor. Considerable evidence is there which shows that poor people benefit immensely from basic payment, savings and insurance services. Although, financial services are available to poor people, they are compelled to pay four times the price we pay for them because they are not linked to formal financial system and have to rely on unreliable informal sector providers. The RBI has since the last decade addressed these asymmetries through macro policy interventions: 1. Branch Expansion With a view to increasing banking penetration and ensuring financial inclusion, domestic commercial banks, both in the public and private sectors, were advised to draw up Board-approved Financial Inclusion Plans (FIP) with a view to rolling them out over the next three years. The same were submitted to the Reserve Bank. Banks were advised to devise FIPs congruent with their business strategy and comparative advantage to make it an integral part of their corporate plans. These plans broadly include self-set targets in respect of rural brick and mortar branches opened; business correspondents (BC) employed; coverage of unbanked villages with population above 2000 as also other unbanked villages with population below 2000 through branches/BCs/other modes; no-frill accounts opened including through BC-ICT; Kisan Credit Cards (KCC) and General Credit Cards (GCC) issued; and other specific products designed by them to cater to the financially excluded segments. The implementation of these plans is being closely monitored by the Reserve Bank. The domestic SCBs have been mandated in the Monetary Policy Statement – April 2011 to open at least 25 per cent of their total number of branches to be opened during a year in unbanked rural (Tier 5 and Tier 6) centres. Further, banks have been advised in the Monetary Policy Statement of May 2013 to front–load the opening of branches in unbanked rural centres over a 3 year cycle co–terminus with their FIP (2013-16). Credit will be given for branches opened in unbanked rural centres in excess of 25 percent in a year which will be carried forward to the subsequent year of the FIP. This is expected to accelerate the progress in opening of bank branches in the rural areas. 2. Relaxed Know Your Customer (KYC) requirements – To facilitate easy access to bank accounts, Know Your Customer (KYC) requirements have been simplified to such an extent that small accounts can be opened with self certification in the presence of bank officials. Further, RBI has allowed ‘Aadhaar’ the unique identification number allotted by UIDAI, GOI to be used as one of the eligible document for meeting the KYC requirement for opening a bank account. Recently in September 2013, we have allowed banks to provide e-KYC services based on Aadhaar, thus paving the way for account opening of all the people. 3. Allowing correspondent banking - In January 2006, the Reserve Bank permitted banks to utilise the services of intermediaries in providing banking services through the use of business facilitators and business correspondents. The BC model allows banks to do ‘cash in - cash out’ transactions at a location much closer to the rural population, thus addressing the last mile problem. 4. Combination of Branch and BC Structure to deliver Financial Inclusion The idea is to have a combination of Brick and Mortar structure which will be helpful in extending financial inclusion especially in geographically dispersed areas. To ensure increased banking penetration, and control over operations of BCs, banks have been advised to establish low cost branches in the form of intermediate brick and mortar structures in rural centres between the present base branch and BC locations, so as to provide support to a cluster of BCs (about 8-10 BC) units at a reasonable distance of about 3-4 kilometres. Such branches, with minimum infrastructure, such as a Core Banking Solution (CBS) terminal linked to a pass book printer, a safe for cash retention for operating large customer transactions. etc. is expected provide support for BC operations and for quick redressal of customer grievances. 5. Using electronic payments into bank accounts for Government payments - The recent introduction of direct benefit transfer for validating the identity of the beneficiary through Aadhaar will help facilitate delivery of social welfare benefits by direct credit to the bank accounts of beneficiaries. The government, in future, has plans of routing all social security payments through the banking network using the Aadhaar based platform as a unique financial address of beneficiaries. The condition of full withdrawal by beneficiary’s proof of disbursement should be removed; this will promote usage of accounts for savings. The legality and statutory status of a single National Identification Authority need to be resolved at the earliest, along with its scope as a unitary issuer of e-KYC, UEBA and real time authentication, without these being mandatory. 6. The RBI had in September 2013, appointed Dr. Nachiket Mor Committee on Committee on Comprehensive Financial Services for Small Business and Low Income Households to examine the challenges to Financial Inclusion. The Committee, while laying down its vision statement for financial inclusion and deepening, has suggested providing a universal bank account to all Indians above the age of eighteen years and has recommended a Vertically Differentiated Banking System with Payments Banks for Deposits & Payments and Wholesale Banks for credit outreach with relaxed entry point norms. The recommendations of the Mor Committee relating to Financial Inclusion like allowing NBFCs to work as BCs, removing distance criteria of 30 kms for BCs, single proof of address either permanent or current for KYC compliance have already been implemented. Further, the draft guidelines for licensing of payment and small banks have been issued. Technology for improvement in borrowers’ Identification and credit reporting “Technologies that reduce asymmetric information in credit markets are technological innovations which can be leveraged for improved borrower identification. Bio-metric authentication helps to reduce leakages and ensure that Government transfers direct to bank accounts achieve the desired objective of financial inclusion, thus creating a better enabling environment and increasing penetrative outreach for optimal results.” “Financial inclusion is critical to ensure equitable economic growth and a just Society.” Leveraging technology makes it easy to leap frog the barriers of geography for sustainable, scalable financial inclusion. Empowering Small Banks Alternate types of Payment Banks are also viable options. We also require effective financial literacy to bridge the gap to demand and supply of financial services. One Key barrier the poor and small businesses face in accessing financial services is the lack of sufficient understanding of these services and the opportunities and risks they present. Financial Literacy has been given a great push by the RBI to help the poor people, better manage their finances and protect them against exploitation. RBI has advised banks to organise literacy camp. Usage of Credit Bureau also helps to build credit histories and it affects how they are evaluated for credit. There are three sides of the triangle – Financial literacy, Financial Inclusion leading to Financial Stability. Financial Literacy We also require effects of financial literacy to bridge the gap between demand and supply of financial products and services. Financial Literacy is an important adjunct for promoting financial inclusion, consumer protection and ultimately financial stability. RBI has advised banks to set up Financial Literacy Centre's (FLC) in all the districts of the country. Banks have already set up around 942 FLCs as of March 2014. Banks have been further advised to scale up financial literacy efforts through conduct of outdoor Financial Literacy Camps, at least once a month, both by the FLCs and also by all the rural branches. In order to ensure consistency in the messages reaching the target audience of financially excluded people during the Financial Literacy Camps, RBI has prepared a comprehensive Financial Literacy Guide containing Guidance Note for Trainers, Operational Guidelines for conduct of Financial Literacy Camps & Financial Literacy Material as also a Financial Diary and a set of 16 posters. Banks have been advised to use the material as a standard curriculum to impart basic conceptual understanding of financial products and services. While improving financial literacy is a necessary step in protecting consumer from exploitation or exclusionary practices, it is not a sufficient step. Regulation must be redesigned to ensure that while extending adequate precaution the poor are not kept within the financial services because of regulatory barriers. Roadmap for providing banking outlets in unbanked villages The Reserve Bank continued efforts to create a conducive and enabling environment for access to financial services to extend door step banking facilities in all the unbanked villages in a phase-wise manner. During Phase I, 74,414 unbanked villages with population more than 2,000 were identified and allotted to various banks through SLBCs for coverage through various modes, that is, branches, BCs or other modes such as ATMs and satellite branches etc. All these unbanked villages have been covered by opening banking outlets comprising 2,493 branches, 69,589 BCs and 2,332 through other modes. In Phase II, under the roadmap for provision of banking outlets in unbanked villages with population less than 2,000, about 4,90,000 unbanked villages have been identified and allotted to banks for coverage in a time bound manner by March 31, 2016. As per the progress reports received from SLBCs, banks had opened banking outlets in 183,993 unbanked villages by March 2014, comprising 7,761 branches, 163,187 BCs and 13,045 through other modes. The Reserve Bank is closely monitoring the progress made by the banks under the roadmap. Financial inclusion plan and its performance evaluation The Reserve Bank has used (Financial Inclusion Plans) FIPs to gauge the performance of banks under their (FI) initiatives. With the completion of the first phase, a large banking network has been created and a large number of bank accounts have also been opened (Table 1) However, it has been observed that the accounts opened and the banking infrastructure created has not seen substantial operations in terms of transactions. In order to continue with the process of ensuring meaningful access to banking services to the excluded, banks were advised to draw up fresh three-year FIPs for 2013-16. Banks were also advised that the FIPs prepared by them are disaggregated and percolate down to the branch level so as to ensure the involvement of all the stakeholders in FI efforts and also to ensure uniformity in the reporting structure under FIPs. The focus under the new plan is now more on the volume of transactions in the large number of accounts opened. A brief of the performance of banks under FIP up to March 31, 2014 is:

Though, the number of BC-ICT transactions has shown a considerable increase during the last year the average transaction per account still remains low. The focus of monitoring is now more on usage of these accounts through issue of more credit products through the channel. The Reserve Bank also issued guidelines to strengthen the BC model. Implementation and monitoring of financial inclusion targets should focus on usage of bank accounts, and expand beyond transfer payouts. As the recent inter Media survey shows, only half the bank accounts have been active over the previous three months. In order to increase transactions, there should be clear communication to customers about the mission and banks should be incentivised to provide appropriate products that increase usage. Way forward- Structure With adoption of new branchless delivery channels by banks, there is a need for banks to revamp the structure for carrying out banking operations considering their competitive, comparative advantage and build strategy and a business case. Each bank has to based on its business strategy develop a structure that can enhance its financial inclusion efforts. Innovation

BC Model There are many challenges being faced while implementing BC model. Sustainability and scalability of the BC model is essential. More and more innovative products will have to be introduced which would benefit both banks as well as the rural people and at the same time make the BC model more viable. Direct Benefit Transfers The Direct Benefits Transfer (DBT) programme, launched in 2013 as a game changer, has not progressed as smoothly as envisioned. With the new government now ready to move vigorously ahead on this front, this policy brief looks at experiences from within the country and abroad to distil the key inputs to get the programme going on the right path. The main priority is to streamline the Direct Benefits Transfer programme to work efficiently through electronic channels the such interoperative RuPay Debit card. The government should accelerate the de-duplication and seeding of bank accounts under one agency instead of leaving line ministries to handle the implementation of individual schemes. Transactions During the first phase of our FI initiative, we have had success as regards creating access through opening of banking outlets by banks and also in opening bank accounts for large number of individuals in the rural areas. Going forward our idea is to enable more transactions in these accounts by providing more credit products, which will not only help rural people to avail of credit at comparatively lower rates of interest but at the same time also make the BC model viable for banks. Banks have been advised to leverage upon the Direct Benefit Transfer initiative of the Government of India for linking all the individuals to the banking system and for utilizing the large amounts likely to be credited in these accounts for encouraging issue of deposit and credit products. Financial Literacy and Education We have adopted an integrated approach for financial inclusion wherein the supply side initiatives will be ably supported by initiatives on the demand side. In this direction banks will have to elevate financial literacy and awareness drives to make people understand the benefits of linking with the banking system. Banks have to take initiative continuously train the BC’s as they primarily provide the last mile link with the customers. Synergies Essentially, financial inclusion cannot be achieved without the active involvement of all stakeholders and the commitment from all the people. Besides consideration of economic efficiency, there is a compelling morale argument for financial inclusion to create a just society which provides economic growth with equity.    |

हे पेज शेअर करा:

भारतीय रिझर्व्ह बँक मोबाईल ॲप्लिकेशन इंस्टॉल करा आणि नवीनतम बातम्यांचा त्वरित ॲक्सेस मिळवा!

आमचे अॅप इंस्टॉल करण्यासाठी QR कोड स्कॅन करा

पेज अंतिम अपडेट तारीख: