IST,

IST,

Agriculture Loan Bank Accounts – A Waiver Scenario Analysis

| Mint Street Memo No. 04 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Agriculture Loan Bank Accounts – A Waiver Scenario Analysis | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Rajendra Raghumanda, Ravi Shankar and Sukhbir Singh 1 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

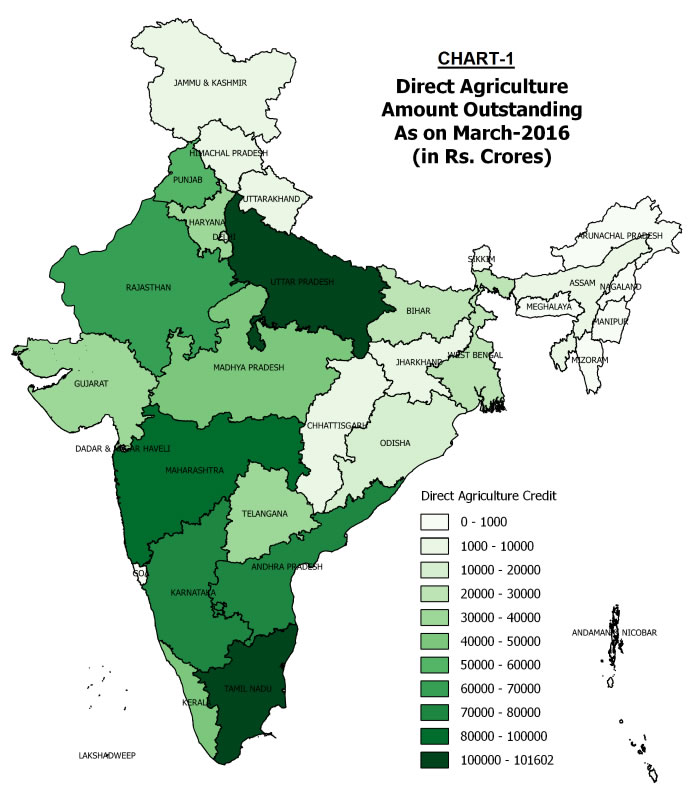

Abstract Many state governments have announced farm debt waiver schemes with varying features / coverage to provide relief to indebted farmers. This note presents a scenario-based analysis of possible size of debt waiver using account level data on bank credit. The estimates range from ₹ 2.2 lakh crore to ₹ 4.2 lakh crore, depending on the extent of coverage under the waiver schemes. In all cases, however, loan waiver by states could adversely impact their fiscal position. I. Introduction Agricultural credit is a critical resource support to farm sector in India, given the dependence of a large section of its population on agricultural activities. In the recent times, multiple challenges have led to stress in the agricultural sector, which also got manifested in episodes of untimely deaths of distressed farmers. Farm loan waiver is often suggested as a possible solution to such distress situations. The first ever nation-wide farm loan waiver was announced in 1990. Subsequently, the Government of India implemented the Agricultural Debt Waiver and Debt Relief Scheme in 2008 to address the then prevailing agrarian crisis. In the recent years too, there have been demands for similar policy response and some of the state Governments have implemented such schemes. Andhra Pradesh and Telangana implemented their loan waiver schemes in 2014 and Tamil Nadu in 2016. In the current year, four states (namely, Maharashtra, UP, Punjab and Karnataka) have announced farm loan waiver scheme, with varying criteria. The coverage and quantum of debt relief announced by these states are presented in Table 1. However, loan waiver is often considered to be an imprudent policy due to its resultant fiscal burden as well as the adverse impact on credit discipline/banking habits of borrowers. This note attempts to assess the overall quantum of farm debt waiver under various scenarios, based on the data reported by banks as at end-March 2016, which is the cut-off date for some of the loan waivers announced recently. II. Bank Credit to Agriculture – Stylised Facts II.A Data The study uses account-level data from the Reserve Bank of India’s Basic Statistical Returns on credit (BSR-1) as reported by the scheduled commercial banks (SCBs) [including regional rural banks (RRBs)]. Loans extended by co-operative banks are not captured in BSR-1. II.B Composition of Bank Credit to Agriculture There were nearly 77 million agriculture credit accounts 2 with SCBs as on March 2016 with the average size of credit at ₹ 1.16 lakh. Around 70 per cent of these are crop loans, which account for nearly 67 per cent of the outstanding loan amount ( Table 2). As on the cut-off date, a majority of these crop loan recipients (38 million) had outstanding loans up to ₹ 1 lakh and their average loan amount was ₹ 44,088. The loans for investment in equipment (e.g., tractors) had a share of nearly 27 per cent and 23 per cent in the number of accounts and the loan amount respectively ( Table 2). Of the total 77 million agriculture credit accounts under consideration, about 39 million accounts were held by small and marginal farmers having land holding up to 2 hectares. 3 For small and marginal farmers, crop loans constituted over 75 per cent of their total loan amount. The size of the crop loans is normally small – around 74% of crop loan accounts of small and marginal farmers were ‘up to ₹ 1 lakh’. II. C Regional Distribution of Bank Credit to Agriculture Tamil Nadu (11.4 per cent), UP (11.3 per cent), Maharashtra (9.0 per cent), Karnataka (8.7 per cent) and Andhra Pradesh (8.5 per cent) are the top five states, which together account for about half of the total agriculture credit ( Chart 1). III. Assessment of Debt Waiver State Governments have generally focussed on crop loans to small and marginal farmers in designing their waiver schemes with the twin objective of larger coverage and comparatively lesser burden on state finances. They have also prescribed different criteria for farm loan waiver schemes, based on their budget constraints. As such, an assessment of total loan waiver at national-level would entail assumptions on coverage and eligibility criteria. In view of the above empirical facts, the following uniform criteria are considered for this analysis:

III.A Assessment of Aggregate Loan Waiver – Scenario Analysis Under the above criteria, the states have the choice to either waive off all agricultural loans (taken for various purposes) or only crop loans. Similarly, the coverage of loan waiver could either be extended to all loan accounts or to small and marginal farmers having land holdings of size up to 2 Hectares. The quantum of farm loan waiver has been assessed under the following four alternative choices / scenarios: Scenario 1: All Agriculture loans are waived This scenario envisages coverage of loan waiver to be extended to all farm loan accounts irrespective of the type of loan or size of land holdings. In such a scheme, coverage would be maximum but the burden on the state finances would also be higher. The quantum of bank loans from SCBs is assessed to be about ₹ 4,50,000 crore by applying these selection criteria to account-level loan data at the national level. The amount is revised to ₹ 4,33,000 crore when adjusted for the estimated coverage already announced by the four states. Scenario 2: All crop loans are waived This scenario envisages covering majority of farmers but excludes investment loans and also loans towards allied activities. In this scenario, the total waiver could amount to ₹ 3,27,000 crore which moves up to ₹ 3,34,000 crore when adjusted for the amount already announced recently by the four states. Scenario 3: Agriculture loans of only small and marginal farmers are waived In a scenario where the coverage of loan waiver could be restricted to the small and marginal farmers to limit the fiscal burden, the total waiver amount is assessed to be about ₹ 2,20,000 crore. This estimate may move up to ₹ 2,56,000 crore with the coverage announced by the four states. Scenario 4: Only crop loans of small and marginal farmers are waived The empirical data suggests that loan waiver coverage might be limited to smaller sized crop loans availed by small and marginal farmers, to strike a balance between the two objectives - supporting the farmers and budget constraints. In such a scenario, the total loan waiver would amount to ₹ 1,73,000 crore at the national level. Once adjusted for the already announced schemes, the estimated waiver amount turns out to be ₹ 2,18,000 crore. Given the public policy environment, this scenario seems closer to reality. III.B Fiscal Deficit - Impact The estimated loan waiver amounts for SCBs at all-India level for different scenarios are summarised in Table 3 along with the impact on outstanding liabilities of the states and centre as percentage to GDP. State-wise assessment of the scenario-based loan waiver is provided in Statement-1. As per these scenarios, the crop loan waiver for small and marginal farmers alone would result in waiver of more than 65% of the outstanding crop loans. IV. Summing Up The scenario-based analysis gives the agriculture loan waiver amount in the range of ₹ 2.2 lakh crore in Scenario-4 (all crop loans of small and marginal farmers- more likely scenario) to ₹ 4.2 lakh crore in Scenario-1 (All agriculture loans - less likely scenario). Nearly 17 per cent of the agricultural credit that is given by cooperative banks 4 , etc. is not covered here, and its adjustment would take Scenario-4 amounting to around ₹ 2.4 lakh crore, once adjusted for the given amount for the four states. These estimates would vary from the actual situation, based on claims processed and identification of eligible beneficiaries. States are following varying criteria (amount, nature, institutions, etc.) for loan waiver schemes. The nature of financing of increased expenditure would be important for overall macroeconomic impact. States may resort to other additional revenue mobilisation measures / expenditure cuts / additional borrowings, etc., to part-finance the loan waiver. In all cases, however, loan waiver by states would adversely impact their fiscal position.

1 Ravi Shankar is Director and Rajendra Raghumanda and Sukhbir Singh are Research Officers in the Department of Statistics and Information Management. The findings and views in this paper are entirely those of the authors and should not necessarily be interpreted as the official views of Reserve Bank of India. 2 As per National Sample Survey (NSS) Round 70, rural India had an estimated total of 90.2 million agricultural households in 2013. 3 The NSS Round 70 estimated about 78 million households having land holding up to 2 Hectares. A hectare is equal to 10,000 square metres. 4 NABARD Annual Report 2015-16, Table 1.3 which gives agency-wise share of credit flow to agriculture and same is assumed for agriculture loans outstanding for this exercise. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

ਇਸ ਪੇਜ ਨੂੰ ਸ਼ੇਅਰ ਕਰੋ:

ਭਾਰਤੀ ਰਿਜ਼ਰਵ ਬੈਂਕ ਮੋਬਾਈਲ ਐਪਲੀਕੇਸ਼ਨ ਇੰਸਟਾਲ ਕਰੋ ਅਤੇ ਨਵੀਨਤਮ ਖਬਰਾਂ ਤੱਕ ਤੇਜ਼ ਐਕਸੈਸ ਪ੍ਰਾਪਤ ਕਰੋ!

ਸਾਡੀ ਐਪ ਇੰਸਟਾਲ ਕਰਨ ਲਈ QR ਕੋਡ ਸਕੈਨ ਕਰੋ।

ਪੇਜ ਅੰਤਿਮ ਅੱਪਡੇਟ ਦੀ ਤਾਰੀਖ: