|

On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (February 8, 2024) decided to:

- Keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 6.50 per cent.

Consequently, the standing deposit facility (SDF) rate remains unchanged at 6.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 6.75 per cent.

- The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

Assessment and Outlook

- Global growth is likely to remain steady in 2024 after a surprisingly resilient performance in a turbulent year gone by. Inflation is edging down from multi-decade highs, with intermittent upticks. Financial market sentiments have been fluctuating with changing views about an early pivot by central banks in advanced economies (AEs). The likelihood of lower interest rates has spurred rallies in equity markets, although uncertainty about the timing of interest rate reduction is reflected in bidirectional movements in the US dollar and sovereign bond yields. Emerging market economies (EMEs) are facing currency fluctuations amidst volatile capital flows.

- Domestic economic activity is strengthening. As per the first advance estimates (FAE) released by the National Statistical Office (NSO), real gross domestic product (GDP) is expected to grow by 7.3 per cent, year-on-year (y-o-y) in 2023-24, underpinned by strong investment activity. On the supply side, gross value added (GVA) expanded by 6.9 per cent in 2023-24, with manufacturing and services sectors as the key drivers.

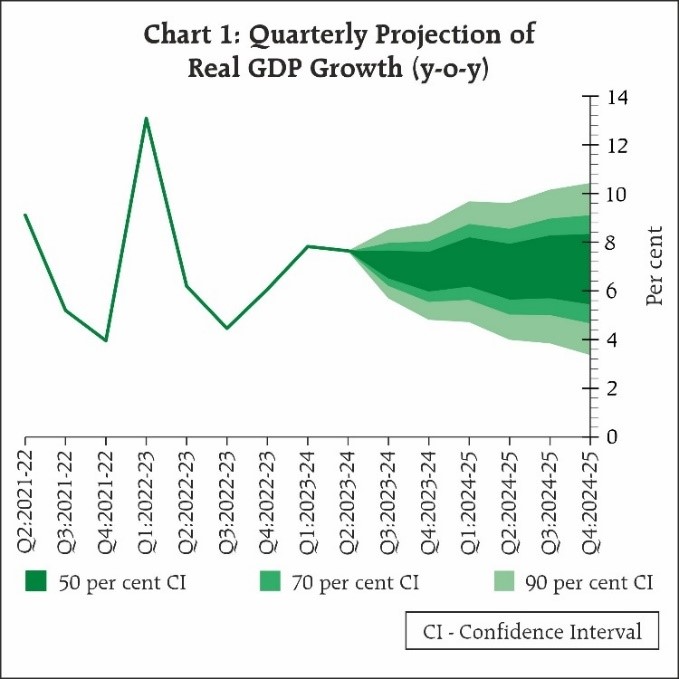

- Looking ahead, recovery in rabi sowing, sustained profitability in manufacturing and underlying resilience of services should support economic activity in 2024-25. Among the key drivers on demand side, household consumption is expected to improve, while prospects of fixed investment remain bright owing to upturn in the private capex cycle, improved business sentiments, healthy balance sheets of banks and corporates; and government’s continued thrust on capital expenditure. Improving outlook for global trade and rising integration in global supply chain will support net external demand. Headwinds from geopolitical tensions, volatility in international financial markets and geoeconomic fragmentation, however, pose risks to the outlook. Taking all these factors into consideration, real GDP growth for 2024-25 is projected at 7.0 per cent with Q1 at 7.2 per cent; Q2 at 6.8 per cent; Q3 at 7.0 per cent; and Q4 at 6.9 per cent (Chart 1). The risks are evenly balanced.

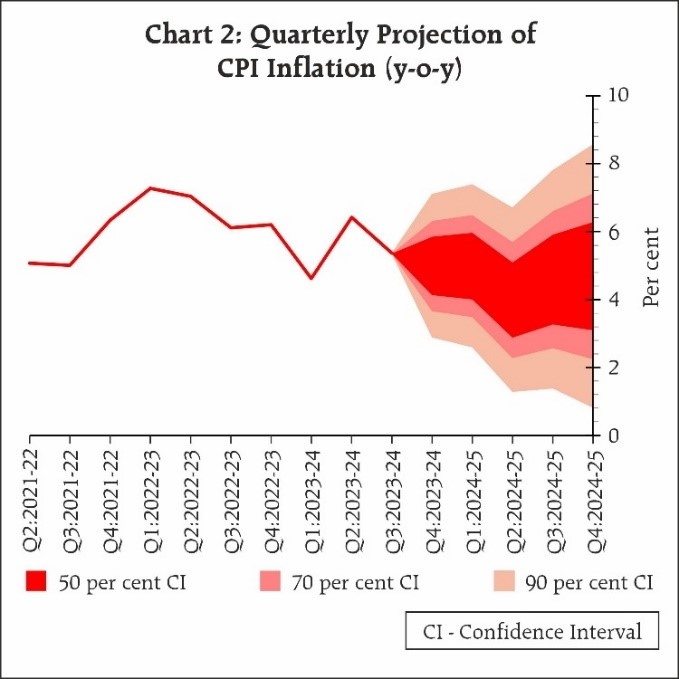

- From its October 2023 trough of 4.9 per cent, CPI inflation increased successively in the next two months to 5.7 per cent by December. Food inflation, primarily y-o-y vegetable price increases, drove the pick-up in headline inflation, even as deflation in fuel deepened. Core inflation (CPI inflation excluding food and fuel) softened to a four-year low of 3.8 per cent in December.

- Going forward, the inflation trajectory would be shaped by the evolving food inflation outlook. Rabi sowing has surpassed last year’s level. The usual seasonal correction in vegetable prices is continuing, though unevenly. Yet considerable uncertainty prevails on the food price outlook from the possibility of adverse weather events. Effective supply side responses may keep food price pressures under check. The continuing pass-through of monetary policy actions and stance is keeping core inflation muted. Crude oil prices, however, remain volatile. Manufacturing firms covered in the Reserve Bank’s enterprise surveys expect some softening in the growth of input costs and selling prices in Q4:2023-24, while services and infrastructure firms expect higher input cost pressures and growth in selling prices. Taking into account these factors, CPI inflation is projected at 5.4 per cent for 2023-24 with Q4 at 5.0 per cent. Assuming a normal monsoon next year, CPI inflation for 2024-25 is projected at 4.5 per cent with Q1 at 5.0 per cent; Q2 at 4.0 per cent; Q3 at 4.6 per cent; and Q4 at 4.7 per cent (Chart 2). The risks are evenly balanced.

- The MPC noted that domestic economic activity is holding up well and is expected to be backed by the momentum in investment demand, optimistic business sentiments and rising consumer confidence. On the inflation front, large and repetitive food price shocks are interrupting the pace of disinflation that is led by the moderation of core inflation. Geopolitical events and their impact on supply chains, and volatility in international financial markets and commodity prices are key sources of upside risks to inflation. The cumulative effect of policy repo rate increases is still working its way through the economy. The MPC will carefully monitor any signs of generalisation of food price pressures to non-food prices which can fritter away the gains in the easing of core inflation. As the path of disinflation needs to be sustained, the MPC decided to keep the policy repo rate unchanged at 6.50 per cent in this meeting. Monetary policy must continue to be actively disinflationary to ensure anchoring of inflation expectations and fuller transmission. The MPC will remain resolute in its commitment to aligning inflation to the target. The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth.

- Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to keep the policy repo rate unchanged at 6.50 per cent. Prof. Jayanth R. Varma voted to reduce the policy repo rate by 25 basis points.

- Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth. Prof. Jayanth R. Varma voted for a change in stance to neutral.

- The minutes of the MPC’s meeting will be published on February 22, 2024.

- The next meeting of the MPC is scheduled during April 3 to 5, 2024.

(Yogesh Dayal)

Chief General Manager

Press Release: 2023-2024/1826

|

IST,

IST,