IST,

IST,

INDIA@75 - Speech delivered by Dr. Michael Debabrata Patra, Deputy Governor, Reserve Bank of India in an event to celebrate Azadi Ka Amrit Mohotsav organised by Reserve Bank of India - August 13, 2022, Bhubaneswar

Dr. Michael Debabrata Patra, Deputy Governor, Reserve Bank of India

delivered-on ਅਗ 13, 2022

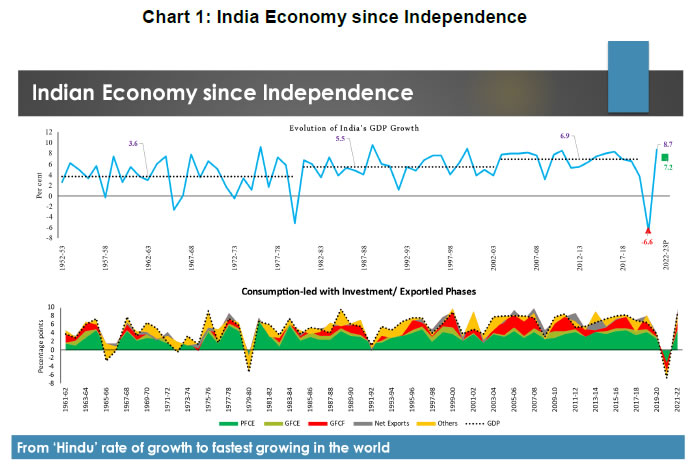

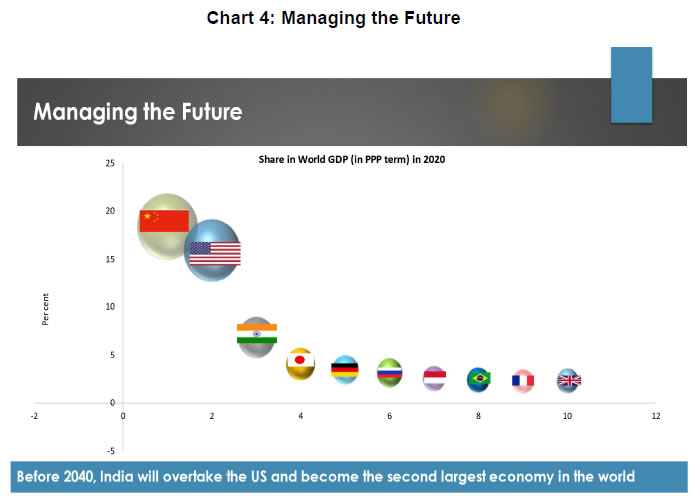

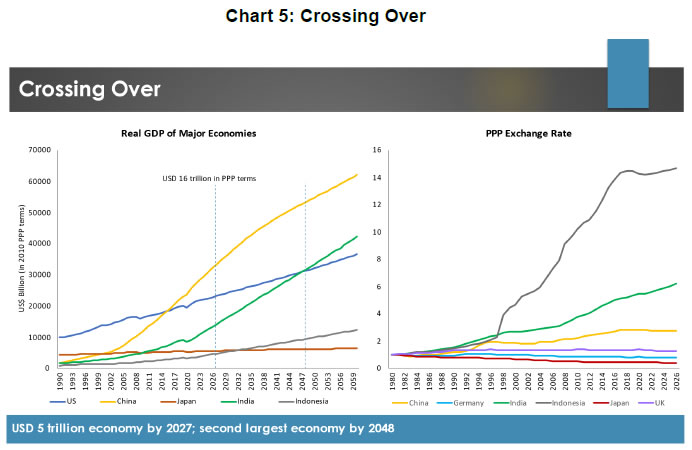

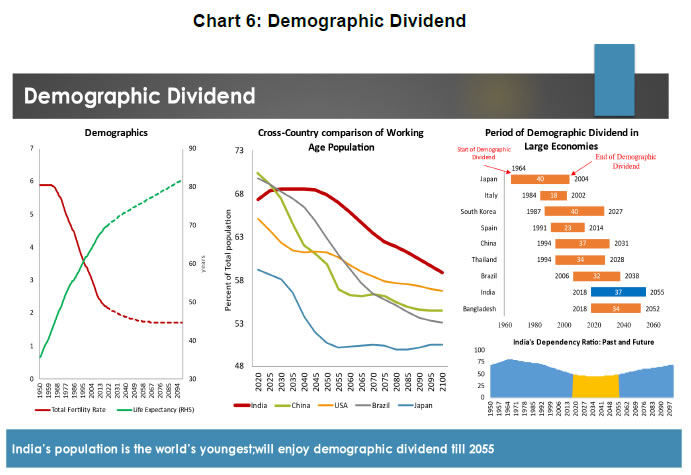

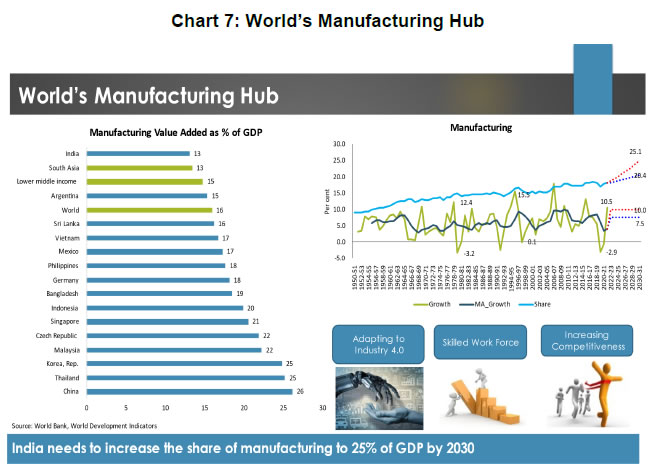

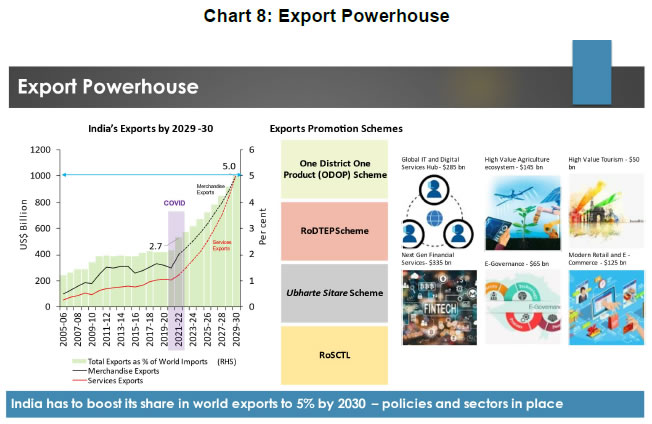

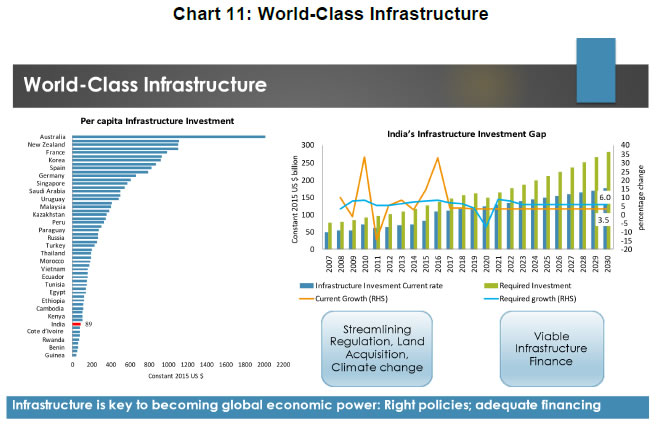

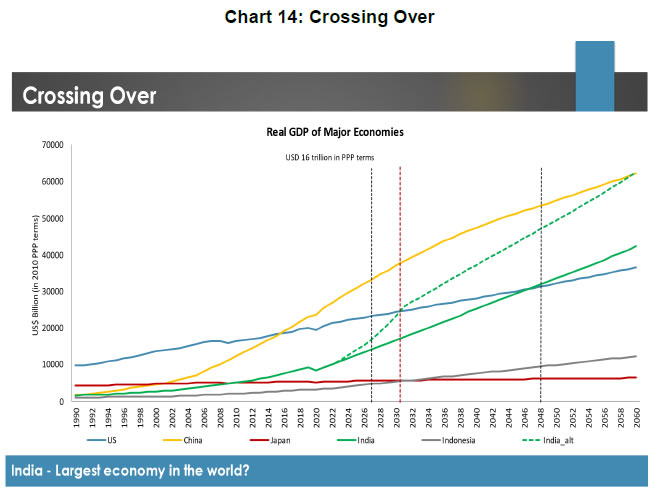

Dr. Hrudananda Panda, Regional Director, Reserve Bank of India (RBI), Bhubaneswar, distinguished guests of the RBI from the Government of Odisha, academia, banks, financial institutions, industry associations, the media, scholars and students, my colleagues from the RBI, Ladies and Gentlemen, I am deeply honoured to be invited to deliver this address as part of the celebration of the 75th year of our Independence. I thank Dr. Panda for inviting me and more than that, for the innovative drive and gracious hospitality – he and his team – which has made this event possible. At this defining moment, the elixir of energy, inspiration, new ideas and pledges awakens us to a bright and self-reliant future, marked by the fulfilment of our dreams. In many ways, Bhubaneshwar is the embodiment of this Mahotsav – a rich and glorious heritage; a happening present; and a smart city of the future – in every respect, Tribhuvan. While my talk will attempt to kaleidoscope India’s journey through the last 75 years, the focus is on the future – India in the next 10-50 years. It is said that there is nothing more powerful than an idea whose time has come2. I do believe with the all the strength of my conviction that India’s time has come. As the famous song marking the UN’s International Day of Peace goes3, you may say I am a dreamer, but I hope that after my talk, I will not be the only one. You too will dream with me, and the world will be as one. So, I invite you to join me in this journey of dreams as India takes off to make a tryst with destiny. India at Take-off It is said that if the history of the universe can be compared to a journey of a 100 km, it will not be until the 71st km or a little later that one will encounter life, and the entire period of human existence comprises the last 1-2 metres. Seen against this humbling perspective, independent India’s journey of 75 years has been quite astonishing. Between 2006 and just before the COVID-19 pandemic struck, more than 300 million people in India have been lifted out of poverty, the highest rate of poverty reduction anywhere in the world. The Indian economy is a world leader in the production of various agricultural commodities. In 2021, India has emerged as the world’s Number 1 rice exporter, with more than the combined exports of world Numbers 2 and 3. India has one of the widest manufacturing bases among emerging economies, ranging from the largest producer and exporter of tractors and two wheelers to among the top 10 exporters of smartphones, cars and spacecraft. In several services, including shipping personnel and information technology (IT), India is a world leader. In the case of IT, India has come to be known as the back office of the world. A widely used indicator of economic progress of a country is the growth of gross domestic product, which is the value of all the final goods and services produced in an economy during say a quarter or a year. If one looks back over the last 75 years, statistical tests (Bai-Perron structural break tests) reveal that India’s growth trajectory has gone through three phases. Up to the 1970s, India averaged GDP growth of 3.6 per cent – the so called Hindu rate of growth – which has been associated with inward-looking policies adopted over that period. Growth picked up to 5.5 per cent during 1980 - 2002 as liberalisation, opening up and an outward orientation commenced. Thereafter, GDP growth rose to an average of about 7 per cent till the pandemic arrived. In 2020-21, GDP declined by 6.6 per cent due to the pandemic. In 2021-22, it recovered to 8.7 per cent, taking GDP 1.5 per cent above its pre-pandemic level. For the current financial year, i.e., 2022-23, the RBI has projected GDP to grow by 7.2 per cent, which places India among the fastest growing economies of the world. What are the drivers of India’s growth? It turns out that the Indian economy is powered by “We”, the people – private final consumption expenditure (PFCE) comprising households’ spending on goods, services, rents, insurance, pension contributions and such other expenses that correspond with daily livelihood. Private consumption constitutes 55 per cent of GDP, although this share has come down from above 75 per cent in the 1960s. There have been phases of export-led and investment-led growth, which could not be sustained, but they did provide turning points in the growth path. In particular, investment, which is the production of goods that, in turn, produce other goods is seen as India’s game changer, as for most developing countries that are capital scarce. The investment rate (total investment/GDP) is widely regarded as the most important lever of growth in India. A striking feature in India is that our growth is home financed – investment is financed primarily by domestic savings, with foreign savings playing only a supplemental role. Another noteworthy feature is that the saving rate has started slowing down since 2007-08 after the global financial crisis. Eventually, this pulled down the investment rate which has exhibited deceleration since 2012-13. Reversing this trend is critical to achieve higher growth. The current account deficit (CAD) in the country’s balance of payments (BoP) determines how much of foreign savings or net capital inflows into the country can be absorbed or used for growth. Exports earn foreign exchange while imports have to be paid for in foreign exchange. A country like India relies on the rest of the world for imports of items we don’t produce such as crude oil and items such as machinery, equipment and technology in which other nations either have a comparative advantage or they closely hold. For India, imports typically exceed exports and hence earnings of foreign exchange are not sufficient for covering import payments. The gap has to be filled by borrowing from abroad which, however, has to be serviced through principal and interest payments. If debt servicing exceeds our earnings, we have to either reduce imports and stifle our growth prospects or default on debt payments and face international isolation. Our experience has been that India can sustain a current account deficit of 2.5-3.0 per cent without getting into an external sector crisis. In fact, in a telling reminder of this fact, a record increase in oil prices and high gold imports took the current account deficit above this Plimsoll line and to historically high levels during 2011-13. When the US Federal Reserve contemplated the end of easy monetary policy in the summer of 2013, India faced the taper tantrum and was labelled as among the fragile five4. A Cross-Country Perspective Stepping back a little, it is useful to observe India’s progress in a cross-country setting. Let me turn to the rise and fall of the top ten economies of the world since the early 1960s when developing countries in Asia started to put in place strategies for take-off after two centuries of western dominance. Noteworthy is the age of Japan which started in the 1960s and lasted through 1970s and 1980s. The age of China began in the early 1990s, taking it to the position of the second largest economy of the world. It is from 2015 that India’s time seems to be arriving. Today, India is the world’s sixth largest economy in terms of market exchange rates. For the year 2022, the International Monetary Fund (IMF) projects global growth at 3.2 per cent in 2022, lower than 6.1 per cent in 2021. India is projected to grow by 7.4 per cent in 2022. In spite of the pandemic and the war in Europe, India is going to contribute about 14 per cent of global growth. In fact, India is likely to be the second most important driver of global growth in 2022 after China. The use of market exchange rates for cross-comparisons of economic performance measured by GDP has been questioned. After all, exchange rates are subjected to bouts of volatility and idiosyncratic behaviour that makes them diverge from reality. An alternative measure is purchasing power parity. It is the price of an average basket of goods and services that a household needs for livelihood in each country. An often used example is the McDonald’s burger which is supposed to have the same wheat, potatoes and other ingredients in every outlet in every country. To show you how this works, with the money paid in the US for a big Mac, one can buy 2.5 Macs in India. So, what does this tell us about the exchange rate and GDP? Currently, India is the third largest economy in the world in terms of purchasing power parity (PPP) terms, with a share of 7 per cent of global GDP [after China (18 per cent) and the US (16 per cent)]. India’s GDP in market exchange rates is expected to reach US$ 5 trillion by 2027. By that year, India’s GDP in purchasing power parity terms will exceed US$ 16 trillion (up from US $ 10 trillion in 2021). The OECD’s 2021 calculations indicate that the Indian economy will be overtake the US by 2048. This would make India the largest economy in the world after China. In terms of PPP, the exchange rate appreciates with the prosperity of a nation and a rise in its productivity. The Indonesian Rupiah is set to become the strongest currency in the world, with the Indian Rupee emerging as the second strongest currency. The Window of Opportunity With this bird’s eye image of where India is today, I will turn to the four engines that can power India to achieve escape velocity from the emerging economy orbit and take off towards becoming an economic superpower. (i) Demographics I will start with the underlying realities of the widely cited demographic dividend. The world’s population growth fell below 1 per cent for the first time in 2021. It will slow down through the rest of this century. India’s population at 1.38 billion is the world’s youngest at 28.4 years. By 2023 (that is next year), India will be the most populous country in the world (1.43 billion)5. Aging will close India’s youth dividend by 2045, as it did for Japan in 2004 and Italy in 2002. This is evident from the changing structure of the population. A key indicator is the total fertility rate – the average number of children born to a woman over her lifetime. As per the findings of India’s latest National Family Health Survey (2019-21), the total fertility rate (TFR) of 2.0 (down from 2.2 in 2015-16 and 2.7 in 2005-06) has fallen below the replacement level for the first time. According to the United Nations (UN), a generation with a total fertility rate6 lower than 2.1 is not producing enough children to replace itself. Such a situation results in an outright reduction in the population of that country. On the other hand, the life expectancy of Indians has been rising and is likely to increase from the current level of about 70 years to about 82 years by 2099. A comparison of the ratio India’s working-age7 population (WAP) to the total population with that of other countries, viz., China, Brazil, USA, and Japan, shows that India stands at an advantageous position. The working-age populations of these countries have started declining already while India's WAP ratio will increase till 2045, even exceeding that of China by 2030. Making the most of this demographic dividend is India’s opportunity as well as a challenge. (ii) Manufacturing Another engine for take-off is manufacturing. India’s development experience has been widely regarded as remarkable because it broke away from the usual path of a country moving from primary activities to secondary and then to tertiary activities8. India leapfrogged the secondary phase and progressed from primary activities to the tertiary sector. Services account for two-thirds of India’s economy today. In hindsight, the Indian experience may not have been the miracle it is credited to be – India failed to absorb into gainful employment large masses of its less-skilled labour force that migrated from agriculture. Apart from this labour absorptive capacity, the manufacturing sector has backward and forward linkages with other sectors of the economy. A robust growth of manufacturing is essential for boosting India’s exports. Hence it is necessary to overturn the conventional wisdom and catch up with other leading manufacturers of the world. According to the World Bank, India’s manufacturing sector as a proportion to GDP (in constant 2015 US dollar terms) remains much below the world average as well as most peers. The growth of Indian manufacturing has been quite volatile, ranging between a peak of 17.8 per cent (2006-07) and a trough of -3.2 per cent (1979-80). Since the 1990s, the average growth of manufacturing has been 7.0-7.5 per cent. If 7.5 per cent growth is attained in the next decade, manufacturing would reach a share of 20.4 per cent of overall gross value added (GVA) by 2030-31. If manufacturing were to grow at 10 per cent – the target set by the ‘Make in India’ campaign – its share would reach 25 per cent in 2030-31. India would become the manufacturing shop floor of the world with positive effects for employment and other sectors of the economy. To achieve this, three things are essential. First, the manufacturing sector must adapt to the fourth industrial revolution (automation; data exchange; cyber-physical systems; the internet of things; cloud computing; cognitive computing; the smart factory; and advanced robotics)9. Second, India must develop a skilled labour force by stepping up investment in human capital. Third, efforts must be directed to boost international competitiveness that allows manufacturing to find expression in global markets. India must raise the share of manufacturing to at least 25 per cent of GDP to become a global manufacturing hub. (iii) Exports Exports provide an avenue for the widening of markets and production capabilities beyond national borders. Currently, India’s exports of goods and services at close to US $ 800 billion constitute 2.7 per cent of the world total. The Government of India has set a target of US $ 1 trillion to be achieved by 2030. This would take India’s share to 5 per cent of the global total and India would become an export powerhouse. Several initiatives are in place to actualise this goal:

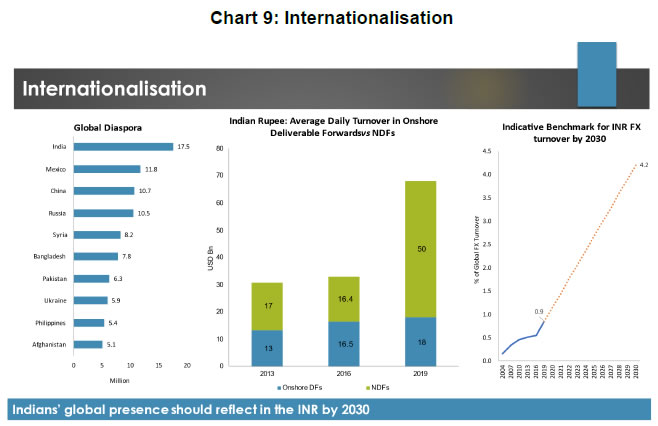

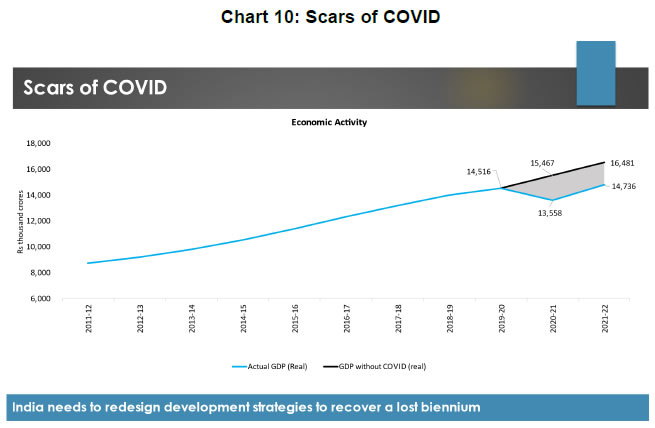

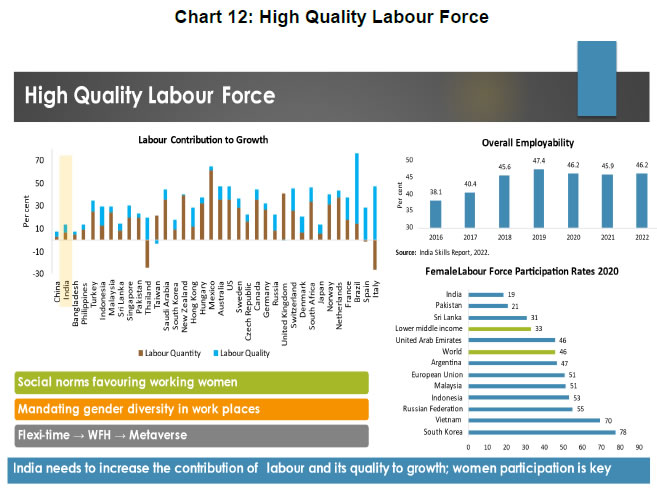

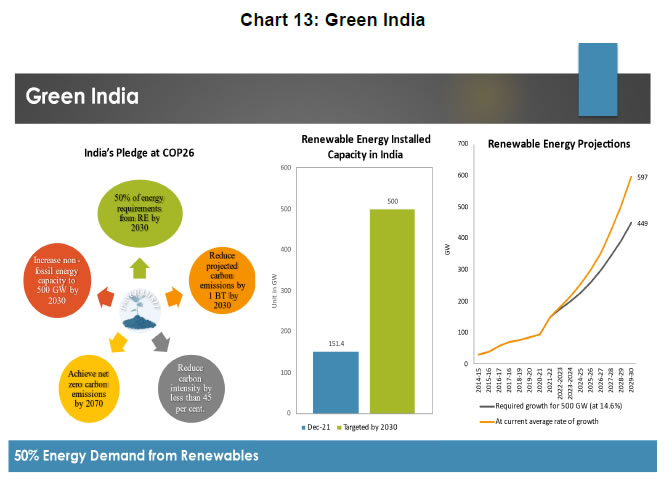

Raising India’s share in world exports to at least 5 per cent is within reach. (iv) Internationalisation Indians are among the most internationalised people in the world. The Indian diaspora is the biggest in the world and India is the top recipient of remittances. The Indian rupee trades three times more offshore than onshore. Yet we still talk of internationalisation as if it is a last frontier. The economist Niall Ferguson writes that in human history, there have been 70 empires. The 69th and 70th empires are the People’s Republic of China and the European Union, respectively. The 68th empire has all the attributes of an empire, including waging wars beyond its borders. Yet it is different in one fundamental way – it does not annex foreign lands. Ferguson calls it the reluctant empire – it is the USA. Drawing an analogy, India can be regarded as a reluctant internationaliser. If the INR turnover rises to equal the share of non-US non-Euro currencies in global forex turnover (4 per cent), the INR will have arrived as an international currency, reflecting India’s position in the global economy. Challenges Let me now address the challenges that confront us on the runway to take-off. In my view, the focus should be on four major challenges. The first one is the loss of output and livelihood due to the pandemic. The agglutination of supply disruptions, the health crisis, an unparalleled mass migration and a hostile global environment took a heavy toll on the Indian economy. The combination of demand compression and supply disruption that took hold in the pandemic and in its wake caused severe debilitating effects. As stated earlier, the Indian economy contracted by 6.6 per cent in 2020-21. In the first quarter of that year when the first wave of the pandemic raged, GDP contracted by 24 per cent, among the steepest in the world. If a trend line is fitted to the level of India’s GDP and extended up to 2021-22 at the compound annual growth rate (CAGR) of 6.6 per cent that prevailed over 2013-20, a comparison for this trend GDP with the actual GDP in 2020-21 and 2021-22 will give a rough measure of the output lost to the pandemic. Recovering this lost output may take several years – this I will regard as the first most important challenge. The second challenge is India’s infrastructure gap. India’s per capita investment in infrastructure is one of the lowest in the world (US $ 88.6 in constant 2015 dollars). Infrastructure investment by India is currently around 4.6 per cent of GDP. If India were to invest in infrastructure to the tune of 6 per cent of GDP, it will achieve a GDP level of US $ 7.5 trillion by 2030, as estimated by the Global Infrastructure Hub10, and the infrastructure gap will close. This is also consistent with our target of becoming a US$ 5 trillion economy by 2027. The main requirements for the infrastructure drive are transparent and faster regulatory processes; clear, transparent and efficient land acquisition and climate clearance policies; and viable infrastructure finance that takes into long gestation in infrastructure projects. Building world class infrastructure is the next big challenge for India’s take-off. The third challenge is developing a high quality labour force. The contribution of labour, in terms of both quality and quantity, to GDP growth in India remains much lower than developed as well as many emerging market economies. 83 per cent of the workforce is employed in the unorganised sector. As India transforms into a manufacturing hub and powerhouse exporter, the workforce has to expand and become more skilled over time. The emphasis should be on increasing the contribution of the quality of growth to GDP rather than quantity. Of India’s total labour force, employability (appropriate skills for a particular job) is less than 50 per cent. One important lever to break this constraint is to increase the participation of women in the workforce. According to the World Bank, (World Development Indicators), India ranks 178 among 187 countries in terms of the female labour force participation rate in 2020. We must create workplaces that do not stigmatise women at work and instead, encourage them to earn their livelihoods with dignity and satisfaction. This requires spreading awareness to influence social norms in favour of working women; incentivising institutes to maintain diversity of students and employees; flexible working hours; women friendly policies and facilities at workplaces, including taxation systems that are favourable for working parents and mandatory maternity/paternity leave across workspaces; availability of work closer to the household; and increased formalization of jobs. Women participation is key to developing a high quality labour force. The fourth challenge is a greener, cleaner India. At the Conference of the Parties 26 (COP26) in Glasgow in November 2021, India took five pledges, viz., the Panchamrit, reflecting its commitment towards the environment. They include (i) attaining 500 gigawatts (GW) non-fossil energy capacity by 2030; (ii) energy mix comprising 50 percent renewable energy by 2030; (iii) reducing total projected carbon emissions by one billion tonnes from now onwards till 2030; (iv) reducing the carbon intensity of our economy by less than 45 percent by 2030; and (v) achieving net zero emissions by 2070 by cutting greenhouse gas emissions to as close to zero as possible.The scale of finance needed to meet the above commitments is significant. The Council on Energy, Environment and Water11 has estimated that a cumulative investment of US$ 10.1 trillion is needed to meet net zero commitments by 2070. Of this, US$ 8.4 trillion investment is needed to meet power sector transformation – shift to renewable energy – alone. Industry (reduction in coal and ramping up hydrogen usage) will require US$ 1.5 trillion, and the mobility sector is estimated to need US$ 198 billion. There is a silver lining, however, in respect of renewables. In order to reach 500 GW by 2030, renewables should grow at a compound annual growth rate of 14.2 per cent per annum. At the current average rate of growth at 18.7 per cent (2014-15 to 2020-21), we may achieve the 500 GW target by 2027. India will require adequate energy storage facilities to wedge the gap between the timing of renewable power generation and actual power consumption. We have to minimise transmission and distribution losses. We have to address the regional concentration of renewable energy as it is location specific – mostly the southern states – and not evenly distributed. The tariff structure must reflect actual costs while eschewing cross-subsidies that hurt industries and commercial establishments. And we have to find a solution to the problem of legacy debts of DISCOMs. Conclusion If India capitalises on its opportunities and overcomes the challenges that I have addressed in the time available for this talk, it is widely believed that India will bend time. So, revisiting the purchasing power parity projections I alluded to earlier, it is possible to imagine India striking out into the next decade with a growth rate of 11 per cent. If this is achieved, India will become the second largest economy in the world not by 2048 as shown earlier, but by 2031. Even if it does not sustain this pace and slows to 4-5 per cent in 2040-50, it will become the largest economy of the world by 2060. As I said in my opening remarks, you may think that I am a dreamer, but let me remind you that while history does not repeat itself, it often rhymes. The distinguished British economist, Angus Maddison, who specialised in the measurement and analysis of economic growth and development, has documented economic performance over long periods of time and across major countries in every continent of the world. According to his work, India was the largest economy of the world with the highest share in world GDP during 1 to 1000 AD. Over the next 600 years, India intermittently fell to the second position, but reclaimed the position of the world’s largest economy by 1700 AD with a share of 24.4 per cent of world GDP. Since then, there has been an inexorable loss of share. Ladies and gentlemen, the time has come to halt the decline, reverse it and repossess our rightful place on the world’s stage. Thank you.               1 Speech delivered by Michael Debabrata Patra, Deputy Governor, Reserve Bank of India in an event to celebrate Azadi Ka Amrit Mohotsav organised by Reserve Bank of India, Bhubaneswar on August 13, 2022. Valuable inputs and comments from Rajeev Jain, Atri Mukharjee, V Dhanya, Dhirendra Gajbhiye, Ashish Thomas George, Harendra Behera, Sonna Thangzason and Kunal Priyadarshi, and editorial help from Vineet Kumar Srivastava and Samir Ranjan Behera are gratefully acknowledged. 2 Victor Hugo in Histore d’un Crime, 1877. 4 The fragile five were Brazil, India, Indonesia, South Africa, and Turkey. 5 World Population Prospects 2022; United Nations, July 2022. 6 Number of children per woman. 8 Primary sector activity relates to agriculture and allied activities, mining and quarrying; secondary sector activity relates to manufacture, electricity generation and construction; tertiary activity relates to services. 9 The first industrial revolution occurred during 1760-1840, marked by coal, steam engines and trains. The second revolution occurred between 1870-1940 driven by oil, electricity, the internal combustion engine and the car. The third revolution occurred between 1930-2000 and was based on nuclear energy, natural gas, computers, robots and planes. 10 A non-profit organisation supported by G20. 11 Asia’s leading not-for-profit policy research institution. |

ਇਸ ਪੇਜ ਨੂੰ ਸ਼ੇਅਰ ਕਰੋ:

ਭਾਰਤੀ ਰਿਜ਼ਰਵ ਬੈਂਕ ਮੋਬਾਈਲ ਐਪਲੀਕੇਸ਼ਨ ਇੰਸਟਾਲ ਕਰੋ ਅਤੇ ਨਵੀਨਤਮ ਖਬਰਾਂ ਤੱਕ ਤੇਜ਼ ਐਕਸੈਸ ਪ੍ਰਾਪਤ ਕਰੋ!

ਸਾਡੀ ਐਪ ਇੰਸਟਾਲ ਕਰਨ ਲਈ QR ਕੋਡ ਸਕੈਨ ਕਰੋ।

ਪੇਜ ਅੰਤਿਮ ਅੱਪਡੇਟ ਦੀ ਤਾਰੀਖ: