IST,

IST,

Third Bi-monthly Monetary Policy Statement, 2015-16

By Monetary and Liquidity Measures On the basis of an assessment of the current and evolving macroeconomic situation, it has been decided to:

Consequently, the reverse repo rate under the LAF will remain unchanged at 6.25 per cent, and the marginal standing facility (MSF) rate and the Bank Rate at 8.25 per cent Assessment 2. Since our last statement, global economic activity has recovered modestly in Q2 of calendar 2015. The US economy rebounded on stronger consumption growth and steadily improving labour market conditions, though recent wage data suggest continuing slack. The Euro area has grown at a moderate pace through the first half of 2015, supported by consumer spending, easing financing conditions and a modest downturn in still-high unemployment. In Japan, growth slowed in Q2 after an upside surprise in Q1. Domestic consumption is still weak, but manufacturing activity picked up in July and strengthening exports and corporate profitability could stimulate capital spending in H2. In the emerging market economies (EMEs), activity decelerated through H1 due to headwinds from weak external demand, tightening external financing conditions, deteriorating structural bottlenecks and spill overs from unsettled conditions in financial markets. Despite aggressive policy stimuli, the Chinese economy is slowing on macroeconomic rebalancing, sizable stock market corrections, a cooling property market and excess capacity in several manufacturing industries. Manufacturing activity weakened further in July, clouding near-term expectations. Recessionary conditions persist in both Russia and Brazil, with downside risks from commodity prices and geopolitical developments casting a shadow on the outlook, including for other EMEs. 3. In recent months, financial markets have experienced high turbulence due to the Greek crisis, the Chinese stock market slump and shifts between risk-on and risk-off sentiments based on changes in beliefs about when the Federal Reserve will start raising rates. Bond market sell-offs originating in Germany lifted bond yields across the world, including in EMEs, and tightened financing conditions. Equity markets were buoyed by the search for yields which stretched asset valuations until end-June, when sharp stock market corrections in China pulled down share prices globally. Currency markets were dominated by the rising US dollar, which impacted foreign currency borrowing exposures, increased exchange rate volatility and also produced sizable capital outflows from EMEs. Investors have reduced exposures to EMEs as an asset class, but a generalised flight to safety is yet to be seen. Investors have also shunned commodities affected by the Chinese slowdown, including bullion. 4. In India, the economic recovery is still work in progress. After strong rainfall in June, July has been below par, but on net, the monsoon is near normal. Higher reservoir levels also auger well for the prospects of kharif output, particularly for areas that are dependent on irrigation. Consequently, kharif sowing has expanded significantly relative to a year ago, especially in respect of oilseeds, pulses, rice and coarse cereals. These developments, supported by contingency plans for vulnerable districts, provide cushion against adverse weather shocks. If prospects of a good harvest strengthen, currently weak rural demand will improve to provide an important boost to activity. Shrinking exports in some industries, in part a result of weak global demand and global overcapacity in those industries and in part a result of the significant depreciation of currencies of some major trading partners against the rupee, also contributed to weak aggregate demand. The Reserve Bank’s survey-based indicators point to flat capacity utilisation and new orders, with corporate sales growth declining – although lower inflation explains some of the compression in top lines. Although overall business confidence is positive, the level of optimism was a shade lower in April-June than in the preceding quarter. Investment, as measured by new projects, is still weak, primarily because of still-low capacity utilization. In the critically important power sector, where final demand is strong, the recent step-up in generation in response to the commendable easing of bottlenecks in coal supply is being partly negated by structural problems relating to clogging of transmission grids and the dire financial state of electricity distribution companies (DISCOMs). 5. However, there are signs that consumption demand, especially in urban areas, is picking up. Car sales for July were strong. Nominal bank credit growth is lower than previous years, but adjusted for lower inflation as well as for lower borrowing by oil marketing companies and increased borrowing from commercial paper markets, credit availability seems to be adequate for most sectors. 6. The services sector continues to emit mixed signals. The pick-up in heavy commercial vehicle sales and rising port and domestic air freight in Q1 suggest strengthening transportation activity (for Indian data, Q refers to fiscal year quarters). Purchasing managers’ indices were in contraction zone in June, mainly due to lower new and existing business conditions. Survey-based expectations of the outlook for the services sector point to positive sentiment in Q2 on the back of an expected increase in turnover and profit margin. 7. Headline consumer price index (CPI) inflation rose for the second successive month in June 2015 to a nine-month high on the back of a broad based increase in upside pressures, belying consensus expectations. The sharp month-on-month increase in food and non-food items overwhelmed the sizable ‘base effect’ in that month. Food inflation rose 60 basis points over the preceding month, driven by a spike in prices of vegetables, protein items - especially pulses, meat and milk - and spices. 8. Furthermore, excluding food and fuel, inflation rose in respect of all sub-groups other than housing. The momentum of price increases remained high for education. Inflation pressures increased for personal care and effects and household goods and services sub-groups. Inflation in CPI excluding food, fuel, petrol and diesel has been rising steadily since April and exceeded headline inflation through Q1. Near-term inflation expectations of households returned to double digits after two quarters, although those of professional forecasters remained anchored. Rural wage growth was moderate but there are indications of incipient pressures from corporate staff costs. 9. Liquidity conditions have been very easy in June and July. A seasonal reduction in demand for currency and increased spending by Government coupled with structural factors such as low credit deployment relative to the volume of deposit mobilisation contributed to surplus conditions in the money markets. This resulted in a significantly lower average daily net liquidity injection under the fixed rate repos under LAF, and variable rate term repo/reverse repo and MSF at ₹477 billion in June, down from ₹1031 billion in May. In July there was net absorption of ₹120 billion through these facilities. In response to the reduction in the policy repo rate in June the weighted average call rate eased from 7.47 per cent in May to 7.11 per cent in June. The Reserve Bank also conducted open market sales worth ₹83 billion in the second week of July, essentially in response to lack of demand for longer duration reverse repos. The call money rate remained below the repo rate through July, reflecting comfortable liquidity conditions. 10. Headwinds from weak global demand conditions restrained merchandise exports. The contraction in exports in Q1 of 2015-16, both volume and value, was the steepest since Q2 of 2009-10. The sharp fall in international commodity prices - especially crude oil - compressed import payments, helping to narrow the trade deficit. Domestic production shortages and lower international prices were, however, evident in higher imports of electronic goods, pulses, iron ore and fertilisers. Net surpluses on account of trade in services were sustained in Q1 and have, along with the lower trade deficit, helped reduce the current account deficit (CAD). Despite slowing portfolio flows, other forms of foreign capital flows such as foreign direct investment and non-resident deposits were sustained. With the shrinking external financing requirement, reserves were built up to an all-time high at the end of June, providing a buffer against adverse global shocks. Policy Stance and Rationale 11. The bi-monthly policy statements of April and June indicated that the accommodative stance of monetary policy will be maintained going forward, but monetary policy actions will be conditioned by (a) fuller transmission by banks of the Reserve Bank’s front-loaded rate reductions into their lending rates; (b) developments in food prices and their management, especially the effects of the monsoon, while looking through both seasonal as well as base effects; (c) a continuation and even acceleration of policy efforts to unclog the supply side so as to make available key inputs such as power and land, as also repurposing of public spending from poorly targeted subsidies towards public investment and reducing the pipeline of stalled investment; and (d) signs of normalisation of the US monetary policy. In the June statement, it was pointed out that a targeted infusion of bank capital is also warranted so that adequate credit flows to the productive sectors as investment picks up. 12. Since the first rate cut in January, the median base lending rates of banks has fallen by around 30 basis points, a fraction of the 75 basis points in rate cut so far. As loan demand picks up in Q3 of 2015-16, banks will see more gains from cutting rates to secure new lending, and more transmission will take place. The welcome announcement by Government of infusion of bank capital into public sector banks will help loan growth and hence transmission, as will currently easy liquidity conditions. 13. During 2015-16 so far, inflation conditions have evolved around the path projected in April and June bi-monthly policy statements, though they surprised somewhat on the upside in June. Large base effects, which the Reserve Bank will look through, are expected to pull down headline inflation in July and August. From September, favourable base effects wane. 14. Turning to the balance of inflation risks, most worrisome is the sustained hardening of inflation excluding food and fuel. Moreover, the full effects of the service tax increase, which took effect from June, will feed through over the rest of the year. Some food prices, particularly of protein-rich items, pulses and oilseeds have risen sharply in recent months. They will have to be carefully monitored as they tend to be sticky and impart an upward bias to inflation and inflation expectations. This assumes significance in view of households’ inflation expectations rising again. Several factors, however, could have a significant mitigating influence. These include the sharp fall in crude prices since June and the likelihood of this softness persisting in view of the global supply glut and expanding production by Iran; the welcome increase in planting of pulses and oilseeds and prospects of rainfall in August and September according to some forecasters; the effects of the Government’s current pro-active supply management to contain shocks to food prices, especially of vegetables, alongside its decision to keep increases in minimum support prices moderate. 15. Relative to the projections of the second bi-monthly statement, inflation projections in this bi-monthly statement are elevated by the higher than expected June observation but reduced by prospects of softer crude prices and a near-normal monsoon thus far. This implies that inflation projections for January-March 2016 are lower by about 0.2 per cent, with risks broadly balanced around the target of 6.0 per cent for January 2016 (Chart 1). 16. Taking into account all this, and given that policy action was front-loaded in June, it is prudent to keep the policy rate unchanged at the current juncture while maintaining the accommodative stance of monetary policy. Short term real risk free rates are nevertheless supportive of borrowing by interest rate sensitive consumer segments such as housing and automobiles. Significant uncertainty will be resolved in the coming months, including the likely persistence of recent inflationary pressures, the full monsoon outturn, as well as possible Federal Reserve actions. As the Reserve Bank awaits greater transmission of its front-loaded past actions, it will monitor developments for emerging room for more accommodation. 17. The outlook for growth is improving gradually. Favourable real income effects could accrue from weaker commodity prices, in particular crude oil, and a possible step-up in agricultural activity if monsoon conditions continue to improve. On the other hand, global growth projections for 2015 have generally been revised downwards and, therefore, the export contraction could become a prolonged drag on growth going forward. Notwithstanding some improvement in the state of stalled projects, supply constraints continue to be binding and new investment demand emanating from the private sector and the central Government remains subdued. On an assessment of the evolving balance of risks, the projected output growth for 2015-16 has been retained at 7.6 per cent (Chart 2). 18. The fourth bi-monthly monetary policy statement will be announced on September 29, 2015. Alpana Killawala Press Release : 2015-2016/297 |

Share this page:

Install the RBI mobile application and get quick access to the latest news!

Scan the QR code to install our app

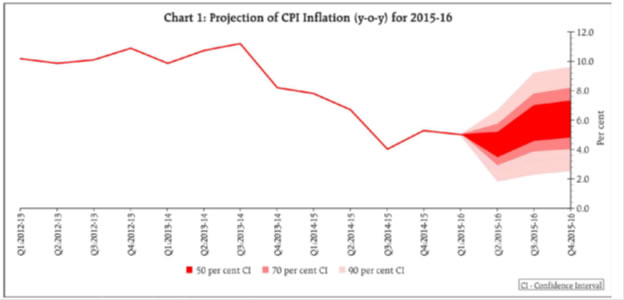

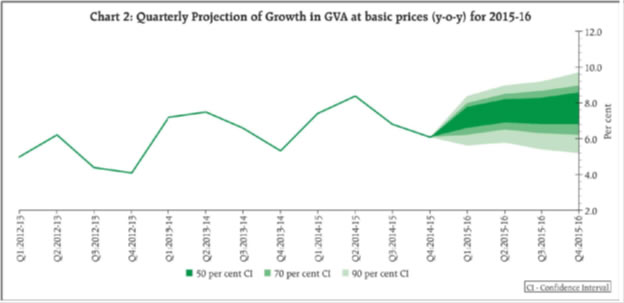

Page Last Updated on: