|

Bank credit has continued to grow at a strong pace. Sustained growth of bank credit was accommodated by acceleration in deposit growth. Concomitantly, broad money growth has remained above the indicative trajectory, reflecting strong demand conditions. Banks’ SLR investments, as a proportion of their net demand and time liabilities (NDTL), have declined further from their end-March 2006 levels. The Reserve Bank continued to modulate market liquidity with the help of LAF repo and reverse repos and issuance of securities under the Market Stabilisation Scheme (MSS). Furthermore, the Reserve Bank raised cash reserve ratio (CRR) by 50 basis points in two phases with effect from the fortnight beginning December 23, 2006.

Monetary Survey

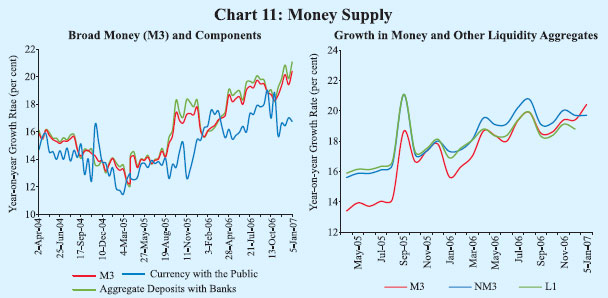

Broad money (M3) growth, year-on-year (y-o-y), accelerated to 20.4 per cent as on January 5, 2007 from 17.0 per cent at end-March 2006 and 16.0 per cent a year ago. On a fiscal year basis too, M3 growth during 2006-07 so far (January 5, 2007 over March 31, 2006), at 11.9 per cent, was higher than that of 8.8 per cent in the corresponding period of 2005-06 (January 6, 2006 over April 1, 2005). Taking into account, inter alia, these trends in monetary aggregates, sustained growth in credit offtake, and additional absorption of liquidity under the MSS, the Reserve Bank, on December 8, 2006, decided to increase the CRR by 50 basis points in two stages – 25 basis points each effective the fortnights beginning December 23, 2006 and January 6, 2007. Other developments in the domestic economy impacting upon the decision to increase the CRR included growth in real GDP, acceleration in inflation, expectations of the private corporate sector of higher increase in prices of both inputs and outputs, reports of growing strains on domestic capacity utilisation, and challenges emanating from capital flows and consequent impact on increasing liquidity (see Box 1, Chapter IV). The increase in the CRR is estimated to have absorbed banks’ resources to the extent of Rs.13,500 crore.

Expansion in the residency-based new monetary aggregate (NM3) – which, inter alia, does not directly reckon non-resident foreign currency deposits such as India Millennium Deposits (IMDs) and FCNR(B) – was lower than M3, partly reflecting lower recourse to call/term funding from financial institutions. Growth in liquidity aggregate L1 was lower than that in NM3 on account of decline in postal deposits (Chart 11 and Table 17).

Amongst its major components, both currency and time deposits

contributed to acceleration in growth in M3 (Table 18).

On a year-on-year basis,

Table 17: Monetary Indicators |

(Amount in Rupees crore) |

Item |

Outstanding as on

January 5, 2007 |

Variation (year-on-year) |

January 6, 2006 |

January 5, 2007 |

|

Amount |

Per cent |

Amount |

|

Percent

|

1 |

2 |

3 |

4 |

5 |

|

6 |

|

I. |

Reserve Money* |

6,41,790 |

69,213 |

14.9 |

1,06,846 |

|

20.0 |

|

II. |

Broad Money (M3) |

30,54,159 |

3,50,747 |

16.0 |

5,17,318 |

|

20.4 |

|

|

a) |

Currency with the Public |

4,64,820 |

53,106 |

15.4 |

66,719 |

|

16.8 |

|

|

b) |

Aggregate Deposits |

25,83,864 |

2,97,561 |

16.2 |

4,49,751 |

|

21.1 |

|

|

|

|

i) |

Demand Deposits |

4,06,292 |

76,065 |

28.7 |

65,584 |

|

19.2 |

|

|

|

|

ii) |

Time Deposits |

21,77,571 |

2,21,496 |

14.1 |

3,84,167 |

|

21.4 |

|

|

|

|

|

of which: Non-Resident Foreign Currency Deposits |

65,068 |

-19,944 |

-26.5 |

9,658 |

|

17.4 |

|

III. |

NM3 |

|

30,64,566 |

3,79,996 |

17.4 |

5,04,467 |

|

19.7 |

|

|

of which: Call Term Funding from FIs |

84,629 |

16,070 |

24.6 |

3,265 |

|

4.0 |

|

IV. |

a) |

L1 |

|

31,20,180 |

4,02,881 |

18.1 |

4,92,888 |

|

18.8 |

|

|

|

of which: Postal Deposits |

95,752 |

17,552 |

21.0 |

-5,447 |

|

-5.4 |

|

|

b) |

L2 |

|

31,23,112 |

4,03,916 |

18.1 |

4,92,888 |

|

18.7 |

|

|

c) |

L3 |

|

31,44,806 |

4,05,712 |

18.1 |

4,92,888 |

|

18.6 |

|

V. |

Major Sources of Broad Money |

|

|

|

|

|

|

|

|

a) |

Net Bank Credit to the Government (i+ii) |

8,02,930 |

22,088 |

2.9 |

21,932 |

|

2.8 |

|

|

|

i) |

Net Reserve Bank Credit to Government |

-312 |

21,206 |

- |

-19,253 |

|

- |

|

|

|

|

of which: to the Centre |

-919 |

22,611 |

- |

-19,845 |

|

- |

|

|

|

ii) |

Other Banks' Credit to Government |

8,03,242 |

882 |

0.1 |

41,184 |

|

5.4 |

|

|

b) |

Bank Credit to Commercial Sector |

19,51,885 |

3,16,802 |

26.1 |

4,20,026 |

|

27.4 |

|

|

c) |

Net Foreign Exchange Assets of Banking Sector |

8,28,046 |

60,495 |

10.1 |

1,68,746 |

|

25.6 |

Memo: |

SCBs Aggregate Deposits |

23,81,242 |

2,85,182 |

17.2 |

4,38,037 |

|

22.5 |

SCBs Non-food Credit |

17,14,396 |

3,11,013 |

31.2 |

4,07,735 |

|

31.2 |

|

* : Data pertain to January 19, 2007.

SCBs : Scheduled Commercial Banks. FIs : Financial Institutions.

NBFCs : Non-Banking Financial Companies. NM3 is the residency-based

broad money aggregate and L1, L2 and L3 are liquidity aggregates

compiled on the recommendations of the Working Group on Money Supply

(Chairman: Dr. Y.V. Reddy, 1998). Liquidity aggregates are defined

as follows:

L1= NM3 + Select deposits with the post office saving banks.

L2= L1 +Term deposits with term lending institutions and refinancing

institutions (FIs) + Term borrowing by

FIs + Certificates of deposits issued by FIs.

L3= L2 + Public deposits of non-banking financial companies.

Note : 1. Data are provisional.

2. Liquidity aggregates pertain to end-December 2006.

3. Data reflect redemption of India Millennium Deposits (IMDs) on

December 29, 2005.

|

growth in currency with the public increased from 15.4 per cent as on January 6, 2006 to a peak of 19.4 per cent as on October 27, 2006 before moderating to 16.8 per cent as on January 5, 2007. Acceleration in growth in October 2006 could be partly attributed to the early onset of festival season currency demand during the current year (Table 18).

Growth in aggregate deposits accelerated to 21.1 per cent, y-o-y, as on January 5, 2007 from 16.2 per cent a year ago, on the back of higher accretion to time

|

Table 18: Monetary

Aggregates – Variations

|

|

(Rupees crore)

|

|

|

Variation during

|

|

2005-06

|

2005-06

|

2006-07

|

2005-06

|

2006-07

|

|

(April- March)

|

(up to Jan 6)

|

(up to Jan 5)

|

Q1

|

Q2

|

Q3

|

Q4

|

Q1

|

Q2

|

Q3

|

|

1

|

2

|

3

|

4

|

5

|

6

|

7

|

8

|

9

|

10

|

11

|

|

M3 (=1+2+3=4+5+6+7-8)

|

3,96,868

(17.0)

|

2,04,175

(8.8)

|

3,24,624

(11.9)

|

27,448

|

1,22,456

|

45,104

|

2,01,860

|

55,427

|

1,65,903

|

67,757

|

|

Components

|

|

1.

|

Currency with the Public

|

58,272

|

43,230

|

51,677

|

20,492

|

-10,835

|

30,124

|

18,491

|

23,773

|

-3,099

|

27,988

|

|

|

|

(16.4 )

|

(12.2)

|

(12.5)

|

|

|

|

|

|

|

|

|

2.

|

Aggregates Deposits with Banks

|

3,38,037

|

1,62,637

|

2,74,350

|

8,819

|

1,32,531

|

15,729

|

1,80,958

|

33,271

|

1,68,549

|

40,131

|

|

|

|

(17.1)

|

(8.2)

|

(11.9)

|

|

|

|

|

|

|

|

|

|

2.1 Demand Deposits with Banks

|

83,861

|

19,346

|

1,069

|

-21,953

|

41,566

|

-2,357

|

66,604

|

-41,235

|

41,558

|

-7,167

|

|

|

|

(26.1)

|

(6.0 )

|

(0.3)

|

|

|

|

|

|

|

|

|

|

2.2 Time Deposits with Banks

|

2,54,176

|

1,43,291

|

2,73,282

|

30,772

|

90,965

|

18,086

|

1,14,354

|

74,506

|

1,26,991

|

47,298

|

|

|

|

(15.4)

|

(8.7)

|

(14.4)

|

|

|

|

|

|

|

|

|

3.

|

'Other' Deposits with Banks

|

560

|

-1,692

|

-1,403

|

-1,862

|

760

|

-750

|

2,411

|

-1,617

|

453

|

-363

|

|

Sources

|

|

4

|

Net Bank Credit to Government

|

20,386

(2.7 )

|

32,292

(4.3)

|

33,838

(4.4)

|

17,398

|

-5,017

|

-5,722

|

13,726

|

20,933

|

15,705

|

-16,375

|

|

|

4.1 RBI's net credit to Government

|

35,799

|

46,603

|

-8,448

|

18,963

|

-25,251

|

19,879

|

22,208

|

53

|

2,826

|

-12,754

|

|

|

4.1.1 RBI's net credit to Centre

|

33,374

|

47,140

|

-6,079

|

19,556

|

-25,251

|

19,812

|

19,256

|

3,071

|

2,584

|

-12,568

|

|

|

4.2 Other Banks' Credit to Government

|

-15,413

(-2.0)

|

-14,311

(-1.8 )

|

42,286

(5.6)

|

-1,565

|

20,234

|

-25,601

|

-8,481

|

20,881

|

12,879

|

-3,621

|

|

5

|

Bank Credit to Commercial Sector

|

3,59,703

(27.0)

|

2,00,600

(15.1)

|

2,60,924

(15.4)

|

10,235

|

1,18,712

|

61,731

|

1,69,025

|

16,973

|

1,39,990

|

79,885

|

|

6

|

Net Foreign Exchange Assets of Banking Sector

|

78,291

|

11,397

|

1,01,852

|

-12,026

|

24,062

|

27,701

|

38,554

|

58,087

|

20,197

|

27,250

|

|

|

6.1 Net Foreign Exchange Assets of RBI

|

61,545

|

6,980

|

1,06,806

|

-13,243

|

24,823

|

23,741

|

26,224

|

71,845

|

11,392

|

27,250

|

|

7

|

Governments' Currency Liabilities to the Public

|

1,306

|

1,193

|

-700

|

384

|

910

|

-100

|

112

|

-920

|

155

|

66

|

|

8

|

Net Non-Monetary liabilities of Banking Sector

|

62,817

|

41,308

|

71,289

|

-11,456

|

16,210

|

38,507

|

19,557

|

39,646

|

10,144

|

23,069

|

|

Memo:

|

|

1

|

Non-resident Foreign Currency Deposits with SCBs

|

-16,876

|

-20,741

|

5,793

|

804

|

187

|

1,856

|

-19,723

|

3,917

|

1,671

|

490

|

|

2

|

SCB' Call-term Borrowing from Financial Institutions

|

11,224

|

9,443

|

1,485

|

-1,002

|

7,359

|

1,836

|

3,031

|

3,118

|

-1,576

|

-4,883

|

|

3

|

Overseas Borrowing by SCBs

|

1,295

|

2,198

|

-3,691

|

-925

|

3,618

|

-622

|

-775

|

3,301

|

-3.685

|

-2,787

|

|

SCBs: Scheduled Commercial Banks.

Note: 1. Variation during 2006-07 is worked out

from March 31, 2006 whereas the variation during 2005-06 is worked

out from April 1, 2005.

2. Figures in parentheses are percentage variations during the fiscal

year.

3. Data reflect redemption of India Millennium Deposits (IMDs) on

December 29, 2005.

|

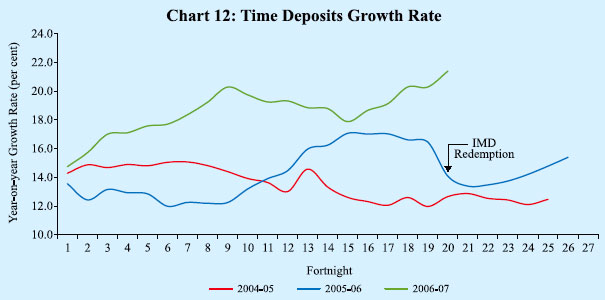

Deposits. On a y-o-y basis, growth in demand deposits (19.2 per cent) as on January 5, 2007 was of a lower order than a year ago (28.7 per cent). Accretion to time deposits was, however, significantly higher than that in the previous year (Chart 12). Growth in time deposits of scheduled commercial banks accelerated to 22.9 per cent (y-o-y) as on January 5, 2007 from 15.0 per cent a year ago. This, apart from acceleration in economic activity, could be attributed to higher interest rates on deposits as well as tax benefits. Interest rates on time deposits of 1-3 years maturity offered by public sector banks increased from a range of 5.75-6.75 per cent in March 2006 to 6.75-8.25 per cent in January 2007. Rates offered by private sector banks on deposits of similar maturity increased from a range of 5.50-7.75 per cent to 6.75-9.25 per cent over the same period. Growth in time deposits also appears to have benefited from the recently introduced tax benefits under Section 80C for deposits with maturity of five years and above. Concomitantly, with unchanged interest rates, postal deposits have witnessed a significant decline since end-March 2006.

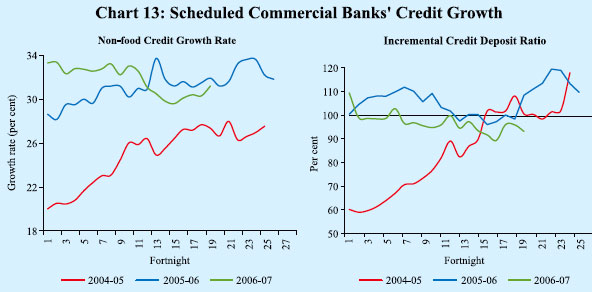

Commercial sector’s demand for bank credit has continued to remain strong during 2006-07 so far. On a year-on-year basis, non-food credit of scheduled commercial banks (SCBs) registered a growth of 31.2 per cent as on January 5, 2007 – the same rate as a year ago. On a fiscal year basis, growth in non-food credit decelerated marginally to 16.9 per cent as on January 5, 2007 from 17.5 per cent a year ago. In view of the acceleration in deposits, the incremental credit-deposit ratio of SCBs, after remaining above/around 100 per cent for the most part since October 2004, has exhibited some moderation in recent months. As on January 5, 2007, the incremental credit-deposit ratio was around 93 per cent (y-o-y) as compared with 108 per cent a year ago (Chart 13). Scheduled commercial banks’ food credit has recorded a modest rise (5.9 per cent) during 2006-07 (up to January 5, 2007), reflecting lower order of procurement of foodgrains.

Disaggregated data available up to October 2006 show that credit growth has been largely broad-based (Table 19). About 34 per cent of incremental non-food credit was absorbed by industry, 12 per cent by agriculture, 15 per cent by loans to the housing sector and another 11 per cent by ‘other retail loans’. Loans to commercial real estate, which increased by 84 per cent, y-o-y, absorbed 5 per cent of incremental non-food credit.

Apart from bank credit, the corporate sector continued to rely on non-bank sources of funds for financing their requirements. Resources raised through domestic equity issuances during the first nine months of 2006-07 (Rs 23,843 crore) were more than double of that in the corresponding period of 2005-06. After remaining subdued during the second quarter, amounts raised from the primary market picked up during the third quarter of 2006-07. Mobilisation of resources through equity issuances abroad (ADRs/GDRs) during April-December 2006 (Rs.8,019 crore) were 55 per cent higher than that in the same period of 2005. Recourse to external commercial borrowings (ECBs) during the first half of 2006-07 was almost double of that in the corresponding period of 2005-06, with net disbursements under ECBs increasing from Rs.17,551 crore during April-September 2005 to Rs.34,031 crore during April-September 2006. Mobilisation through issuances of commercial papers during April-December 2006 was more than three times of that a year ago, notwithstanding some sluggishness in the third quarter. Finally, internal sources of funds continued to provide large financing support to the domestic corporate sector during the first half of 2006-07. Profits after tax of select non-financial non-government companies during April-September 2006 were almost 40 per cent higher than those in the first half of 2005-06. Profits after tax during the second quarter of 2006-07 were higher than those in each of the five preceding quarters (Table 20).

|

Table 19: Deployment

of Non-food Bank Credit

|

|

(Amount in Rupees crore)

|

|

Sector/Industry

|

Outstanding

as on

October 27, 2006

|

Year-on-year Variations

|

|

2005-06 (October 28, 2005

over October 29, 2004)

|

2006-07 (October 27, 2006

over October 28, 2005)

|

|

Absolute

|

Per cent

|

Absolute

|

Per cent

|

|

1

|

2

|

3

|

4

|

5

|

6

|

|

Non-food Gross Bank Credit (1 to 4)

|

15,37,978

|

2,66,092

|

32.4

|

3,51,904

|

29.7

|

|

1.

|

Agriculture and Allied Activities

|

1,86,533

|

37,867

|

37.2

|

43,919

|

30.8

|

|

2.

|

Industry (Small, Medium and Large)

|

5,95,310

|

81,666

|

24.0

|

1,18,481

|

24.8

|

|

|

Small Scale Industries

|

94,518

|

10,641

|

15.8

|

15,976

|

20.3

|

|

3.

|

Personal Loans

|

3,98,055

|

n.a.

|

n.a.

|

1,01,631

|

34.3

|

|

|

Housing

|

2,09,468

|

n.a.

|

n.a.

|

51,191

|

32.3

|

|

|

Advances against Fixed Deposits

|

33,744

|

4,957

|

19.3

|

3,005

|

9.8

|

|

|

Credit Cards

|

11,870

|

n.a.

|

n.a.

|

4,016

|

51.1

|

|

|

Education

|

12,692

|

n.a.

|

n.a.

|

4,435

|

53.7

|

|

|

Consumer Durables

|

9,291

|

195

|

2.7

|

804

|

9.5

|

|

4.

|

Others

|

3,58,080

|

n.a.

|

n.a.

|

87,873

|

32.5

|

|

|

Transport Operators

|

20,671

|

n.a.

|

n.a.

|

9,673

|

88.0

|

|

|

Professional and Others

|

18,286

|

n.a.

|

n.a.

|

5,978

|

48.6

|

|

|

Trade

|

90,855

|

n.a.

|

n.a.

|

25,593

|

39.2

|

|

|

Real Estate Loans

|

37,838

|

n.a.

|

n.a.

|

17,260

|

83.9

|

|

|

Non-Banking Financial Companies

|

33,317

|

5,791

|

33.3

|

7,453

|

28.8

|

|

Memo:

|

|

Priority Sector

|

5,41,017

|

1,30,751

|

45.1

|

1,08,056

|

25.0

|

|

Industry (Small, Medium and Large)

|

5,95,310

|

81,666

|

24.0

|

1,18,481

|

24.8

|

|

Food Processing

|

32,399

|

3,301

|

16.2

|

6,181

|

23.6

|

|

Textiles

|

65,203

|

9,647

|

28.3

|

16,631

|

34.2

|

|

Paper and Paper Products

|

10,179

|

787

|

12.8

|

2,139

|

26.6

|

|

Petroleum, Coal Products and Nuclear Fuels

|

29,423

|

3,566

|

22.6

|

8,708

|

42.0

|

|

Chemical and Chemical Products

|

51,476

|

3,584

|

12.0

|

10,916

|

26.9

|

|

Rubber, Plastic and their Products

|

7,757

|

2,302

|

81.0

|

2,260

|

41.1

|

|

Iron and Steel

|

56,693

|

9,529

|

36.2

|

14,554

|

34.5

|

|

Other Metal and Metal Products

|

18,638

|

3,001

|

32.7

|

4,817

|

34.9

|

|

Engineering

|

37,803

|

4,562

|

18.0

|

5,008

|

15.3

|

|

Vehicles, Vehicle Parts and Transport Equipments

|

19,154

|

5,335

|

95.9

|

3,302

|

20.8

|

|

Gems and Jewellery

|

22,474

|

3,802

|

33.1

|

4,014

|

21.7

|

|

Construction

|

16,079

|

2,366

|

30.8

|

5,321

|

49.5

|

|

Infrastructure

|

1,18,840

|

23,814

|

36.4

|

22,353

|

23.2

|

|

n.a. : Not available.

Note:

1. Data are provisional and relate to select scheduled commercial

banks.

2. Owing to change in classification of sectors/industries and coverage

of banks, data for 2006 are not

comparable with earlier data.

|

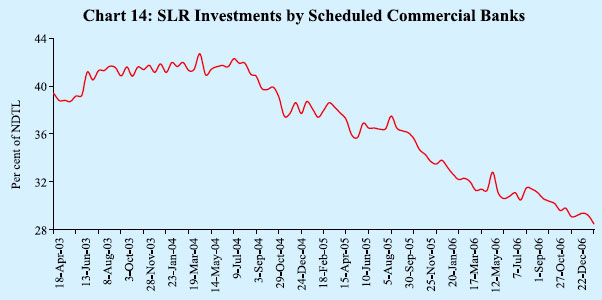

In the fiscal year 2006-07 (up to January 5, 2007), commercial banks’ investments in gilts witnessed a large expansion of Rs.43,222 crore in contrast to a decline of Rs.15,580 crore a year ago, reflecting the need to meet statutory requirements. On a y-o-y basis, commercial banks’ investments in gilts increased by 5.6 per cent as against a decline of 0.1 per cent a year ago (Table 21). Over the same period, growth in commercial banks’ NDTL accelerated to 20.7 per cent from 18.3 per cent a year ago. With incremental investment in gilts not keeping pace with the high growth in NDTL, commercial banks’ holdings of Government securities

Table 20: Select Sources of Funds to Industry |

(Rupees crore) |

Item |

2005-06 |

2005-06 |

2006-07 |

2005-06 |

2006-07 |

(April- March) |

April-December@ |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

10 |

11 |

A. |

Bank Credit to Industry # |

1,22,165 |

39,209 |

46,566 |

11,148 |

28,061 |

24,484 |

58,472 |

-2,724 |

49,290 |

- |

B. |

Flow from Non-banks to Corporates |

|

|

|

|

|

|

|

|

|

|

1. |

Capital Issues (i+ii) |

13,871 |

9,571 |

24,334 |

1,264 |

2,758 |

5,549 |

4,210 |

10,627 |

1,882 |

11,825 |

|

|

i) |

Non-Government Public Ltd. Companies (a+b) |

13,408 |

9,571 |

24,334 |

1,264 |

2,758 |

5,549 |

3,837 |

10,627 |

1,882 |

11,825 |

|

|

|

a) Bonds/Debentures |

245 |

118 |

491 |

118 |

0 |

0 |

127 |

0 |

0 |

491 |

|

|

|

b) Shares |

13,163 |

9,453 |

23,843 |

1,146 |

2,758 |

5,549 |

3,710 |

10,627 |

1,882 |

11,334 |

|

|

ii) |

PSUs and Government Companies |

373 |

0 |

0 |

0 |

0 |

0 |

373 |

0 |

0 |

0 |

|

2. |

ADR/GDR Issues |

7,263 |

5,171 |

8,019 |

789 |

739 |

3,643 |

2,092 |

4,965 |

2,130 |

924 |

|

3. |

External Commercial |

|

|

|

|

|

|

|

|

|

|

|

|

Borrowings (ECBs) |

45,078 |

17,551 |

34,031 |

4,317 |

13,234 |

9,677 |

17,850 |

20,366 |

13,665 |

- |

|

4. |

Issue of CPs |

-1,517 |

2,999 |

10,618 |

3,562 |

1928 |

-2,491 |

-4,516 |

6,931 |

4,795 |

-1,108 |

C. |

Depreciation Provision + |

28,883 |

13,625 |

15,710 |

7,137 |

7,617 |

7,748 |

8,340 |

8,449 |

8.892 |

- |

D. |

Profit after Tax + |

67,506 |

32,016 |

44,927 |

16,726 |

18,169 |

18,790 |

21,634 |

24,845 |

27,710 |

- |

|

#:Data pertain to select scheduled commercial banks. Figures for

2005-06 are not comparable with those of 2006-07 due to increase

in number of banks selected in the sample.

+:Data are based on audited/ unaudited abridged results of select

non-Government non-financial listed public limited companies. Quarterly

variations may not add up to annual or half-yearly variations due

to difference in coverage of companies.

@:Data for bank credit, ECBs, depreciation provision and profit

after tax pertain to April-September.

Note:

1.Data are provisional.

2. Data on capital issues pertain to gross issuances excluding issues

by banks and financial institutions.

Figures are not adjusted for banks’ investments in capital

issues, which are not expected to be significant.

3. Data on ADR/GDR issues exclude issuances by banks and financial

institutions.

4. Data on ECBs include short-term credit. Data for 2005-06 are

exclusive of the IMD redemption.

|

declined to 28.6 per cent of their NDTL as on January 5, 2007 from 31.3 per cent at end-March 2006 and 32.6 per cent a year ago (Chart 14). Excess SLR investments

Table 21: Scheduled Commercial Banks' Survey |

(Amount in Rupees crore) |

Item |

Outstanding

as on January

5, 2007 |

Variation (year-on-year) |

As on Jan 6, 2006 |

As on Jan 5, 2007 |

Amount |

Per cent |

Amount |

|

Percent

|

1 |

2 |

3 |

4 |

5 |

|

6 |

Sources of Funds |

1. |

Aggregate Deposits |

23,81,242 |

2,85,182 |

17.2 |

4,38,037 |

|

22.5 |

2. |

Call/Term Funding from Financial Institutions |

84,629 |

16,070 |

24.6 |

3,265 |

|

4.0 |

3. |

Overseas Foreign Currency Borrowings |

26,143 |

5,644 |

22.5 |

-4,595 |

|

-14.9 |

4. |

Capital and Reserves |

1,96,070 |

39,528 |

30.3 |

26,034 |

|

15.3 |

Uses of Funds |

1. |

Bank Credit |

17,57,479 |

3,09,053 |

29.7 |

4,07,718 |

|

30.2 |

|

of which: Non-food Credit |

17,14,396 |

3,11,013 |

31.2 |

4,07,735 |

|

31.2 |

2. |

Investments in Government Papers |

7,43,964 |

-729 |

-0.1 |

39,288 |

|

5.6 |

3. |

Investments in Other Approved Securities |

21,821 |

-2,710 |

-13.1 |

3,793 |

|

21.0 |

4. |

Investments in Non-SLR Securities |

1,39,237 |

-11,957 |

-8.6 |

11,761 |

|

9.2 |

5. |

Foreign Currency Assets |

50,617 |

7,388 |

23.1 |

11,261 |

|

28.6 |

6. |

Balances with the RBI |

1,30,341 |

19,399 |

23.7 |

29,223 |

|

28.9 |

Note: Data are provisional. |

of SCBs fell to Rs.96,407 crore as on January 5, 2007 from Rs.1,68,029 crore a year ago. Funds raised through equity issuances in the primary market as well as higher internal reserves also enabled banks to fund strong credit demand.

Reserve Money Survey

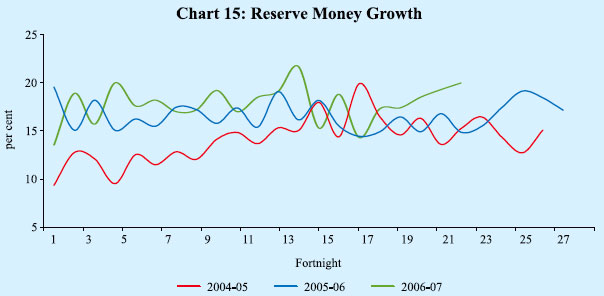

Reserve money expanded by 20.0 per cent, y-o-y, as on January 19, 2007 as compared with 14.9 per cent a year ago (Chart 15). Adjusted for the first round effect of the hike in the CRR, reserve money growth was 17.4 per cent as on January 19, 2007. Reserve money movements over the course of the year reflected the Reserve Bank’s market operations.

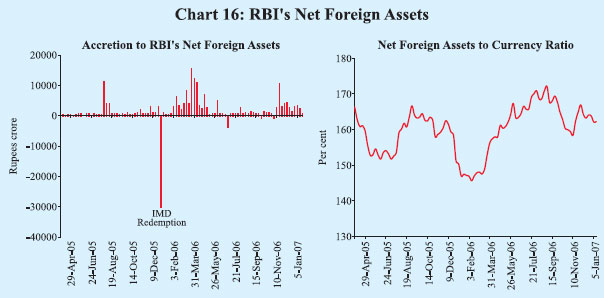

The Reserve Bank’s foreign currency assets (net of revaluation) increased by Rs.80,166 crore during the fiscal year 2006-07 (up to January 19, 2007) as compared with an increase of Rs.11,185 crore during the corresponding period of the previous year (Table 22 and Chart 16).

Mirroring the liquidity management operations through LAF, the Reserve Bank’s holdings of Government securities increased by Rs.10,615 crore during 2006-07 (up to January 19, 2007) as against an increase of Rs.27,435 crore in the corresponding period of 2005-06. During 2006-07 so far, Central Government

Table 22: Variation in Reserve Money |

(Rupees crore) |

Item |

Outstanding as on Jan.

19, 2007 |

Variation during |

2005-06 |

2006-07

(up to

Jan.19) |

2005-06 |

2006-07 |

(April-

March) |

(up to

Jan.20) |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

|

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

10 |

11 |

12 |

Reserve Money |

6,41,790 |

83,930 |

45,809 |

68,724 |

7,177 |

1,061 |

25,438 |

50,254 |

13,463 |

18,666 |

14,243 |

|

|

|

(17.2) |

(9.4) |

(12.0) |

|

|

|

|

|

|

|

Components (1+2+3) |

|

|

|

|

|

|

|

|

|

|

|

1. |

Currency in Circulation |

4,88,251 |

62,015 |

48,574 |

57,575 |

19,877 |

-9,479 |

29,154 |

22,462 |

22,283 |

-2,011 |

26,771 |

|

|

|

(16.8) |

(13.2) |

(13.4) |

|

|

|

|

|

|

|

2. |

Bankers’ Deposits with RBI |

1,47,830 |

21,515 |

-870 |

12,319 |

-10,680 |

9,780 |

-2,967 |

25,382 |

-7,204 |

20,224 |

-12,165 |

3. |

Other Deposits with the RBI |

5,709 |

401 |

-1,896 |

-1,170 |

-2,021 |

760 |

-750 |

2,411 |

-1,617 |

453 |

-363 |

Sources (1+2+3+4-5) |

|

|

|

|

|

|

|

|

|

|

|

1. |

RBI’s net credit to Government |

12,242 |

26,111 |

45,297 |

4,106 |

9,275 |

-25,251 |

19,879 |

22,208 |

53 |

2,826 |

-12,754 |

|

of which: to Centre (i+ii+iii+iv-v) |

12,123 |

28,417 |

50,622 |

6,963 |

14,600 |

-25,251 |

19,812 |

19,256 |

3,071 |

2,584 |

-12,568 |

|

i. Loans and Advances |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

|

ii. Treasury Bills held by the RBI |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

|

iii. RBI’s Holdings of Dated Securities |

81,024 |

13,869 |

27,435 |

10,615 |

8,221 |

-17,243 |

19,378 |

3,513 |

-27,610 |

24,944 |

22,733 |

|

iv. RBI’s Holdings of Rupee coins |

117 |

7 |

73 |

-37 |

-40 |

-33 |

157 |

-77 |

9 |

-107 |

97 |

|

v. Central Government Deposits |

69,018 |

-14541 |

-23,113 |

3,615 |

-6,419 |

7,974 |

-277 |

-15,820 |

-30,672 |

22,253 |

35,398 |

2. |

RBI’s credit to banks and commercial sector |

9,711 |

535 |

1,776 |

2,528 |

1,155 |

-1,869 |

101 |

1,148 |

-3,135 |

3,107 |

2,065 |

3. |

NFEA of RBI |

7,87,321 |

60,193 |

2,043 |

1,14,337 |

-14,595 |

24,823 |

23,741 |

26,224 |

71,845 |

11,392 |

27,250 |

|

|

|

(9.8) |

(0.3) |

(17.0) |

|

|

|

|

|

|

|

|

of which: FCA, adjusted for revaluation |

|

68,834 |

11,185 |

80,166 |

5,034 |

23,665 |

11,998 |

28,137 |

28,107 |

10,948 |

31,634 |

4. |

Governments’ Currency Liabilities to the Public |

8,054 |

1,306 |

1,216 |

-700 |

384 |

910 |

-100 |

112 |

-920 |

155 |

66 |

5. |

Net Non-Monetary liabilities of RBI |

1,75,537 |

4,215 |

4,524 |

51,547 |

-10,957 |

-2,449 |

18,183 |

-562 |

54,380 |

-1,186 |

2,384 |

Memo: |

Net Domestic Assets |

-1,45,531 |

23,737 |

43,766 |

-45,613 |

21,771 |

-23,761 |

1,697 |

24,030 |

-58,382 |

7,274 |

-13,007 |

Reserve Bank’s Primary |

|

10,000 |

0 |

0 |

0 |

0 |

0 |

10,000 |

0 |

0 |

0 |

Subscription to Dated Securities |

|

|

|

|

|

|

|

|

|

|

|

LAF, Repos (+) / Reverse Repos (-) |

11,810 |

12,080 |

33,100 |

19,060 |

9,660 |

-14,835 |

18,635 |

-1,380 |

-23,060 |

28,395 |

22,195 |

Net Open Market Sales # |

|

3,913 |

3,405 |

3,656 |

1,543 |

941 |

261 |

1,168 |

1,536 |

1,176 |

389 |

Mobilisation under MSS |

40,491 |

-35,149 |

-24,508 |

11,429 |

7,469 |

-4,353 |

-19,713 |

-18,552 |

4,062 |

8,940 |

-3,315 |

Net Purchases(+)/Sales(-) from |

|

32,884 |

-14,932 |

35,901@ |

0 |

17,027 |

0 |

15,857 |

21,545 |

0 |

14,356@ |

Authorised Dealers |

|

|

|

|

|

|

|

|

|

|

|

NFEA/RM (per cent) (end-period) |

122.7 |

117.4 |

114.9 |

122.7 |

120.5 |

125.3 |

123.7 |

117.4 |

127.0 |

125.0 |

126.5 |

NFEA/Currency (per cent) (end-period) |

161.3 |

156.3 |

147.4 |

161.3 |

154.0 |

164.4 |

158.4 |

156.3 |

164.4 |

167.7 |

164.0 |

NFEA : Net Foreign Exchange Assets. FCA : Foreign Currency Assets. @ : up to end-November 2006.

*: At face value.

#: Excludes Treasury Bills

$ : Adjusted for Centre’s surplus investment.

Note: 1. Data are based on March 31 for Q4 and last reporting Friday for all other quarters.

2. Figures in parentheses are percentage variations during the fiscal year. |

deposits with the Reserve Bank have increased by Rs.3,615 crore. The Reserve Bank’s net credit to the Centre, thus, increased by Rs.6,963 crore during the fiscal year 2006-07 (up to January 19, 2007) as against an increase of Rs.50,622 crore during the corresponding period of 2005-06 (see Table 22).

Liquidity Management

The Reserve Bank continued to ensure that appropriate liquidity is maintained in the system so that all legitimate requirements of credit are met, particularly for productive purposes, consistent with the objective of price and financial stability. Towards this end, the Reserve Bank continued with its policy of active demand management of liquidity through OMO including MSS, LAF and CRR, and using all the policy instruments at its disposal flexibly. However, liquidity management emerged to be more complex during the past year, with greater variation in market liquidity, largely reflecting variations in cash balances of the Governments and capital flows.

During the first quarter, unwinding of the Centre’s surplus balances with the Reserve Bank and the Reserve Bank’s purchase of foreign exchange from authorised dealers led to ample liquidity into the banking system. This was mirrored in an increase in the LAF reverse repo balances. However, in view of some build-up of Centre’s cash balances with the Reserve Bank during August 2006, the absorption under LAF reverse repos witnessed some decline during the second quarter.

Beginning mid-September 2006, liquidity conditions turned tight on account of advance tax outflows and festival season currency demand. The Reserve Bank injected liquidity through repos on eight occasions between mid-September 2006 and end-October 2006. However, net injection of liquidity was witnessed only on two occasions (October 20 and October 23, 2006). Liquidity pressures

Table 23: Reserve Bank’s Liquidity Management Operations |

(Rupees crore) |

Item |

2005-06

(April-

March) |

2006-07

(April-

Jan 19) |

Variations during |

2006-07 |

Q1 |

Q2 |

Q3 |

Oct. |

Nov. |

Dec. |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

A. |

Drivers of Liquidity (1+2+3+4) |

-31,719 |

2,678 |

36,271 |

-16,675 |

-26,143 |

-8,006 |

8,552 |

-26,689 |

1. |

RBI’s Foreign Currency Assets |

|

|

|

|

|

|

|

|

|

(adjusted for revaluation) |

68,834 |

80,166 |

28,517 |

10,538 |

34,821 |

4,031 |

17,066 |

13,724 |

2. |

Currency with the Public |

-57,280 |

-58,870 |

-19,624 |

-1,049 |

-27,435 |

-18,228 |

-170 |

-9,038 |

3. |

Surplus Cash balances of the Centre |

|

|

|

|

|

|

|

|

|

with the Reserve Bank |

-22,726 |

401 |

40,207 |

-26,199 |

-30,761 |

8,953 |

-5,437 |

-34,277 |

4. |

Others (residual) |

-20,547 |

-19,019 |

-12,828 |

36 |

-2,767 |

-2,762 |

-2,908 |

2,902 |

B. |

Management of Liquidity (5+6+7+8) |

57,969 |

-5,154 |

-39,003 |

32,026 |

31,625 |

-8,382 |

-1,541 |

41,548 |

5. |

Liquidity impact of LAF Repos |

12,080 |

19,060 |

-35,315 |

40,650 |

33,600 |

-10,355 |

-3,725 |

47,680 |

6. |

Liquidity impact of OMOs (Net) * |

10,740 |

715 |

545 |

145 |

25 |

0 |

10 |

15 |

7. |

Liquidity impact of MSS |

35,149 |

-11,429 |

-4,232 |

-8,769 |

4,750 |

1,973 |

2,174 |

603 |

8. |

First round liquidity impact due to CRR change |

0 |

-13,500 |

0 |

0 |

-6,750 |

0 |

0 |

-6,750 |

C. |

Bank Reserves (A+B) # |

26,250 |

-2,476 |

-2,732 |

15,351 |

5,482 |

-16,388 |

7,011 |

14,859 |

(+): Indicates injection of liquidity into the banking system.

(-): Indicates absorption of liquidity from the banking system.

#: Includes vault cash with banks and adjusted for first round liquidity impact due to CRR change.

*: Adjusted for Consolidated Sinking Funds (CSF) and Other Investments and including private placement.

Note: Data pertain to March 31 and last Friday for all other months. |

eased by end-October 2006 following some decline in Centre’s surplus cash balances (Table 24). Liquidity conditions eased during November 2006, partly

|

Table 24: Liquidity

Management

|

|

(Rupees crore)

|

|

Outstanding as on last Friday of

|

LAF

|

MSS

|

Centre's Surplus

with the

RBI @

|

Total (2 to 4)

|

|

1

|

2

|

3

|

4

|

5

|

|

2005

|

|

March*

|

19,330

|

64,211

|

26,102

|

1,09,643

|

|

April

|

27,650

|

67,087

|

6,449

|

1,01,186

|

|

May

|

33,120

|

69,016

|

7,974

|

1,10,110

|

|

June

|

9,670

|

71,681

|

21,745

|

1,03,096

|

|

July

|

18,895

|

68,765

|

16,093

|

1,03,753

|

|

August

|

25,435

|

76,936

|

23,562

|

1,25,933

|

|

September

|

24,505

|

67,328

|

34,073

|

1,25,906

|

|

October

|

20,840

|

69,752

|

21,498

|

1,12,090

|

|

November

|

3,685

|

64,332

|

33,302

|

1,01,319

|

|

December

|

-27,755

|

46,112

|

45,855

|

64,212

|

|

2006

|

|

January

|

-20,555

|

37,280

|

39,080

|

55,805

|

|

February

|

-12,715

|

31,958

|

37,013

|

56,256

|

|

March*

|

7,250

|

29,062

|

48,828

|

85,140

|

|

April

|

47,805

|

24,276

|

5,611

|

77,692

|

|

May

|

57,245

|

27,817

|

0

|

85,062

|

|

June

|

42,565

|

33,295

|

8,621

|

84,481

|

|

July

|

44,155

|

38,995

|

8,770

|

91,920

|

|

August

|

23,985

|

42,364

|

26,791

|

93,140

|

|

September

|

1,915

|

42,064

|

34,821

|

78,800

|

|

October

|

12,270

|

40,091

|

25,868

|

78,229

|

|

November

|

15,995

|

37,917

|

31,305

|

85,217

|

|

December

|

-31,685

|

37,314

|

65,582

|

71,211

|

|

January (as on 19th)

|

-11,810

|

40,491

|

48,428

|

77,109

|

|

@ : Excludes minimum cash balances with the Reserve Bank.

* : Data pertain to March 31.

Note : Negative sign in column 2 indicates injection

of liquidity through LAF repo.

|

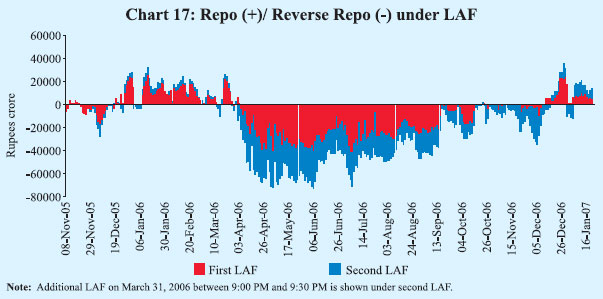

reflecting market purchases of foreign exchange by the Reserve Bank. This was mirrored in balances under LAF reverse repos, which increased to Rs 34,255 crore as on December 6, 2006 (Chart 17).

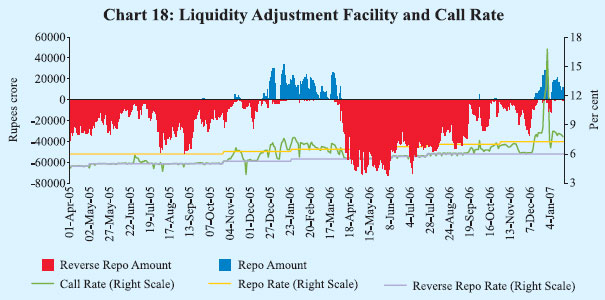

Liquidity conditions, however, turned tight from the second week of December 2006 largely due to payments for auctioned Central Government securities, advance tax outflows (with concomitant increase in the Centre’s surplus cash balances with the Reserve Bank from Rs.42,716 crore as on December 15, 2006 to Rs.73,634 crore as on December 22, 2006), and the increase in the CRR by 50 basis points in two phases. In view of the prevailing liquidity conditions, the Reserve Bank injected liquidity into the system through repo operations from December 12, 2006 (Chart 18). Average

daily net injection of liquidity by the Reserve Bank increased from Rs.5,615 crore during December 13-21, 2006 to Rs.25,585 crore during December 22-29, 2006, in contrast to the average daily absorption of Rs.12,262 crore and Rs.9,937 crore during October 2006 and November 2006, respectively. Average daily net injection of liquidity by the Reserve Bank moderated to Rs.10,814 crore during January 2007 (up to January 20, 2007), as liquidity pressures eased partly on account of reduction in the Centre’s balance with the Reserve Bank from Rs.65,682 crore as on December 29, 2006 to Rs 48,528 crore as on January 19, 2007. Net outstanding balance under LAF repos was Rs.10,190 crore as on January 24, 2007.

|

IST,

IST,