IST,

IST,

अनरेटड एक्सपोज़र के लिए बनाए गए विवेकपूर्ण विनियमों का बड़े उधारकर्ताओं के रेटिंग स्वरूप पर असर

|

मिंट स्ट्रीट मेमो क्र. 20 पल्लवी चव्हाण और एस. के. रिताधि* बिना रेटिंग वाले ऋण उधारकर्ताओं की साख और बैंकों का पूंजी स्तर, दोनों के सटीक आकलन के लिए चुनौतियां उत्पन्न कर सकते हैं। रिज़र्व बैंक ने 2016 में विवेकपूर्ण विनियामक दिशानिर्देशों को संशोधित किया, ताकि उधारकर्ता को एक निश्चित सीमा से ऊपर दिए गए रेटेड और अनरेटेड बैंक ऋणों के बीच जोखिम भारों संबंधी विनियामकीय कमियों का लाभ उठाने की प्रवृत्ति को रोका जा सके। रिग्रेशन डिसकंटिन्यूटी डिजाइन में इस न्यूनतम ऋण सीमा का उपयोग करने पर इस अध्ययन में यह पाया गया कि पॉलिसी निर्धारण पश्चात के उधारकर्ता समूह में रेटेड से अनरेटेड श्रेणी में स्विच को हतोत्साहित करने में इस पॉलिसी का अपेक्षित प्रभाव पड़ा है। सामान्य भाषा में कहा जाए तो पॉलिसी में बदलाव के कारण तिमाहियों के दौरान पॉलिसी निर्धारण पश्चात के उधारकर्ता समूह में रेटेड से अनरेटेड श्रेणी में स्विच की संभावना में 50 प्रतिशत की कमी आई है। पॉलिसी में बदलाव का असर निजी क्षेत्र के बैंकों के उधारकर्ताओं की तुलना में सरकारी क्षेत्र के बैंकों के उधारकर्ताओं पर उल्लेखनीय रूप से अधिक रहा। 1. प्रस्तावना क्रेडिट रेटिंग बैंकों को अपने संभावित उधारकर्ताओं की साख का आकलन करने में मदद करती है। बैंकिंग पर्यवेक्षण पर बेसल समिति (बीसीबीएस) की पूंजी पर्याप्तता ढांचे के तहत ऋण / निवेश जोखिम के लिए पूंजी आवश्यकता का आकलन करने के लिए रेटिंग भी एक महत्वपूर्ण नियामक साधन है। बीसीबीएस द्वारा निर्धारित मानकीकृत दृष्टिकोण के तहत, जिसका वर्तमान में भारत में सभी अनुसूचित वाणिज्यिक बैंकों (एससीबी) द्वारा पालन किया जाता है - क्रेडिट जोखिम के लिए पूंजी की गणना हेतु बाहरी रेटिंग (मान्यता प्राप्त क्रेडिट रेटिंग एजेंसियों द्वारा दी गई) का उपयोग किया जाता है। इस संदर्भ में, अन-रेटेड एक्सपोज़र की उपस्थिति बैंकों में पूंजी की गणना को प्रभावित कर सकती है क्योंकि इस तरह के एक्सपोज़र की गुणवत्ता के बारे में जानकारी प्रदान करने में उनकी स्पष्टता का पता नहीं चलता।1 रिज़र्व बैंक के वृहद ऋणों पर सूचना के केंद्रीय भंडार (सीआरआईएलसी) में अन-रेटेड उधारकर्ताओं की हिस्सेदारी कुल संख्या का लगभग 60 प्रतिशत और "बड़े" उधारकर्ताओं (50 मिलियन रुपए से अधिक निधि आधारित और गैर निधि आधारित ऋण) को दिए गए कुल ऋण का 40 प्रतिशत है (आकृति 1, बायां पैनल)। सरकारी क्षेत्र के बैंकों (पीएसबी) की तुलना में निजी क्षेत्र के बैंकों (पीवीबी) की हिस्सेदारी उल्लेखनीय रूप से अधिक है (आकृति 2)। चूंकि कुल एक्सपोज़र में कुल उधारकर्ताओं की तुलना में अनरेटेड उधारकर्ताओं की हिस्सेदारी कम है, इससे यह संकेत मिलता है कि कम एक्सपोज़र वाले उधारकर्ताओं की रेटिंग न होने की संभावना अधिक है। तथापि जब हम अनरेटेड उधारकर्ताओं की अनर्जक आस्तियों (एनपीए) की जांच करते हैं तो स्थिति को उससे विपरीत पाते हैं। जून 2014 (पहली तिमाही, जिसके लिए सीआरआईएलसी का डाटा उपलब्ध है) और दिसंबर 2015 के बीच (क) अनरेटेड उधारकर्ताओं की कुल संख्या में एनपीए उधारकर्ताओं की संख्या और (ख) अनरेटेड एक्सपोज़र की कुल राशि में एनपीए की राशि में तुलनात्मक दृष्टि से वृद्धि और प्रवृत्ति दिखाई दी (आकृति 1, दायां पैनल)। तथापि दिसंबर 2015 के बाद इनकी हिस्सेदारियों में अंतर बढ़ा। अनरेटेड एक्सपोज़र में एनपीए राशि की हिस्सेदारी गैर निष्पादनकारी उधारकर्ताओं की हिस्सेदारी से अधिक हो गई। एक ओर जहां गैर निष्पादनकारी उधारकर्ताओं की हिस्सेदारी 13-14 प्रतिशत के बीच बनी हुई हैं वहीं दिसंबर 2018 तक अनरेटेड एक्सपोज़र में एनपीए की हिस्सेदारी तेजी से बढ़ कर लगभग 24 प्रतिशत हो गई। आकृति 1 से स्पष्ट होता है कि यद्यपि अधिकांश अनरेटेड उधारकर्ताओं के एक्सपोज़र छोटे हैं, गैर निष्पादनकारी अनरेटेड उधारकर्ताओं की संख्या तुलनात्मक रूप से अधिक है। यदि पर्यवेक्षी दृष्टि से देखा जाए तो ज्ञात होता है कि केवल अनरेटेड उधारकर्ताओं की बड़ी मात्रा में संख्या ही नहीं, बल्कि रेटेड श्रेणी से अनरेटेड श्रेणी में स्विच भी चिंता का विषय हो सकता है। बैंकों के मामले में यह स्पष्ट है कि उन्हें ऐसे स्विच से लाभ होगा क्योंकि रेटेड और अनरेटेड श्रेणी के जोखिम भारों के बीच यदि विनियामकीय अंतर होगा तो उनकी पूंजी आवश्यकता में कमी आएगी। उधारकर्ताओं के लिए भी अनरेटेड श्रेणी में अंतरित होना लाभकारी होगा क्योंकि वे आसन्न श्रेणीह्रास को टाल सकेंगे। सामान्य रूप से यह देखा गया है कि रेटेड से अनरेटेड श्रेणी में वे बड़े उधारकर्ता अंतरित होते हैं जिनके नाम सीआरआईएलसी में दर्ज हैं। सीआरआईएलसी में दर्ज अनरेटेड गैर निष्पादनकारी उधारकर्ता उपसमूह में से लगभग 79 प्रतिशत पहली तिमाही में अनरेटेड हो गए थे जब संबंधित बैंकों ने उन्हें एनपीए घोषित कर दिया था (सारणी 1)। तथापि इनमें से अनरेटेड गैर निष्पादनकारी उधारकर्ताओं के लगभग 54 प्रतिशत एनपीए बनने से पहले सीआरआईएलसी में अपनी अवधि के दौरान अनरेटेड थे जबकि 25 प्रतिशत ऐसे थे जिनकी एनपीए बनने से पहले कम से कम एक तिमाही में क्रे्डिट रेटिंग थी किंतु बाद की अवधि में वे अनरेटेड श्रेणी में अंतरित हो गए। अनरेटेड एक्सपोज़रों से जुड़े क्रेडिट जोखिमों का सही आकलन करने और चूंकि रेटेड से अनरेटेड स्विच पर कम पूंजी आवश्यकता होती है इसलिए ऐसे अंतरणों के लिए बैंकों के प्रोत्साहन को रोकने के लिए एक महत्वपूर्ण साधन यह है कि रेटेड और अनरेटेड एक्सपोज़रों के बीच जोखिम भारों का जो विनियामकीय अंतर है उसे समाप्त कर दिया जाए जो कि रिज़र्व बैंक ने अगस्त 2016 में किया था। एससीबी के लिए लागू विवेकपूर्ण विनियामकीय दिशानिर्देशों को संशोधित किया गया था जिसके तहत कार्पोरेट्स, एसेट फिनान्स कंपनियों (एएफसी) और गैर बैंकिंग वित्तीय कंपनियों-इन्फ्रास्ट्रक्चर फिनान्स कंपनी (एनबीएफसी-आईएफसी) (जिन्हें बैंकिंग प्रणाली से 1 बिलियन रुपए से अधिक का सकल एक्सपोज़र है) के मामले में, जिनके एक्सपोज़र पहले रेटेड थे और बाद में अनरेटेड हो गए, दिए गए ऋणों के लिए जोखिम भारों को बढ़ाकर 150 प्रतिशत कर दिया गया था। इसके अलावा बैंकों की निवेशसूचियों को रेटिंग देने हेतु बढ़ावा देने के लिए ऐसे कार्पोरेट, एएमसी, एनबीएफसी-आईएफसी जिनको बैंकिंग प्रणाली से सकल रूप से 2 बिलियन रुपए से अधिक का एक्सपोज़र है, के सभी अनरेटेड ऋणों के जोखिम भार को बढ़ा कर 150 प्रतिशत कर दिया गया। अर्थात यह भार उन भारों के बराबर कर दिए गए जो कार्पोरेट्स को दिए गए बीबी या उससे कम2 रेटिंग वाले दीर्घावधि ऋणों के लिए तय किए गए थे। इस पॉलिसी में निर्धारित एक्सपोज़र की न्यूनतम सीमा और समय सीमा, जिसके बाद यह पॉलिसी लागू हुई, एक ऐसा समुचित अनुसंधान डिजाइन उपलब्ध कराती है जिससे कि इस बात का अनुमान लगाया जा सकता है कि इस पॉलिसी से उधारकर्ताओं की रेटिंग स्थिति पर, विशेषकर रेटेड से अनरेटेड स्विच के मामले में, उसका क्या असर हुआ है। एक्सपोज़र न्यूनतम सीमा के कारण स्पष्ट रूप से दो समूह बन जाते हैं – एक वह जिनको 1 बिलियन रुपए से कम का प्रणालीगत एक्सपोज़र है। यह समूह इस पॉलिसी से प्रभावित नहीं होता। दूसरा समूह वह है जिसे 1 बिलियन रुपए से अधिक का प्रणालीगत एक्सपोज़र प्राप्त है। यह वह समूह है जिस पर यह पॉलिसी लागू होती है। हमने इस न्यूनतम सीमा के आस-पास के एक अल्प दायरे में इस पॉलिसी के असर का अध्ययन करने के लिए रिग्रेशन डिस्कंटिन्यूटी डिजाइन (आरडीडी) में इस एक्सपोज़र की न्यूनतम सीमा का उपयोग किया। इसमें मुख्य बात यह है कि 1 बिलियन रुपए की न्यूनतम सीमा से नीचे और ऊपर के अल्प दायरे (इस अध्ययन में 100 मिलियन रुपए निर्धारित किया गया) में आने वाले उधारकर्ता सभी दृष्टि से तुलनायोग्य हैं किंतु ऐसे उधारकर्ता जिन्हें, उदा. 1.03 बिलियन रुपए का प्रणालीगत एक्सपोज़र हो, उन पर यह पॉलिसी लागू होती है जबकि 0.98 बिलियन रुपए राशि जैसे एक्सपोज़र वाले उधारकर्ता पर यह पॉलिसी लागू नहीं है। आरडीडी फ्रेमवर्क इन दो समूहों के उधारकर्ताओं के संबंध में परिणामों की तुलना करता है। यदि अधिकांश बिंदुओं पर इन दो समूहों के उधारकर्ताओं की तुलना की जा सकती हो तो यह माना जा सकता है कि इस पॉलिसी के लागू होने के बाद नतीजों में जो परिवर्तन दिखाई दिए वह केवल इस पॉलिसी के कारण हुए।3 एक्सपोज़र की न्यूनतम सीमा के आस-पास के अल्प दायरे के भीतर इस पॉलिसी के असर का मूल्यांकन करने के लिए आरडीडी एक स्वच्छ दृष्टिकोण उपलब्ध कराता है, किंतु न्यूनतम सीमा से जैसे-जैसे अंतर बढ़ता है इसकी उपयोगिता घटती जाती है। अत: 0.98 बिलियन रुपए राशि जैसे एक्सपोज़र वाले उधारकर्ता को अधिकांश बिंदुओं पर 1.02 बिलियन रुपए राशि जैसे एक्सपोजर वाले उधारकर्ता के साथ भले ही तुलनात्मक होने की बात कही जाती हो, किंतु यही बात 0.7 बिलियन रुपए और 1.4 बिलियन रुपए के एक्सपोज़र वाले उधारकर्ताओं के लिए नहीं कही जा सकती। चूंकि अन्य बिंदुओं पर इन उधाकर्ताओं में भिन्नता हो सकती है, परिणामों में हुए परिवर्तन के बारे में यह नहीं का जा सकता कि वे पूर्णतया इस पॉलिसी के कारण हुए हैं। इस संबंध में आरडीडी आकलन नीतिगत न्यूनतम सीमा के एक अल्प दायरे की सीमा तक ही वैध है जो लोकल एरिया ट्रीटमेंट इफेक्ट (एलएटीई) की जानकारी देता है और साथ ही इस रीसर्च डिजाइन की बाह्य वैधता पर चिंता पैदा करता है। बाह्य वैधता की चिंता का समाधान करने के लिए हमने इस पॉलिसी प्रयोज्यता में समय-विविधता का भी उपयोग किया। इसके अलावा सुपरिभाषित ट्रीटमेंट और कंट्रोल समूह बनाए गए ताकि डिफरेन्स इन डिफरेन्स फ्रेमवर्क का उपयोग करते हुए सभी उधारकर्ताओं के संबंध में रेटेड से अनरेटेड श्रेणी में स्विच पर इस पॉलिसी के आकस्मिक असर का आकलन किया जा सके। इस रणनीति के अंतर्गत हम उधारकर्ताओं के दो समूहों (1 बिलियन रुपए से कम और अधिक एक्सपोज़र) के बीच पॉलिसी परिवर्तन के पहले और बाद की अवधि में हुए परिवर्तनों के नतीजों की तुलना करते हैं। 2 डेटा और प्रयोगसिद्ध रणनीति यह अध्ययन सीआरआईएलसी के उधारकर्ता स्तर के आंकड़ों पर आधारित है, जिसमें 18 तिमाहियों (जून 2014 से सितंबर 2018 तक) के आंकड़ों को शामिल किया गया है। दीर्घकालीन होरिज़न, पॉलिसी के मूल्यांकन के हेतु प्रत्येक आठ तिमाहियों के लिए ट्रीटमेंट से पूर्व और ट्रीटमेंट के बाद के आंकड़े प्रदान करता है। हम पॉलिसी के बारे में पूर्व ज्ञान से प्रभावित होने वाले उधारकर्ताओं के व्यवहार से संबंधित किसी भी चिंता को दूर करने के लिए ट्रीटमेंट से पूर्व अवधि में से जून 2016 की तिमाही को हटा रहे हैं। सीआरआईएलसी में अवलोकन की इकाई उधारकर्ता-बैंक है। जैसा कि बैंकिंग प्रणाली में उधारकर्ताओं के कुल एक्सपोज़र पर पॉलिसी लागू है, एक निश्चित तिमाही में बैंकिंग प्रणाली में उधारकर्ता का कुल एक्सपोज़र प्राप्त करने के लिए सभी बैंकों में किसी एक उधारकर्ता के निधिक एक्सपोज़र को संकलित (एक उधारकर्ता के लिए जिसके कई बैंकों से संबंध हैं) किया गया है। इसके अलावा, केवल कॉर्पोरेट्स, एएफसी और एनबीएफसी-आईएफसी के एक्सपोज़र को इन गणनाओं के लिए माना गया है। जैसे कि पहले ही बताया गया है, पॉलिसी की प्रयोज्यता के लिए एक तीव्र थ्रेसहोल्ड की मौजूदगी दो अलग-अलग प्रयोगसिद्ध रणनीतियों के माध्यम से कारण-संबंधी पहचान की अनुमति देती है। पहला एक तीव्र आरडीडी है जिसमें 1 बिलियन रुपये के एक्सपोज़र थ्रेसहोल्ड का उपयोग किया गया है। तर्कसंगत मान्यता के तहत यह कि थ्रेसहोल्ड के दोनों ओर उधारकर्ता तुलनीय हैं, उधारकर्ताओं द्वारा थ्रेसहोल्ड के चारों ओर एक संकीर्ण बैंडविड्थ के भीतर रेटेड से अनरेटेड में स्विच करने की सापेक्ष संभावना अनुमानित है4। यदि पॉलिसी प्रभावी है, तो हमें थ्रेसहोल्ड के दाहिनी ओर स्थित उधारकर्ताओं के लिए स्विच करने की संभावना में तीव्र गिरावट की उम्मीद है। इस दृष्टिकोण को लागू करने के लिए, हम पहले द्विआधारी चर 1 को प्रत्यावर्तित करने के लिए एक रैखिक संभाव्यता मॉडल का उपयोग करते हैं यदि उधारकर्ता ने तिमाही में उधारकर्ता की परिसंपत्ति श्रेणी पर (लैग्स सहित) (उधारकर्ताओं के एनपीए और विशेष उल्लेख खाते की (एसएमए) स्थिति के संदर्भ में), एक्सपोज़र में एक द्विघात, और उधारकर्ता-वर्ष, उद्योग-तिमाही, बैंक और क्रेडिट-रेटिंग निश्चित प्रभाव पर किसी रेटेड श्रेणी से अनरेटेड श्रेणी में स्विच किया है। अवलोकन योग्य उधारकर्ता, बैंक और समय विशेषताओं के आंशिक रूप से हटाने के बाद हम इस विनिर्देशन से शेष प्राप्त करते हैं, जो एक उधारकर्ता की रेटेड श्रेणी से अनरेटेड श्रेणी में स्विच करने की संभावना की जानकारी देते हैं। इसके बाद, हम 0.9 बिलियन और 1.1 बिलियन रुपये की श्रेणी में 0.01 बिलियन के प्रत्येक 20 समान अंतरालों में इस शेष का औसत प्राप्त करते हैं। यद्यपि एक कारक ट्रीटमेंट प्रभाव उत्पन्न करने के लिए एक्सपोज़र थ्रेसहोल्ड का उपयोग करता है, जैसा कि पहले उल्लेख किया गया था, इसमें यह नुकसान है कि यह केवल स्थानीय औसत ट्रीटमेंट प्रभाव (LATE) को कैप्चर करता है। आरडीडी अनुमान केवल संकीर्ण बैंडविड्थ में ही मान्य है, जो डिजाइन की बाहरी वैधता पर सवाल उठाता है। इस प्रतिबंध को दूर करने के लिए, हम पॉलिसी के कारण संबंधी औसत प्रभाव की पहचान करने के लिए DiD फ्रेमवर्क में पॉलिसी की प्रयोज्यता में समय भिन्नता के अलावा एक्सपोज़र थ्रेसहोल्ड से उधारकर्ता की दूरी पर ध्यान दिए बिना स्पष्ट रूप से परिभाषित ट्रीटमेंट और कंट्रोल ग्रुप्स की मौजूदगी को जोड़ते हैं। यह भी उधारकर्ता-वर्ष, उद्योग-तिमाही, बैंक और क्रेडिट-रेटिंग निश्चित वस्तुओं पर प्रतिबंधात्मक है। इसके अतिरिक्त, हम उधारकर्ता के एक्सपोज़र में उधारकर्ताओं की परिसंपत्ति श्रेणी की स्थिति (लैग्स सहित) और द्विघात को नियंत्रित करते हैं। 3 परिणाम: विवरणात्मक विश्लेषण प्रयोगसिद्ध प्रक्रिया से प्राप्त परिणामों पर चर्चा करने से पहले, हम कुछ वर्णनात्मक रुझान प्रस्तुत करेंगे, जो उधारकर्ताओं के रेटेड से अनरेटेड में स्विच करने की संभावना से संबंधित है। 1. स्विच करने वाले उधारकर्ताओं के अनुपात में कुल गिरावट उधारकर्ताओं को उनके कुल एक्सपोज़र पर आधारित 1 बिलियन रुपये की पॉलिसी थ्रेसहोल्ड के आधार पर दो श्रेणियों में विभाजित करने पर, हम समय के साथ एक तिमाही में रेटेड उधारकर्ताओं से अनरेटेड उधारकर्ता में स्विच होने वाले उधारकर्ताओं की संभावना में गिरावट (अप्रतिबंधित) देखते हैं (आकृति 3)। तथापि, पॉलिसी के तुरंत बाद की तिमाहियों में 1 बिलियन रुपये से अधिक के एक्सपोज़र वाले उधारकर्ताओं के लिए कोई विशिष्ट विभेदक रुझान प्रत्यक्ष नहीं है (अगस्त 2016- आकृति 3 में लाल रेखा से प्रदर्शित किया गया है)। 2. नीतिगत बदलाव के बाद स्विच करने वाले उधारकर्ताओं के अनुपात में गिरावट हम ट्रीटमेंट से पूर्व और ट्रीटमेंट के बाद की दोनों अवधियों में (एक सहज अप्रतिबंधित DiD आकलनकर्ता के सार में)5 रेटेड उधारकर्ताओं से अनरेटेड श्रेणी में स्विच करने की कुल और तिमाही औसत संभावना की गणना करते हैं। चित्र 4ए तिमाहियों में स्विचिंग की औसत संभावना प्रस्तुत करता है और दिखाता है कि त्रैमासिक अप्रतिबंधित DiD गुणांक 0.01 था, जो यह संकेत देता है कि पॉलिसी वास्तव में ट्रीटेड उधारकर्ताओं के लिए स्विचिंग व्यवहार को कम करती है। 3. पीएसबी के स्विच करने वाले उधारकर्ताओं के अनुपात में अधिक गिरावट चूंकि ट्रीटमेंट बैंक के स्तर पर हुआ है, अतः हमें आशा है कि कम पूंजी वाले बैंक यह सुनिश्चित करने में अधिक सक्रिय होंगे कि पॉलिसी द्वारा प्रभावित अतिरिक्त पूंजी आवश्यकताओं से बचने के लिए उधारकर्ता निवेश ग्रेड में रेटेड बने रहें। चूंकि पीएसबी में आम तौर पर पीवीबी की तुलना में कम पूंजी अनुपात होता है, इसलिए स्विचिंग की संभावना दो बैंक समूहों के लिए अलग-अलग अनुमानित की गई थी। जैसा कि आकृति 4बी में देखा जा सकता है कि पॉलिसी का प्रभाव पीएसबी के लिए ज्यादा मजबूत था। पीवीबी के लिए भी संभावना में गिरावट आई है (आकृति 4सी), लेकिन यह उधारकर्ताओं के ट्रीटमेंट और कंट्रोल दोनों समूहों में हुआ हैं। हम ट्रीटमेंट से पूर्व और ट्रीटमेंट के बाद की पूरी अवधि में उधारकर्ताओं की स्विचिंग की संभावना की तुलना करते हैं। यहां ब्याज का परिणाम यह है कि क्या उधारकर्ता ट्रीटमेंट से पूर्व और ट्रीटमेंट के बाद की पूरी अवधि में कम से कम एक बार रेटेड श्रेणी से अनरेटेड श्रेणी में स्विच हुआ है, भले ही स्विचिंग की तिमाही कुछ भी हो। इस प्रक्रिया से DiD का अनुमान 0.04 (आकृति 4डी) था और पीएसबी (आकृति 4ई) द्वारा पुन: संचालित किया गया था। सामूहिक रूप से, वर्णनात्मक रुझान से संकेत मिलता है कि पॉलिसी, उधारकर्ताओं के बीच रेटेड से अनरेटेड में स्विचिंग को कम करने में प्रभावी थी। 4 परिणाम: अर्थमितीय विश्लेषण हम पूर्वगामी अनुभाग में चर्चा किए गए नवीन DiD आकलक का प्रयोग करते हुए किए गए अवलोकन के सहयोग के लिए आरडीडी आकलन पर आधारित अधिक सटीक परीक्षण का प्रयोग करते हैं। अवलोकनीय उधारी विशेषताएँ और आकृति 5 में दिये गए उधारकर्ता के प्रणालीगत एक्सपोजर पर आधारित 20 बराबर स्पेस एक्सपोजर बिन हेतु समय स्थिर फैक्टर (बैंक और उद्योग तिमाही नियत प्रभाव) को आंशिक रूप से बाहर निकालने के बाद अवशेष की गणना की गई। प्रत्येक सर्कल उस एक्सपोजर अंतराल के अंदर रेटड से अनरेटड श्रेणी से उधारीकर्ता स्विचिंग संभावना प्रस्तुत करता है। लाइन लिनियर फिट प्रस्तुत करता है और आच्छादित क्षेत्र 95 प्रतिशत कोन्फ़िडेंस अंतराल है।

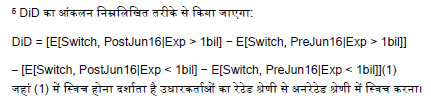

DiD विनिर्देश का प्रयोग उधारकर्ता से पूरा नमूना लेने के लिए किया जाता है जिससे सुपरिभाषित प्रतितथ्यात्मक समूह (₹ 1 बिलियन और उससे कम के कुल एक्सपोजर के उधारकर्ता जो पॉलिसी से अप्रभावी है) और पॉलिसी प्रयोज्यता में समय विविधता पर आधारित उधारकर्ता के स्विचिंग की संभावना पर पॉलिसी के प्रभाव का आकलन किया जा सके (सितंबर 2016 तिमाही के पहले और बाद)। सारणी 3 में पहला कॉलम सभी उधारकर्ता-विशिष्ट कोवेरिएट्स को शामिल नहीं करता है (किन्तु उधारकर्ता -वर्ष, बैंक उद्योग-तिमाही और क्रेडिट रेटिंग प्रभावों को शामिल करता है) और दिखाता है कि पॉलिसी में अनरेटड श्रेणी6 में उधारकर्ता के स्विचिंग की संभावना में 50 प्रतिशत कमी हुई। कॉलम (2) यह दिखाता है कि उधारकर्ता विशिष्ट कोवेरिएट्स के जुड़ने से न ही इसके सह-प्रभावी आकार या इसकी शुद्धता7 पर प्रभाव डालता है। जैसा सभी 8 पोस्ट ट्रीटमेंट तिमाहियों पर ट्रीटमेंट के प्रभाव का आकलन किया गया, यह पाया गया कि पॉलिसी से लंबी अवधि में उधारकर्ता की स्विचिंग की संभावना में कमी का लगातार प्रभाव देखा गया है। कॉलम (3) केवल जून 2015 से सितंबर 2017 के बीच के डेटा का उपयोग करके विशेष विवरण का आगणित प्रदान करता है और दर्शाता है कि पॉलिसी लागू होने के एक साल के भीतर इसका प्रभाव पड़ा। अंत में, पॉलिसी का पीएसबी और पीवीबी पर विभेदक प्रभाव की जांच करने के लिए कॉलम (4) में ट्रिपल डिफरेंस का आकलन किया गया है। आकृति 8 के अनुरूप परिणाम दर्शाते हैं कि पीएसबी के लिए यह ट्रीटमेंट अधिक प्रभावी रहा। यद्यपि इसका सीधा प्रभाव नकारात्मक है, यह दर्शाता है कि पीवीबी में 1 बिलियन रुपये से अधिक एक्सपोज़र वाले उधारकर्ताओं का पॉलिसी के बाद अंतरित होने की ओर कम संभावना दिखी। ट्रिपल इंटरएक्शन कोएफ़ीसेंट नकारात्मक तथा सांख्यिकीय रूप से उल्लेखनीय था जो यह दर्शाता है कि ट्रीटमेंट का पीएसबी उधारकर्ताओं पर व्यापक असर रहा। संक्षेप में, परिणाम दर्शाते हैं कि पॉलिसी हस्तक्षेप का उधारकर्ता के रेटेड श्रेणी से अनरेटेड श्रेणी में स्विच करने की संभावना पर आर्थिक और सांख्यिकीय रूप से महत्वपूर्ण प्रभाव पड़ता है। आर्थिक दृष्टि से, ₹ 1 बिलियन से अधिक के उधारकर्ताओं में स्विच करने की संभावना रेटेड श्रेणी के 100 उधारकर्ताओं में से 8 से कम होकर 4 पर आ गई है जो पीएसबी के प्रभावों द्वारा संचालित है। महत्वपूर्ण रूप से, पॉलिसी के प्रभाव समय के साथ लगातार बने रहे और पॉलिसी से लगभग दो साल बाद भी दिखाई दे रहे थे। 5 निष्कर्ष बैंकों में पूंजी पर्याप्तता के मूल्यांकन में क्रेडिट रेटिंग के व्यापक उपयोग से अनरेटेड एक्सपोज़र बैंकों के साथ-साथ पर्यवेक्षक के लिए भी सूचना अवरोध उत्पन्न कर सकती है। बैंकिंग प्रणाली में बड़े अनरेटेड एक्सपोज़र की व्यापकता को देखते हुए, इस प्रकार के एक्सपोज़र के लिए जोखिम भार में वृद्धि हेतु रिज़र्व बैंक द्वारा किए गए पॉलिसी उपाय संभावित विनियामक मध्यस्थता को नियंत्रित करने और बैंकों को रेटेड एक्सपोज़र के लिए प्रोत्साहित करने की ओर एक कदम है। जैसा कि स्टडी में दिखाया गया है, पॉलिसी का बड़े उधारकर्ताओं के बीच रेटेड से अनरेटेड श्रेणी में स्विच करने को कम करने में वांछित प्रभाव पड़ा है। इसका प्रभाव पीएसबी और पीवीबी दोनों पर स्पष्ट दिखता है और पीएसबी पर विशिष्ट रूप से अधिक है। रिज़र्व बैंक द्वारा अनरेटेड एक्सपोज़र के लिए जोखिम भार में वृद्धि का फैसला प्रचलित बीसीबीएस दिशा-निर्देश8 से भिन्न है। चूंकि बीसीबीएस ने भी क्रेडिट जोखिम के लिए मानकीकृत दृष्टिकोण में संशोधन का सुझाव दिया है और अनरेटेड एक्सपोज़र के लिए जोखिम भार को बाद में 2017 में पुनर्गठित किया है इसलिए इस निर्णय को दूरदर्शी भी माना जा सकता है।9 यद्यपि जोखिम भार में वृद्धि एक बार का उपयुक्त विनियामक उपाय है, फिर भी बैंकों द्वारा बैंक -उधार कर्ता संबंध के इतिहास और बाजार स्रोतों से एकत्रित जानकारी का उपयोग करके व्यापक अनरेटेड एक्सपोज़र की निरंतर निगरानी आवश्यक है। इसके अलावा, बैंक इस तथ्य को अनदेखा नहीं कर सकते हैं कि उधारकर्ता की क्रेडिट गुणवत्ता पर की जाने वाली बाह्य रेटिंग उनके द्वारा की जा रही आंतरिक समुचित सावधानी का विकल्प नहीं हो सकती है। 6 संदर्भ आल्टमेन, ई., एस. भरत, एंड ए. सांडर्स (2002). “क्रेडिट रेटिंग्स एंड द बीआईएस कैपिटल एडिकव्सि रिफॉर्म एजेंडा।” जर्नल ऑफ बैंकिंग फ़ाईनेन्स। 26(5). बीसीबीएस (2017). “हाई-लेवल समरी ऑफ बासेल III रिफार्म्स।“ https://www.bis.org/bcbs/publ/d424-hlsummary.pdf पर डाउनलोड हेतु उपलब्ध निनी, जी. (2004). “द रोल ऑफ लोकल बैंक्स इन प्रोमोटिंग एक्सटरनल फ़ाईनेन्स: अ सिंडीकेटड़ लेंडिंग टु इमरजिंग मार्केट बोरोवर्स।” सीजीएफ़एस वर्किंग ग्रुप ऑन फ़ाईनेन्सशियल सेक्टर एफ़डीआई। स्मिथ, डी. (2003). “लोन्स टु जापानीस बोरोवर्स।” जर्नल ऑफ जापानीस एंड इंटेरनेशनल इकोनॉमिक्स।17. * लेखक बैंकिंग पर्यवेक्षण विभाग में क्रमश: निदेशक और प्रबंधक (अनुसंधान) के पद पर कार्यरत हैं। इस अध्ययन में व्यक्त दृष्टिकोण और विचार लेखकों के हैं और जरूरी नहीं कि वे भारतीय रिज़र्व बैंक के दृष्टिकोण को व्यक्त करते हों। 1 सामग्री में अनरेटेड उधारकर्ताओं का संबंध अधिक ऋण जोखिम और कम पारदर्शिता से है। स्मिथ (2003) और निनि (2004) देखें। 2 विभिन्न रेटिंग श्रेणी के जोखिम भारों हेतु https://rbi.org.in/Scripts/NotificationUser.aspx?Id=10569&Mode=0 पर 25 अगस्त 2016 का ‘रिव्यू ऑफ प्रूडेन्शियल नॉर्म्स रिस्क् वेट्स फॉर एक्सपोज़र टू कॉर्पोरेट्स, एएफसी और एनबीएफसी-आईएफसी’ तथा https://rbidocs.rbi.org.in/rdocs/content/pdfs/58BS300685FL.pdf पर 31 मार्च 2016 का ‘बेसल-।।। कैपिटल रेग्यूलेशन’ देखें। 3 इस परिदृश्य में रिग्रेशन डिस्कंटिन्यूटी डिजाइन (आरडीडी) में निहित एक चिंता यह है कि एक्सपोज़रों में संवृद्धि के संबंध में उधारकर्ताओं के पास अपनी निजी जानकारी होती है और पॉलिसी का उल्लघंन करते हुए वे 1 बिलियन रुपए की न्यूनतम सीमा पार करने से पहले अनरेटेड श्रेणी में अंतरित हो सकते हैं। यदि ऐसा होता है तो हम अपेक्षा कर सकते हैं कि 1 बिलियन रुपए की न्यूनतम सीमा से कुछ ही कम वाले उधारकर्ताओं का सितंबर 2016 की बाद की अवधि में रेटेड श्रेणी से अनरेटेड श्रेणी में जो स्विच हुआ उससे दिखाई देने वाली वृद्धि उचित नहीं थी। मजबूती संबंधी अलग जांच में हमने पता किया कि 1 बिलियन रुपए की न्यूनतम सीमा से कुछ ही कम वाले उधारकर्ता सितंबर 2016 की बाद की अवधि में स्विच संबंधी कोई विभेदात्मक दर प्रदर्शित नहीं करते जिससे प्रयोगसिद्ध रणनीति की यह चिंता दूर हो जाती है। 4 हम तालिका 2 में इसे प्रयोगसिद्ध रूप से सत्यापित करते हैं, जहां हम 1 बिलियन रुपये की पॉलिसी थ्रेसहोल्ड के प्रत्येक पक्ष पर 0.1 बिलियन / 100 मिलियन बैंडविड्थ के भीतर के उधारकर्ताओं के लिए शेष दिखाते हैं। 6 इसकी गणना कोएफ़ीसेंट रिलेटिव की तुलना पूरी अवधि के दौरान स्विच करने की संभावना के औसत (0.04/0.08) पर की जाएगी। 7 उधारकर्ता-विशिष्ट कोवेरिएट्स में उधारकर्ता के आस्ति श्रेणी का डमी (चार लैग सहित) और संबंधित बैंक से लैग्ड फंडेड बकाया राशि (चार लैग सहित) शामिल है। 8 बीसीबीएस ने अनरेटेड एक्सपोज़र (बीसीबीएस, 2017) के लिए 100 प्रतिशत जोखिम भार निर्धारित किया है। वास्तव में, अनरेटेड एक्सपोज़र पर बीसीबीएस मार्गदर्शन को साहित्य में "विवादास्पद" करार दिया गया है और अध्ययनों द्वारा तर्क दिया गया है कि मार्गदर्शन का कोई "आर्थिक या सांख्यिकीय" तर्क नहीं हैं, Altman et al. (2002) देखें। 9 इसने उधारकर्ता की चुकौती क्षमता के आधार पर अनरेटेड एक्सपोज़र को तीन ग्रेड (ए, बी और सी) में विभाजित करने की सिफारिश की है; ग्रेड सी ऐसे एक्सपोज़र को दर्शाता है जिसमें बैंक के 150 प्रतिशत संशोधित जोखिम भार के साथ मटीरीअलाइज़ डिफ़ॉल्ट जोखिम हो (बाहरी रेटिंग के लिए बी से कम जोखिम भार के बराबर)। क्रेडिट जोखिम के लिए संशोधित मानकीकृत दृष्टिकोण के कार्यान्वयन की तारीख 1 जनवरी 2022 (बीसीबीएस, 2017) निर्दिष्ट की गई है। |

इस पेज को शेयर करें:

आरबीआई मोबाइल एप्लीकेशन इंस्टॉल करें और लेटेस्ट न्यूज़ का तुरंत एक्सेस पाएं!

हमारा ऐप इंस्टॉल करने के लिए QR कोड स्कैन करें

पृष्ठ अंतिम बार अपडेट किया गया: