IST,

IST,

Monetary Policy Statement, 2024-25 Resolution of the Monetary Policy Committee (MPC) April 3 to 5, 2024

|

On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (April 5, 2024) decided to:

Consequently, the standing deposit facility (SDF) rate remains unchanged at 6.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 6.75 per cent.

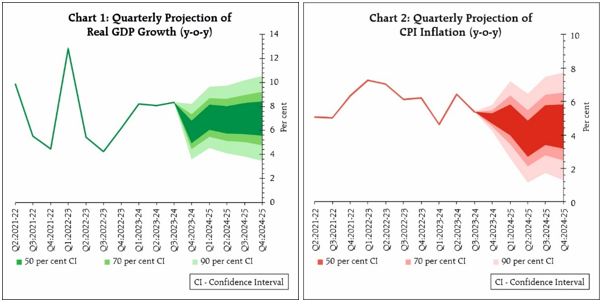

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. Assessment and Outlook 2. The global economy exhibits resilience and is likely to maintain its steady growth in 2024. Inflation is treading down, supported by favourable base effects though stubborn services prices are keeping it elevated relative to targets. As the central banks navigate the last mile of disinflation, financial markets are responding to changing perceptions on the timing and pace of monetary policy trajectories. Equity markets are rallying, while sovereign bond yields and the US dollar are exhibiting bidirectional movements. Gold prices have surged on safe haven demand. 3. The domestic economy is experiencing strong momentum. As per the second advance estimates (SAE), real gross domestic product (GDP) expanded at 7.6 per cent in 2023-24 on the back of buoyant domestic demand. Real GDP increased by 8.4 per cent in Q3, with strong investment activity and a lower drag from net external demand. On the supply side, gross value added recorded a growth of 6.9 per cent in 2023-24, driven by manufacturing and construction activity. 4. Looking ahead, an expected normal south-west monsoon should support agricultural activity. Manufacturing is expected to maintain its momentum on the back of sustained profitability. Services activity is likely to grow above the pre-pandemic trend. Private consumption should gain steam with further pick-up in rural activity and steady urban demand. A rise in discretionary spending expected by urban households, as per the Reserve Bank’s consumer survey, and improving income levels augur well for the strengthening of private consumption. The prospects of fixed investment remain bright with business optimism, healthy corporate and bank balance sheets, robust government capital expenditure and signs of upturn in the private capex cycle. Headwinds from geopolitical tensions, volatility in international financial markets, geoeconomic fragmentation, rising Red Sea disruptions, and extreme weather events, however, pose risks to the outlook. Taking all these factors into consideration, real GDP growth for 2024-25 is projected at 7.0 per cent with Q1 at 7.1 per cent; Q2 at 6.9 per cent; Q3 at 7.0 per cent; and Q4 at 7.0 per cent (Chart 1). The risks are evenly balanced. 5. Headline inflation softened to 5.1 per cent during January-February 2024, from 5.7 per cent in December. After correcting in January, food inflation edged up to 7.8 per cent in February primarily driven by vegetables, eggs, meat and fish. Fuel prices remained in deflation for the sixth consecutive month in February. CPI core (CPI excluding food and fuel) disinflation took it down to 3.4 per cent in February – this was one of the lowest in the current CPI series, with both goods and services components registering a fall in inflation. 6. Going ahead, food price uncertainties would continue to weigh on the inflation outlook. An expected record rabi wheat production in 2023-24, however, will help contain cereal prices. Early indications of a normal monsoon also augur well for the kharif season. On the other hand, the increasing incidence of climate shocks remains a key upside risk to food prices. Low reservoir levels, especially in the southern states and outlook of above normal temperatures during April-June, also pose concern. Tight demand supply conditions in certain pulses and the prices of key vegetables need close monitoring. Fuel price deflation is likely to deepen in the near term following the recent cut in LPG prices. After witnessing sustained moderation, cost push pressures faced by firms are showing upward bias. The recent firming up of international crude oil prices warrants close monitoring. Geo-political tensions and volatility in financial markets also pose risks to the inflation outlook. Taking into account these factors and assuming a normal monsoon, CPI inflation for 2024-25 is projected at 4.5 per cent with Q1 at 4.9 per cent; Q2 at 3.8 per cent; Q3 at 4.6 per cent; and Q4 at 4.5 per cent (Chart 2). The risks are evenly balanced.

8. Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to keep the policy repo rate unchanged at 6.50 per cent. Prof. Jayanth R. Varma voted to reduce the policy repo rate by 25 basis points. 9. Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth. Prof. Jayanth R. Varma voted for a change in stance to neutral. 10. The minutes of the MPC’s meeting will be published on April 19, 2024. 11. The next meeting of the MPC is scheduled during June 5 to 7, 2024.

(Yogesh Dayal) Press Release: 2024-2025/42 |

এই পৃষ্ঠাটো শ্বেয়াৰ কৰক:

ভাৰতীয় ৰিজাৰ্ভ বেংক মোবাইল এপ্পলিকেষ্যন ইনষ্টল কৰক আৰু নৱীনতম বাতৰিৰ প্ৰৱেশাধিকাৰ পাওক!

আমাৰ এপটো ইনষ্টল কৰিবলৈ QR ক’ড স্কেন কৰক

পৃষ্ঠাটো শেহতীয়া আপডেট কৰা তাৰিখ: