IST,

IST,

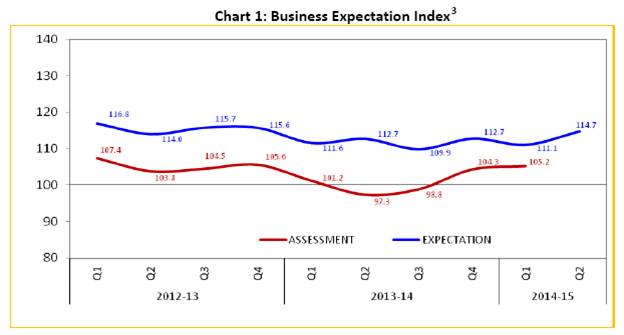

Industrial Outlook Survey- Q1: 2014-15 (Round 66)

The Industrial Outlook Survey conducted during May-June 2014, provides qualitative assessment of business situation of companies in the Indian manufacturing sector for Q1:2014-15 and their expectations for the ensuing quarter Q2:2014-15. The survey elicited response from 1,293 manufacturing companies. Highlights:

Expectation quarter (Q2:2014-15)

Assessment quarter (Q1:2014-15)

1The 65rd round (Q4:2013-14) survey results were released on April 1, 2014 with the publication “Macroeconomic and Monetary Developments 2014-15 (An Update)” on the RBI Website. The survey results are those of the respondents and are not necessarily shared by the Reserve Bank of India. 2Net Response (NR) is the difference of percentage of the respondents reporting optimism and that reporting pessimism. The range is -100 to 100. Any value greater than zero indicates expansion/optimism and any value less than zero indicates contraction/pessimism i.e. NR = (I – D); Where, I is the percentage response of ‘Increase/optimism’, and D is the percentage response of ‘Decrease/pessimism’ and E is the percentage response as ‘no change/Equal’; I+D+E=100. 3The Business Expectation Index (BEI), is a composite indicator calculated as weighted net response of nine business parameters, and gives a single snap shot of business outlook in every quarter. The range of BEI lies between 0 to 200, and 100 is the threshold line separating expansion from contraction. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Share this page:

Install the RBI mobile application and get quick access to the latest news!

Scan the QR code to install our app

Page Last Updated on: