IST,

IST,

Fifth Bi-monthly Monetary Policy Statement, 2018-19

On the basis of an assessment of the current and evolving macroeconomic situation at its meeting today, the Monetary Policy Committee (MPC) decided to:

Consequently, the reverse repo rate under the LAF remains at 6.25 per cent, and the marginal standing facility (MSF) rate and the Bank Rate at 6.75 per cent. The decision of the MPC is consistent with the stance of calibrated tightening of monetary policy in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. The main considerations underlying the decision are set out in the statement below. Assessment 2. Since the last MPC meeting in October 2018, global economic activity has shown increasing signs of weakness on rising trade tensions. Among advanced economies (AEs), economic activity appears to be slowing in the US in Q4:2018, after a buoyant Q3. The Euro area growth lost pace in Q3, impacted by weaker trade growth and new vehicle emission standards. The Japanese economy contracted in Q3 on subdued external and domestic demand. 3. Economic activity also decelerated in major emerging market economies (EMEs) in Q3. In China, growth slowed down on weak domestic demand. The ongoing trade tensions and the possible cooling of the housing market pose major risks to growth in China. The Russian economy lost some traction, pulled down largely by a weak agriculture harvest, though the growth was buttressed by strong performance of the energy sector. The Brazilian economy seems to be recovering gradually from the economic disruption in the first half of the year. The South African economy expanded in Q3, after contracting in the previous two quarters, driven by agriculture and manufacturing. 4. Crude oil prices have declined sharply, reflecting higher supplies and easing of geo-political tensions. Base metal prices have continued to decline on selling pressure following weak demand from major economies. Gold price has risen underpinned by safe haven demand triggered by political uncertainty in some geographies, though a strong dollar may stem the rise. The inflation scenario has remained broadly unchanged in the US and the Euro area. In many key EMEs, however, inflation has risen, though the recent retreat in energy prices, tightening of policy stances by central banks and stabilising of currencies may have a salutary impact, going forward. 5. Global financial markets have been driven mainly by rising policy rates in the US, volatile crude oil prices and expectations of a slowdown compared with earlier projections. Among AEs, equity markets in the US witnessed a selloff on the weakening outlook for corporate earnings caused by rising borrowing costs, while the European stock markets declined on political uncertainties. The Japanese stock market also shed gains on global cues and the gradual strengthening of the yen. EM stock markets have corrected on shrinking global liquidity, weak economic data in some key EMEs, and lingering trade tensions. The 10-year yield in the US, which surged on robust economic data at the beginning of October, softened subsequently on the unchanged Fed stance. Among other AEs, bond yields in the Euro area and Japan softened on weak economic sentiment and idiosyncratic factors. In most EMEs, bond yields have softened in recent weeks on falling crude oil prices and steadying currencies. In currency markets, the US dollar, which was strengthening on a widening growth differential with its peers, eased in the second half of November. The euro has weakened on Brexit and budget concerns in Italy, while the yen appreciated on safe haven buying in November. EME currencies have been trading with an appreciating bias, supported by a sharp decline in crude oil prices and conservative domestic monetary policy stances. 6. On the domestic front, gross domestic product (GDP) growth slowed down to 7.1 per cent year-on-year (y-o-y) in Q2:2018-19, after four consecutive quarters of acceleration, weighed down by moderation in private consumption and a large drag from net exports. Private consumption slowed down possibly on account of moderation in rural demand, subdued growth in kharif output, depressed prices of agricultural commodities and sluggish growth in rural wages. However, growth in government final consumption expenditure (GFCE) strengthened, buoyed by higher spending by the central government. Gross fixed capital formation (GFCF) expanded by double-digits for the third consecutive quarter, driven mainly by the public sector’s thrust on national highways and rural infrastructure, which was also reflected in robust growth in cement production and steel consumption. Growth of imports accelerated at a much faster pace than that of exports, resulting in net exports pulling down aggregate demand. 7. On the supply side, growth of gross value added (GVA) at basic prices decelerated to 6.9 per cent in Q2, reflecting moderation in agricultural and industrial activities. Slowdown in agricultural GVA was largely the outcome of tepid growth in kharif production. Within industry, growth in manufacturing decelerated due to lower profitability of manufacturing firms, pulled down largely by a rise in input costs, while that in mining and quarrying turned negative, caused by a contraction in output of crude oil and natural gas. Growth in electricity, gas, water supply and other utility services strengthened. Services sector growth remained unchanged at the previous quarter’s level. Of its constituents, growth in construction activity decelerated sequentially, but it was much higher on a y-o-y basis. Growth in public administration and defence services accelerated sharply. 8. Looking beyond Q2, rabi sowing so far (up to end-November) has been 8.3 per cent lower as compared with the same period last year due mainly to lower soil moisture levels resulting from a deficient monsoon and a delayed kharif harvest across states. Precipitation during the north-east monsoon as on November 28 was 49 per cent below the long period average. Storage in major reservoirs, the main source of irrigation during the rabi season, was at 61 per cent of the full reservoir level as on November 29. 9. Growth in the index of industrial production (IIP) slowed down to 4.5 per cent in September 2018. Capacity utilisation (CU), measured by the Reserve Bank’s Order Books, Inventories and Capacity Utilisation Survey (OBICUS), increased from 73.8 per cent in Q1 to 76.1 per cent in Q2, which was higher than the long-term average of 74.9 per cent; seasonally adjusted CU also increased to 76.4 per cent. Available high frequency indicators suggest that industrial activity has been improving in Q3. The growth in core industries recovered in October on the back of double-digit expansion in coal, cement and electricity. The purchasing managers’ index (PMI) for manufacturing touched an eleven-month high of 54.0 in November, supported by an expansion in output, and domestic and export orders. According to the assessment of the Reserve Bank’s Industrial Outlook Survey (IOS), the overall business sentiment in Q3 remained stable, with sustained optimism about production and exports. 10. High frequency indicators of service sector activity showed a mixed picture in September- October. Growth in tractors sales – an indicator of rural demand – turned negative in September. Growth in two-wheeler sales, another indicator of rural demand, rebounded in October, supported by a base effect. Growth in passenger vehicles sales – an indicator of urban demand – turned marginally positive in October, after three consecutive months of negative growth coincident with changes in mandatory long-term third-party insurance requirements and a sharp increase in fuel prices. Commercial vehicle sales growth remained robust in September-October, despite some deceleration. Railway freight traffic improved markedly in October to touch a five-year high growth. While domestic air passenger traffic sustained robust growth, international passenger traffic contracted. PMI for services registered a sharp uptick in November, driven by new business. The composite PMI output index touched a two-year high of 54.5 in November. 11. Retail inflation, measured by y-o-y change in CPI, declined from 3.7 per cent in September to 3.3 per cent in October. A large fall in food prices pushed food group into deflation and more than offset the increase in inflation in items excluding food and fuel. Adjusting for the estimated impact of an increase in house rent allowance (HRA) for central government employees, headline inflation was 3.1 per cent in October. 12. Within the food and beverages group, deflation in vegetables, pulses and sugar deepened in October. Among other items, there was a broad-based softening across food items, especially cereals, milk, fruits and prepared meals. Milk and milk products inflation softened caused by surplus supplies in the domestic market. Fruits inflation moderated, while prepared meals registered a price decline for the first time in the CPI series. Inflation, however, showed an uptick in meat and fish, and non-alcoholic beverages. 13. Inflation in the fuel and light group remained elevated, driven by liquefied petroleum gas prices in October, tracking international petroleum product prices. Kerosene prices also edged up, reflecting the calibrated increase in their administered price. However, electricity prices softened in October. Inflation in rural fuel items such as firewood and chips and dung cake also moderated. 14. CPI inflation excluding food and fuel accelerated to 6.1 per cent in October; adjusted for the estimated HRA impact, it was 5.9 per cent. Transport and communication registered a marked increase, pulled up by higher petroleum product prices, transportation fares and prices of automobiles. A broad-based increase was also observed in health, household goods and services, and personal care and effects. However, inflation moderated significantly in clothing and footwear, as also housing on waning of the HRA impact of central government employees. 15. Inflation expectations of households, measured by the November 2018 round of the Reserve Bank’s survey, softened by 40 basis points for the three-month ahead horizon over the last round reflecting decline in food and petroleum product prices, while they remained unchanged for the twelve-month ahead horizon. Producers’ assessment for input prices inflation eased marginally in Q3 as reported by manufacturing firms polled by the Reserve Bank’s IOS. Domestic farm and industrial input costs remained high. Rural wage growth remained muted in Q2, while staff cost growth in the manufacturing sector remained elevated. 16. The weighted average call rate (WACR) traded below the policy repo rate on 14 out of 21 days in October, on all 18 days in November and both days in December (December 3 and 4). The WACR traded below the repo rate on an average by 5 basis points in October, 9 basis points in November and 16 basis points in December. There was large currency expansion in October and especially during the festive season in November. Currency in circulation, however, contracted in each of the last three weeks in November. Liquidity needs arising from the growth in currency and the Reserve Bank’s forex operations were met through a mixture of tools based on an assessment of the evolving liquidity conditions. The Reserve Bank injected durable liquidity amounting to ₹360 billion in October and ₹500 billion in November through open market purchase operations, bringing total durable liquidity injection to ₹1.36 trillion for 2018-19. Liquidity injected under the LAF, on an average daily net basis, was ₹560 billion in October, ₹806 billion in November and ₹105 billion in December (up to December 4). 17. India’s merchandise exports rebounded in October 2018, after moderating in the previous month, driven mainly by petroleum products, engineering goods, chemicals, electronics, readymade garments, and gems and jewellery. Imports also grew at a faster pace in October relative to the previous month, contributed mainly by petroleum products and electronic goods. Consequently, the trade deficit widened in October 2018 sequentially as also in comparison with the level a year ago. Provisional data suggest a modest improvement in net exports of services in Q2:2018- 19, which augurs well for the current account balance. On the financing side, net FDI flows moderated in April-September 2018. Portfolio flows turned positive in November on account of a sharp decline in oil prices, indications of a less hawkish stance by the US Fed and a softer US dollar. However, during the year, there were net portfolio outflows of US$ 14.8 billion (up to November 30). Non-resident deposits increased markedly in H1:2018-19 on a net basis over their level a year ago. India’s foreign exchange reserves were at US$ 393.7 billion on November 30, 2018. Outlook 18. In the fourth bi-monthly resolution of October 2018, CPI inflation was projected at 4.0 per cent in Q2:2018-19, 3.9-4.5 per cent in H2 and 4.8 per cent in Q1:2019-20, with risks somewhat to the upside. Excluding the HRA impact, CPI inflation was projected at 3.7 per cent in Q2:2018-19, 3.8-4.5 per cent in H2 and 4.8 per cent in Q1:2019-20. The actual inflation outcome in Q2 at 3.9 per cent was marginally lower than the projection of 4.0 per cent. However, the October inflation print at 3.3 per cent turned out to be unexpectedly low. 19. There have been several important developments since the October policy which will have a bearing on the inflation outlook. First, despite a significant scaling down of inflation projections in the October policy primarily due to moderation in food inflation, subsequent readings have continued to surprise on the downside with the food group slipping into deflation. At a disaggregated level, deflation in pulses, vegetables and sugar widened, while cereals inflation moderated sequentially. The broad-based weakening of food prices imparts downward bias to the headline inflation trajectory, going forward. Secondly, in contrast to the food group, there has been a broad-based increase in inflation in non-food groups. Thirdly, international crude oil prices have declined sharply since the last policy; the price of Indian crude basket collapsed to below US$ 60 a barrel by end-November after touching US$ 85 a barrel in early October. However, selling prices, as reported by firms polled in the Reserve Bank’s latest IOS, are expected to edge up further in Q4 on the back of increased demand. Fourthly, global financial markets have continued to be volatile with EME currencies showing a somewhat appreciating bias in the last one month. Finally, the effect of the 7th Central Pay Commission’s HRA increase has continued to wane along expected lines. Taking all these factors into consideration and assuming a normal monsoon in 2019, inflation is projected at 2.7-3.2 per cent in H2:2018-19 and 3.8-4.2 per cent in H1:2019-20, with risks tilted to the upside (Chart 1). The projected inflation path remains unchanged after adjusting for the HRA impact of central government employees as this impact dissipates completely from December 2018 onwards. Although recent food inflation prints have surprised on the downside and prices of petroleum products have softened considerably, it is important to monitor their evolution closely and allow heightened short-term uncertainties to be resolved by incoming data. 20. Turning to growth projections, although Q2 growth was lower than that projected in the October policy, GDP growth in H1 has been broadly along the line in the April policy when for the year as a whole GDP growth was projected at 7.4 per cent. Going forward, lower rabi sowing may adversely affect agriculture and hence rural demand. Financial market volatility, slowing global demand and rising trade tensions pose negative risk to exports. However, on the positive side, the decline in crude oil prices is expected to boost India’s growth prospects by improving corporate earnings and raising private consumption through higher disposable incomes. Increased capacity utilisation in the manufacturing sector also portends well for new capacity additions. There has been significant acceleration in investment activity and high frequency indicators suggest that it is likely to be sustained. Credit offtake from the banking sector has continued to strengthen even as global financial conditions have tightened. FDI flows could also increase with the improving prospects of the external sector. The demand outlook as reported by firms polled in the Reserve Bank’s IOS has improved in Q4. Based on an overall assessment, GDP growth for 2018-19 has been projected at 7.4 per cent (7.2- 7.3 per cent in H2) as in the October policy, and for H1:2019-20 at 7.5 per cent, with risks somewhat to the downside (Chart 2). 21. Even as inflation projections have been revised downwards significantly and some of the risks pointed out in the last resolution have been mitigated, especially of crude oil prices, several uncertainties still cloud the inflation outlook. First, inflation projections incorporate benign food prices based on the realised outcomes of food inflation in recent months. The prices of several food items are at unusually low levels and there is a risk of sudden reversal, especially of volatile perishable items. Secondly, available data suggest that the effect of revision in minimum support prices (MSPs) announced in July on prices has been subdued so far. However, uncertainty continues about the exact impact of MSP on inflation, going forward. Thirdly, the medium-term outlook for crude oil prices is still uncertain due to global demand conditions, geo-political tensions and decision of OPEC which could impinge on supplies. Fourthly, global financial markets continue to be volatile. Fifthly, though households’ near-term inflation expectations have moderated in the latest round of the Reserve Bank’s survey, one-year ahead expectations remain elevated and unchanged. Sixthly, fiscal slippages, if any, at the centre/state levels, will influence the inflation outlook, heighten market volatility and crowd out private investment. Finally, the staggered impact of HRA revision by State Governments may push up headline inflation. While the MPC will look through the statistical impact of HRA revisions, it will be watchful of any second-round effects on inflation. 22. The MPC noted that the benign outlook for headline inflation is driven mainly by the unexpected softening of food inflation and collapse in oil prices in a relatively short period of time. Excluding food items, inflation has remained sticky and elevated, and the output gap remains virtually closed. The MPC also noted that even as escalating trade tensions, tightening of global financial conditions and slowing down of global demand pose some downside risks to the domestic economy, the decline in oil prices in recent weeks, if sustained, will provide tailwinds. The acceleration in investment activity also bodes well for the medium-term growth potential of the economy. The time is apposite to further strengthen domestic macroeconomic fundamentals. In this context, fiscal discipline is critical to create space for and crowd in private investment activity. 23. Against this backdrop, the MPC decided to keep the policy repo rate on hold and maintain the stance of calibrated tightening. While the decision on keeping the policy rate unchanged was unanimous, Dr. Ravindra H. Dholakia voted to change the stance to neutral. The MPC reiterates its commitment to achieving the medium-term target for headline inflation of 4 per cent on a durable basis. The minutes of the MPC’s meeting will be published by December 19, 2018. 24. The next meeting of the MPC is scheduled from February 5 to 7, 2019. Statement on Developmental and Regulatory Policies This Statement sets out various developmental and regulatory policy measures for strengthening regulation and supervision; broadening and deepening of the financial markets; and enhancing customer education, protection and financial inclusion. I. Regulation and Supervision 1. External Benchmarking of New Floating Rate Loans by Banks The Report of the Internal Study Group to Review the Working of the Marginal Cost of Funds based Lending Rate (MCLR) System (Chairman: Dr. Janak Raj) released on October 4, 2017 for public feedback, had recommended the use of external benchmarks by banks for their floating rate loans instead of the present system of internal benchmarks [Prime Lending Rate (PLR), Benchmark Prime Lending Rate (BPLR), Base rate and Marginal Cost of Funds based Lending Rate (MCLR)]. As a step in that direction, it is proposed that all new floating rate personal or retail loans (housing, auto, etc.) and floating rate loans to Micro and Small Enterprises extended by banks from April 1, 2019 shall be benchmarked to one of the following: - Reserve Bank of India policy repo rate, or - Government of India 91 days Treasury Bill yield produced by the Financial Benchmarks India Private Ltd (FBIL), or - Government of India 182 days Treasury Bill yield produced by the FBIL, or - Any other benchmark market interest rate produced by the FBIL. The spread over the benchmark rate — to be decided wholly at banks’ discretion at the inception of the loan — should remain unchanged through the life of the loan, unless the borrower’s credit assessment undergoes a substantial change and as agreed upon in the loan contract. Banks are free to offer such external benchmark linked loans to other types of borrowers as well. In order to ensure transparency, standardisation, and ease of understanding of loan products by borrowers, a bank must adopt a uniform external benchmark within a loan category; in other words, the adoption of multiple benchmarks by the same bank is not allowed within a loan category. The final guidelines will be issued by the end of December 2018. 2. Mandatory Loan Component in Working Capital Finance With a view to promoting greater credit discipline among working capital borrowers, it was proposed in the Statement on Developmental and Regulatory Policies announced on April 5, 2018 to stipulate a minimum level of ‘loan component’ in fund-based working capital finance for larger borrowers. Accordingly, the draft guidelines in this regard were issued on June 11, 2018 for comments of the stakeholders. Taking into account the views of the stakeholders, the final guidelines which take effect from April 1, 2019 are being issued today. 3. Aligning Statutory Liquidity Ratio with Liquidity Coverage Ratio As per the existing roadmap, scheduled commercial banks have to reach the minimum Liquidity Coverage Ratio (LCR) of 100 per cent by January 1, 2019. Presently, Statutory Liquidity Ratio (SLR) is 19.5 per cent of Net Demand and Time Liabilities (NDTL). Further, the assets allowed to be reckoned as Level 1 High Quality Liquid Assets (HQLAs) for the purpose of computing the LCR of banks, inter alia, include (a) Government securities in excess of the minimum SLR requirement; and (b) within the mandatory SLR requirement, Government securities to the extent allowed by RBI under (i) Marginal Standing Facility (MSF) [presently 2 per cent of the bank’s NDTL] and (ii) Facility to Avail Liquidity for Liquidity Coverage Ratio (FALLCR) [presently 13 per cent of the bank’s NDTL]. In order to align the SLR with the LCR requirement, it is proposed to reduce the SLR by 25 basis points every calendar quarter until the SLR reaches 18 per cent of NDTL. The first reduction of 25 basis points will take effect in the quarter commencing January 2019. 4. Board of Management in Primary (Urban) Cooperative Banks (UCBs) The Expert Committee on licensing of new Urban Co-operative Banks (2010) under the chairmanship of Shri Y.H. Malegam had recommended, inter alia, that a Board of Management (BoM) be constituted in every Primary (Urban) Co-operative Bank (UCB), in addition to the Board of Directors (BoD) with a view to strengthening governance in the UCBs. This was reiterated by the High Powered Committee on Urban Co-operative Banks (Chairman: Shri R. Gandhi) constituted in January 2015. Reserve Bank of India had released draft guidelines on constituting BoM in UCBs on June 25, 2018 inviting comments from banks and other stakeholders. It is proposed in the guidelines to require UCBs to make a provision in their bye laws for setting up a BoM. The guidelines also propose that regulatory approvals such as expansion of area of operation and opening of new branches may be allowed only for UCBs that have made such a provision in their bye laws. Taking into consideration the responses received, it is proposed to issue final guidelines by the end of December 2018. II. Financial Markets 5. Access for Non-Residents to the Interest Rate Derivatives Market It was proposed in the Statement on Developmental and Regulatory Policies announced on April 5, 2018 that non-residents shall be given access to the Rupee Interest Rate Derivatives (IRD) market in India. The draft directions in this regard propose allowing non-residents to hedge their rupee interest rate risk flexibly using any available IRD instrument. Non-residents will also be permitted to participate in the Overnight Indexed Swap (OIS) market for non-hedging purposes, subject to a macro-prudential limit on exposure of all non-residents in terms of the interest rate risk undertaken (measured as PV01). Draft directions are being issued today for public feedback. 6. Measures to Improve Liquidity Management by Banks Currently, the Cash Reserve Ratio (CRR) balance of banks at the end of the day is being disclosed with a lag of 2-3 days, while the details of the currency in circulation are being released with a lag of one week. In order to enable banks to forecast their liquidity requirements with a greater degree of precision, it has been decided that the Reserve Bank will provide information on daily CRR balance of the banking system to market participants on the very next day. Accordingly, the daily Money Market Operations press release will contain the CRR figure for the previous day, with effect from December 6, 2018. 7. Rationalisation of Borrowing and Lending Regulations under FEMA, 1999 As part of the ongoing efforts at rationalising multiple regulations framed over a period of time under FEMA, 1999, it is proposed to consolidate the regulations governing all types of borrowing and lending transactions between a person resident in India and a person resident outside India in both foreign currency and INR, in consultation with the Government. The proposed regulations, viz., Foreign Exchange Management (Borrowing or Lending) Regulations, 2018 shall subsume the existing Notification No. FEMA. 3/2000-RB dated May 3, 2000, Notification No. FEMA. 4/2000-RB dated May 3, 2000 and Regulation 21 of Notification No. FEMA. 120/RB-2004 dated July 7, 2004, and rationalise the extant framework for external commercial borrowings and Rupee denominated bonds with a view to improving the ease of doing business. The consolidated regulation and guidelines will be issued by the end of December 2018. III. Customer Education, Protection and Financial Inclusion 8. Ombudsman Scheme for Digital Transactions With the digital mode for financial transactions gaining traction in the country, there is an emerging need for a dedicated, cost-free and expeditious grievance redressal mechanism for strengthening consumer confidence in this channel. It has therefore been decided to implement an ‘Ombudsman Scheme for Digital Transactions’ covering services provided by entities falling under Reserve Bank’s regulatory jurisdiction. The Scheme will be notified by the end of January 2019. 9. Framework for Limiting Customer Liability in respect of Unauthorised Electronic Payment Transactions involving Prepaid Payment Instruments The Reserve Bank has issued instructions on limiting customer liability in respect of unauthorised electronic transactions involving banks and credit card issuing non-banking financial companies (NBFCs). As a measure of consumer protection, it has been decided to bring all customers up to the same level with regard to electronic transactions made by them and extend the benefit of limiting customer liability for unauthorised electronic transactions involving Prepaid Payment Instruments (PPIs) issued by other entities not covered by the extant guidelines on the subject. The guidelines will be issued by the end of December 2018. 10. Expert Committee on Micro, Small and Medium Enterprises Micro, Small and Medium Enterprises (MSMEs) contribute significantly to employment, entrepreneurship and growth in the economy. They remain, by their predominantly informal nature, vulnerable to structural and cyclical shocks, at times with persistent effects. It is important to understand the economic forces and transactions costs affecting the performance of the MSMEs, while often the rehabilitation approach to the MSMEs stress has focused on deploying favourable credit terms and regulatory forbearances. To this end, an Expert Committee will be constituted by the Reserve Bank of India to identify causes and propose long-term solutions for the economic and financial sustainability of the MSME sector. The composition of the Committee and its Terms of Reference will be finalised by the end of December 2018 and the report will be submitted by the end of June 2019. * Released on December 05, 2018. |

இந்த பக்கத்தை பகிரவும்:

இந்திய ரிசர்வ் வங்கி மொபைல் செயலியை நிறுவுங்கள் மற்றும் சமீபத்திய செய்திகளுக்கான விரைவான அணுகலை பெறுங்கள்!

எங்கள் செயலியை நிறுவ QR குறியீட்டை ஸ்கேன் செய்யவும்

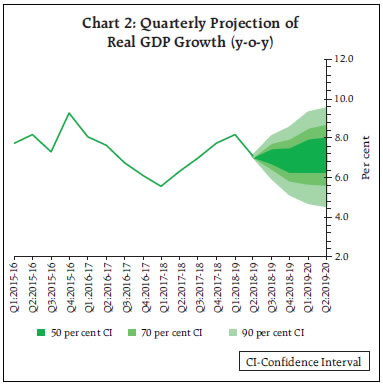

கடைசியாக புதுப்பிக்கப்பட்ட பக்கம்: