IST,

IST,

Resolution of the Monetary Policy Committee (MPC)

On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (August 5, 2022) decided to:

Consequently, the standing deposit facility (SDF) rate stands adjusted to 5.15 per cent and the marginal standing facility (MSF) rate and the Bank Rate to 5.65 per cent.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. The main considerations underlying the decision are set out in the statement below. Assessment Global Economy 2. Since the MPC’s meeting in June 2022, the global economic and financial environment has deteriorated with the combined impact of monetary policy tightening across the world and the persisting war in Europe heightening risks of recession. Gripped by risk aversion, global financial markets have experienced surges of volatility and large sell-offs. The US dollar index soared to a two-decade high in July. Both advanced economies (AEs) and emerging market economies (EMEs) witnessed weakening of their currencies against the US dollar. EMEs are experiencing capital outflows and reserve losses which are exacerbating risks to their growth and financial stability. Domestic Economy 3. Domestic economic activity remains resilient. As on August 4, 2022, the south-west monsoon rainfall was 6 per cent above the long period average (LPA). Kharif sowing is picking up. High frequency indicators of activity in the industrial and services sectors are holding up. Urban demand is strengthening while rural demand is gradually catching up. Merchandise exports recorded a growth of 24.5 per cent during April-June 2022, with some moderation in July. Non-oil non-gold imports were robust, indicating strengthening domestic demand. 4. CPI inflation eased to 7.0 per cent (year-on-year, y-o-y) during May-June 2022 from 7.8 per cent in April, although it persists above the upper tolerance band. Food inflation has registered some moderation, especially with the softening of edible oil prices, and deepening deflation in pulses and eggs. Fuel inflation moved back to double digits in June primarily due to the rise in LPG and kerosene prices. While core inflation (i.e., CPI excluding food and fuel) moderated in May-June due to the full direct impact of the cut in excise duties on petrol and diesel pump prices, effected on May 22, 2022, it remains at elevated levels. 5. Overall system liquidity continues in surplus, with average daily absorption under the LAF at ₹3.8 lakh crore during June-July. Money supply (M3) and bank credit from commercial banks rose (y-o-y) by 7.9 per cent and 14.0 per cent, respectively, as on July 15, 2022. India’s foreign exchange reserves were placed at US$ 573.9 billion as on July 29, 2022. Outlook 6. Spillovers from geopolitical shocks are imparting considerable uncertainty to the inflation trajectory. More recently, food and metal prices have come off their peaks. International crude oil prices have eased in recent weeks but remain elevated and volatile on supply concerns even as the global demand outlook is weakening. The appreciation of the US dollar can feed into imported inflation pressures. Rising kharif sowing augurs well for the domestic food price outlook. The shortfall in paddy sowing, however, needs to be watched closely, although stocks of rice are well above the buffer norms. Firms polled in the Reserve Bank’s enterprise surveys expect input cost pressures to soften across sectors in H2. Cost pressures are, however, expected to get increasingly transmitted to output prices across manufacturing and services sectors. Taking into account these factors and on the assumption of a normal monsoon in 2022 and average crude oil price (Indian basket) of US$ 105 per barrel, the inflation projection is retained at 6.7 per cent in 2022-23, with Q2 at 7.1 per cent; Q3 at 6.4 per cent; and Q4 at 5.8 per cent, and risks evenly balanced. CPI inflation for Q1:2023-24 is projected at 5.0 per cent (Chart 1). 7. On the outlook for growth, rural consumption is expected to benefit from the brightening agricultural prospects. The demand for contact-intensive services and the improvement in business and consumer sentiment should bolster discretionary spending and urban consumption. Investment activity is expected to get support from the government’s capex push, improving bank credit and rising capacity utilisation. Firms polled in the Reserve Bank’s industrial outlook survey expect sequential expansion in production volumes and new orders in Q2:2022-23, which is likely to sustain through Q4. On the other hand, elevated risks emanating from protracted geopolitical tensions, the upsurge in global financial market volatility and tightening global financial conditions continue to weigh heavily on the outlook. Taking all these factors into consideration, the real GDP growth projection for 2022-23 is retained at 7.2 per cent, with Q1 at 16.2 per cent; Q2 at 6.2 per cent; Q3 at 4.1 per cent; and Q4 at 4.0 per cent, and risks broadly balanced. Real GDP growth for Q1:2023-24 is projected at 6.7 per cent (Chart 2).   8. Headline inflation has recently flattened and the supply outlook is improving, helped by some easing of global supply constraints. The MPC, however, noted that inflation is projected to remain above the upper tolerance level of 6 per cent through the first three quarters of 2022-23, entailing the risk of destabilising inflation expectations and triggering second round effects. Given the elevated level of inflation and resilience in domestic economic activity, the MPC took the view that further calibrated monetary policy action is needed to contain inflationary pressures, pull back headline inflation within the tolerance band closer to the target, and keep inflation expectations anchored so as to ensure that growth is sustained. Accordingly, the MPC decided to increase the policy repo rate by 50 basis points to 5.40 per cent. The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. 9. All members of the MPC – Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das – unanimously voted to increase the policy repo rate by 50 basis points to 5.40 per cent. 10. All members - Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das, except Prof. Jayanth R. Varma - voted to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. Prof. Jayanth R. Varma expressed reservations on this part of the resolution. 11. The minutes of the MPC’s meeting will be published on August 19, 2022. 12. The next meeting of the MPC is scheduled during September 28-30, 2022. * Released on August 5, 2022. |

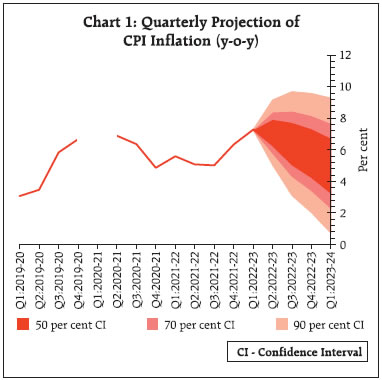

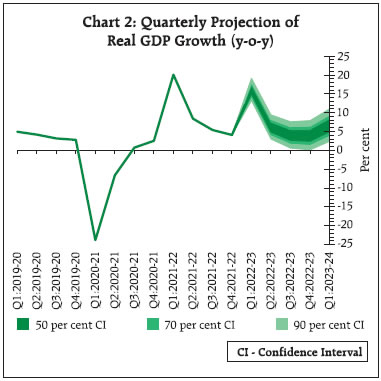

ଏହି ପେଜ୍ ଶେୟାର୍ କରନ୍ତୁ:

ରିଜର୍ଭ ବ୍ୟାଙ୍କ ଅଫ୍ ଇଣ୍ଡିଆ ମୋବାଇଲ୍ ଆପ୍ଲିକେସନ୍ ଇନଷ୍ଟଲ୍ କରନ୍ତୁ ଏବଂ ଲାଟେଷ୍ଟ ନିଉଜ୍ କୁ ଶୀଘ୍ର ଆକ୍ସେସ୍ ପାଆନ୍ତୁ!

ଆମର ଆପ୍ ଇନଷ୍ଟଲ୍ କରିବାକୁ QR କୋଡ୍ ସ୍କାନ୍ କରନ୍ତୁ

ପେଜ୍ ଅନ୍ତିମ ଅପଡେଟ୍ ହୋଇଛି: