IST,

IST,

Monetary and Credit Information Review

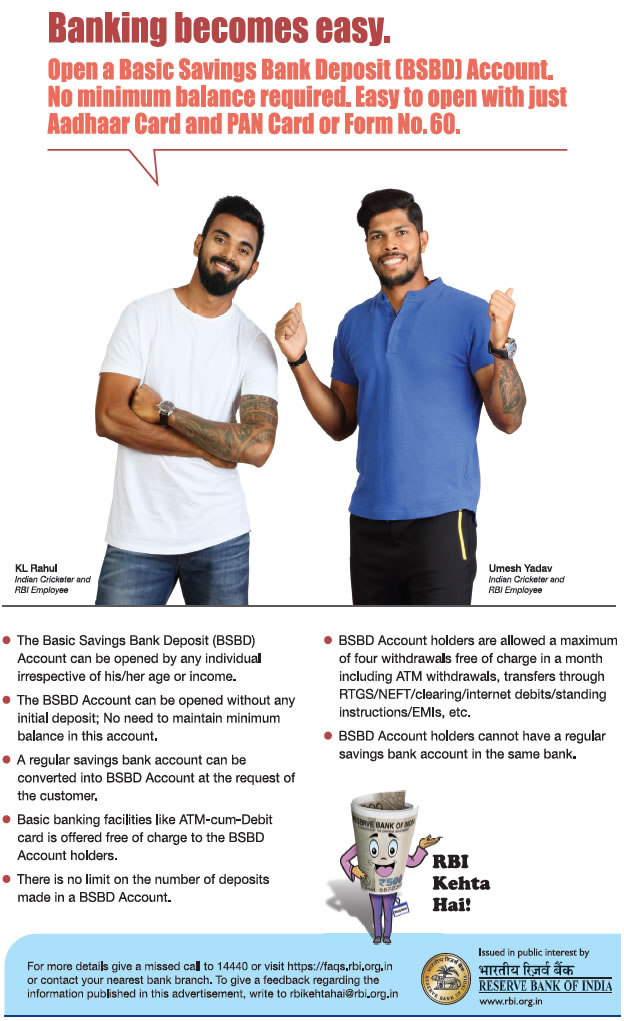

Volume XIV MONETARY AND CREDIT INFORMATION REVIEW Monetary Policy First Bi-monthly Monetary Policy Statement, 2018-19 Resolution of the MPC On the basis of an assessment of the current and evolving macroeconomic situation at its meeting on April 5, 2018, the Monetary Policy Committee (MPC) decided to keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 6.0 per cent. Consequently, the reverse repo rate under the LAF remains at 5.75 per cent, and the marginal standing facility (MSF) rate and the Bank Rate at 6.25 per cent. The decision of the MPC is consistent with the neutral stance of monetary policy in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. (/en/web/rbi/-/press-releases/first-bi-monthly-monetary-policy-statement-2018-19-resolution-of-the-monetary-policy-committee-mpc-reserve-bank-of-india-43573) Statement on Developmental and Regulatory Policies Mandatory Loan Component in Working Capital Finance With a view to promoting greater credit discipline among working capital borrowers, it is proposed to stipulate a minimum level of ‘loan component’ in fund based working capital finance for larger borrowers. Countercyclical Capital Buffer Based on the review and empirical testing of countercyclical capital buffer (CCCB) indicators, it has been decided that it is not necessary to activate CCCB at this point in time. Deferment of Ind AS Implementation Pending the necessary legislative amendments – to make the format of financial statements, prescribed in the Third Schedule to Banking Regulation Act 1949, compatible with accounts under Ind AS – under consideration of the Government, and the level of preparedness of many banks, it has been decided to defer implementation of Ind AS by one year from April 1, 2018 by when the necessary legislative changes are expected. Access for Non-residents into the IRS Market With a view to develop a deep Rupee Interest Rate Swap (IRS) market that accommodates divergent participants, it is proposed to permit non-residents access to the Rupee IRS market in India. Introduction of Rupee Swaptions It is proposed to permit interest rate swaptions in Rupees so as to enable better timing flexibility for those seeking to hedge interest rate risk. Review of STRIPS Directions With a view to encouraging trading in Separate Trading of Registered Interest and Principal Securities (STRIPS) in Government Securities by making it more aligned with market requirements and to meet the diverse needs of the investors, it is proposed to review the STRIPS guidelines. LEI Mechanism for Non-individual Market Participants Continuing with the endeavour to improve transparency in financial markets, it is proposed to implement the Legal Entity Identifier (LEI) mechanism for all financial market transactions undertaken by non-individuals, in interest rate, currency or credit markets. Single Master Form for FDI Reporting The Reserve Bank plans to introduce an online reporting by June 30, 2018 via a Single Master Form which would subsume all reporting requirements, irrespective of the instrument through which the foreign investment is made. Creation of the Reserve Bank Data Sciences Lab It is critical for a full-service central bank, such as, the Reserve Bank of India, with diverse responsibilities – inflation management, currency management, debt management, reserves management, banking regulation and supervision, financial inclusion, financial market intelligence and analysis, and overall financial stability– to employ relevant data and apply the right filters for improving its forecasting, nowcasting, surveillance and early-warning detection abilities that aid policy formulation. In the backdrop of ongoing explosion in information gathering, computing capability and analytical toolkits, policy making benefits not only from data collected through regulatory returns and surveys but also from large volumes of structured and unstructured real-time information sourced from consumer interactions in the digital world. Accordingly, it has been decided to gainfully harness the power of Big Data analytics by setting up a Data Sciences Lab within the Reserve Bank that will comprise experts and budding analysts, internal as well as lateral, who are trained, inter-alia, in Computer Science, Data Analytics, Statistics, Economics, Econometrics and/ or Finance. It is envisaged that the unit will become operational by December 2018. (/en/web/rbi/-/press-releases/statement-on-developmental-and-regulatory-policies-43574) Financial Inclusion and Development Revamp of Lead Bank Scheme Apropos deliberation on the recommendations of the Committee of Executive Directors’ with various stakeholders and based on their feedback, the Reserve Bank on April 6, 2018 decided that the following ‘action points’ will be implemented by the State Level Bankers’ Committee (SLBC) Convener Banks/Lead Banks- • SLBC meetings should primarily focus on policy issues with participation of only the senior functionaries of the banks/ Government Departments. All routine issues may be delegated to sub-committee(s) of the SLBC. A Steering Sub-committee may be constituted in the SLBC to deliberate on agenda proposals from different stakeholders and finalise a compact agenda for the SLBC meetings. Typically, the Sub-Committee could consist of SLBC Convenor, Reserve Bank of India (RBI) and National Bank for Agriculture and Rural Development (NABARD) representatives and senior State Government representative from the concerned department, such as, Finance/Institutional Finance and two to three banks having major presence. Other issue-specific sub-committees may be constituted as required. • In cases where the Managing Director/Chief Executive Officer/Executive Director of the SLBC Convenor Bank is unable to attend SLBC Meetings, the Regional Director of the Reserve Bank shall co-chair the meetings along with the Additional Chief Secretary/Development Commissioner of the State concerned. • The corporate business targets for branches, blocks, districts and states may be aligned with the Annual Credit Plans (ACP) under the Lead Bank Scheme to ensure better implementation. The Controlling Offices of the banks in each state should synchronise their internal business plans with the ACP under Lead Bank Scheme. • At present, discussions at the Quarterly Meetings of the various LBS fora namely, State Level Bankers’ Committee (SLBC), District level Consultative Committee (DCC) and Block Level Bankers’ Committee (BLBC) primarily focuses on the performance of banks in the disbursement of loans with regard to the allocated target under the Annual Credit Plan. The integrity and timeliness of the data submitted by banks for the purpose has been an issue as a significant portion of this data is manually compiled and entered into the Data Management Systems of the SLBC Convener Banks. The extent to which this data corresponds with the data present in the Core Banking Solution (CBS) of the respective banks also varies significantly. Therefore, there is need for a standardised system to be developed on the website maintained by each SLBC to enable uploading and downloading of the data pertaining to the Block, District as well as the State. The relevant data must also be directly downloadable from the CBS and/ or Management Information System (MIS) of the banks with a view to keeping manual intervention to a minimal level in the process. Necessary modifications may be made on the SLBC websites and to the CBS and MIS systems of all banks to implement the envisaged data flow mechanism. • To strengthen the BLBC forum which operates at the base level of the Lead Bank Scheme, it is necessary that all branch managers attend BLBC meetings and enrich the discussions with their valuable inputs. Controlling Heads of banks may also attend a few of the BLBC meetings selectively. • Rural Self Employment Training Institutes (RSETIs) should be more actively involved and monitored at various fora of LBS particularly at the DCC level. Focus should be on development of skills to enhance the credit absorption capacity in the area and renewing the training programmes towards sustainable micro enterprises. RSETIs should design specific programmes for each district/ block, keeping in view the skill mapping and the potential of the region for necessary skill training and skill up gradation of the rural youth in the district. (/en/web/rbi/-/notifications/revamp-of-lead-bank-scheme-action-points-for-slbc-convenor-banks-lead-banks-11246) RBI releases Customised Financial Literacy Content Shri B. P. Kanungo, Deputy Governor, Reserve Bank released the customised financial literacy content, meant for five select target groups, in the form of five booklets on April 18, 2018. Financial Inclusion and Development Department, developed the customised content for use by the trainers in financial literacy programmes, meant for farmers, small entrepreneurs, school children, self-help groups and senior citizens. The content is available for download on the financial education webpage of the Reserve Bank (/en/web/rbi/financial-education). A ticker titled financial awareness messages on the home page of the Reserve Bank leads to the financial education webpage wherein the books have been hyperlinked to the third paragraph with a ‘New’ flash message. The entire material prepared in Hindi and English will also be translated in other Indian languages in due course and uploaded on the financial education website of the Reserve Bank. Financial Literacy Centres (FLCs) of banks may structure the pedagogy for the mandated target specific financial literacy camps with the help of the five books. Action Points to Enhance Effectiveness of LDMs In view of the changes that have taken place in the financial sector over the years, Reserve Bank of India had constituted a “Committee of Executive Directors” of the Reserve Bank to study the efficacy of the Scheme and suggest measures for improvement. The Committee’s recommendations were discussed with various stakeholders and based on their feedback, the Reserve Bank on April 6, 2018 decided that the following ‘action points’ will be implemented by the Lead Banks. • In view of the critical role played by Lead District Managers (LDMs), it may be ensured that officials posted as LDMs possess requisite leadership skills. • Apart from the provision of a separate office space, technical infrastructure like computers, printer, data connectivity, etc., which are basic necessities for LDMs to discharge their core responsibilities may be provided to LDMs’ Office without exception. • It is suggested that a dedicated vehicle may be provided to LDMs to facilitate closer liaison with the bank officials, district administration officials as also to organise/attend various financial literacy initiatives and meetings. • The absence of a specialist officer/assistant for data entry/ analysis is a common and major issue faced by LDMs. Liberty to hire the services of skilled computer operator may be given to the LDMs to overcome the shortage of staff/ in case appropriate staff is not posted at LDM office. Banks are advised to take appropriate action as required. Further, for successful functioning of the Lead Bank Scheme, the Reserve Bank expects Lead Banks to go the extra mile to provide facilities over and above the bare minimum to these critical field functionaries. (/en/web/rbi/-/notifications/action-points-for-lead-banks-on-enhancing-the-effectiveness-of-lead-district-managers-ldms-11247) Banking Regulation Creation of IFR With a view to addressing the systemic impact of sharp increase in the yields on Government Securities, the Reserve Bank on April 2, 2018 decided to grant banks the option to spread provisioning for Mark to Market (MTM) losses on investments held in Available for Sale (AFS) and Held for Trading (HFT) for the quarters ended December 31, 2017 and March 31, 2018. The provisioning for each of these quarters may be spread equally over up to four quarters, commencing with the quarter in which the loss is incurred. Banks that utilise the above option shall make suitable disclosures in their notes to accounts/ quarterly results providing details of - • the provisions for depreciation of the investment portfolio for the quarters ended December 2017 and March 2018 made during the quarter/year and, • the balance required to be made in the remaining quarters. Further, with a view to building up of adequate reserves to protect against increase in yields in future, all banks are advised to create an Investment Fluctuation Reserve (IFR) with effect from the year 2018-19, as under: An amount not less than the lower of the following: • net profit on sale of investments during the year • net profit for the year less mandatory appropriations shall be transferred to the Investment Fluctuation Reserve (IFR), until the amount of IFR is at least 2 per cent of the HFT and AFS portfolio, on a continuing basis. Where feasible, this should be achieved within a period of 3 years. A bank may, at its discretion, draw down the balance available in IFR in excess of 2 per cent of its HFT and AFS portfolio, for credit to the balance of profit/loss as disclosed in the profit and loss account at the end of any accounting year. In the event the balance in the IFR is less than 2 per cent of the HFT and AFS investment portfolio, a draw down will be permitted subject to the following conditions: • The drawn down amount is used only for meeting the minimum CET1/Tier 1 capital requirements by way of appropriation to free reserves or reducing the balance of loss, and • The amount drawn down is not more than the extent the MTM provisions made during the aforesaid year exceed the net profit on sale of investments during that year. IFR shall be eligible for inclusion in Tier 2 capital. (/en/web/rbi/-/notifications/prudential-norms-for-classification-valuation-and-operation-of-investment-portfolio-by-banks-spreading-of-mtm-losses-and-creation-of-investment-fluctuation-reserve-ifr-11236) Comprehensive Guidelines on Derivatives The Reserve Bank on April 6, 2018 decided that stand-alone plain vanilla forex options (without attached structures) purchased by clients will be exempt from the ‘user suitability and appropriateness’ norms, and the regulatory requirements will be at par with forex forward contracts. (/en/web/rbi/-/notifications/comprehensive-guidelines-on-derivatives-modifications-11242) Foreign Exchange Management LRS for Resident Individuals In order to improve monitoring and also to ensure compliance with the Liberalised Remittance Scheme (LRS) limits, the Reserve Bank on April 12, 2018 decided to put in place a daily reporting system by Authorised Dealers (AD) banks of transactions undertaken by individuals under LRS, which will be accessible to all the other ADs. Accordingly, from the date of issue of this circular, all AD Category-I banks are required to upload daily transaction-wise information undertaken by them under LRS at the close of business of the next working day. In case no data is to be furnished, AD banks shall upload a ‘Nil’ report. AD banks can upload the LRS data as CSV file (comma delimited), by accessing XBRL. (/en/web/rbi/-/notifications/liberalised-remittance-scheme-lrs-for-resident-individuals-daily-reporting-of-transactions-11255) Investment by FPI in Government Securities - Review After consultation with the Government of India, the Reserve Bank of India on April 6, 2018 revised the Foreign Portfolio Investors (FPI) limits as under: Revision of Investment Limits • The limit for FPI investment in Central Government securities (G-secs) would be increased by 0.5 per cent each year to 5.5 per cent of outstanding stock of securities in 2018-19 and 6 per cent of outstanding stock of securities in 2019-20. • The limit for FPI investment in State Development Loans (SDLs) would remain unchanged at 2 per cent of outstanding stock of securities. • The overall limit for FPI investment in corporate bonds will be fixed at 9 per cent of outstanding stock of corporate bonds. All the existing sub-categories under the category of corporate bonds will be discontinued and there would be a single limit for FPI investment in all types of corporate bonds. • No fresh allocation has been made to the ‘Long-term’ sub-category under SDLs. Out of the existing limit of ₹ 13,600 crore for this sub-category, an amount of ₹ 6,500 crore has been transferred to the G-secs category. • The allocation of increase in G-sec limit over the two sub-categories – ‘General’ and ‘Long-term’ – remains at the current ratio of 25:75. However, based on an assessment of investment interest, this ratio has been re-set at 50:50 for the year 2018-19. • Coupon reinvestment by FPIs in G-secs, which was hitherto outside the investment limit, will now be reckoned within the G-sec limits. FPIs may, however, continue to reinvest coupons without any constraint, as they do now. Only at the time of periodic re-setting of limits, coupon investments would be added to the amount of utilisation. Accordingly, for the year 2018-19, the stock of coupon investment of ₹ 4,760 crore as on March 31, 2018, would be added to the actual utilisation under the ‘General’ sub-category of G-secs. Since this is a new policy, as a one-time measure, the investment limit in the ‘General’ sub-category of G-secs has been increased by an amount equal to the stock of coupon reinvestment as on March 31, 2018. This increase in limit on account of coupon investment amount is over and above the limit indicated earlier. • This coupon reinvestment arrangement will be extended to other debt categories subsequently. Accordingly, the limits for the various categories, after rounding off, would be revised. (/en/web/rbi/-/notifications/investment-by-foreign-portfolio-investors-fpi-in-government-securities-medium-term-framework-review-11241) Prohibition on dealing in VCs In view of the associated risks, the Reserve Bank on April 6, 2018 decided that, with immediate effect, entities regulated by the Reserve Bank shall not deal in Virtual Currencies (VCs) or provide services for facilitating any person or entity in dealing with or settling VCs. Such services include maintaining accounts, registering, trading, settling, clearing, giving loans against virtual tokens, accepting them as collateral, opening accounts of exchanges dealing with them and transfer / receipt of money in accounts relating to purchase/ sale of VCs. Regulated entities which already provide such services shall exit the relationship within three months from the date of this circular. (/en/web/rbi/-/notifications/prohibition-on-dealing-in-virtual-currencies-vcs-11243) Payment and Settlement System Storage of Payment System Data In order to ensure better monitoring, it is important to have unfettered supervisory access to data stored with these system providers as also with their service providers /intermediaries/third party vendors and other entities in the payment ecosystem. The Reserve Bank on April 6, 2018 decided that: • All system providers shall ensure that the entire data relating to payment systems operated by them are stored in a system only in India. This data should include the full end-to-end transaction details/information collected/carried/processed as part of the message/payment instruction. For the foreign leg of the transaction, if any, the data can also be stored in the foreign country, if required. • System providers shall ensure compliance within a period of six months and report compliance of the same to the Reserve Bank latest by October 15, 2018. • System providers shall submit the System Audit Report (SAR) on completion. The audit should be conducted by CERT-IN empaneled auditors certifying completion of activity. The SAR duly approved by the Board of the system providers should be submitted to the Reserve Bank not later than December 31, 2018. In recent times, there has been considerable growth in the payment ecosystem in the country. Such systems are also highly technology dependent, which necessitate adoption of safety and security measures, which are best in class, on a continuous basis. It is observed that not all system providers store the payments data in India. (/en/web/rbi/-/notifications/storage-of-payment-system-data-11244) Currency Management Cash Management Activities of Banks - Standards The Reserve Bank on April 6, 2018 advised banks to put in place certain minimum standards in their arrangements with the service providers for cash management related activities. Banks are advised to review their existing outsourcing arrangements and bring them in line with these instructions within 90 days from the date of this circular. As the cash held with the service providers and their sub-contractors continue to remain the property of the banks and the banks are liable for all associated risks, the banks shall put in place appropriate business continuity plan approved by their boards to deal with any related contingencies. In view of the increasing reliance of the banks on outsourced service providers and their sub-contractors in cash management logistics, certain minimum standards will be prescribed for the service provider / sub-contractors who are engaged by the banks for this purpose. (/en/web/rbi/-/notifications/cash-management-activities-of-the-banks-standards-for-engaging-the-service-provider-and-its-sub-contractor-11245) Cassette - Swaps in ATMs The recommendations of the Committee on Currency Movement (CCM) have been examined and in order to mitigate risks involved in open cash replenishment/ top-up, the Reserve Bank on April 12, 2018 advised banks to consider using lockable cassettes in their ATMs which shall be swapped at the time of cash replenishment. This may be implemented in a phased manner covering at least one - third ATMs operated by the banks every year, such that all ATMs achieve cassette swap by March 31, 2021. The banks are required to furnish a quarterly report to the Issue Department of the Regional Office under whose jurisdiction their Head Office is situated, within 15 days of the close of every quarter commencing June 30, 2018 by email. The Reserve Bank had constituted a Committee on Currency Movement (CCM) [Chair: Dr D.K. Mohanty, Executive Director] to review the entire gamut of security of the treasure in transit. (/en/web/rbi/-/notifications/cassette-swaps-in-atms-11256) Mint Street Memos Impact of Increase in HRA on CPI Inflation The Reserve Bank on April 23, 2018 uploaded on the RBI website the eleventh in the series of Mint Series Memos on ‘Impact of Increase in House Rent Allowance on CPI Inflation’ by Praggya Das. This paper studies the impact of increase in house rent allowance (HRA), following recommendations of the 7th Central Pay Commission (CPC), on headline inflation and comes up with the following suggestions: (i) For the future base revisions, while preparing fixed sample of dwellings for each State for collecting house rent data, representative share of government houses that reflect the actual share of Central and State government houses in the States may be kept; and (ii) As States’ impact unfolds going forward, for the existing series, housing index may be published separately for the government dwellings and other dwellings. (/en/web/rbi/-/impact-of-increase-in-house-rent-allowance-on-cpi-inflation) RBI Kehta Hai: BSBD Accounts The Reserve Bank, on April 19, 2018, launched the renewed public awareness campaign. To start with, print and audio-visual creatives on Basic Savings Bank Deposit (BSBD) accounts were released. Film on BSBD Accounts As part of the campaign, the Reserve Bank, has started airing a video spot on opening BSBD Accounts, during the current IPL matches. The spots are being aired on Star Sports and Doordarshan, channels that have exclusive telecast rights for IPL matches. The film is available on YouTube channel https://www.youtube.com/watch?v=bh3vS2BJBNI&sns=em to create public awareness. Coming Soon: * ₹ 10 Coins *Know Your Liability *Safeguards for Digital Banking *Senior Citizens *Banking Ombudsman Scheme *Risk vs.Return  Edited and published by Jose J. Kattoor for the Reserve Bank of India, Department of Communication, Central Office, Shahid Bhagat Singh Marg, Mumbai - 400 001. MCIR can be accessed at https://mcir.rbi.org.in |

شارك هذه الصفحة:

بھارت موبائل ایپلی کیشن کے ریزرو بینک کو انسٹال کریں اور تازہ ترین خبروں تک فوری رسائی حاصل کریں!

ہماری ایپ انسٹال کرنے کے لیے QR کوڈ اسکین کریں۔

صفحے پر آخری اپ ڈیٹ: