IST,

IST,

Non-Banking Financial Institutions (Part 2 of 6)

crore and up to Rs.10 crore' and ‘Rs.50 crore and above’. Significantly, the share of the deposit class ‘Rs.50 crore and above’ in total deposits was 82 per cent, while that of other deposit classes combined together was only about 18 per cent of total public deposits of the NBFC sector. Region-wise Composition of Deposits held by NBFCs 6.56 Following the trend of the previous year, deposits held by NBFCs across all the regions declined during 2007-08 (Table VI.19). As in the previous year, the southern region accounted for the largest share of

deposits (80 per cent), followed by the northern region (14 per cent) and the western region (4.1 per cent). The presence of NBFCs in the north-eastern region continued to be nil during the year. Among the metropolitan cities, Chennai continued to hold the largest share of deposits, while New Delhi continued to account for the largest number of NBFCs. Interest Rate on Public Deposits with NBFCs 6.57 The share of deposits contracted by NBFCs in the interest rates up to 10 per cent declined (from 88.5 per cent to 73.1 per cent), while those contracted in the bracket ‘more than 10 per cent and up to 12 per cent’ witnessed a sharp rise (from 9.7 per cent to 25.4 per cent), partly reflecting the hardening of interest rates during the year (Table VI.20).

Maturity Pattern of Public Deposits 6.58 Deposits with the maturity period of 'less than 1 year', 'more than 3 years and up to 5 years' and '5 years and above' declined during the year. Deposits in the maturity bucket of ‘more than 1 years and up to 2 years’ increased marginally, while deposits in the maturity bucket of ‘ more than 2 years and up to 3 years’ increased significantly at end-March 2008. As a result, their share in total deposits increased (Table VI.21).

Borrowings by NBFCs 6.59 The outstanding borrowings by NBFCs increased by 55.3 per cent during 2007-08 (Table VI.22). Borrowings by equipment

leasing and hire purchase companies declined, while those by loan companies, investment companies and asset finance companies increased during the year partly reflecting the reclassification of NBFCs. AFCs continued to hold the largest share (64.4 per cent) of borrowings of all NBFCs, followed by loan companies (27.7 per cent). 6.60 Borrowings by NBFCs from banks and financial institutions and by way of bonds and debentures and ‘other sources’ (which include miscellaneous factors including inter alia, money borrowed from other companies, unsecured loans from directors/ promoters, commercial paper, borrowings from mutual funds and any other type of funds which are not treated as public deposits), increased sharply during 2007-08. This broadly reflected the pattern of borrowings of asset finance companies (Table VI.23). Significantly, the borrowing from Government, which was nil during 2006-07, increased sharply to Rs.2,319 crore during 2007-08 largely due to inclusion of IFCI Ltd. and TFCI Ltd. in this category.

Assets of NBFCs 6.61 The sharp increase in assets of deposit-taking NBFCs was mainly on account of increase in assets of asset finance companies and loan companies. Loans and advances as well as investments of NBFCs also increased during the year (Table VI.24). At end-March 2008, 64.1 percent of assets, 71.2 per cent of total loans and advances and 34.5 per cent of investments by all NBFCs were held by asset finance companies.

Distribution of NBFCs-D According to Asset Size 6.62 The asset size of NBFCs varies significantly from less than Rs.25 lakh to above Rs.500 crore. The asset holding pattern remained skewed in 2007-08, with fifteen NBFCs with asset size of ‘above Rs.500 crore’ holding 94.9 per cent of total assets of all NBFCs, while the remaining 318 NBFCs held about 5.1 per cent of total assets at end-March 2008 (Table VI.25).

Distribution of Assets of NBFCs – Type of Activity 6.63 While assets held in the form of equipment and leasing witnessed a sharp decline during 2007-08, assets in the form of loans and inter-corporate deposits as also other assets witnessed a sharp growth. Assets in the form of loans and bills, which had witnessed a decline during 2006-07, increased sharply by 39.8 per cent. Assets held in the hire purchase activity as well as investment activity, however witnessed a deceleration. The hire purchase activity continued to constitute the largest share (46.7 per cent) in total assets, followed by loans and inter-corporate deposits (28.3 per cent) and investments (16.4 per cent) (Table VI.26).

Financial Performance of NBFCs 6.64 Financial performance of NBFCs continued to improve during 2007-08. Both fund based income (79.8 per cent) and fee based income (56.6 per cent) increased sharply. As a result, even though expenditure witnessed an increase of 45.4 per cent, operating profits increased by 263.2 per cent and net profits by 298.3 per cent. The cost to income ratio declined sharply (to 68.5 per cent in 2007-08 from 84.4 per cent in 2006-07) (Table VI.27).

6.65 Out of the total cost incurred by NBFCs, the non-interest cost continued to constitute the largest share (94. 5 per cent in 2007-08 as compared with 89.5 per cent in 2006-07). The interest cost constituted a smaller share of the total cost (Table VI. 28).

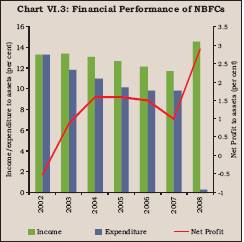

6.66 While income as percentage of assets increased, expenditure (including provisions) as percentage of assets declined sharply, resulting in a rise in the net profits to asset ratio (Chart VI.3). Soundness Indicators Asset Quality of NBFCs-D 6.67 Continuing the trend witnessed during the last few years, gross NPAs as well as net NPAs (as percentage of gross advances and net advances, respectively) of reporting NBFCs declined further during the year ended March 2008 (Table VI.29).

6.68 Gross NPAs (as percentage of gross advances) of equipment leasing and hire purchase companies increased during 2007-08, due to reclassification of NBFCs, while those of asset finance companies and loan companies declined. Net NPAs (as percentage of net advances) increased marginally in case of asset finance companies, hire purchase companies and investment companies, while those of equipment leasing companies, and loan companies improved further (Table VI.30).

6.69 Asset quality of various types of NBFCs as reflected in various categories of NPAs (substandard, doubtful and loss) remained broadly at the previous year’s level. The sharp increase in the standard assets of asset finance companies and the corresponding sharp decline in the case of equipment leasing companies and hire purchase companies was mainly due to the reclassification of NBFCs (Table VI.31).

Capital Adequacy Ratio 6.70 Capital to risk-weighted assets ratio (CRAR) norms were made applicable to NBFCs in 1998, in terms of which every deposit-taking NBFC is required to maintain a minimum capital, consisting of Tier-I and Tier-II capital, of not less than 12 per cent (15 per cent in the case of unrated deposit-taking loan/investment companies) of its aggregate risk-weighted assets and of risk-adjusted value of off-balance sheet items. Total of Tier-II capital, at any point of time, cannot exceed 100 per cent of Tier-I capital. The number of NBFCs with less than the minimum regulatory CRAR of 12 per cent increased to 44 at end-March 2008 from 20 at end-March 2007 (Table VI.32). At end-March 2008, 276 out of 320 NBFCs had CRAR of 12 per cent or more as against 354 out of 374 NBFCs at end-March 2007. The number of NBFCs with CRAR more than 30 also declined to 238 at end-March 2008 from 305 at end-March 2007. Notwithstanding this, it is noteworthy that the NBFC sector is witnessing a consolidation process in the last few years, wherein the weaker NBFCs are gradually exiting, paving the way for a stronger NBFC sector. 6.71 Net owned fund (NOF) of NBFCs is the aggregate of paid-up capital and free reserves, netted by (i) the amount of accumulated losses; and (ii) deferred revenue expenditure and other intangible assets, if any, and

adjusted by investments in shares, and loans and advances to (a) subsidiaries, (b) companies in the same group, and (c) other NBFCs (in excess of 10 per cent of owned fund). Information about NOF can complement the information on CRAR. The ratio of public deposits to NOF in the case of loan companies and MNBCs declined during the year ended March 2008, while that of other category companies witnessed a marginal increase. The ratio of equipment leasing companies continued to be negative because of negative net owned funds, although there was some moderation. The ratio of public deposit to NOF for all categories of NBFCs taken together was 0.2 per cent at end-March 2008 as compared with 0.3 per cent at end-March 2007 (Table VI.33).

6.72 Net owned funds of NBFCs range from less than Rs.25 lakh to above Rs.500 crore. Public deposits, as ratio of NOF, held by NBFCs in the category of NOF of ‘more than Rs.2 crore and up to Rs.10 crore’, ‘more than Rs.50 crore and upto Rs.100 crore' and 'above Rs.500 crore' remained constant, while those by NBFCs in all other ranges of NOF generally declined except in the case of the category ‘more than Rs.100 crore and upto Rs.500 crore’ (Table VI.34).

Residuary Non-Banking Companies (RNBCs) 6.73 Assets of the RNBCs increased by 5.5 per cent during the year ended March 2008. Their assets in the form of unencumbered approved securities declined, while those in bonds/debentures and fixed deposits/ certificates of deposit of SCBs registered an increase. Net owned funds of RNBCs increased by 25.5 per cent during 2007-08 on top of the rise of 15.5 per cent witnessed during 2006-07 (Table VI.35).

6.74 In continuation of the trend witnessed in 2006-07, the increase in income of RNBCs during 2007-08 was more than the increase in expenditure, as a result of which the operating profit of RNBCs increased sharply. Even though the provision for taxation also registered a sharp rise, the net profit of RNBCs increased by 86.9 per cent during 2007-08 as compared with 27.5 per cent during 2006-07. Regional Pattern of Deposits of RNBCs 6.75 Of the two RNBCs, one is based in the Eastern region (Kolkata) and the other in the Central region. The public deposits held by RNBCs in both the Eastern region and Central region registered a marginal decline. Of the four metropolitan cities, RNBCs held public deposits only in one metropolitan city, i.e., Kolkata (Table VI.36).

Investment Pattern of RNBCs 6.76 The investment pattern of RNBCs as prescribed in the Residuary Non-Banking (Reserve Bank) Directions, 1987 was reviewed and modified on March 31, 2006. The aggregate liability to depositor (ALD) was bifurcated under two heads, viz., aggregate liability to depositor (ALD) as on December 31, 2005 and incremental ALDs. Incremental ALDs are the liabilities to the depositors exceeding the aggregate amount of the liabilities to the depositors as on December 31, 2005. RNBCs were advised to invest, with effect from April 1, 2006, not less than 95 per cent of the ALD as on December 31, 2005 and the entire incremental ALD in the prescribed manner. RNBCs were also advised that on and from April 1, 2007, the entire amount of ALD would be invested in directed investments only and no discretionary investment would be allowed to be made by them. 6.77 Aggregate liability to depositor (ALD) declined marginally by 1.7 per cent during 2007-08. While fixed deposits with banks and bonds and debentures increased, unencumbered approved securities and other investments registered a decline (Table VI.37).

Non-Deposit Taking Systemically Important Non-Banking Finance Companies (NBFCs - ND - SI) 6.78 Information based on the returns received from non-deposit taking systemically important NBFCs (with asset size of Rs.100 crore and above) for the year ended March 2008 showed an increase of 28.6 per cent in their liabilities/assets over the year ended March 2007. Unsecured loans continued to constitute the single largest source of funds for NBFCs-ND-SI, followed by secured loans and reserves and surplus (Table VI.38).

Borrowings 6.79 Total borrowings (secured and unsecured) by NBFCs-ND-SI increased by 28.0 per cent to Rs.2,71,288 crore during the year ended March 2008, constituting 66.4 per cent of their total liabilities. During the quarter ended June 2008, the total borrowings increased further by 3.0 per cent to Rs.2,79,491 crore (Table VI.39).

Application of Funds 6.80 The pattern of application of funds by NBFCs-ND-SI during the year ended March 2008 remained broadly in line with the pattern witnessed during the previous year. The secured loans continued to constitute the largest share (44.7 per cent), followed by unsecured loans with a share of 24.8 per cent (Table VI.40).

Financial Performance 6.81 NBFCs-ND-SI earned a profit of Rs.8,705 crore during the year ended March 2008, which was higher by 16.7 per cent as compared with the profit earned during the year ended March 2007 (Rs.7,460 crore) (Table VI.41).

6.82 The gross NPAs to total assets ratio of NBFCs-ND-SI remained unchanged at 2.3 per cent for the year ended March 2008 and also for the quarter ended June 2008. The net NPAs to total assets ratio increased from 1.5 per cent as at end March 2007 to 1.6 per cent as at end March 2008, but declined to 1.4 per cent during the quarter ended June 2008 (Table VI.42).

4. Primary Dealers 6.83 In order to strengthen the market infrastructure of Government securities market and make it vibrant, liquid and broad-based, the primary dealers (PDs) system was introduced by Reserve Bank in 1995. The PD system is designed to facilitate Government's market borrowing programme and improve the secondary market trading system by contributing to price discovery, enhancing liquidity and turnover and encouraging voluntary holding of Government securities amongst a wider investor base. The PD system developed significantly over the years and currently it serves as an effective conduit for conducting open market operations. 6.84 The PD system continued to

play a significant role in the Government securities market during the year 2007-08.

The number of PDs increased to 19 at end-March 2008 as compared with 17

at the end-March 2007. Of these 19 entities, 10 were banks undertaking PD business

departmentally (Bank-PDs) and the remaining nine were stand-alone, non-bank entities.

HDFC Bank Limited was authorised to take up PD business with effect from April

2, 2007 and one new stand-alone PD, viz., Lehman Brothers Fixed Income

Securities Pvt. Limited (LBFISL), was also authorised to undertake PD business

with effect from November 1, 2007. However, following the filing of a petition

under Chapter 11 of the US Bankruptcy code by Lehman Brothers Holding Inc. in

the US, the Reserve Bank announced certain measures in public interest and in

the interest of financial stability. As such, LBFISL was advised not to declare

any interim dividend or remit any amount to its holding company or any other group

company without prior approval of the Reserve Bank. Further, they were advised

not to undertake transactions in Government securities as a PD in the primary

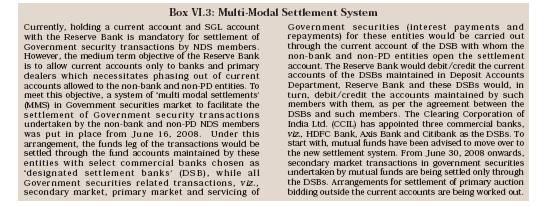

market. 6.86 The Reserve Bank initiated steps to phase out current account facility allowed to the non-bank and non-PD entities. The establishment of Multi Modal Settlements (MMS) system was a major step in this regard (Box VI.3) 6.87 In recent years, the non-competitive bidding facility has been receiving good response. The Working Group on Auction Process of Government of India Securities (Chairman: H.R. Khan), which submitted its report in March 2008, made several important recommendations regarding the non-competitive bidding facility (Box VI.4). 6.88 The bidding commitment of PDs in the underwriting auction of dated Government of India securities was revised from the earlier stipulation of a minimum of 3 per cent of the notified amount to an amount equal to the minimum underwriting commitment (MUC) with effect from November 22, 2007. Operations and Performance of PDs 6.89 A significant portion of the market demand for Government securities in the primary market emanates from the PDs. The aggregate bids submitted by the PDs in the auctions of Treasury Bills and dated securities, as reflected in the bid-cover ratio, tended to increase in recent years in tandem with the increase in issuances. The PDs also maintained a dominant share of over 45 per cent in primary auction allotments. 6.90 During 2007-08, cumulative bidding commitments in Treasury Bills auctions were fixed to ensure that PDs bid for the notified amount. The aggregate bids at Rs.3,18,201 crore were, however, much higher at 3.04 times of the aggregate commitment of Rs.1,04,385 crore (under the regular borrowing programme). Bids amounting to Rs.1,04,819 crores were accepted in Treasury Bill auctions. PDs are required to achieve a success ratio of 40 per cent of bidding commitment in respect of Treasury Bill auctions on a half-yearly basis. While the PDs achieved a success ratio of 94.43 per cent during the year 2006-07, the achievement during 2007-08 was higher at 100.42 per cent. The PDs’ share in the primary auctions of Treasury Bills increased to 48 per cent during 2007-08 from 38 per cent during 2006-07. 6.91 In terms of the Fiscal Responsibility and Budget Management Act, 2003, the Reserve Bank was prohibited from participating in the primary auctions of Central Government securities. The PDs were, therefore, enjoined to underwrite the entire notified amount in the auctions of dated Government of India securities. During 2007-08, the PDs offered to underwrite the auctions of Central Government dated securities to the extent of Rs.2,76,518 crore as against the notified amount of Rs.1,56,000 crore. This represented a bid-cover ratio of 1.77 in underwriting auctions. Of the total thirty five primary auctions of dated securities held during the year, there was a devolvement of Rs.957 crore on PDs in one auction. 6.92 The actual bids tendered by the PDs (Rs.2,54,253 crore) in the auction of dated securities were 1.6 times of the notified amount. Of the total bids made by PDs in dated securities, bids worth Rs.72,122 crore were accepted. The success ratio at 46.2 per cent was a marginal increase over 44.3 per cent during the period 2006-07 (Table VI.43).

6.93 The secondary market turnover of Treasury Bills and Government dated securities (both outright and repo) traded by stand-alone PDs amounted to Rs.1,57,747 crore and Rs.16,80,073 crore, respectively, constituting 16 per cent and 17 per cent, respectively, of the market turnover. The share of PDs in total market turnover worked out to 16 per cent. Sources and Application of Funds 6.94 The consolidated balance sheet size of nine stand-alone PDs at end-March 2008 declined by 19.7 per cent as compared with the position at end-March 2007 due to restructuring of their businesses. Three PDs hived off their PD operations to newly set up group entities with reduced capital. Capital funds of the stand-alone PDs declined by 27.8 per cent as on March 31, 2008 in contrast with the sharp increase of 46.3 per cent as on March 31, 2007. On the sources side, secured loans increased by 17.1 per cent during 2007-08, while unsecured loans registered a sharp decline of 36.1 per cent. The decline in the growth rate of unsecured loans during 2007-08 was in contrast with the sharp rise (of 20.3 per cent) witnessed during 2006-07. On the deployment side, investments in corporate bonds increased by 4.3 per cent (from Rs.595 crore to Rs.621 crore) in contrast to the decline of 12.7 per cent witnessed during 2006-07. (Table VI.44). The share of Government securities and Treasury Bills in total assets of PDs increased to 70 per cent at end-March 2008 from 55 per cent at end-March 2007.

Financial Performance of PDs 6.95 The income earned by the PDs declined by 33 per cent during the year 2007-08 as compared with that in 2006-07, due to restructuring of business by PDs and consequent decline in income from other activities that were not allowed to be undertaken by PDs. However, a corresponding sharp decline on the expenditure front and a rise in trading profits restricted the decline in net profit during the year (Table VI.45).

however, increased from 9.5 per cent during 2006-07 to 10.8 per cent in 2007-08, reflecting the better use of capital. (Appendix Table VI.5). The cost-income ratio declined from 50 per cent in 2006-07 to 25 per cent in 2007-08 as some PDs significantly improved their efficiency ratio. 6.97 Stand-alone PDs continued to be adequately capitalised. The capital to risk weighted-assets ratio (CRAR) of individual stand-alone PDs remained above the prescribed minimum CRAR of 15 per cent. The CRAR of the stand-alone PDs as a group was at 38 per cent as on March 31, 2008. (Appendix Table VI.6 and Table VI.47).

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

شارك هذه الصفحة:

بھارت موبائل ایپلی کیشن کے ریزرو بینک کو انسٹال کریں اور تازہ ترین خبروں تک فوری رسائی حاصل کریں!

ہماری ایپ انسٹال کرنے کے لیے QR کوڈ اسکین کریں۔

صفحے پر آخری اپ ڈیٹ: