IST,

IST,

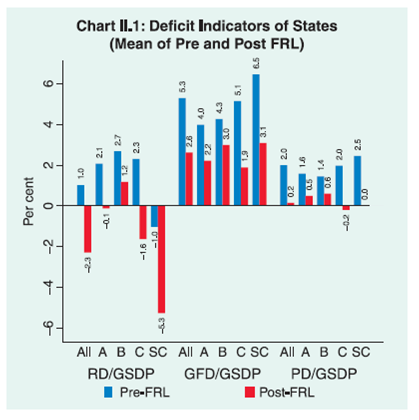

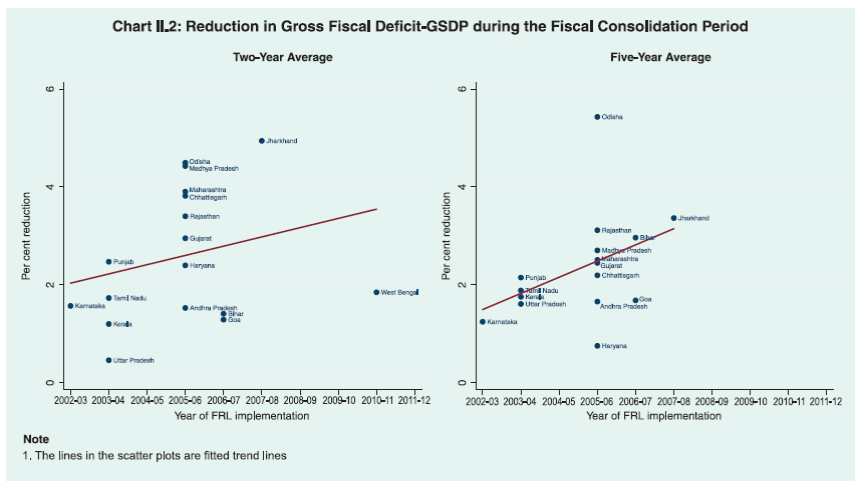

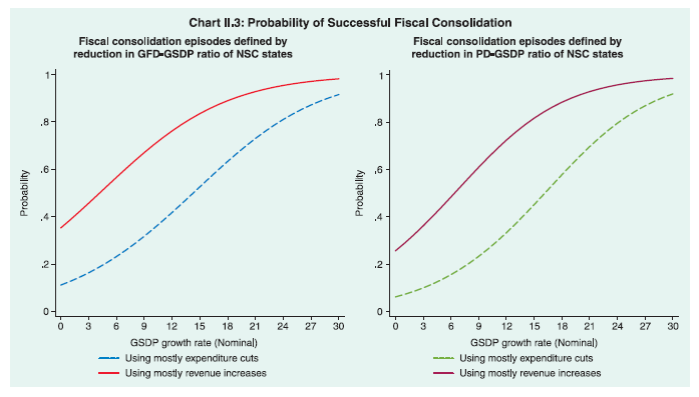

II. Fiscal Consolidation: Assessment and Medium Term Prospects

States have recommitted to fiscal consolidation under their Fiscal Responsibility and Budget Management Acts. Empirical evidence presented in this chapter shows that fiscal correction among states has not been at the cost of growth. More emphasis is required on the quality of fiscal consolidation. Medium-term fiscal consolidation would be determined by factors such as efficient utilisation of the enhanced resources through tax devolution under the Fourteenth Finance Commission award, states’ preparedness for the proposed GST, efforts to mobilise non-tax revenue, impact of pay revisions, realistic capital outlays and an appropriate measurement of debt to include off-budget high risk liabilities. 1. Introduction 2.1 Fiscal consolidation at the sub-national level in India has been undertaken under a rule-based framework through the enactment of Fiscal Responsibility and Budget Management (FRBM) legislations by states. Five states had passed FRBM Acts before the Twelfth Finance Commission (FC-XII) award, with three states passing it even before the centre’s FRBM Act in August 20031. Twenty one states enacted FRBM legislations, incentivised by the FC-XII award in terms of debt and interest rate relief. The last entrants are West Bengal and Sikkim which enacted FRBM legislations in 2010 in response to incentives provided by the Thirteenth Finance Commission (FC-XIII2.) There are subtle variations across the states in terms of design and features of the Acts. 2.2 This chapter discusses the key aspects of this fiscal consolidation process. Section 2 reviews the literature on fiscal consolidation and its link with growth. Stylised facts on the differential impact of fiscal legislation on states’ key deficit indicators are set out in Section 3. Section 4 empirically examines the impact of fiscal consolidation on growth in the states. In Section 5, sources and composition of fiscal consolidation is examined. Finally, Section 6 concludes this chapter by setting out medium term prospects for fiscal consolidation of the states. 2. Why Does Fiscal Consolidation Matter? 2.3 The mainstream advocacy for fiscal consolidation has essentially hinged around prudent housekeeping, especially in the aftermath of periods of fiscal profligacy either to accelerate growth as in the 1980s (Giavazzi and Pagano, 1990) or to reduce public debt and limit its adverse impact on output and growth after the fiscal stimulus as in 2008-10 (Barrios et al, 2010). 2.4 Lower fiscal deficits can ease the pressure on interest rates and thereby increase investment (Mcdermott and Wescott, 1996). A cut in government spending, if perceived as durable, implies a permanent reduction in the future tax burden, generating positive expectations among various economic agents. Fiscal adjustment is found to be associated with higher growth in transition economies mainly through two channels: (i) reduced government borrowing necessity, which lower the need to monetize budget deficits; and (ii) improved policy credibility, which signal a political commitment to long-term fiscal sustainability and macroeconomic stability (Segura-Ubiergo et al., 2006). 2.5 Empirical evidence suggests that design and timing are critical to the success of fiscal consolidation. Fiscal adjustment is found to have a higher likelihood of success if it is expenditure-based (Alesina and Perotti,1995; McDermott and Wescott, 1996; Alesina and Ardagna, 1998). However, expenditure-based fiscal consolidation is also found to slow growth down when there are credit supply restrictions. A gradual fiscal consolidation based on a mix of revenue and expenditure measures can support growth, while reducing public debt (Baldacci et al., 2014). Higher initial levels of debt may also increase the probability of government pursuing successful fiscal consolidation (Barrios et al.,2010). 2.6 Sub-national fiscal consolidation in India has drawn considerable attention in the literature with a rich variety in the assessment of the extent of and manner in which the consolidation has been achieved. For instance, although conventional deficit indicators declined after the enactment of FRBM legislation, the effect of fiscal rules on fiscal performance has been found to be weak if central transfers are netted out (Simone and Topalova, 2009). Fiscal correction undertaken by the states appears smaller if only their own revenue deficits and gross fiscal deficits are considered rather than the conventional aggregate measures (Lalvani and Karnik, 2014). The extent of dependence on central transfers is relatively high for the special category states and low income states (Rao and Srivastava, 2014). Both revenue enhancement and expenditure reduction contributed to the process of fiscal correction of the states, without it being inimical to expenditure for development purposes (Misra and Khundrakpam, 2009). A more recent study, however, shows that although fiscal rules have helped, deficit targets have been met largely by reducing development expenditure (Chakraborty and Dash, 2013). 3. Fiscal Responsibility Legislations and States’ Fiscal Consolidation 2.7 A summary assessment of states’ fiscal consolidation efforts can be made in terms of key deficit indicators [as ratios of gross state domestic product (GSDP)] expressed as period averages. The time period for assessment of fiscal performance for each state is undertaken by considering a window around the implementation of FRBM legislation during 1992-93 and 2012-13. Since different states implemented these legislations at different time points, the pre-FRBM and post-FRBM periods for each state differ. Annex 1 provides the year of implementation of FRBM across states, categorised on the basis of the earliest year of FRBM implementation. States were segregated into non-special category (NSC) and special category (SC) states, with NSC states further classified into three groups on the basis of their per capita incomes3 (Annex 2). 2.8 On an average, revenue accounts of all the 17 NSC states were in deficit, prior to the enactment of FRBM. However, 12 of these states turned around and recorded revenue surpluses during the post-FRBM period. The improvement was more pronounced in the case of low-income states, all of which posted revenue surpluses. In comparison, fewer relatively affluent states - 3 out of 5 states in group ‘A’ and 2 out of 5 states in group ‘B’ - recorded revenue surpluses after the enactment of FRBM legislation. Few NSC states which had consistently high revenue deficit (RD-GSDP) ratios even after the enactment of FRBM also registered improvements. At the consolidated level, SC states’ marginal surpluses in the revenue account during the pre-FRBM period increased significantly in the post-FRBM period due to large central transfers (Chart II.1). 2.9 Prior to the FRBM enactment, the GFD of 15 out of the 17 NSC states was above 3 per cent of GSDP, on average. All group ‘A’ states as also 6 out of the 7 states in group C lowered their GFD-GSDP ratios below 3 per cent after the enactment of FRBM. In a similar vein, SC states halved their GFD-GSDP ratios during the post- FRBM period. 2.10 The primary deficits of all states also came down during the post-FRBM period. In particular, group C states which, on average, recorded the highest primary deficit in the pre-FRBM period turned around to record primary surpluses in the post-FRBM period. 2.11 To sharpen the analysis, an event study approach was undertaken. Accordingly, two windows were considered for the NSC states. The first window considers two years prior to and after the enactment of FRBM legislations, excluding the year of the legislation. As five states enacted FRBM prior to the FC-XII award period, a longer window of five years pre-and post-FRBM enactment was considered to internalise the benefits received under the FC-XII award4. Although the average reduction in the GFD-GSDP ratio of NSC states which had enacted FRBM legislation before the rest was lower than most states, the extent of reduction in both the windows were comparable except for one state which registered a steep decline in the five-year window, aided in large part by debt and interest relief under the FC-XII award (Chart II.2). 4. Fiscal Consolidation and Sub-national Growth: An Empirical Exploration 2.12 Tracing the effects of fiscal consolidation on states’ economic growth can begin by adopting the definition of a ‘tight year’. In a developing country like India, resorting to a tight fiscal policy5 on a sustained basis may not be desirable. In fact, it can prove counter-productive by constraining growth-inducing capital outlay by the government. In a federal set-up, the revenue raising capacity of states is restricted while their expenditure responsibilities are large. Consequently the definition of a ‘tight year’ may need to be dovetailed to domestic realities. Accordingly, a ‘tight year’ can be regarded as one in which the primary deficit declines by at least one per cent (alternatively, the primary surplus increases at least by one per cent), on the basis of the maximum decline observed in the primary balance of NSC states. 2.13 A fiscal consolidation episode is expansionary if the average trend growth between periods t and t+2 is greater than that between periods t-1 and t-2 (de Cos and Benito, 2011). It is possible to identify a total of 23 fiscal consolidation episodes (i.e., the primary balance improved by one per cent or more) for the NSC states after the FRBM enactment. Fiscal consolidation was expansionary in 17 of these episodes, highlighting the growth-inducing effects of consolidation6 (Table II.1). 5. Sources and Composition of Fiscal Consolidation 2.14 It is useful to drill deeper and identify the main drivers of successful consolidation episodes. Episodes of fiscal consolidation7 have been deemed as successful if the debt-GSDP ratio declined by at least 3 per centage points by the second year after fiscal tightening commenced (Mcdermott and Wescott, 1996). During the period 2000-01 to 2012-13, reduction in ratios of GFD-GSDP and PD-GSDP among NSC states was observed in 58 episodes and 49 episodes, respectively, of which 35 episodes and 26 episodes, respectively turned out to be successful (Table II.2). In the exercise conducted here, fiscal consolidation is considered to be revenue-led if the increase in revenue receipts contributes to at least 50 per cent of the reduction in GFD/PD. Alternatively, fiscal consolidation is expenditure-led if more than 50 per cent of the reduction in GFD/PD is brought about by a decrease in total expenditure (TE) or primary expenditure(PE)/GSDP, respectively. 2.15 Advancing the argument through a logistic probability model (LPM)8 using maximum likelihood estimation in which the dependent variable equals 1 if fiscal consolidation is successful and 0, otherwise, the probability of a successful fiscal consolidation for NSC states9 is higher when consolidation is primarily revenue-led, irrespective of the size of GSDP growth rate (Table II.3 and Chart II.3). A key implication of this is that the chances of achieving successful fiscal consolidation improve significantly provided the process is revenue-led (Table II.3). 2.16 A decomposition of all the revenue-led and expenditure-led fiscal consolidation episodes defined in terms of PD reduction during the post-FRBM period shows that in the years preceding the global crisis, revenue-led consolidation was largely driven by central transfers in the low-income states. States’ own revenues played a dominant role in high and middle income states. Besides own tax revenues (OTR), own non-tax revenue (ONTR), particularly from state lotteries and various user charges contributed significantly to the reduction in PD in some of these states. Post-crisis revenue-led consolidation is confined to only two states, both of which benefitted from higher central transfers (Table II.4a). 2.17 Expenditure-led fiscal consolidation during the pre-crisis period has been achieved essentially through reduction in revenue expenditure. Post-crisis expenditure-led fiscal consolidation was seen in 6 states, all of which also witnessed an increase in revenue receipts during the consolidation year (Table II.4b). With the exception of one episode when capital outlay increased, the reduction in expenditure was across the board, with development revenue expenditure contributing the most to this reduction. Most episodes of expenditure-led fiscal consolidation have resulted from reduction in capital outlay and development revenue expenditure. 6. Fiscal Consolidation: A Medium Term Perspective 2.18 Sub-national fiscal consolidation during the post-FRBM period has been largely facilitated by higher explicit and implicit transfers from the centre in the form of increased share in central taxes under the Finance Commission (FC) awards, higher tax buoyancy of central taxes during the high growth phase and interest relief provided by the centre under debt consolidation and relief facility (DCRF). The increase in own revenues, particularly after the introduction of the value added tax, also contributed to the improvement in fiscal position of NSC states with higher per capita incomes. Fiscal consolidation in the post-crisis phase has largely been expenditure-led. 2.19 Several factors will have a bearing on the capacity of states to sustain successful fiscal consolidation over the medium-term. First, the sharp increase in states’ share in tax devolution to 42 per cent of the divisible pool based on the FC-XIV’s recommendation would increase the flow of unconditional transfers to states, which would need to be deployed to meet state-specific developmental activities. Buoyancy of central taxes will obviously have a bearing on the size of transfers. 2.20 Second, transition from the present origin-based indirect tax regime to a destination-based tax regime under the proposed goods and services tax (GST) from April 1, 2016 should improve tax compliance and create a buoyant source of revenue in the medium term, notwithstanding some loss of revenue in the near term to be compensated on a tapering basis. The Union Budget for 2015-16 has taken steps to bridge the trust deficit between the centre and the states. 2.21 Third, states have to improve their efforts in mobilising non-tax revenues. Although expenditure on economic, social and general services by state governments has been rising, there has been no commensurate recovery from these services. Further, the low profitability of public sector undertakings (PSUs) also contributes to the low non-tax revenue of states. In this context, revising electricity tariffs regularly to match cost of electricity generation and supply to avoid adverse impact on fiscal health of states has been underscored (Buiter and Patel, 2010; Patel and Bhattacharya, 2010). The FC-XIV has also emphasised effective independent regulation in insulating the pricing of public utility services from avoidable policy fluctuations. Regarding revenues from natural resources, coal rich states would have windfall gains from coal block auctions, which should be utilised for funding developmental needs. 2.22 Fourth, with increased convergence of state government pay scales with those of the central government, particularly since the implementation of the fifth central pay commission, finances of states have been significantly impacted by pay revisions. In this regard, the FC-XIV, reiterating the view of the FC-XI, has called for the evolution of a national policy for salaries and emoluments through a forum such as the Inter- State Council. It has also recommended linking pay with productivity, with simultaneous focus on technology, skills and incentives and adoption of new pension schemes by those states which have not done so far. 2.23 Fifth, focus needs to be on the quality rather than the size of fiscal consolidation. Revenue surpluses posted by several states have enabled them to increase their capital outlay without undue pressure on GFD. While capital outlay has a lasting impact on growth through higher multipliers, it is important that the state governments do not make over-ambitious investment proposals which result in delays in project implementation and management with attendant cost and time overruns. The FC-XIV had recommended that both union and state governments provide a statutory ceiling on the sanction of new capital works to an appropriate multiple of the annual budget provision. Implementation of this proposal could improve the effectiveness of capital spending. 2.24 Finally, in assessing fiscal sustainability, it is important to focus attention on a broader concept of debt. Sustained efforts by the states are required to keep debt levels from rising. Furthermore, conventional debt does not include the governments’ risk exposure to PSUs due to government guarantees, off-budget borrowings and accumulated losses of financially weak PSUs. The FC-XIV has proposed a definition of extended debt to include in the overall public debt and weighted sum of guarantees of high risk public sector enterprises such as those in power and transport sectors. It has further recommended that both union and state governments adopt a template for collating, analysing and annually reporting the total extended public debt in their respective budgets. A more realistic assessment of the states’ fiscal position and along with it, a better evaluation of the magnitude and quality of states’ fiscal consolidation and its implications for overall growth and macroeconomic stability, could then emerge. 1 Based on FC-XI recommendation, a States’ Fiscal Reform Facility (FRF) scheme was introduced for the period 2000-01 to 2004-05, backed by a Fiscal Reform Facility Incentive Fund to incentivise states to collectively eliminate revenue deficits. Realising the importance of fiscal discipline, some states enacted their FRBM legislations. 2 The FC-XIII recommended that the Debt Consolidation and Relief Facility may be extended to West Bengal and Sikkim, provided they enact their FRBM Acts. All states amended their FRBM Acts in line with the recommendation of the FC-XIII. 3 Group ‘A’ constitutes the top five states in terms of their real per capita incomes [as in 2013-14]. It includes Goa, Maharashtra, Haryana, Gujarat and Tamil Nadu. Group ‘B’ constitutes the middle income states viz., Kerala, Punjab, Karnataka, Andhra Pradesh and West Bengal and group ‘C’ includes remaining NSC states i.e., Rajasthan, Jharkhand, Chhattisgarh, Madhya Pradesh, Odisha, Uttar Pradesh and Bihar. 4 West Bengal was excluded from the second window because there were not sufficient observations in the post-FRBM period as the state enacted its FRBM legislation only in 2010. 5 A tight fiscal policy is defined as one in which the ratio of the primary deficit to GDP falls (or the ratio of primary surplus to GDP increases) by at least 1.5 per centage points [Alesina et. al (1998)]. 6 Fiscal stance cannot be the only factor for growth enhancement for the states; there are several other factors which could be relevant such as resource endowments, population, level of industrial development, availability of skilled man power, level of education, etc. 7 We use two alternative specifications for episodes of fiscal consolidation defined by reduction in primary deficit or gross fiscal deficit. An episode of consolidation is defined as one in which deficit (PD or GFD) as per cent of GSDP has reduced by atleast 1 per cent over two years and does not increase in either of the two years. 9 A similar exercise done for special category states shows that the only variable to be statistically significant is the dummy variable for revenue-led consolidation. |

Share this page:

Install the RBI mobile application and get quick access to the latest news!

Scan the QR code to install our app

Page Last Updated on: