IST,

IST,

Third Bi-Monthly Monetary Policy Statement, 2014-15

By Monetary and Liquidity Measures On the basis of an assessment of the current and evolving macroeconomic situation, it has been decided to:

Consequently, the reverse repo rate under the LAF will remain unchanged at 7.0 per cent, and the marginal standing facility (MSF) rate and the Bank Rate at 9.0 per cent. Assessment 2. Since the second bi-monthly monetary policy statement of June 2014, global economic activity has been picking up at a modest space from a sharp slowdown in Q1. Investor risk appetite has buoyed financial markets, partly drawing strength from assurances of continuing monetary policy support in industrial countries. Portfolio flows to emerging market economies (EMEs) have risen strongly. This implies, however, that EMEs remain vulnerable to changes in investor risk appetite driven by any reassessment of the future path of US monetary policy or possible escalation of geopolitical tensions. 3. Sentiment on domestic economic activity appears to be reviving, with incoming data suggesting a firming up of industrial growth and exports. The June round of the Reserve Bank’s industrial outlook survey also points to improvement in business expectations in Q2. Leading indicators of the services sector are mixed, although there are early signs of modest strengthening of corporate sales and business flows. While the initial slow progress of the monsoon and its uneven spatial distribution raised serious concerns regarding agricultural production, these have been mitigated, though not entirely dispelled, by the pick-up in the monsoon through much of the country in July. The implementation of government policy actions that have been announced should create a congenial setting for a steady improvement in domestic demand and supply conditions. 4. Retail inflation measured by the consumer price index (CPI) has eased for the second consecutive month in June, with a broad-based moderation accompanied by deceleration in momentum. Higher prices of vegetables, fruits and protein-based food items were offset by the muted increase in the prices of non-food items, particularly those of household requisites and transport and communication. CPI inflation excluding food and fuel decelerated further, extending the decline that began in September 2013. However, with some continuing uncertainty about the path of the monsoon, it would be premature to conclude that future food inflation, and its spill-over to broader inflation, can be discounted. 5. Liquidity conditions have remained broadly stable, barring episodic tightness on account of movements in the cash balances of the Government maintained with the Reserve Bank. While the system’s recourse to liquidity from the LAF, and regular and additional term repos has been around 1.0 per cent of the NDTL of banks, access to the MSF has been minimal and temporary. In order to manage transient liquidity pressures associated with tax outflows and sluggish spending by the Government, the Reserve Bank injected additional liquidity aggregating over ` 940 billion through nine special term repos of varying maturities during the months of June and July. Despite the reduction in the export credit refinance effected in early June, average utilisation of the facility has only been around 70 per cent of the available limit. The Reserve Bank will review existing liquidity arrangements and continue to monitor and manage liquidity to ensure adequate flow of credit to the productive sectors. 6. With the buoyancy in export performance sustained through Q1, the trade deficit has narrowed from its level a year ago. While oil imports rose in June partly on higher international crude prices, gold import growth picked up in response to some liberalization of import restrictions, and non-oil non-gold import growth has turned positive since May. Turning to external financing, all categories of capital flows have been buoyant. Surges in capital inflows in excess of the current account financing requirement and the repayment of swaps by oil marketing companies have bolstered international reserves. Policy Stance and Rationale 7. The moderation in CPI headline inflation for two consecutive months, despite the seasonal firming up of prices of fruits and vegetables since March, is due to both base effects and the steady deceleration in CPI inflation excluding food and fuel. The recent fall in international crude prices, the benign outlook on global non-oil commodity prices and still-subdued corporate pricing power should all support continued disinflation, as should measures undertaken to improve food management. There are, however, upside risks also, in the form of the pass-through of administered price increases, continuing uncertainty over monsoon conditions and their impact on food production, possibly higher oil prices stemming from geo-political concerns and exchange rate movement, and strengthening growth in the face of continuing supply constraints. Accordingly, the upside risks to the target of ensuring CPI inflation at or below 8 per cent by January 2015 remain, although overall risks are more balanced than in June (Chart 1). It is, therefore, appropriate to continue maintaining a vigilant monetary policy stance as in June, while leaving the policy rate unchanged. 8. Prospects for reinvigoration of growth have improved modestly. The firming up of export growth should support manufacturing and service sector activity. If the recent pick-up in industrial activity is sustained in an environment conducive to the revival of investment and unlocking of stalled projects, with ongoing fiscal consolidation releasing resources for private enterprise, external demand picking up and international crude prices stabilising, the central estimate of real GDP growth of 5.5 per cent within a likely range of 5 to 6 per cent that was set out in the April projection for 2014-15 can be sustained. On the other hand, if risks relating to the global recovery, the monsoon and geo-political tensions intensify, the balance of risks could tilt to the downside (Chart 2). 9. The Reserve Bank will continue to monitor inflation developments closely, and remains committed to the disinflationary path of taking CPI inflation to 8 per cent by January 2015 and 6 per cent by January 2016. While inflation at around 8 per cent in early 2015 seems likely, it is critical that the disinflationary process is sustained over the medium-term. The balance of risks around the medium-term inflation path, and especially the target of 6 per cent by January 2016, are still to the upside, warranting a heightened state of policy preparedness to contain these risks if they materialise. In the months ahead, government actions on food management and to facilitate project completion should improve supply, but as consumer and business confidence pick up, aggregate demand will also strengthen. The Reserve Bank will act as necessary to ensure sustained disinflation. 10. In the second bi-monthly monetary policy statement of June 2014, the Reserve Bank reduced the SLR to 22.5 per cent of NDTL in anticipation of recovery in economic activity. With the Union Budget for 2014-15 renewing commitment to the medium-term fiscal consolidation roadmap and budgeting 4.1 per cent of GDP as the fiscal deficit for the year, space has opened up further for banks to expand credit to the productive sectors in response to its financing needs as growth picks up. Accordingly, the SLR is reduced by a further 0.5 per cent of NDTL. 11. In consonance with the calibrated reduction in the SLR, it is necessary to enhance liquidity in the money and debt markets so that financial intermediation expands apace with a growing economy. Currently, banks are permitted to exceed the limit of 25 per cent of total investments under the held to maturity (HTM) category provided the excess comprises only SLR securities, and banks’ total holdings of SLR securities in the HTM category is not more than 24.5 per cent of their NDTL as on the last Friday of the second preceding fortnight. In order to enable banks greater participation in financial markets, this ceiling is being brought down to 24 per cent of NDTL with effect from the fortnight beginning August 9, 2014. 12. The Reserve Bank has taken a number of steps to enhance efficiency, increase entry, speed up resolution, and improve access to financial services, such as modified regulations on long term lending and borrowing, proposals for licensing payment banks and small banks, a framework to deal with stressed assets, actions to further the use of mobile phones in banking, and efforts to simplify know your customer (KYC) norms, among others. The Reserve Bank will continue to carry forward its banking sector reforms agenda. 13. The fourth bi-monthly monetary policy statement is scheduled on Tuesday, September 30, 2014. Sangeeta Das Press Release: 2014-2015/248 |

شارك هذه الصفحة:

بھارت موبائل ایپلی کیشن کے ریزرو بینک کو انسٹال کریں اور تازہ ترین خبروں تک فوری رسائی حاصل کریں!

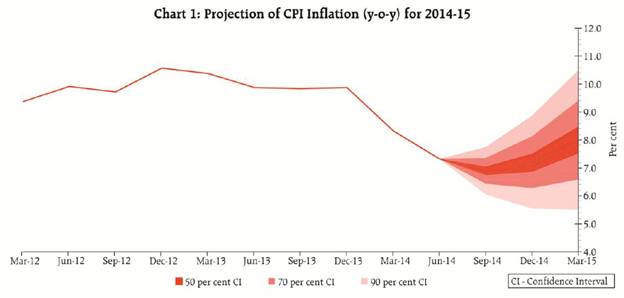

ہماری ایپ انسٹال کرنے کے لیے QR کوڈ اسکین کریں۔

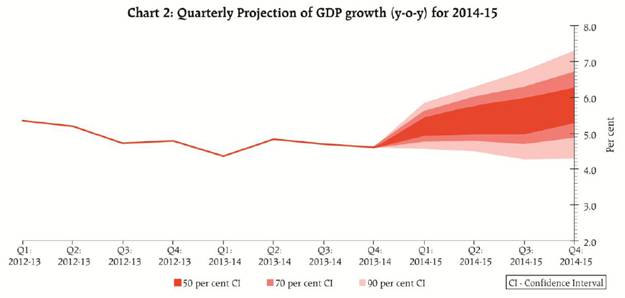

صفحے پر آخری اپ ڈیٹ: