IST,

IST,

Business Continuity Management during Pandemic

Business Continuity Management (BCM) has hitherto meant protecting organisations against events like natural calamities, geo-political disturbances, cyber-attacks and other disruptions that have the potential of interrupting smooth functioning of an organisation. An unknown virus, i.e., coronavirus, of the size of 0.125 microns, unleashed a once in a century pandemic and completely redefined our understanding of BCM. At risk this time were lives, livelihoods, systems and processes and, especially for regulators like the Reserve Bank of India (RBI), potential systemic disruptions in market infrastructure, cyber systems, business processes and operations, communication and availability of skilled personnel. We in RBI mobilised on an unprecedented scale and speed to put in place a cross-functional response that ensured the discharge of all our responsibilities and mandates effectively without compromising on the well-being of our employees and their families. Through these troubled times, RBI had to (a) continually assess and revalidate its readiness for uninterrupted operations; (b) leverage varied data feeds for continuous monitoring; (c) consider consequences and impacts of its measures; and (d) design and implement rapid but co-ordinated responses across verticals. We also proactively communicated through public statements and in other forms of guidance, reassuring the public at large about the stability and resilience of the financial system while supporting banks and financial institutions and the economy as a whole. Our basic message was: RBI is tirelessly at work to shield the Indian economy from the pandemic. From creating a globally acknowledged bio-bubble to keeping payment and settlement and treasury operations running glitch-free, to introducing innovative monetary and liquidity instruments, to taking care of its over 13000 employees and their families by extending adequate support, financial or otherwise, to ensuring adequate availability of currency in the country, RBI was at the frontline, ceaselessly nurturing India’s financial system and ensuring that it successfully sails through uncharted waters. This compendium seeks to put together the various measures taken by RBI during the COVID-19 pandemic times. I congratulate our Corporate Strategy and Budget Department for bringing out this comprehensive compendium in co-operation with other departments. In doing so, I am reminded of the words of Mahatma Gandhi, and I quote: “If patience is worth anything, it must endure to the end of time. And a living faith will last in the midst of the blackest storm”1. Shaktikanta Das February 17, 2023

“Failing to plan is planning to fail” - Benjamin Franklin2 When the COVID-19 pandemic began, there was no standard operating procedure on how to tackle this once-in-a-lifetime cataclysm. The Reserve Bank of India (RBI) mobilised on an unprecedented scale and speed to safeguard lives and livelihood while ensuring the uninterrupted conduct of its crucial functions and unstinted support to employees, service providers and other stakeholders. Central office departments (CODs) and regional offices (ROs) undertook various measures, like work from home (WFH) protocols; quarantines; direct settlement of hospital bills; dedicated COVID-19 care package for employees including vaccination drives; modifications of regulatory prescriptions for regulated entities and financial markets; ensuring availability of adequate currency across the country; and maintaining a hot standby for glitch-free treasury operations, among various other pandemic related business continuity measures and processes. This compendium encapsulates RBI’s fight against the pandemic. It is not just a compilation but also a testimony of courage and dedication in the face of daunting and life-threatening challenges. The compendium is organised into three parts, viz., Introduction, Measures and Epilogue. It covers actions taken across diverse areas such as human resources, information technology, currency management, monetary policy, liquidity management, internal debt management, financial institutions and financial markets and their regulation and supervision, customer grievance redressal, foreign exchange, communication, payment and settlement systems, financial inclusion, banking services for governments and banks, internal accounting and auditing, service provider management, premises and special measures taken by the Regional Offices. This compendium has been prepared in the Business Continuity Management (BCM) Division of Corporate Strategy and Budget Department (CSBD) under the supervision of Shri Jose J Kattoor, Executive Director. Smt Rajani Prasad, Chief General Manager, CSBD provided overall guidance and led the BCM team comprising Shri Sumed Jawade, General Manager, at the helm, Smt Arunothaya M, Assistant General Manager, Shri Akash Choudhary, Manager, Shri Akshay Singh Rathore, Manager and Ms. Mahima Chaudhary, Manager. Dr. Vineet Kumar Srivastava, Director, Department of Economic Policy and Research (DEPR), Shri Suddhasattwa Ghosh, General Manager (retired) and Smt Shailaja Singh, Deputy General Manager, Financial Inclusion and Development Department made editorial contributions. Shri Abhay Mohite, Assistant Manager, DEPR made valuable contributions to designing the cover jacket of the compendium. The compendium is available on the Reserve Bank’s website (www.rbi.org.in). Feedback / comments, if any, may be sent to Chief General Manager, Corporate Strategy and Budget Department, Central Office, 2nd Floor, Main Building, Reserve Bank of India, Shahid Bhagat Singh Marg, Fort, Mumbai – 400 001 or through email (cgmcsbdco@rbi.org.in). Michael Debabrata Patra February 17, 2023 “No pessimist ever discovered the secret of the stars, or sailed to an uncharted land, or opened a new doorway for the human spirit.” - Helen Keller3 I.1 Shocks, whether macro or micro; external or internal, can throw a spanner in the seamless functioning of an organisation. A commitment to organisational resilience in letter and spirit equips and empowers an organisation to tackle the challenges4 posed by the ever-evolving business environment. In keeping with this, business continuity planning helps an entity to build and improve resilience and provides the capability for an effective response to upsetting events. Defined as the capability of an organisation to continue the delivery of products or services at pre-defined acceptable levels following a disruptive incident,5 business continuity planning is the ability to stay in business after a disaster strikes and recover to an operational state within a reasonably short period. I.2 The global financial crisis of 2008-09 and the COVID-19 pandemic have dispelled the notion that tail risks to the financial system will materialise only rarely. Hence, it is imperative that the approach to risk management should be in tune with the realisation of more frequent, varied and bigger risk events than in the past. Institutions must remember the old saying that care and diligence bring luck. To paraphrase Oscar Wilde, being caught unprepared in the face of a shock may be regarded as a misfortune, but to be caught unawares more than once may be a sign of carelessness.6 I.3 The significance of business continuity planning gains even more prominence during the occurrence of black swan events like the COVID-19 pandemic. In the face of this Knightian uncertainty7, RBI stepped forward and proactively dealt with the organisational and management challenges that arose during the pandemic. It also responded swiftly and comprehensively for securing critical business processes and ensured business continuity in the financial system. With the pandemic and geopolitical tensions looming large on the global economy, RBI worked tirelessly to mitigate their adverse impact on the Indian financial system and the economy. In the words of Mahatma Gandhi, “it is when the horizon is the darkest and human reason is beaten down to the ground that faith shines brightest and comes to our rescue.”8 I.4 COVID-19 posed challenges to business continuity not only in terms of safety and health of RBI’s human resources, but also in securing availability of an adequate contingent of healthy and skilled personnel to efficiently perform its operations and functions. In response, all the Business Units (BUs)9 took measures that ensured smooth functioning of RBI’s activities. I.5 This compendium chronicles RBI’s response to the COVID-19 pandemic, rather than providing only a summary description of steps taken by BUs. It also compares the steps taken by other central banks during the period. It is intended that this compendium shall serve as a reference document for future. II.1 The strength of an institution lies significantly in its workforce. It is the harmonious correlation between personal goals and organisational values that enables an institution to attain greater heights. The COVID-19 pandemic posed significant risks affecting human health and endangering lives. Therefore, safeguarding the health and well-being of its employees was of paramount importance to the Reserve Bank of India (RBI) and various measures were taken in this direction.

II.2 To safeguard the health of its employees and also contain the spread of COVID-19, the concept of Work from Home (WFH) was introduced for the first time in RBI. This was done even before a nationwide lockdown was imposed by the Government of India (GoI). All the regional offices of RBI (ROs) were advised to work with bare minimum staff and steps were taken to obtain special permission from various authorities to ensure that persons associated with entities authorised by RBI for operating critical payment systems could access their workplaces (other than the centralised payment systems (CPS), which is dealt with subsequently). II.3 Due to the risk of direct exposure to infection from people and surfaces, protective gears and face shields were provided to security guards and maintenance staff as they were frontline workers. Office premises were sanitised at periodic intervals. An alternate office site was immediately setup at one of the residential colonies in Mumbai to as a safe and secure location for the top management of RBI to work from. II.4 In March 2020, employees were advised to restrict their domestic travel to essential ones and not undertake foreign visits unless specifically approved by the top management. RBI’s training establishments were advised not to conduct any training programmes till further orders and ROs and central office departments (CODs) were instructed not to depute staff for any domestic or foreign training programmes. Employees were also advised to take preventive measures enumerated below, to curb the spread of COVID-19: a) Maintaining social distancing; b) Observing good personal hygiene starting with the practice of washing hands frequently with soap and cleaning hands with alcohol-based hand rub; c) Following basic respiratory etiquette like covering mouth while sneezing and coughing; d) Avoiding touching eyes, nose, and mouth; e) Seeking medical care at the earliest if there was fever, cough or difficulty in breathing; f) Staying informed and following instructions of healthcare provider; g) Infected employees to follow quarantine instructions; and h) Following the advisory on post-travel (air / road / rail) state specific quarantine requirements. II.5 RBI took many proactive steps in respect of the medical requirements of its employees and retirees which were tweaked dynamically in view of the evolving situation over the period. Some of these are enumerated below: a) A Standard Operating Procedure (SOP) for reporting of COVID-19 cases was issued, clarifying on the quarantine requirements and WFH during the quarantine period. The SOP facilitated coordinated reporting of COVID-19 cases across RBI and contained general advisory for nodal officers of CODs and ROs on matters pertaining to COVID-19. b) To effectively follow the policy of test, track and treat, various Rapid Antigen Testing and Reverse Transcription Polymerase Chain Reaction (RTPCR) testing camps were conducted across the offices of RBI. c) RBI introduced dedicated isolation arrangements for employees and dependent family members with hospitals in various centres for quarantine requirements. This was later extended to staff of service providers working on critical operations. d) A dedicated ‘Home Care Package’ was introduced for COVID-19 infected employees and family members. e) In case of mild symptoms which did not require hospitalisation, home quarantine was advised as per government guidelines. f) With the possibility of children being infected in the third wave of COVID-19, specialised children’s hospitals were empanelled for direct settlement. g) Wherever necessary, powers were delegated to ensure frictionless admission to hospitals. h) ROs having arrangement with local empanelled service providers, were advised to provide medicines to retirees at their doorstep. i) Medical facilities were extended to part-time / contractual doctors (BMO / BMC) and pharmacists of RBI as a welfare measure in view of their role as frontline workers during the pandemic. j) Settlement of bills for COVID-19 related medical charges were permitted beyond the rates prescribed under the medical schedule in view of the increased rates due to demand-supply mismatches. k) In view of COVID-19 cases being reported regularly, quarantine facilities were arranged in the residential colonies for staff and their family members. l) During the 2nd wave of the COVID-19 pandemic, ROs were advised to purchase oxygen concentrators for dispensaries, to counter the shortage in hospitals. m) ROs were advised to provide immunity boosting medicines to employees and their family members through dispensaries to ensure better immunity. n) Vaccines were provided centrally from pharmaceutical companies for Mumbai and a few other centres. o) RBI also tied-up with various hospitals for vaccination of its staff and their dependent family members. Several COVID-19 vaccination camps were conducted at various RBI premises and colonies. The staff and their family members were sensitised to get vaccinated at the earliest. II.6 Instructions for granting leave were liberalised to minimise hardship to employees: a) On account of the sudden nation-wide lockdown announced by GoI, those employees who were on pre-sanctioned leave with permission to leave headquarters were allowed to work remotely as they were unable to report back for duty. b) Employees who contracted COVID-19 were permitted to avail special casual leave (SCL) for quarantine. This leave was available for fifteen days in a calendar year, excluding Saturdays, Sundays and holidays. c) Admissible leave availed for self-quarantine purpose was not counted as an additional leave spell for the purpose of bad leave record. II.7 Prior to COVID-19, senior officers were provided with laptop / Tablet PC / i-Pad while junior officers were provided laptops on a need-basis. To enable work from home during pandemic, Class III employees were also reckoned as eligible employees for allotment of laptops on a need-basis. Wherever considered necessary, laptops were temporarily allotted to contract employees / service providers providing critical support to RBI. II.8 RBI adopted the approach of BEAT-UP-COVID, viz., Benchmarking, Administration, Tweaking, Up-gradation, Paediatric care, Calibrating, Organisation, Vaccinating, Involving and De-stressing, by setting up a COVID-19 Response Group (CRG) to provide help on a real time basis to tackle the third wave of COVID-19 pandemic. The CRG was constituted to harmonise, synchronise, and oversee the diverse and disparate steps being taken at various levels. II.9 RBI obtained membership of the GoI’s Aadhaar based Jeevan Pramaan Portal and Samadhan (RBI’s Human Resources Management Portal) was integrated with it to facilitate acceptance of life certificates in digital format. Pensioners could visit any Aadhaar Centre and generate Digital Life Certificate which could be updated in Samadhan automatically. II.10 To avoid crowding at the entry / exit points, RBI introduced staggered office timings. II.11 When the world experienced an unprecedented macroeconomic shock in the face of COVID-19, resulting in lockdowns, lack of accessibility, threat to life and an uncertain future, central banks across the world faced enormous challenges on multi-dimensional fronts. For RBI, this challenge included keeping its payments and market infrastructure11 and internal functioning up and running efficiently. While observing adherence to COVID-19 protocols, RBI undertook innovative measures in discharge of its functions. II.12 To perform the critical functions of RBI with zero downtime and with full efficacy, a secured, quarantine environment, viz., a “Bio-Bubble” arrangement was put in place for all the Data Centres.

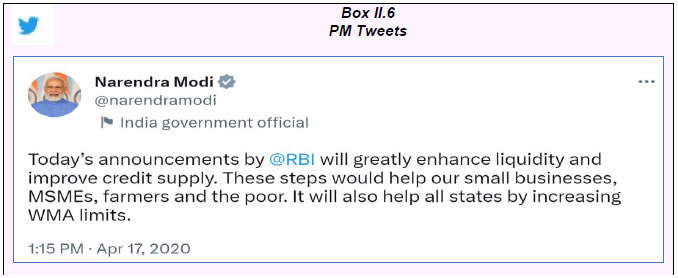

II.13 After the concept of WFH was introduced, as stated earlier, laptops and access for work from home was provided. Access was also provided to Samadhan, from home. Anticipating the requirement of Video Conferencing (VC) facility over the internet, a collaborative platform for audio / video based interactions, viz., Sampark (a Video Conference Platform) was introduced. Virtual meetings were conducted through Sampark. Sarthi (RBI’s Electronic Document Management Application) was also introduced to further facilitate WFH. CODs and ROs were advised to invariably keep a backup of all important data / files and update them frequently, while ensuring the safety and confidentiality of data. II.14 For the staff required to attend offices at various locations, arrangements were made to ensure uninterrupted supply of drinking water / tea and food in the premises. Regular announcements were made on public address system to ensure that staff / visitors attending office followed COVID-19 appropriate behaviour. Service providers / Data Entry Operators (DEOs) were asked to join the office on rotation basis during the pandemic period. Wash rooms and premises were sanitised regularly. II.15 The Reserve Bank Staff College (RBSC) and the Zonal Training Centres (ZTCs) shifted to online training sessions. II.16 To ensure business continuity, important applications like Bloomberg terminal, Refinitiv Eikon, Cogencis and Negotiated Dealing System - Order Matching (NDS-OM) were made available over internet by the respective service providers. In order to enable Secured Remote Access to RBI’s IT applications, two factor authentication (2FA) was configured on official Laptops. II.17 Internal meetings of the Inter-Departmental Group (IDG) on growth and inflation and the Commodity Price Monitoring Group (CPMG) transited from physical presentations to online interactions and information flow in the run up to policies was uninterrupted. II.18 The landline contact numbers at CoDs were diverted to the respective official’s mobile handset to ensure continuity with no disruptions. II.19 COVID-19 pandemic and the lockdown restrictions imposed thereafter, posed challenges for ensuring (a) undisrupted functioning of currency related activities through the currency management network comprising the printing presses, ROs and currency chests (CCs), branches of banks and the automated teller machines (ATMs); and (b) availability of adequate currency in every part of the country. II.20 The major challenges faced included, ensuring sufficient printing of currency, timely supply of currency and ensuring availability of currency at the last point while bearing in mind the safety of treasure and human resources involved. Execution of the above activities involved considerable coordination with the multiple stakeholders in the network. Some of the measures taken are as under: a) Paper mills and printing presses were advised to monitor inventory of raw materials and to activate a Business Continuity Plan (BCP); b) The overall stock and withdrawal pattern of notes was closely monitored to ensure adequate availability of notes and coins in the ROs and the CCs; c) Adequate supply of banknotes and coins in various denominations to the public was ensured by arranging dedicated trains and airlifting of currency; d) To ensure speedier and timely supply of banknotes, increased emphasis was accorded towards direct remittances from printing presses to CCs. e) Availability of cash in ATMs across the country was monitored by RBI on a daily basis to ensure timely replenishment, which involved close coordination between RBI, cash-in-transit companies and the government. f) To tackle the accumulation of soiled notes and freeing up space in CCs, the ROs operated CVPS and the shredding and briquetting system (SBS) machines in extended hours and night shifts, wherever required. II.21 With a view to enhance efficiency and productivity in currency management operations, the process pertaining to remittances of fresh notes (from presses to ROs of RBI, from ROs to currency chests and direct remittances to currency chests) was rationalised which reduced both the time involved in the remittance of currency and human intervention while handling currency. II.22 In March 2020, the policy repo rate was reduced by 75 basis points to 4.40 per cent. It was decided to maintain the accommodative stance of monetary policy as long as considered necessary to revive growth, mitigate the impact of COVID-19, while ensuring that inflation remained within the target. The fixed rate reverse repo rate, which sets the floor of the Liquidity Adjustment Facility (LAF) corridor, was reduced by 90 basis points to 4.00 per cent, thus creating an asymmetric corridor.  II.23 In April 2020, the fixed rate reverse repo rate was reduced by 25 basis points to 3.75 per cent. In May 2020, the repo rate was cut by another 40 basis points to 4.00 per cent and the fixed rate reverse repo rate by a similar magnitude to 3.35 per cent. Fine-tuning variable rate repo auctions were conducted during March 2020 to provide flexibility to the banking system in its liquidity management towards the year end. As a special case, standalone primary dealers (SPDs) were allowed to participate in these auctions along with other eligible participants.  II.24 On September 11 and September 14, 2020, RBI conducted two 56-day term repo auctions for amount totalling to ₹1.0 lakh crore to foster orderly market conditions. II.25 As per Section 45ZI (1) and (2) of the Reserve Bank of India Act, 1934, RBI is required to convene at least four meetings of the Monetary Policy Committee (MPC) in a year and the schedule of the meetings of the MPC for the year has to be published at least one week before the first meeting in that year. However, due to the evolving macroeconomic situation arising out of the COVID-19 pandemic, off-cycle meetings of MPC were convened in March and May 2020. II.26 The Governor, RBI held periodic press conferences, issued statements in the press where the rationale of RBI’s actions were explained in the best traditions of accountability and transparency, the hallmark of a modern market-based approach to monetary policy making.13 This acted as a major confidence boosting measure during the uncertain times. II.27 To optimise human resource deployment in the context of disruptions caused by COVID-19 and to provide eligible participants of LAF / Marginal Standing Facility (MSF) greater flexibility in managing their end of the day cash reserve ratio (CRR) balances, RBI decided to provide an optional automated sweep-in and sweep-out (ASISO) facility in its eKuber (RBI’s Core Banking Solution). II.28 The following schemes / operations were announced since the onset of COVID-19, to mitigate liquidity stress in regulated entities and markets. a) Long Term Repo Operations (LTROs) were announced for a cumulative amount of ₹2.00 lakh crore, of which ₹1.25 lakh crore was availed. These were for tenors of one year and three years, respectively. b) In view of the tightening of financial conditions as reflected in the hardening of yields and widening of spreads, RBI conducted regular Open Market Operations (OMO) to ensure that the yield curve evolved in an orderly manner. c) Secondary market G-sec acquisition programme (G-SAP) was announced, under which RBI committed upfront to a specific amount of open market purchases of government securities. Overall, net liquidity injected through OMO purchases, including G-SAP, amounted to ₹3.13 lakh crore during 2020–21 and ₹2.10 lakh crore during 2021-22. d) In order to distribute liquidity more evenly across the yield curve and improve transmission, 22 auctions of operation twists (OTs) were conducted during 2020-21 and 2021-22. e) To facilitate year-end liquidity management of SPDs, the limit of liquidity available to them under the Standing Liquidity Facility (SLF) was enhanced from ₹2,800 crore to ₹10,000 crore till April 17, 2020. f) As a one-time measure to help banks tide over the disruption caused by COVID-19, it was decided to reduce the cash reserve ratio (CRR) by 100 basis points to 3.0 per cent of net demand and time liabilities (NDTL) with effect from the reporting fortnight beginning March 28, 2020. This reduction in CRR released primary liquidity of about ₹1,37,000 crore uniformly across the banking system. Furthermore, the requirement of minimum daily CRR balance maintenance was reduced from 90 per cent to 80 per cent, which was in effect till September 25, 2020. SCBs were also allowed exemption from maintenance of cash reserve ratio (CRR) on incremental credit disbursed by them between January 31 and July 31, 2020 on retail loans for automobiles, residential housing and loans to MSMEs. g) Under the MSF, banks could, prior to the COVID-19 pandemic, borrow overnight at their discretion by dipping up to 2 per cent into the Statutory Liquidity Ratio (SLR). To provide comfort to the banking system, the limit was increased from 2 per cent to 3 per cent of their NDTL effective March 27, 2020. This measure was available up to December 31, 2021. This provided comfort to the banking system by allowing it to avail an additional ₹1,37,000 crore of liquidity under LAF window in times of stress. h) Targeted Long-Term Repo Operations (TLTROs)14 were announced on March 27, 2020 for a cumulative amount of ₹1 lakh crore. Liquidity availed by banks under the scheme was required to be deployed in investment grade corporate bonds, commercial paper, and non-convertible debentures {including Mutual Funds and Non-Banking Financial Company (NBFC)} over and above the outstanding level of their investments in these bonds as on March 27, 2020. TLTRO 2.0 was announced on April 17, 2020 for tenors up to three years for ₹50,000 crore, to further augment the scheme (providing adequate system level liquidity as well as targeted liquidity provision to sectors and entities experiencing liquidity constraints). i) Considering the impact of disruptions due to the lockdown and social distancing, it was decided to temporarily suspend the revised liquidity management framework and the window for Fixed Rate Reverse Repo (FRRR) and MSF operations were made available throughout the day with effect from March 31, 2020. This was intended to provide eligible market participants with greater flexibility in their liquidity management. The window timings of FRRR and MSF were brought back to normal with effect from March 1, 2022. j) To minimise the risks arising due to COVID-19, the trading hours for various RBI regulated markets were revised to begin at 10.00 am and close at 2.00 pm effective from April 7, 2020. Subsequently, with the phased removal of lockdown and easing of restrictions on movement of people and resumption of normal functioning of offices, the trading hours were restored in a phased manner, beginning November 9, 2020. k) Special refinance facilities (including additional standing liquidity facility) cumulatively amounting to ₹1,41,000 crore were provided to all India financial institutions (AIFIs) viz., National Bank for Agriculture and Rural Development (NABARD), Small Industries Development Bank of India (SIDBI), National Housing Bank (NHB) and Export-Import Bank of India (EXIM Bank), to support their role in meeting funding requirements of various sectors. l) With a view to ease liquidity pressures on Mutual Funds (MF), a special liquidity facility (SLF-MF) of ₹50,000 crore for banks was opened to meet the liquidity requirements of mutual funds. Under the SLF-MF, RBI conducted repo operations of 90 days tenor at the fixed repo rate. The SLF-MF was on-tap and open-ended. The scheme was available from April 27, 2020 till May 11, 2020. Later, the regulatory benefits announced under the SLF-MF scheme were extended to all banks, irrespective of whether they availed funding from RBI or deployed their own resources under the scheme. m) In July 2020, RBI injected liquidity through back-to-back funding by subscribing to government guaranteed special securities issued by a special purpose vehicle (SPV) to improve liquidity position of NBFCs (including Micro-Finance Institutions - MFIs) / Housing Finance Companies (GoI notified scheme of ₹30,000 crore) to avoid any potential systemic risks to the financial sector. n) To increase the focus of liquidity measures on revival of activity in specific sectors, on October 9, 2020, on tap TLTRO scheme was announced up to three-year tenor for a total amount of up to ₹1,00,000 crore at a floating rate (repo rate) with end-use guidance. The scheme was extended till December 31, 2021. o) To provide an additional avenue for liquidity management, LAF and MSF were extended to Regional Rural Banks (RRBs), subject to meeting certain conditions, on December 4, 2020. p) An on-tap term liquidity window of ₹50,000 crore was announced to ease access to emergency health services, with tenors of up to three years at the repo rate till June 30, 2022. q) To provide further support to small business units, micro and small industries, and other unorganised sector entities adversely affected during the pandemic, special three-year long-term repo operations (SLTROs) of ₹10,000 crore at repo rate were conducted for the Small Finance Banks. The funds so raised were required to be deployed for fresh lending of up to ₹10 lakh per borrower. This facility was initially made available till October 31, 2021 and later extended to December 31, 2021. r) A separate liquidity window for contact intensive sectors for an amount of ₹15,000 crore was announced with tenors of up to three years at the repo rate till June 30, 2022.

II.29 A hot-standby dealing room and back office (HSDRBO) site was made operational as an alternative site at another location of RBI where a few dealers were stationed permanently. During normal times, the dealing rooms carry out Markets Intervention Operations, LAF Operations, OMOs and other tasks as assigned internally. However, commencing March 18, 2020, critical activities were carried out from BCP site. From May 11, 2020 onwards, the staff at HSDRBO, resumed normal working from office and critical operations were carried out jointly in co-ordination with the minimal staff working at the BCP site. As the staff started attending office in a staggered manner, operations at the BCP’s were closed with effect from August 21, 2020 and all activities were resumed fully from the dealing room jointly with HSDRBO. II.30 In the second wave of the pandemic that spanned from April 2021 onwards, the TSCAs pertaining to the dealing room were efficiently conducted by officers working from home. II.31 On a review of financial market conditions affected by the spread of COVID-19 and taking into consideration the requirement of US Dollars in the market, it was decided to undertake two 6-month US Dollar sell / buy swaps in March 2020 to provide liquidity to the foreign exchange market, which cumulatively provided US Dollar liquidity amounting to USD 2.7 billion. II.32 The Ways and Means Advances (WMA) limit of states / union territories (UTs) was enhanced first by 30 per cent and then by 60 per cent over and above the level as on March 31, 2020. The increased limit was made available till September 30, 2020. II.33 As financial conditions eased, a calibrated restoration of the revised liquidity management framework instituted in February 2020 was set in motion through rebalancing liquidity in a non-disruptive manner away from the fixed rate reverse repo operations to market based auctions of variable rate reverse repos (VRRRs). II.34 RBI successfully completed the government borrowing programme despite the multiple challenges and uncertainties posed. There was a record market borrowing by the central and the state governments due to COVID-19 and the borrowing calendar was periodically revised during the financial years 2020-21 and 2021-22. RBI adapted to the emerging circumstances by constantly reviewing the preparedness, collaborated with all stakeholders and ensured that the market borrowing programme was done seamlessly. Some of the measures taken by RBI are detailed hereunder: a) To strengthen the business continuity planning arrangements and to remain in operational readiness, alternative emergency back-up sites were identified at various RBI office locations in Mumbai and elsewhere. Further, back-up resources having prior experience of conducting auctions and related activities were identified from alternate offices. b) To provide greater comfort to the central and state governments in undertaking COVID-19 containment and mitigation measures, and to enable them to plan their market borrowings, the WMA limit was enhanced. The limit for WMA of the GoI for the remaining part of first half of the financial year 2020-21 (April 2020 to September 2020) was revised from ₹1,20,000 crore to ₹2,00,000 crore. The WMA limit for GoI for the second half of 2020-21 was fixed at ₹1,25,000 crore, an increase of 257 per cent over the previous half year (second half of 2019-20). c) Several state governments created and maintained a Consolidated Sinking Fund (CSF) to facilitate redemption of state’s market loans in an orderly manner and to increase their credibility in raising loans at lower rates in future through auctions. The scheme for constitution and administration of CSF for state government was reviewed and the rules governing withdrawal from CSF were relaxed, while ensuring that a sizeable corpus is retained in the Fund. II.35 Based on a review of the rapidly evolving situation, and consistent with the globally coordinated action committed to by the Basel Committee on Banking Supervision (BCBS), regulatory measures were announced15 to alleviate the impact of COVID-19 on the global banking system. Governor, Shri Shaktikanta Das summed up RBI’s actions stating, “The Reserve Bank is not hostage to any rule book and no action is off the table when the need of the hour is to safeguard the economy.”16 In view of this, while regulatory prescriptions were eased during COVID-19, the dispensations were not unbridled and sunset clauses were inbuilt in most cases. II.36 Measures were initiated to mitigate the burden of debt servicing and to ensure the continuity of viable businesses. The salient features of these measures included rescheduling of payments for term loans and working capital facilities, easing of working capital financing and exemption from classification of special mention account (SMA) and Non-Performing Assets (NPA) on account of implementation of the above measures. II.37 Based on the review and empirical analysis of counter cyclical capital buffer (CCyB) indicators, it was decided not to activate CCyB for a period of one year, i.e., till April 2021 and subsequently it was decided that it was not necessary to activate CCyB at that point in time. II.38 It was decided that in respect of all accounts for which lending institutions decide to grant moratorium or deferment, and which were ‘standard’ as on March 1, 2020, the 90-days NPA norm shall exclude the moratorium period, i.e., there would be an asset classification standstill for all such accounts from March 1, 2020 to May 31, 2020. At the same time, with the objective of ensuring that banks maintain sufficient buffers and remain adequately provisioned to meet future challenges, they will have to maintain higher provision of 10 per cent on all such accounts under the standstill, spread over two quarters, i.e., March 2020 and June 2020. These provisions were allowed to be adjusted later against the provisioning requirements for actual slippages in such accounts. II.39 Under RBI’s prudential framework for resolution of stressed assets dated June 7, 2019, in case of large accounts under default, scheduled commercial banks (SCBs) were required to hold an additional provision of 20 per cent if a resolution plan was not implemented within 210 days from the date of such default. Recognising the challenges to resolution of stressed assets in the then volatile environment, it was decided to extend the period for implementation of resolution plan by 90 days. Further extension of the resolution timelines was provided after a review on account of continued challenges to resolution of stressed assets in a volatile environment. II.40 A window for resolution of COVID-19 related stress {applicable to all commercial banks (including small finance banks, local area banks and regional rural banks), all primary (Urban) co-operative banks / state co-operative banks / district central co-operative banks, NBFCs (including housing finance companies) and all India financial institutions – AIFIs} was provided to facilitate revival of real sector activities which were under financial stress due to economic fallout on account of the COVID-19 pandemic, subject to certain conditions. II.41 The resolution framework was to be invoked not later than December 31, 2020 and had to be implemented within 90 days of invocation in respect of personal loans and 180 days of invocation for other eligible loan exposures.

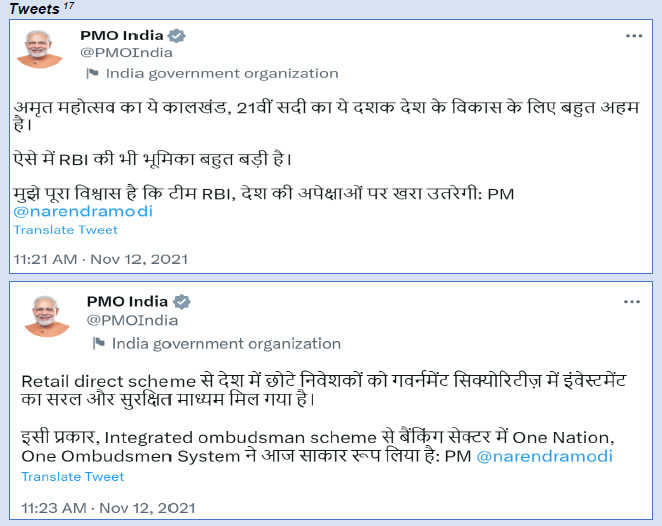

II.42 With a view to conserve capital of banks to retain their capacity to support the economy and absorb losses in an environment of heightened uncertainty, SCBs were directed not to make any further dividend pay-outs from profits pertaining to the financial year ended March 31, 2020 until further instructions. This restriction was to be reviewed based on the financial position of banks for the quarter ended September 30, 2020. In April 2021, SCBs were allowed to declare dividend on equity shares from the profits for the financial year ended March 31, 2021, subject to certain conditions. II.43 The Net Stable Funding Ratio (NSFR), which reduces funding risk by requiring banks to fund their activities with sufficiently stable sources of funding over a time horizon of a year to mitigate the risk of future funding stress, was required to be introduced by banks in India from April 1, 2020. It was decided to defer the implementation of NSFR initially by six months till October 1, 2020 and later to October 1, 2021. Accordingly, the guidelines on NSFR have come into effect from October 1, 2021. II.44 To ease the liquidity position at the level of individual institutions, the Liquidity Coverage Ratio (LCR) requirement for SCBs was brought down from 100 per cent to 80 per cent with effect from April 17, 2020. The requirement was gradually restored back in two phases, viz., 90 per cent by October 1, 2020 and 100 per cent by April 1, 2021. II.45 The capital conservation buffer (CCB) is designed to ensure that banks build up capital buffers during normal times (i.e., outside periods of stress), which can be drawn down if losses are incurred during a stressed period. Considering the potential stress on account of COVID-19, the implementation of the last tranche of 0.625 per cent of the CCB was deferred from March 31, 2020 to September 30, 2020 and then till October 1, 2021. The last tranche was implemented with effect from October 1, 2021. II.46 Interest equalisation scheme on pre and post shipment rupee export credit was extended by the government of India for one year, i.e., up to March 31, 2021, with same scope and coverage and all extant operational instructions issued by RBI under the said captioned scheme continued to remain in force up to March 31, 2021. II.47 With a view to facilitate greater flow of resources to corporates that faced difficulties in raising funds from the capital market and predominantly depended on bank funding, a bank’s exposure under the Large Exposure Framework to a group of connected counterparties was increased from 25 per cent to 30 per cent of the eligible capital base of the bank. II.48 Banks were permitted to reckon the funds infused by promoters in their Micro, Small and Medium Enterprises (MSMEs) units through loans availed under the government’s credit guarantee scheme for subordinate debt for stressed MSMEs as equity / quasi equity from the promoters for purpose of debt-equity computation. Existing loans to MSMEs where the banks, AIFIs and NBFCs having aggregate exposure of not more than ₹25 crore and are classified as 'standard' as on March 1, 2020, were permitted to be restructured without a downgrade in the asset classification. The restructuring had to be implemented by March 31, 2021. II.49 To mitigate the economic impact of the COVID-19 pandemic on households, entrepreneurs and small businesses, loan-to-value ratio (LTV) for loans against pledge of gold ornaments and jewellery for non-agricultural purposes was increased from 75 per cent to 90 per cent. This enhanced LTV was applicable up to March 31, 2021. II.50 As per earlier regulations, claims secured by residential property falling under the category of individual housing loans were assigned differential risk weights based on the size of the loan as well as the LTV. Recognising the criticality of real estate sector in the economic recovery, it was decided as a countercyclical measure to rationalise the risk weights irrespective of the size of the loan amount. II.51 In respect of working capital facilities sanctioned in the form of cash credit / overdraft, lending institutions could recalculate drawing power by reducing margins and / or by reassessing the working capital cycle for the borrowers. Such changes were not to result in asset classification downgrade. II.52 The moratorium on term loans, the deferring of interest payments on working capital and the easing of working capital financing did not qualify as a default for the purposes of supervisory reporting and reporting to credit information companies (CICs) by the lending institutions. Hence, there was no adverse impact on the credit history of the beneficiaries. II.53 The RBI Integrated Ombudsman Scheme (RBI IOS) was launched by Hon’ble Prime Minister, Shri Narendra Modi on November 12, 2021. The scheme leveraged technology and innovation for enhancing the efficiency of RBI’s services and provided a customer friendly manner of lodging grievances at customer’s convenience and comfort. The Scheme adopted ‘One Nation One Ombudsman’ approach by making the RBI Ombudsman mechanism jurisdiction neutral with one portal, one email, and one address for the customers to lodge their complaints. The scheme provided a multi-lingual toll-free number which would give relevant information on grievance redress and assistance for filing complaints. As was the case with the earlier ombudsman schemes, the redressal continued to be cost-free for customers of banks and members of the public.

II.54 In view of the difficulties arising out of reduced mobility and access on account of the lockdown, RBI curtailed the market trading hours for RBI-regulated financial markets. When the pandemic-related constraints eased, the trading hours were restored in a phased manner. II.55 The following measures were taken by RBI to provide greater flexibility in complying with regulatory requirements during the pandemic: (a) Foreign portfolio investors that were allotted investment limits under the voluntary retention route (VRR) for investment in debt securities between January 24, 2020 and April 30, 2020 were allowed an additional time of three months to meet their investment commitments. (b) The timeline for implementation of legal entity identifier (LEI) in non-derivative financial markets was extended from March 31, 2020 to September 30, 2020. (c) The implementation date for the directions on hedging of foreign exchange risk (dated April 7, 2020) was deferred from June 1, 2020 to September 1, 2020. II.56 The submission of Form A and VII returns to RBI using digital signature was introduced. This ensured timely publication of press communique statements. II.57 As many primary (urban) co-operative banks (UCBs), state co-operative banks and central co-operative banks were facing difficulties in finalising their Annual Accounts, they were given time up to September 30, 2021, (from June 30, 2021) to submit the returns to RBI. II.58 RBI increased the period for realisation and repatriation of export proceeds to India from nine months to fifteen months from the date of export, in respect of exports made up to or on July 31, 2020. II.59 The timeline for completion of remittances against normal imports, i.e., excluding import of gold / diamonds and precious stones / jewellery (except in cases where amounts were withheld towards guarantee of performance) was increased from six to twelve months from the date of shipment for such imports made on or before July 31, 2020. II.60 ROs were advised to consider, with the approval of their Empowered Committee, requests received from Full Fledged Money Changers (FFMCs) for extension of time for submitting renewal application if the requirement was on account of reasons relating to the COVID-19 situation. II.61 Based on a letter from Department of Financial Services (DFS), Ministry of Finance to allow remittance service providers {under Money Transfer Service Scheme (MTSS)} to function normally and allowing the intended recipients to withdraw their money remitted from abroad, ROs were advised to direct all MTSS agents under their respective jurisdictions to ensure that (a) beneficiaries in India do not face problems in accessing the funds remitted to them under the MTSS; and (b) the payment services provided to beneficiaries by MTSS agents remained operational during the period of lockdown. II.62 With a view to providing relief to borrowers facing difficulty in utilising already drawn down External Commercial Borrowings (ECBs) due to the COVID-19 pandemic induced restrictions, a one-time relaxation was provided, whereby unutilised ECB proceeds drawn down on or before March 01, 2020 could be parked in term deposits with authorised dealer category-I banks18 in India, prospectively for an additional period up to March 01, 2022. II.63 Due to the COVID-19 pandemic and considering the difficulties being faced in submitting returns, ECB returns were allowed to be submitted by borrowers through email. Similarly, considering the difficulties expressed by applicants in submitting payment instruments for paying compounding amount within 15 days of compounding order during the lockdown, payment of compounding amount beyond time limit was permitted. Further, personal hearings with the applicants were held in virtual mode, instead of in-person meetings. II.64 In consultation with the GoI, receipt of foreign inward remittances from non-residents through non-resident exchange houses in favour of the ‘Prime Minister’s Citizen Assistance and Relief in Emergency Situations (PM-CARES) Fund’ was permitted subject to the condition that authorised dealer category-I banks shall directly credit the remittances to the Fund and maintain full details of the remitters. II.65 Communication has gained importance although it works both ways – while too much of communication can confuse the market, too little may keep it guessing about the central bank’s policy intent. Therefore, central banks have to tread a very fine line.19 RBI has been mindful of the importance of communication during this period given its multifarious responsibilities and wider ramifications of its actions. II.66 Governor and Deputy Governors held regular meetings with the managing directors (MDs) and chief executive officers (CEOs) of major regulated entities. RBI ensured all channels of communication were kept open with major players in the financial system. II.67 As two-way communication is important for making informed policy decisions. Therefore, RBI held detailed interactions with analysts, economists, researchers, banks, academic bodies and research institutions, trade and industry associations, and several others for monetary policy and other policy actions. This enabled building a confidence channel through communication and instilled wider confidence in RBI’s policies. II.68 Beginning March 2020, several BCP resilience measures were taken, which inter alia, included: a) Critical website operations relating to timely updation of content on RBI’s website were shifted to PDC and the staff deputed there were assigned the following responsibilities: i) Co-ordination with IRIS Business Services Limited staff for timely updation and uploading of various documents on RBI’s website. ii) Technical issues were handled in co-ordination with Reserve Bank Information Technology Private Limited (ReBIT), IRIS and the Department of Information Technology. iii) Virtual Private Network (VPN) access was configured to put in place a BCP in case of non-availability of data centre.

Payment and Settlement Systems II.69 With monthly transactions of around 124.68 crore in volume and ₹2.06 lakh crore in value, as on March 31, 2020, Unified Payments Interface (UPI) well served the payment needs of the public. To keep the vast system of electronic and paper-based payment systems (processing around 299.77 crore monthly transactions amounting to ₹155.90 lakh crore, as on March 31, 2020) running glitch-free, RBI acted immediately and earnestly. II.70 For ensuring continuity in critical interfaces and preventing any disruption of services, authorised Payment System Operators (PSOs) were advised to ensure adequate Operational and Business Continuity Plans and take contingency measures to manage the risks. RBI closely co-ordinated with the National Payments Corporation of India (NPCI) and other authorised PSOs to ensure uninterrupted operations of all the payment systems. II.71 The pandemic situation necessitated the use of digital payment options to ensure social distancing. The constituents of the payment systems were allowed to operate throughout the lockdown, which facilitated unhindered movement of people and other resources across the country and took care of smooth operations of the payments systems. Measures were taken to enhance public awareness on the availability of various digital payments that could be used from home. Authorised PSOs and participants were advised to undertake targeted multi-lingual campaigns to educate their users on the safe and secure use of digital payments. II.72 Comprehensive business continuity arrangements and resilience measures were deployed by RBI during the COVID-19 pandemic. The operations of Clearing Corporation of India (CCIL), a systemically important Financial Market Infrastructure, are critical to the smooth functioning of banking services. RBI designated CCIL and its two subsidiaries, viz. Clearcorp Dealing Systems (India) Limited (Clearcorp) and Legal Entity Identifier India Limited (LEIL) as ‘Essential Service’ during the lockdown and ensured that CCIL adopted a comprehensive BCP. The operations of CCIL were closely monitored during the pandemic. II.73 Overseas Principals which facilitated small-value cross-border remittances under MTSS were encouraged to use digital payments and afford direct credit to beneficiaries’ bank accounts wherever possible, to overcome difficulties faced by beneficiaries in collecting cash pay-outs from agent locations, due to COVID-19 protocols. II.74 Direct Benefit Transfer (DBT) to the bank accounts of the beneficiaries for schemes of central and state governments was facilitated during the COVID-19 pandemic through Aadhaar Payments Bridge System (APBS) and National Automated Clearing House (NACH) platforms. More than ₹36,659 crore {₹27,442 crore [centrally sponsored scheme (CSS) and central sector schemes (CS)] and ₹9,717 crore [state government schemes (SGS)]} was transferred to the bank accounts of 16.01 crore beneficiaries {11.42 crore [CSS / CS] and 4.59 crore [State]} between March 24, 2020 and April 17, 2020. Till July 2021 (taking into account the first and second phases of COVID-19), an amount of ₹5.41 lakh crore was transferred to beneficiaries under DBT. II.75 All the Central Counter Parties (CCPs), including CCIL, mark to market positions (MTM) and call MTM margin on a daily basis (and sometimes intraday) to avoid building up of risk and limit their current exposure. During peak COVID-19 triggered volatility, Initial Margin (IM) and MTM Margin increased and the increase in MTM margin was much higher than the increase in IM. In Securities segment, Volatility Margin was imposed on seven days between March and December 2020. There were some instances of Intraday MTM margin calls. II.76 Criteria for counting of days while calculating the time available for resolving a failed transaction was modified. II.77 RTGS was made available round the clock on all days of the year with effect from December 14, 2020. With this enablement, the settlement and default risks were reduced in the system and made the payments ecosystem more efficient. The system also facilitated settlement of Aadhaar Enabled Payment System (AePS), Immediate Payment Service (IMPS), National Electronic Toll Collection (NETC), National Financial Switch (NFS), RuPay and UPI transactions on all days of the week. II.78 A standard operating procedure (SOP) was prepared to ensure availability of payment and settlement systems operated by RBI and minimise disruptions. The SOP clearly delineated roles and responsibilities of stakeholder departments, offices and agencies. Despite lockdown curbs being in effect during the pandemic, the SOP ensured timely and effective response in emergencies. II.79 Timelines for compliance with various payment system requirements were extended. II.80 In the words of Governor, Shri Shaktikanta Das, “We must continue our efforts for greater financial inclusion in pursuance of the goal of sustainable future for all.”20 During the pandemic, with a view to assess the ground level situation and understanding the challenges being faced by Business Correspondent (BC) agents in rendering services during the lockdown, comments / inputs were sought from banks, through Indian Banks’ Association (IBA) on the broad topics of impact on BC transactions, cash management, customer grievance redressal, technical issues, and inactive BCs. Further, good practices adopted by select banks, during the pandemic, to support and strengthen the BC model were shared with all the banks through IBA. II.81 Meetings were held with banks and NABARD to deliberate, inter-alia, on issues related to BC Model, data submissions and so on. Most of these meetings, held through virtual mode in the WFH environment, helped in understanding different BC models being used by banks and their unique challenges. Inputs from these meetings also helped in identifying areas for improvement in the BC Model and resulted in timely submission of error-free data by banks. II.82 To ensure that farmers did not have to pay penal interest and continued to derive benefits of the interest subvention scheme, 2% interest subvention (IS) and 3% prompt repayment incentive (PRI) to farmers was continued for the extended period of repayment up to August 31, 2020 or the date of repayment, whichever was earlier. Further, on account of movement restrictions imposed by state governments during the lockdown imposed in the second wave of COVID-19, the benefit was extended to the farmers whose accounts had become or would have become due between March 1, 2021 to June 30, 2021, for the extended period of repayment of loans up to June 30, 2021 or date of actual repayment whichever was earlier. II.83 References received from the central government, state governments, NABARD and banks for declaring COVID-19 as a natural calamity were analysed in the context of the larger relief package announced by RBI, granting moratorium and restructuring to all borrowers. II.84 The Lead Bank Scheme (LBS) which coordinates the activities of banks and other developmental agencies through various fora {State / Union Territory Level Bankers’ Committee (SLBC / UTLBC), District Consultative Committee (DCC), District Level Review Committee (DLRC) and Block Level Bankers’ Committee (BLBC)} to achieve the objective of enhancing the flow of bank finance to the priority sector and other sectors and to promote banks' role in the overall development of the rural sector. To achieve this, meetings of all the LBS fora are required to be convened at quarterly intervals. Despite lockdown, the meetings of LBS fora were conducted through virtual mode by convener banks and lead banks which were attended by ROs. The COD attended some of the SLBC meetings through VC. II.85 Automation in uploading of Data in the Automated Data Extraction Project (ADEPT) portal was carried out and the production support and maintenance of ADEPT was done via roster to ensure social distancing. II.86 Since conducting of awareness camps under the challenging circumstances would have been difficult, ROs were instructed to explore innovative approaches to promote financial literacy amongst the masses. Initiatives introduced included campaigns through various digital channels, such as, VC and social media. ROs also leveraged media channels such as community radio channels, local TV channels and local frequency modulation (FM) radio stations to impart financial education. II.87 Financial Literacy Centres (FLCs) of SCBs (including RRBs) and rural branches of banks were instructed to explore innovative approaches, such as, leveraging digital technology for disseminating financial literacy content among various target groups. II.88 For ensuring better monitoring of financial literacy activities conducted under Financial Literacy Architecture for Regional Office Environment-Unified Programme (FLARE-UP), FLCs and CFLs, quarterly reports were called for from ROs. II.89 The conduct of Financial Literacy Week (FLW) 2021 with the theme, “Credit discipline and credit from formal institutions”, was undertaken in digital mode. Content in the form of posters were prepared for digital display by banks and other stakeholders. II.90 The challenges posed by the pandemic also offered an opportunity to innovatively meet the multifarious demands of the time, both with respect to the internal functioning of RBI as an organisation and in respect of conducting its statutory obligations. II.91 RBI adopted a balanced approach for deployment of resources for off-site assessment and on-site inspection of the banks. On virtual mode, the Senior Supervisory Manager (SSM) teams engaged with the senior management of banks on a continuous basis on issues emanating from off-site surveillance and monitoring. On-site inspections were conducted adhering to all COVID-19 related protocols. Data was obtained from the banks for conducting off-site examination so that on-site visits could be minimised. Off-site inspection and IT examination of supervised entities (commercial banks / small finance banks / urban co-operative banks / non-banking financial companies) was conducted through Sampark. II.92 In order to proactively sensitise the top management of the supervised entities, a series of meetings were convened online on cyber security preparedness and broad cyber / IT threats. More than 150 supervised entities represented by their MDs and CEOs and their Chief Technology Officers (CTOs) participated in the online meetings. User Acceptance Test (UAT) work related to Corporate Identification Number (CIN) validation was completed with limited resources during the lockdown period. II.93 To ensure continuity in effective supervision of the authorised PSOs, ROs were advised to undertake off-site inspections by calling for required information / data and conducting virtual meetings. Off-site compliance audit of NPCI was conducted to verify the compliance of the earlier inspection observations. Inspection of CCIL was conducted annually, in both the years, viz., 2020 and 2021, in a timely manner. While it was decided that the inspection would be carried out in a hybrid mode (both on-site and off-site), majority of the inspection was conducted on CCIL’s premises observing all COVID-19 related protocols. II.94 With reference to RBI’s internal inspection, while majority of the inspections were online, on-site inspections were carried out ensuring adherence to the local requirements and protocols. Data for conducting the inspections was called through returns over email. II.95 With reference to discharge of statutory function of banker to government, despite COVID-19 related restrictions in place, RBI continued to facilitate the integration of various important government projects with RBI’s eKuber such as the Treasury Single Account System enabling just-in-time e-payments by Central Government Autonomous Bodies, and SPARSH [System of Pension Administration (Raksha)] of the Office of Controller General of Defence Accounts for pension payments. In addition, during 2020 and 2021, inspections of agency banks that undertook government business on behalf of RBI was done mostly on off-site basis. Internal Accounting and Auditing II.96 RBI is vested with the statutory responsibility of (a) preparing and transmitting to the central government, weekly accounts of the Issue and Banking Departments (the Weekly Statement of Affairs – WSA) and (b) transmit to the central government a signed copy of the annual accounts, and certified by the auditors within two months from the date on which the annual accounts of RBI are closed, both of which are TSCAs. II.97 During the period affected by COVID-19, the WSA for each week ending on Friday was prepared and placed for approval before the Central Board / Committee of Central Board (CCB), as the case may be, by the staff working in the Bio-bubble. The annual closing of the books of RBI for the period 2019-20 (from remote location at PDC) and for 2020-21 (with limited availability of staff owing to outbreak of second wave) was successfully completed in time. II.98 In order to ensure successful completion of annual closing and statutory audit, RBI initiated several measures including consultation with nodal CODs and ROs, preparation of detailed SOP with definite timeline for sub-processes, inputs / documents / reports required to be identified and kept ready for audit purpose. As the statutory audit of RBI was being conducted off-site manner for the first time, a special walk-through of all critical functions of RBI was conducted for those auditors auditing RBI for the first time. SOPs were shared with the auditors and detailed action plan was put in place and various financial reports electronically shared with the auditors, in advance. The above measures ensured that statutory audit was completed within the prescribed timeline and annual accounts submitted to the government for the accounting years 2020-2021 and 2021-2022.21 II.99 For service provider management and outsourced staff at the various data centres, it was ensured that they followed protocols and attendance requirements. Meetings were arranged through Sampark and information was disseminated through emails. II.100 To handle the IT related issues, likely to be faced by the officials of the Department of Currency Management (DCM) during WFH scenario, it appointed two Facility Management Services (FMS) engineers in order to ensure adequate back-up for such services and providing round the clock IT related support to all the officials. II.101 Availability of services of empanelled service providers was ensured for handling IT and other critical operations running on on-site and off-site locations. Local Area Network (LAN) engineers were provided accommodation at residential colonies of RBI to ensure availability and smooth functioning of network services. II.102 Centralised Administration Division, Accounts Section, HRMD (CAD) is the nodal section for payment of service provider bills and reimbursement to staff of most of the CODs. In the normal course, CAD makes such payments after receiving the duly sanctioned and audited original hard copies of bills. During the WFH scenario, the requisite documents were sought in soft copies and payment was done through eKuber. The post-payment audit of the bills settled by CAD was carried out through e-mail / soft copies. II.103 For service provider management and outsourced on-site support for Audit Management and Risk Monitoring System (AMRMS), Inspection Department ensured that protocols and attendance requirements were adhered to. Adequate substitute arrangements were chalked out to take care of absence due to infection. II.104 Renewal of Annual Maintenance Contracts (AMCs), floating of tenders and issue of work orders were done well within the stipulated time by Premises Department (PD) to ensure business continuity. Arrangement of taxi services to service providers was made during the lockdown to facilitate smooth functioning of the central office building (COB). To keep them motivated, various service provider teams were felicitated on their meritorious work during lockdown. II.105 Interaction with the service provider for IRIS portal (ReBIT) was done through Sampark. II.106 To avoid disruption in functioning, as conducting ‘in person’ meetings was no longer an option, they were convened online. Sampark, implemented in June 2020, aided in convening virtual interactions and meetings, both internal and external. II.107 To fulfil the statutory requirements of holding at least six meetings of the Central Board in a year and at least once in each quarter, the meetings were held in virtual mode, over end-to-end encrypted mode of Sampark. A secure web-based application was already in use for circulating agenda papers electronically. II.108 Similar to the meetings of the Central Board, face-to-face meetings of the Committee of Central Board (CCB), which as per convention are convened in the last week of the month, were also held over Sampark. Meeting of the Administrators of the Reserve Bank Employees' Provident Fund was also conducted through Sampark. II.109 Upon easing of lockdown measures, meetings of the Central Board were convened ensuring strict compliance of COVID-19 protocols and observance of social distancing norms. These meetings were held in hybrid form with participants attending meetings seated in multiple rooms and connected through Sampark. II.110 Meetings of the Senior Management Committee (SMC) and Deputy Governors’ Committee (DGC) were held through Sampark as and when required with participants provided necessary support to ensure smooth conduct of meetings. II.111 A meeting of the Standing Committee on Finance was organised successfully on September 04, 2021, following all COVID-19 protocols. II.112 Steps taken for maintenance and sanitisation of COB and safety measures in the context of the COVID-19 pandemic are given below: a) MERV-13 filters and Ultraviolet Germicidal Irradiation (UVGI) assemblies were provided in all the Air Handling Units (AHUs) to arrest and deactivate bacteria, virus and fungi. b) UV based disinfection boxes provided on all the floors to disinfect the papers. c) Thermal Cameras (walk through) were installed at the entry to monitor body temperature of the staff and visitors. d) Foot-operated and sensor-based sanitiser dispensers were provided on all floors and at entry / exit points of the building and in opposite the washrooms. e) Hands-free soap dispensers, hand dryers and sensor-based taps were provided near wash basins, and foot-operated door opening mechanism were provided for the washroom doors. f) Air Conditioning duct cleaning was carried out at COB at regular intervals and regular checking of Air Quality was introduced. Eight Air Handling Units (AHU) were replaced for providing better cooling at COB. g) One set of 2x120 KVA Uninterrupted Power Supply (UPS) was replaced for providing uninterrupted power supply to critical IT related load of COB. II.113 Being an unprecedented issue, the effects of pandemic impaired the execution of projects, especially due to lockdown, ban on construction works, restrictions in movement of men and material, de-mobilisation / mobilisation of labour and so on. To address certain issues / concerns raised by the service providers due to the financial crunch faced by them following steps were taken: a) Extension of time was allowed without liquidated damages and price adjustment (wherever applicable). b) Instructions were issued in June 2021, advising reduction of performance bank guarantee from 5 per cent to 3 per cent for tenders invited on or before December 31, 2021. II.114 ROs are RBI’s front office. Most ROs were open even during lockdown ensuring that essential financial services were made available to all the stake holders and customers. They also ensured that the morale of the staff remained high so that they could cope with the pressures of dealing with the hitherto unknown life-threatening health hazard.

“We have lost lives and loved ones, but not hope, not the conviction that we will overcome and emerge stronger” - Shri Shaktikanta Das22 The foregoing pages laying out RBI’s pandemic-time policy responses and process documentation intend to serve as a useful snapshot of its resolve to ‘do whatever is necessary to shield the economy’ in the face of an unprecedented crisis. As a central bank with perhaps the widest possible mandate and, so to say, more than a billion customers, COVID-19 underscored like never before the need for fine and fruitful intersection between our people, processes and technology23. Viewing this sudden threat as an opportunity, RBI sought to reorganise its work processes to build in newer methods for process improvement and augmenting our roles, procedures and technologies. Governor, Shri Shaktikanta Das succinctly conveyed RBI’s commitment when, recalling Nobel Laureate Dr. Martin Luther King Jr.’s words, he said “We must accept finite disappointment, but never lose infinite hope.” Accordingly, this period witnessed, across verticals, a ceaseless cycle of observing, identifying, analysing and reworking of its business processes.24 While the pandemic threatened to cause never-before disruptions across the business landscape, recognising its people as pivots, RBI chose to assign primacy to employee empathy so that the workforce well-being is not compromised and the employees remain safe and motivated. From proactively arranging for vaccination for all the employees and their dependents across locations to making its medical and welfare schemes more liberal and inclusive, for serving as well as the superannuated, to providing additional technological tools to its teams working in isolation, RBI’s focus on workplace empathy led to more innovative and effective employee-engagement initiatives through this period. In turn, RBI employees across CODs, ROs and also hierarchies, responded remarkably to the emerging work challenges and made sure that RBI continued to perform all its tasks efficiently. Going ahead, this comprehensive approach to ideate, innovate and implement would be iterative and RBI stands committed to respond, monitor, design and optimise processes and policies so as to drive continuous improvements to its workflows and enhance outcomes. 1 Selections from Gandhi (Encyclopaedia of Gandhi's Thoughts); Chapter 16, Life of a Satyagrahi; YI, 17-6-26, 215; Nirmal Kumar Bose; Navajivan Mudranalaya, Ahemadabad-380014 India @ Navajivan Trust, 1960. 2 The Minneapolis Tribune (Star Tribune), Quote Page 10, Column 2, January 7, 1970. 3 Helen Keller – Books, Essays and Speeches – Part-III, Optimism – An Essay (1903) - Source: https://www.afb.org/about-afb/history/helen-keller/books-essays-speeches/optimism-1903. 4 “The challenges of today will only strengthen our resilience and self-belief.” (Shri Shaktikanta Das, Governor, RBI - Governor’s Statement – August 6, 2020). 5 Business Continuity Institute (BCI) Good Practice Guidelines 2013. 6 Shri Shaktikanta Das, Governor, RBI at the 7th SBI Banking & Economics Conclave, July 11, 2020. 7 “We are living in a world of Knightian uncertainty in the absence of determinate knowledge about the next mutation of COVID-19. The ability to forecast the future course of the economy is so contingent on the evolution of the virus that one prognosis is as good or as bad as the other and as ephemeral.” (Shri Shaktikanta Das, Governor, RBI - Governor’s Statement – February 10, 2022). 8 Mahatma Gandhi, Young India, March 21, 1929, Quoted by Shri Shaktikanta Das, Governor, RBI - Governor’s Statement – May 22, 2020. 9 Business Units (BUs) are the central office departments (CODs), regional offices (ROs) and training establishments of the Reserve Bank of India. 10 Details at Box II.4 11 RBI worked through the COVID-19 pandemic to create a new real-time gross settlement system that can operate around the clock. This included the challenge of putting essential staff inside a “bio-bubble” to shield them from the virus. The new system shall open up avenues for greater payments innovation at lower cost.” (Central Banking Award for Payment and Market Infrastructure – Wholesale, 2022 conferred on RBI). 12 “We were perhaps the only central bank in the world to have set up a special quarantine facility with about 200 officers, staff and service providers, engaged in critical activities to ensure business continuity in banking and financial market operations and payment systems.” – Shri Shaktikanta Das, Governor, RBI - Governor’s Statement – August 6, 2020. 13 Excerpts from address by Governor, RBI on March 4, 2022 – delivered at the National Defence College, Ministry of Defence, Government of India, New Delhi. 14 Targeted Long Term Repo Operations (TLTROs) allows banks to borrow funds from RBI over a one to three year period at the repo rate. The borrowing is against government securities with similar or higher tenure as collateral. The funds so borrowed can be utilised for investment in specific sectors through debt instruments {corporate bonds, commercial papers, and non-convertible debentures (NCDs)}. It was introduced to mitigate the adverse effects on economic activity due to pressures on cash flows across sectors, arising out of the COVID-19 pandemic. 15 RBI had taken numerous measures (over 100) during the pandemic. Many of these have been summarised in this compendium. 16 Shri Shaktikanta Das, Governor, RBI - Governor’s Statement – April 8, 2022. 17 Translation: 18 Authorised dealer category-I banks are banks which are permitted to undertake all current and capital account transactions according to RBI directions issued from time-to-time. 19 “Be not careless in your deeds, nor confused in words, nor rambling in thought.” – Meditations by Marcus Aurelius, Book VIII, (51), (c. 161 - 180 AD). 20 Inaugural address by Shri Shaktikanta Das, Governor, RBI - July 15, 2021 - delivered at the Economic Times Financial Inclusion Summit. 21 RBI transited its accounting year from July to June to April to March in the year 2020-2021. 2020-2021 was a nine month year (from July 2020 to March 2021). In spite of the restrictions running on account of COVID-19, the transition was smooth and non-disruptive. 22 Shri Shaktikanta Das, Governor, RBI - Governor’s Statement – December 4, 2020. 23 “Although social distancing separates us, we stand united and resolute. Eventually, we shall cure; and we shall endure.” (Shri Shaktikanta Das, Governor, RBI - Governor’s Statement – April 17, 2020). 24 “It is worthwhile to remember that tough times never last; only tough people and tough institutions do.” (Shri Shaktikanta Das, Governor, RBI - Governor’s Statement – March 27, 2020). | |||||||||||||||||

Install the RBI mobile application and get quick access to the latest news!

Scan the QR code to install our app

Page Last Updated on: