|

The Reserve Bank has been conducting the survey of professional forecasters (SPF) since September 2007. Forty-four panellists participated in the 91st round of the bi-monthly survey conducted during November 2024. The survey results are summarised in terms of their median forecasts and summary statistics are presented in Annexes 1-7.

Highlights:

A. Regular Survey

The results presented in this section are based on the forecasts submitted before the release of the estimates of gross domestic product (GDP) for Q2:2024-25 by the National Statistics Office (NSO) on November 29, 2024 (Friday), after which a quick follow-up survey was conducted among the SPF panellists and they were advised to provide their updated forecasts for annual GDP growth and headline consumer price index (CPI) inflation by December 02, 2024 (Monday). The results of the quick follow-up survey are presented in section B.

1. Output

-

As per the regular survey, real GDP was expected to grow by 6.8 per cent in 2024-25, revised down by 10 basis points (bps) from the previous round. It was expected to grow by 6.6 per cent in 2025-26 (Table 1).

-

SPF panellists placed GDP growth forecasts in the range of 6.1-7.7 per cent for 2024-25 and in the range of 6.0-7.2 per cent for 2025-26 (Annexes 1 and 2).

-

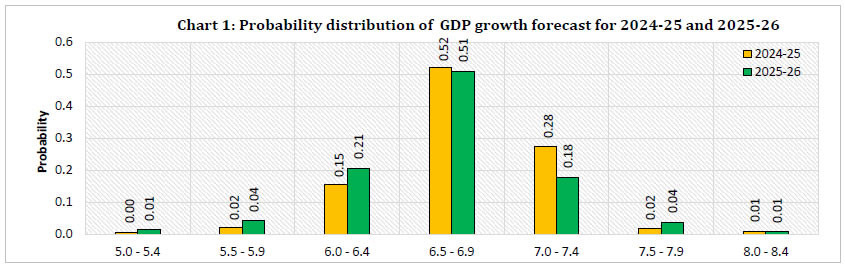

Forecasters had assigned highest probability to real GDP growth in the range of 6.5-6.9 per cent for both 2024-25 and 2025-26 (Chart 1).

Note: Tail parts of the distributions are not presented in this chart but are included in Annex 6.

- Annual growth in real private final consumption expenditure (PFCE) and real gross fixed capital formation (GFCF) for 2024-25 were expected at 6.2 per cent and 7.9 per cent, respectively.

| Table 1: Median Forecast of Growth in GDP, GVA and components |

| (in per cent) |

| |

2024-25 |

2025-26 |

| Real GDP |

6.8

(-0.1) |

6.6

(-0.1) |

| a. Real PFCE |

6.2

(-0.3) |

6.5

(0.0) |

| b. Real GFCF |

7.9

(0.0) |

7.5

(-0.5) |

| Nominal PFCE |

10.1

(0.0) |

10.2

(+0.2) |

| Real GVA |

6.7

(-0.1) |

6.4

(-0.1) |

| a. Agriculture and Allied Activities |

3.7

(-0.2) |

3.4

(-0.1) |

| b. Industry |

6.8

(-0.2) |

6.8

(0.0) |

| c. Services |

7.5

(0.0) |

7.1

(0.0) |

Gross Saving Rate

[per cent of gross national disposable income] |

30.0

(0.0) |

30.3

(0.0) |

Gross Capital Formation Rate

[per cent of GDP at current market prices] |

33.5

(0.0) |

33.5

(0.0) |

| Note: The figures in parentheses indicate the extent of revision in median forecasts (in percentage points) relative to the previous SPF round (applicable for Tables 1-4). |

-

Real gross value added (GVA) growth projection was revised down marginally to 6.7 per cent for 2024-25 and 6.4 per cent for 2025-26.

-

In terms of quarterly path, real GDP growth (y-o-y) was expected at 6.9 per cent during third and fourth quarters of 2024-25 and, subsequently, it was expected to moderate to 6.6-6.7 per cent during Q1 and Q2 of 2025-26 (Table 2).

| Table 2: Median Growth Forecast of Quarterly GDP, GVA and components |

| |

Q2:2024-25 |

Q3:2024-25 |

Q4:2024-25 |

Q1:2025-26 |

Q2:2025-26 |

| Real GDP |

6.6

(-0.4) |

6.9

(0.0) |

6.9

(0.0) |

6.7

(0.0) |

6.6

(0.0) |

| a. Real PFCE |

6.5

(-0.2) |

6.2

(-0.3) |

6.5

(0.0) |

6.3

(-0.2) |

6.3

(-0.2) |

| b. Real GFCF |

7.5

(-0.1) |

8.0

(0.0) |

8.0

(0.0) |

8.0

(0.0) |

7.9

(-0.1) |

| Real GVA |

6.5

(-0.3) |

6.7

(-0.1) |

6.7

(+0.1) |

6.5

(0.0) |

6.4

(0.0) |

2. Inflation

-

As per the regular survey, annual headline inflation, based on CPI-Combined, was expected at 4.8 per cent during 2024-25 and at 4.3 per cent during 2025-26 (Annexes 1 and 2).

-

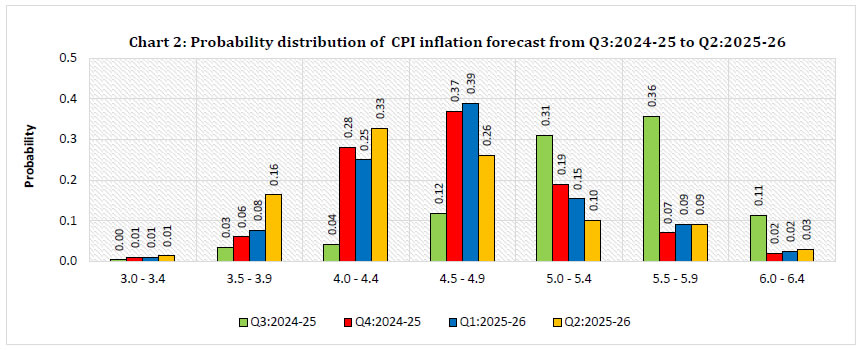

Headline CPI inflation (y-o-y) was expected at 5.5 per cent in Q3:2024-25; it was projected to decrease over the subsequent three quarters to remain between 4.2-4.6 per cent (Table 3).

- CPI inflation, excluding food and beverages, pan, tobacco and intoxicants, and fuel and light, was expected at 3.8 per cent during Q3:2024-25; it was projected to rise successively to 4.2-4.3 per cent in the subsequent three quarters.

| Table 3: Median Forecast of Quarterly Inflation |

| (in per cent) |

| |

Q3:2024-25 |

Q4:2024-25 |

Q1:2025-26 |

Q2:2025-26 |

| CPI Combined (General) |

5.5

(+0.9) |

4.6

(+0.2) |

4.6

(+0.1) |

4.2

(0.0) |

| CPI Combined excluding food and beverages, pan, tobacco and intoxicants and fuel and light |

3.8

(-0.1) |

4.2

(-0.1) |

4.2

(0.0) |

4.3

(0.0) |

| WPI All Commodities |

2.6

(+0.3) |

3.3

(0.0) |

3.0

(+0.4) |

3.3

(+0.2) |

| WPI Non-food Manufactured Products |

0.7

(-0.7) |

2.0

(-0.5) |

1.8

(-0.7) |

2.2

(-0.3) |

Note: Tail parts of the distributions are not presented in this chart but are included in Annex 7.

3. External Sector

-

Merchandise exports and imports were projected to grow by 2.4 per cent and 4.6 per cent, respectively, during 2024-25 and by 5.5 per cent and 6.0 per cent, respectively, during 2025-26, in US dollar terms (Table 4).

-

Current account deficit (CAD) was expected at 1.0 per cent (of GDP at current market prices) for both 2024-25 and 2025-26.

| Table 4: Median Forecast of Select External Sector Variables |

| |

2024-25 |

2025-26 |

Merchandise Exports in US $ terms

(annual growth in per cent) |

2.4

(-1.0) |

5.5

(0.0) |

Merchandise Imports in US $ terms

(annual growth in per cent) |

4.6

(0.0) |

6.0

(+0.1) |

Current Account Balance

(per cent of GDP at current market prices) |

-1.0

(0.0) |

-1.0

(0.0) |

B. Quick Follow-up Survey

-

Twenty-nine panellists responded to the quick follow-up survey2 conducted after the release of the GDP estimates for Q2:2024-25. The median of GDP growth projections of the forecasters who responded to the follow-up survey has been lower by 40 bps and 10 bps for 2024-25 and 2025-26, respectively, relative to their responses in the regular survey round. The median forecast of the annual CPI headline inflation for 2024-25 remained unchanged from the regular survey round but was revised down by 10 bps for 2025-26.

|

The Reserve Bank thanks the following panellists for their participation in this round of the Survey of Professional Forecasters (SPF):

Abhiman Das (Indian Institute of Management Ahmedabad), Aditi Nayar (ICRA Ltd.), Aditya Vyas (STCI Primary Dealer Ltd.), Anuradha Patnaik (University of Mumbai), Barclays Bank PLC, CRISIL Ltd., Debopam Chaudhuri (Piramal Enterprises Ltd.), Devendra Kumar Pant (India Ratings & Research), Garima Kapoor (Elara Securities), Gaura Sen Gupta (IDFC FIRST Bank), Gaurav Kapur (IndusInd Bank Ltd.), ICICI Securities Primary Dealership Ltd., Indranil Pan (Yes Bank Ltd.), Janaki Samant (Centre for Monitoring Indian Economy Pvt. Ltd.), Kanika Pasricha (Union Bank of India), Madhavi Arora (Emkay Global Financial Services Ltd.), Nikhil Gupta (Motilal Oswal Financial Services Ltd.), Rajani Sinha (CareEdge Ratings Ltd.), Shailesh Kejariwal (B&K Securities India Pvt. Ltd.), Shubhada Rao (QuantEco Research), Siddhartha Sanyal (Bandhan Bank), Soumya Kanti Ghosh (State Bank of India), Suvodeep Rakshit (Kotak Securities), Tanvee Gupta Jain (UBS Securities India Private Ltd.), Tirthankar Patnaik (National Stock Exchange), Upasna Bhardwaj (Kotak Mahindra Bank Ltd.), Vikram Chhabra (360 ONE Asset Management) and Vikram Murarka (Kshitij Consultancy Services).

The Bank also acknowledges the contribution of sixteen other SPF panellists, who prefer to remain anonymous.

|

| Annex 1: Annual Forecasts for 2024-25 |

| |

Key Macroeconomic Indicators |

Annual Forecasts for 2024-25 |

| Mean |

Median |

Max |

Min |

1st quartile |

3rd quartile |

| 1 |

GDP at constant (2011-12) prices: Annual Growth (per cent) |

6.8 |

6.8 |

7.7 |

6.1 |

6.7 |

6.9 |

| a |

Private Final Consumption Expenditure (PFCE) at constant (2011-12) prices: Annual Growth (per cent) |

6.1 |

6.2 |

7.3 |

3.5 |

5.6 |

6.9 |

| b |

Gross Fixed Capital Formation (GFCF) at constant (2011-12) prices: Annual Growth (per cent) |

7.8 |

7.9 |

10.3 |

6.1 |

6.9 |

8.5 |

| 2 |

Private Final Consumption Expenditure (PFCE) at current prices: Annual Growth (per cent) |

10.0 |

10.1 |

12.5 |

7.5 |

9.0 |

10.5 |

| 3 |

Gross Capital Formation Rate (per cent of GDP at current market prices) |

33.2 |

33.5 |

36.1 |

29.3 |

33.0 |

33.8 |

| 4 |

GVA at constant (2011-12) prices: Annual Growth (per cent) |

6.7 |

6.7 |

7.1 |

6.2 |

6.6 |

6.8 |

| a |

Agriculture & Allied Activities at constant (2011-12) prices: Annual Growth (per cent) |

3.6 |

3.7 |

5.7 |

1.0 |

3.1 |

4.2 |

| b |

Industry at constant (2011-12) prices: Annual Growth (per cent) |

6.8 |

6.8 |

9.5 |

5.1 |

6.2 |

7.0 |

| c |

Services at constant (2011-12) prices: Annual Growth (per cent) |

7.5 |

7.5 |

8.8 |

6.7 |

7.3 |

7.8 |

| 5 |

Gross Saving Rate (per cent of Gross National Disposable Income) -at current prices |

30.3 |

30.0 |

32.5 |

27.0 |

29.7 |

31.4 |

| 6 |

Fiscal Deficit of Central Govt. (per cent of GDP at current market prices) |

4.9 |

4.9 |

6.5 |

4.6 |

4.8 |

4.9 |

| 7 |

Combined Gross Fiscal Deficit (per cent to GDP at current market prices) |

7.9 |

7.9 |

9.5 |

7.4 |

7.8 |

8.0 |

| 8 |

Bank Credit of Scheduled commercial banks: Annual Growth (per cent) |

13.2 |

13.0 |

20.0 |

10.0 |

12.0 |

13.8 |

| 9 |

Yield on 10-Year G-Sec of Central Govt. (end-period) |

6.7 |

6.7 |

7.1 |

6.3 |

6.6 |

6.8 |

| 10 |

Yield on 91-day T-Bill of Central Govt. (end-period) |

6.4 |

6.4 |

7.0 |

6.2 |

6.3 |

6.5 |

| 11 |

Merchandise Exports (BoP basis in US$ terms): Annual Growth (per cent) |

1.6 |

2.4 |

8.1 |

-7.0 |

0.1 |

3.2 |

| 12 |

Merchandise Imports (BoP basis in US$ terms): Annual Growth (per cent) |

4.0 |

4.6 |

11.6 |

-8.0 |

3.1 |

6.1 |

| 13 |

Current Account Balance in US$ bn. |

-37.1 |

-37.6 |

-19.5 |

-52.0 |

-42.9 |

-32.2 |

| a |

Current Account Balance (per cent to GDP at current market prices) |

-1.0 |

-1.0 |

-0.6 |

-1.8 |

-1.1 |

-0.9 |

| 14 |

Overall BoP in US$ bn. |

38.2 |

38.8 |

77.0 |

-0.5 |

30.0 |

50.0 |

| 15 |

Inflation based on CPI Combined: Headline |

4.8 |

4.8 |

6.0 |

4.0 |

4.7 |

4.9 |

| 16 |

Inflation based on CPI Combined: excluding Food and Beverages, Pan, Tobacco and Intoxicants and Fuel and Light |

3.7 |

3.7 |

5.5 |

3.4 |

3.6 |

3.8 |

| 17 |

Inflation based on WPI: All Commodities |

2.4 |

2.5 |

3.1 |

-1.0 |

2.3 |

2.7 |

| 18 |

Inflation based on WPI: Non-food Manufactured Products |

1.0 |

1.0 |

3.0 |

-1.6 |

0.8 |

1.5 |

| Annex 2: Annual Forecasts for 2025-26 |

| |

Key Macroeconomic Indicators |

Annual Forecasts for 2025-26 |

| Mean |

Median |

Max |

Min |

1st quartile |

3rd quartile |

| 1 |

GDP at constant (2011-12) prices: Annual Growth (per cent) |

6.6 |

6.6 |

7.2 |

6.0 |

6.5 |

6.8 |

| a |

Private Final Consumption Expenditure (PFCE) at constant (2011-12) prices: Annual Growth (per cent) |

6.1 |

6.5 |

7.0 |

4.0 |

5.8 |

6.6 |

| b |

Gross Fixed Capital Formation (GFCF) at constant (2011-12) prices: Annual Growth (per cent) |

7.7 |

7.5 |

9.8 |

5.9 |

7.0 |

8.4 |

| 2 |

Private Final Consumption Expenditure (PFCE) at current prices: Annual Growth (per cent) |

10.1 |

10.2 |

12.8 |

8.0 |

9.4 |

10.7 |

| 3 |

Gross Capital Formation Rate (per cent of GDP at current market prices) |

33.3 |

33.5 |

35.9 |

29.2 |

33.0 |

34.5 |

| 4 |

GVA at constant (2011-12) prices: Annual Growth (per cent) |

6.5 |

6.4 |

7.0 |

6.0 |

6.3 |

6.6 |

| a |

Agriculture & Allied Activities at constant (2011-12) prices: Annual Growth (per cent) |

3.3 |

3.4 |

4.3 |

1.0 |

3.0 |

3.9 |

| b |

Industry at constant (2011-12) prices: Annual Growth (per cent) |

6.8 |

6.8 |

9.5 |

5.5 |

6.3 |

7.0 |

| c |

Services at constant (2011-12) prices: Annual Growth (per cent) |

7.2 |

7.1 |

8.0 |

6.6 |

6.9 |

7.5 |

| 5 |

Gross Saving Rate (per cent of Gross National Disposable Income) -at current prices |

30.6 |

30.3 |

32.5 |

27.0 |

30.0 |

31.9 |

| 6 |

Fiscal Deficit of Central Govt. (per cent of GDP at current market prices) |

4.6 |

4.5 |

6.3 |

4.4 |

4.5 |

4.5 |

| 7 |

Combined Gross Fiscal Deficit (per cent to GDP at current market prices) |

7.5 |

7.4 |

9.0 |

7.0 |

7.2 |

7.5 |

| 8 |

Bank Credit of Scheduled commercial banks: Annual Growth (per cent) |

12.8 |

12.4 |

19.0 |

9.9 |

12.0 |

13.6 |

| 9 |

Yield on 10-Year G-Sec of Central Govt. (end-period) |

6.5 |

6.5 |

7.0 |

6.1 |

6.4 |

6.6 |

| 10 |

Yield on 91-day T-Bill of Central Govt. (end-period) |

6.2 |

6.1 |

7.0 |

5.8 |

6.0 |

6.3 |

| 11 |

Merchandise Exports (BoP basis in US$ terms): Annual Growth (per cent) |

4.6 |

5.5 |

13.3 |

-4.0 |

3.0 |

6.8 |

| 12 |

Merchandise Imports (BoP basis in US$ terms): Annual Growth (per cent) |

4.7 |

6.0 |

8.8 |

-5.1 |

3.2 |

8.1 |

| 13 |

Current Account Balance in US$ bn. |

-38.5 |

-41.7 |

-7.0 |

-59.4 |

-49.5 |

-33.2 |

| a |

Current Account Balance (per cent to GDP at current market prices) |

-1.0 |

-1.0 |

-0.2 |

-2.1 |

-1.2 |

-0.8 |

| 14 |

Overall BoP in US$ bn. |

42.2 |

37.7 |

92.0 |

-2.0 |

28.2 |

60.0 |

| 15 |

Inflation based on CPI Combined: Headline |

4.4 |

4.3 |

6.2 |

3.7 |

4.2 |

4.5 |

| 16 |

Inflation based on CPI Combined: excluding Food and Beverages, Pan, Tobacco and Intoxicants and Fuel and Light |

4.3 |

4.3 |

5.5 |

3.5 |

4.0 |

4.5 |

| 17 |

Inflation based on WPI: All Commodities |

3.0 |

3.5 |

4.5 |

-1.5 |

2.6 |

4.0 |

| 18 |

Inflation based on WPI: Non-food Manufactured Products |

2.1 |

2.5 |

4.0 |

-2.5 |

1.5 |

3.3 |

| Annex 3: Quarterly Forecasts from Q2:2024-25 to Q2:2025-26 |

| |

Key Macroeconomic Indicators |

Quarterly Forecasts |

| Q2: 2024-25 |

Q3: 2024-25 |

Q4: 2024-25 |

| Mean |

Median |

Max |

Min |

Mean |

Median |

Max |

Min |

Mean |

Median |

Max |

Min |

| 1 |

GDP at constant (2011-12) prices: Annual Growth (per cent) |

6.6 |

6.6 |

7.5 |

6.0 |

6.9 |

6.9 |

8.3 |

5.6 |

6.8 |

6.9 |

7.4 |

5.4 |

| a |

Private Final Consumption Expenditure (PFCE) at constant (2011-12) prices: Annual Growth (per cent) |

6.1 |

6.5 |

7.5 |

3.0 |

6.1 |

6.2 |

8.0 |

4.1 |

6.3 |

6.5 |

8.5 |

4.6 |

| b |

Gross Fixed Capital Formation (GFCF) at constant (2011-12) prices: Annual Growth (per cent) |

7.5 |

7.5 |

15.5 |

3.8 |

8.4 |

8.0 |

12.5 |

5.8 |

8.3 |

8.0 |

14.8 |

5.5 |

| 2 |

Private Final Consumption Expenditure (PFCE) at current prices: Annual Growth (per cent) |

10.1 |

9.6 |

13.0 |

8.2 |

10.0 |

10.2 |

12.6 |

7.1 |

10.4 |

10.8 |

12.7 |

7.6 |

| 3 |

Gross Fixed Capital Formation (GFCF) Rate (per cent of GDP at current market prices) |

31.8 |

31.7 |

35.4 |

28.6 |

30.7 |

30.6 |

33.8 |

28.5 |

32.0 |

31.6 |

36.0 |

28.8 |

| 4 |

GVA at constant (2011-12) prices: Annual Growth (per cent) |

6.5 |

6.5 |

7.1 |

6.0 |

6.7 |

6.7 |

7.5 |

6.0 |

6.7 |

6.7 |

7.4 |

5.7 |

| a |

Agriculture & Allied Activities at constant (2011-12) prices: Annual Growth (per cent) |

3.5 |

3.2 |

5.6 |

1.5 |

4.2 |

4.2 |

6.1 |

1.0 |

3.8 |

3.8 |

6.0 |

-1.5 |

| b |

Industry at constant (2011-12) prices: Annual Growth (per cent) |

5.5 |

5.5 |

8.0 |

2.2 |

6.8 |

6.9 |

9.0 |

4.7 |

6.5 |

6.4 |

9.6 |

3.4 |

| c |

Services at constant (2011-12) prices: Annual Growth (per cent) |

7.5 |

7.4 |

8.6 |

6.5 |

7.4 |

7.5 |

9.1 |

6.5 |

7.5 |

7.5 |

11.0 |

5.9 |

| 5 |

IIP (2011-12=100): Quarterly Average Growth (per cent) |

- |

- |

- |

- |

5.0 |

4.8 |

6.9 |

3.1 |

5.1 |

5.2 |

7.0 |

2.5 |

| 6 |

Merchandise Exports -BoP basis (in US$ bn.) |

104.7 |

104.1 |

110.2 |

95.4 |

111.9 |

112.5 |

117.2 |

104.5 |

119.8 |

122.0 |

129.0 |

98.5 |

| 7 |

Merchandise Imports -BoP basis (in US$ bn.) |

176.9 |

178.6 |

184.4 |

148.1 |

180.6 |

183.8 |

193.6 |

158.7 |

178.3 |

178.1 |

197.2 |

153.5 |

| 8 |

Rupee per US $ Exchange rate (end-period) |

83.8 |

83.8 |

83.8 |

83.7 |

84.3 |

84.4 |

85.0 |

81.0 |

84.4 |

84.5 |

85.5 |

78.5 |

| 9 |

Crude Oil (Indian basket) price (US $ per barrel) (end-period) |

- |

- |

- |

- |

73.9 |

74.4 |

87.0 |

70.0 |

73.8 |

73.1 |

89.0 |

65.0 |

| 10 |

Policy Repo Rate (end-period) |

- |

- |

- |

- |

6.44 |

6.50 |

6.50 |

6.00 |

6.26 |

6.25 |

6.50 |

5.50 |

| |

Key Macroeconomic Indicators |

Quarterly Forecasts |

| Q1: 2025-26 |

Q2: 2025-26 |

| Mean |

Median |

Max |

Min |

Mean |

Median |

Max |

Min |

| 1 |

GDP at constant (2011-12) prices: Annual Growth (per cent) |

6.7 |

6.7 |

8.5 |

6.0 |

6.6 |

6.6 |

7.5 |

6.0 |

| a |

Private Final Consumption Expenditure (PFCE) at constant (2011-12) prices: Annual Growth (per cent) |

6.1 |

6.3 |

7.5 |

4.5 |

6.2 |

6.3 |

7.0 |

4.3 |

| b |

Gross Fixed Capital Formation (GFCF) at constant (2011-12) prices: Annual Growth (per cent) |

7.9 |

8.0 |

10.2 |

5.3 |

8.2 |

7.9 |

14.5 |

5.6 |

| 2 |

Private Final Consumption Expenditure (PFCE) at current prices: Annual Growth (per cent) |

10.4 |

10.4 |

13.9 |

8.0 |

10.4 |

10.7 |

13.3 |

7.5 |

| 3 |

Gross Fixed Capital Formation (GFCF) Rate (per cent of GDP at current market prices) |

31.7 |

31.7 |

35.3 |

29.7 |

32.2 |

31.9 |

37.6 |

28.6 |

| 4 |

GVA at constant (2011-12) prices: Annual Growth (per cent) |

6.5 |

6.5 |

7.3 |

5.5 |

6.5 |

6.4 |

7.1 |

5.8 |

| a |

Agriculture & Allied Activities at constant (2011-12) prices: Annual Growth (per cent) |

3.4 |

3.5 |

5.0 |

1.0 |

3.1 |

3.3 |

4.1 |

1.5 |

| b |

Industry at constant (2011-12) prices: Annual Growth (per cent) |

6.6 |

6.6 |

9.0 |

5.3 |

6.5 |

6.3 |

9.0 |

4.6 |

| c |

Services at constant (2011-12) prices: Annual Growth (per cent) |

7.2 |

7.2 |

7.9 |

5.9 |

7.2 |

7.1 |

8.1 |

6.5 |

| 5 |

IIP (2011-12=100): Quarterly Average Growth (per cent) |

5.1 |

5.2 |

5.9 |

3.8 |

5.5 |

5.0 |

9.1 |

3.6 |

| 6 |

Merchandise Exports -BoP basis (in US$ bn.) |

115.6 |

116.5 |

122.0 |

110.0 |

113.7 |

113.5 |

122.0 |

109.5 |

| 7 |

Merchandise Imports -BoP basis (in US$ bn.) |

179.2 |

179.7 |

190.4 |

167.1 |

181.9 |

188.1 |

197.4 |

145.0 |

| 8 |

Rupee per US $ Exchange rate (end-period) |

84.5 |

84.7 |

86.0 |

78.0 |

84.6 |

84.8 |

86.5 |

78.0 |

| 9 |

Crude Oil (Indian basket) price (US $ per barrel) (end-period) |

72.6 |

72.5 |

92.0 |

60.0 |

72.5 |

72.0 |

95.0 |

60.0 |

| 10 |

Policy Repo Rate (end-period) |

6.00 |

6.00 |

6.50 |

5.25 |

5.88 |

6.00 |

6.25 |

5.00 |

| Annex 4: Forecasts of CPI Combined Inflation |

| (per cent) |

| |

CPI Combined (General) |

CPI Combined excluding Food and Beverages, Pan, Tobacco and Intoxicants and Fuel and Light |

| Mean |

Median |

Max |

Min |

Mean |

Median |

Max |

Min |

| Q3:2024-25 |

5.4 |

5.5 |

6.3 |

4.4 |

3.8 |

3.8 |

4.2 |

3.5 |

| Q4:2024-25 |

4.7 |

4.6 |

6.3 |

4.0 |

4.1 |

4.2 |

4.6 |

3.5 |

| Q1:2025-26 |

4.7 |

4.6 |

6.1 |

3.7 |

4.2 |

4.2 |

5.0 |

3.1 |

| Q2:2025-26 |

4.4 |

4.2 |

6.3 |

3.6 |

4.2 |

4.3 |

5.0 |

3.1 |

| Annex 5: Forecasts of WPI Inflation |

| (per cent) |

| |

WPI All Commodities |

WPI Non-food Manufactured Products |

| Mean |

Median |

Max |

Min |

Mean |

Median |

Max |

Min |

| Q3:2024-25 |

2.5 |

2.6 |

3.5 |

1.1 |

0.9 |

0.7 |

2.5 |

-0.8 |

| Q4:2024-25 |

3.2 |

3.3 |

5.1 |

-0.5 |

1.9 |

2.0 |

3.8 |

-0.8 |

| Q1:2025-26 |

2.7 |

3.0 |

4.2 |

-0.5 |

1.7 |

1.8 |

3.0 |

-0.8 |

| Q2:2025-26 |

3.2 |

3.3 |

5.0 |

0.3 |

2.2 |

2.2 |

3.8 |

0.5 |

| Annex 6: Mean probabilities attached to possible outcomes of Real GDP growth |

| Growth Range |

Forecasts for 2024-25 |

Forecasts for 2025-26 |

| 12.0 per cent or more |

0.00 |

0.00 |

| 11.5 to 11.9 per cent |

0.00 |

0.00 |

| 11.0 to 11.4 per cent |

0.00 |

0.00 |

| 10.5 to 10.9 per cent |

0.00 |

0.00 |

| 10.0 to 10.4 per cent |

0.00 |

0.00 |

| 9.5 to 9.9 per cent |

0.00 |

0.00 |

| 9.0 to 9.4 per cent |

0.00 |

0.00 |

| 8.5 to 8.9 per cent |

0.00 |

0.00 |

| 8.0 to 8.4 per cent |

0.01 |

0.01 |

| 7.5 to 7.9 per cent |

0.02 |

0.04 |

| 7.0 to 7.4 per cent |

0.28 |

0.18 |

| 6.5 to 6.9 per cent |

0.52 |

0.51 |

| 6.0 to 6.4 per cent |

0.15 |

0.21 |

| 5.5 to 5.9 per cent |

0.02 |

0.04 |

| 5.0 to 5.4 per cent |

0.00 |

0.01 |

| 4.5 to 4.9 per cent |

0.00 |

0.01 |

| 4.0 to 4.4 per cent |

0.00 |

0.00 |

| 3.5 to 3.9 per cent |

0.00 |

0.00 |

| 3.0 to 3.4 per cent |

0.00 |

0.00 |

| 2.5 to 2.9 per cent |

0.00 |

0.00 |

| 2.0 to 2.4 per cent |

0.00 |

0.00 |

| 1.5 to 1.9 per cent |

0.00 |

0.00 |

| 1.0 to 1.4 per cent |

0.00 |

0.00 |

| 0.5 to 0.9 per cent |

0.00 |

0.00 |

| 0.0 to 0.4 per cent |

0.00 |

0.00 |

| below 0.0 per cent |

0.00 |

0.00 |

| Note: The sum of the probabilities may not add up to one due to rounding off. |

| Annex 7: Mean probabilities attached to possible outcomes of CPI (Combined) inflation |

| Inflation Range |

Forecasts for Q3:2024-25 |

Forecasts for Q4:2024-25 |

Forecasts for Q1:2025-26 |

Forecasts for Q2:2025-26 |

| 9.0 per cent or above |

0.00 |

0.00 |

0.00 |

0.00 |

| 8.5 to 9.0 per cent |

0.00 |

0.00 |

0.00 |

0.00 |

| 8.0 to 8.4 per cent |

0.00 |

0.00 |

0.00 |

0.00 |

| 7.5 to 7.9 per cent |

0.00 |

0.00 |

0.00 |

0.00 |

| 7.0 to 7.4 per cent |

0.00 |

0.00 |

0.00 |

0.00 |

| 6.5 to 6.9 per cent |

0.02 |

0.00 |

0.00 |

0.00 |

| 6.0 to 6.4 per cent |

0.11 |

0.02 |

0.02 |

0.03 |

| 5.5 to 5.9 per cent |

0.36 |

0.07 |

0.09 |

0.09 |

| 5.0 to 5.4 per cent |

0.31 |

0.19 |

0.15 |

0.10 |

| 4.5 to 4.9 per cent |

0.12 |

0.37 |

0.39 |

0.26 |

| 4.0 to 4.4 per cent |

0.04 |

0.28 |

0.25 |

0.33 |

| 3.5 to 3.9 per cent |

0.03 |

0.06 |

0.08 |

0.16 |

| 3.0 to 3.4 per cent |

0.00 |

0.01 |

0.01 |

0.01 |

| 2.5 to 2.9 per cent |

0.00 |

0.00 |

0.00 |

0.01 |

| 2.0 to 2.4 per cent |

0.00 |

0.00 |

0.00 |

0.00 |

| 1.5 to 1.9 per cent |

0.00 |

0.00 |

0.00 |

0.00 |

| 1.0 to 1.4 per cent |

0.00 |

0.00 |

0.00 |

0.00 |

| 0.5 to 0.9 per cent |

0.00 |

0.00 |

0.00 |

0.00 |

| 0.0 to 0.4 per cent |

0.00 |

0.00 |

0.00 |

0.00 |

| -0.5 to -0.1 per cent |

0.00 |

0.00 |

0.00 |

0.00 |

| -1.0 to -0.6 per cent |

0.00 |

0.00 |

0.00 |

0.00 |

| Below -1.0 per cent |

0.00 |

0.00 |

0.00 |

0.00 |

| Note: The sum of the probabilities may not add up to one due to rounding off. |

Note: CPI: Consumer Price Index; GDP: Gross Domestic Products; GFCF: Gross Fixed Capital Formation; GVA: Gross Value Added; IIP: Index of Industrial Production; PFCE: Private Final Consumption Expenditure; WPI: Wholesale Price Index.

|

IST,

IST,