IST,

IST,

Union Budget 2025-26: An Assessment

|

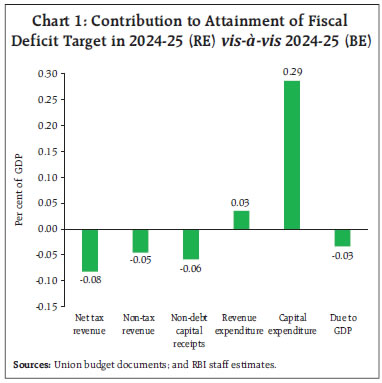

by Akash Raj, Harshita Yadav, Kovuri Akash Yadav, Aayushi Khandelwal, Anoop K Suresh, and Samir Ranjan Behera^ The Union Budget 2025–26 reaffirms the Government’s commitment to fiscal discipline while fostering inclusive, long-term economic growth in line with the vision of ‘Viksit Bharat’. The Budget announced several measures under four engines of growth – agriculture, MSMEs, investment, and exports. The Government continued with its focus on capex alongside measures to support consumption. With a fiscal deficit target of 4.4 per cent of GDP, the Budget prudently balances fiscal consolidation and growth objectives. Introduction The Union Budget 2025–26 focuses on accelerating growth, securing inclusive development, invigorating private sector investments, uplifting household sentiments, and enhancing the spending power of India’s rising middle class. Four principal drivers – agriculture, micro, small and medium enterprises (MSMEs), investment, and exports – are envisaged to propel growth, with innovation and reform acting as the vital catalysts. The Budget presents a balanced focus on immediate socio-economic relief and long-term structural transformation. It underscores the deployment of targeted measures across ten thematic areas, ranging from agricultural productivity and rural prosperity to the modernisation of urban infrastructure and the strengthening of energy security. The Budget articulates a reform agenda spanning six domains - taxation, power, urban development, mining, financial sector, and regulatory frameworks - to enhance overall factor productivity and ensure a more efficient allocation of resources in the economy. On the direct tax front, the Budget proposes tax relief of ₹1 lakh crore focused on middle-class taxpayers, which is expected to bolster household disposable incomes, and stimulate consumption, savings, and investment. In the realm of indirect taxation, revised customs duties target tariff simplification and address duty inversions. On the expenditure side, the Budget 2025-26 earmarks ₹11.2 lakh crore (3.1 per cent of GDP) for capital expenditure, continuing the impetus observed in the previous fiscal years. Similarly, the effective capital expenditure is budgeted to increase to 4.3 per cent of GDP in 2025-26 from 4.1 per cent of GDP in 2024-25 (RE). Revenue expenditure is projected to fall from 11.4 per cent of GDP in 2024-25 (RE) to 11.0 per cent in 2025-26 (BE). To further encourage State governments to augment their own capital spending, the ‘Special Assistance as Loans to States for Capital Expenditure’ has been extended with a provision of ₹1.5 lakh crore. The Union Budget balances growth imperatives with fiscal prudence by targeting gross fiscal deficit (GFD) at 4.4 per cent of GDP in 2025-26 (BE), down from the revised estimates (RE) of 4.8 per cent in 2024-25, adhering to its objective of bringing the GFD below 4.5 per cent of GDP by 2025-26. From 2026-27 onwards, the Government aims to maintain the fiscal deficit on a trajectory that ensures a declining public debt-to-GDP ratio, reaching around 50 per cent by March 2031. Against this backdrop, the rest of the article is divided into eight sections. Section II is a discussion of the underlying drivers of fiscal deficit, followed by analyses of revenue and expenditure trends in Sections III and IV, respectively. Section V outlines the Government’s outstanding debt position, while Section VI focuses on the major sources of fiscal deficit financing. Section VII examines the transfer of resources to States whereas Section VIII puts forth the concluding observations. II. Fiscal Deficit – The Underlying Dynamics As against the budgeted GFD of 4.9 per cent of GDP for 2024-25, the revised estimates are placed at 4.8 per cent. The 10-basis point consolidation is primarily attributable to lower than budgeted capital expenditure (Chart 1). The GFD for 2025-26 (BE) is set at 4.4 per cent of the GDP.1 The envisaged consolidation of 45 basis points for 2025-26 (BE) vis-à-vis 2024-25 (RE) is sought to be achieved through containment of revenue expenditure at 11.0 per cent of GDP [from 11.4 per cent in 2024-25 (RE)] and maintaining capital expenditure at 3.1 per cent of GDP, while aiming to augment gross tax revenues to 12.0 per cent of GDP (from 11.9 per cent of GDP in RE for 2024-25) [Table 1]. The revenue expenditure - capital outlay (RE-CO) ratio – a summary indicator of the quality of expenditure - is retained at 4.4 in 2025-26 (BE).

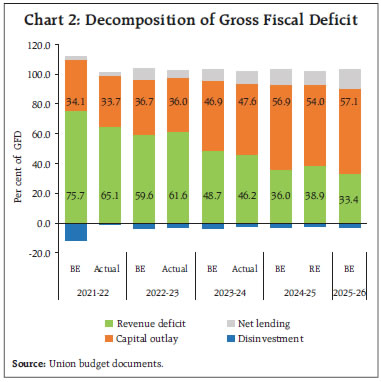

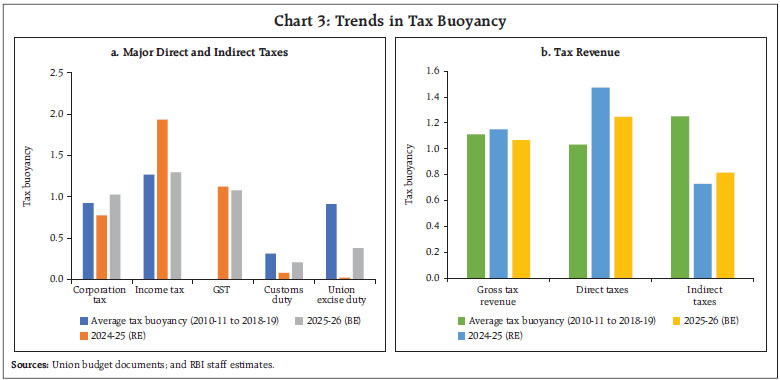

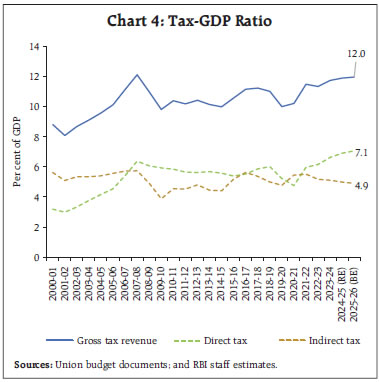

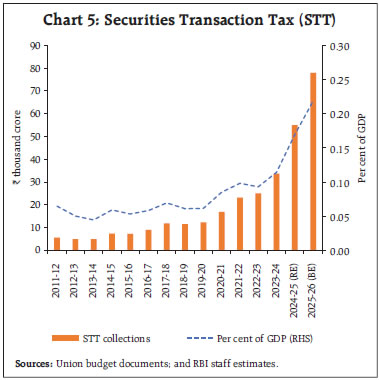

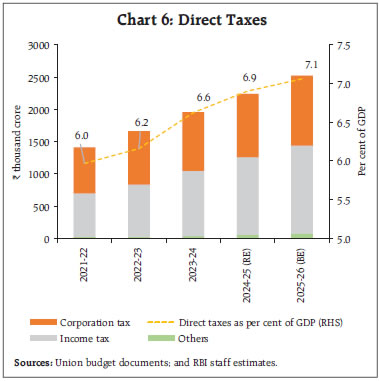

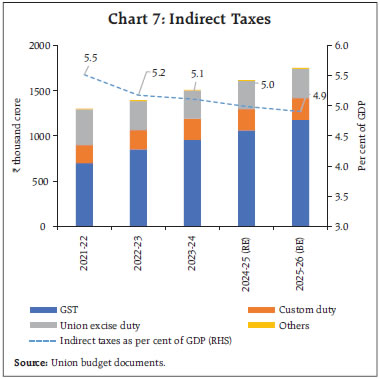

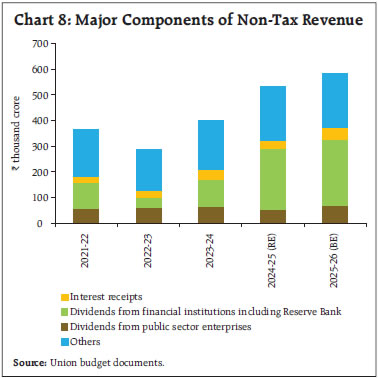

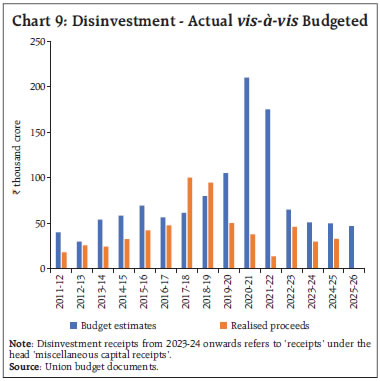

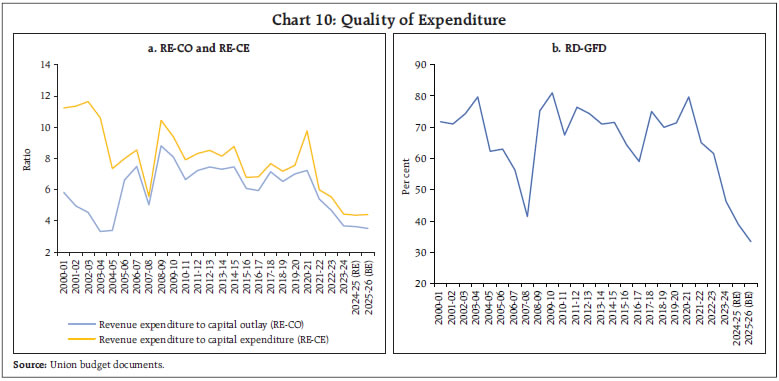

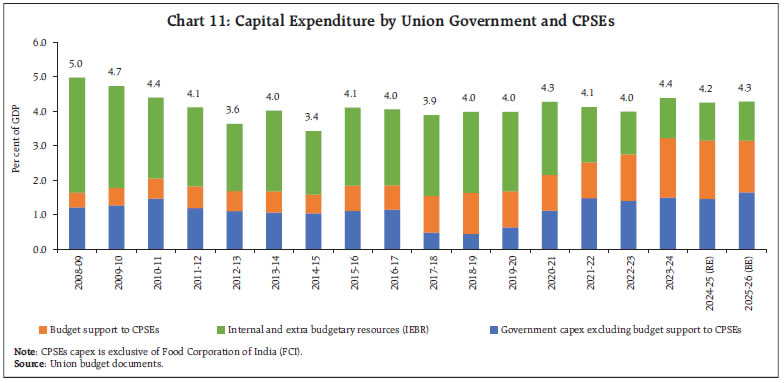

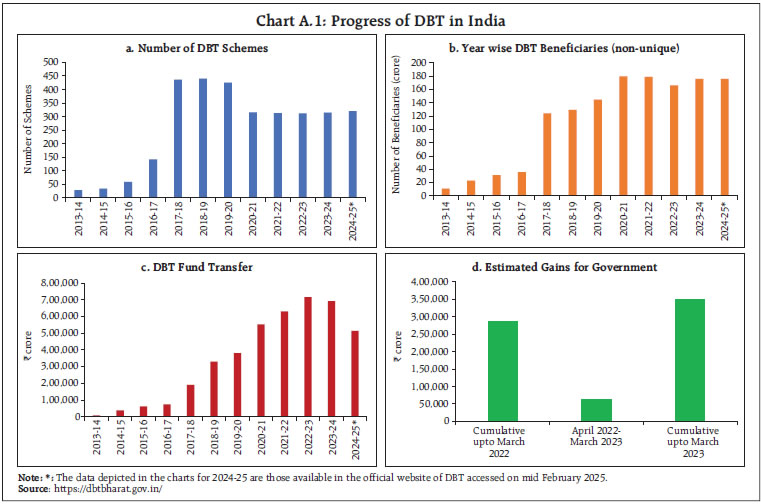

Decomposition of GFD The share of GFD appropriated by revenue deficit (RD) declined from an average of around 65.7 per cent during 2018-19 to 2023-24, to 38.9 per cent in 2024-25 (RE), is budgeted to fall further to 33.4 per cent in 2025-26. Concomitantly, the share of growth-inducing capital outlay in GFD has risen to 54.0 per cent in 2024-25 (RE) and is expected to reach 57.1 per cent in 2025-26 (BE), from an average of around 35.2 per cent over 2018-19 to 2023-24 (Chart 2). Total non-debt receipts recorded a growth of 12.8 per cent in 2024-25 (RE) and stood at 9.7 per cent of the GDP. The robust growth in tax revenue, higher surplus transfers from the Reserve Bank, and improved dividend income from public sector banks and financial institutions supported the improved performance of receipts in 2024-25 (RE) vis-à-vis 2023-24. For 2025-26 (BE), the government expects the non-debt receipts to maintain their momentum, growing from 9.7 per cent of GDP in 2024-25 (RE) to 9.8 per cent of GDP in 2025-26 (BE). Gross tax revenue is budgeted to grow by 10.8 per cent in 2025-26, along with a 9.8 per cent increase in non-tax revenue. With devolution to the States budgeted to grow by 10.5 per cent vis-à-vis 2024-25 (RE), net tax revenue is expected to increase by 11.0 per cent in 2025-26 (BE).  Tax Revenues Gross tax revenue recorded a growth of 11.2 per cent in 2024-25 (RE) over 2023-24, driven by income tax and GST collections. For 2025-26, the government has budgeted a 10.8 per cent growth in gross tax revenue, with the tax buoyancy remaining broadly in line with the average during 2010-11 to 2018-19. The buoyancy of the direct taxes is placed lower at 1.25 in 2025-26 (BE) compared to 1.47 in 2024-25 (RE) reflecting income tax relief, while that of indirect taxes is expected to recover to 0.82 in 2025-26 (BE) from 0.73 in 2024-25 (RE) on the back of gains in customs and excise duties (Chart 3a and b).  The gross tax-GDP ratio is budgeted to increase to 12.0 per cent in 2025-26, the highest post 2007-08 (Chart 4). The Budget has raised the tax-free income limit from ₹7 lakh to ₹12 lakh under the new tax regime. Moreover, tax slabs have been revised across all income brackets. The tax relief is expected to enhance disposable incomes and provide a boost to household consumption and investments. The total revenue foregone on account of various measures is estimated at around ₹1 lakh crore in direct taxes and ₹2,600 crore in indirect taxes.3  Direct Taxes With a growth of 14.4 per cent, direct taxes in 2024-25 (RE) surpassed the budget estimates by ₹30,000 crore. Income tax revenues with a growth of 18.8 per cent offset the shortfall of ₹40,000 crore in corporate tax collections compared to the BE. During 2024-25 (RE), the securities transaction tax outperformed its BE of ₹37,000 crore by 48.6 per cent; it is budgeted to further increase by 41.8 per cent in 2025-26 (BE) [Chart 5]. For 2025-26 (BE), direct tax revenues are expected to grow by 12.7 per cent, with growth in income and corporate tax at 13.1 per cent and 10.4 per cent, respectively (Chart 6). The Budget has announced various simplification and rationalisation measures aimed at promoting compliance and broadening the tax base. Indirect Taxes Indirect tax revenues rose by 7.1 per cent in 2024-25 (RE) but were below the budgeted amount, primarily on account of ₹14,000 crore shortfall in union excise duties.4 The GST collections were in line with the budget estimates. In 2025-26 (BE), the growth in the indirect tax collections is budgeted at 8.3 per cent, with GST, customs, and excise collections growth at 10.9 per cent, 2.1 per cent, and 3.9 per cent, respectively (Chart 7).    Non-Tax Revenue Supported by the higher surplus transfer from the Reserve Bank, non-tax revenue recorded a growth of 32.2 per cent in 2024-25 (RE). For 2025-26 (BE), the non-tax revenue growth is placed at 9.8 per cent, led by 25.5 per cent growth in dividends and profits from public sector enterprises (PSEs), and 9.3 per cent from the Reserve Bank, public sector banks and financial institutions (Chart 8).  Non-Debt Capital Receipts Non-debt capital receipts in 2024-25 (RE) fell short of BE by ₹19,000 crore, primarily due to lower disinvestment receipts. In 2025-26 (BE), non-debt capital receipts are budgeted to grow by 28.8 per cent, with the disinvestment target of ₹47,000 crore (Chart 9). Total expenditure of the Union government recorded a growth of 6.1 per cent in 2024-25 (RE), and it was ₹1.04 lakh crore below the BE mainly due to the underutilisation of allocated capital expenditure (Table 2). The revenue expenditure, in contrast, was in line with the budget estimates and posted a growth of 5.8 per cent in 2024-25 (RE). For 2025-26 (BE), total expenditure is budgeted to rise by 7.4 per cent, reaching 14.2 per cent of GDP. Capital expenditure is expected to recover with a growth of 10.1 per cent. Additionally, effective capital expenditure is budgeted to register a growth of 17.4 per cent in 2025-26 vis-à-vis 5.2 per cent growth in 2024-25 (RE) on account of 42.4 per cent growth in grants-in-aid for creation of capital assets. The Budget maintains the allocation of ₹1.5 lakh crore for the ‘Scheme for Special Assistance to States for Capital Expenditure’, in 2025-26 (BE) as in 2024-25 (BE). Revenue expenditure is budgeted to grow by 6.7 per cent, and RE-IP-TS by 5.1 per cent (6.3 per cent of GDP).  Quality of Expenditure The revenue expenditure - capital outlay (RE-CO) ratio stood at its lowest at 4.4 in both 2024-25 (RE) and 2025-26 (BE). Revenue deficit as per cent of gross fiscal deficit (RD-GFD) also stood at its all-time low of 33.4 per cent, indicating improvement in the quality of expenditure (Chart 10a and b).  Capital Outlay Capital outlay (capital expenditure less loans and advances) grew by 7.6 per cent in 2024-25 (RE). It fell short of the budgeted target by ₹70,959 crore, inter alia, due to the model code of conduct in the run-up to the general elections and heavy rains in the monsoon season. In 2025-26 (BE), capital outlay is budgeted to grow by 5.6 per cent (Table 3). Capital outlays of Railways, and Road and Bridges – the major drivers of the Centre’s capital spending – in 2025-26 (BE) have been retained at their 2024-25 (RE) levels. Combined Capex of the Union Government and Central Public Sector Enterprises Central public sector enterprises (CPSEs) finance their capex through internal and extra budgetary resources (IEBR)5 and budgetary support from the Union government, which forms a part of the government’s total capex. The combined capex of the Union government and CPSEs will increase marginally from 4.2 per cent of GDP in 2024-25 (RE) to 4.3 per cent of GDP in 2025-26 (BE) [Chart 11].  Major Government Schemes Among central sector programmes, PMGKAY receives the largest allocation at 4.0 per cent of total expenditure in 2025-26 (BE) [4.2 per cent in 2024-25 (RE)], with the outlay rising by 3.0 per cent to ₹2.03 lakh crore. PM-KISAN allocation has been maintained at last year’s level; and road works’ outlay has been expanded by 5.2 per cent to ₹1.16 lakh crore. Amongst the Centrally sponsored schemes, MGNREGA is unchanged at ₹86,000 crore, the Jal Jeevan Mission’s outlay is budgeted at ₹67,000 crore (195.2 per cent increase). PM Awas Yojana’s outlay has been increased by 64.1 per cent, with the Centre sustaining its focus on housing (Table 4). In recent years, there has been a significant increase in fund transfer by the government to beneficiaries under various social programmes through the DBT mechanism, resulting in savings for the government (Box A).

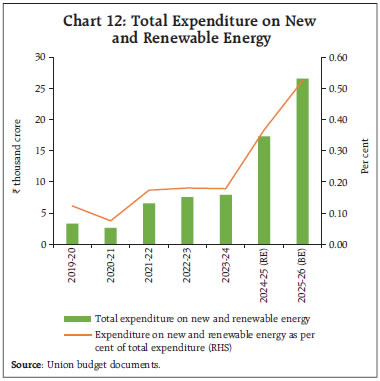

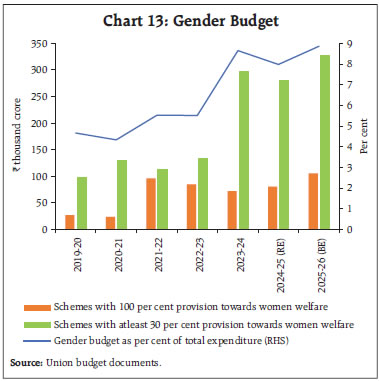

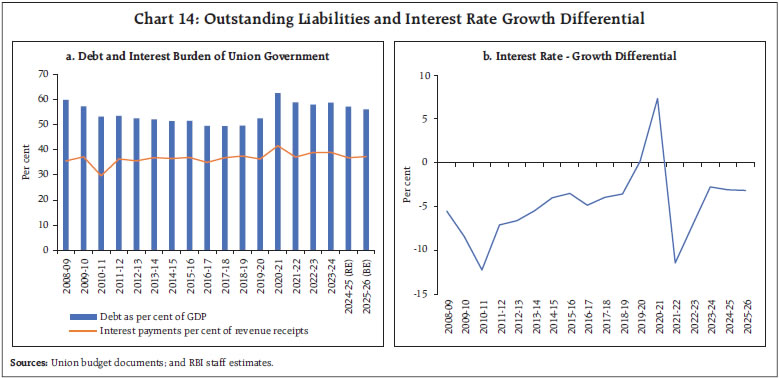

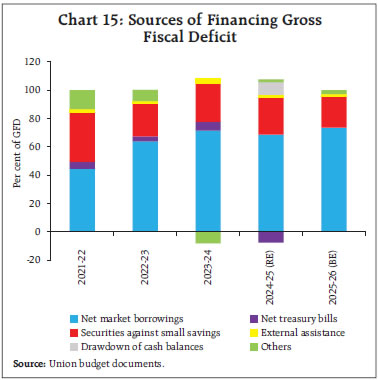

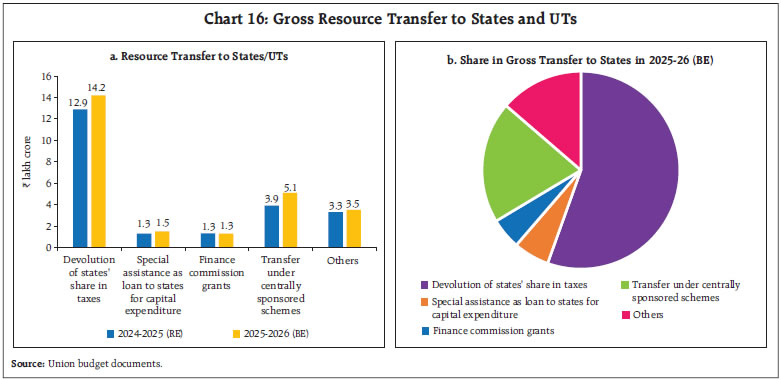

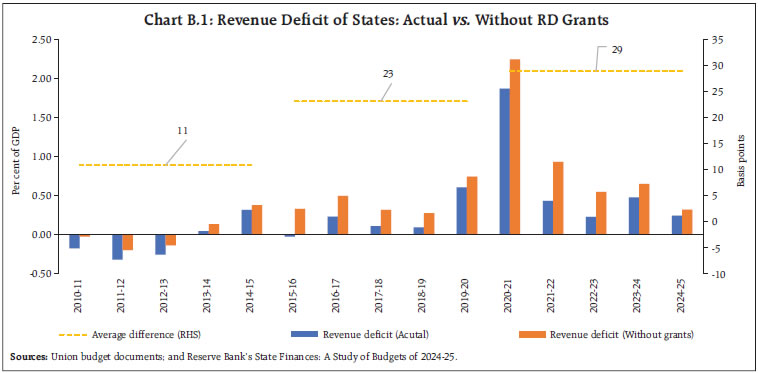

The expenditure towards new and renewable energy is budgeted to increase from 0.37 per cent of total expenditure in 2024-25 (RE) to 0.52 per cent in 2025-26 (BE) led by increased allocations towards PM Surya Ghar Muft Bijli Yojana (Chart 12). The gender budget of the Union government is also budgeted to increase to 8.9 per cent of its total expenditure in 2025-26, led by Pradhan Mantri Garib Kalyan Anna Yojana and Pradhan Mantri Awas Yojana (Chart 13). After peaking at 62.6 per cent of GDP in 2020-21 amidst the COVID-19 pandemic, the total outstanding debt of the Union government declined to 57.1 per cent of GDP in 2024-25 (RE) from 58.7 per cent in 2023-24 and is budgeted to decline further to 56.0 per cent of GDP in 2025-26. The interest payment to revenue receipts ratio is budgeted at 37.3 per cent in 2025-26. The interest rate – growth rate differential (IRGD), an indicator of debt sustainability, remains favourable (Chart 14a and b). Going forward, the government has indicated that it would maintain a fiscal deficit level which will help in bringing Centre’s debt-to-GDP ratio to 50 ±1 per cent by March 31, 2031.  VI. Gross Fiscal Deficit Financing On the financing side, gross market borrowings through dated securities for 2025-26 are budgeted at ₹14.82 lakh crore [an increase of about 5.8 per cent over ₹14.01 lakh crore in 2024-25 (RE)]. Net market borrowings are placed at ₹11.54 lakh crore as compared with the previous year’s ₹10.75 lakh crore.7 The Budget has also provided for gross switches of securities totalling ₹2.50 lakh crore in 2025-26, as against ₹1.47 lakh crore in the previous year’s revised estimates. The government has not budgeted for any buyback of securities during 2025-26. Net market borrowings are expected to finance 73.5 per cent of GFD in 2025-26 (BE), higher than 68.5 per cent in 2024-25 (RE). An amount of ₹3.43 lakh crore from small savings (NSSF) would finance 21.9 per cent of GFD in 2025-26 (BE), down from ₹4.12 lakh crore (26.2 per cent) in 2024-25(RE) [Chart 15].  The gradual downscaling in the market borrowing requirements (as per cent of GDP) of the Union government towards the pre-pandemic level will facilitate greater availability of resources for the private sector (Table 5). VII. Resource Transfer from Centre to States The gross transfers to States have been budgeted to increase by 12.5 per cent for 2025-26 [10.2 per cent during 2024-25 (RE)], largely on account of transfers under centrally sponsored schemes and special assistance to States for capital expenditure. The gross transfer of resources to States will increase from 7.0 per cent of GDP during 2024-25 (RE) to 7.2 per cent during 2025-26 (BE). Devolution of States’ share in taxes constitutes the largest component of gross transfers (Chart 16a and b).8   While tax devolution forms the cornerstone of fiscal transfers, post-devolution revenue deficit grants (RDGs) play a crucial role in stabilising state finances by bridging structural fiscal gaps (Box B).

Finance commission Grants are budgeted to increase by 4.4 per cent in 2025-26, mainly due to increase in grants for local bodies (both urban and rural) as well as grants for health sector (Table 6). The Budget has allocated ₹1.5 lakh crore under the 50-year interest-free loans for States’ capital expenditure and reform-linked incentives. Urban sector reforms will be incentivised, focusing on governance and municipal services. Towards boosting infrastructure, States will be encouraged to seek funding for PPP projects under the India Infrastructure Project Development Fund. The Budget proposes key power sector reforms to improve State-level electricity distribution and infrastructure. States will be incentivised to enhance financial health and efficiency of electricity distribution companies. To support this, States undertaking reforms will be allowed an additional borrowing of 0.5 per cent of gross state domestic product.. Many sector-specific initiatives in partnership with the States have been announced. In agriculture, States’ partnership is sought to implement schemes like Prime Minister Dhan-Dhaanya Krishi Yojana, Rural Prosperity and Resilience Programme and Comprehensive Programme for Vegetables and Fruits. The Jal Jeevan Mission is extended until 2028, with MoUs to be signed with States to ensure sustainable rural water supply. The Union government will also partner with States to develop 50 tourist destinations through a challenge-based mode. States must provide land for infrastructure to qualify for funding. The Union Budget 2025–26 reaffirms the Government’s commitment to fiscal discipline while fostering inclusive, long-term economic growth in line with the vision of ‘Viksit Bharat’. Towards this objective, the Budget has announced several measures under four engines of growth – agriculture, MSMEs, investment, and exports propelled by innovation and structural reforms. The Government has continued with its focus on capex alongside consumption boosting measures which would help the economy to improve its growth momentum. With a fiscal deficit target of 4.4 per cent of GDP, the Budget balances consolidation and growth objectives. The government would deploy debt/GDP ratio as a medium-term fiscal anchor going forward to preserve macroeconomic stability. Through structural reforms, augmented investments in critical sectors, and the rationalisation of taxes and expenditure, the Government seeks to maintain a stable macroeconomic environment conducive to robust and sustainable growth. ^ The authors are thankful to Smt. Rekha Misra for her overall guidance in preparing this article. The authors are from the Department of Economic and Policy Research of the Reserve Bank of India. The views expressed in this article are those of the authors and do not necessarily represent the views of the Reserve Bank of India. 1 The Union Budget has projected GDP for 2025-26 at ₹356,97,923 crore which is 10.1 per cent over the first advance estimates (FAE) for 2024-25 of ₹324,11,406 crore released by the Ministry of Statistics & Programme Implementation (MoSPI) on January 7, 2025. 2 For details, please refer to Annex I. 3 As mentioned in the Union Budget 2025-26 speech of the Finance Minister. 4 The moderation in union excise duties was led by a shortfall of ₹7,460 crore under special additional excise duties (SAED). In July 2022, the Union government introduced a SAED on production of crude oil and export of petrol, diesel and aviation turbine fuel. As per the notification issued by the Ministry of Finance, the same was rescinded in December 2024 (Source: Union Budget 2025-26; Petroleum Planning and Analysis Cell; and Central Board of Indirect Taxes & Customs). 5 IEBR comprises of internal resources (comprising of retained profits - net of dividend to Government, depreciation provision and carry forward of reserves and surpluses) and extra budgetary resources (consisting of receipts from issue of bonds, debentures, external commercial borrowing, suppliers’ credit, deposit receipts and term loans from financial institutions). Budgetary support and IEBR together finance the capital expenditure (capex) of CPSEs. 6 Data is upto March 2023 and has been sourced from https://dbtbharat.gov.in/. 7 Net market borrowing figures for 2024-25 (RE) includes buy back of securities [₹ (-)88,164.01 crore]. 8 For details, please refer to Annex II. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

ਇਸ ਪੇਜ ਨੂੰ ਸ਼ੇਅਰ ਕਰੋ:

ਭਾਰਤੀ ਰਿਜ਼ਰਵ ਬੈਂਕ ਮੋਬਾਈਲ ਐਪਲੀਕੇਸ਼ਨ ਇੰਸਟਾਲ ਕਰੋ ਅਤੇ ਨਵੀਨਤਮ ਖਬਰਾਂ ਤੱਕ ਤੇਜ਼ ਐਕਸੈਸ ਪ੍ਰਾਪਤ ਕਰੋ!

ਸਾਡੀ ਐਪ ਇੰਸਟਾਲ ਕਰਨ ਲਈ QR ਕੋਡ ਸਕੈਨ ਕਰੋ।

ਪੇਜ ਅੰਤਿਮ ਅੱਪਡੇਟ ਦੀ ਤਾਰੀਖ: