Today, the Reserve Bank released the results of the 94th round of the Industrial Outlook Survey (IOS) conducted during April-June 2021. The survey encapsulates qualitative assessment of the business climate by Indian manufacturing companies for Q1:2021-22 and their expectations for Q2:2021-221. In all, 1281 companies responded in this round of the survey. Owing to uncertainty driven by the COVID-19 pandemic, an additional block was included in this round of the survey for assessing the outlook on key parameters for two quarters ahead as well as three quarters ahead. Highlights: A. Assessment for Q1: 2021-22 -

Manufacturing companies assessed deterioration in demand condition measured in terms of production, order books and employment situation during Q1:2021-22 (Table A). -

Sentiments on financial situation turned negative, driven by decline in all three sources of finance (viz., banks, internal accruals and overseas). -

Manufacturers perceived higher cost burdens from cost of finance and salary outgo. Input cost pressure remained high but the pessimism was somewhat lower than the previous round. -

Respondents polled moderation in selling prices and the sentiments on profit margins remained subdued. -

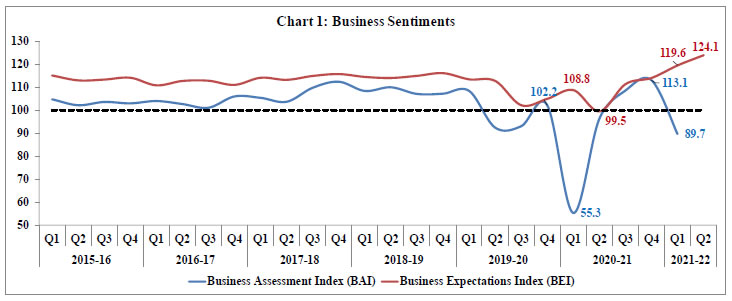

The business assessment index (BAI)2 contracted to 89.7 in Q1 from 113.1 in previous quarter (Chart 1); the decline was much lower than that witnessed around the onset of the pandemic during Q1:2020-21. B. Expectations for Q2: 2021-22 -

Production volumes, new orders and job landscape are expected to improve in Q2:2021-22. -

Manufacturers expect improvement in overall financial situation. -

A major segment of the respondents anticipates continued pressure from input costs and salary outgo, though the share of such companies declined marginally. -

More companies expect profit margins to improve. -

The business expectations index (BEI) increased further to 124.1 in Q2:2021-22 from 119.6 in Q1:2021-22 (Chart 1). C. Expectations for Q3:2021-22 and Q4:2021-22 -

Manufacturers perceive further improvement in production and overall business situation in Q3:2021-22; and exhibit optimism for Q4:2021-22 (Table B). -

Capacity utilisation and employment conditions are expected to improve. -

Respondents expect input cost pressure to continue, albeit with marginal easing, and selling prices to harden. | Table A: Summary of Net responses3 on Survey Parameters | | (per cent) | | Parameters | Assessment period | Expectation period | | Q4:2020-21 | Q1:2021-22 | Q1:2021-22 | Q2:2021-22 | | Production | 36.3 | -25.9 | 43.7 | 52.0 | | Order Books | 33.1 | -16.4 | 43.2 | 50.4 | | Pending Orders | -3.0 | 10.0 | -2.4 | -3.7 | | Capacity Utilisation | 29.1 | -26.1 | 38.0 | 45.4 | | Inventory of Raw Materials | -11.1 | -0.3 | -11.8 | -17.5 | | Inventory of Finished Goods | -7.6 | -4.2 | -10.9 | -19.4 | | Exports | 15.5 | -7.8 | 29.6 | 43.6 | | Imports | 16.4 | 1.7 | 26.1 | 42.8 | | Employment | 10.9 | -3.5 | 17.9 | 26.1 | | Financial Situation (Overall) | 29.4 | -12.7 | 47.3 | 48.2 | | Availability of Finance (from internal accruals) | 23.7 | -4.3 | 34.7 | 38.6 | | Availability of Finance (from banks & other sources) | 16.5 | -2.4 | 25.6 | 35.5 | | Availability of Finance (from overseas, if applicable) | 2.7 | 1.6 | 13.4 | 42.7 | | Cost of Finance | -3.4 | -4.5 | -13.9 | -31.5 | | Cost of Raw Material | -69.0 | -52.3 | -62.4 | -54.9 | | Salary/ Other Remuneration | -18.7 | -19.9 | -41.6 | -31.6 | | Selling Price | 22.7 | 19.6 | 29.2 | 28.2 | | Profit Margin | 2.0 | -32.2 | 11.0 | 32.7 | | Overall Business Situation | 36.5 | -20.6 | 52.5 | 52.4 | | Note: Please see the excel file for time series data |

| Table B: Business Expectations of Select Parameters for extended period – Net response | | (per cent) | | Parameters | Round 93 | Round 94 | | Q1:2021-22 | Q2:2021-22 | Q3:2021-22 | Q4:2021-22 | | Overall Business Situation | 52.5 | 52.4 | 71.2 | 70.4 | | Production | 43.7 | 52.0 | 72.0 | 69.6 | | Order Books | 43.2 | 50.4 | 72.8 | 70.1 | | Capacity Utilisation | 38.0 | 45.4 | 63.0 | 61.6 | | Employment | 17.9 | 26.1 | 43.1 | 32.8 | | Cost of Raw Materials | -62.4 | -54.9 | -55.7 | -53.7 | | Selling Prices | 29.2 | 28.2 | 43.0 | 32.2 |

| Table 1: Assessment and Expectations for Production | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q1:2020-21 | 802 | 8.3 | 72.2 | 19.5 | -63.9 | 37.8 | 14.1 | 48.1 | 23.7 | | Q2:2020-21 | 959 | 42.4 | 32.1 | 25.5 | 10.3 | 41.4 | 30.2 | 28.5 | 11.2 | | Q3:2020-21 | 1,011 | 46.6 | 19.4 | 34.0 | 27.2 | 43.4 | 16.9 | 39.7 | 26.4 | | Q4:2020-21 | 967 | 48.9 | 12.6 | 38.5 | 36.3 | 43.7 | 12.2 | 44.0 | 31.5 | | Q1:2021-22 | 1,281 | 16.5 | 42.3 | 41.2 | -25.9 | 53.3 | 9.7 | 37.0 | 43.7 | | Q2:2021-22 | | | | | | 58.8 | 6.8 | 34.3 | 52.0 | ‘Increase’ in production is optimistic.

Note: The sum of components may not add up to total due to rounding off (This is applicable for all tables). |

| Table 2: Assessment and Expectations for Order Books | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q1:2020-21 | 802 | 8.9 | 63.8 | 27.3 | -54.9 | 33.5 | 15.1 | 51.4 | 18.4 | | Q2:2020-21 | 959 | 37.2 | 31.3 | 31.5 | 5.9 | 36.4 | 28.4 | 35.3 | 8.0 | | Q3:2020-21 | 1,011 | 40.3 | 19.8 | 40.0 | 20.5 | 39.2 | 18.6 | 42.2 | 20.6 | | Q4:2020-21 | 967 | 46.4 | 13.3 | 40.3 | 33.1 | 41.1 | 13.7 | 45.2 | 27.3 | | Q1:2021-22 | 1,281 | 20.0 | 36.5 | 43.5 | -16.4 | 51.0 | 7.8 | 41.1 | 43.2 | | Q2:2021-22 | | | | | | 56.9 | 6.5 | 36.7 | 50.4 | | ‘Increase’ in order books is optimistic. |

| Table 3: Assessment and Expectations for Pending Orders | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Above Normal | Below Normal | Normal | Net response | Above Normal | Below Normal | Normal | Net response | | Q1:2020-21 | 802 | 6.1 | 47.3 | 46.6 | 41.2 | 4.6 | 16.2 | 79.1 | 11.6 | | Q2:2020-21 | 959 | 7.2 | 30.1 | 62.7 | 22.8 | 5.8 | 31.8 | 62.4 | 26.0 | | Q3:2020-21 | 1,011 | 7.2 | 19.2 | 73.6 | 12.0 | 7.4 | 21.5 | 71.1 | 14.2 | | Q4:2020-21 | 967 | 13.2 | 10.2 | 76.6 | -3.0 | 5.6 | 14.8 | 79.7 | 9.2 | | Q1:2021-22 | 1,281 | 7.4 | 17.5 | 75.1 | 10.0 | 11.6 | 9.2 | 79.3 | -2.4 | | Q2:2021-22 | | | | | | 10.8 | 7.2 | 82.0 | -3.7 | | Pending orders ‘Below Normal’ is optimistic. |

| Table 4: Assessment and Expectations for Capacity Utilisation (Main Product) | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q1:2020-21 | 802 | 6.0 | 67.6 | 26.3 | -61.6 | 25.5 | 14.2 | 60.3 | 11.3 | | Q2:2020-21 | 959 | 31.8 | 30.2 | 37.9 | 1.6 | 36.2 | 28.6 | 35.2 | 7.6 | | Q3:2020-21 | 1,011 | 35.3 | 18.0 | 46.7 | 17.3 | 32.4 | 15.0 | 52.6 | 17.5 | | Q4:2020-21 | 967 | 40.6 | 11.5 | 47.9 | 29.1 | 34.7 | 10.6 | 54.7 | 24.1 | | Q1:2021-22 | 1,281 | 13.4 | 39.5 | 47.1 | -26.1 | 45.2 | 7.3 | 47.5 | 38.0 | | Q2:2021-22 | | | | | | 51.6 | 6.2 | 42.2 | 45.4 | | ‘Increase’ in capacity utilisation is optimistic. |

| Table 5: Assessment and Expectations for Level of CU (compared to the average in last 4 quarters) | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Above Normal | Below Normal | Normal | Net response | Above Normal | Below Normal | Normal | Net response | | Q1:2020-21 | 802 | 2.7 | 63.6 | 33.7 | -60.9 | 9.1 | 16.4 | 74.5 | -7.3 | | Q2:2020-21 | 959 | 5.9 | 43.4 | 50.8 | -37.5 | 5.8 | 39.2 | 55.0 | -33.5 | | Q3:2020-21 | 1,011 | 11.3 | 23.2 | 65.5 | -12.0 | 8.3 | 25.5 | 66.2 | -17.2 | | Q4:2020-21 | 967 | 21.3 | 12.2 | 66.5 | 9.1 | 11.7 | 15.3 | 73.0 | -3.6 | | Q1:2021-22 | 1,281 | 5.2 | 18.4 | 76.3 | -13.2 | 25.3 | 8.4 | 66.2 | 16.9 | | Q2:2021-22 | | | | | | 15.6 | 7.9 | 76.5 | 7.7 | | ‘Above Normal’ in Level of capacity utilisation is optimistic. |

| Table 6: Assessment and Expectations for Assessment of Production Capacity (with regard to expected demand in next 6 months) | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | More than adequate | Less than adequate | Adequate | Net response | More than adequate | Less than adequate | Adequate | Net response | | Q1:2020-21 | 802 | 19.0 | 24.5 | 56.5 | -5.6 | 13.7 | 8.8 | 77.5 | 4.9 | | Q2:2020-21 | 959 | 15.9 | 17.2 | 66.9 | -1.3 | 18.7 | 17.3 | 64.0 | 1.3 | | Q3:2020-21 | 1,011 | 14.1 | 11.2 | 74.6 | 2.9 | 15.9 | 12.3 | 71.8 | 3.5 | | Q4:2020-21 | 967 | 15.5 | 10.0 | 74.5 | 5.5 | 14.2 | 9.3 | 76.5 | 5.0 | | Q1:2021-22 | 1,281 | 10.8 | 13.0 | 76.2 | -2.2 | 20.2 | 7.3 | 72.5 | 12.9 | | Q2:2021-22 | | | | | | 28.4 | 5.8 | 65.8 | 22.6 | | ‘More than adequate’ in Assessment of Production Capacity is optimistic. |

| Table 7: Assessment and Expectations for Exports | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q1:2020-21 | 802 | 8.7 | 50.4 | 40.9 | -41.7 | 22.5 | 11.5 | 66.0 | 11.0 | | Q2:2020-21 | 959 | 25.3 | 25.9 | 48.8 | -0.6 | 23.1 | 26.9 | 50.0 | -3.8 | | Q3:2020-21 | 1,011 | 22.5 | 17.9 | 59.5 | 4.6 | 25.1 | 17.6 | 57.3 | 7.5 | | Q4:2020-21 | 967 | 31.6 | 16.0 | 52.4 | 15.5 | 25.1 | 12.1 | 62.7 | 13.0 | | Q1:2021-22 | 1,281 | 18.3 | 26.1 | 55.6 | -7.8 | 38.7 | 9.0 | 52.3 | 29.6 | | Q2:2021-22 | | | | | | 49.8 | 6.2 | 44.0 | 43.6 | | ‘Increase’ in exports is optimistic. |

| Table 8: Assessment and Expectations for Imports | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q1:2020-21 | 802 | 7.6 | 40.5 | 51.8 | -32.9 | 16.9 | 10.3 | 72.8 | 6.6 | | Q2:2020-21 | 959 | 18.4 | 21.2 | 60.5 | -2.8 | 19.9 | 21.0 | 59.1 | -1.0 | | Q3:2020-21 | 1,011 | 19.6 | 13.3 | 67.2 | 6.3 | 17.3 | 12.4 | 70.4 | 4.9 | | Q4:2020-21 | 967 | 25.8 | 9.3 | 64.9 | 16.4 | 17.7 | 9.1 | 73.2 | 8.5 | | Q1:2021-22 | 1,281 | 18.9 | 17.1 | 64.0 | 1.7 | 32.6 | 6.6 | 60.8 | 26.1 | | Q2:2021-22 | | | | | | 47.3 | 4.5 | 48.3 | 42.8 | | ‘Increase’ in imports is optimistic. |

| Table 9: Assessment and Expectations for level of Raw Materials Inventory | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Above average | Below average | Average | Net response | Above average | Below average | Average | Net response | | Q1:2020-21 | 802 | 21.3 | 13.5 | 65.2 | -7.8 | 9.8 | 6.9 | 83.3 | -2.9 | | Q2:2020-21 | 959 | 16.7 | 10.9 | 72.3 | -5.8 | 15.5 | 9.7 | 74.8 | -5.9 | | Q3:2020-21 | 1,011 | 13.1 | 7.7 | 79.3 | -5.4 | 11.5 | 7.4 | 81.1 | -4.2 | | Q4:2020-21 | 967 | 17.5 | 6.5 | 76.0 | -11.1 | 12.0 | 5.3 | 82.8 | -6.7 | | Q1:2021-22 | 1,281 | 11.5 | 11.2 | 77.3 | -0.3 | 17.2 | 5.4 | 77.4 | -11.8 | | Q2:2021-22 | | | | | | 23.7 | 6.2 | 70.0 | -17.5 | | ‘Below average’ Inventory of raw materials is optimistic. |

| Table 10: Assessment and Expectations for level of Finished Goods Inventory | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Above average | Below average | Average | Net response | Above average | Below average | Average | Net response | | Q1:2020-21 | 802 | 27.0 | 14.3 | 58.7 | -12.6 | 10.4 | 6.2 | 83.4 | -4.3 | | Q2:2020-21 | 959 | 18.9 | 10.2 | 70.9 | -8.7 | 17.2 | 9.5 | 73.3 | -7.6 | | Q3:2020-21 | 1,011 | 12.8 | 8.1 | 79.1 | -4.6 | 12.4 | 7.2 | 80.4 | -5.3 | | Q4:2020-21 | 967 | 15.2 | 7.5 | 77.3 | -7.6 | 11.5 | 5.1 | 83.4 | -6.3 | | Q1:2021-22 | 1,281 | 14.4 | 10.2 | 75.4 | -4.2 | 16.4 | 5.5 | 78.1 | -10.9 | | Q2:2021-22 | | | | | | 25.0 | 5.6 | 69.4 | -19.4 | | ‘Below average’ Inventory of finished goods is optimistic. |

| Table 11: Assessment and Expectations for Employment | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q1:2020-21 | 802 | 3.9 | 32.5 | 63.7 | -28.6 | 14.3 | 9.0 | 76.7 | 5.2 | | Q2:2020-21 | 959 | 11.8 | 21.0 | 67.2 | -9.2 | 11.0 | 18.7 | 70.3 | -7.7 | | Q3:2020-21 | 1,011 | 15.5 | 11.6 | 73.0 | 3.9 | 14.5 | 12.1 | 73.3 | 2.4 | | Q4:2020-21 | 967 | 19.4 | 8.5 | 72.1 | 10.9 | 14.6 | 7.3 | 78.1 | 7.2 | | Q1:2021-22 | 1,281 | 9.1 | 12.7 | 78.2 | -3.5 | 23.5 | 5.5 | 71.0 | 17.9 | | Q2:2021-22 | | | | | | 28.6 | 2.5 | 69.0 | 26.1 | | ‘Increase’ in employment is optimistic. |

| Table 12: Assessment and Expectations for Overall Financial Situation | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Better | Worsen | No change | Net response | Better | Worsen | No change | Net response | | Q1:2020-21 | 802 | 8.7 | 57.6 | 33.6 | -48.9 | 33.1 | 8.8 | 58.0 | 24.3 | | Q2:2020-21 | 959 | 31.8 | 23.9 | 44.3 | 7.8 | 34.6 | 23.2 | 42.2 | 11.4 | | Q3:2020-21 | 1,011 | 40.4 | 12.9 | 46.7 | 27.5 | 36.7 | 11.4 | 51.9 | 25.3 | | Q4:2020-21 | 967 | 43.0 | 13.6 | 43.4 | 29.4 | 39.2 | 6.2 | 54.6 | 33.0 | | Q1:2021-22 | 1,281 | 17.8 | 30.6 | 51.6 | -12.7 | 53.4 | 6.1 | 40.5 | 47.3 | | Q2:2021-22 | | | | | | 54.0 | 5.8 | 40.2 | 48.2 | | ‘Better’ overall financial situation is optimistic. |

| Table 13: Assessment and Expectations for Working Capital Finance Requirement | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q1:2020-21 | 802 | 36.9 | 18.8 | 44.4 | 18.1 | 28.8 | 5.7 | 65.5 | 23.1 | | Q2:2020-21 | 959 | 33.3 | 11.4 | 55.3 | 21.9 | 37.2 | 11.5 | 51.3 | 25.7 | | Q3:2020-21 | 1,011 | 30.7 | 7.1 | 62.2 | 23.7 | 31.3 | 6.9 | 61.8 | 24.4 | | Q4:2020-21 | 967 | 30.8 | 7.7 | 61.4 | 23.1 | 28.5 | 3.7 | 67.8 | 24.8 | | Q1:2021-22 | 1,281 | 24.4 | 14.0 | 61.7 | 10.4 | 37.6 | 5.2 | 57.3 | 32.4 | | Q2:2021-22 | | | | | | 44.7 | 3.0 | 52.2 | 41.7 | | ‘Increase’ in working capital finance is optimistic. |

| Table 14: Assessment and Expectations for Availability of Finance (from Internal Accruals) | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Improve | Worsen | No change | Net response | Improve | Worsen | No change | Net response | | Q1:2020-21 | 802 | 7.2 | 38.0 | 54.8 | -30.8 | 23.1 | 6.0 | 70.9 | 17.0 | | Q2:2020-21 | 959 | 22.2 | 18.4 | 59.5 | 3.8 | 22.5 | 16.1 | 61.3 | 6.4 | | Q3:2020-21 | 1,011 | 27.2 | 9.7 | 63.1 | 17.4 | 24.8 | 9.7 | 65.5 | 15.1 | | Q4:2020-21 | 967 | 33.3 | 9.6 | 57.1 | 23.7 | 28.3 | 5.6 | 66.1 | 22.8 | | Q1:2021-22 | 1,281 | 13.3 | 17.6 | 69.1 | -4.3 | 39.7 | 5.1 | 55.2 | 34.7 | | Q2:2021-22 | | | | | | 42.4 | 3.8 | 53.7 | 38.6 | | ‘Improvement’ in availability of finance is optimistic. |

| Table 15: Assessment and Expectations for Availability of Finance (from banks and other sources) | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Improve | Worsen | No change | Net response | Improve | Worsen | No change | Net response | | Q1:2020-21 | 802 | 12.9 | 15.8 | 71.3 | -3.0 | 18.1 | 6.4 | 75.4 | 11.7 | | Q2:2020-21 | 959 | 20.3 | 8.3 | 71.4 | 12.0 | 20.4 | 9.8 | 69.8 | 10.6 | | Q3:2020-21 | 1,011 | 21.0 | 6.1 | 72.8 | 14.9 | 19.4 | 5.8 | 74.8 | 13.6 | | Q4:2020-21 | 967 | 23.1 | 6.6 | 70.3 | 16.5 | 19.6 | 4.3 | 76.1 | 15.3 | | Q1:2021-22 | 1,281 | 10.7 | 13.1 | 76.1 | -2.4 | 30.0 | 4.4 | 65.6 | 25.6 | | Q2:2021-22 | | | | | | 38.4 | 2.9 | 58.8 | 35.5 | | ‘Improvement’ in availability of finance is optimistic. |

| Table 16: Assessment and Expectations for Availability of Finance (from overseas, if applicable) | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Improve | Worsen | No change | Net response | Improve | Worsen | No change | Net response | | Q1:2020-21 | 802 | 3.2 | 13.5 | 83.3 | -10.3 | 7.9 | 4.0 | 88.1 | 4.0 | | Q2:2020-21 | 959 | 6.8 | 7.4 | 85.7 | -0.6 | 7.9 | 9.9 | 82.2 | -2.0 | | Q3:2020-21 | 1,011 | 5.8 | 5.0 | 89.2 | 0.8 | 7.2 | 6.6 | 86.1 | 0.6 | | Q4:2020-21 | 967 | 7.5 | 4.8 | 87.7 | 2.7 | 7.2 | 3.4 | 89.3 | 3.8 | | Q1:2021-22 | 1,281 | 13.6 | 12.0 | 74.5 | 1.6 | 16.5 | 3.1 | 80.3 | 13.4 | | Q2:2021-22 | | | | | | 44.0 | 1.3 | 54.7 | 42.7 | | ‘Improvement’ in availability of finance is optimistic. |

| Table 17: Assessment and Expectations for Cost of Finance | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q1:2020-21 | 802 | 16.3 | 15.9 | 67.8 | -0.4 | 12.7 | 6.6 | 80.6 | -6.1 | | Q2:2020-21 | 959 | 17.5 | 14.7 | 67.7 | -2.8 | 17.6 | 10.9 | 71.5 | -6.7 | | Q3:2020-21 | 1,011 | 13.3 | 13.5 | 73.2 | 0.2 | 15.5 | 8.8 | 75.7 | -6.7 | | Q4:2020-21 | 967 | 16.7 | 13.3 | 70.0 | -3.4 | 13.3 | 8.3 | 78.4 | -5.0 | | Q1:2021-22 | 1,281 | 15.7 | 11.3 | 73.0 | -4.5 | 22.2 | 8.2 | 69.6 | -13.9 | | Q2:2021-22 | | | | | | 34.9 | 3.3 | 61.8 | -31.5 | | ‘Decrease’ in cost of finance is optimistic. |

| Table 18: Assessment and Expectations for Cost of Raw Materials | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q1:2020-21 | 802 | 39.9 | 10.7 | 49.4 | -29.3 | 38.9 | 5.3 | 55.7 | -33.6 | | Q2:2020-21 | 959 | 46.1 | 8.2 | 45.7 | -38.0 | 37.8 | 5.7 | 56.5 | -32.0 | | Q3:2020-21 | 1,011 | 55.5 | 3.9 | 40.6 | -51.6 | 36.7 | 4.6 | 58.7 | -32.1 | | Q4:2020-21 | 967 | 71.0 | 2.0 | 26.9 | -69.0 | 45.2 | 2.6 | 52.2 | -42.7 | | Q1:2021-22 | 1,281 | 58.1 | 5.8 | 36.1 | -52.3 | 64.9 | 2.5 | 32.6 | -62.4 | | Q2:2021-22 | | | | | | 56.8 | 2.0 | 41.2 | -54.9 | | ‘Decrease’ in cost of raw materials is optimistic. |

| Table 19: Assessment and Expectations for Salary/Other Remuneration | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q1:2020-21 | 802 | 12.4 | 22.0 | 65.5 | 9.6 | 35.8 | 2.7 | 61.5 | -33.1 | | Q2:2020-21 | 959 | 15.7 | 12.9 | 71.4 | -2.8 | 16.5 | 12.5 | 70.9 | -4.0 | | Q3:2020-21 | 1,011 | 20.8 | 6.8 | 72.3 | -14.0 | 15.8 | 6.8 | 77.4 | -9.0 | | Q4:2020-21 | 967 | 21.8 | 3.1 | 75.1 | -18.7 | 19.9 | 3.9 | 76.2 | -16.0 | | Q1:2021-22 | 1,281 | 26.4 | 6.5 | 67.1 | -19.9 | 42.7 | 1.2 | 56.1 | -41.6 | | Q2:2021-22 | | | | | | 32.5 | 0.9 | 66.6 | -31.6 | | ‘Decrease’ in Salary / other remuneration is optimistic. |

| Table 20: Assessment and Expectations for Selling Price | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q1:2020-21 | 802 | 9.5 | 26.6 | 64.0 | -17.1 | 18.0 | 9.7 | 72.3 | 8.3 | | Q2:2020-21 | 959 | 13.9 | 19.7 | 66.4 | -5.8 | 12.9 | 18.9 | 68.1 | -6.0 | | Q3:2020-21 | 1,011 | 21.9 | 12.5 | 65.6 | 9.4 | 12.8 | 13.0 | 74.3 | -0.2 | | Q4:2020-21 | 967 | 31.3 | 8.6 | 60.1 | 22.7 | 19.6 | 8.9 | 71.5 | 10.7 | | Q1:2021-22 | 1,281 | 26.9 | 7.3 | 65.8 | 19.6 | 35.0 | 5.8 | 59.1 | 29.2 | | Q2:2021-22 | | | | | | 31.1 | 2.9 | 66.0 | 28.2 | | ‘Increase’ in selling price is optimistic. |

| Table 21: Assessment and Expectations for Profit Margin | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q1:2020-21 | 802 | 5.0 | 61.8 | 33.2 | -56.8 | 17.5 | 20.4 | 62.1 | -2.9 | | Q2:2020-21 | 959 | 15.3 | 41.8 | 43.0 | -26.5 | 13.7 | 40.5 | 45.8 | -26.8 | | Q3:2020-21 | 1,011 | 17.4 | 29.1 | 53.5 | -11.8 | 14.7 | 26.7 | 58.6 | -12.0 | | Q4:2020-21 | 967 | 24.9 | 22.9 | 52.1 | 2.0 | 17.8 | 20.1 | 62.1 | -2.4 | | Q1:2021-22 | 1,281 | 11.8 | 44.0 | 44.2 | -32.2 | 28.8 | 17.8 | 53.4 | 11.0 | | Q2:2021-22 | | | | | | 43.7 | 11.0 | 45.3 | 32.7 | | ‘Increase’ in profit margin is optimistic. |

| Table 22: Assessment and Expectations for Overall Business Situation | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Better | Worsen | No change | Net response | Better | Worsen | No change | Net response | | Q1:2020-21 | 802 | 8.3 | 68.5 | 23.2 | -60.2 | 38.6 | 10.4 | 50.9 | 28.2 | | Q2:2020-21 | 959 | 39.6 | 27.9 | 32.5 | 11.8 | 41.0 | 25.3 | 33.6 | 15.7 | | Q3:2020-21 | 1,011 | 46.7 | 13.8 | 39.6 | 32.9 | 45.7 | 12.8 | 41.6 | 32.9 | | Q4:2020-21 | 967 | 49.0 | 12.4 | 38.6 | 36.5 | 48.2 | 7.6 | 44.2 | 40.7 | | Q1:2021-22 | 1,281 | 18.6 | 39.2 | 42.3 | -20.6 | 57.7 | 5.1 | 37.2 | 52.5 | | Q2:2021-22 | | | | | | 59.9 | 7.5 | 32.5 | 52.4 | | ‘Better’ Overall Business Situation is optimistic. |

| Table 23: Business Sentiments | | Quarter | Business Assessment Index (BAI) | Business Expectations Index (BEI) | | Q1:2020-21 | 55.3 | 108.8 | | Q2:2020-21 | 96.2 | 99.5 | | Q3:2020-21 | 108.6 | 111.4 | | Q4:2020-21 | 113.1 | 114.1 | | Q1:2021-22 | 89.7 | 119.6 | | Q2:2021-22 | | 124.1 |

|

IST,

IST,