IST,

IST,

Importance of strong Governance & Secure IT Operations for Urban Co-operative Banks to Remain Relevant

Shri N.S. Vishwanathan, Deputy Governor, Reserve Bank of India

delivered-on আগ 24, 2018

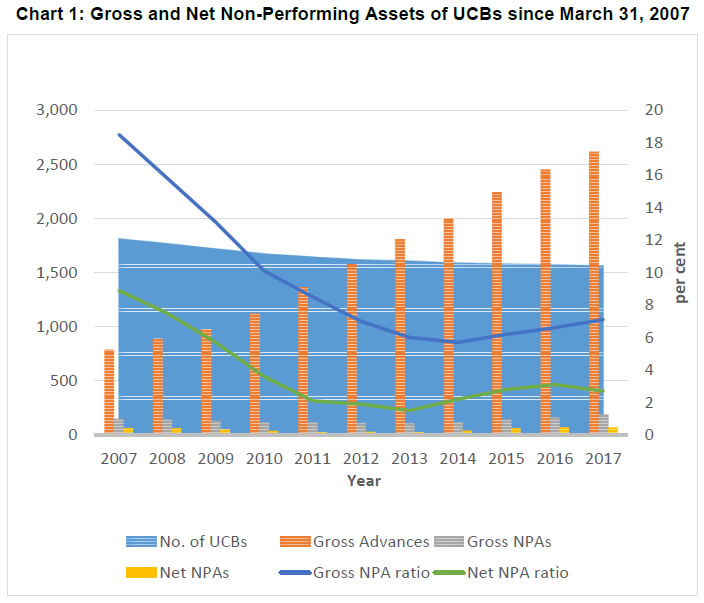

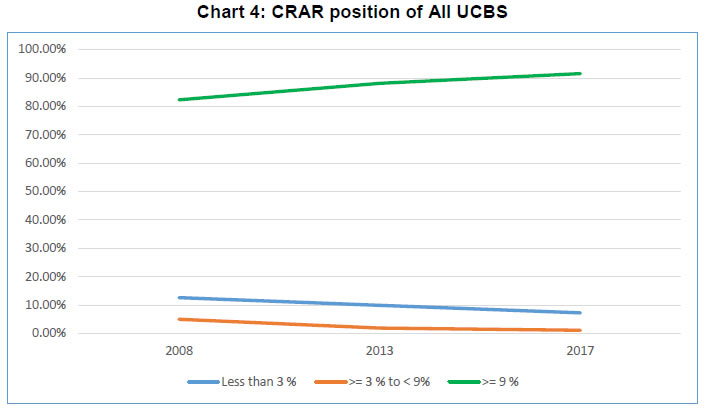

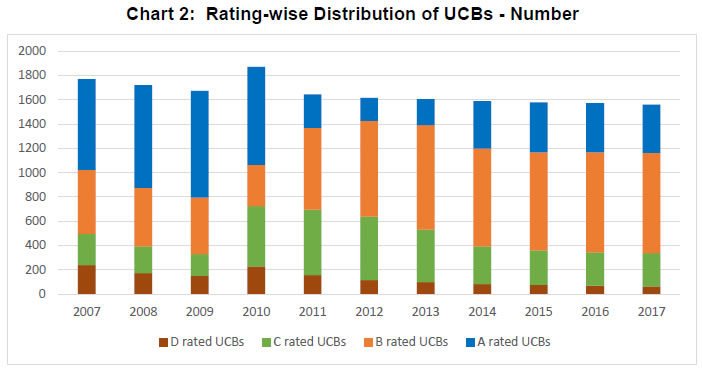

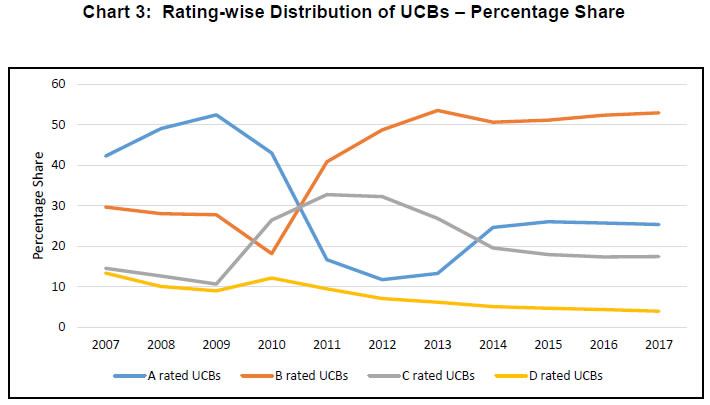

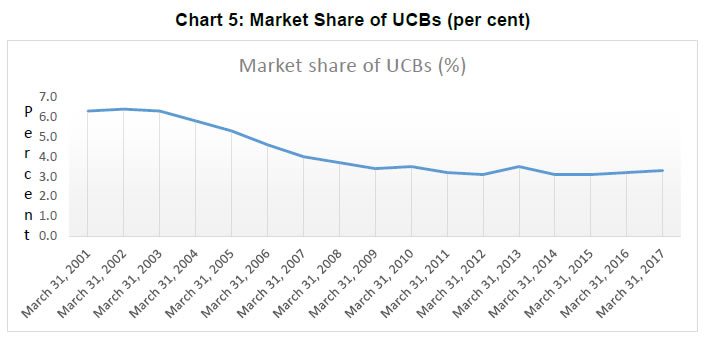

I am happy to be here in this edition of Sahakar Setu organised by the Gujarat Urban Cooperative Banks Federation. The Federation has been proactive in providing leadership to the cooperative movement in the State of Gujarat. It is because of the efforts of the Federation and its member banks, the cooperative banks in the State could emerge stronger out of the Madhavpura Bank crisis. The Federation has taken several measures particularly in adoption of technology by the Urban Cooperative Banks (UCBs). Let me share a few thoughts on where the Urban Cooperative Banking sector is today and try to give a perspective on some of the policies that Reserve Bank has been pursuing. I would also like to give you an idea of what we are looking at for the sector in future. Here are some numbers to begin with. As on March 31, 2017, there were 1562 UCBs with deposits aggregating ₹ 443,468 crore and advances totalling ₹ 261,225 crore. The sector accounted for about 3.6 per cent of deposits and 2.9 per cent of the advances of the banking sector. On an aggregate, deposits clocked a growth of 13.1 per cent and advances grew by 6.6 per cent year-on-year during 2016-17. The gross NPAs stood at little more than 7 per cent. The return on assets (ROA) was 0.77 per cent and about 91 per cent of the banks were reasonably well capitalised with Capital to Risk weighted Assets Ratio(CRAR) above 9 per cent. As many of you may be aware, the market share of UCBs had declined from about 6.3 per cent to about 5.8 per cent immediately after the Madhavpura Bank crisis. Several measures were taken by the Reserve Bank to restore public confidence in the sector. These included the signing of Memorandum of Understanding (MoUs) with the state governments and formation of Task Force on Co-operative Urban Banks(TAFCUB) in most states. The charts below indicate the performance of the sector on important parameters over the last 10 years. Asset Quality of UCBs: The asset quality of the sector has improved consistently over the years:  Rating–wise Distribution of UCBs: UCBs are subject to supervision under the CAMELS (Capital, Assets, Management, Earnings, Liquidity and Systems) model and based on the assessment, given a supervisory rating from A to D, A being the highest rating and D being the lowest. It may be seen that there has been a notable decline in the number of UCBs that were assigned the supervisory rating of ‘C’ or ‘D’ since 2007. (chart 2) The chart 3 below shows the decline in percentage share of UCBs having lower rating. CRAR-wise Distribution of UCBs: Overall, the number of UCBs having CRAR of less than 3 per cent has come down from 224 as on March 31, 2008 to 160 as on March 31, 2013 to 114 as on March 31, 2017. The percentage of UCBs complying with the regulatory prescription of CRAR of 9 per cent has increased over the years from 82.3 per cent as on March 31, 2008 to 88.1 per cent as on March 31, 2013 to 91.5 per cent as on March 31, 2017.  Board of Management and Voluntary Conversion to Small Finance Banks (SFBs) There has, no doubt, been a steady improvement on various parameters indicating that Reserve Bank and the sector were able to jointly work to address the issues arising from the Madhavpura Bank crisis. But do these numbers allow us to draw comfort? Let us take a look at the data on Non-Performing Assets (NPAs). With UCBs primarily dealing in small ticket advances, NPAs of 7 per cent at the aggregate level is not very comforting. UCBs are still under Basel I framework and, therefore, mere compliance with CRAR may not be enough. The real barometer of public confidence is the market share of the sector. As mentioned earlier, the market share of UCBs which was as high at 6.4 per cent in 2002 has declined to 3.3 per cent in 2017. The fall in market share as indicated in Chart 5 necessitates an analysis as to why there is a dip in the market share of UCBs and determine what needs to be done to address this. I used to mention often in the past, and it requires a reiteration now, that banking business relies on the trust of the public because the main resource for a bank is deposits and deposits will grow only when the members of public have confidence in the bank. While one may be tempted to attribute the decline in market share of UCBs to emergence of other competing alternatives within and outside the banking sector, there is no gainsaying the fact that UCBs need to regain and retain the confidence of their depositors. Usually such confidence comes, among other things, from the evidence that:

The first two factors are directly related to governance in the UCBs. When we talk of governance, the need to infuse professionalism in the boards of the UCBs comes to the fore. Many a time, either due to ignorance or otherwise, decisions are taken that might be detrimental to the interests of the depositors. I do agree that over the years efforts have been made by the sector to induct professionals into their boards but there is always the inherent conflict arising from the electorate of the board being members, who are also borrowers of the bank. The much discussed dual control results in lesser ability of the Reserve Bank to address problems that arise. I must hasten to add here that after the signing of the MoU, there has been improvement on this score, but the process is still a convoluted one. Moreover, there needs to be a proper segregation of the roles between the governance structure having responsibility for adherence to cooperative principles by the UCB and the one entrusted to run the entity as a bank funded by public deposits. It is for this reason that the Reserve Bank recently came out with the draft guidelines on Board of Management. I heard that there is some misconception about this. Let me clarify that the purpose of the Board of Management is to improve governance in the UCBs, which will enhance public confidence in the sector. The Board of Management provides an institutional framework for professionalising the governance structure which will manage the banking operations of the UCB. As you are all aware, this is a suggestion made long ago and we have been looking at various ways to implement it. I am happy to mention that this proposal has emerged out of stakeholder consultations so that the need to bring legislative changes is obviated. I am sure you all appreciate that the proposed measure will enhance public confidence in the UCBs and help them regain their market share. As a part of this effort at confidence building, the Reserve Bank also announced the intent to allow UCBs to voluntarily convert into Small Finance Banks (SFB). In terms of the larger financial inclusion objective, the SFBs perform a role similar to UCBs. In fact, they have a mandate to achieve 75 per cent Priority Sector Lending (PSL) target and also to ensure that at least 50 per cent of their advances are of ticket size less than ₹ 25 lakhs. The asset profile of several UCBs does not meet this norm. More worrying is the fact that some UCBs do not even meet the 40 per cent PSL target fixed for them. Thus, the option for a UCB to convert into a SFB will not undermine the financial inclusion agenda, but more importantly, it can add to the confidence of the depositors of UCBs. This is because, the depositors will have the comfort that the bank can migrate to a different framework, which not only provides it the ability to raise capital from the market to grow with adequate balance sheet resilience, but also a better resolution regime. In any case, this is purely voluntary, and it is only fair that the shareholders of a bank have such an option. Issues and Challenges Let me now turn to some of the other issues and challenges Capital The UCBs are still under Basel I norms. As many of you might be aware, the CRAR computed under these norms may not adequately reflect resilience and ability to absorb shocks. Reserve Bank appreciates the constraints of the UCBs in raising capital and, therefore, has allowed the UCBs to continue under Basel I norms although this also restrains the UCBs from entering into new businesses and expanding their presence vis-à-vis the commercial banks. Many banks in the sector are small to have a systemic impact, if stressed. However, failure of a bank, irrespective of its size, dents the public confidence in the sector. Moreover, a few UCBs have a larger balance sheet than some commercial banks. This makes it imperative for all stakeholders to ensure that the banks are well capitalised and have the resilience to deal with stress situations. I may mention here that as per stress tests conducted by Reserve Bank for the banking sector to check the resilience of the system, under a scenario of increase in Gross Non Performing Assets (GNPAs) by two Standard Deviations (SD), while the system-level CRAR of Scheduled UCBs (SUCBs) remained above the minimum regulatory requirement, at the individual level, several SUCBs (26 out of 54) may not be able to maintain the minimum CRAR. Given that these findings are based on Basel I computation, the outcome of stress tests would have been more severe under Basel II and III norms. There is thus, need for the UCBs to strengthen their capital base further. The sector has to identify sources of high quality capital, not just Tier 2 capital. Competition At one time, UCBs had a niche market. But that is less so today. Many traditional banks are now bracing up to attract customers who were in the past the exclusive domain of cooperative banks. Currently, lending to the borrowers in the lower economic strata has become profitable with use of technology. But UCBs need to be aware of competition from the new players even more. While on the liabilities side, the SFBs and Payments Banks provide the smaller depositors an additional option, on the asset side, the SFBs and NBFCs are in the market for customers similar to those of UCBs. However, given that India has such a vast potential, there is space for all good players. For UCBs to be relevant in their current market, they must adopt Information Technology (IT) and should raise themselves to a position to manage all risks arising from technology enabled banking services. In this context, it becomes all the more necessary for UCBs to strengthen their governance and financials. Information technology Modern banking cannot be carried out without IT, be it for banks’ own housekeeping and MIS or for customer interface. IT reduces the cost of operations and brings tremendous efficiencies but at the same time, it also considerably increases the operational risk and consequently underlines the need for managing them. Digital banking comes with risks associated with cyber security concerns. Banks therefore, need to have robust IT systems and subject them to regular IS audits. Moreover, implementation of IT system in banks makes it obligatory on part of the banks to have a robust IT risk management architecture. The banks also need to have skilled staff on their rolls rather than depend completely on outsourcing the risk management. The customer grievances related to unauthorized electronic banking transactions should be a high priority issue for the UCBs offering financial services through digital channels. The UCBs which do not have the requisite controls, could be a soft target for such unauthorized transactions. I am aware that some of the larger UCBs have put in place robust IT system architecture; but I am worried about the smaller UCBs - 124 banks with deposit size of less than ₹ 10 Crore and another 232 banks with deposit size of between ₹ 10 crore and ₹ 25 Crore. The argument that adoption and implementation of IT increases the cost of operations is not acceptable because IT enabled operations are a necessity to be relevant in the market place and at the same time, one needs to do what it takes to ensure safety of depositors. Use of IT enabled processes also help contain frauds. In this context, it is a matter of concern that there are still 171 UCBs which have yet to fully implement CBS and have also not availed the assistance being provided by Reserve Bank in this regard. Some Recent Measures: As many of you might be aware, we have recently made it easier for non-scheduled UCBs to open accounts with Reserve Bank, harmonised the PSL guidelines, brought the Scheduled UCBs under the Marginal Standing Facility (MSF) arrangement, expanded the list of counterparties with whom UCBs can undertake trading in Non-SLR securities and allowed the spread of MTM losses in the investments portfolio over four quarters, as has been done for commercial banks. We are thus providing an enabling regulatory framework for UCBs to function and play their role effectively. At the same time as banks, UCBs have to ensure that they strictly comply with the AML/CFT directions because any weak link in this chain will be misused by persons who might want to undertake transactions that are not in conformity with the requirements. Let me now share a few thoughts on the way forward. Consolidation in the UCB sector The Reserve Bank followed a liberal licensing policy during the period 1992-2004. During this period there was a sharp increase in the number of UCBs. Lack of professional governance and weak internal controls led to poor financial health in several UCBs. Based on the Vision Document 2005, the Reserve Bank introduced a scheme for merger within the UCB sector and rolled out separate guidelines for merger of UCBs into commercial banks in the year 2010. As per these guidelines, mergers are voluntary in keeping with the co-operative spirit and ethos. This paved the way for consolidation in the sector by way of mergers and exits. Since the year 2005, till March 2018, there have been 127 mergers. As banking becomes more complex and competition intense, the need for skilled workforce will increase, regular investments in IT infrastructure would be required and the cost of compliance would go up. To achieve scale and remain relevant in the medium term, the sector needs some consolidation. So far, most mergers have happened only out of compulsion, i.e., when a bank became weak. I feel that there is a need for UCB managements to assess their ability to sustain their viability in the future and consider some consolidation even when they are currently strong. The sector needs to deliberate over the issues and come out with appropriate solutions. Umbrella Organization It would be evident that many of the major issues confronting the sector emanate from lack of resources, low scales of operations and increasing compliance requirements which get accentuated in a competitive environment. Apart from consolidation, forming an umbrella organization for the UCBs will help address some of the concerns. This idea was mooted in the year 2006 by the working group set up by Reserve Bank on augmentation of capital of UCBs. It was endorsed subsequently by several committees. The basic idea behind the umbrella organization is to create an institution to provide liquidity support to UCBs in times of need and sharing of resources, particularly the IT resources and managerial support. Such a system is prevalent in several countries where cooperative banking has done well. However, there was no consensus among stakeholders on the structure and functions of the umbrella organisation. In the year 2016, NAFCUB (National Federation of Urban Co-operative Banks & Credit Societies) set up a committee to examine the issues and give its recommendations. Reserve Bank has formally received the Report of the Committee. I am glad to mention that we are actively examining the recommendations of the Committee. Conclusion Let me now conclude. UCBs play an important role in furthering the financial inclusion agenda. At the same time, it must be recognised that banking is becoming complex on the one hand while on the other, there is competition in the market segment that was once considered the exclusive preserve of UCBs. The competition is posed by traditional and new players because IT and Fintech have enabled them to access this market. For UCBs to remain relevant, the sector needs to adopt technology, brace up for the risks that IT enabled operations bring, have the right governance structure, employ skilled HR and attain the right scale of operations. The Reserve Bank will continue to pursue policies that enhance depositor confidence in the UCBs and at the same time ensure that the UCBs do not become a weak link in our efforts to provide a clean banking system. I hope the deliberations in this edition of Sahakar Setu would come up with ideas to help the sector and the Reserve Bank move in that direction. I wish the event all success. Thank you all. 1 Inaugural Address delivered by Shri N S Vishwanathan, Deputy Governor at Sahakar Setu – An event organised by Gujarat Urban Co-operative Banks Federation on August 4, 2018 at Gandhinagar. |

এই পৃষ্ঠাটো শ্বেয়াৰ কৰক:

ভাৰতীয় ৰিজাৰ্ভ বেংক মোবাইল এপ্পলিকেষ্যন ইনষ্টল কৰক আৰু নৱীনতম বাতৰিৰ প্ৰৱেশাধিকাৰ পাওক!

আমাৰ এপটো ইনষ্টল কৰিবলৈ QR ক’ড স্কেন কৰক

পৃষ্ঠাটো শেহতীয়া আপডেট কৰা তাৰিখ: