FAQ Page 1 - आरबीआय - Reserve Bank of India

Content Type:

Withdrawal of Legal Tender Character of the old Bank Notes in the denominations of ₹ 500/- and ₹ 1000/- (Updated as on December 27, 2016)

Careers FAQ

Remittances are an important source of family and national income and also are one of the largest sources of external financing. Beneficiaries in India can receive cross-border inward remittances through banking and postal channels. Banks have general permission to enter into a partnership with other banks for conducting remittance business. The International Financial System (IFS) platform of Universal Post Union (UPU) is generally used for the postal channel. Besides, there are two more channels for receiving inward remittances, viz. Rupee Drawing Arrangement (RDA) and Money Transfer Service Scheme (MTSS) which are the most common arrangements under which the remittances are received into the country. These FAQs are mainly relating to the common queries relating to RDA and MTSS and may be referred to for general guidance. The Authorised Persons and their constituents may refer to respective circulars/ notifications for detailed information, if so needed.

Rupee Drawing Arrangement (RDA)

Targeted Long Term Repo Operations (TLTROs)

Updated: मे 28, 2021

Ans: Yes. The banks will have to maintain amount of specified securities for the amount received in TLTRO in its HTM book at all times till maturity of TLTRO.

FAQs on Non-Banking Financial Companies

FOREWORD

FAQs on Non-Banking Financial Companies

FOREWORD

The Reserve Bank of India is entrusted with the responsibility of regulating and supervising the Non-Banking Financial Companies by virtue of powers vested in Chapter III B of the Reserve Bank of India Act, 1934. The regulatory and supervisory objective, is to:

- ensure healthy growth of the financial companies;

- ensure that these companies function as a part of the financial system within the policy framework, in such a manner that their existence and functioning do not lead to systemic aberrations; and that

- the quality of surveillance and supervision exercised by the Bank over the NBFCs is sustained by keeping pace with the developments that take place in this sector of the financial system.

In view of the significant growth registered by the NBFC segment during the last decade, the powers of the Bank were enhanced by amending the provisions of the Act during 1997 to facilitate regulation and supervision by RBI covering several aspects of the activities of the NBFCs. Following the amendments to Chapter IIIB of the Act, the Bank has since introduced a new regulatory framework effective January 31, 1998 which directs the focus of the regulatory-cum-supervisory attention primarily on the NBFCs which accept deposits from the public.

The changes introduced in the regulatory framework are comprehensive and broadbased and it has been felt necessary to explain the rationale underlying these changes and provide clarification on certain operational matters for the benefit of the NBFCs, members of public, rating agencies, audit profession, the different Associations of the NBFCs etc. To meet this need, this booklet in the form of questions and answers, is being brought out by the RBI (Department of Non-Banking Supervision) with the hope that it will provide better understanding of the new regulatory framework.

(V.S.N. Murty)

Chief General Manager

RESERVE BANK OF INDIA,

DEPARTMENT OF NON-BANKING SUPERVISION,

CENTRAL OFFICE,

MUMBAI

FEBRUARY 16, 1998

CONTENTS

CONTENTS

1. | |

2. | |

3. | |

4. | |

5. | |

6. | |

7. | |

8. | |

9. | |

10. | |

11. | |

12. | Extent of Regulations over NBFCs accepting public deposits and not accepting public deposits |

13. | |

14. | |

15. | |

16. | |

17. |

Registration

Domestic Deposits

I. Domestic Deposits

Housing Loans

Retail Direct Scheme

Scheme related queries

Retail Direct Scheme is a one-stop solution to facilitate investment in Government Securities by individual investors. Under this scheme individual retail investors can open a Gilt Securities Account – “Retail Direct Gilt (RDG)” account with RBI. Using this account, retail investors can buy and sell government securities through the online portal – https://rbiretaildirect.org.in

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

General Instructions

Annual return on Foreign Liabilities and Assets (FLA) has been notified under FEMA 1999 (A.P. (DIR Series) Circular No. 45 dated March 15, 2011) and it is required to be submitted by all the India-resident companies/ LLPs / Others [(include SEBI registered Alternative Investment Funds (AIFs), Partnership Firms, Public Private Partnerships (PPP)] (hereafter referred as ‘entities’) which have received FDI and/ or made overseas investment in any of the previous year(s), including the current year.

The Reserve Bank participates in the Co-ordinated Direct Investment Survey (CDIS) and Co-ordinated Portfolio Investment Survey (CPIS) conducted by the International Monetary Fund (IMF). Here, consolidated information collected from FLA return related to foreign financial liabilities and assets position as at end-March of the previous financial year (FY) and end-March of the latest FY of these entities are reported. This information is also used in the compilation of India’s Balance of Payments (BoP) and International Investment Position (IIP).

Confidentiality Clause

Eligible entities and requirements to submit the FLA return

Ans: The annual return on Foreign Liabilities and Assets (FLA) is required to be submitted by the following entities which have received FDI (foreign direct investment) and/or made FDI abroad (i.e. overseas investment) in the previous year(s) including the current year i.e., who holds foreign assets or/and liabilities in their balance sheets;

-

A Company within the meaning of section 1(4) of the Companies Act, 2013.

-

A Limited Liability Partnership (LLP) registered under the Limited Liability Partnership Act, 2008

-

Others [include SEBI registered Alternative Investment Funds (AIFs), Partnership Firms, Public Private Partnerships (PPP) etc.]

Framework for Compromise Settlements and Technical Write-offs

Circular dated June 8, 2023 on ‘Framework for Compromise Settlements and Technical Write-offs’

A. COMPROMISE SETTLEMENT IN WILFUL DEFAULT AND FRAUD CASES

No. The said provision enabling banks to enter into compromise settlement in respect of borrowers categorised as fraud or wilful defaulter is not a new regulatory instruction and has been the settled regulatory stance for more than 15 years. This enabler is already available to banks as per the extant instructions, as given under:

-

RBI had advised IBA vide letter dated May 10, 2007 that, “(i) banks may enter into compromise settlement with wilful defaulters/ fraudulent borrowers without prejudice to the criminal proceeding underway against such borrowers; (ii) All such cases of compromise settlements should be vetted by Management Committee/ Board of banks.”

-

Master Circular on Wilful Defaulters dated July 1, 2015 envisages lenders agreeing to compromise settlement with borrowers classified as wilful defaulters and states that such cases need not be reported to Credit Information Companies provided inter alia that, “the borrower has fully paid the compromised amount.”

-

Master Directions on Frauds dated July 1, 2016 provides for compromise settlement with borrowers classified as fraud, subject to the condition that, “No compromise settlement involving a fraudulent borrower is allowed unless the conditions stipulate that the criminal complaint will be continued.”

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

Bank Accounts with Paytm Payments Bank

Yes. You can continue to use, withdraw or transfer your funds from your account upto the available balance in your account.

Similarly, you can continue to use your debit card to withdraw or transfer funds upto the available balance in your account.

Remittances (Money Transfer Service Scheme (MTSS) and Rupee Drawing Arrangement (RDA))

Remittances are an important source of family and national income and also are one of the largest sources of external financing. Beneficiaries in India can receive cross-border inward remittances through banking and postal channels. Banks have general permission to enter into a partnership with other banks for conducting remittance business. The International Financial System (IFS) platform of Universal Post Union (UPU) is generally used for the postal channel. Besides, there are two more channels for receiving inward remittances, viz. Rupee Drawing Arrangement (RDA) and Money Transfer Service Scheme (MTSS) which are the most common arrangements under which the remittances are received into the country.

These FAQs are mainly relating to the common queries relating to RDA and MTSS and may be referred to for general guidance. The Authorised Persons and their constituents may refer to respective circulars/ notifications for detailed information, if so needed.

Rupee Drawing Arrangement (RDA)

External Commercial Borrowings (ECB) and Trade Credits

PART I – EXTERNAL COMMERCIAL BORROWINGS

A. BASIC QUERIES

Master Direction No. 5 on ‘External Commercial Borrowings, Trade Credits and Structured Obligations dated March 26, 2019 may be referred to for guidance on the extant framework on ECB and TC. ECBs and TCs raised under the prior frameworks should continue to be in compliance with the corresponding guidelines applicable at the time of availing the ECBs and TCs.

All you wanted to know about NBFCs

Updated: एप्रि 23, 2025

A. Definitions

A Non-Banking Financial Company (NBFC) is a company registered under the Companies Act, 1956 or Companies Act, 2013, and engaged in the business of loans and advances, acquisition of shares/stocks/bonds/debentures/securities issued by Government or local authority or other marketable securities of a like nature, leasing, hire-purchase, etc., as their principal business, but does not include any institution whose principal business is that of agriculture activity, industrial activity, purchase or sale of any goods (other than securities) or providing any services and sale/purchase/construction of immovable property. A non-banking institution which is a company and has principal business of receiving deposits under any scheme or arrangement in one lump sum or in installments by way of contributions or in any other manner, is also a non-banking financial company (Residuary non-banking company).

Indian Currency

Updated: एप्रि 15, 2025

A) Basics of Indian Currency/Currency Management

The Indian currency is called the Indian Rupee (INR). One Rupee consists of 100 Paise. The symbol of the Indian Rupee is ₹. The design resembles both the Devanagari letter "₹" (ra) and the Latin capital letter "R", with a double horizontal line at the top.

Foreign Investment in India

These FAQs attempt to put in place the common queries that users have on the subject in an easy to understand language. However, for conducting a transaction, the Foreign Exchange Management Act, 1999 (FEMA) and the Regulations made or directions issued thereunder may be referred to. The relevant principal regulations are the Foreign Exchange Management (Transfer or Issue of Security by a Person Resident Outside India) Regulations, 2017 dated November 7, 2017 as amended from time to time (hereinafter referred to as FEMA 20 (R)). The modalities as to how the foreign exchange business has to be conducted by the Authorised Persons with their customers/ constituents with a view to implementing the regulations framed is laid down in Master Direction on Foreign investment in India.

Answer: The routes under which foreign investment can be made is as under:

- Automatic Route: Foreign Investment is allowed under the automatic route without prior approval of the Government or the Reserve Bank of India, in all activities/ sectors as specified in the Regulation 16 of FEMA 20 (R).

- Government Route: Foreign investment in activities not covered under the automatic route requires prior approval of the Government. Procedure for applying for Government approval is given at http://fifp.gov.in/Forms/SOP.pdf

Government Securities Market in India – A Primer

Disclaimer

The contents of this primer are for general information and guidance purpose only. The Reserve Bank will not be liable for actions and/or decisions taken based on this Primer. Readers are advised to refer to the specific circulars issued by Reserve Bank of India from time to time. While every effort has been made to ensure that the information set out in this document is accurate, the Reserve Bank of India does not accept any liability for any action taken, or reliance placed on, any part, or all, of the information in this document or for any error in or omission from, this document.

Preface

The G-Secs market has witnessed significant changes during the past decade. Introduction of an electronic screen-based trading system, dematerialized holding, straight through processing, establishment of the Clearing Corporation of India Ltd. (CCIL) as the Central Counter Party (CCP) for guaranteed settlement, new instruments, and changes in the legal environment are some of the major aspects that have contributed to the rapid development of the G-Sec market. Major participants in the G-Secs market historically have been large institutional investors. With the various measures for development, the market has also witnessed the entry of smaller entities such as co-operative banks, small pension, provident and other funds etc. These entities are mandated to invest in G-Secs through respective regulations. However, some of these new entrants have often found it difficult to understand and appreciate various aspects of the G-Secs market. The Reserve Bank of India has, therefore, taken several initiatives to bring awareness about the G-Secs market among small investors. These include workshops on the basic concepts relating to fixed income securities/ bonds like G-Secs, trading and investment practices, the related regulatory aspects and the guidelines. This primer is yet another initiative of the Reserve Bank to disseminate information relating to the G-Secs market to the smaller institutional players as well as the public. An effort has been made in this primer to present a comprehensive account of the market and the various processes and operational aspects related to investing in G-Secs in an easy-to-understand, question-answer format. The primer also has, as annexes, a list of primary dealers (PDs), useful excel functions and glossary of important market terminology. I hope the investors, particularly the smaller institutional investors will find the primer useful in taking decisions on investment in G-Secs. Reserve Bank of India would welcome suggestions in making this primer more user-friendly. Shri B.P. Kanungo Deputy Governor

1.1 A bond is a debt instrument in which an investor loans money to an entity (typically corporate or government) which borrows the funds for a defined period of time at a variable or fixed interest rate. Bonds are used by companies, municipalities, states and sovereign governments to raise money to finance a variety of projects and activities. Owners of bonds are debt holders, or creditors, of the issuer.

What is a Government Security (G-Sec)?

1.2 A Government Security (G-Sec) is a tradeable instrument issued by the Central Government or the State Governments. It acknowledges the Government’s debt obligation. Such securities are short term (usually called treasury bills, with original maturities of less than one year) or long term (usually called Government bonds or dated securities with original maturity of one year or more). In India, the Central Government issues both, treasury bills and bonds or dated securities while the State Governments issue only bonds or dated securities, which are called the State Development Loans (SDLs). G-Secs carry practically no risk of default and, hence, are called risk-free gilt-edged instruments.

a. Treasury Bills (T-bills)

1.3 Treasury bills or T-bills, which are money market instruments, are short term debt instruments issued by the Government of India and are presently issued in three tenors, namely, 91 day, 182 day and 364 day. Treasury bills are zero coupon securities and pay no interest. Instead, they are issued at a discount and redeemed at the face value at maturity. For example, a 91 day Treasury bill of ₹100/- (face value) may be issued at say ₹ 98.20, that is, at a discount of say, ₹1.80 and would be redeemed at the face value of ₹100/-. The return to the investors is the difference between the maturity value or the face value (that is ₹100) and the issue price (for calculation of yield on Treasury Bills please see answer to question no. 26).

b. Cash Management Bills (CMBs)

1.4 In 2010, Government of India, in consultation with RBI introduced a new short-term instrument, known as Cash Management Bills (CMBs), to meet the temporary mismatches in the cash flow of the Government of India. The CMBs have the generic character of T-bills but are issued for maturities less than 91 days.

c. Dated G-Secs

1.5 Dated G-Secs are securities which carry a fixed or floating coupon (interest rate) which is paid on the face value, on half-yearly basis. Generally, the tenor of dated securities ranges from 5 years to 40 years.

| The Public Debt Office (PDO) of the Reserve Bank of India acts as the registry / depository of G-Secs and deals with the issue, interest payment and repayment of principal at maturity. Most of the dated securities are fixed coupon securities. |

The nomenclature of a typical dated fixed coupon G-Sec contains the following features - coupon, name of the issuer, maturity year. For example, - 7.17% GS 2028 would mean:

| Coupon | : 7.17% paid on face value |

| Name of Issuer | : Government of India |

| Date of Issue | : January 8, 2018 |

| Maturity | : January 8, 2028 |

| Coupon Payment Dates | : Half-yearly (July 08 and January 08) every year |

| Minimum Amount of issue/ sale | : ₹10,000 |

In case, there are two securities with the same coupon and are maturing in the same year, then one of the securities will have the month attached as suffix in the nomenclature. eg. 6.05% GS 2019 FEB, would mean that G-Sec having coupon 6.05% that mature in February 2019 along with the other similar security having the same coupon. In this case, there is another paper viz. 6.05%GS2019 which bears same coupon rate and is also maturing in 2019 but in the month of June. Each security is assigned a unique number called ISIN (International Security Identification Number) at the time of issuance itself to avoid any misunderstanding among the traders.

If the coupon payment date falls on a Sunday or any other holiday, the coupon payment is made on the next working day. However, if the maturity date falls on a Sunday or a holiday, the redemption proceeds are paid on the previous working day.

1.6 Instruments:

i) Fixed Rate Bonds – These are bonds on which the coupon rate is fixed for the entire life (i.e. till maturity) of the bond. Most Government bonds in India are issued as fixed rate bonds.

For example – 8.24%GS2018 was issued on April 22, 2008 for a tenor of 10 years maturing on April 22, 2018. Coupon on this security will be paid half-yearly at 4.12% (half yearly payment being half of the annual coupon of 8.24%) of the face value on October 22 and April 22 of each year.

ii) Floating Rate Bonds (FRB) – FRBs are securities which do not have a fixed coupon rate. Instead it has a variable coupon rate which is re-set at pre-announced intervals (say, every six months or one year). FRBs were first issued in September 1995 in India. For example, a FRB was issued on November 07, 2016 for a tenor of 8 years, thus maturing on November 07, 2024. The variable coupon rate for payment of interest on this FRB 2024 was decided to be the average rate rounded off up to two decimal places, of the implicit yields at the cut-off prices of the last three auctions of 182 day T- Bills, held before the date of notification. The coupon rate for payment of interest on subsequent semi-annual periods was announced to be the average rate (rounded off up to two decimal places) of the implicit yields at the cut-off prices of the last three auctions of 182 day T-Bills held up to the commencement of the respective semi-annual coupon periods.

iii) The Floating Rate Bond can also carry the coupon, which will have a base rate plus a fixed spread, to be decided by way of auction mechanism. The spread will be fixed throughout the tenure of the bond. For example, FRB 2031 (auctioned on May 4, 2018) carry the coupon with base rate equivalent to Weighted Average Yield (WAY) of last 3 auctions (from the rate fixing day) of 182 Day T-Bills plus a fixed spread decided by way of auction. Zero Coupon Bonds – Zero coupon bonds are bonds with no coupon payments. However, like T- Bills, they are issued at a discount and redeemed at face value. The Government of India had issued such securities in 1996. It has not issued zero coupon bonds after that.

iv) Capital Indexed Bonds – These are bonds, the principal of which is linked to an accepted index of inflation with a view to protecting the Principal amount of the investors from inflation. A 5 year Capital Indexed Bond, was first issued in December 1997 which matured in 2002.

v) Inflation Indexed Bonds (IIBs) - IIBs are bonds wherein both coupon flows and Principal amounts are protected against inflation. The inflation index used in IIBs may be Whole Sale Price Index (WPI) or Consumer Price Index (CPI). Globally, IIBs were first issued in 1981 in UK. In India, Government of India through RBI issued IIBs (linked to WPI) in June 2013. Since then, they were issued on monthly basis (on last Tuesday of each month) till December 2013. Based on the success of these IIBs, Government of India in consultation with RBI issued the IIBs (CPI based) exclusively for the retail customers in December 2013. Further details on IIBs are available on RBI website under FAQs.

vi) Bonds with Call/ Put Options – Bonds can also be issued with features of optionality wherein the issuer can have the option to buy-back (call option) or the investor can have the option to sell the bond (put option) to the issuer during the currency of the bond. It may be noted that such bond may have put only or call only or both options. The first G-Sec with both call and put option viz. 6.72% GS 2012 was issued on July 18, 2002 for a maturity of 10 years maturing on July 18, 2012. The optionality on the bond could be exercised after completion of five years tenure from the date of issuance on any coupon date falling thereafter. The Government has the right to buy-back the bond (call option) at par value (equal to the face value) while the investor had the right to sell the bond (put option) to the Government at par value on any of the half-yearly coupon dates starting from July 18, 2007.

vii) Special Securities - Under the market borrowing program, the Government of India also issues, from time to time, special securities to entities like Oil Marketing Companies, Fertilizer Companies, the Food Corporation of India, etc. (popularly called oil bonds, fertiliser bonds and food bonds respectively) as compensation to these companies in lieu of cash subsidies These securities are usually long dated securities and carry a marginally higher coupon over the yield of the dated securities of comparable maturity. These securities are, however, not eligible as SLR securities but are eligible as collateral for market repo transactions. The beneficiary entities may divest these securities in the secondary market to banks, insurance companies / Primary Dealers, etc., for raising funds.

Government of India has also issued Bank Recapitalisation Bonds to specific Public Sector Banks in 2018. These securities are named as Special GoI security and are non-transferable and are not eligible investment in pursuance of any statutory provisions or directions applicable to investing banks. These securities can be held under HTM portfolio without any limit.

viii) STRIPS – Separate Trading of Registered Interest and Principal of Securities. - STRIPS are the securities created by way of separating the cash flows associated with a regular G-Sec i.e. each semi-annual coupon payment and the final principal payment to be received from the issuer, into separate securities. They are essentially Zero Coupon Bonds (ZCBs). However, they are created out of existing securities only and unlike other securities, are not issued through auctions. Stripped securities represent future cash flows (periodic interest and principal repayment) of an underlying coupon bearing bond. Being G-Secs, STRIPS are eligible for SLR. All fixed coupon securities issued by Government of India, irrespective of the year of maturity, are eligible for Stripping/Reconstitution, provided that the securities are reckoned as eligible investment for the purpose of Statutory Liquidity Ratio (SLR) and the securities are transferable. The detailed guidelines of stripping/reconstitution of government securities is available in RBI notification IDMD.GBD.2783/08.08.016/2018-19 dated May 3, 2018. For example, when ₹100 of the 8.60% GS 2028 is stripped, each cash flow of coupon (₹ 4.30 each half year) will become a coupon STRIP and the principal payment (₹100 at maturity) will become a principal STRIP. These cash flows are traded separately as independent securities in the secondary market. STRIPS in G-Secs ensure availability of sovereign zero coupon bonds, which facilitate the development of a market determined zero coupon yield curve (ZCYC). STRIPS also provide institutional investors with an additional instrument for their asset liability management (ALM). Further, as STRIPS have zero reinvestment risk, being zero coupon bonds, they can be attractive to retail/non-institutional investors. Market participants, having an SGL account with RBI can place requests directly in e-kuber for stripping/reconstitution of eligible securities (not special securities). Requests for stripping/reconstitution by Gilt Account Holders (GAH) shall be placed with the respective Custodian maintaining the CSGL account, who in turn, will place the requests on behalf of its constituents in e-kuber.

ix) Sovereign Gold Bond (SGB): SGBs are unique instruments, prices of which are linked to commodity price viz Gold. SGBs are also budgeted in lieu of market borrowing. The calendar of issuance is published indicating tranche description, date of subscription and date of issuance. The Bonds shall be denominated in units of one gram of gold and multiples thereof. Minimum investment in the Bonds shall be one gram with a maximum limit of subscription per fiscal year of 4 kg for individuals, 4 kg for Hindu Undivided Family (HUF) and 20 kg for trusts and similar entities notified by the Government from time to time, provided that (a) in case of joint holding, the above limits shall be applicable to the first applicant only; (b) annual ceiling will include bonds subscribed under different tranches during initial issuance by Government and those purchased from the secondary market; and (c) the ceiling on investment will not include the holdings as collateral by banks and other Financial Institutions. The Bonds shall be repayable on the expiration of eight years from the date of issue of the Bonds. Pre-mature redemption of the Bond is permitted after fifth year of the date of issue of the Bonds and such repayments shall be made on the next interest payment date. The bonds under SGB Scheme may be held by a person resident in India, being an individual, in his capacity as an individual, or on behalf of minor child, or jointly with any other individual. The bonds may also be held by a Trust, HUFs, Charitable Institution and University. Nominal Value of the bonds shall be fixed in Indian Rupees on the basis of simple average of closing price of gold of 999 purity published by the India Bullion and Jewelers Association Limited for the last three business days of the week preceding the subscription period. The issue price of the Gold Bonds will be ₹ 50 per gram less than the nominal value to those investors applying online and the payment against the application is made through digital mode. The Bonds shall bear interest at the rate of 2.50 percent (fixed rate) per annum on the nominal value. Interest shall be paid in half-yearly rests and the last interest shall be payable on maturity along with the principal. The redemption price shall be fixed in Indian Rupees and the redemption price shall be based on simple average of closing price of gold of 999 purity of previous 3 business days from the date of repayment, published by the India Bullion and Jewelers Association Limited. SGBs acquired by the banks through the process of invoking lien/hypothecation/pledge alone shall be counted towards Statutory Liquidity Ratio. The above subscription limits, interest rate discount etc. are as per the current scheme and are liable to change going forward.

x) 7.75% Savings (Taxable) Bonds, 2018: Government of India has decided to issue 7.75% Savings (Taxable) Bonds, 2018 with effect from January 10, 2018 in terms of GoI notification F.No.4(28) - W&M/2017 dated January 03, 2018 and RBI issued notification vide IDMD.CDD.No.1671/13.01.299/2017-18 dated January 3, 2018. These bonds may be held by (i) an individual, not being a Non-Resident Indian-in his or her individual capacity, or in individual capacity on joint basis, or in individual capacity on any one or survivor basis, or on behalf of a minor as father/mother/legal guardian and (ii) a Hindu Undivided Family. There is no maximum limit for investment in these bonds. Interest on these Bonds will be taxable under the Income Tax Act, 1961 as applicable according to the relevant tax status of the Bond holders. These Bonds will be exempt from wealth-tax under the Wealth Tax Act, 1957. These Bonds will be issued at par for a minimum amount of ₹1,000 (face value) and in multiples thereof. RBI vide its notification IDMD.CDD No.21/13.01.299/2018-19 dated July 2, 2018 has issued Master Directions on Relief/Savings Bonds providing details on appointment/delisting of brokers, payment and rates of brokerage for saving bonds and nomination facility etc.

d. State Development Loans (SDLs)

1.7 State Governments also raise loans from the market which are called SDLs. SDLs are dated securities issued through normal auction similar to the auctions conducted for dated securities issued by the Central Government (please see question 3). Interest is serviced at half-yearly intervals and the principal is repaid on the maturity date. Like dated securities issued by the Central Government, SDLs issued by the State Governments also qualify for SLR. They are also eligible as collaterals for borrowing through market repo as well as borrowing by eligible entities from the RBI under the Liquidity Adjustment Facility (LAF) and special repo conducted under market repo by CCIL. State Governments have also issued special securities under “Ujjwal Discom Assurance Yojna (UDAY) Scheme for Operational and Financial Turnaround of Power Distribution Companies (DISCOMs)” notified by Ministry of Power vide Office Memorandum (No 06/02/2015-NEF/FRP) dated November 20, 2015.

Coordinated Portfolio Investment Survey – India

Updated: जून 02, 2025

General Information

The Coordinated Portfolio Investment Survey (CPIS) is a voluntary data collection exercise conducted under the auspices of the International Monetary Fund (IMF). The purpose of the CPIS is to improve the quality of portfolio investment statistics in the international investment position (IIP)—that is, holdings of portfolio investment assets in the form of equity and investment fund shares, long-term debt securities, and short-term debt securities — and the availability of these statistics by counterpart economies. Therefore, the CPIS supports the objective of developing from-whom-to-whom cross-border data and contributes to a better understanding of financial interconnectedness.

India began participating in annual CPIS of the IMF since 2004. Thereafter, as per IMF’s recommendation under G-20 Data Gaps Initiative (DGI), India moved to semi-annual reporting of CPIS in 2014, as per India’s commitment under Special Data Dissemination Standards (SDDS). The Reserve Bank of India submits the CPIS data to IMF on behalf of India.

Confidentiality Clause

The entity-wise information collected under the CPIS are kept confidential and only consolidated aggregates are submitted by the Reserve Bank of India to IMF.

Eligible entities and requirements to report under CPIS

Ans: Presently the banks, mutual fund companies, non-financial companies, non-banking financial companies and insurance companies are surveyed under the CPIS.

Biennial survey on Foreign Collaboration in Indian Industry (FCS)

Updated: जून 02, 2025

General Instructions

The Reserve Bank has been conducting FCS Survey for a long time because it is not only beneficial for the researchers but also helpful for the industries as it gives them an idea of the potential areas of competition. After introduction of the mandatory FLA census in 2011, this survey was restructured in 2012 to supplement the FLA census.

The survey captures information on a wide range of indicators of performance (production, exports, imports, cost of material, etc.,) along with the crucial features of technology transfer agreements (nature, duration, mode of payment, export restriction, provision of exclusive rights, use of technology after expiry of the agreements, etc.).

The survey is currently conducted biennially for Indian direct investment companies which have entered into foreign technical collaboration agreements with foreign companies as at end-March of the two financial years.

The survey is launched via RBI press release. Simultaneously, email notifications are also sent to the reporting entities along with excel based survey schedules. Reporting entities then submit duly filled-in survey schedule to generic email id of RBI, which are then processed on RBI’s internal intranet portal.

The data submitted by reporting entities are analysed internally and aggregate level results are published on RBI website biennially.

Confidentiality Clause

The company-wise information provided will be kept confidential and only consolidated aggregates will be released by the Reserve Bank.

Note: The respondent companies should fill-up the survey schedule in excel format (*.xls format) available on RBI website. Respondents are requested to read the Instruction sheet (available in survey schedule) thoroughly before filling the survey schedule.

Important points to remember while participating in FCS survey

Ans.: The respondent companies should follow the below-mentioned points while filling the survey schedule:

-

The company must use the latest survey schedule which is in .xls format without any macros.

-

The company is required to save the survey schedule in Excel 97-2003 workbook i.e., in .xls format only.

-

In order to save the survey schedule in .xls format, follow the below-mentioned steps:

a. Go to Office Button / File → Save As → Save As type

b. Select “Excel 97-2003 Workbook” and Save the survey schedule in .xls format. -

The company must use the .xls format of the survey schedule provided by RBI and are requested not to incorporate any macros in the survey schedule while submitting the same.

-

Please note that survey schedules submitted in any other format (other than .xls format) will be auto rejected by the system.

-

Please ensure, all information furnished in the survey schedule are complete and no information is missed out.

-

After filling Part-I to III, the company has to fill the Declaration sheet. The Declaration sheet helps in confirming and validating that the information entered by the company are double checked before submitting the same to RBI. This would help to avoid errors like data entry errors, missed data etc.

-

Further the respondents are requested to not use any special characters i.e., [!@#$%^&*_()] and comma while data filing in all parts of survey schedule.

Core Investment Companies

Updated: मे 08, 2025

FOREWORD

The Reserve Bank of India is entrusted with the responsibility of regulating and supervising the Non-Banking Financial Companies by virtue of powers vested in Chapter III B of the Reserve Bank of India Act, 1934. Accordingly, Reserve Bank has issued the Master Direction DoR(NBFC).PD.003/03.10.119/2016-17 dated August 25, 2016 for regulating Core Investment Companies (CICs).

It has been felt necessary to explain the rationale underlying the regulatory framework and provide clarification on certain operational matters for the benefit of the CICs, members of public, rating agencies, Chartered Accountants etc. To meet this need, the clarifications in the form of questions and answers, is being brought out by the Reserve Bank of India .

The Frequently Asked Questions (FAQs) are listed under four broad categories viz., (A) Definitions, (B) Registration and related matters, (C) Overseas Investments/ ECB, and (D) Miscellaneous. The information given in the FAQ on CICs is of general nature for the benefit of the public and the clarifications given do not substitute the extant regulatory directions/instructions issued by the Bank to the CICs.

A. Definitions:

Ans. A CIC is a Non-Banking Financial Company

(i) with asset size of ₹ 100 crore and above;

(ii) carrying on the business of acquisition of shares and securities and which satisfies the following conditions as on the date of the last audited balance sheet;

(iii) it holds not less than 90% of its net assets in the form of investment in equity shares, preference shares, bonds, debentures, debt or loans in group companies;

(iv) its investments in the equity shares (including instruments compulsorily convertible into equity shares within a period not exceeding 10 years from the date of issue) in group companies and units of Infrastructure Investment Trusts (InvITs) only as sponsor constitutes not less than 60% of its net assets as mentioned in clause (iii) above;

(v) Provided that the exposure of such CICs towards InvITs shall be limited to their holdings as sponsors and shall not, at any point in time, exceed the minimum holding of units and tenor prescribed in this regard by SEBI (Infrastructure Investment Trusts) Regulations, 2014, as amended from time to time. It does not trade in its investments in shares, bonds, debentures, debt or loans in group companies except through block sale for the purpose of dilution or disinvestment;

(vi) it does not carry on any other financial activity referred to in Section 45I(c) and 45I(f) of the RBI act, 1934 except investment in bank deposits, money market instruments including money market mutual funds that make investments in debt/money market instruments with a maturity of up to 1 year, government securities, loans to and investments in debt issuances of group companies or guarantees issued on behalf of group companies;

(vii) it accepts public funds.

FAQs on Priority Sector Lending (PSL)

Updated: मे 08, 2025

A. Classification of loans

Clarification : Priority Sector Lending (PSL) eligibility of loans outstanding as on April 1, 2025 shall be determined with reference to the provisions of the Master Directions on Priority Sector Lending 2025

B. Computation of Adjusted Net Bank Credit (ANBC)

Clarification : The net PSLC outstanding (PSLC Buy minus(-) PSLC Sell) is added to the Net Bank Credit, as mentioned in para 6 of the Master Directions on Priority Sector Lending, 2025 (updated from time to time). Further, a PSLC remains outstanding until its expiry (s. no. ix of Annex to circular on Priority Sector Lending certificates dated April 07, 2016). All PSLCs will expire by March 31st and will not be valid beyond the reporting date (i.e. March 31st), irrespective of the date it was first bought/sold. Accordingly, the effect of PSLC buy is increase in ANBC and conversely the effect of PSLC sell is decrease in ANBC and the net of PSLC buy/sell is adjusted to the ANBC for every quarter. Thus, PSLCs bought or sold in any quarter of a FY will have to be taken into account in all subsequent quarters till the end of that FY.

Clarification:

(i) Outstanding deposits with NABARD made on account of PSL shortfall are eligible to be reckoned towards Agriculture sub-target and count for the achievement of overall PSL target as well.

(ii) Outstanding deposits with SIDBI and MUDRA are eligible to be reckoned under MSME lending and count for the achievement of the overall PSL target.

(iii) Outstanding deposits with NHB are eligible to be reckoned under Housing and count for the achievement of overall PSL target.

(iv) All outstanding deposits as above shall be added to Net Bank Credit (NBC) for the computation of ANBC.

Clarification: (i) In terms of the circulars mentioned above, the amount eligible for exclusion from ANBC is the incremental advances extended out of the resources generated from the eligible incremental FCNR (B) / NRE deposits. The incremental advance is calculated as the difference between outstanding advances in India as on March 7, 2014 and the Base Date (July 26, 2013).

(ii) The amount to be excluded from ANBC for computation of priority sector targets will not exceed incremental FCNR (B) / NRE deposits eligible for exemption from maintenance of CRR / SLR in terms of the circulars mentioned above.

(iii) In case, the difference in the amount of outstanding advances between March 7, 2014 and base date is zero or negative, no amount would be eligible for deduction from ANBC for the purpose of arriving at the priority sector lending targets.

Clarification: The bills purchased/ discounted/ negotiated (payment to beneficiary not under reserve) under LC is allowed to be treated as interbank exposure only for the limited purpose of computing exposure and capital requirements. It should not be excluded from the computation of ‘bank credit in India’ [As prescribed in item No.VI of Form 'A’ under Section 42(2) of the RBI Act, 1934] which allows for exclusion of interbank advance. While exposure may be to the LC issuing bank, the bills purchased/discounted amount to bank credit to its borrower constituent. If this advance is eligible for priority sector classification, the bank can classify it as PSL. Banks have to take note of the above aspect while reporting Net Bank Credit in India as well as while computing the Adjusted Net Bank Credit for PSL targets and achievement.

Housing Loans

Your bank will assess your repayment capacity while deciding the home loan eligibility. Repayment capacity is based on your monthly disposable / surplus income, (which in turn is based on factors such as total monthly income / surplus less monthly expenses) and other factors like spouse's income, assets, liabilities, stability of income etc. The main concern of the bank is to make sure that you comfortably repay the loan on time and ensure end use. The higher the monthly disposable income, higher will be the amount you will be eligible for loan. Typically a bank assumes that about 55-60 % of your monthly disposable / surplus income is available for repayment of loan. However, some banks calculate the income available for EMI payments based on an individual’s gross income and not on his disposable income.

The amount of the loan depends on the tenure of the loan and the rate of interest also as these variables determine your monthly outgo / outflow which in turn depends on your disposable income. Banks generally fix an upper age limit for home loan applicants.

Targeted Long Term Repo Operations (TLTROs)

Ans: Under TLTRO scheme, banks will have to invest the amount borrowed under TLTROs in fresh acquisition of securities (i.e., over and above their outstanding statement in specified securities it was holding as on March 26, 2020) from primary/secondary market. However, participation in TLTRO scheme will not impinge on the existing investment of the bank and the bank may continue to operate their AFS/HFT portfolio, as hitherto, in terms of extant regulatory/internal guidelines.

FAQs on Non-Banking Financial Companies

Registration

Remittances (Money Transfer Service Scheme (MTSS) and Rupee Drawing Arrangement (RDA))

Rupee Drawing Arrangement (RDA)

Domestic Deposits

I. Domestic Deposits

Annual Return on Foreign Liabilities and Assets (FLA) under FEMA 1999

Eligible entities and requirements to submit the FLA return

Ans: Entities who comply with the criterion mentioned in Q1 are mandatorily required to submit the FLA return under FEMA 1999 based on audited/ unaudited accounts of the entity by July 15 every year.

Framework for Compromise Settlements and Technical Write-offs

A. COMPROMISE SETTLEMENT IN WILFUL DEFAULT AND FRAUD CASES

No. The penal measures currently applicable to borrowers classified as fraud or wilful defaulter in terms of the Master Directions on Frauds dated July 1, 2016 and the Master Circular on Wilful Defaulters dated July 1, 2015, respectively, remain unchanged and shall continue to be applicable in cases where the banks enter into compromise settlement with such borrowers.

Such penal measures entail inter alia that no additional facilities should be granted by any bank/ FI to borrowers listed as wilful defaulters, and that such companies (including their entrepreneurs/ promoters) get debarred from institutional finance for floating new ventures for a period of five years from the date of removal of their name from the list of wilful defaulters. In addition, borrowers classified as fraud are debarred from availing bank finance for a period of five years from the date of full payment of the defrauded amount.

Retail Direct Scheme

Scheme related queries

Opening an RDG account will allow individuals to buy Government securities directly in the primary market (auctions) as well as buy/sell in the secondary market. For the retail investor, Government securities offer an option for long term investment. The advantages for retail investors can be listed as under:

-

G-sec are risk free: G-sec in the domestic market context are risk free and carry no credit risk.

-

G-sec offer decent yields for longer duration. G-sec yield curve extends up to 40 years. With Government issuing securities at different points on the yield curve, G-sec offer an attractive option for savers who need low risk investment options for longer durations.

-

G-sec offer prospect of capital gains: As there is an inverse relationship between bond price and interest rate, there is a prospect of capital gains when the interest rates moderate. One, however, must be conscious of market risks that could result in losses in case the interest rate cycle reverses.

-

G-sec have reasonable liquidity: G-sec have reasonable liquidity and can be transacted on NDS-OM. With the introduction of Retail Direct Portal, retail investors can now participate easily in primary and secondary market.

-

G-sec help to diversify portfolio: Investments in government securities would help in portfolio diversification and consequently reduce risk for retail investors.

-

Zero charges under Retail Direct Scheme: Retail Direct Account is completely free of charge and does not involve any intermediary. It would reduce overall transaction charges for individual investors in terms of the charges which they are otherwise required to pay for investing through aggregators or taking indirect exposure through mutual funds.

Business restrictions imposed on Paytm Payments Bank Limited vide Press Releases dated January 31 and February 16, 2024

Bank Accounts with Paytm Payments Bank

No. After March 15, 2024, you will not be able to deposit money into your account with Paytm Payments Bank. No credits or deposits other than interest, cashbacks, sweep-in from partner banks or refunds are allowed to be credited.

Government Securities Market in India – A Primer

2.1 Holding of cash in excess of the day-to-day needs (idle funds) does not give any return. Investment in gold has attendant problems in regard to appraising its purity, valuation, warehousing and safe custody, etc. In comparison, investing in G-Secs has the following advantages:

-

Besides providing a return in the form of coupons (interest), G-Secs offer the maximum safety as they carry the Sovereign’s commitment for payment of interest and repayment of principal.

-

They can be held in book entry, i.e., dematerialized/ scripless form, thus, obviating the need for safekeeping. They can also be held in physical form.

-

G-Secs are available in a wide range of maturities from 91 days to as long as 40 years to suit the duration of varied liability structure of various institutions.

-

G-Secs can be sold easily in the secondary market to meet cash requirements.

-

G-Secs can also be used as collateral to borrow funds in the repo market.

-

Securities such as State Development Loans (SDLs) and Special Securities (Oil bonds, UDAY bonds etc) provide attractive yields.

-

The settlement system for trading in G-Secs, which is based on Delivery versus Payment (DvP), is a very simple, safe and efficient system of settlement. The DvP mechanism ensures transfer of securities by the seller of securities simultaneously with transfer of funds from the buyer of the securities, thereby mitigating the settlement risk.

-

G-Sec prices are readily available due to a liquid and active secondary market and a transparent price dissemination mechanism.

-

Besides banks, insurance companies and other large investors, smaller investors like Co-operative banks, Regional Rural Banks, Provident Funds are also required to statutory hold G-Secs as indicated below:

A. Primary (Urban) Co-operative Banks (UCBs)

2.2 Section 24 (2A) of the Banking Regulation Act 1949, (as applicable to co-operative societies) provides that every primary (urban) cooperative bank shall maintain liquid assets, the value of which shall not be less than such percentage as may be specified by Reserve Bank in the Official Gazette from time to time and not exceeding 40% of its DTL in India as on the last Friday of the second preceding fortnight (in addition to the minimum cash reserve ratio (CRR) requirement). Such liquid assets shall be in the form of cash, gold or unencumbered investment in approved securities. This is referred to as the Statutory Liquidity Ratio (SLR) requirement. It may be noted that balances kept with State Co-operative Banks / District Central Co-operative Banks as also term deposits with public sector banks are now not eligible for being reckoned for SLR purpose w.e.f April 1, 2015.

B. Rural Co-operative Banks

2.3 As per Section 24 of the Banking Regulation Act 1949, the State Co-operative Banks (SCBs) and the District Central Co-operative Banks (DCCBs) are required to maintain assets as part of the SLR requirement in cash, gold or unencumbered investment in approved securities the value of which shall not, at the close of business on any day, be less than such per cent, as prescribed by RBI, of its total net demand and time liabilities. DCCBs are allowed to meet their SLR requirement by maintaining cash balances with their respective State Co-operative Bank.

C. Regional Rural Banks (RRBs)

2.4 Since April 2002, all the RRBs are required to maintain their entire Statutory Liquidity Ratio (SLR) holdings in Government and other approved securities.

D. Provident funds and other entities

2.5 The non- Government provident funds, superannuation funds and gratuity funds are required by the Central Government, effective from January 24, 2005, to invest 40% of their incremental accretions in Central and State G-Secs, and/or units of gilt funds regulated by the Securities and Exchange Board of India (SEBI) and any other negotiable security fully and unconditionally guaranteed by the Central/State Governments. The exposure of a trust to any individual gilt fund, however, should not exceed five per cent of its total portfolio at any point of time. The investment guidelines for non- Government PFs have been recently revised in terms of which minimum 45% and up to 50% of investments are permitted in a basket of instruments consisting of (a) G-Secs, (b) Other securities (not in excess of 10% of total portfolio) the principal whereof and interest whereon is fully and unconditionally guaranteed by the Central Government or any State Government SDLs and (c) units of mutual funds set up as dedicated funds for investment in G-Secs (not more than 5% of the total portfolio at any point of time and fresh investments made in them shall not exceed 5% of the fresh accretions in the year), effective from April 2015.

External Commercial Borrowings (ECB) and Trade Credits

A. BASIC QUERIES

All you wanted to know about NBFCs

A. Definitions

Financial activity as principal business is when a company’s financial assets constitute more than 50 per cent of the total assets (netted off by intangible assets) and income from financial assets constitute more than 50 per cent of the gross income. A company which fulfils both these criteria needs to get registered as NBFC with the Reserve Bank. The term 'principal business' has not been defined in the Reserve Bank of India Act, 1934. Hence, the Reserve Bank has defined it vide Press Release 1998-99/1269 dated April 08, 1999 so as to ensure that only companies predominantly engaged in financial activity get registered with it and are regulated and supervised by it. Hence, if there are companies engaged in agricultural operations, industrial activity, purchase and sale of goods, providing services or purchase, sale or construction of immovable property as their principal business and are doing some financial business in a small way, they will not be regulated by the Reserve Bank. Interestingly, this test is popularly known as 50-50 test and is applied to determine whether or not a company is into financial business.

Indian Currency

A) Basics of Indian Currency/Currency Management

Legal Tender is a coin or a banknote that is legally tenderable for discharge of debt or obligation.

The coins issued by Government of India under Section 6 of The Coinage Act, 2011, shall be legal tender in payment or on account provided that a coin has not been defaced and has not lost weight so as to be less than such weight as may be prescribed in its case. Coin of any denomination not lower than one rupee shall be legal tender for any sum not exceeding one thousand rupee in any single transaction. Fifty paise (half rupee) coin shall be legal tender for any sum not exceeding ten rupee. While anyone cannot be forced to accept coins beyond the limits mentioned above, voluntarily accepting coins for amounts exceeding the limits mentioned above is not prohibited.

Every banknote issued by Reserve Bank of India (₹2, ₹5, ₹10, ₹20, ₹50, ₹100, ₹200, ₹500, and ₹2000*), unless withdrawn from circulation, shall be legal tender at any place in India in payment or on account for the amount expressed therein, and shall be guaranteed by the Central Government, subject to provisions of sub-section (2) Section 26 of RBI Act, 1934. ₹1 notes issued by Government of India are also Legal Tender. ₹500 and ₹1000 banknotes of Mahatma Gandhi series issued up to November 08, 2016, have ceased to be Legal Tender with effect from the midnight of November 8, 2016.

*₹2000 denomination notes continue to be legal tender. For more details, please refer to our press release 2023-2024/851 dated September 01, 2023 (https://website.rbi.org.in/web/rbi/-/press-releases/withdrawal-of-%E2%82%B92000-denomination-banknotes-status-56301).

Foreign Investment in India

Coordinated Portfolio Investment Survey – India

Updated: जून 03, 2024

Eligible entities and requirements to report under CPIS

Ans: Presently, the survey is conducted half-yearly in India for capturing the end-March and end-September position of the previous financial year (FY).

Biennial survey on Foreign Collaboration in Indian Industry (FCS)

Details of survey launch

Ans.: The RBI launches the FCS survey during the month of June every year with the last two financial year end-March as the reference date.

Core Investment Companies

A. Definitions:

Ans: CICs (a) with an asset size of less than ₹100 crore, irrespective of whether accessing public funds or not and (b) with an asset size of ₹100 crore and above and not accessing public funds are not required to register with the Bank under Section 45IA of the RBI Act, 1934 in terms of para 6 of Master Direction DoR(NBFC).PD.003/03.10.119/2016-17, and are termed as ‘Unregistered CICs’. An Unregistered CIC as per the aforementioned criteria is not required to submit any application to continue as Unregistered CIC. Such Unregistered CICs are exempted from the regulation of Reserve Bank. However, if they wish to make overseas investments in the financial sector, they are required to hold a Certificate of Registration from the Reserve Bank and have a prior approval of the Bank as required in para 34 of the Master Direction.

FAQs on Priority Sector Lending (PSL)

C. Adjustment for Weights in PSL Achievement

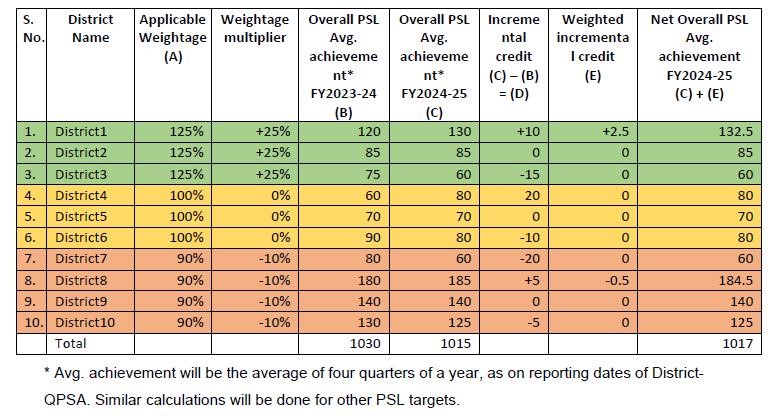

Clarification: If there is a decline in credit, the weighted incremental credit will be zero (0). The methodology as given below will be considered for all the districts for which data is reported in ADEPT and District-QPSA statement. Further, based on the methodology detailed below, banks are expected to monitor their own PSL achievement during the year taking into account the prescription of differential weights for credit in identified districts, for the purpose of trading in PSLCs.

Clarification: For mapping a credit facility to a particular district, the ‘place of utilization of credit’ shall be the qualifying criteria.

Clarification: While calculating district-wise incremental credit for assigning weights, the organic credit i.e. only the credit directly disbursed by banks and for which the actual borrower/beneficiary wise details are maintained in the books of the bank, will be considered. Credit disbursed through the following inorganic routes shall not be considered for incremental weights.

- Investments by banks in securitised assets

- Transfer of Assets through Direct Assignment/Outright purchase

- Inter Bank Participation Certificates (IBPCs)

- Priority Sector Lending Certificates (PSLCs)

- Bank loans to MFIs (NBFC-MFIs, Societies, Trusts, etc.) for on-lending

- Bank loans to NBFCs for on-lending

Bank loans to HFCs for on-lending

D. Agriculture

Clarification: The PSL guidelines are activity and beneficiary specific and are not based on type of collateral. Therefore, bank loans given to individuals/ businesses for undertaking agriculture activities do not automatically become ineligible for priority sector classification, only on account of the fact that underlying asset is gold jewellery/ornament etc. It may, however, be noted that as per FIDD Circular dated December 6, 2024, it has been advised that banks may waive collateral security and margin requirements for agricultural loans upto ₹2 lakh. Therefore, bank should have extended the loan based on scale of finance and assessment of credit requirement for undertaking the agriculture activity and not solely based on available collateral in the form of gold. Further, as applicable to all loans under PSL, banks should put in place proper internal controls and systems to ensure that the loans extended under PSL are for approved purposes and the end use is continuously monitored.

Housing Loans

Targeted Long Term Repo Operations (TLTROs)

Ans: There is no maturity restriction on the specified securities to be acquired under TLTRO scheme. However, the outstanding amount of specified securities in bank’s HTM portfolio should not fall below the level of amount availed under TLTRO scheme.

FAQs on Non-Banking Financial Companies

Registration

Framework for Compromise Settlements and Technical Write-offs

A. COMPROMISE SETTLEMENT IN WILFUL DEFAULT AND FRAUD CASES

No. The cooling period has been introduced as a general prescription for normal cases of compromise settlements, without prejudice to the penal measures applicable in respect of borrowers classified as fraud or wilful defaulter as per the Master Directions on Frauds dated July 1, 2016 and the Master Circular on Wilful Defaulters dated July 1, 2015, respectively, as mentioned at (2) above.

Remittances (Money Transfer Service Scheme (MTSS) and Rupee Drawing Arrangement (RDA))

Rupee Drawing Arrangement (RDA)

भारतीय रिझर्व्ह बँक मोबाईल ॲप्लिकेशन इंस्टॉल करा आणि नवीनतम बातम्यांचा त्वरित ॲक्सेस मिळवा!