Today, the Reserve Bank released the results of the 96th round of the Industrial Outlook Survey (IOS). The survey encapsulates qualitative assessment of the business climate by Indian manufacturing companies for Q3:2021-22 and their expectations for Q4:2021-221. In all, 1082 companies responded in this round of the survey conducted during October-December 2021. Owing to uncertainty driven by the COVID-19 pandemic, an additional block was included in this round of the survey for assessing the outlook on key parameters for two quarters ahead as well as three quarters ahead. Highlights: A. Assessment for Q3: 2021-22 -

Manufacturing enterprises assessed improvement in demand condition in terms of production, order books and employment situation in Q3:2021-22, albeit at a slower pace when compared to the previous survey round (Table A). -

Sentiments on capacity utilisation and availability of finance improved further in Q3:2021-22. -

Manufacturers perceived continued price pressures with some softening in the pace of increase in input cost and selling prices. -

Profit margin is assessed to remain in positive terrain with some moderation vis-à-vis the preceding quarter. -

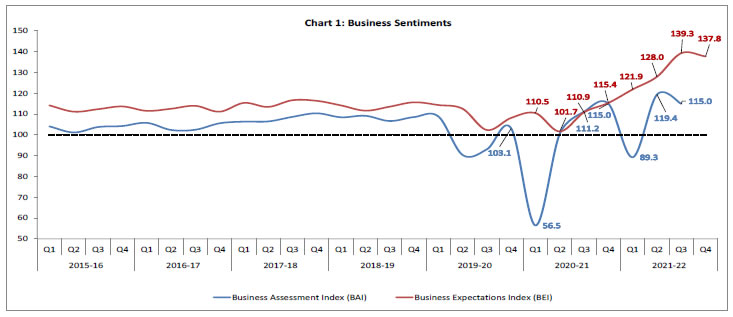

Business sentiments of manufacturers remained well in the expansion terrain though it waned marginally, as reflected in the business assessment index (BAI)2 which stood at 115.0 in Q3:2021-223 as compared to 119.4 in the previous quarter (Chart 1). B. Expectations for Q4: 2021-22 -

Respondents expressed optimism in Q4:2021-22 on demand parameters such as production volumes, new orders and job landscape. -

Capacity utilisation and overall financial situation are expected to improve further in Q4:2021-22, though the optimism moderated from the previous quarter. -

Input cost pressures are likely to remain elevated in Q4:2021-22; the pace of rise in selling prices is expected to witness some softening. -

Overall business expectations index (BEI) moderated to 137.8 in Q4:2021-22 from 139.3 in the previous quarter (Chart 1). C. Expectations for Q1:2022-23 and Q2:2022-23 -

Manufacturers perceive sequential improvements in demand conditions, capacity utilisation and overall business situation till Q2:2022-23 (Table B). -

Respondents expect input cost pressures to continue, albeit with marginal easing, in the first half of 2022-23. | Table A: Summary of Net responses4 on Survey Parameters | | (per cent) | | Parameters | Assessment period | Expectation period | | Q2:2021-22 | Q3:2021-22 | Q3:2021-22 | Q4:2021-22 | | Production | 33.8 | 30.9 | 71.5 | 61.2 | | Order Books | 34.7 | 29.5 | 70.3 | 61.5 | | Pending Orders | -1.6 | 3.6 | -4.1 | -0.5 | | Capacity Utilisation | 28.8 | 22.2 | 65.2 | 52.6 | | Inventory of Raw Materials | -14.7 | -11.4 | -29.4 | -29.0 | | Inventory of Finished Goods | -14.9 | -9.8 | -30.7 | -27.2 | | Exports | 31.5 | 20.0 | 64.3 | 54.7 | | Imports | 30.2 | 19.9 | 60.4 | 51.8 | | Employment | 24.9 | 19.8 | 50.9 | 47.2 | | Financial Situation (Overall) | 32.8 | 28.3 | 68.6 | 59.3 | | Availability of Finance (from internal accruals) | 28.5 | 24.8 | 61.9 | 52.9 | | Availability of Finance (from banks & other sources) | 28.3 | 22.4 | 58.7 | 49.8 | | Availability of Finance (from overseas, if applicable) | 31.5 | 19.0 | 65.9 | 50.9 | | Cost of Finance | -28.6 | -19.4 | -55.8 | -48.6 | | Cost of Raw Material | -61.0 | -58.8 | -75.2 | -73.6 | | Salary/ Other Remuneration | -31.3 | -26.9 | -50.4 | -49.9 | | Selling Price | 38.2 | 28.2 | 57.4 | 50.3 | | Profit Margin | 9.4 | 3.8 | 51.7 | 39.8 | | Overall Business Situation | 34.0 | 32.5 | 70.3 | 63.4 | | Note: Please see the excel file for time series data. |

| Table B: Business Expectations of Select Parameters for extended period – Net response | | (per cent) | | Parameters | Round 95 | Round 96 | | Q3:2021-22 | Q4:2021-22 | Q1:2022-23 | Q2:2022-23 | | Overall Business Situation | 70.3 | 63.4 | 66.8 | 67.2 | | Production | 71.5 | 61.2 | 65.4 | 67.1 | | Order Books | 70.3 | 61.5 | 62.8 | 64.5 | | Capacity Utilisation | 65.2 | 52.6 | 58.6 | 59.5 | | Employment | 50.9 | 47.2 | 53.1 | 51.6 | | Cost of Raw Materials | -75.2 | -73.6 | -71.2 | -69.8 | | Selling Prices | 57.4 | 50.3 | 55.9 | 53.6 |

| Table 1: Assessment and Expectations for Production | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q3:2020-21 | 1,011 | 46.6 | 19.4 | 34.0 | 27.2 | 43.4 | 16.9 | 39.7 | 26.4 | | Q4:2020-21 | 967 | 48.9 | 12.6 | 38.5 | 36.3 | 43.7 | 12.2 | 44.0 | 31.5 | | Q1:2021-22 | 1,281 | 16.5 | 42.3 | 41.2 | -25.9 | 53.3 | 9.7 | 37.0 | 43.7 | | Q2:2021-22 | 1,414 | 44.5 | 10.7 | 44.8 | 33.8 | 58.8 | 6.8 | 34.3 | 52.0 | | Q3:2021-22 | 1,082 | 42.5 | 11.6 | 45.9 | 30.9 | 75.3 | 3.8 | 20.9 | 71.5 | | Q4:2021-22 | | | | | | 66.5 | 5.3 | 28.3 | 61.2 | ‘Increase’ in production is optimistic.

Note: The sum of components may not add up to total due to rounding off (This is applicable for all tables). |

| Table 2: Assessment and Expectations for Order Books | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q3:2020-21 | 1,011 | 40.3 | 19.8 | 40.0 | 20.5 | 39.2 | 18.6 | 42.2 | 20.6 | | Q4:2020-21 | 967 | 46.4 | 13.3 | 40.3 | 33.1 | 41.1 | 13.7 | 45.2 | 27.3 | | Q1:2021-22 | 1,281 | 20.0 | 36.5 | 43.5 | -16.4 | 51.0 | 7.8 | 41.1 | 43.2 | | Q2:2021-22 | 1,414 | 44.9 | 10.1 | 45.0 | 34.7 | 56.9 | 6.5 | 36.7 | 50.4 | | Q3:2021-22 | 1,082 | 39.0 | 9.5 | 51.5 | 29.5 | 73.9 | 3.6 | 22.4 | 70.3 | | Q4:2021-22 | | | | | | 66.2 | 4.7 | 29.1 | 61.5 | | ‘Increase’ in order books is optimistic. |

| Table 3: Assessment and Expectations for Pending Orders | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Above Normal | Below Normal | Normal | Net response | Above Normal | Below Normal | Normal | Net response | | Q3:2020-21 | 1,011 | 7.2 | 19.2 | 73.6 | 12.0 | 7.4 | 21.5 | 71.1 | 14.2 | | Q4:2020-21 | 967 | 13.2 | 10.2 | 76.6 | -3.0 | 5.6 | 14.8 | 79.7 | 9.2 | | Q1:2021-22 | 1,281 | 7.4 | 17.5 | 75.1 | 10.0 | 11.6 | 9.2 | 79.3 | -2.4 | | Q2:2021-22 | 1,414 | 9.6 | 8.1 | 82.3 | -1.6 | 10.8 | 7.2 | 82.0 | -3.7 | | Q3:2021-22 | 1,082 | 7.2 | 10.9 | 81.9 | 3.6 | 8.8 | 4.8 | 86.4 | -4.1 | | Q4:2021-22 | | | | | | 8.5 | 7.9 | 83.6 | -0.5 | | Pending orders ‘Below Normal’ is optimistic. |

| Table 4: Assessment and Expectations for Capacity Utilisation (Main Product) | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q3:2020-21 | 1,011 | 35.3 | 18.0 | 46.7 | 17.3 | 32.4 | 15.0 | 52.6 | 17.5 | | Q4:2020-21 | 967 | 40.6 | 11.5 | 47.9 | 29.1 | 34.7 | 10.6 | 54.7 | 24.1 | | Q1:2021-22 | 1,281 | 13.4 | 39.5 | 47.1 | -26.1 | 45.2 | 7.3 | 47.5 | 38.0 | | Q2:2021-22 | 1,414 | 39.2 | 10.4 | 50.4 | 28.8 | 51.6 | 6.2 | 42.2 | 45.4 | | Q3:2021-22 | 1,082 | 31.2 | 9.0 | 59.8 | 22.2 | 68.3 | 3.1 | 28.5 | 65.2 | | Q4:2021-22 | | | | | | 57.0 | 4.5 | 38.5 | 52.6 | | ‘Increase’ in capacity utilisation is optimistic. |

| Table 5: Assessment and Expectations for Level of CU (compared to the average in last 4 quarters) | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Above Normal | Below Normal | Normal | Net response | Above Normal | Below Normal | Normal | Net response | | Q3:2020-21 | 1,011 | 11.3 | 23.2 | 65.5 | -12.0 | 8.3 | 25.5 | 66.2 | -17.2 | | Q4:2020-21 | 967 | 21.3 | 12.2 | 66.5 | 9.1 | 11.7 | 15.3 | 73.0 | -3.6 | | Q1:2021-22 | 1,281 | 5.2 | 18.4 | 76.3 | -13.2 | 25.3 | 8.4 | 66.2 | 16.9 | | Q2:2021-22 | 1,414 | 15.4 | 7.7 | 76.9 | 7.8 | 15.6 | 7.9 | 76.5 | 7.7 | | Q3:2021-22 | 1,082 | 12.6 | 8.4 | 78.9 | 4.2 | 30.4 | 3.7 | 65.9 | 26.7 | | Q4:2021-22 | | | | | | 30.1 | 5.8 | 64.2 | 24.3 | | ‘Above Normal’ in Level of capacity utilisation is optimistic. |

| Table 6: Assessment and Expectations for Assessment of Production Capacity (with regard to expected demand in next 6 months) | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | More than adequate | Less than adequate | Adequate | Net response | More than adequate | Less than adequate | Adequate | Net response | | Q3:2020-21 | 1,011 | 14.1 | 11.2 | 74.6 | 2.9 | 15.9 | 12.3 | 71.8 | 3.5 | | Q4:2020-21 | 967 | 15.5 | 10.0 | 74.5 | 5.5 | 14.2 | 9.3 | 76.5 | 5.0 | | Q1:2021-22 | 1,281 | 10.8 | 13.0 | 76.2 | -2.2 | 20.2 | 7.3 | 72.5 | 12.9 | | Q2:2021-22 | 1,414 | 17.3 | 7.6 | 75.1 | 9.7 | 28.4 | 5.8 | 65.8 | 22.6 | | Q3:2021-22 | 1,082 | 13.2 | 6.1 | 80.6 | 7.1 | 31.0 | 4.0 | 65.1 | 27.0 | | Q4:2021-22 | | | | | | 30.7 | 4.0 | 65.3 | 26.7 | | ‘More than adequate’ in Assessment of Production Capacity is optimistic. |

| Table 7: Assessment and Expectations for Exports | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q3:2020-21 | 1,011 | 22.5 | 17.9 | 59.5 | 4.6 | 25.1 | 17.6 | 57.3 | 7.5 | | Q4:2020-21 | 967 | 31.6 | 16.0 | 52.4 | 15.5 | 25.1 | 12.1 | 62.7 | 13.0 | | Q1:2021-22 | 1,281 | 18.3 | 26.1 | 55.6 | -7.8 | 38.7 | 9.0 | 52.3 | 29.6 | | Q2:2021-22 | 1,414 | 39.2 | 7.7 | 53.0 | 31.5 | 49.8 | 6.2 | 44.0 | 43.6 | | Q3:2021-22 | 1,082 | 29.8 | 9.7 | 60.5 | 20.0 | 67.3 | 3.1 | 29.6 | 64.3 | | Q4:2021-22 | | | | | | 59.2 | 4.5 | 36.4 | 54.7 | | ‘Increase’ in exports is optimistic. |

| Table 8: Assessment and Expectations for Imports | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q3:2020-21 | 1,011 | 19.6 | 13.3 | 67.2 | 6.3 | 17.3 | 12.4 | 70.4 | 4.9 | | Q4:2020-21 | 967 | 25.8 | 9.3 | 64.9 | 16.4 | 17.7 | 9.1 | 73.2 | 8.5 | | Q1:2021-22 | 1,281 | 18.9 | 17.1 | 64.0 | 1.7 | 32.6 | 6.6 | 60.8 | 26.1 | | Q2:2021-22 | 1,414 | 36.0 | 5.8 | 58.2 | 30.2 | 47.3 | 4.5 | 48.3 | 42.8 | | Q3:2021-22 | 1,082 | 26.8 | 6.9 | 66.3 | 19.9 | 63.4 | 2.9 | 33.7 | 60.4 | | Q4:2021-22 | | | | | | 55.6 | 3.8 | 40.6 | 51.8 | | ‘Increase’ in imports is optimistic. |

| Table 9: Assessment and Expectations for level of Raw Materials Inventory | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Above average | Below average | Average | Net response | Above average | Below average | Average | Net response | | Q3:2020-21 | 1,011 | 13.1 | 7.7 | 79.3 | -5.4 | 11.5 | 7.4 | 81.1 | -4.2 | | Q4:2020-21 | 967 | 17.5 | 6.5 | 76.0 | -11.1 | 12.0 | 5.3 | 82.8 | -6.7 | | Q1:2021-22 | 1,281 | 11.5 | 11.2 | 77.3 | -0.3 | 17.2 | 5.4 | 77.4 | -11.8 | | Q2:2021-22 | 1,414 | 20.2 | 5.5 | 74.4 | -14.7 | 23.7 | 6.2 | 70.0 | -17.5 | | Q3:2021-22 | 1,082 | 16.5 | 5.1 | 78.4 | -11.4 | 33.7 | 4.4 | 61.9 | -29.4 | | Q4:2021-22 | | | | | | 32.7 | 3.7 | 63.5 | -29.0 | | ‘Below average’ Inventory of raw materials is optimistic. |

| Table 10: Assessment and Expectations for level of Finished Goods Inventory | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Above average | Below average | Average | Net response | Above average | Below average | Average | Net response | | Q3:2020-21 | 1,011 | 12.8 | 8.1 | 79.1 | -4.6 | 12.4 | 7.2 | 80.4 | -5.3 | | Q4:2020-21 | 967 | 15.2 | 7.5 | 77.3 | -7.6 | 11.5 | 5.1 | 83.4 | -6.3 | | Q1:2021-22 | 1,281 | 14.4 | 10.2 | 75.4 | -4.2 | 16.4 | 5.5 | 78.1 | -10.9 | | Q2:2021-22 | 1,414 | 20.0 | 5.2 | 74.8 | -14.9 | 25.0 | 5.6 | 69.4 | -19.4 | | Q3:2021-22 | 1,082 | 15.3 | 5.5 | 79.2 | -9.8 | 34.4 | 3.8 | 61.8 | -30.7 | | Q4:2021-22 | | | | | | 31.1 | 3.9 | 64.9 | -27.2 | | ‘Below average’ Inventory of finished goods is optimistic. |

| Table 11: Assessment and Expectations for Employment | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q3:2020-21 | 1,011 | 15.5 | 11.6 | 73.0 | 3.9 | 14.5 | 12.1 | 73.3 | 2.4 | | Q4:2020-21 | 967 | 19.4 | 8.5 | 72.1 | 10.9 | 14.6 | 7.3 | 78.1 | 7.2 | | Q1:2021-22 | 1,281 | 9.1 | 12.7 | 78.2 | -3.5 | 23.5 | 5.5 | 71.0 | 17.9 | | Q2:2021-22 | 1,414 | 29.5 | 4.6 | 65.9 | 24.9 | 28.6 | 2.5 | 69.0 | 26.1 | | Q3:2021-22 | 1,082 | 25.3 | 5.4 | 69.3 | 19.8 | 52.2 | 1.3 | 46.5 | 50.9 | | Q4:2021-22 | | | | | | 49.2 | 2.0 | 48.8 | 47.2 | | ‘Increase’ in employment is optimistic. |

| Table 12: Assessment and Expectations for Overall Financial Situation | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Better | Worsen | No change | Net response | Better | Worsen | No change | Net response | | Q3:2020-21 | 1,011 | 40.4 | 12.9 | 46.7 | 27.5 | 36.7 | 11.4 | 51.9 | 25.3 | | Q4:2020-21 | 967 | 43.0 | 13.6 | 43.4 | 29.4 | 39.2 | 6.2 | 54.6 | 33.0 | | Q1:2021-22 | 1,281 | 17.8 | 30.6 | 51.6 | -12.7 | 53.4 | 6.1 | 40.5 | 47.3 | | Q2:2021-22 | 1,414 | 41.7 | 8.9 | 49.4 | 32.8 | 54.0 | 5.8 | 40.2 | 48.2 | | Q3:2021-22 | 1,082 | 38.1 | 9.8 | 52.0 | 28.3 | 71.5 | 2.9 | 25.7 | 68.6 | | Q4:2021-22 | | | | | | 64.0 | 4.7 | 31.3 | 59.3 | | ‘Better’ overall financial situation is optimistic. |

| Table 13: Assessment and Expectations for Working Capital Finance Requirement | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q3:2020-21 | 1,011 | 30.7 | 7.1 | 62.2 | 23.7 | 31.3 | 6.9 | 61.8 | 24.4 | | Q4:2020-21 | 967 | 30.8 | 7.7 | 61.4 | 23.1 | 28.5 | 3.7 | 67.8 | 24.8 | | Q1:2021-22 | 1,281 | 24.4 | 14.0 | 61.7 | 10.4 | 37.6 | 5.2 | 57.3 | 32.4 | | Q2:2021-22 | 1,414 | 39.6 | 4.7 | 55.7 | 34.9 | 44.7 | 3.0 | 52.2 | 41.7 | | Q3:2021-22 | 1,082 | 31.6 | 4.5 | 63.9 | 27.1 | 63.3 | 2.2 | 34.4 | 61.1 | | Q4:2021-22 | | | | | | 54.7 | 2.9 | 42.4 | 51.7 | | ‘Increase’ in working capital finance is optimistic. |

| Table 14: Assessment and Expectations for Availability of Finance (from Internal Accruals) | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Improve | Worsen | No change | Net response | Improve | Worsen | No change | Net response | | Q3:2020-21 | 1,011 | 27.2 | 9.7 | 63.1 | 17.4 | 24.8 | 9.7 | 65.5 | 15.1 | | Q4:2020-21 | 967 | 33.3 | 9.6 | 57.1 | 23.7 | 28.3 | 5.6 | 66.1 | 22.8 | | Q1:2021-22 | 1,281 | 13.3 | 17.6 | 69.1 | -4.3 | 39.7 | 5.1 | 55.2 | 34.7 | | Q2:2021-22 | 1,414 | 35.3 | 6.8 | 57.9 | 28.5 | 42.4 | 3.8 | 53.7 | 38.6 | | Q3:2021-22 | 1,082 | 30.6 | 5.8 | 63.6 | 24.8 | 64.1 | 2.1 | 33.8 | 61.9 | | Q4:2021-22 | | | | | | 55.7 | 2.8 | 41.5 | 52.9 | | ‘Improvement’ in availability of finance is optimistic. |

| Table 15: Assessment and Expectations for Availability of Finance (from banks and other sources) | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Improve | Worsen | No change | Net response | Improve | Worsen | No change | Net response | | Q3:2020-21 | 1,011 | 21.0 | 6.1 | 72.8 | 14.9 | 19.4 | 5.8 | 74.8 | 13.6 | | Q4:2020-21 | 967 | 23.1 | 6.6 | 70.3 | 16.5 | 19.6 | 4.3 | 76.1 | 15.3 | | Q1:2021-22 | 1,281 | 10.7 | 13.1 | 76.1 | -2.4 | 30.0 | 4.4 | 65.6 | 25.6 | | Q2:2021-22 | 1,414 | 33.2 | 4.9 | 61.8 | 28.3 | 38.4 | 2.9 | 58.8 | 35.5 | | Q3:2021-22 | 1,082 | 26.2 | 3.9 | 69.9 | 22.4 | 60.6 | 1.9 | 37.5 | 58.7 | | Q4:2021-22 | | | | | | 52.0 | 2.1 | 45.9 | 49.8 | | ‘Improvement’ in availability of finance is optimistic. |

| Table 16: Assessment and Expectations for Availability of Finance (from overseas, if applicable) | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Improve | Worsen | No change | Net response | Improve | Worsen | No change | Net response | | Q3:2020-21 | 1,011 | 5.8 | 5.0 | 89.2 | 0.8 | 7.2 | 6.6 | 86.1 | 0.6 | | Q4:2020-21 | 967 | 7.5 | 4.8 | 87.7 | 2.7 | 7.2 | 3.4 | 89.3 | 3.8 | | Q1:2021-22 | 1,281 | 13.6 | 12.0 | 74.5 | 1.6 | 16.5 | 3.1 | 80.3 | 13.4 | | Q2:2021-22 | 1,414 | 33.8 | 2.3 | 63.9 | 31.5 | 44.0 | 1.3 | 54.7 | 42.7 | | Q3:2021-22 | 1,082 | 22.4 | 3.4 | 74.1 | 19.0 | 66.5 | 0.6 | 32.8 | 65.9 | | Q4:2021-22 | | | | | | 52.5 | 1.5 | 46.0 | 50.9 | | ‘Improvement’ in availability of finance is optimistic. |

| Table 17: Assessment and Expectations for Cost of Finance | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q3:2020-21 | 1,011 | 13.3 | 13.5 | 73.2 | 0.2 | 15.5 | 8.8 | 75.7 | -6.7 | | Q4:2020-21 | 967 | 16.7 | 13.3 | 70.0 | -3.4 | 13.3 | 8.3 | 78.4 | -5.0 | | Q1:2021-22 | 1,281 | 15.7 | 11.3 | 73.0 | -4.5 | 22.2 | 8.2 | 69.6 | -13.9 | | Q2:2021-22 | 1,414 | 32.5 | 4.0 | 63.5 | -28.6 | 34.9 | 3.3 | 61.8 | -31.5 | | Q3:2021-22 | 1,082 | 24.9 | 5.5 | 69.5 | -19.4 | 58.3 | 2.5 | 39.3 | -55.8 | | Q4:2021-22 | | | | | | 50.7 | 2.1 | 47.2 | -48.6 | | ‘Decrease’ in cost of finance is optimistic. |

| Table 18: Assessment and Expectations for Cost of Raw Materials | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q3:2020-21 | 1,011 | 55.5 | 3.9 | 40.6 | -51.6 | 36.7 | 4.6 | 58.7 | -32.1 | | Q4:2020-21 | 967 | 71.0 | 2.0 | 26.9 | -69.0 | 45.2 | 2.6 | 52.2 | -42.7 | | Q1:2021-22 | 1,281 | 58.1 | 5.8 | 36.1 | -52.3 | 64.9 | 2.5 | 32.6 | -62.4 | | Q2:2021-22 | 1,414 | 62.5 | 1.4 | 36.1 | -61.0 | 56.8 | 2.0 | 41.2 | -54.9 | | Q3:2021-22 | 1,082 | 62.0 | 3.2 | 34.8 | -58.8 | 76.6 | 1.4 | 22.1 | -75.2 | | Q4:2021-22 | | | | | | 75.1 | 1.5 | 23.3 | -73.6 | | ‘Decrease’ in cost of raw materials is optimistic. |

| Table 19: Assessment and Expectations for Salary/Other Remuneration | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q3:2020-21 | 1,011 | 20.8 | 6.8 | 72.3 | -14.0 | 15.8 | 6.8 | 77.4 | -9.0 | | Q4:2020-21 | 967 | 21.8 | 3.1 | 75.1 | -18.7 | 19.9 | 3.9 | 76.2 | -16.0 | | Q1:2021-22 | 1,281 | 26.4 | 6.5 | 67.1 | -19.9 | 42.7 | 1.2 | 56.1 | -41.6 | | Q2:2021-22 | 1,414 | 33.1 | 1.8 | 65.2 | -31.3 | 32.5 | 0.9 | 66.6 | -31.6 | | Q3:2021-22 | 1,082 | 29.3 | 2.4 | 68.3 | -26.9 | 51.2 | 0.9 | 47.9 | -50.4 | | Q4:2021-22 | | | | | | 50.9 | 1.0 | 48.2 | -49.9 | | ‘Decrease’ in Salary / other remuneration is optimistic. |

| Table 20: Assessment and Expectations for Selling Price | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q3:2020-21 | 1,011 | 21.9 | 12.5 | 65.6 | 9.4 | 12.8 | 13.0 | 74.3 | -0.2 | | Q4:2020-21 | 967 | 31.3 | 8.6 | 60.1 | 22.7 | 19.6 | 8.9 | 71.5 | 10.7 | | Q1:2021-22 | 1,281 | 26.9 | 7.3 | 65.8 | 19.6 | 35.0 | 5.8 | 59.1 | 29.2 | | Q2:2021-22 | 1,414 | 42.0 | 3.9 | 54.1 | 38.2 | 31.1 | 2.9 | 66.0 | 28.2 | | Q3:2021-22 | 1,082 | 34.5 | 6.3 | 59.2 | 28.2 | 59.7 | 2.3 | 38.0 | 57.4 | | Q4:2021-22 | | | | | | 54.0 | 3.7 | 42.3 | 50.3 | | ‘Increase’ in selling price is optimistic. |

| Table 21: Assessment and Expectations for Profit Margin | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Increase | Decrease | No change | Net response | Increase | Decrease | No change | Net response | | Q3:2020-21 | 1,011 | 17.4 | 29.1 | 53.5 | -11.8 | 14.7 | 26.7 | 58.6 | -12.0 | | Q4:2020-21 | 967 | 24.9 | 22.9 | 52.1 | 2.0 | 17.8 | 20.1 | 62.1 | -2.4 | | Q1:2021-22 | 1,281 | 11.8 | 44.0 | 44.2 | -32.2 | 28.8 | 17.8 | 53.4 | 11.0 | | Q2:2021-22 | 1,414 | 30.0 | 20.6 | 49.5 | 9.4 | 43.7 | 11.0 | 45.3 | 32.7 | | Q3:2021-22 | 1,082 | 22.8 | 19.0 | 58.2 | 3.8 | 59.9 | 8.2 | 31.9 | 51.7 | | Q4:2021-22 | | | | | | 49.5 | 9.7 | 40.8 | 39.8 | | ‘Increase’ in profit margin is optimistic. |

| Table 22: Assessment and Expectations for Overall Business Situation | | (Percentage responses) | | Quarter | Total response | Assessment | Expectations | | Better | Worsen | No change | Net response | Better | Worsen | No change | Net response | | Q3:2020-21 | 1,011 | 46.7 | 13.8 | 39.6 | 32.9 | 45.7 | 12.8 | 41.6 | 32.9 | | Q4:2020-21 | 967 | 49.0 | 12.4 | 38.6 | 36.5 | 48.2 | 7.6 | 44.2 | 40.7 | | Q1:2021-22 | 1,281 | 18.6 | 39.2 | 42.3 | -20.6 | 57.7 | 5.1 | 37.2 | 52.5 | | Q2:2021-22 | 1,414 | 43.5 | 9.5 | 47.0 | 34.0 | 59.9 | 7.5 | 32.5 | 52.4 | | Q3:2021-22 | 1,082 | 42.3 | 9.8 | 47.9 | 32.5 | 73.1 | 2.8 | 24.1 | 70.3 | | Q4:2021-22 | | | | | | 67.6 | 4.2 | 28.2 | 63.4 | | ‘Better’ Overall Business Situation is optimistic. |

| Table 23: Business Sentiments | | Quarter | Business Assessment Index (BAI) | Business Expectations Index (BEI) | | Q3:2020-21 | 111.2 | 110.9 | | Q4:2020-21 | 115.0 | 115.4 | | Q1:2021-22 | 89.3 | 121.9 | | Q2:2021-22 | 119.4 | 128.0 | | Q3:2021-22 | 115.0 | 139.3 | | Q4:2021-22 | | 137.8 |

|

IST,

IST,