Notes on Tables - ଆରବିଆଇ - Reserve Bank of India

Notes on Tables

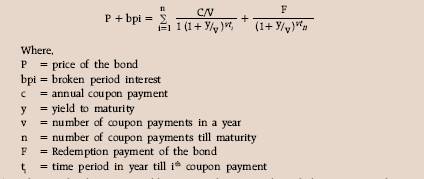

Table No. 1 (1) Annual data are averages of the months. The gold reserves of Issue Department were valued at Rs.84.39 per 10 grams up to October 16, 1990 and from October 17, 1990 they are valued close to international market prices. The expression ‘Banking System’ or ‘Banks’ means (a) State Bank of India and its associates (b) Nationalised Banks (c) Banking companies as defined in clause ‘C’ of Section 5 of the Banking Regulation Act, 1949 (d) Co-operative banks (as far as scheduled co-operative banks are concerned) (e) Regional Rural Banks and (f) any other financial institution notified by the Central Government in this regard. (1) Excludes borrowings of any scheduled state co-operative bank from the State Government and any Reserve Fund deposit required to be maintained with such bank by any co-operative society within the area of operation of such bank. (2) Deposits of co-operative banks with scheduled state co-operative banks are excluded from this item but are included under ‘Aggregate deposits’. (3) Excludes borrowings of regional rural banks from their sponsor banks. (4) Wherever it has not been possible to provide the data against the item ‘Other demand and time liabilities’ under ‘Liabilities to the Banking System’ separately, the same has been included in the item ‘Other demand and time liabilities’ under ‘Liabilities to others’. (5) Data reflect redemption of India Millennium Deposits (IMDs) on December 29, 2005. (6) Other than from the Reserve Bank of India, NABARD and Export-Import Bank of India. (7) Figures relating to scheduled banks’ borrowings in India are those shown in the statement of affairs of the Reserve Bank of India. Borrowings against usance bills and/or promissory notes are under section 17(4) of the Reserve Bank of India Act, 1934. (8) Includes borrowings by scheduled state co-operative banks under Section 17(4AA) of the Reserve Bank of India Act, 1934. (9) As per the Statement of Affairs of the Reserve Bank of India. (10) Advances granted by scheduled state co-operative banks to co-operative banks are excluded from this item but included under ‘Loans, cash-credits and overdrafts’. (11) At book value; it includes treasury bills and treasury receipts, treasury savings certificates and postal obligations. (12) Includes participation certificates (PCs) issued by scheduled commercial banks to other banks and financial institutions. (13) Includes participation certificates (PCs) issued by scheduled commercial banks to others. (14) Figures in brackets relate to advances of scheduled commercial banks for financing food procurement operations. (1) Total of demand and time deposits from ‘Others’. (2) Includes borrowings from the Industrial Development Bank of India and National Bank for Agriculture and Rural Development. (3) At book value; includes treasury bills and treasury receipts, treasury savings certificates and postal obligations. (4) Total of ‘Loans, cash credits and overdrafts’ and ‘Bills purchased and discounted’. (5) Includes advances of scheduled state co-operative banks to central co-operative banks and primary cooperative banks. With a view to enable the banks to meet any unanticipated additional demand for liquidity in the context of the century date change, a ‘Special Liquidity Support’ (SLS) facility was made available to all scheduled commercial banks (excluding RRBs) for a temporary period from December 1, 1999 to January 31, 2000. (1) With effect from April 13,1996, banks are provided export credit refinance against their rupee export credit and post-shipment export credit denominated in U.S. Dollars taken together. (2) General Refinance Facility was replaced by Collateralised Lending Facility (CLF)/Additional Collateralised Facility (ACLF) effective April 21, 1999. ACLF was withdrawn with the introduction of Liquidity Adjustment Facility (LAF), effective June 5, 2000. CLF was withdrawn completely effective October 5, 2002. (3) Special Liquidity Support Facility which was introduced effective September 17, 1998 was available upto March 31, 1999. (4) Post-shipment credit denominated in US dollars (PSCFC) scheme was withdrawn effective February 8, 1996 and the refinance facility thereagainst was withdrawn effective April 13, 1996. The scheme of government securities refinance was terminated effective July 6, 1996. (a) The data includes cheque clearing for both i.e. clearing houses managed by Reserve Bank of India and clearing houses managed by other banks. Paper based inter-bank clearing has been discontinued at all the centres, the last June, 2005. “The other MICR Centres are Agra, Allahabad, Amritsar, Aurangabad, Baroda, Bhilwara, Coimbatore, Dehradun, Ernakulum, Erode, Gorakhpur, Gwalior, Hubli, Indore ,Jabalpur, Jalandhar, Jamshedpur, Jammu, Jodhpur, Kolhapur, Kozhikode, Lucknow, Ludhiana, Madurai, Mangalore, Mysore, Nasik, Panaji, Pondicherry, Pune, Raipur, Rajkot, Ranchi, Salem, Sholapur, Surat, Thiruchirapalli, Tirupur, Thrissur, Udaipur, Varanasi, Vijayawada and Vishakhapatnam.“ (b) Graphs: The graphs 3 and 4 on Paper and Electronic payments - the Electronic Payment System data include Retail Electronic Payment Systems, RTGS (customer and inter-bank) and CCIL operated systems.“ (c) Non MICR Data pertains to the Clearing Houses managed by 10 banks namely SBI (688), SBBJ (50), SB Indore (27), PNB (3), SBT (81), SBP (52), SBH (51), SBS (28), SBM (46) and United Bank of India (4). (Figures in bracket indicate Non MICR Cheque Clearing Houses managed by the bank.)“ (d) The other MICR Centres includes 43 centres managed by 13 PSBs namely Andhra Bank, Bank of Baroda, Bank of India, Canara Bank, Central Bank of India, Corporation Bank, Oriental Bank of Commerce, Punjab National Bank, State Bank of India, State Bank of Indore, State Bank of Travancore, State Bank of Hyderabad and Union Bank of India." Table No. 9A The data pertain to retail electronic payment. The data pertain to Large Value Payment Systems. The figures for CCIL, the operations pertain to selected services, are taken from the CCIL published data. (a) For details of money stock measures according to the revised series, reference may be made to January 1977 issue of this Bulletin (pages 70-134). (b) Banks include commercial and co-operative banks. (C) Financial year data relate to March 31, except scheduled commercial banks’ data which relate to the last reporting Friday of March. For details, see the note on page S 963 of October 1991 issue of this Bulletin. (d) Scheduled commercial banks’ time deposits reflect redemption of Resurgent India Bonds (RIBs), since October 1, 2003 and of India Millennium Deposits (IMDs) since December 29, 2005. (e) Data are provisional. (1) Net of return of about Rs.43 crore of Indian notes from Pakistan upto April 1985. (2) Estimated : ten-rupee commemorative coins issued since October 1969, two-rupee coins issued since November 1982 and five-rupee coins issued since November 1985 are included under rupee coins. (3) Excludes balances held in IMF Account No.1, Reserve Bank of India Employees’ Provident Fund, Pension Fund, Gratuity and Superannuation Fund and Co-operative Guarantee Fund, the amount collected under the Additional Emoluments (Compulsory Deposit) Act, 1974 and the Compulsory Deposit Scheme (Income-Tax Payers’) Act. (f) Revised in line with the new accounting standards and consistent with the Methodology of Compilation (June 1998). The revision is in respect of pension and provident funds with commercial banks which are classified as other demand and time liabilities and includes those banks which have reported such changes so far. (a) On the establishment of National Bank for Agriculture and Rural Development (NABARD), on July 12, 1982, certain assets and liabilities of the Reserve Bank were transferred to NABARD, necessitating some reclassification of aggregates in the sources of money stock from that date. (b) Please see item (c) of notes to Table 10. (C) Data are provisional. (1) Includes special securities and also includes Rs.751.64 crore (equivalent of SDRs 211.95 million) incurred on account of Reserve Assets subscription to the IMF towards the quota increase effective December 11, 1992. (2) Represents investments in bonds/shares of financial institutions, loans to them and holdings of internal bills purchased and discounted. Excludes since the establishment of NABARD, its refinance to banks. (3) Inclusive of appreciation in the value of gold following its revaluation close to international market price effective October 17, 1990. Such appreciation has a corresponding effect on Reserve Bank’s net non-monetary liabilities. The conceptual basis of the compilation of the Commercial Bank Survey are available in the report of the Working Group on Money Supply: Analytics and Methodology of Compilation (Chairman: Dr. Y.V.Reddy), RBI Bulletin, July 1998, which recommended changes in the reporting system of commercial banks and the article entitled “New Monetary Aggregates: An Introduction”, RBI Bulletin, October 1999. (1) Time Deposits of Residents : These do not reckon non-residents’ foreign currency repatriable fixed deposits (such as FCNR(B) deposits, Resurgent India Bonds (RIBs) and India Millennium Deposits (IMDs)) based on the residency criterion and exclude banks’ pension and provident funds because they are in the nature of other liabilities and are included under ‘other demand and time liabilities’. (3) Domestic Credit : It includes investments of banks in non-SLR securities, comprising commercial paper, shares and bonds issued by the public sector undertakings, private sector and public financial institutions and net lending to primary dealers in the call/term money market, apart from investment in government and other approved securities and conventional bank credit (by way of loans, cash credit, overdrafts and bills purchased and discounted). (4) Net Foreign Currency Assets of Commercial Banks : Represent their gross foreign currency assets netted for foreign currency liabilities to non-residents. (5) Capital Account : It consists of paid-up capital and reserves. (6) Other Items (net) : It is the residual balancing the components and sources of the Commercial Banking Survey and includes scheduled commercial banks’ other demand and time liabilities, net branch adjustments, net inter-bank liabilities, etc. The conceptual basis of the compilation of new monetary aggregates are available in the report of the Working Group on Money Supply: Analytics and Methodology of Compilation (Chairman: Dr. Y.V. Reddy), RBI Bulletin, July 1998. A link series between the old and present monetary series has been published in the article entitled “New Monetary Aggregates: An Introduction”, RBI Bulletin, October 1999. (1) NM2 and NM3 : Based on the residency concept and hence does not directly reckon non-resident foreign currency repatriable fixed deposits in the form of FCNR(B) deposits, Resurgent India Bonds (RIBs) and India Millennium Deposits (IMDs). (2) NM2 : This includes M1 and residents’ short-term time deposits (including and up to the contractual (3) Domestic Credit : Consistent with the new definition of bank credit which includes investments of banks in non-SLR securities, comprising of commercial paper, shares and bonds issued by the public sector undertakings, private sector and public financial institutions and net lending to primary dealers in the call/term money market. The RBI’s loans and advances to NABARD would be included in the RBI credit to commercial sector. Other components such as credit to Government, investments in other approved securities and conventional bank credit remain unchanged. (4) Net Foreign Assets of The Banking Sector : It comprises the RBI’s net foreign assets and scheduled commercial banks’ net foreign currency assets (refer to note 4 of Table 11A). (5) Capital Account : It consists of paid-up capital and reserves. (6) Other Items (net) of the Banking System : It is the residual balancing the components and sources of money stock, representing other demand and time liabilities etc. of the banking system. The conceptual basis of the compilation of the Reserve Bank Survey is given in the report of the Working Group on Money Supply: Analytics and Methodology of Compilation (Chairman: Dr. Y.V. Reddy), RBI Bulletin, July 1998 and the article “New Monetary Aggregates: An Introduction”, RBI Bulletin, October 1999. The components of reserve money (to be referred as M0) remain unchanged. On the sources side, the RBI’s refinance to the National Bank for Agriculture and Rural Development (NABARD), which was hitherto part of RBI’s claims on banks has been classified as part of RBI credit to commercial sector. The Reserve Bank’s net non-monetary liabilities are classified into capital account (comprising capital and reserves) and other items (net). Please see item (c) of notes to Table 10. Table No. 27C (a) Month-end yields for different integer valued residual maturities are estimated using interpolation technique on weighted average yields of select indicative securities derived from SGL transactions data on government securities observed during a select month-end day. Yield corresponding to each transaction in a security is calculated from the following Yield to Maturity (YTM) and price relationship.

(b) The weighted average yield corresponding to each traded security on that particular day is calculated from the yields of all transactions on that security using amount (Face Value) traded as the weights. (c) Broken period (number of days) is based on day count convention of 30 days a month and 360 days a year. Table 29 presents Index Numbers of Industrial Production (Sectoral and Use-based Classification). Due to revision of the indices of the mining sector and also the deletion of four items, viz., radio receivers, photosensitised paper, chassis (assembly) for HCVs (bus, truck) and engines from the item–basket of the manufacturing sector, the IIP data have been revised from 1994-95 onwards. This has also resulted in the change in redistribution of weights in use-based classification of IIP. Table 30 contains data on manufacturing sector at two digit level of 17 groups. (a) Figures exclude data on private placement and offer for sale but include amounts raised by private financial institutions. Table No. 35 The ban on forward trading in gold and silver, effective November 14, 1962 and January 10, 1963, has been lifted with effect from April 1, 2003. Annual data relate to average of the months April to March.

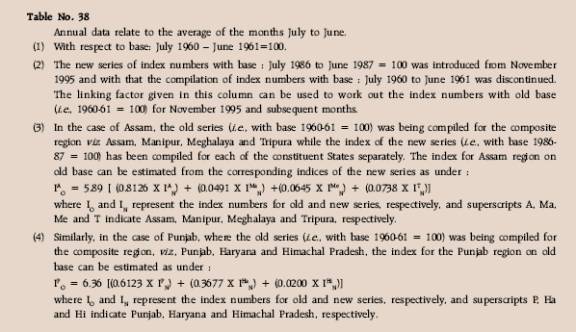

(5) Indices for the State compiled for the first time from November, 1995. (7) Average of 8 months (November 1995 - June 1996). The new series of index numbers with base 1993-94=100 was introduced in April 2000. Details regarding the scope and coverage of new series are published in June 2000 issue of the Bulletin. Annual data presented in Table No. 40 are average of monthly data. The foreign trade data relate to total sea, air and land trade, on private and government accounts. Exports are on f.o.b. basis and imports are on c.i.f. basis. Exports include re-exports of foreign merchandise previously imported to India and imports relate to foreign merchandise whether intended for home consumption, bonding or re-exportation. Direct transit trade, transshipment trade, passengers baggage, ship’s stores, defence goods and transactions in treasure i.e. gold and current coins and notes, diplomatic goods, “proscribed substances” under Atomic Energy Act, 1962, are excluded from the trade data, while indirect transit trade, transactions in silver (other than current coins) and in notes and coins not yet in circulation or withdrawn from circulation are included. (1) Data up to 1980-81 are final, subsequent data are preliminary actuals. (3) The item “Non-monetary Gold Movement” has been deleted from Invisibles in conformity with the IMF (4) Since 1990-91 the value of defence related imports are recorded under imports (merchandise debit) with credits financing such imports shown under “Loans (External Commercial Borrowings to India)” in the capital account. Interest payments on defence debt owed to the General Currency Area (GCA) are recorded under Investment Income debit and principal repayments under debit to “Loans (External Commercial Borrowings to India)”. In the case of the Rupee Payment Area (RPA), interest payment on and principal repayment of debt is clubbed together and shown separately under the item “Rupee Debt Service” in the capital account. This is in line with the recommendations of the High Level Committee on Balance of Payments (Chairman : Dr. C. Rangarajan). (5) In accordance with the provisions of IMF’s Balance of Payments Manual (5th Edition), gold purchased from the Government of India by the RBI has been excluded from the BOP statistics. Data from the earlier years have, therefore, been amended by making suitable adjustments in “Other Capital Receipts” and “Foreign Exchange Reserves”. Similarly, item “SDR Allocation” has been deleted from the table. (6) In accordance with the recommendations of the Report of the Technical Group on Reconciling of Balance of Payments and DGCI & S Data on Merchandise Trade, data on gold and silver brought in by the Indians returning from abroad have been included under import payments with contra entry under Private Transfer Receipts since 1992-93. (7) In accordance with the IMF’s Balance of Payments Manual (5th edition), ‘compensation of employees’ has been shown under head, “income” with effect from 1997-98; earlier, ‘compensation of employees’ was recorded under the head “Services – miscellaneous”. (8) Since April 1998, the sales and purchases of foreign currency by the Full Fledged Money Changers (FFMC) are included under “travel” in services. (9) Exchange Rates : Foreign currency transactions have been converted into rupees at the par/central rates up to June 1972 and on the basis of average of the Bank’s spot buying and selling rates for sterling and the monthly averages of cross rates of non-sterling currencies based on London market thereafter. Effective March 1993, conversion is made by crossing average spot buying and selling rate for US dollar in the forex market and the monthly averages of cross rates of non-dollar currencies based on the London market. Balance of payments is a statistical statement that systematically summarises, for a specific time period, the economic transactions of an economy with the rest of the world. Merchandise credit relate to export of goods while merchandise debit represent import of goods. Travel covers expenditure incurred by non-resident travellers during their stay in the country and expenditure incurred by resident travellers abroad. Transportation covers receipts and payments on account of international transportation services. Insurance comprises receipts and payments relating to all types of insurance services as well as reinsurance. Government not included elsewhere (G.n.i.e.) relates to receipts and payments on government account not included elsewhere as well as receipts and payments on account of maintenance of embassies and diplomatic missions and offices of international institutions. Miscellaneous covers receipts and payments in respect of all other services such as communication services, construction services, software services, technical know-how, royalties, etc. Transfers (official, private) represent receipts and payments without a quid pro quo. Investment Income transactions are in the form of interest, dividend, profit and others for servicing of capital transactions. Investment income receipts comprise interest received on loans to non-residents, dividend/profit received by Indians on foreign investment, reinvested earnings of Indian FDI companies abroad, interest received on debentures, floating rate notes (FRNs), Commercial Papers (CPs), fixed deposits and funds held abroad by ADs out of foreign currency loans/export proceeds, payment of taxes by nonresidents/refunds of taxes by foreign governments, interest/discount earnings on RBI investment. etc. Investment income payments comprise payment of interest on non-resident deposits, payment of interest on loans from non-residents, payment of dividend/profit to non-resident share holders, reinvested earnings of the FDI companies, payment of interest on debentures, FRNs, CPs, fixed deposits, Government securities, charges on Special Drawing Rights (SDRs), etc. Foreign investment has two components, namely, foreign direct investment and portfolio investment. 1. Gold is valued at average London market price during the month. The 5-country indices of REER/NEER were replaced with new 6-currency indices in December 2005. The RBI Bulletin December 2005 carried a detailed article on the rationale and methodology for the replacement. A revision has now been undertaken in the construction of the 6-currency REER indices. This revision was necessitated by a sudden spurt in Chinese inflation indices during April-May, 2006. It may be mentioned that Chinese inflation indices are not readily available in the public domain. The National Bureau of Statistics provides only point-to-point inflation rates on a monthly basis in the public domain. In view of this, inflation indices were constructed taking into account the inflation rates with 1993-94 as the base year. It may be further mentioned that the period from January 1993 to December 1995 was marked by continuous double digit inflation rates in China. This lent an upward bias to the Chinese inflation indices (base: 1993-94=100) leading to a sharp fall in the value of 6-currency REER in April 2006. In order to remove the distortion in REER on account of sudden spurt in Chinese inflation numbers, a new series of Chinese inflation indices has been constructed taking 1990 as the base year (a year with much less volatility in inflation rates). Subsequently, the base year of the new series of Chinese inflation indices has been changed from 1990 to 1993-94 through splicing to facilitate the construction of the 6-currency REER (base 1993-94=100). Table No. 53 (a) In terms of Government of India’s notification No. 10(45)/82-AC(5) dated July 6, 1982, loans and advances granted by the RBI to state co-operative banks and regional rural banks under section 17 [except subclause (a) of clause(4)] of RBI Act, 1934 and outstanding as on July 11, 1982 would be deemed to be loans and advances granted by NABARD under section 21 of NABARD Act, 1981. With effect from the date of the establishment of NABARD, i.e. July 12, 1982, RBI does not grant loans and advances to state co-operative banks except (i)for the purpose of general banking business against the pledge of Government and other approved securities under section 17(4)(a) of the RBI Act, 1934 and (ii) on behalf of urban co-operative banks under section 17(2)(bb) of the RBI Act, 1934. Loans and advances granted by the Reserve Bank of India to the state co-operative banks under section 17(4)(a) of the Reserve Bank of India Act, 1934 are not covered in this table. (1) Includes an amount of Rs.10 lakh advance for marketing of minor forest produce. Table No. 54 Outstanding relate to end of period and include Indian Union’s share of the pre-partition liabilities and repayments include those from the pre-partition holding of Indian investors. (1) Receipts and Outstanding include interest credited to depositors’ account from time to time. (2) Relate to 5-year, 10-year and 15-year cumulative time deposits. (3) Data on Public Provident Fund (PPF) relate to Post Office transactions and do not include PPF mobilised by banks. (4) Relate to Social Securities Certificates only. (5) Excluding Public Provident Fund. (6) Negative figures are due to rectification of misclassification. Table No. 55 Amounts are at face value. |

ଏହି ପେଜ୍ ଶେୟାର୍ କରନ୍ତୁ:

ରିଜର୍ଭ ବ୍ୟାଙ୍କ ଅଫ୍ ଇଣ୍ଡିଆ ମୋବାଇଲ୍ ଆପ୍ଲିକେସନ୍ ଇନଷ୍ଟଲ୍ କରନ୍ତୁ ଏବଂ ଲାଟେଷ୍ଟ ନିଉଜ୍ କୁ ଶୀଘ୍ର ଆକ୍ସେସ୍ ପାଆନ୍ତୁ!