IST,

IST,

Content Type:

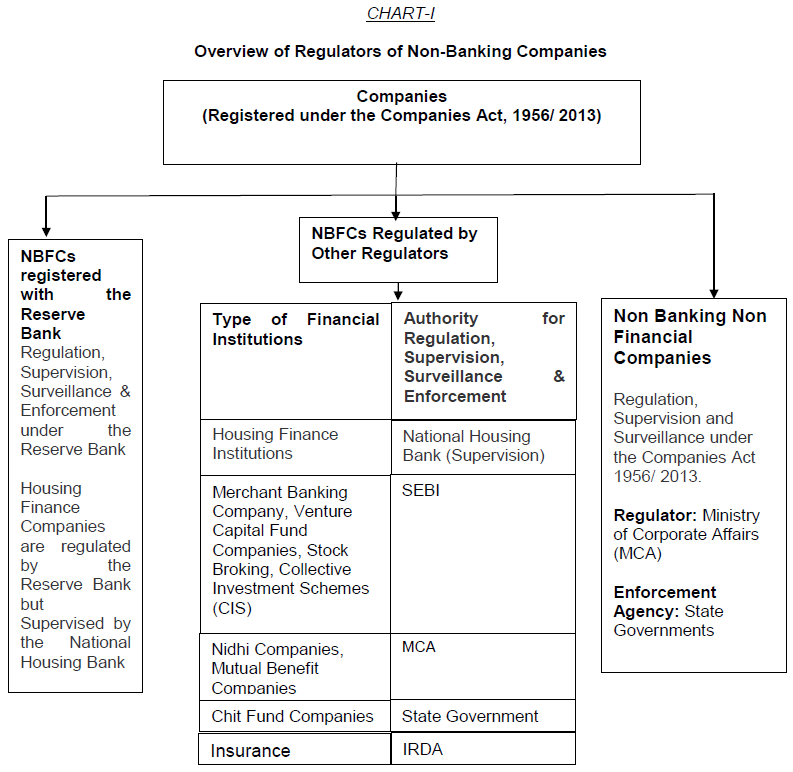

All you wanted to know about NBFCs

H. Other/ miscellaneous aspects

Commercial Real Estate (CRE) would consist of loans to builders/ developers/ others for creation/ acquisition of commercial real estate (such as office building, retail space, multi-purpose commercial premises, multi-tenanted commercial premises, industrial or warehouse space, hotels, land acquisition, development and construction etc.) where the prospects for repayment, or recovery in case of default, would depend primarily on the cash flows generated by the asset by way of lease/rental payments, sale etc. Further, loans for third dwelling unit onwards to an individual will be treated as CRE exposure. Exposure shall also include non-fund based limits.

Commercial Real Estate – Residential Housing (CRE–RH) is a sub-category of CRE that consist of loans to builders/ developers for residential housing projects (except for captive consumption). Such projects should ordinarily not include non-residential commercial real estate. However integrated housing project comprising of some commercial spaces (e.g., shopping complex, school etc.) can also be specified under CRE-RH, provided that the commercial area in the residential housing project does not exceed 10 percent of the total Floor Space Index (FSI) of the project. In case the FSI of the commercial area in the predominantly residential housing complex exceed the ceiling of 10 percent, the entire loan should be classified as CRE and not CRE-RH.

No, the group requires to consolidate total assets of only those NBFCs which have been granted Certificate of Registration by the Bank. However, in case unregistered CICs in the group with asset size below ₹100 crore have accessed public funds, the asset size of such CICs shall be consolidated for the above purpose, but it would not change the status of unregistered CICs.

Loans against units of mutual funds (except units of exclusively debt oriented mutual funds) would attract LTV requirements as applicable to loans against shares. Further, the LTV requirement for loans/ advances against units of exclusively debt-oriented mutual funds may be decided by individual NBFCs in accordance with their loan policy.

In this case prior written approval of the Reserve Bank is to be obtained by the NBFC ‘A’. In case NBFC ‘A’ would cease to exist after the merger, the Certificate of Registration shall be surrendered for cancellation. Where ‘B’ is an NBFC, as a result of merger if there is change in control in ‘B’, or change in shareholding pattern of paid-up equity capital of ‘B’ by 26% or more, or change in management in ‘B’ which would result in change in more than 30% of the directors (excluding independent directors), prior written approval of the Reserve Bank is required. If ‘B’ is not an NBFC but is likely to meet Principal Business Criteria (i.e., 50-50 criteria) post-merger, it would also need to approach the Reserve Bank for prior written approval as well as registration as an NBFC.

Where a non-NBFC mergers with an NBFC, prior written approval of the Reserve Bank would be required if such a merger satisfies any one or all of the conditions viz., (i) any change in control in the NBFC due to merger, (ii) any change in the shareholding of the NBFC consequent to the merger which would result in change in shareholding of 26% or more of the paid up equity capital of the NBFC, (iii) any change in the management of the NBFC which would result in change in more than 30% of the directors, excluding independent directors. It may be noted that the NBFC shall continue to fulfil the Principal Business Criteria (i.e., 50-50 criteria) after merger to be eligible to hold the Certificate of Registration as an NBFC.

The NBFCs being amalgamated will require to obtain prior written approval of the Reserve Bank. Depending upon the nature of amalgamation/merger proposal, requisite approvals as per regulations needs to be sought.

Yes, prior approval of the Reserve Bank would have to be obtained before approaching any Court or Tribunal seeking orders for merger/ amalgamation in all such cases which would ordinarily fall under the scenarios explained in FAQs 84, 85 or 86.

Disclaimer: These FAQs are issued by the Reserve Bank for information and general guidance purposes only. The Reserve Bank will not be held responsible for actions taken and/or decisions made on the basis of the same. For clarifications or interpretations, if any, one may be guided by the relevant circulars and notifications issued from time to time.

| Related Press Release | |

| May 31, 2013 | Check before Depositing Money with Financial Entities: RBI Advisory |

Install the RBI mobile application and get quick access to the latest news!

Scan the QR code to install our app