IST,

IST,

Going Bust for Growth

Dr. Raghuram G. Rajan, Governor, Reserve Bank of India

delivered-on مئی 19, 2015

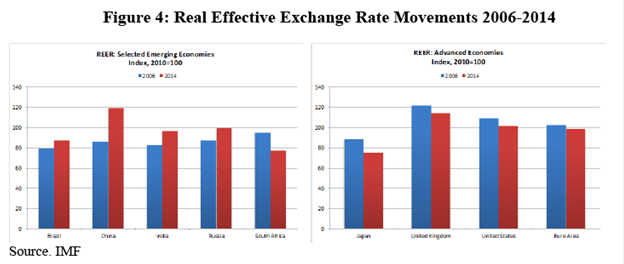

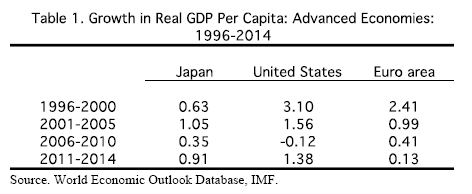

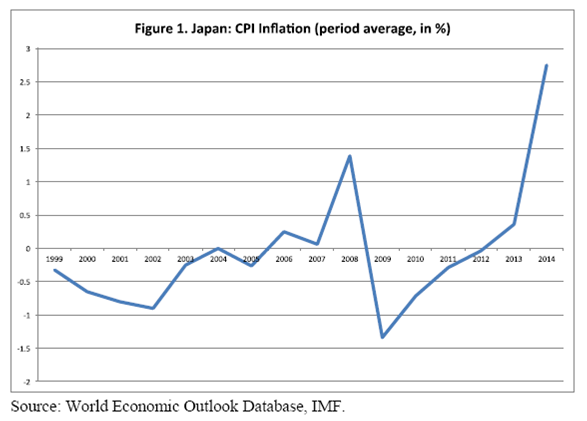

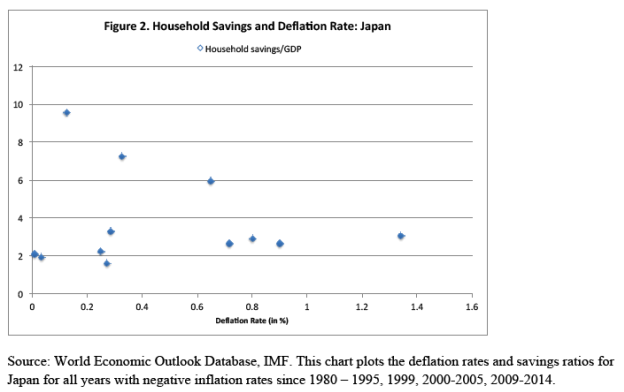

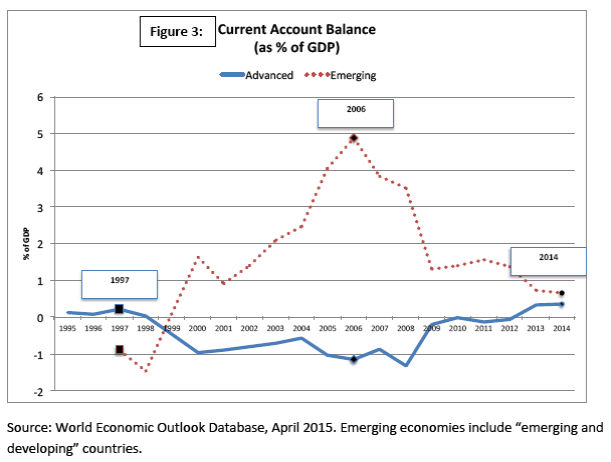

There are few areas of robust growth around the world, with the IMF repeatedly reducing its growth forecasts in recent quarters. This period of slow growth is particularly dangerous because both industrial countries and emerging markets need high growth to quell rising domestic political tensions. Policies that attempt to divert growth from others rather than create new growth are more likely under these circumstances. Even as we create conditions for sustainable growth, we need new rules of the game, enforced impartially by multilateral organizations, to ensure countries adhere to international responsibilities. The conventional diagnosis and remedy Why is the world finding it so hard to restore pre-Great Recession growth rates? The obvious answer is that the financial boom preceding the Great Recession left industrial countries with an overhang of debt, and debt, whether on governments, households, or banks, is holding back growth.2 While the remedy may be to write down debt so as to revive demand from the indebted, it is debatable whether additional debt fuelled demand is sustainable in the long run. At any rate, large-scale debt write-offs (or fiscal transfers to the heavily indebted) seem politically difficult even if they are economically warranted. How does one offset weak household and government demand if debt write-downs are off the table? Ideally, the response would be to incentivize investment and job creation through low interest rates and tax incentives. But if final demand from consumers is likely to be very weak for a considerable period of time because of debt overhang, the real return on new investment may collapse. The Wicksellian neutral real rate – loosely speaking the interest rate required to bring the economy back to full employment with stable inflation -- may even be strongly negative.3 This typically has been taken as grounds for aggressive monetary policy. Because policy rates cannot be reduced significantly below zero (though a number of European countries are testing these limits), equilibrium long term interest rates may stay higher than levels necessary to incentivize investment. Hence, central banks have embarked on unconventional monetary policy (UMP), which would directly lower long rates. Another way to stimulate demand is for governments that still have the ability to borrow to increase spending. Since this will increase already-high levels of government debt, proponents suggest investing in infrastructure, which may have high returns today when construction costs and interest rates are low. However, high-return infrastructure investment is harder to identify and implement in developed countries where most obvious investments have already been made – political influence is as likely to create bridges to nowhere or unviable high speed train networks as needed infrastructure. Also, while everyone can see the need for repair and renovation of existing infrastructure, this requires far more decentralized spending than mega projects, and may be harder to initiate and finance from the centre. Put differently, high-return infrastructure investment is a good idea but may be hard to implement on a large scale for most advanced country governments. To the extent that such debt fuelled spending creates a self-fulfilling virtuous cycle of confidence and activity, it can be a bridge to sustainable growth. But to the extent that it misallocates capital (because there are insufficient “shovel-ready” projects, so much of the emergency spending is diverted to rent-seeking pork), it can worsen public anxieties about the future, reducing corporate investment and increasing household savings. All this highlights another concern. Even if stimulus works in raising growth temporarily -- and the above discussion suggests it may not – this growth has to be a bridge to sustained aggregate demand. But what if it isn’t? The Productivity Puzzle, Secular Stagnation, and other concerns. The arguments I have just enunciated for action apply to an economy where nothing fundamentally is wrong except perhaps excessive debt – what is needed is a cyclical return of growth to potential growth. Yet a number of economists such as Tyler Cowen, Robert Gordon, and Larry Summers have raised the possibility that potential growth in industrial countries had fallen even before the Great Recession. Perhaps then the growth that we are trying to return to is unachievable without serious distortions. The term “secular stagnation” used by Larry Summers to describe the current persistent economic malaise, echoing Alvin Hansen’s speech in 1938 in the midst of the Great Depression, has caught on.4 But different economists focus on different aspects and causes of the stagnation.5 Summers emphasizes the inadequacy of aggregate demand, and the fact that the zero lower bound as well as the potential for financial instability prevents monetary policy from being more active. Among the reasons for weak aggregate demand include ageing populations that want to consume less and the increasing income share of the very rich, whose marginal propensity to consume is small. Tyler Cowen and Robert Gordon on the other hand, emphasize a weak supply potential.6 They argue that the post-World War II years were an aberration because growth was helped in industrial countries by reconstruction, the spread of technologies such as electricity, telephones, and automobiles, rising educational attainment, higher labour participation rates as women entered the work force, a restoration of global trade, and increasing investments of capital. However, post-war total factor productivity growth – the part of growth stemming from new ideas and methods of production – was lower than its 1920-50 high. More recently, not only has productivity growth fallen further (with a temporary positive uptick towards the end of the 1990s because of the IT revolution), but growth has been held back by the headwinds of plateauing education levels and labour participation rates, as well as a shrinking labour force in some countries because of population ageing. It is obvious from these lists of factors that it is hard to disentangle the effects of weak aggregate demand from slow growth in potential supply. Population ageing contributes to both. Indeed, one may cause the other. For example, anticipating a slowdown in growth potential, households, worried about impending retirement in the face of undeliverable pension and healthcare entitlements, may try and build savings. This will depress demand further. Conversely, anticipated weak demand may reduce incentives for corporations to invest in physical and human capital, causing supply potential to grow more slowly. Structural reforms, typically ones that increase competition, foster innovation, and drive institutional change, are the way to raise potential growth. But these immediately hurt protected constituencies that have become accustomed to the rents they get from the status quo. Moreover, the gains to constituencies that are benefited are typically later and uncertain while the pain is immediate and its incidence clear. No wonder Jean-Claude Juncker, then Luxembourg’s prime minister, said at the height of the Euro crisis, “We all know what to do, we just don't know how to get re-elected after we've done it!” The Growth Imperative If indeed fundamentals are such that that the industrial world has, and will, grow slowly for a while before new technologies and new markets come to the rescue, would it be politically easy to settle for slower growth? After all, per capita income is high in industrial countries, and a few years of slow growth would not be devastating at the aggregate level. Why is there so much of a political need for growth? One reason is the need to fulfil government commitments. As sociologist Wolfgang Streeck writes, in the strong growth years of the 1960s when visions of a “Great Society” seemed attainable, industrial economies made enormous promises of social security to the wider public.7 Promises have been augmented since then in some countries by politically convenient (because hidden from budgets) but fiscally unsound increases in pension and old age healthcare commitments to public sector workers. And most recently, the government debt taken on before and after the Great Recession has added to government commitments, even while the Baby Boomer generation has started retiring in large numbers. Without the immediate promise of growth, all these commitments could soon be seen as unsustainable. Another reason to desire growth is that economies tend to favour insiders – those who have jobs for example. The brunt of the joblessness caused by slow growth is born by new entrants to the labour market. Not only are they unemployed in larger numbers, but the lifetime earnings of cohorts that enter the labour force in difficult times is lower. Growth is necessary for inter-generational equity, especially because these are the generations that will be working to pay off commitments to older generations. Given these are also the cohorts that can take to the streets, growth is essential for social harmony. Not only are the benefits of growth unequally distributed across generations, they are also very unequally distributed within generation. Because of changes in technology and the expansion of global competition, routine repetitive jobs, whether done by the skilled or the unskilled, have diminished greatly in industrial countries. Many of these jobs, ranging from assembly line worker to legal aides or insurance clerks, have either been automated or outsourced. The desirable high-paying jobs are non-routine skilled ones such as that of a consultant or an app designer, but they require skills. The middle class recognizes that they need quality higher education and training to not slip into competing with the poor for low-skilled non-routine jobs such as security guard or gardener. But the poor quality early education they have received, as well as the prohibitive cost of quality higher education, puts many better livelihoods out of reach. With every percentage point of growth creating fewer “good” jobs for the unskilled or moderately skilled, more growth is needed to keep them happily employed. Equally, the rapid deterioration in skills for the unemployed is an additional reason to push for growth. The Deflation Fear Finally, a big factor persuading authorities in industrial countries to push for higher growth is the fear of deflation. The canonical example here is Japan, where many are persuaded that the key mistake it made was to slip into deflation, which has persisted and held back growth. A closer look at the Japanese experience suggests that it is by no means clear that its growth has been slower than warranted let alone that deflation caused slow growth. It is true that after its devastating crisis in the early 1990s, Japan may have prolonged the slowdown by not taking early action to clean up its banking system or restructure over-indebted corporations. But once it took decisive action in the late 1990s and early 2000s, Japanese growth per capita or per worker looks comparable with other industrial countries (Table 1).8 Slow aggregate Japanese economic growth may simply be because its population is shrinking, and fewer people are entering the labour force rather than because it is underperforming other developed economies. What about the deleterious effects of deflation? One worrisome effect of deflation is that if wages are downwardly-sticky, real wages rise and cause unemployment. Yet Japanese unemployment has averaged 4.5% between 2000-2014, compared to 6.4% in the US and 9.4% in the Euro area during the same period.9 In part, the Japanese have obtained wage flexibility by moving away from the old lifetime unemployment contracts for new hires to short term contracts. Indeed, with the decline in union power across industrial countries and the increase in temporary or even “zero hour” workers, downward wage flexibility may be significantly higher than previously estimated. While not without social costs, such flexibility allows an economy to cope with sustained deflation. Another concern has been that moderately low inflation spirals down into seriously large deflation, where the zero lower bound on nominal interest rates keeps real interest rates unconscionably high. Once again, it is not clear this happened in Japan. In the years 1999 to 2012, average CPI deflation ranged between -0.01% in 2004 to -1.3% in 2009, but without any clear spiralling pattern (Figure 1). Even if deflation is moderate, it may cause customers to postpone purchases and increase savings in anticipation of a lower price in the future, especially if the zero lower bound raises real interest rates above their desired value. In Fig 2, we plot household savings as a share of GDP in Japan against the deflation rate. Again, it is hard to see a sustained pattern of higher savings with higher deflation. Finally, it is true that deflation increases the real burden of existing debt, thus exacerbating debt overhang. But this is true of any unanticipated disinflation, and is not specific to deflation. If debt is excessive, a targeted restructuring is better than inflating it away across the board. Regardless of all these arguments, the spectre of deflation haunts central bankers. When coupled with the other political concerns raised by slow and unequal growth listed above, it is no wonder that the authorities in developed countries do not want to settle for low growth, even if that is indeed their economy’s potential. So the central dilemma in industrial economies has been how to reconcile the political imperative for strong growth with the reality that cyclical stimulus measures have proved ineffective in restoring high growth, debt write-offs are politically unacceptable, and structural reforms have the wrong timing, politically speaking, of pain versus gain. There is, however, one other channel for growth – exports. Emerging Market Response If industrial countries are stuck in low growth, can emerging markets (I use the term broadly to also stand for developing or frontier markets) take up the global slack in demand? After all, emerging markets have a clear need for infrastructure investment, as well as growing populations that can be a source of final demand. Why cannot industrial countries export to emerging markets as a way to bolster growth? After all, they have done so in the past. Emerging markets have no less of an imperative for growth than industrial countries. While many do not have past entitlement promises to deliver on, some have ageing populations that have to be provided for, and many have young, poor, populations with sky-high expectations of growth. Ideally, emerging markets would invest for the future, funded by the rich world, thus bolstering aggregate world demand. The 1990s were indeed a period when emerging markets borrowed from the rest of the world in attempting to finance infrastructure and development. It did not end well, with credit booms, large unviable prestige projects, and eventual busts. The Mexican Crisis of 1994, the Asian Crisis of 1997-98, and the Argentinian Crisis of 2001 highlighted the inability of emerging markets to manage large increases in domestic investment funded by foreign capital inflows. The lesson from the 1990s crises was that emerging market reliance on foreign capital for growth was dangerous. With investment prudently limited to domestic savings, this naturally curtailed their ability to serve as growth engines for the world. Following the 1990s crises, as the dotted line in Figure 3 indicates, a number of emerging markets went further to run current account surpluses after cutting investment sharply, and started accumulating foreign exchange reserves to preserve exchange competitiveness. Rather than generating excess demand for the world’s goods, they became suppliers (or equivalently, savers), searching for demand elsewhere. And the debt-fuelled demand from the industrial countries before the Global Financial Crisis, as indicated by their current account deficits, spilled over into a demand for emerging market goods. The years before the crisis were years of plenty for countries like China that catered directly to industrial country demand, and countries in AFfrica, Asia, and Latin America that sold commodities and intermediate goods to the direct suppliers. In 2005, Ben Bernanke, then a governor at the Federal Reserve, coined the term “Global Savings Glut” to describe the current account surpluses, especially of emerging markets, that were finding their way into the United States.10 He argued that these depressed U.S. interest rates, enhancing consumption, and the U.S. current account deficit. Bernanke pointed to a number of adverse consequences to the United States from these flows including the misallocation of resources to non-traded goods like housing away from tradable manufacturing. He suggested that it would be good if United States’ current account deficit shrank, but that primarily required emerging markets to reduce their exchange rate intervention rather than actions on the part of the United States. So pre-global financial crisis, emerging markets and industrial countries were locked in a dangerous relationship of capital flows and demand that reversed the equally dangerous pattern before the emerging market crises in the late 1990s. Sustained exchange rate intervention by emerging market central banks, as well as an excessive tolerance for leverage in industrial countries contributed to the eventual global disaster. But post-financial crisis, the pattern is reversing once again. Post global financial crisis, much like the emerging markets in the early 2000s, industrial countries have curtailed their investment without increasing their consumption (as a fraction of GDP), thus reducing their demand for foreign goods and their reliance on foreign finance. Indeed, as the solid line in Figure 3 indicates, advanced economies ran current account surpluses in 2013 and were also projected to do so in 2014, a shift in current account balances of about 1.5 percentage points of GDP since 2008. The counterpart of this shift of advanced economies from current account deficit (demand creating) to surplus (supply creating) has been a substantial fall in current account surpluses in emerging markets over the same period. This relative increase in demand for foreign goods from emerging markets has come about through a ramp up in investment from 2008, rather than a fall in savings – a shift of 2.7 percentage points of GDP in current account balances between 2008 and 2014. Facilitating or causing this shift has been a broad appreciation of real effective exchange rates in emerging markets and a depreciation in industrial country rates between 2006-2014.  Have industrial country central banks policies, similar to the sustained exchange rate intervention by emerging market central banks in the early 2000s, accelerated this current account adjustment? Possibly, and likely candidates would be what are broadly called unconventional monetary policies (UMP). Unconventional Monetary Policy Unconventional monetary policies include both policies where the central bank attempts to commit to hold interest rates at near zero for long, as well as policies that affect central bank balance sheets such as buying assets in certain markets, including exchange markets, in order to affect market prices.11 There clearly is a role for unconventional policies – when markets are broken or grossly dysfunctional, central bankers may step in with their balance sheets to mend markets. The key question is what happens when these policies are prolonged long beyond repairing markets to actually distorting them. The benefit to cost ratio there is less clear. Take, for instance, the zero-lower-bound problem. Because short term policy rates cannot be pushed much below zero, and because long rates tack on a risk premium to short rates, central banks may use UMP to directly affect long rates. Direct action by a risk tolerant central bank, such as purchasing long bonds, effectively shrinks the risk premium available on remaining long assets.12 This has two effects. First, those who can rebalance between short and long assets now prefer holding short term assets because, risk adjusted, these are a better deal. Thus as the central bank increases bond purchases under quantitative easing, the willingness of commercial banks to hold unremunerated reserves rather than long term assets increases. Second, those institutions that cannot shift to short term assets, such as pension funds, bond mutual funds, and insurance companies, will either continue holding their assets and suffer a relative under-compensation for risk, or turn to riskier assets. This behaviour, also termed the search for yield, will occur if the relative under-compensation for risk in more exotic assets is lower, or simply because institutions have to meet a fixed nominal rate of return constraint on their portfolios. Of course, such portfolio rebalancing will also take place because the central bank buys long duration bonds out of institutional portfolios, leaving them cash to redeploy. None of this need be a problem if everyone knows when to stop. Unfortunately, there are few constraints on central banks undertaking these policies since they are self-financing (commercial banks become more willing to hold central bank reserves as the risk premium on long bonds shrinks). If the policy does not seem to be increasing growth, one can simply do more. All the while, the distortion in asset prices and the mis-allocation of funds can increase, which can be very costly when the central bank decides to exit. Equally important though, is that domestic fund managers can search for yield abroad, depreciating the sending country’s currency and causing the receiving country’s currency to appreciate, perhaps significantly more so than ordinary monetary policy. This may indeed cause the increase in domestic competitiveness that could energize the sending country’s exports. But such increases in competitiveness and “demand shifting” can be very detrimental for global stability, especially if unaccompanied by domestic demand creation. Spill Overs to Emerging Markets and Musical Crises If UMP enhances financial risk taking in the originating country without enhancing domestic investment or consumption, the exchange rate impact of UMP may simply shift demand away from countries not engaging in UMP, without creating much compensating domestic demand for their goods. If so, UMP would resemble very much the exchange rate intervention policies of the emerging markets pre-global financial crisis. Indeed, the post-global crisis capital flows into emerging markets have been huge, despite the best efforts of emerging markets to push them back by accumulating reserves (net capital flows to emerging economies reached US$ 550 bn in 2013 compared to US$120 bn in 2006).13 14 These flows have increased local leverage, not just due to the direct effect of cross-border banking flows but also the indirect effect, as the appreciating exchange rate and rising asset prices, especially of real estate, make it seem that emerging market borrowers have more equity than they really have. Bernanke’s concerns in 2005 about mal-investment in the United States resulting from capital inflows from emerging markets have surfaced in emerging markets post-crisis as a result of capital inflows from industrial countries. Have crises in emerging markets in the 1990s been transformed into crises in industrial countries in the 2000s and once again into vulnerabilities in emerging markets in the 2010s, as countries react to the problem of inadequate global demand by exporting their problems to other countries? The “taper tantrum” in July 2013 certainly seemed to suggest that emerging markets that ran large current account deficits were vulnerable once again.15 Is the world engaged in a macabre game of musical crises as each country attempts to boost growth? If possibly yes, as suggested by the previous discussion, how do we break this cycle? Good Policies…and Good Behaviour In an ideal world, the political imperative for growth would not outstrip the economy’s potential. Given that we do not live in such a world, and given that social security commitments, over-indebtedness, and poverty are not going to disappear, it is probably wiser to look for ways to enhance sustainable growth. Clearly, the long run response to weak global growth should be policies that promote innovation as well as structural reforms that enhance efficiency. Given that growth within countries is poorly distributed, policies that improve the domestic distribution of capabilities and opportunities without significantly dampening incentives for innovation and efficiency are also needed. In the short run though, the need for sensible investment is paramount. In industrial countries, green energy initiatives such as carbon taxes or emission limits, while giving industry clear signals on where to invest, also have the ability to move the needle on aggregate investment and help long run goals on environment protection. Most emerging markets have large infrastructure investment needs. We still need to understand how to improve project selection and finance – too much public sector involvement results in sloth and rent seeking, too much private sector involvement leads to risk intolerance and profiteering. Going forward, well-designed public private partnerships, drawing on successful experiences elsewhere, should complement private initiative. The Australian Presidency of the G 20 created a welcome mechanism to share best investment practices across countries. At the same time, we must recognize that large scale investment projects need patient risk capital, which is in short supply in emerging markets. Private investors rarely have the risk tolerance that governments or multilateral institutions have. So, in addition to knowledge sharing, global growth would benefit from an augmentation of the capital base of multilateral institutions like the World Bank, the African Development Bank, and the Asian Development Bank, so that they can provide part of the patient risk tolerant capital the emerging world needs. Despite competing domestic demands, industrial countries should recognize the important catalytic role that the development banks can play and help bolster their capital. At the very least, they should not stand in the way of others augmenting capital and taking more ownership. Clearly, sensible investment has a much better chance of paying dividends when macroeconomic policies are sound. And such policies are easier when the adverse spill overs from cross-border capital flows are limited. This may require new rules of the game for policy making. New Rules of the Game? How do we focus on domestic demand creation and avoid this game of musical crises with countries trying to depreciate their exchange rate through sustained direct exchange rate intervention or through unconventional monetary policies (where demand creating transmission channels are blocked)?16 It might be useful to examine and challenge the rationales used to justify such actions. Rationale 1: Would the world not be better off if we grew strongly? Undoubtedly, if there were no negative spill overs from a country’s actions, the world would indeed be better off if the country grew. But the whole point about policies that primarily affect domestic growth by depreciating the domestic exchange rate is that they work by pulling growth from others, not creating growth for others. Rationale 2: We are in a deep recession. We need to use any means available to jump start growth. Once we get out of recession, the payoff for other countries from our growth will be considerable. This may be a legitimate rationale if the policy is a “one-off” and once the country gets out of its growth funk, it is willing to let its currency appreciate so that it absorbs imports, thus pulling other countries with it. But if the strengthening currency leads to a continuation of the unconventional policies as the country’s authorities become unwilling to give back the growth they obtained by undervaluing their currency, or if the strengthening currency leads to greater domestic political clamour about foreign countries undervaluing their currencies, this rationale is suspect. Moreover, policies that encourage sustained unidirectional capital outflows to other countries can be very debilitating for the recipient’s financial stability, over and above any effects on their competitiveness. Thus any “one-off” has to be limited in duration. Rationale 3: Our domestic mandate requires us to do what it takes to fulfil our inflation objective, and unconventional monetary policy is indeed necessary when we hit against the zero lower bound. This rationale has two weaknesses. First, it places a domestic mandate above an international responsibility. If this were seen to be legitimate, then no country would ever respect international responsibilities when inconvenient. Second, it implicitly assumes that the only way to achieve the inflation mandate is through unconventional monetary policy (even assuming UMPs are successful in elevating inflation on a sustained basis, for which there is little evidence). Rationale 4: We take into account the feedback effects to our economy from the rest of the world while setting policy. Therefore, we are not oblivious to the consequences of unconventional monetary policies on other countries. Ideally, responsible global citizenship would require a country to act as it would act in a world without boundaries. In such a world, a policy maker should judge whether the overall positive domestic and international benefits of a policy, discounted over time, outweigh its costs. Some policies may have largely domestic benefits and foreign costs, but they may be reasonable in a world without boundaries because more people are benefited than are hurt. By this definition, Rationale 4 does not necessarily amount to responsible global citizenship because a country only takes into account the global “spillbacks” to itself from any policies it undertakes, instead of the spill overs also. So, for example, Country A may destroy industry I in country B through its policies, but will only take into account the spillback from industry I purchasing less of country A’s exports. Rationale 5: Monetary policy with a domestic focus is already very complicated and hard to communicate. It would be impossibly complex if we were additionally burdened with having to think about the effects of (unconventional) monetary policies on other countries. This widely-heard rationale is really an abandonment of responsibility. It amounts to asserting that the monetary authority only has a domestic mandate, which is Rationale 3 above. In an interconnected globalized world, “complexity” cannot be a defense. Rationale 6: We will do what we must, you can adjust. Adjustments are never easy, and sometimes very costly – one reason why Ben Bernanke placed the burden of change in his “Savings Glut” speech outside the United States. Emerging markets may not have the institutions that can weather the exchange rate volatility and credit growth associated with large capital flows – for instance, sharp exchange rate depreciations can translate quickly into inflation if the emerging market central bank does not have credibility, while exchange rate depreciations may be more easily endured by an industrial country. The bottom line is that multilateral institutions like the IMF should re-examine the “rules of the game” for responsible policy, and develop a consensus around new ones. No matter what a central bank’s domestic mandate, international responsibilities should not be ignored. The IMF should analyze each new unconventional monetary policy (including sustained unidirectional exchange rate intervention), and based on their effects and the agreed rules of the game, declare them in- or out-of-bounds. By halting policies that primarily work through the exchange rate, it will also contribute to solving a classic Prisoner’s Dilemma problem associated with policies that depreciate the exchange rate -- once some countries undertake these policies, staying out is difficult (the country that eschews these policies sees its currency appreciate and demand fall). Exit is also difficult (the exiting country faces sharp appreciation). Therefore, in the absence of collective action, these policies will be undertaken even when sub-optimal, and will carry on too long. Of course, with country authorities in almost every industrial country focused on appeasing populist anti-trade anti-finance (and anti-central bank) political movements, there is little appetite for taking on further international commitments. We clearly need further dialogue and public debate on the issues that have been raised, while recognizing that progress will require strong political leadership. International Safety Nets Emerging economies have to work to reduce vulnerabilities in their economies, to get to the point where, like Australia or Canada, they can allow exchange rate flexibility to do much of the adjustment for them to capital inflows. But the needed institutions take time to develop. In the meantime, the difficulty for emerging markets in absorbing large amounts of capital quickly and in a stable way should be seen as a constraint, much like the zero lower bound, rather than something that can be altered quickly. Even while resisting the temptation of absorbing flows, emerging markets will look to safety nets. So another way to prevent a repeat of substantial emerging market reserve accumulation, this time for precautionary rather than competitive purposes, is to build stronger international safety nets. For instance, one possibility is an unsolicited liquidity line from the IMF, where countries are pre-qualified by the IMF and told (perhaps privately) how much of a line they would qualify for under current policy – with access limits revised in the annual dialogue the Fund has with a country, and any curtailment becoming effective 6 months later. Access to the line would get activated by the IMF Board in a situation of generalized liquidity shortage (as, for example, when policy tightening in source countries after an extended period of low rates causes investment managers to become risk averse). In turn, the Fund could finance this liquidity by intermediating swaps with central banks (and thus guaranteeing central banks against default). Such proposals allow countries access to liquidity without the stigma of approaching the Fund, and without the conditionality that accompanies most Fund arrangements, and thus are more likely to be acceptable as precautionary measures. It would also be a useful exercise for the Fund, in a period of growing vulnerability to capital flow reversals, to determine those countries that do not have own, bilateral, regional, or multilateral liquidity arrangements to fall back on, and to work to improve their access to some safety net. Conclusion The current non-system in international monetary policy is, in my view, a source of substantial risk, both to sustainable growth as well as to the financial sector. It is not an industrial country problem, nor an emerging market problem, it is a problem of collective action. We are being pushed towards competitive monetary easing and musical crises. I use Depression era terminology because I fear that in a world with weak aggregate demand, we may be engaged in a risky competition for a greater share of it. We are thereby also creating financial sector risks for when unconventional policies end. We need stronger well-capitalized multilateral institutions with widespread legitimacy, some of which can provide patient capital and others that can monitor new rules of the game. We also need better international safety nets. And each one of us has to work hard in our own countries to develop a consensus for free trade, open markets, and responsible global citizenry. If we can achieve all this even as recent economic events make us more parochial and inward-looking, we will truly have set the stage for the strong sustainable growth we all desperately need. 1 Remarks by Raghuram Rajan, Governor of the Reserve Bank of India on May 19, 2015 to the Economic Club of New York. Rajan thanks Dr. Prachi Mishra of the Reserve Bank for very useful comments and research support. 2 See the interesting evidence in Atif Mian and Amir Sufi, House of Debt (Princeton University Press, New Jersey, 2014) and the cross-country evidence in Carmen Reinhart and Kenneth Rogoff, This Time is Different (Princeton University Press, New Jersey, 2008). For an illuminating overall view of the global financial crisis and the policy remedies, see Martin Wolf, The Shifts and the Shocks: What We've Learned and Have Still to Learn from the Financial Crisis (Penguin USA 2015). 3 Though see a thoughtful piece by Claudio Borio and Piti Disyatat at http://www.voxeu.org/article/low-interest-rates-secular-stagnation-and-debt suggesting that the real neutral interest rate may be influenced by low policy rates. Intuitively, the authors argue that low policy rates can sow the seeds for investment misallocation, financial distress, and debt overhang, all of which can combine to drive down the future real return on investment, and therefore the real neutral long term rate today. 4 Summers, L. (2014), “U.S. Economic Prospects: Secular Stagnation, Hysterisis and Zero Lower Bound”, speech delivered to the National Association for Business Economics, Economic Policy Conference, February 24, 2014. 5 See, for example, “The Crises of Democratic Capitalism”, Wolfgang Streeck, New Left Review 71, Sept/Oct 2011 or “The True Lessons of the Recession: The West Can’t Borrow and Spend its Way to Recovery”, Raghuram Rajan, Foreign Affairs, Volume 91, no 3, May/June 2012 . 6 Tyler Cowen (2013), The Great Stagnation, Ebook, Gordon, R. (2012), “Is US Economic Growth Over? Faltering Innovation Confronts Six Headwinds”, NBER Working Paper 18315. 7 See “The Crises of Democratic Capitalism”, Wolfgang Streeck, New Left Review 71, Sept/Oct 2011. 8 I first learnt of these facts from Jean Claude Trichet. For a more comprehensive look at deflation, see Claudio Borio, Magdalena Erdem, Andrew Filardo and Boris Hofmann, “The costs of deflations: a historical perspective”, BIS Quarterly Review March 2015. 9 Source. World Economic Outlook Database, IMF. 10 “The Global Saving Glut and the U.S. Current Account Deficit”, remarks by Governor Bernanke at the Sandridge Lecture, Virginia Association of Economists, Richmond, Virginia on March 10, 2005, http://www.federalreserve.gov/boarddocs/speeches/2005/200503102/ 11 For an excellent overview, see Claudio Borio and P. Disyatat, "Unconventional monetary policies: An appraisal", The Manchester School; Vol. 78, Issue s1, pp. 53-89, September 2010 12 For instance, because the most risk averse holders of existing long bonds sell first and move to holding short term assets. 13 Based on the World Economic Outlook database. Emerging economies include “emerging and developing” countries. Net capital flows include net direct investment, net protfolio investment, and “other” net investment. 14 Indeed, similar to the behavior of commercial banks, the willingness of emerging market central banks to hold short term paper in response to capital inflows enhances the ability of the industrial country central bank to engage in further UMP. In a sense, emerging market central banks provide liquidity for foreign investors by holding precautionary reserves. 15 For those who advocate allowing exchange rate adjustment as central to macro-management, it should be sobering that countries that allowed the real exchange rate to appreciate the most during the prior period of quantitative easing suffered the greatest adverse impact to financial conditions (see Eichengreen, Barry and Poonam Gupta (2013), “Tapering Talk: The Impact of Expectations of Reduced Federal Reserve Security Purchases on Emerging Markets”, Working Paper, University of California, Berkeley and Mishra, Prachi, Kenji Moriyama, Papa N’Diaye and Lam Nguyen (2014), “The Impact of Fed Tapering Announcements on Emerging Markets”, IMF working paper). 16 See also a very thoughtful piece by Fabrizio Saccomanni, “Monetary spillovers? Boom and bust? Currency wars?”, The international monetary system strikes back”, BIS Special Governors Meeting, Manila, February 2015. |

شارك هذه الصفحة:

بھارت موبائل ایپلی کیشن کے ریزرو بینک کو انسٹال کریں اور تازہ ترین خبروں تک فوری رسائی حاصل کریں!

ہماری ایپ انسٹال کرنے کے لیے QR کوڈ اسکین کریں۔

صفحے پر آخری اپ ڈیٹ: