IST,

IST,

Chapter III : Financial Sector Regulation and Infrastructure

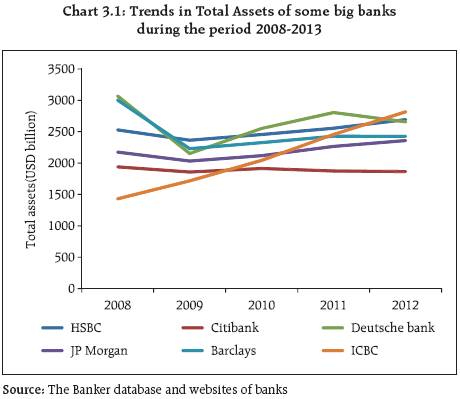

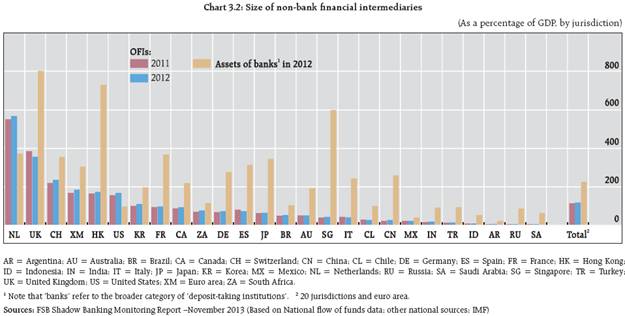

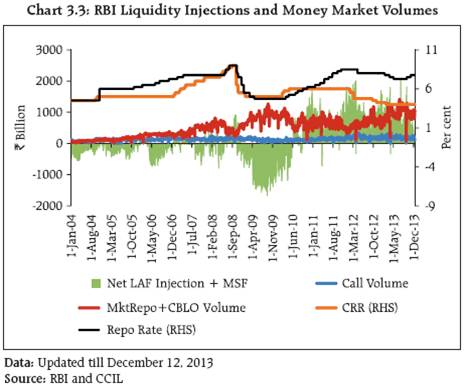

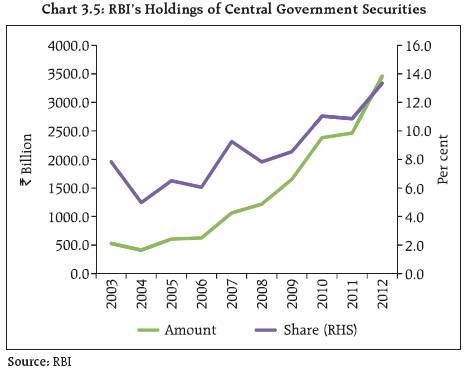

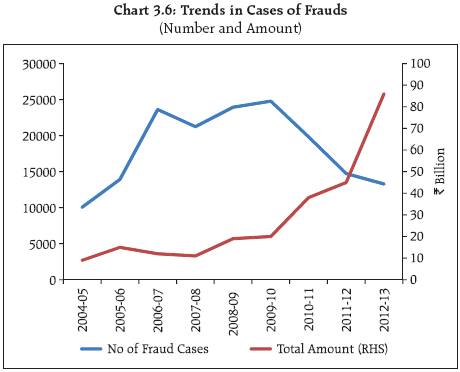

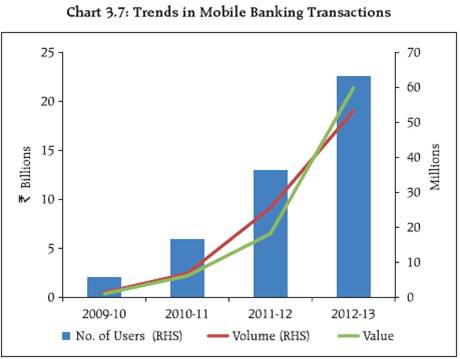

India stands committed to the implementation of the global regulatory reforms and has made considerable progress on this front. Globally, the policies aimed at ending ‘too-big-to-fail’ have not been entirely successful at the ground level. In India, the process of identification of financial conglomerates and their joint supervision/ regulation has received a lot of attention. Some global reform measures, e.g. those related to shadow banking may need to be adopted selectively, based on their relevance to the domestic financial system. The so called shadow banks in India have a key role in expanding the reach of the formal financial system to the remote corners of the country. Emerging regulatory gaps and scope for arbitrage need to be kept in view, while ensuring a healthy growth of the non- banking financial sector. Recent instances of manipulation of benchmarks and prices in international financial markets once more brought into focus the role of greed and the failure of self regulation of financial markets. India has set up a committee to review the systems and procedures in place with regard to the major financial benchmarks used in domestic markets. The initiatives by regulators towards installing centralised databases for large common credit exposures of banks, corporate debentures and insurance policy records are expected to improve the information flow and functioning of the financial system. The work on LEI system is also underway. The Financial Stability and Development Council and its Sub-Committee have been spearheading the work on systemic risk assessment, financial sector development, inter regulatory coordination, financial inclusion and literacy and implementation of regulations to foster financial stability. Global Regulatory Reforms Ending Too-Big-To-Fail 3.1 One of objectives of the reforms after the global financial crisis (GFC) was to develop and implement a policy framework to ensure that systemically important financial institutions (SIFIs) could be resolved without resorting to taxpayer support and/ or causing disruption to the financial system. The global SIFIs (G-SIFIs) were to be subjected to higher capital requirements and more stringent supervisory standards for risk management, data aggregation, risk governance and internal controls. The national resolution regimes were to be strengthened. As part of G-SIFIs, an initial group of global systemically important banks (G-SIBs) were identified in 2011, using a methodology developed by the Basel Committee on Banking Supervision (BCBS). The G-SIBs have been allocated to buckets corresponding to the higher loss absorbency requirements they would need to satisfy from January 2016. 3.2 The list of G-SIBs is updated every year in November by the Financial Stability Board (FSB) and the BCBS. According to the last updated list published in November 2013, 29 banking groups have been identified as G-SIBs. Increasing Size of Big Global Banks 3.3 Although firms and markets are beginning to adjust to the regulatory approach towards ending too-big-to-fail (TBTF), research1 based on bond credit spreads shows lower risk sensitivity for the largest financial institutions indicating continued expectation of sovereign support to such institutions. Even as efforts are under way to end the implicit subsidy associated with the SIFIs, the biggest banks have grown even bigger since 2008 (Chart 3.1). 3.4 Size alone does not capture the essence of the problem of TBTF, (e.g. the case of government owned banks). The complexity, interconnectedness and substitutability aspects of SIFIs make the problem much more difficult. As the big banks have got bigger, the need for a greater degree of transparency and market discipline has not yet been fully addressed. 3.5 The present debate on TBTF revolves around the final numbers for higher additional capital ratios for the SIFIs and their implications for credit and growth, with unresolved issues about the use of divergent accounting practices in respect of derivatives and differences in calculation of risk weighted assets. Meanwhile, at a national level, regulators seek to address the risks posed to domestic financial systems by the G- SIFIs by ring-fencing local operations. There is also a growing concern that lobbying by the very large and transnational firms may cause delays in finalising and implementing effective reform measures to address the fundamental issues related to TBTF. Framework for dealing with India’s Domestic Systemically Important Banks 3.6 There is no Indian bank in the list of G-SIBs. The BCBS and FSB have finalised a principles-based, minimum framework for addressing Domestic Systemically Important Banks (D-SIBs). 3.7 The Reserve Bank has released the draft framework2 for identifying the D-SIBs and the regulatory / supervisory policies applicable to them. The assessment methodology adopted by the Reserve Bank is essentially based on the BCBS methodology, with suitable modifications to capture domestic importance of a bank. The indicators for identification and assessment, proposed in the draft framework are: size, interconnectedness, substitutability and complexity. D-SIBs will be required to have additional Common Equity Tier 1 capital requirement ranging from 0.20 per cent to 0.80 per cent of risk weighted assets. The computation of systemic importance scores will be carried out at yearly intervals. Shadow Banking Divergence in Size and Profile 3.8 In its annual shadow banking monitoring exercise, the FSB uses “Other Financial Intermediaries” (OFIs) as a conservative proxy for the size of shadow banking. The OFIs include all Non- Banking Financial Institutions (NBFIs) except insurance companies, pension funds or public sector development financial entities. While, globally, the average share of OFI assets is about 24 per cent of GDP, there are significant variations in the size for individual jurisdictions (Chart 3.2). 3.9 For a number of emerging market economies, non-bank financial intermediation remained relatively small, compared to the level of GDP. On average, the size of non-bank financial intermediation in terms of assets was equivalent to 52 per cent of the banking system with cross-country differences, ranging from below 10 per cent in some emerging economies to 174 per cent in US at the end of 2012. 3.10 In India and certain other economies like Turkey, Indonesia, Argentina, Russia and Saudi Arabia, the non-bank financial assets remained below 20 per cent of GDP at the end of 2012. However, the sector showed rapid growth, though from a low base, in some of these jurisdictions, including India. While the growth trends need to be monitored, the role and characteristics of NBFIs in most developing countries are different from those in advanced economies. They are predominantly domestic in focus with minimal cross-border activities/risks, support financial inclusion and are subject to regulatory oversight. 3.11 In the Indian context, the Non Banking Finance Companies (NBFCs) are regulated by the Reserve Bank and all types of Mutual Funds (MFs) are regulated by the SEBI. As such India doesn’t have shadow banking entities, in the formal financial system, with potential for creating systemic instability. However, a large number of non-bank financial entities function in the unorganized sector (unincorporated entities – outside the purview of regulatory perimeter), whose collective size and profile of activities need to be gauged to ensure that they do not pose any threat to the ‘trust’ in and ‘stability’ of India’s financial system. Regulatory Arbitrage – NBFCs and Cooperative Societies 3.12 There is also a need to plug the regulatory gaps to stop financial entities from changing their ‘form’ for the implicit purpose of avoiding regulations, as was seen in a recent episode involving a company converting itself into a cooperative society to escape the rules relating to its fund raising and other activities. There are stringent norms for granting Certificate of Registration for NBFCs which are permitted to accept public deposits. The companies are thereafter subject to monitoring and may be restricted from accepting deposits if their financial position weakens. The Reserve Bank also prescribes limits on the quantum of deposits that can be accepted by an NBFC. The requirement of minimum capital and other financial parameters are more relaxed or non-existent in cases of cooperative societies. The cooperative credit societies which provide financial accommodation to their members also accept deposits from members as an activity incidental to their core activity. The quantum of these deposits is not regulated as in the case of NBFCs. The rate of interest which can be paid on public deposits accepted by NBFCs is regulated by Reserve Bank. However the interest rate offered by cooperative societies is not regulated or capped by any regulation. Money Market Mutual Funds – Interconnectedness with Banks 3.13 The previous FSR had mentioned that Money Market Mutual Funds (MMMFs) with constant Net Asset Value (NAV) were not permitted in India. However, the strong interconnectedness among banks and mutual funds has been a cause for concern. Debt mutual funds account for 70 per cent of the assets under management (AUM). 3.14 These mutual funds had experienced difficult liquidity conditions during the global financial crisis and SEBI had taken various regulatory measures viz. restriction on investments in certain instruments, changes in valuation norms, provisions regarding uniform cut-off timings for applicability of NAV etc. With low levels of retail participation, the MMMFs continue to rely on investment by banks, corporates and other institutional investors. 3.15 Due to their interconnectedness with banks, liquidity pressure is felt by the MMMFs whenever redemption requirements of banks are large and simultaneous. The liquid debt mutual funds are large lenders in the over-night markets such as collateralized borrowing and lending obligation (CBLO) and market repo, where banks are large borrowers. Various schemes of mutual funds also invest heavily in certificates of deposit (CDs) of banks. Such circular flow of funds between banks and mutual funds is a source of systemic instability in times of stress/ liquidity crunch, etc. In view of these concerns, banks’ investments in liquid / short term debt schemes of mutual funds was restricted to 10 per cent of their net worth3, effective July 2011. 3.16 Debt mutual funds in India had seen large inflows during 2012-13, from foreign institutional investors (FIIs) during the first five months of calendar year 2013, due to the higher returns offered. The depreciation of the Indian rupee in response to the announcement of tapering by the Fed earlier this year led to large scale sell off by FIIs of debt securities during the month of June 2013. 3.17 As a result of Reserve Bank’s measures on tightening of liquidity during July 2013, investments by banks as a percentage of total AUM of liquid/money market schemes declined (from 21.14 per cent on 15 July 2013 to 13.02 per cent as on 16 July 2013, which further declined to 7.77 per cent as on 31 July 2013). With a view to pre-empt any liquidity crisis for mutual fund industry SEBI and RBI took measures like enhancement (on case to case basis) in the borrowing limit of mutual fund schemes and a Special Reserve Bank Re-Finance Window to commercial banks for meeting the liquidity requirements of the mutual funds industry. However, these facilities were not actually availed, showing improvement in liquidity management by MFs even in the face of heavy redemptions. Financial Markets: Infrastructure and Development ‘Fixing’ in International Financial Markets 3.18 Recent reports of manipulation of benchmark reference rates and prices in international foreign exchange markets and spot oil markets and investigation by authorities in major developed jurisdictions have once again brought to focus concerns regarding the efficacy of self-regulation in financial markets. Some of the largest international banks have been penalised heavily for their role in the irregularities. It appears that the disproportionately large share in trading enjoyed by a few large players allows them to use the information asymmetry to their advantage at the cost of smaller players. The investigations also highlight the role of ethics in finance and the inherent limitations of regulation to pre-empt manipulation by market players of the rules on which the whole edifice of global financial markets rests. Review of Benchmarks in Indian Financial Markets 3.19 The benchmark setting process and governance mechanisms in case of major Indian financial benchmarks, mainly FIMMDA-NSE MIBOR (interest rate benchmark) and RBI Reference Rate (forex benchmark), have been observed to be robust. Although there have been no major instances of manipulation of market rates in India’s domestic markets, the Reserve Bank has constituted a committee to conduct a review of the systems and procedures in place with regard to major financial benchmarks in India. 3.20 The MIBOR is calculated from the polled rates from a select panel of 30 banks/primary dealers, using bootstrapping technique and the mean corresponding to the lowest standard deviation is taken as the fixing rate for the day. The bootstrapping method facilitates random drawing of multiple data sets which guards against the possibility of cartelisation and of extreme observations influencing the fixing rate. The condition requiring a specified minimum number of quotes after trimming mitigates the risk of loss of information due to excessive trimming. Moreover, the biggest safeguard against manipulation of overnight MIBOR fixed by NSE through polling has been the existing system of transparent execution of more than 90 per cent of the inter-bank money market trades on NDSCALL platform and dissemination of the traded rates (of the trades executed on NDS-CALL as well as outside NDS-CALL) in the public domain. 3.21 For the forex benchmarks, the Reserve Bank computes and disseminates the exchange rate of the Indian Rupee against US Dollar and Euro on a daily basis. The process is reviewed periodically in view of the changing dynamics of the domestic foreign exchange market and other factors like its growing linkages with the offshore market. As a result of changes brought into effect in April 2010, the number of banks in the polling panel was significantly expanded, of which a set of banks are selected randomly every day for obtaining quotes. Further, the reference time window was expanded to 30 minutes (1145 IST to 1215 IST) from the earlier 15 minutes, of which a five minute window is selected randomly every day for conducting polling. As bulk of USD/INR inter-bank spot trades are done on Reuters dealing platform and not on telephones, the actual traded rates are available almost instantly which are also compared with the polled rates to ensure that the polled rates are not significantly different from the actual dealt rates. Issues in Indian Fixed Income and Derivatives Markets 3.22 India’s domestic markets for interest rate derivatives, despite an existence of two decades have not taken off, due to the absence of some of the basic building blocks4. Since derivatives are priced through replication portfolios, two building blocks are required to be in place. First, reasonable asset market liquidity and second, a transparent funding curve against which the market makers in the derivatives market can lend or borrow. Even if the asset market liquidity is taken as exogenous, the absence of a funding curve induces pricing inefficiency in the derivatives segment. Even though banks generally have significant appetite for unsecured term borrowing (as the market in CDs as well as borrowing through bulk deposits from institutional corporate participants for shorter tenors show), an inter-bank term lending benchmark has not yet developed. 3.23 Delivery based Interest Rate Futures (IRFs) suffer from inherent limitations owing to non uniform liquidity in the underlying deliverables affecting the price discovery of the product. However, as per the recent guidelines issued on December 5, 2013, all the IRFs will now be cash settled (91days, 2yr & 5yr and 10yr). 10yr IRF will have both cash settled and delivery based options. 3.24 While some issues like narrow institutional ownership, low retail participation and domination of on the run securities have affected the liquidity in Government securities market, the G-Sec market liquidity has improved over the years and in May, the average daily volume had clocked the `1 trillion mark. The anonymous electronic trading platform and CCP based clearing for all G-Sec trades (including OTC) have provided a great fillip to the market liquidity. It is observed that the market liquidity in the present Indian context is more a function of interest rate movements and inflation/interest rate outlook than of structural factors. 3.25 As regards, development of a term money market, there are non-trivial operational issues that are required to be resolved (like benchmark based on secondary market CD trades or primary issuances, cohort of banks) prior to finalising the design of the benchmark. While multiple swap curves based on floating rate indices (currently the individual “base rates” of banks) are symptomatic of market inefficiency, inter-se trading between OIS and the term Interest Rate Swap (IRS) curves is likely to erase any arbitrageable differential. 3.26 While the recent initiative of Reserve Bank to offer term repo facility is expected to develop a term money market curve, introduction of money market futures on the lines of Euro dollar futures would hasten inter-se convergence between curves but introduction of the money market futures should ideally follow establishment of term benchmarks and not the other way round. The liquidity in interest rate derivatives segment as well as government securities segment is likely to be positively affected if non-bank participants enter the fray. Such participants are relatively immune to accounting methodology applicable to banks and hence can winnow out arbitrage opportunities. Liquidity Management in Banks 3.27 The Indian banking system has been persistently borrowing from the Reserve Bank window starting mid-2010 (Chart 3.3), suggesting that banks have become dependent on central bank support in meeting their structural funding deficits. Prior to mid- 2010 banks borrowed only occasionally from the Reserve Bank despite high credit growth (Chart 3.4). In addition, RBI’s holding of GoI securities have also been increasing (Chart 3.5). During the period covered (2004-2013) volumes in overnight unsecured interbank market (call money market) remained broadly unchanged indicating constraints for the overnight unsecured interbank market (an important bench mark market, otherwise) to grow. Move for Reorientation of India Banking System 3.28 In recognition of the need for reviewing the existing structure of Indian banking system, in terms of its size, capacity, ability to meet divergent needs for credit and banking services, access and inclusiveness; the Reserve Bank has initiated a discussion5 on various aspects of intended reorientation of the banking system. The identified building blocks for the revised banking structure in India seek to address issues such as enhancing competition, financing higher growth, providing specialized services, and furthering financial inclusion. The discussion paper also seeks to emphasize the need to address the financial stability concerns arising out of the suggested changes in banking structure. Risk Based Supervision (RBS) for Banks 3.29 Based on the recommendations of the High Level Steering Committee (HLSC), Reserve Bank has finalised a supervisory framework named as SPARC (Supervisory Programme for Assessment of Risk and Capital) under RBS. As part of RBS phase I rollout, 29 banks have been brought under the framework from the financial year 2013. 3.30 The revised framework underscores a comprehensive evaluation of both present and future risks, identification of incipient issues, determination of a supervisory stance based on the evaluation and facilitating timely intervention and corrective action. This would mark a considerable shift from the present CAMELS/ CALCS6 methodology, which is a more compliance-based and transaction testing (point-intime) oriented. The revised supervisory strategy under RBS would be more off-site oriented combined with need based, risk based, focused on site inspections. Central Repository of Large Common Exposures of Banks 3.31 Information asymmetry is a fundamental challenge which affects the debtor-creditor relationship. Debtors are more informed about their financial standing than the creditors who evaluate whether to extend credit to the debtors. In this context, the Reserve Bank initiated a proposal of creating a central repository of large credits to track large common exposures across banks. The database is proposed to be shared with the banks to enable banks themselves to be aware of leverage and common exposures. Accordingly directives were issued to banks on September 11, 2013 under Section 27(2) of the Banking Regulation Act 1949 to operationalise the credit repository of large exposures. 3.32 The information supplied by the banks on their funded and non-funded exposures to large individual/ corporate borrowers (i.e., the borrowers with credit limit of `100 million and above from the banking system) is proposed be used to create the credit registry. The uniqueness of the borrowers is proposed to be captured through the Permanent Account Number (PAN) reported by the banks which will be cross verified from the Income Tax Authority to the extent possible. Borrowers, not having a PAN, will be allotted unique identification number only for the purpose of reporting in the return. Other information to be captured as part of the credit registry include name of the borrower, industry, sector, rating details, facility wise funded and non- funded exposures, limits, etc. An online query module is being offered to the banks, through which they can view any individual large borrower’s asset classification- wise total funded and non- funded exposures to the banking system. The information on large common exposures will be shared with banks only on an aggregate basis without disclosing the names of the banks with which the borrowers have banking relationship. Centralised Database for Corporate Bonds/ Debentures 3.33 Similarly, for the corporate securities markets, while the information in respect of bonds/debentures issued by various issuers is available in a fragmented manner, need was felt for a comprehensive database on corporate bonds. SEBI has initiated action for setting up of ‘Centralised Database for Corporate Bonds/Debentures’ by mandating both the depositories viz. NSDL and CDSL to jointly create, host, maintain and disseminate the centralized database of corporate bonds/debentures. The depositories will obtain requisite information regarding the bonds/ debentures from Issuers, Stock Exchanges, Credit Rating Agencies and Debenture Trustees. All the intermediaries will be required to update the database on ongoing basis, which can be accessed by the public free of charges. Insurance Repository System 3.34 In India risk is not just covered by an individual’s contributions to insurance but also by contributions from employers, banks and cooperative societies, for instance, on behalf of their employees, customers and members, respectively. It becomes difficult for an insured individual (and for the dependents / beneficiaries) to track and list these insurance policies and secure them at a safe and easily retrievable place. Even with the use of technology, visiting multiples offices of the insurance companies or logging requests/ making premium payments through multiple portals of the insurance companies have been posing difficulties to the policyholders. 3.35 The Insurance Regulatory and Development Authority (IRDA) had conceived an initiative to dematerialise the Insurance policies and enable electronic issuance and maintenance of the insurance policies. IRDA has authorised five entities to act as ‘Insurance Repositories’, to enable storage and retrieval of electronic policies. These repositories are otherwise unrelated to Insurance companies and are empowered to meet certain policy servicing requirement. The initiative would enable electronic issuance of insurance policies and it is also possible to convert previously held insurance policies into electronic form through an electronic insurance account (eIA). 3.36 The eIA is offered free of cost to the policyholder and will hold the insurance policies in an electronic form and provides safe custody of insurance policies issued by various Insurance companies. Majority of the service requests can be placed with the Insurance Repositories who will facilitate the delivery of the service by the Insurance companies. The policyholder is relieved from the trouble of visiting offices of multiple insurance companies for the purpose of requests like change of address/nomination etc. The model allows appointment of ‘Approved persons’ who are easily approachable and accessible even to the rural policyholders. The eIA holder can appoint an ‘Authorised representative’ who can operate the account in case of death or disability of the policyholder to facilitate the nominees/assignees in claiming the benefits under the insurance policies. The Insurance Repositories provide a periodic statement to the policyholder with the status of all the insurance policies held under an eIA. 3.37 The initiative of ‘Insurance Repositories’ currently is launched on a pilot basis for life insurance and will soon extend to other lines of business including Annuities, Group and General Insurance policies. Owing to the scale, the Insurance Repositories promise to bring down the cost of policy servicing thus enabling the Insurance companies to achieve efficiencies that possibly reduce the premiums and the turnaround times in delivering services. Progress on LEI System for India 3.38 As reported in the previous FSR, the Reserve Bank had joined the Regulatory Oversight Committee of the global Legal Entity Identifier (LEI) system in January 2013, recognising its importance for the Indian financial system. 3.39 A Steering Committee consisting of representatives from the Reserve Bank, Ministries of Finance and Company Affairs, SEBI and IRDA has been set up to guide the process of implementation of the LEI in India. Regulation and Consumer Protection Regulatory Gaps – Electronic Spot Markets in Commodities 3.40 The recent payment and settlement crisis at the National Spot Exchange limited (NSEL) highlighted, among other things, a gap in the regulation of the commodity spot exchanges in India. Initiatives to launch commodity spot exchanges in India are of relatively recent origin. Setting up of such exchanges was facilitated in the mid-2000s in response to a felt need that a sustained and healthy development of futures market was contingent upon the simultaneous development of the physical or spot market for commodities. In order to provide adequate liquidity on the trading platforms, Government of India permitted the electronic spot exchanges a facility of offsetting (cash settlement) the contracts on the day of entering into contracts, but it also mandated that if the contracts were not offset (cash settled) on the same day, they would have to compulsorily result in delivery of goods. The one-day forward contracts traded on spot exchanges were exempted from the provision of the FCRA, with stiff conditions including a ban on short selling and the launch of longer term contracts. 3.41 Detailed investigations into the various malpractices at NSEL have revealed the need for comprehensively addressing the problems in commodity spot markets in India. The FMC has been brought under the ambit of the Ministry of Finance, Government of India, to ensure better co-ordination among various financial sector regulators. 3.42 The fallout of the events in the NSEL on other exchanges / markets was limited. However, the episode revealed certain systemic concerns with regard to ownership and governance arrangements in exchanges and common ownership of exchanges and existing technology platforms. The episode has emphasized the need for ensuring that no single shareholder or a group of shareholders is permitted to dominate the functioning of the exchange or exercise management control. Frauds and Customer Complaints in Banking System 3.43 While number of fraud cases have shown a decreasing trend from 2009-10 to 2012-13, the total amount involved in cases of frauds has increased substantially over this period (Chart 3.6). 3.44 It is observed that the number of cases of large value frauds (involving amount of `500 Million and above) has increased significantly over the last 3 years from 3 cases in FY 2009-10 to 45 cases during 2012-13, with an even more alarming increase in terms of total amount involved in such cases. The rise in incidences of frauds in large value loan accounts, is a concern and concerted action to improve checks and balances and deterrent action will be required to tackle the problem. 3.45 Online frauds, lottery SMS alerts, advertisements inducing customers to share the details of bank accounts, cloning of cards etc. pose a real challenge for the banks and customers alike in matters of safety and security. Banks need to evolve a comprehensive policy with regard to online banking services, by focusing on compensation, insurance and / or a limited liability clause. 3.46 The Reserve Bank has taken certain measures like introducing compensation for delay in payments of pension. Some other recommendations of the Committee on Customer Service in Banks with regard to payment of pension have also been implemented. The customer complaints redressal system at banks needs strengthening considering their link with operational risk. Rising Trend in Mis-selling in Insurance products 3.47 The previous FSR had raised the risks from mis-selling of insurance products. The complaints under mis-selling have registered a rising trend in recent years (Table 3.1). While mis-selling is not defined in the any of the legislations or regulations governing insurance business, it broadly refers to unfair or fraudulent practices adopted at the time of soliciting and selling insurance policies which have not been sought by the customer or where the customers feel that the policies sold are different from what they wanted or what they were promised. Increasing number of complaints of mis-selling may affect the confidence of general public in insurance products, intermediaries and insurance companies.

3.48 Complaints of mis-selling could impact the continuation of policies affecting the cash flows of insurance companies. More importantly, it seriously affects the demand for insurance which could have serious implications on insurance as an avenue of tapping savings for long term investments for the economy. Regulatory Measures to Check Mis-selling of Insurance Products 3.49 The IRDA (Protection of Policyholders Interests’) Regulation, 2002 provides the framework for protection from mis-selling through the requirements to be met at point of sale, proposal, sale and servicing of insurance products emphasizing on complete disclosures. There is an option of ‘free look cancellation’ within 15 days of receiving the policy document. Misleading publications for soliciting or selling of policies are prohibited under the IRDA (Insurance Advertisements and Disclosure Regulations), 2000. Regulations for licensing of insurance intermediaries like agents, corporate agents and brokers and prescribed code of conduct for their operations are aimed at ensuring that intermediaries do not resort to unfair practices. Guidelines on distance marketing by insurers and intermediaries provide for protection of prospects even if the solicitation or sale is not made in person but through alternate channels like phone, email or internet. Regulations relating to standard proposal form are aimed at better underwriting before sale of policies by analyzing the need of prospect before sale of policies. The improvements in products and disclosures, especially in unit linked policies, are also aimed at providing customers with full information to enable them to make an informed choice. 3.50 IRDA has the power to take regulatory action against insurers and intermediaries which include imposition of fine, issuance of warning, suspension of license and cancellation of license and IRDA has been increasingly using these powers to check mis-selling. Apart from the regulatory framework and powers, the mechanisms for supervision, corporate governance, grievance redressal and consumer education are also aligned to check the unfair business practices like mis-selling. Trends in Pledging of Shares by Promoters 3.51 The pledging of shares by promoters of Indian companies has been an old practice, but earlier the information was not made publicly available. In 2009, SEBI had mandated event based disclosures, which must be made as and when the shares are pledged and periodic disclosures along with quarterly filings with stock exchanges. 3.52 Pledging of shares by promoters is perceived as a significant activity with many implications for risks to the markets, especially when the funding markets face tight conditions. Usually, a high percentage of promoter shareholding is seen as positive since it indicates the faith of the promoters in the business and any dilution in the stake of promoters is perceived as diminishing confidence of promoters. It has been observed that the equity prices of the companies in which the promoters had pledged significant portions of their shares, tend to fall faster than the broader correction in the market. The shares of such companies might have been influenced, apart from other factors, by the risks related to the perceived difficulty in meeting the margin calls triggered by the decrease in the market price of shares. 3.53 Pledging of shares by promoters could pose as a concern in both, falling or rising market scenarios, when large scale pledging of promoter equity could pose concerns for retail investors’ wealth. In a falling market, pledged shares would be under pressure as diminished share prices can turn the collaterals cheaper, prompting lenders to either demand additional margins or sell shares in the open market to protect their interests. Either action could have a cascading impact on stock price, thereby eroding investor’s wealth. The said risk is less in a rising market. In a rising market, the concerns arising out of a downside in collateral value are lesser. However, pledging has a destabilising effect on shareholding pattern. Also, promoters who pledge shares in a rising market could be at a high risk when a bearish trend sets in. 3.54 In an analysis carried out by SEBI, based on Capitaline database, it was observed that in case of 4274 listed companies7, promoters had pledged some or all their shares in those companies. It was seen that out of these, in the case of 286 companies the promoters had pledged more than 50 per cent of their share holding. These 286 companies are grouped into high, medium and low risk categories, based on number of shares pledged by promoters in proportion to the total outstanding shares of the company (Table 3.2). 3.55 The analysis of 202 companies (which were considered as high risk and medium risk companies from the short listed set of 286 companies), after categorising them according to their market capitalisation levels shows that 91 per cent of the high risk and medium risk companies i.e. 183 companies fall under the small cap category and remaining 9 per cent of the high risk and medium risk companies (Table 3.3). Thus a small number of companies under the large cap and mid cap category need to be considered as potential cases for initiating further examination of the trends in pledging of shares by promoters and implications for the wider market. Financial Stability and Development Council 3.56 The Financial Stability and Development Council (FSDC) and its Sub Committee deliberated on various aspects that impinge on financial stability - macroeconomic scenario, both global and domestic and the developments in financial markets. After the publication of the last FSR, the FSDC met once while two meetings of FSDC Sub Committee were held during this period. Some of the other important items taken up for discussion at the FSDC and its Sub Committee include: increased volatility in FX markets and the financing of the current account deficit in the face of sudden reversal of capital flows; the risks to the banking sector on account of deteriorating asset quality; the extra-territorial aspects of regulations by European Securities and Markets Authority (ESMA) and US Commodity Futures Trading Commission (CFTC); trends in bancassurance business with specific reference to single premium policies, etc. In addition, the Sub Committee reviewed issues relating to inter regulatory co-ordination viz., a proposal to facilitate settlement of equity market transactions in central bank money (pursuant to an FSAP recommendation), permitting banks to act as brokers for insurance companies, etc. National Strategy for Financial Education 3.57 The implementation of National Strategy for Financial Education (NSFE) which was prepared under the aegis of the Sub Committee (and was covered in detail in the December 2012 FSR) has commenced. A website for the National Centre for Financial Education8 (which acts as the nodal agency for implementation of NSFE and is supported by all the financial sector regulators) has been launched. Financial inclusion and literacy efforts were further strengthened with initiatives like financial inclusion plans for various segments of the financial sector on the lines of those for banks; nation-wide financial literacy survey; national financial literacy assessment test for students of classes VIII to X; and financial literacy curriculum for schools. Technology and Financial Markets Securing financial transactions in India 3.58 Cyber attacks are being seen as a potentially high risk area with increasing use of Internet Banking, and Mobile Banking for financial transactions (Box 3.1). In view of rising incidents of cyber attacks and implications for financial stability as a whole, there is need for banks to take up protective and proactive measures. Information security awareness among various stakeholders is critical for the banks to secure their information and information infrastructure. Box 3.1: Cyber Security and Cyber Crimes: International Approach The risks of security of the internet and integrity of information and processes in the cyber world have become critical in ensuring a smooth functioning of financial systems, as for other aspects of economic, social and political life. Although, as concluded by some reports9, very few isolated cyber-related events have the capacity to cause a global crisis, there is a need to make detailed assessments of risks and preparations to withstand and recover from a wide range of unwanted cyber events, both accidental and deliberate. The Research Department of the International Organisation of Securities Commission (IOSCO), jointly with the World Federation of Exchanges Office, has conducted a cyber-crime survey10 to bring attention towards the threats from cyber-crimes to some of the most critical financial market infrastructures - the world’s exchanges, from the perspective of securities market. Cyber-crimes can be understood as an attack on the confidentiality, integrity and accessibility of an entity’s online/computer presence or networks – and information contained within. The catastrophic single cyber-related events could include successful attack on one of the underlying technical protocols upon which the Internet depends and a very large-scale solar flare which physically destroys key communications components such as satellites, cellular base stations and switches. The risks from other types of breaches of cyber security such as malware, distributed denial of service, espionage, and the actions of criminals and hackers are expected to be both relatively localised and short-term in impact. The cyber attacks by ‘attack vectors’ which are not reflected in available preventative and detective technologies, with the ability to produce new attack, pose the biggest challenge in this regard. Although, computer systems which are stand-alone or communicate only over proprietary networks are safe from malware, they are still vulnerable to management carelessness and insider threats. In case of cyber space, the defence has to concentrate on resilience – preventive measures plus detailed contingency plans to enable rapid recovery when an attack succeeds as it is often very difficult to identify the actual perpetrator because the computers from which the attack appears to originate will themselves have been taken over and used to relay and magnify the attack commands. It is important to carry out a detailed threat assessment of any specific potential cyber threat based on possible triggering events, likelihood of occurrence, ease of implementation, immediate impact, likely duration, recovery factors etc. As large sections of critical national infrastructure may not be under full and direct government control, there is a need for a clear policy for overall public security and safety from cyber crimes. Apart from the need for action by the government towards having a comprehensive policy framework for national cyber security, spreading awareness, developing forensic resources and research and international cooperation; the respective financial sector regulators and standard setting bodies also need to design, update and implement regulations and standards for security of operations from cyber crimes / attacks, with special emphasis on promoting information sharing. 3.59 Securing electronic transactions through the medium of cards is necessary to ensure confidence and faith in such payments. The Reserve Bank has issued directions to the banks to ensure security of such transactions by mandating an additional factor of authentication for all Card not present transactions (Ecommerce/IVR/Mail Order Telephone Order (MOTO)) and Card present (ATM & POS). The Reserve Bank has also advised the banks to move to EMV Chip & PIN technology for customers who have used their cards at international locations and for issuance of new cards wherein the customer has demanded a card for international usage. Directions have also been given to banks to secure the internet banking transactions and also to provide online alerts to the customers irrespective of the value of transaction for usage of cards at any delivery channel. Cyber Security of India’s FMIs under SEBI 3.60 In the previous FSR it was mentioned that systems and processes instituted at the FMIs have stood them in good stead in the past. However, given the dynamic nature and novelty in data thefts and frauds, FMIs need to constantly upgrade and review their processes and systems to prevent any data theft or security failure. Pursuant to IOSCO Report, the FMIs have reported that they broadly carried out necessary upgradation of their systems and processes. 3.61 In light of the findings of the survey report on “Cyber-Crime, Systemic Risk and Global Securities Markets”, SEBI registered FMIs (exchanges and depositories) acted proactively and already built in reactive and proactive defences along with detection control and disaster recovery to strengthen cyber security in their systems. Payment and Settlement Systems 3.62 The payment and settlement system infrastructure in the country continued to perform without any major disruptions. There were no noteworthy exceptions observed during the Business Continuity Plan / Disaster Recovery (BCP/DR) Drills carried out in July 2013, which covered live operations of Payment and Settlement Systems applications i.e. Real Time Gross Settlement System (RTGS) and Core Banking Solution (CBS) drill. No significant downtime was experienced in the major payment and settlement systems over the last six months, as observed from the DR drills and Vulnerability Assessment and Penetration Testing (VAPT) conducted by 47 Public and Private sector banks for two quarters (April-June 2013 and July-September 2013). Trends in Real Time Gross Settlement System (RTGS) 3.63 The RTGS system was implemented in March 2004 in the country. The new RTGS system with advanced features was operationalised from October 19, 2013. The new RTGS system uses extensible markup language (XML) based messaging system conforming to ISO 20022 standards. A new feature which has been made operational from the day the system went live is the ‘automated gridlock resolution mechanism’. The new RTGS has incorporated some other features with potential for significant improvements in the stability of the system as well as efficiency. Status of compliance with PFMIs 3.64 As part of the Committee on Payment and Settlement Systems (CPSS) and FSB, the Reserve Bank is committed to implement the CPSS-IOSCO “Principles for Financial Market Infrastructure” (PFMIs). A policy document on Regulation and Supervision of Financial Market Infrastructures has been released by Reserve Bank on July 26, 201311. The policy describes in detail the criteria for designating an FMI, applicability of PFMIs to the FMIs, oversight of FMIs, list of FMIs regulated by Reserve Bank and other related aspects. 3.65 An Inter-Agency Implementation Group (IAIG) comprising members from RBI, SEBI, and Forward Markets commission (FMC) has been constituted, on the direction of the FSDC Sub-Committee, for monitoring the implementation of Principles for Financial Market Infrastructures (PFMIs) in India. The Clearing Corporation of India Limited (CCIL) has been identified as an important FMI, under the regulation of the Reserve Bank. Accordingly, the inspection CCIL has been carried out. SEBI has also carried out the assessment of five FMIs under its regulations. The assessment of FMIs done by the respective regulators is being reviewed by the members of the implementation group and the final report will be submitted to the FSDC Sub-Committee. Mobile Banking 3.66 A bank led model for mobile banking has been adopted In India, with only banks which are licensed and supervised in India and having a physical presence in India being permitted to offer mobile banking, with approval from the Reserve Bank. As on date, 78 banks including a few Regional Rural banks (RRBs), Urban Cooperative Banks (UCBs) have been given permission for providing mobile banking services in the country. Helped by the rapid spread of use of mobile telephony, the growth in mobile banking has been encouraging over last three years (Chart 3.7). 3.67 The mobile banking channel has the potential to be one of the key tools for achieving financial inclusion. However, the growth and acceptance of mobile banking as a channel of accessing banking service has been below expectation. Apart from the low levels of awareness and acceptance, the challenges in a faster growth can be attributed to the factors like inability of banks to seed the mobile number with the account number, compatibility of handsets with the mobile banking application, absence of collaboration and revenue sharing models between banks and mobile network operators (MNOs) and inability to get the USD channel in operation for mobile banking etc. Deposit Insurance Single Customer View 3.68 DICGC extends deposit insurance cover to insured banks according to the provisions contained in the DICGC Act, 1961. In the absence of a comprehensive framework for resolution, DICGC is handicapped by inadequate information sharing regarding depositors, thus leading to delay in making payments to the depositors. At the international level, to expedite the claim settlements, a number of countries such as the UK, Canada and Malaysia have mandated banks to capture data on depositor balances in Single Customer View (SCV) format. In case of banks, a Single Customer View is an aggregated, consistent and holistic representation of the data about the depositors. It provides the deposit insurer a consolidated view of all deposit accounts eligible for deposit insurance coverage, enabling it to manage faster, accurate and efficient claim settlement within minimum time period. SCV is heavily dependent on use of technology and in India, presentation of depositor data as required by DICGC poses various challenges. Differential Premium System 3.69 Deposit insurance being a part of safety net mechanism plays a crucial role in maintaining financial stability. A system that differentiates premium on the basis of risk profiles of banks have been increasingly adopted worldwide by various countries as it would enable a deposit insurer perform its role more effectively. Its main objectives are to provide incentives for banks to avoid excessive risk taking and introduce more fairness into the premium assessment process. In Indian context, in order to have a differential premium system based on risk profiles of banks, there is a need to have the risk based ratings of the insured banks. The base for differential premium system may be a combination of both quantitative and qualitative criteria. The system of arriving at the ratings for the banks for this purpose will have to be suitably devised keeping in view the objectives of risk based premium system. 1 Warburton, A. Joseph and Anginer, Deniz and Acharya, Viral V. (2013), “The End of Market Discipline? Investor Expectations of Implicit State Guarantees”, January 1, SSRN: http://ssrn.com/abstract=1961656 or http://dx.doi.org/10.2139/ssrn.1961656. 2 RBI (2013b), “Draft Framework for dealing with Domestic Systemically Important Banks (D-SIBs)”,December 2 (/en/web/rbi/-/notifications/framework-for-dealing-with-domestic-systemically-important-banks-d-sibs-draft-for-comments-226) 3 Investment by banks in liquid/short term debt schemes of mutual funds (/en/web/rbi/-/notifications/investment-by-banks-in-liquid-short-term-debt-schemes-of-mutual-funds-6602) 4 Indranil Chakraborty and R Ayyappan Nair, “Imperfections in Indian fixed-income derivative markets - Plausible rationale”, Unpublished RBI Working Paper 5 RBI (2013a), “Discussion Paper on ‘Banking Structure in India – Way Forward”, September 23 (/en/web/rbi/-/press-releases/rbi-extends-the-date-for-receipt-of-comments-on-the-discussion-paper-on-banking-structure-in-india-the-way-forward-29614) 6 CAMELS (Capital Adequacy, Asset Quality, Management, Earnings, Liquidity, Systems & Controls) approach for domestic banks; CALCS (Capital Adequacy, Asset Quality, Liquidity, Compliance, Systems & Controls) approach for foreign banks 7 Companies which file the share holding pattern details filed by the with the Bombay Stock Exchange (BSE)/ National Stock Exchange (NSE) 9 “Reducing Systemic Cyber-security Risk”: OECD/IFP Project on “Future Global Shocks” By Peter Sommer, Information Systems and Innovation Group, London School of Economics Ian Brown, Oxford Internet Institute, Oxford University 10 Cyber-crime, securities markets and systemic risk: Joint Staff Working Paper of the IOSCO, Research Department and World Federation of Exchanges, Author: Rohini Tendulkar (IOSCO Research Department) Survey: Grégoire Naacke (World Federation of Exchanges Office) and Rohini Tendulkar 11 /en/web/rbi/-/regulation-and-supervision-of-financial-market-infrastructures-regulated-by-rbi-2705 |

||||||||||||||||||||

ਭਾਰਤੀ ਰਿਜ਼ਰਵ ਬੈਂਕ ਮੋਬਾਈਲ ਐਪਲੀਕੇਸ਼ਨ ਇੰਸਟਾਲ ਕਰੋ ਅਤੇ ਨਵੀਨਤਮ ਖਬਰਾਂ ਤੱਕ ਤੇਜ਼ ਐਕਸੈਸ ਪ੍ਰਾਪਤ ਕਰੋ!

ਸਾਡੀ ਐਪ ਇੰਸਟਾਲ ਕਰਨ ਲਈ QR ਕੋਡ ਸਕੈਨ ਕਰੋ।

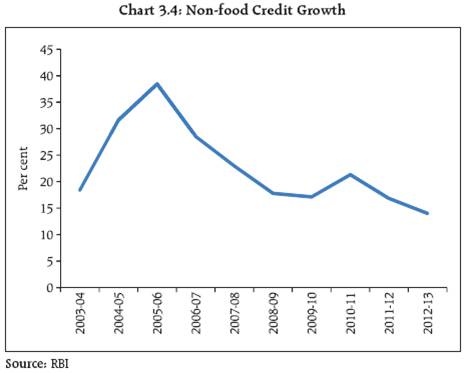

ਪੇਜ ਅੰਤਿਮ ਅੱਪਡੇਟ ਦੀ ਤਾਰੀਖ: